Financial Accounting and Reporting: Superstore Ltd Case, June 2018

VerifiedAdded on 2023/06/07

|13

|2305

|87

Report

AI Summary

This report provides a detailed financial accounting analysis for Superstore Ltd for the year ended June 30, 2018. It addresses several key issues, including the revision of an asset's useful life according to IAS 16, the treatment of prior period items as per IAS 8, and the impact of investment revisions under IAS 39 and IAS 10. The report also covers the accounting of fraudulent cases, the accounting for share issues, and the calculation of current and deferred tax liabilities. Furthermore, it examines the revaluation of property, plant, and equipment, providing journal entries for revaluation and depreciation. Finally, the report addresses the impairment of assets in accordance with IAS 36, calculating impairment losses for different business segments. The analysis includes relevant journal entries and calculations to support the accounting treatments.

Financial Accounting

1 | P a g e

1 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

SOLUTION 1:- DISCLOSURE IN THE FINANCIAL STATEMENTS................................................................3

SOLUTION 2:- ACCOUNTING IN CASE OF ISSUES OF SHARES.................................................................5

SOLUTION 3:- ACCOUNTING OF TAXES..................................................................................................7

SOLUTION 4:- REVALUATION OF PROPERTY, PLANT AND EQUIPMENT.................................................8

SOLUTION 5:- IMPAIRMENT OF ASSETS...............................................................................................11

REFERENCES:.......................................................................................................................................13

2 | P a g e

SOLUTION 1:- DISCLOSURE IN THE FINANCIAL STATEMENTS................................................................3

SOLUTION 2:- ACCOUNTING IN CASE OF ISSUES OF SHARES.................................................................5

SOLUTION 3:- ACCOUNTING OF TAXES..................................................................................................7

SOLUTION 4:- REVALUATION OF PROPERTY, PLANT AND EQUIPMENT.................................................8

SOLUTION 5:- IMPAIRMENT OF ASSETS...............................................................................................11

REFERENCES:.......................................................................................................................................13

2 | P a g e

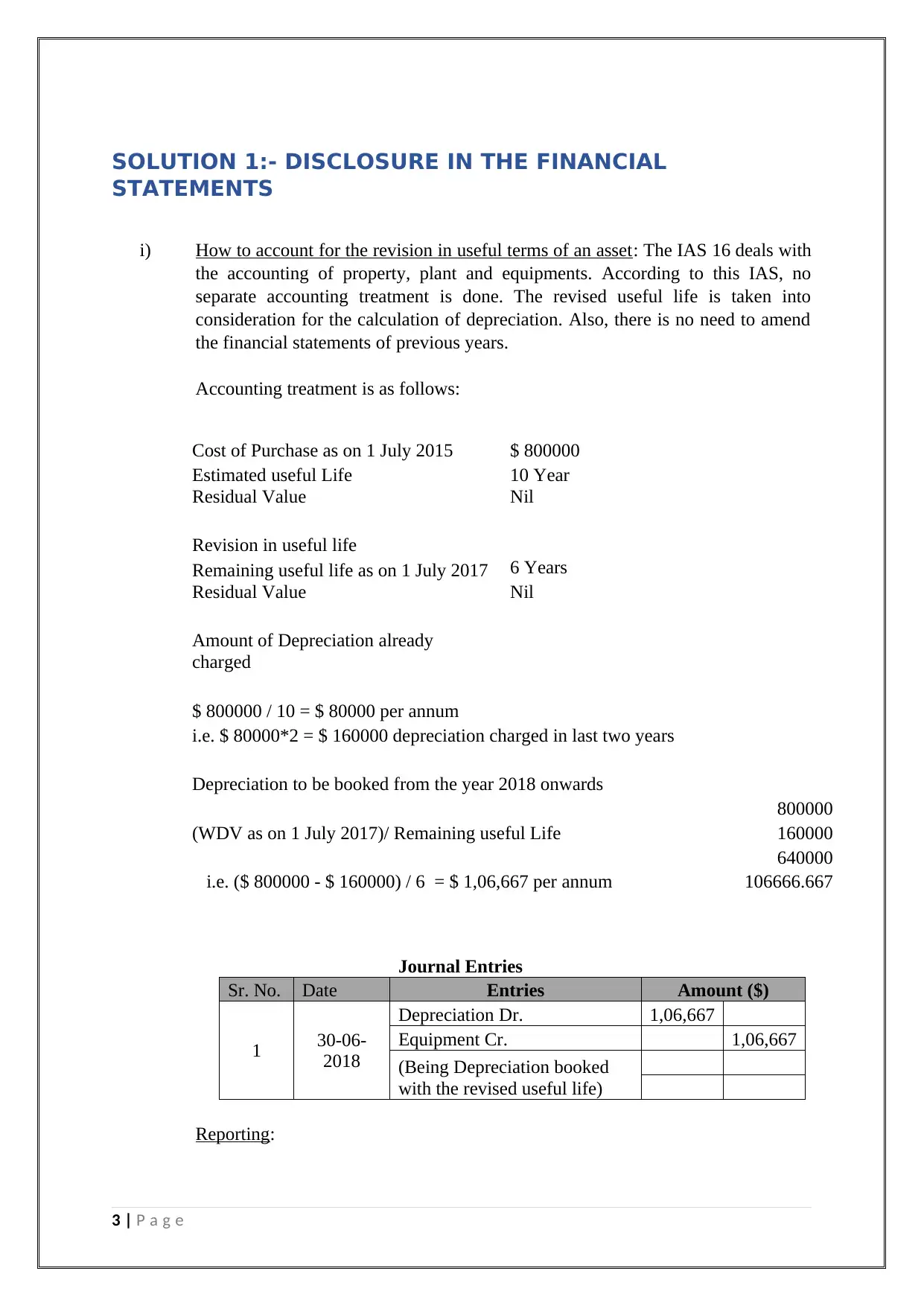

SOLUTION 1:- DISCLOSURE IN THE FINANCIAL

STATEMENTS

i) How to account for the revision in useful terms of an asset: The IAS 16 deals with

the accounting of property, plant and equipments. According to this IAS, no

separate accounting treatment is done. The revised useful life is taken into

consideration for the calculation of depreciation. Also, there is no need to amend

the financial statements of previous years.

Accounting treatment is as follows:

Cost of Purchase as on 1 July 2015 $ 800000

Estimated useful Life 10 Year

Residual Value Nil

Revision in useful life

Remaining useful life as on 1 July 2017 6 Years

Residual Value Nil

Amount of Depreciation already

charged

$ 800000 / 10 = $ 80000 per annum

i.e. $ 80000*2 = $ 160000 depreciation charged in last two years

Depreciation to be booked from the year 2018 onwards

800000

(WDV as on 1 July 2017)/ Remaining useful Life 160000

640000

i.e. ($ 800000 - $ 160000) / 6 = $ 1,06,667 per annum 106666.667

Journal Entries

Sr. No. Date Entries Amount ($)

1 30-06-

2018

Depreciation Dr. 1,06,667

Equipment Cr. 1,06,667

(Being Depreciation booked

with the revised useful life)

Reporting:

3 | P a g e

STATEMENTS

i) How to account for the revision in useful terms of an asset: The IAS 16 deals with

the accounting of property, plant and equipments. According to this IAS, no

separate accounting treatment is done. The revised useful life is taken into

consideration for the calculation of depreciation. Also, there is no need to amend

the financial statements of previous years.

