Comprehensive Accounting Report: Journal Entries to Ratio Analysis

VerifiedAdded on 2023/06/15

|14

|1780

|143

Report

AI Summary

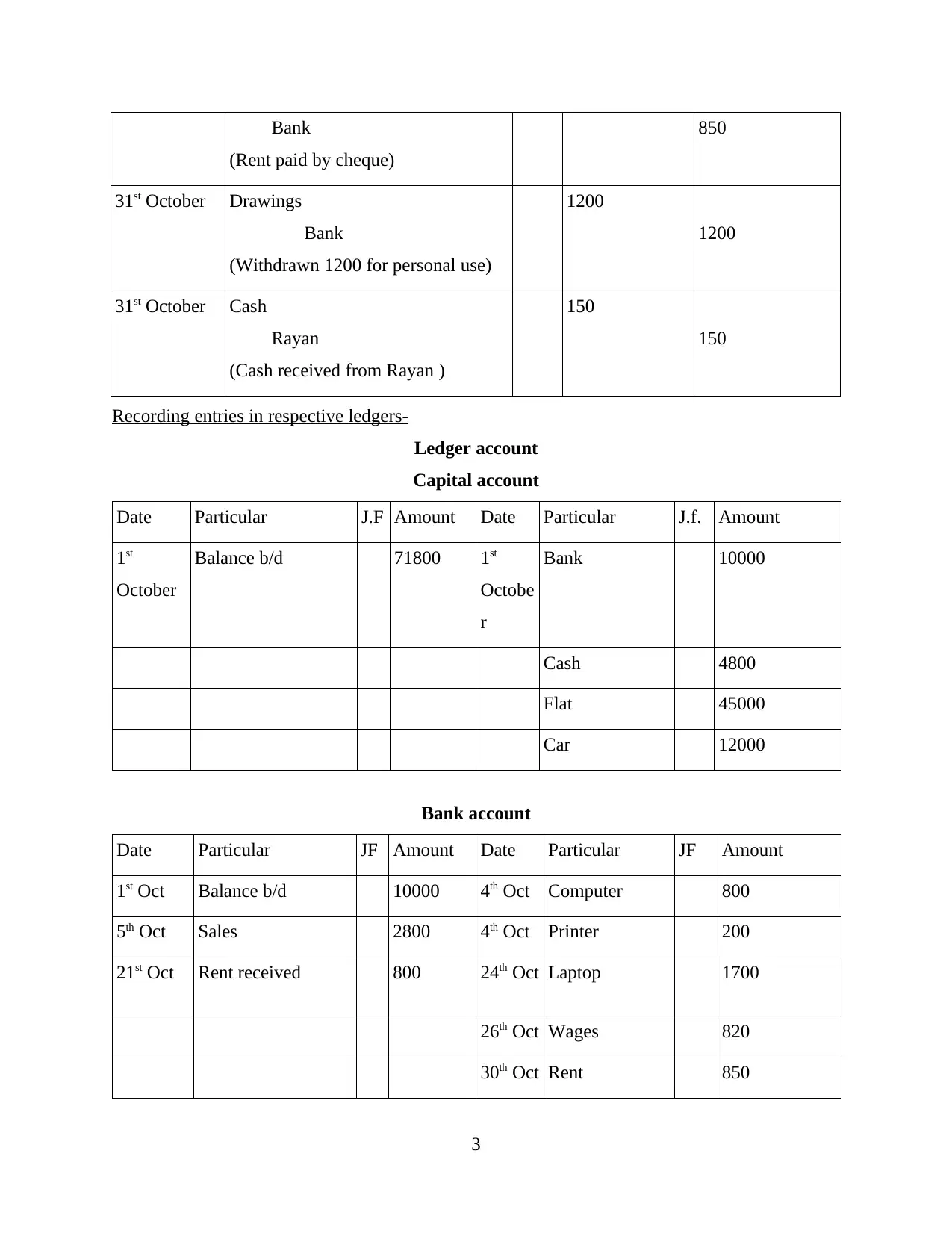

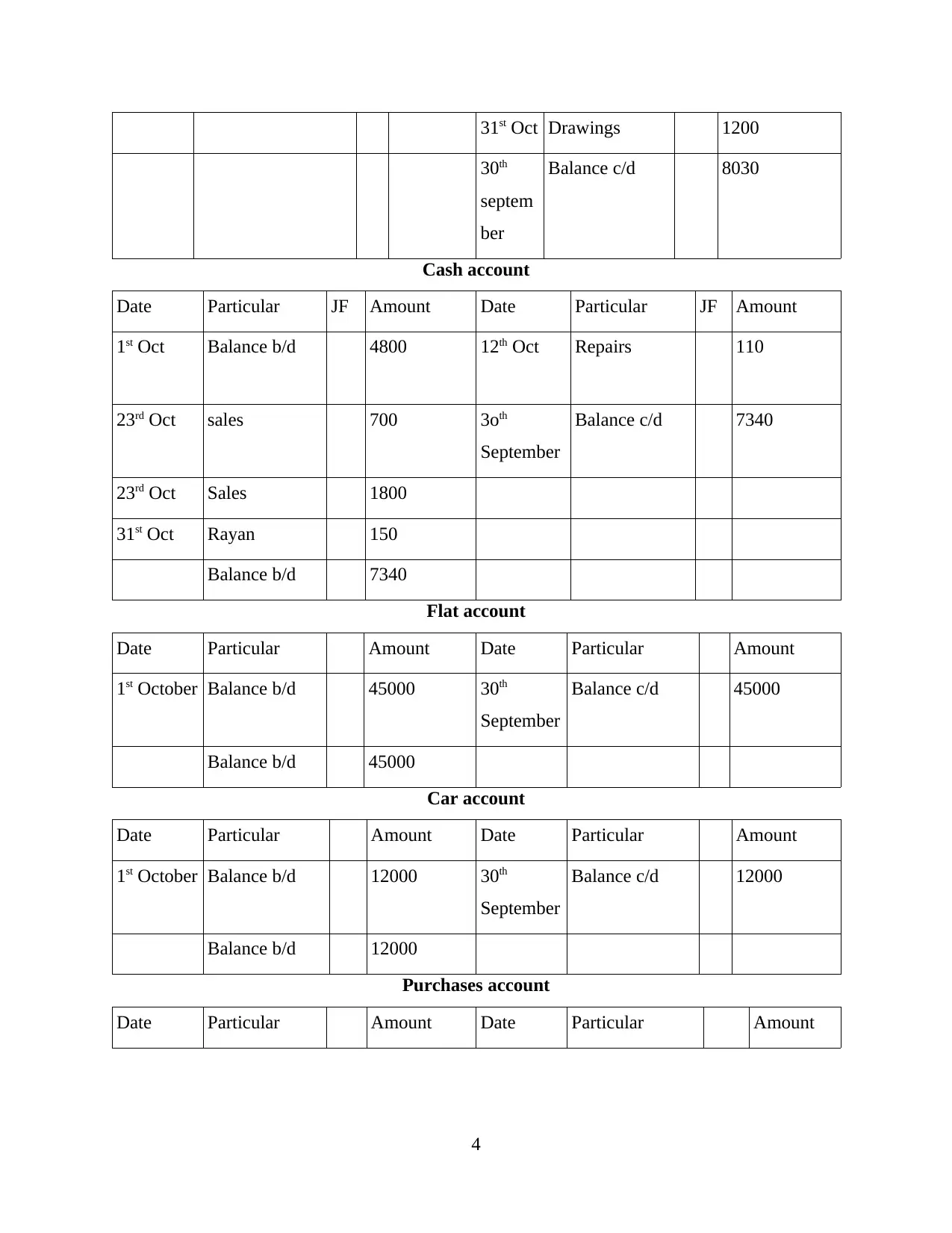

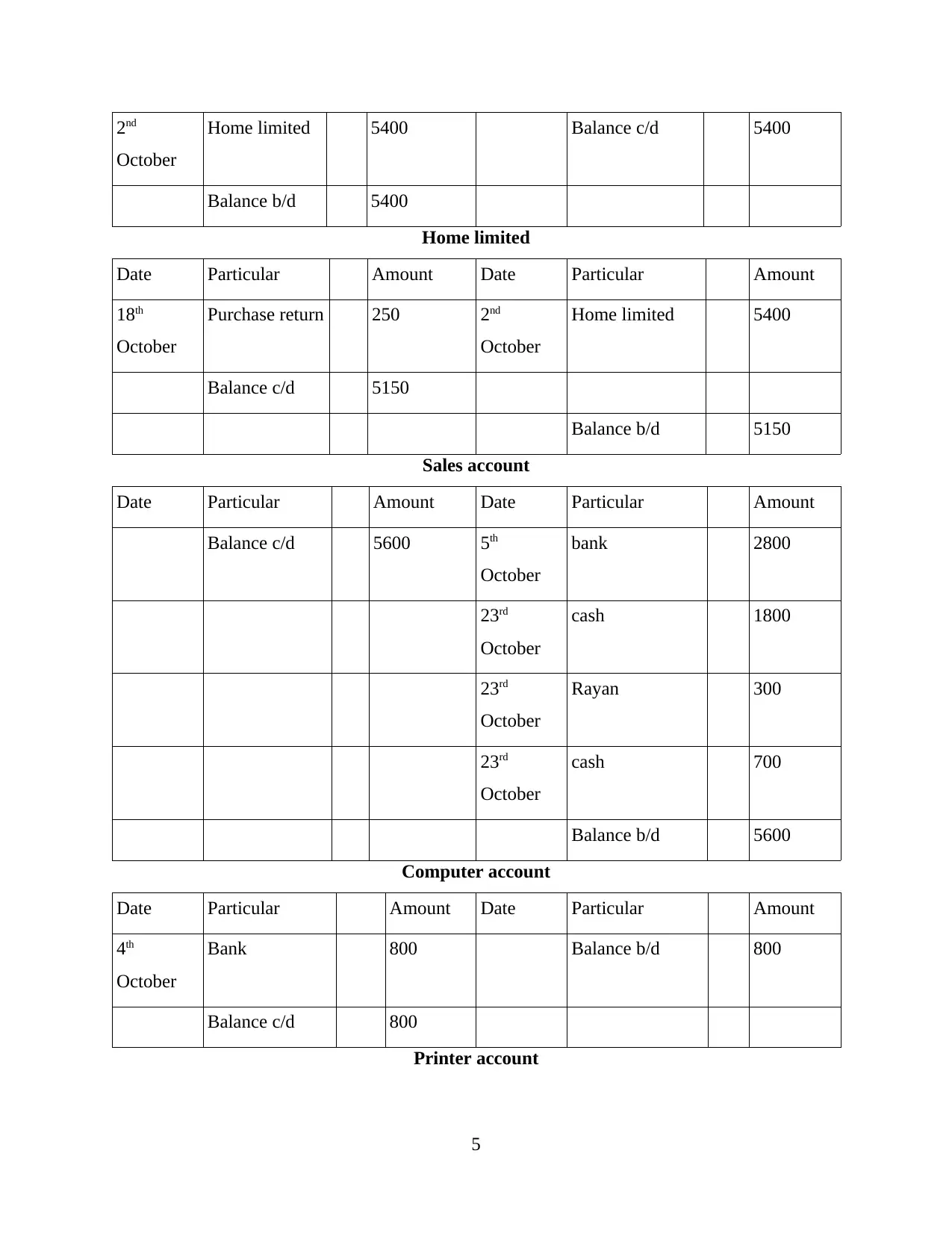

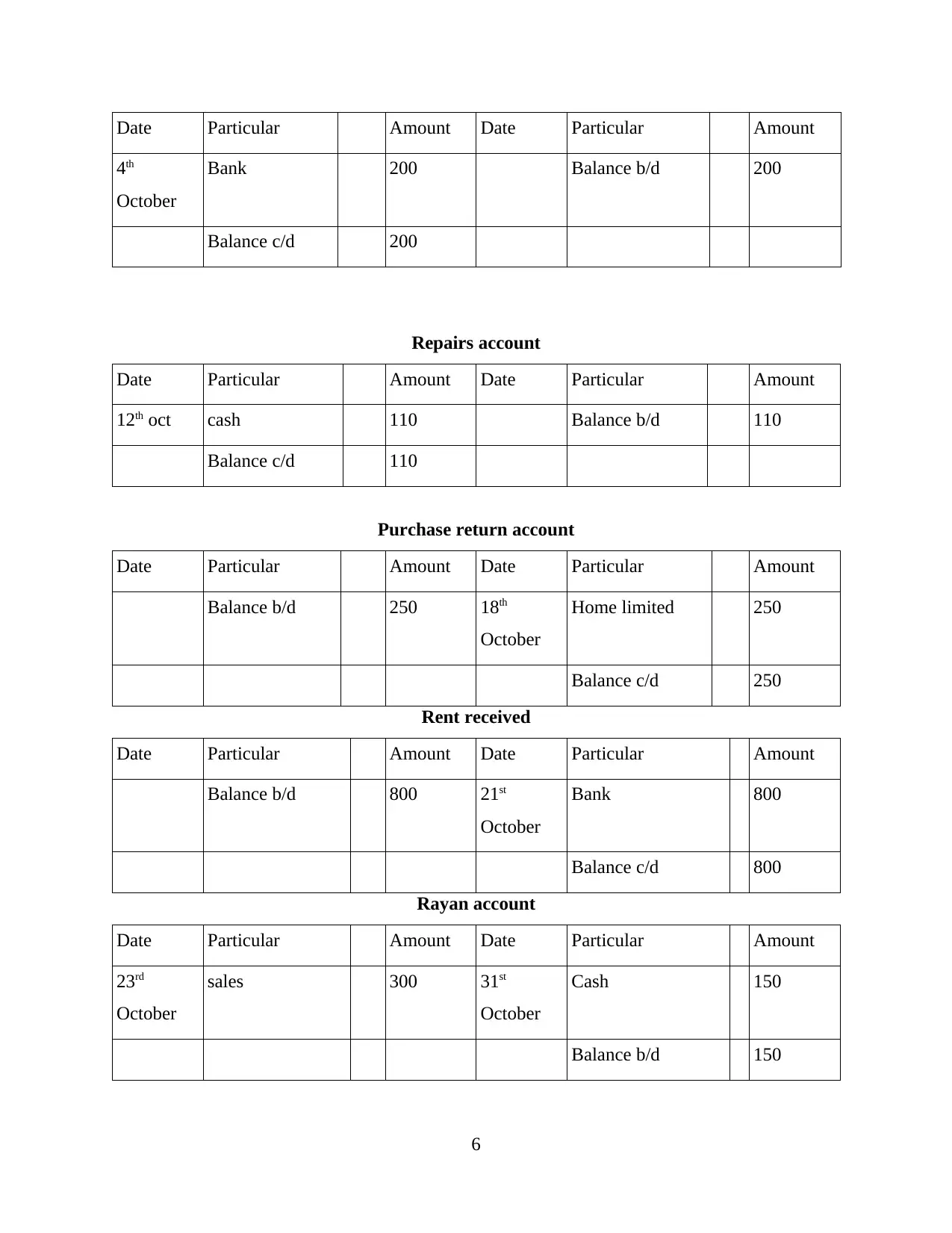

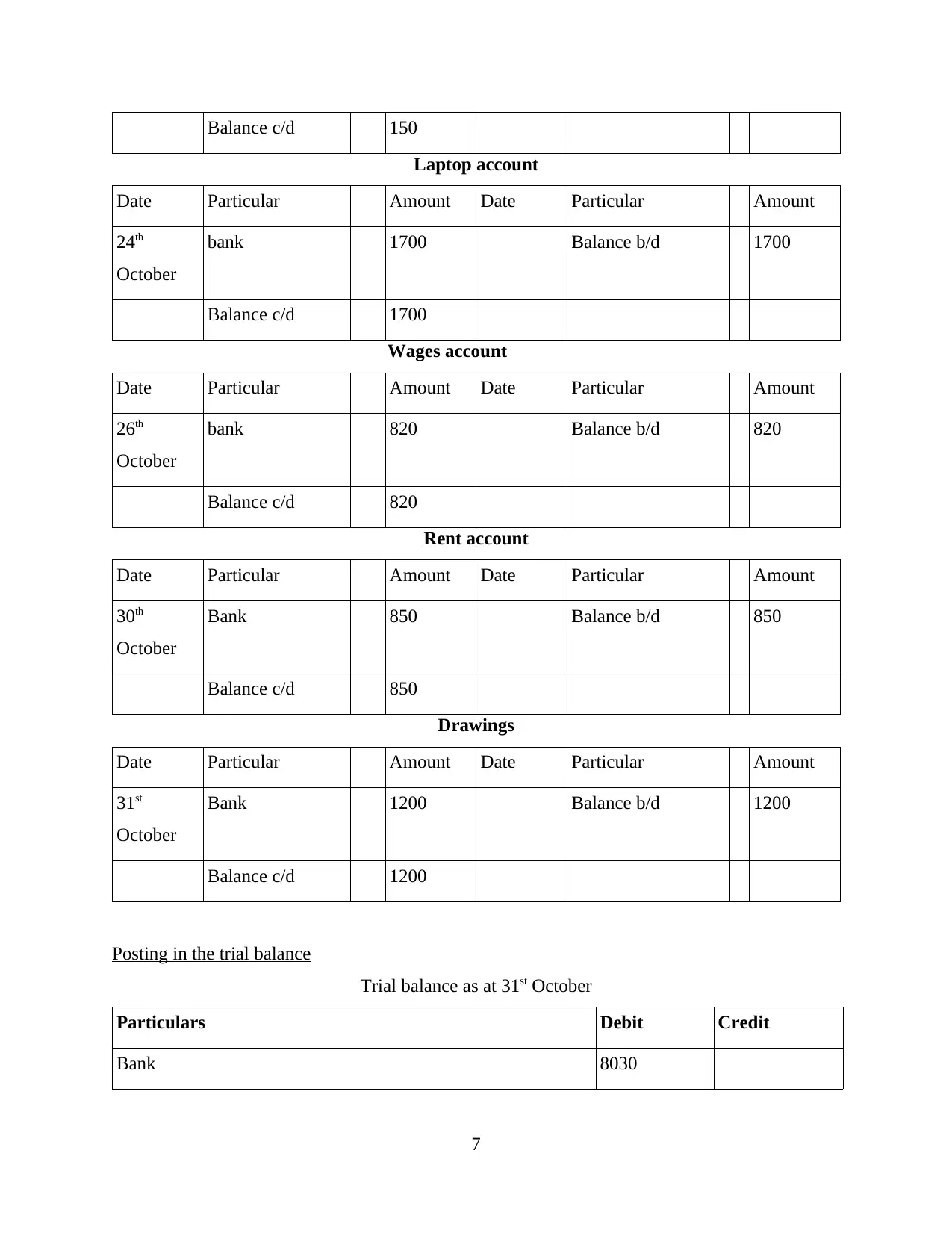