Accounting treatment is as follows:

Cost of Purchase as on 1 July 2015 $ 800000

Estimated useful Life 10 Year

Residual Value Nil

Revision in useful life

Remaining useful life as on 1 July 2017 6 Years

Residual Value Nil

Amount of Depreciation already

charged

$ 800000 / 10 = $ 80000 per annum

i.e. $ 80000*2 = $ 160000 depreciation charged in last two years

Depreciation to be booked from the year 2018 onwards

800000

(WDV as on 1 July 2017)/ Remaining useful Life 160000

640000

i.e. ($ 800000 - $ 160000) / 6 = $ 1,06,667 per annum 106666.667

Journal Entries

Sr. No. Date Entries Amount ($)

1 30-06-

2018

Depreciation Dr. 1,06,667

Equipment Cr. 1,06,667

(Being Depreciation booked

with the revised useful life)

Reporting:

3 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

As per IAS 18, where estimated life of the asset is revised it results in the

accounting estimates has been changed. Thus, any accounting estimates which has

been revised or changed and impact of such revision should be disclosed

separately in the financial statements of an organization.

ii) Treatment of the Prior Period Items: In the present case, in the year 2018, it is

noticed that an invoice of repair was not booked in earlier year and due to this, tax

deducted could not be claimed. These types of mistakes are called as prior period

items.

As per IAS 8, prior period items should be recorded in the books of accounts of

the year in which they would have actually been occurred. In other words,

previous year figures are reinstated with the corresponding changes of these items

(Deloitte, n.d.).

Journal Entries of the transaction will be made as under:

Journal Entries

Sr. No. Date Entries Amount ($)

1 30-06-

2017

Repair Expense Dr. 20,000

Accounts Payable Cr. 20,000

(Being repair expense booked

as prior period item)

2 30-066-

2017

Tax Receivable Dr. 6,000

Provision for Tax Cr. 6,000

(Being tax liability reduced on

repair amount)

2 12-07-

2018

Accounts Payable Dr. 20,000

Bank Cr. 20,000

(Being repair expense paid)

Reporting:

IAS 8 also provides the disclosure of the prior period items in the financial

statements separately. Company should disclose the effects of repair expenses in

the year 2017 and also disclose the impact thereof in the financial statements.

iii) Impact of revision in investment: In instant case, value in market for investments

made in ABC Ltd. is $ 600000 as on 30 June 2018. But, as on July 2018 major fall

in the share market notices and the market value of the investment go down to $

250000.

4 | P a g e

accounting estimates has been changed. Thus, any accounting estimates which has

been revised or changed and impact of such revision should be disclosed

separately in the financial statements of an organization.

ii) Treatment of the Prior Period Items: In the present case, in the year 2018, it is

noticed that an invoice of repair was not booked in earlier year and due to this, tax

deducted could not be claimed. These types of mistakes are called as prior period

items.

As per IAS 8, prior period items should be recorded in the books of accounts of

the year in which they would have actually been occurred. In other words,

previous year figures are reinstated with the corresponding changes of these items

(Deloitte, n.d.).

Journal Entries of the transaction will be made as under:

Journal Entries

Sr. No. Date Entries Amount ($)

1 30-06-

2017

Repair Expense Dr. 20,000

Accounts Payable Cr. 20,000

(Being repair expense booked

as prior period item)

2 30-066-

2017

Tax Receivable Dr. 6,000

Provision for Tax Cr. 6,000

(Being tax liability reduced on

repair amount)

2 12-07-

2018

Accounts Payable Dr. 20,000

Bank Cr. 20,000

(Being repair expense paid)

Reporting:

IAS 8 also provides the disclosure of the prior period items in the financial

statements separately. Company should disclose the effects of repair expenses in

the year 2017 and also disclose the impact thereof in the financial statements.

iii) Impact of revision in investment: In instant case, value in market for investments

made in ABC Ltd. is $ 600000 as on 30 June 2018. But, as on July 2018 major fall

in the share market notices and the market value of the investment go down to $

250000.

4 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

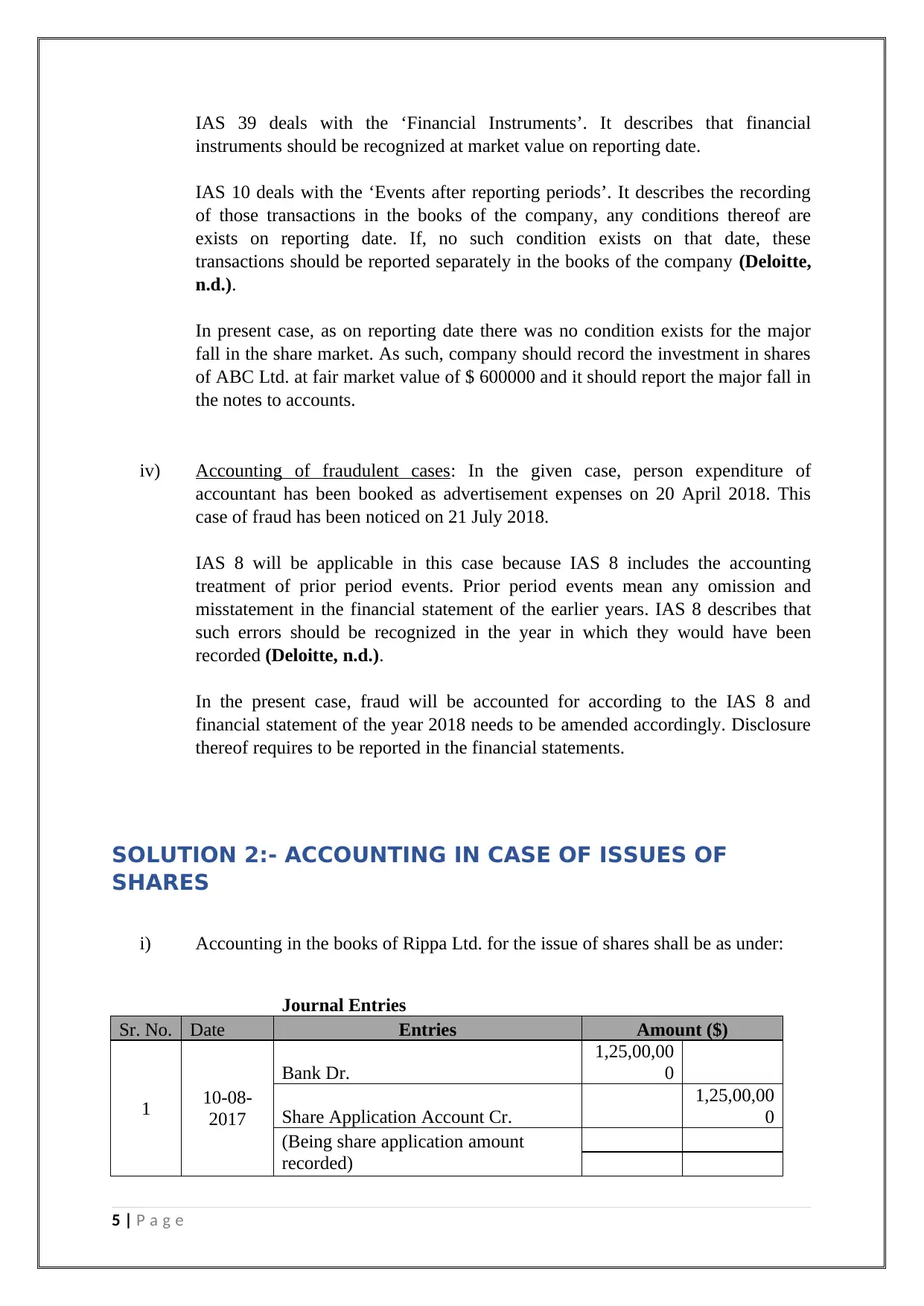

IAS 39 deals with the ‘Financial Instruments’. It describes that financial

instruments should be recognized at market value on reporting date.

IAS 10 deals with the ‘Events after reporting periods’. It describes the recording

of those transactions in the books of the company, any conditions thereof are

exists on reporting date. If, no such condition exists on that date, these

transactions should be reported separately in the books of the company (Deloitte,

n.d.).

In present case, as on reporting date there was no condition exists for the major

fall in the share market. As such, company should record the investment in shares

of ABC Ltd. at fair market value of $ 600000 and it should report the major fall in

the notes to accounts.

iv) Accounting of fraudulent cases: In the given case, person expenditure of

accountant has been booked as advertisement expenses on 20 April 2018. This

case of fraud has been noticed on 21 July 2018.

IAS 8 will be applicable in this case because IAS 8 includes the accounting

treatment of prior period events. Prior period events mean any omission and

misstatement in the financial statement of the earlier years. IAS 8 describes that

such errors should be recognized in the year in which they would have been

recorded (Deloitte, n.d.).

In the present case, fraud will be accounted for according to the IAS 8 and

financial statement of the year 2018 needs to be amended accordingly. Disclosure

thereof requires to be reported in the financial statements.

SOLUTION 2:- ACCOUNTING IN CASE OF ISSUES OF

SHARES

i) Accounting in the books of Rippa Ltd. for the issue of shares shall be as under:

Journal Entries

Sr. No. Date Entries Amount ($)

1 10-08-

2017

Bank Dr.

1,25,00,00

0

Share Application Account Cr.

1,25,00,00

0

(Being share application amount

recorded)

5 | P a g e

instruments should be recognized at market value on reporting date.

IAS 10 deals with the ‘Events after reporting periods’. It describes the recording

of those transactions in the books of the company, any conditions thereof are

exists on reporting date. If, no such condition exists on that date, these

transactions should be reported separately in the books of the company (Deloitte,

n.d.).

In present case, as on reporting date there was no condition exists for the major

fall in the share market. As such, company should record the investment in shares

of ABC Ltd. at fair market value of $ 600000 and it should report the major fall in

the notes to accounts.

iv) Accounting of fraudulent cases: In the given case, person expenditure of

accountant has been booked as advertisement expenses on 20 April 2018. This

case of fraud has been noticed on 21 July 2018.

IAS 8 will be applicable in this case because IAS 8 includes the accounting

treatment of prior period events. Prior period events mean any omission and

misstatement in the financial statement of the earlier years. IAS 8 describes that

such errors should be recognized in the year in which they would have been

recorded (Deloitte, n.d.).

In the present case, fraud will be accounted for according to the IAS 8 and

financial statement of the year 2018 needs to be amended accordingly. Disclosure

thereof requires to be reported in the financial statements.

SOLUTION 2:- ACCOUNTING IN CASE OF ISSUES OF

SHARES

i) Accounting in the books of Rippa Ltd. for the issue of shares shall be as under:

Journal Entries

Sr. No. Date Entries Amount ($)

1 10-08-

2017

Bank Dr.

1,25,00,00

0

Share Application Account Cr.

1,25,00,00

0

(Being share application amount

recorded)

5 | P a g e

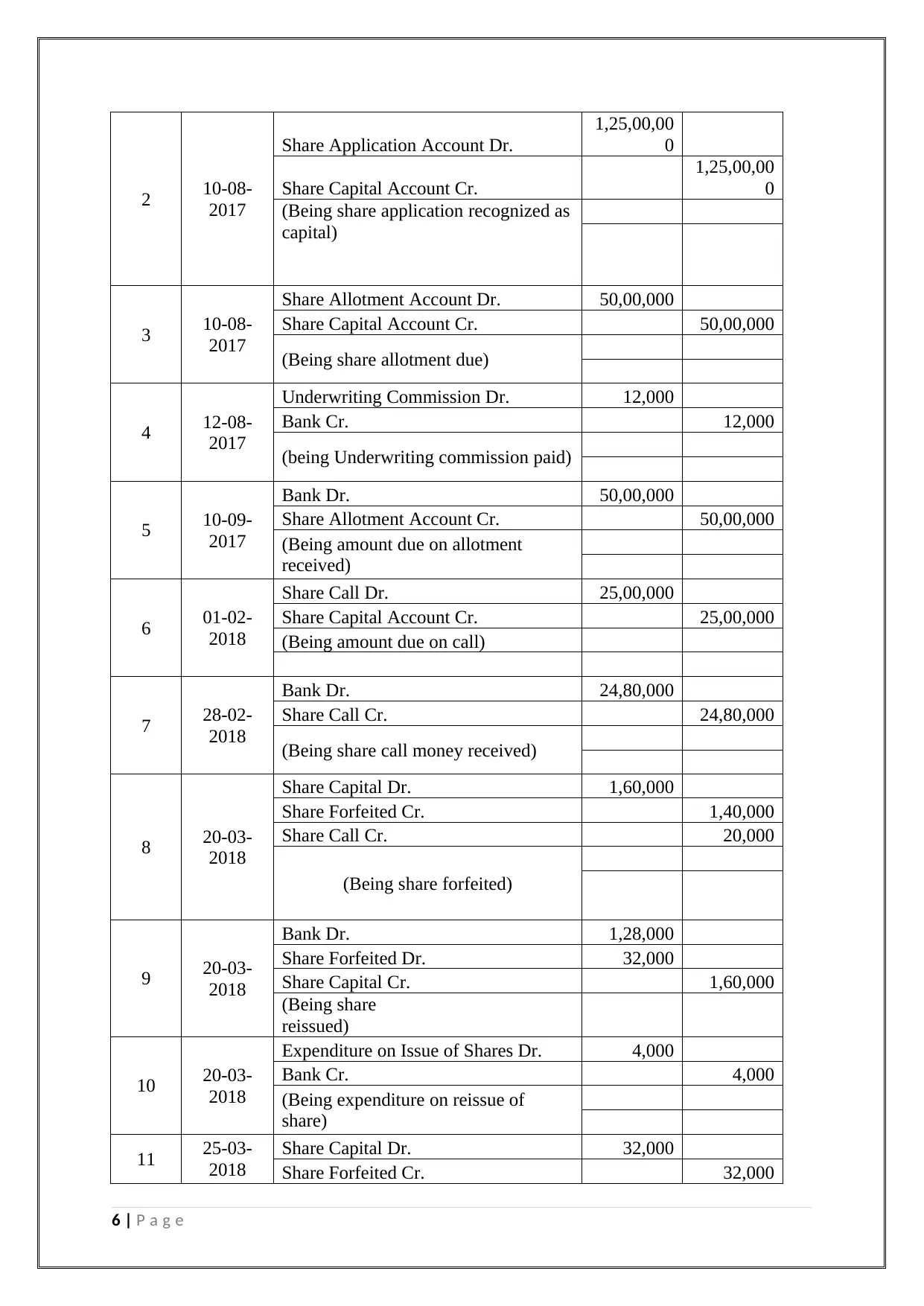

2 10-08-

2017

Share Application Account Dr.

1,25,00,00

0

Share Capital Account Cr.