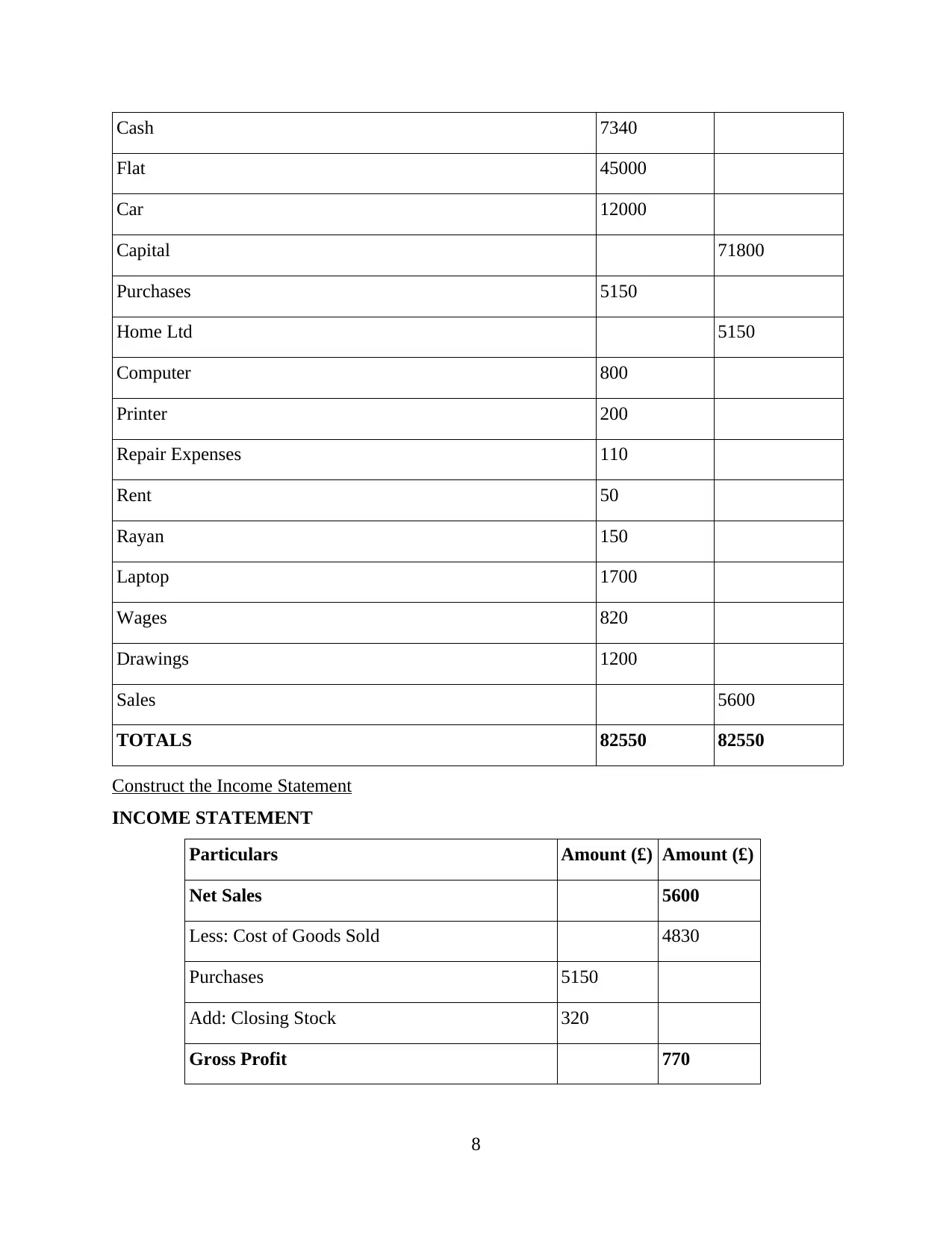

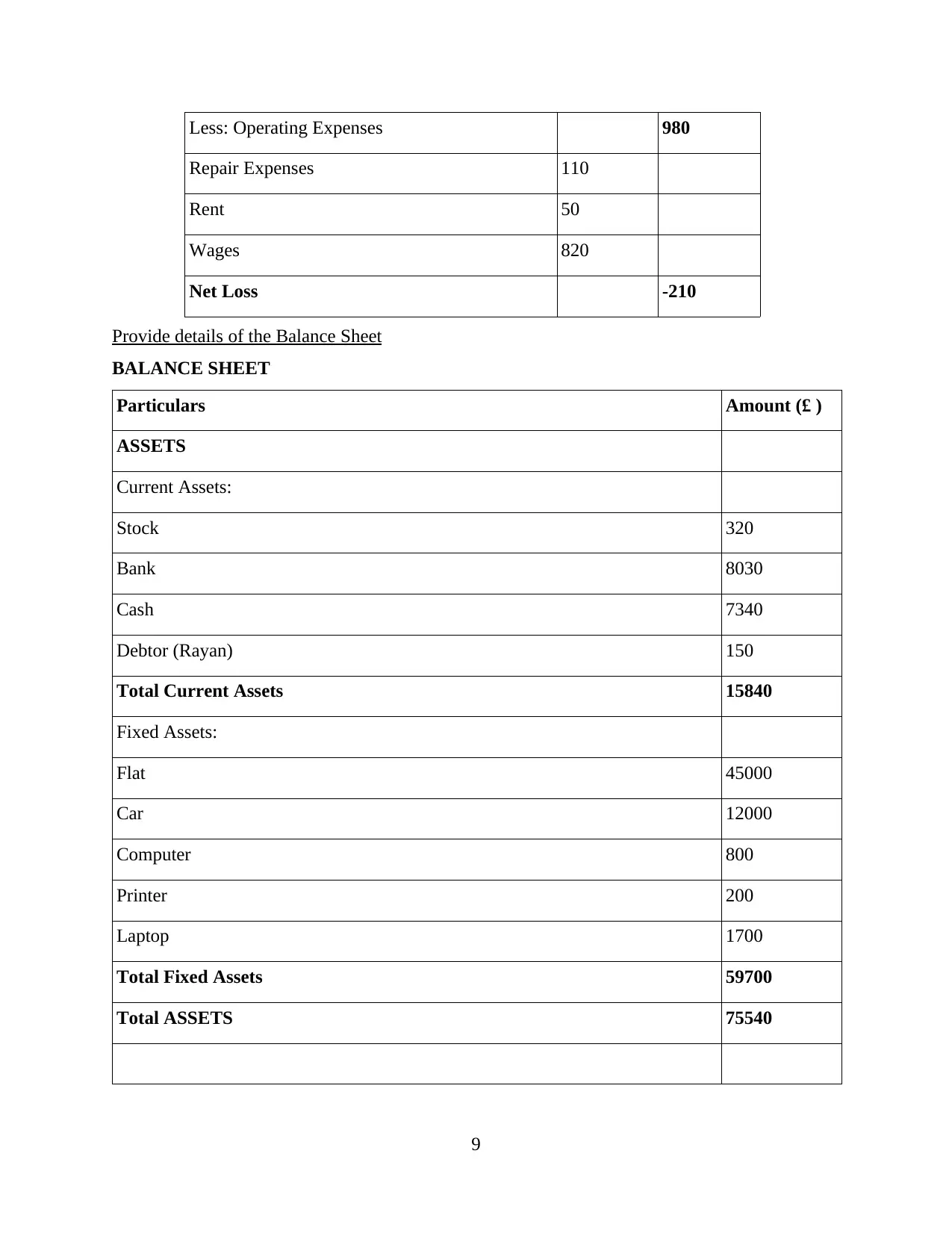

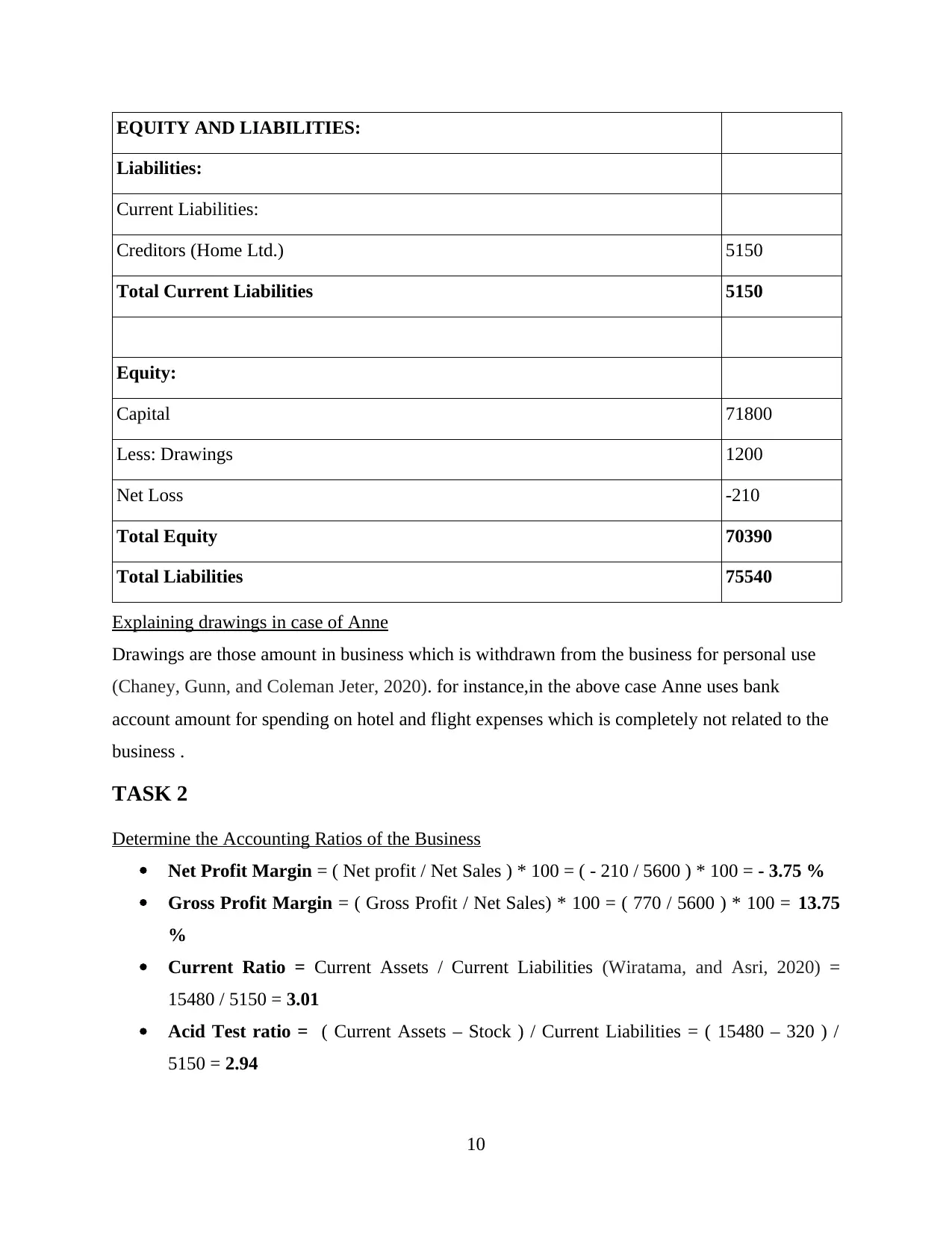

This accounting report provides a detailed analysis of business transactions, starting with journal entries and their posting to respective ledger accounts. A trial balance is prepared to ensure accuracy, followed by the construction of an income statement to determine the business's profitability and a balance sheet to present its assets and liabilities. The report also includes an interpretation of key accounting ratios to assess the company's financial health and compare it with competitors. Furthermore, it discusses the impact of events like COVID-19 on the business's profitability, emphasizing the need for adaptation and resilience in dynamic market conditions. The report concludes that maintaining accurate financial records is crucial for informed decision-making and provides valuable insights for both internal and external stakeholders.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.