1,25,00,00

0

(Being share application recognized as

capital)

3 10-08-

2017

Share Allotment Account Dr. 50,00,000

Share Capital Account Cr. 50,00,000

(Being share allotment due)

4 12-08-

2017

Underwriting Commission Dr. 12,000

Bank Cr. 12,000

(being Underwriting commission paid)

5 10-09-

2017

Bank Dr. 50,00,000

Share Allotment Account Cr. 50,00,000

(Being amount due on allotment

received)

6 01-02-

2018

Share Call Dr. 25,00,000

Share Capital Account Cr. 25,00,000

(Being amount due on call)

7 28-02-

2018

Bank Dr. 24,80,000

Share Call Cr. 24,80,000

(Being share call money received)

8 20-03-

2018

Share Capital Dr. 1,60,000

Share Forfeited Cr. 1,40,000

Share Call Cr. 20,000

(Being share forfeited)

9 20-03-

2018

Bank Dr. 1,28,000

Share Forfeited Dr. 32,000

Share Capital Cr. 1,60,000

(Being share

reissued)

10 20-03-

2018

Expenditure on Issue of Shares Dr. 4,000

Bank Cr. 4,000

(Being expenditure on reissue of

share)

11 25-03-

2018

Share Capital Dr. 32,000

Share Forfeited Cr. 32,000

6 | P a g e

2017

Share Application Account Dr.

1,25,00,00

0

Share Capital Account Cr.

1,25,00,00

0

(Being share application recognized as

capital)

3 10-08-

2017

Share Allotment Account Dr. 50,00,000

Share Capital Account Cr. 50,00,000

(Being share allotment due)

4 12-08-

2017

Underwriting Commission Dr. 12,000

Bank Cr. 12,000

(being Underwriting commission paid)

5 10-09-

2017

Bank Dr. 50,00,000

Share Allotment Account Cr. 50,00,000

(Being amount due on allotment

received)

6 01-02-

2018

Share Call Dr. 25,00,000

Share Capital Account Cr. 25,00,000

(Being amount due on call)

7 28-02-

2018

Bank Dr. 24,80,000

Share Call Cr. 24,80,000

(Being share call money received)

8 20-03-

2018

Share Capital Dr. 1,60,000

Share Forfeited Cr. 1,40,000

Share Call Cr. 20,000

(Being share forfeited)

9 20-03-

2018

Bank Dr. 1,28,000

Share Forfeited Dr. 32,000

Share Capital Cr. 1,60,000

(Being share

reissued)

10 20-03-

2018

Expenditure on Issue of Shares Dr. 4,000

Bank Cr. 4,000

(Being expenditure on reissue of

share)

11 25-03-

2018

Share Capital Dr. 32,000

Share Forfeited Cr. 32,000

6 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

(Being share forfeited balance returned

to shareholder)

ii) Refund of Forfeiture Share Account: The Company had forfeited the shares of the

shareholders, who did not pay the calls money within the due date. All these

happen as per agreements between the company and shareholders. In the instant

case, share was forfeited at $ 3.5 per share. But share refunded at $ 2.7 per share

($ 108000/40000). Difference of $ 0.8 per share amounting to $ 32,000 has not

been paid. Reason thereof is that due to default made by the former shareholders

new share were issued at only $ 3.2 per share. If the default is not made the

company would be receiving the amount at the rate of $ 4 per share. As such, this

loss to company will not be borne by it and company had paid to the former

shareholder at $ 3.2 per instead of $ 3.5 per share.

SOLUTION 3:- ACCOUNTING OF TAXES

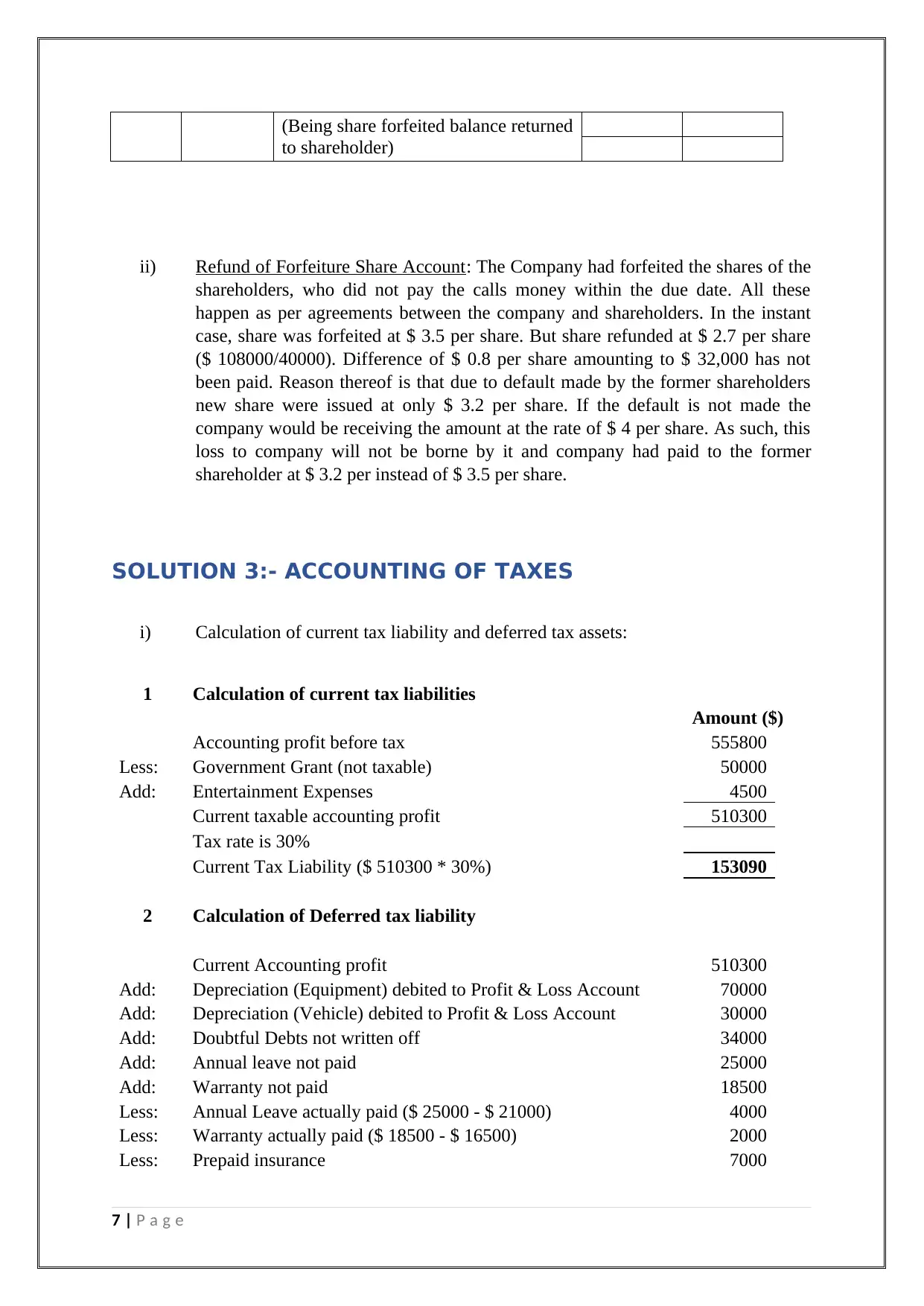

i) Calculation of current tax liability and deferred tax assets:

1 Calculation of current tax liabilities

Amount ($)

Accounting profit before tax 555800

Less: Government Grant (not taxable) 50000

Add: Entertainment Expenses 4500

Current taxable accounting profit 510300

Tax rate is 30%

Current Tax Liability ($ 510300 * 30%) 153090

2 Calculation of Deferred tax liability

Current Accounting profit 510300

Add: Depreciation (Equipment) debited to Profit & Loss Account 70000

Add: Depreciation (Vehicle) debited to Profit & Loss Account 30000

Add: Doubtful Debts not written off 34000

Add: Annual leave not paid 25000

Add: Warranty not paid 18500

Less: Annual Leave actually paid ($ 25000 - $ 21000) 4000

Less: Warranty actually paid ($ 18500 - $ 16500) 2000

Less: Prepaid insurance 7000

7 | P a g e

to shareholder)

ii) Refund of Forfeiture Share Account: The Company had forfeited the shares of the

shareholders, who did not pay the calls money within the due date. All these

happen as per agreements between the company and shareholders. In the instant

case, share was forfeited at $ 3.5 per share. But share refunded at $ 2.7 per share

($ 108000/40000). Difference of $ 0.8 per share amounting to $ 32,000 has not

been paid. Reason thereof is that due to default made by the former shareholders

new share were issued at only $ 3.2 per share. If the default is not made the

company would be receiving the amount at the rate of $ 4 per share. As such, this

loss to company will not be borne by it and company had paid to the former

shareholder at $ 3.2 per instead of $ 3.5 per share.

SOLUTION 3:- ACCOUNTING OF TAXES

i) Calculation of current tax liability and deferred tax assets:

1 Calculation of current tax liabilities

Amount ($)

Accounting profit before tax 555800

Less: Government Grant (not taxable) 50000

Add: Entertainment Expenses 4500

Current taxable accounting profit 510300

Tax rate is 30%

Current Tax Liability ($ 510300 * 30%) 153090

2 Calculation of Deferred tax liability

Current Accounting profit 510300

Add: Depreciation (Equipment) debited to Profit & Loss Account 70000

Add: Depreciation (Vehicle) debited to Profit & Loss Account 30000

Add: Doubtful Debts not written off 34000

Add: Annual leave not paid 25000

Add: Warranty not paid 18500

Less: Annual Leave actually paid ($ 25000 - $ 21000) 4000

Less: Warranty actually paid ($ 18500 - $ 16500) 2000

Less: Prepaid insurance 7000

7 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

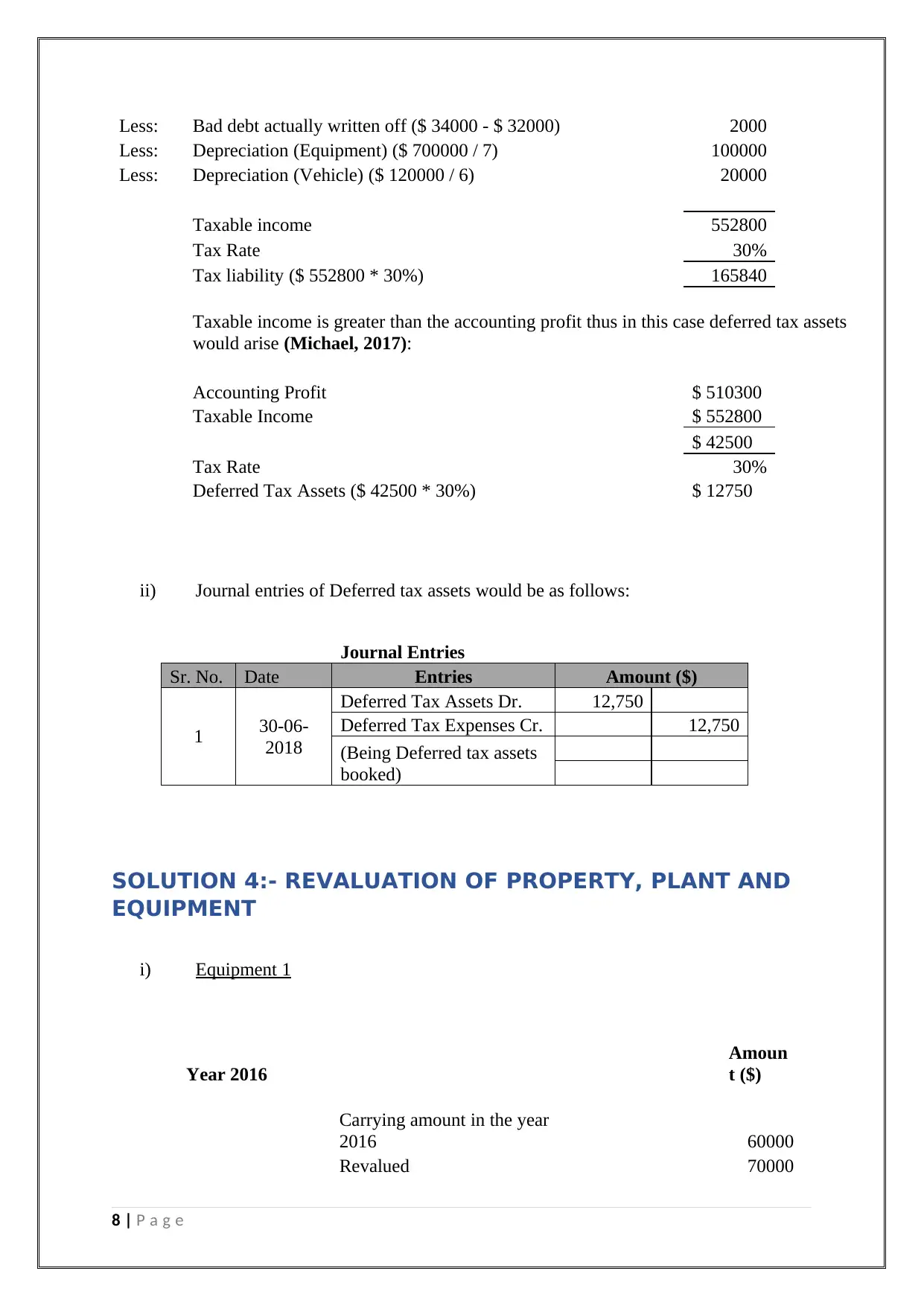

Less: Bad debt actually written off ($ 34000 - $ 32000) 2000

Less: Depreciation (Equipment) ($ 700000 / 7) 100000

Less: Depreciation (Vehicle) ($ 120000 / 6) 20000

Taxable income 552800

Tax Rate 30%

Tax liability ($ 552800 * 30%) 165840

Taxable income is greater than the accounting profit thus in this case deferred tax assets

would arise (Michael, 2017):

Accounting Profit $ 510300

Taxable Income $ 552800

$ 42500

Tax Rate 30%

Deferred Tax Assets ($ 42500 * 30%) $ 12750

ii) Journal entries of Deferred tax assets would be as follows:

Journal Entries

Sr. No. Date Entries Amount ($)

1 30-06-

2018

Deferred Tax Assets Dr. 12,750

Deferred Tax Expenses Cr. 12,750

(Being Deferred tax assets

booked)

SOLUTION 4:- REVALUATION OF PROPERTY, PLANT AND

EQUIPMENT

i) Equipment 1

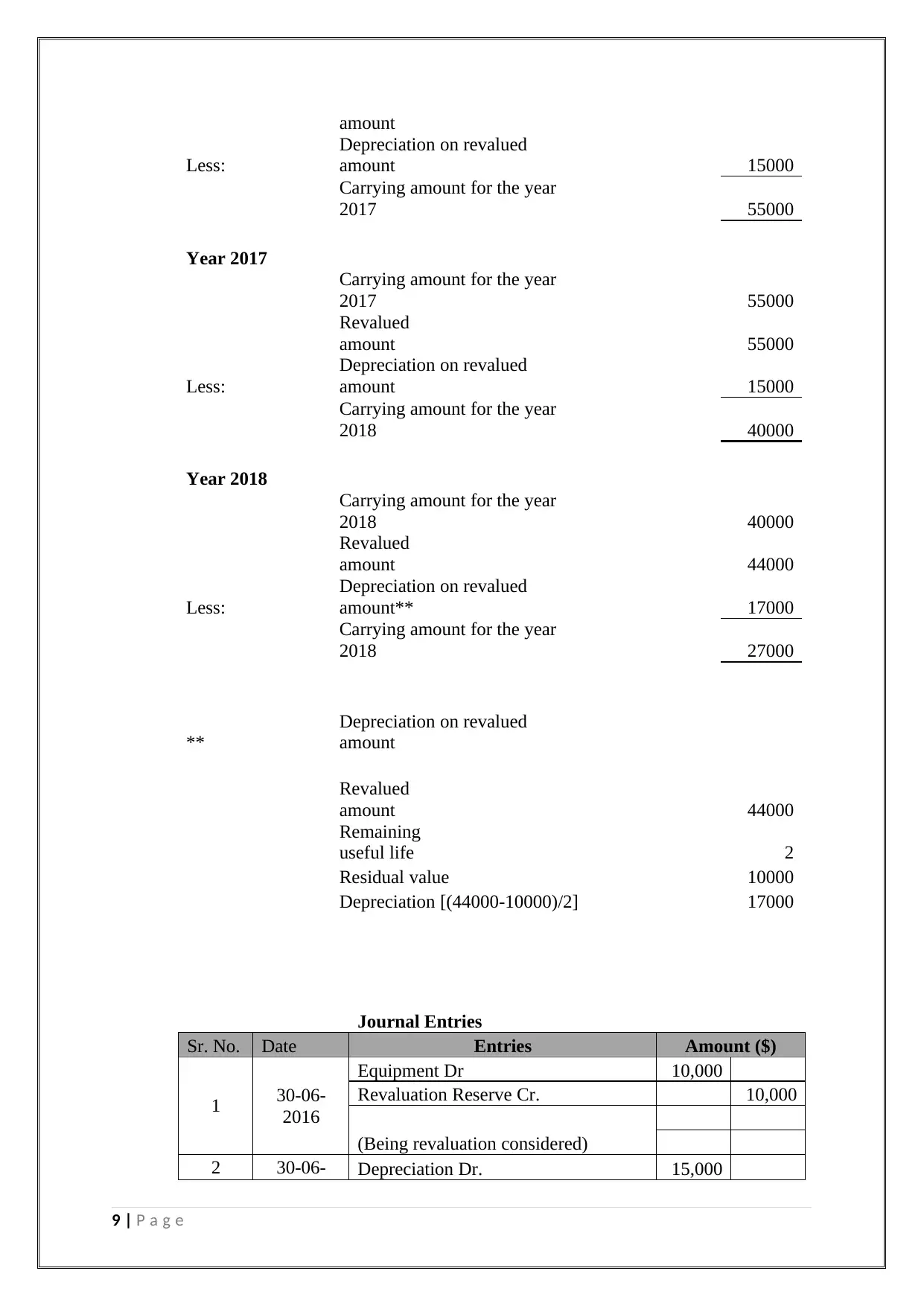

Year 2016

Amoun

t ($)

Carrying amount in the year

2016 60000

Revalued 70000

8 | P a g e

Less: Depreciation (Equipment) ($ 700000 / 7) 100000

Less: Depreciation (Vehicle) ($ 120000 / 6) 20000

Taxable income 552800

Tax Rate 30%

Tax liability ($ 552800 * 30%) 165840

Taxable income is greater than the accounting profit thus in this case deferred tax assets

would arise (Michael, 2017):

Accounting Profit $ 510300

Taxable Income $ 552800

$ 42500

Tax Rate 30%

Deferred Tax Assets ($ 42500 * 30%) $ 12750

ii) Journal entries of Deferred tax assets would be as follows:

Journal Entries

Sr. No. Date Entries Amount ($)

1 30-06-

2018

Deferred Tax Assets Dr. 12,750

Deferred Tax Expenses Cr. 12,750

(Being Deferred tax assets

booked)

SOLUTION 4:- REVALUATION OF PROPERTY, PLANT AND

EQUIPMENT

i) Equipment 1

Year 2016

Amoun

t ($)

Carrying amount in the year

2016 60000

Revalued 70000

8 | P a g e

amount

Less:

Depreciation on revalued

amount 15000

Carrying amount for the year

2017 55000

Year 2017

Carrying amount for the year

2017 55000

Revalued

amount 55000

Less:

Depreciation on revalued

amount 15000

Carrying amount for the year

2018 40000

Year 2018

Carrying amount for the year

2018 40000

Revalued

amount 44000

Less:

Depreciation on revalued

amount** 17000

Carrying amount for the year

2018 27000

**

Depreciation on revalued

amount

Revalued

amount 44000

Remaining

useful life 2

Residual value 10000

Depreciation [(44000-10000)/2] 17000

Journal Entries

Sr. No. Date Entries Amount ($)

1 30-06-

2016

Equipment Dr 10,000

Revaluation Reserve Cr. 10,000

(Being revaluation considered)

2 30-06- Depreciation Dr. 15,000

9 | P a g e

Less:

Depreciation on revalued

amount 15000

Carrying amount for the year

2017 55000

Year 2017

Carrying amount for the year

2017 55000

Revalued

amount 55000

Less:

Depreciation on revalued

amount 15000

Carrying amount for the year

2018 40000

Year 2018

Carrying amount for the year

2018 40000

Revalued

amount 44000

Less:

Depreciation on revalued

amount** 17000

Carrying amount for the year

2018 27000

**

Depreciation on revalued

amount

Revalued

amount 44000

Remaining

useful life 2

Residual value 10000

Depreciation [(44000-10000)/2] 17000

Journal Entries

Sr. No. Date Entries Amount ($)

1 30-06-

2016

Equipment Dr 10,000

Revaluation Reserve Cr. 10,000

(Being revaluation considered)

2 30-06- Depreciation Dr. 15,000

9 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2016

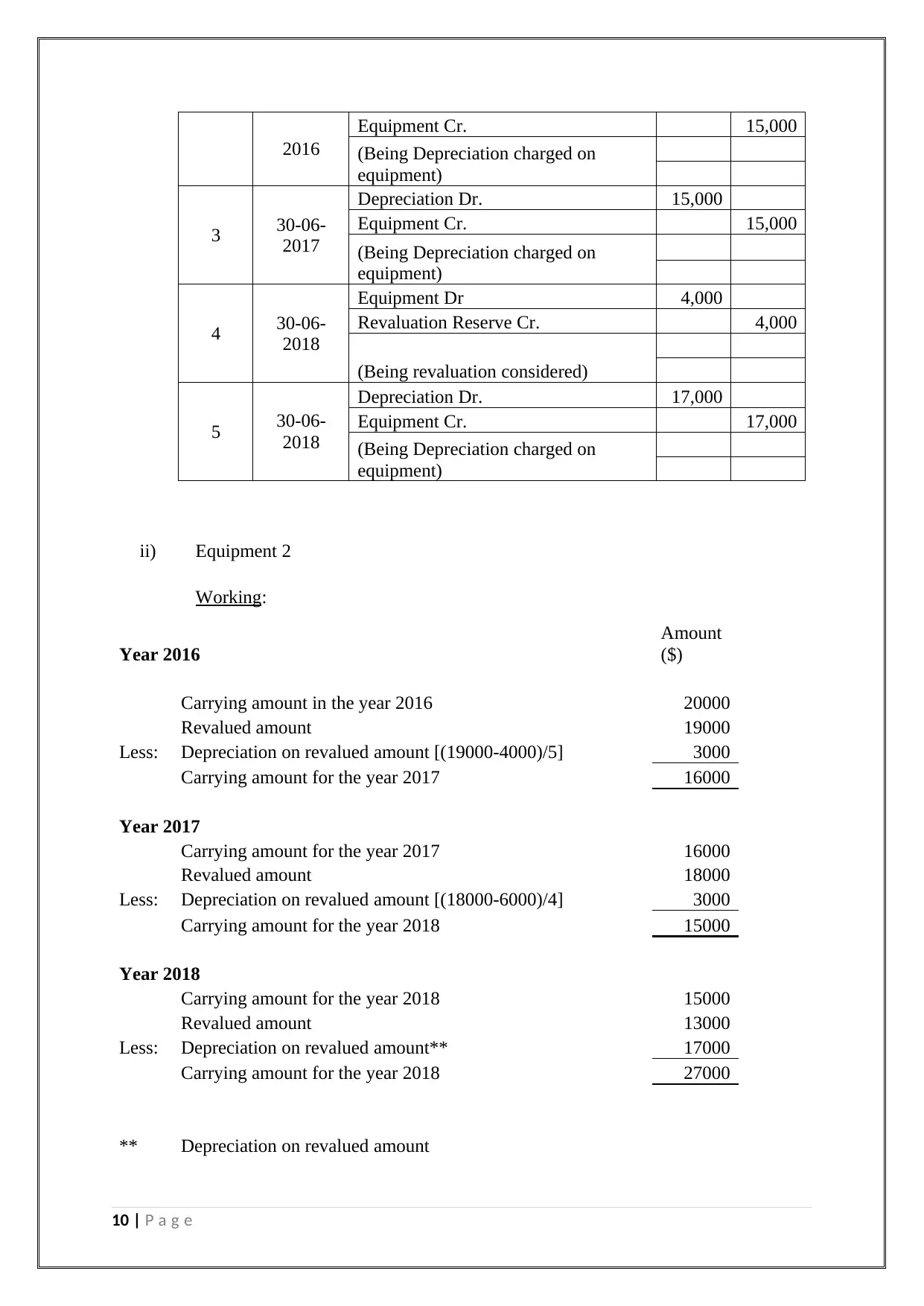

Equipment Cr. 15,000

(Being Depreciation charged on

equipment)

3 30-06-

2017

Depreciation Dr. 15,000

Equipment Cr. 15,000

(Being Depreciation charged on

equipment)

4 30-06-

2018

Equipment Dr 4,000

Revaluation Reserve Cr. 4,000

(Being revaluation considered)

5 30-06-

2018

Depreciation Dr. 17,000

Equipment Cr. 17,000

(Being Depreciation charged on

equipment)

ii) Equipment 2

Working:

Year 2016

Amount

($)

Carrying amount in the year 2016 20000

Revalued amount 19000

Less: Depreciation on revalued amount [(19000-4000)/5] 3000

Carrying amount for the year 2017 16000

Year 2017

Carrying amount for the year 2017 16000

Revalued amount 18000

Less: Depreciation on revalued amount [(18000-6000)/4] 3000

Carrying amount for the year 2018 15000

Year 2018

Carrying amount for the year 2018 15000

Revalued amount 13000

Less: Depreciation on revalued amount** 17000

Carrying amount for the year 2018 27000

** Depreciation on revalued amount

10 | P a g e

Equipment Cr. 15,000

(Being Depreciation charged on

equipment)

3 30-06-

2017

Depreciation Dr. 15,000

Equipment Cr. 15,000

(Being Depreciation charged on

equipment)

4 30-06-

2018

Equipment Dr 4,000

Revaluation Reserve Cr. 4,000

(Being revaluation considered)

5 30-06-

2018

Depreciation Dr. 17,000

Equipment Cr. 17,000

(Being Depreciation charged on

equipment)

ii) Equipment 2

Working:

Year 2016

Amount

($)

Carrying amount in the year 2016 20000

Revalued amount 19000

Less: Depreciation on revalued amount [(19000-4000)/5] 3000

Carrying amount for the year 2017 16000

Year 2017

Carrying amount for the year 2017 16000

Revalued amount 18000

Less: Depreciation on revalued amount [(18000-6000)/4] 3000

Carrying amount for the year 2018 15000

Year 2018

Carrying amount for the year 2018 15000

Revalued amount 13000

Less: Depreciation on revalued amount** 17000

Carrying amount for the year 2018 27000

** Depreciation on revalued amount

10 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Revalued amount 13000

Remaining useful life 3

Residual value 6000

Depreciation [(13000-6000)/3] 2333

SOLUTION 5:- IMPAIRMENT OF ASSETS

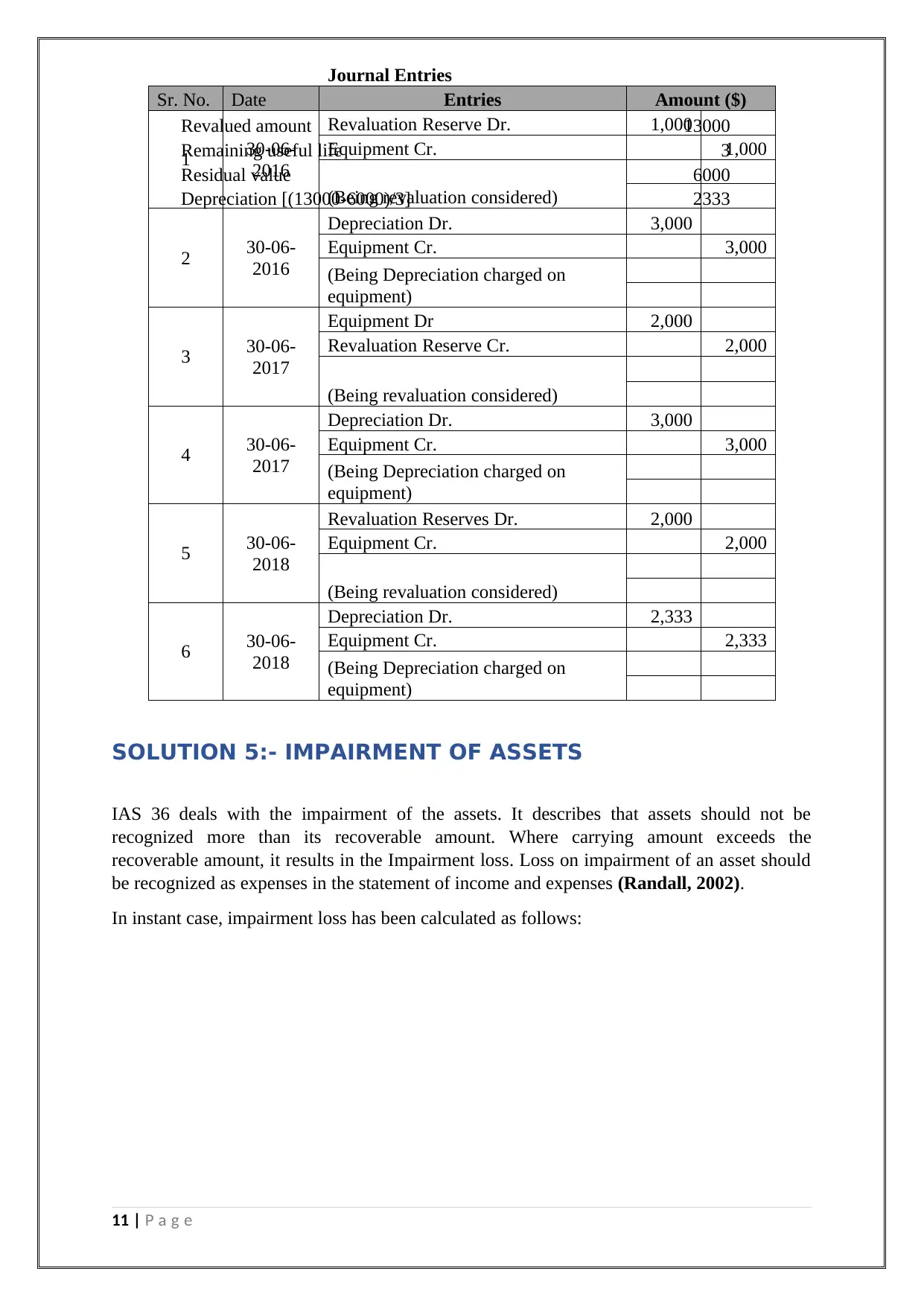

IAS 36 deals with the impairment of the assets. It describes that assets should not be

recognized more than its recoverable amount. Where carrying amount exceeds the

recoverable amount, it results in the Impairment loss. Loss on impairment of an asset should

be recognized as expenses in the statement of income and expenses (Randall, 2002).

In instant case, impairment loss has been calculated as follows:

11 | P a g e

Journal Entries

Sr. No. Date Entries Amount ($)

1 30-06-

2016

Revaluation Reserve Dr. 1,000

Equipment Cr. 1,000

(Being revaluation considered)

2 30-06-

2016

Depreciation Dr. 3,000

Equipment Cr. 3,000

(Being Depreciation charged on

equipment)

3 30-06-

2017

Equipment Dr 2,000

Revaluation Reserve Cr. 2,000

(Being revaluation considered)

4 30-06-

2017

Depreciation Dr. 3,000

Equipment Cr. 3,000

(Being Depreciation charged on

equipment)

5 30-06-

2018

Revaluation Reserves Dr. 2,000

Equipment Cr. 2,000

(Being revaluation considered)

6 30-06-

2018

Depreciation Dr. 2,333

Equipment Cr. 2,333

(Being Depreciation charged on

equipment)

Remaining useful life 3

Residual value 6000

Depreciation [(13000-6000)/3] 2333

SOLUTION 5:- IMPAIRMENT OF ASSETS

IAS 36 deals with the impairment of the assets. It describes that assets should not be

recognized more than its recoverable amount. Where carrying amount exceeds the

recoverable amount, it results in the Impairment loss. Loss on impairment of an asset should

be recognized as expenses in the statement of income and expenses (Randall, 2002).

In instant case, impairment loss has been calculated as follows:

11 | P a g e

Journal Entries

Sr. No. Date Entries Amount ($)

1 30-06-

2016

Revaluation Reserve Dr. 1,000

Equipment Cr. 1,000

(Being revaluation considered)

2 30-06-

2016

Depreciation Dr. 3,000

Equipment Cr. 3,000

(Being Depreciation charged on

equipment)

3 30-06-

2017

Equipment Dr 2,000

Revaluation Reserve Cr. 2,000

(Being revaluation considered)

4 30-06-

2017

Depreciation Dr. 3,000

Equipment Cr. 3,000

(Being Depreciation charged on

equipment)

5 30-06-

2018

Revaluation Reserves Dr. 2,000

Equipment Cr. 2,000

(Being revaluation considered)

6 30-06-

2018

Depreciation Dr. 2,333

Equipment Cr. 2,333

(Being Depreciation charged on

equipment)

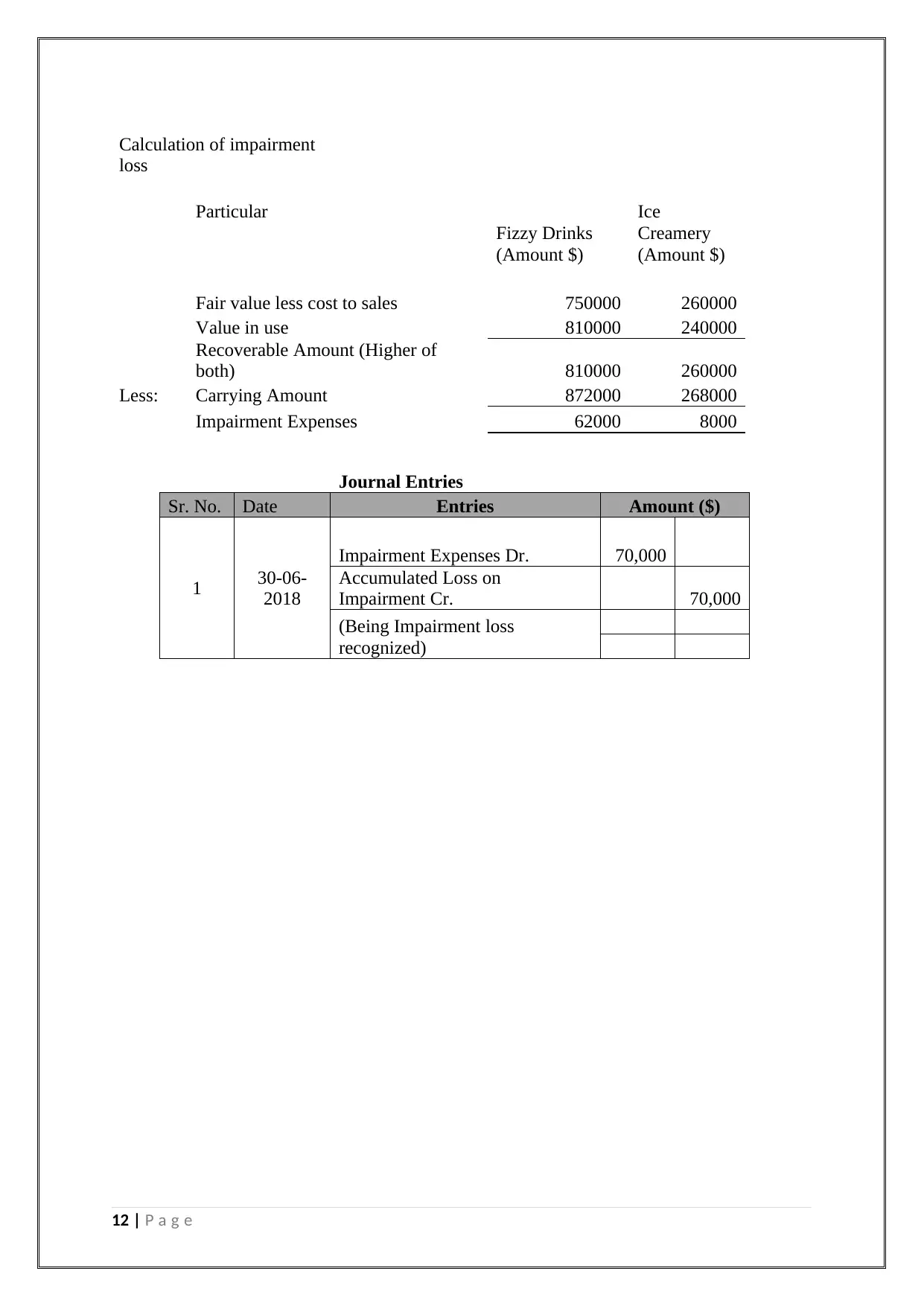

Calculation of impairment

loss

Particular

Fizzy Drinks

(Amount $)

Ice

Creamery

(Amount $)

Fair value less cost to sales 750000 260000

Value in use 810000 240000

Recoverable Amount (Higher of

both) 810000 260000

Less: Carrying Amount 872000 268000

Impairment Expenses 62000 8000

Journal Entries

Sr. No. Date Entries Amount ($)

1 30-06-

2018

Impairment Expenses Dr. 70,000

Accumulated Loss on

Impairment Cr. 70,000

(Being Impairment loss

recognized)

12 | P a g e

loss

Particular

Fizzy Drinks

(Amount $)

Ice

Creamery

(Amount $)

Fair value less cost to sales 750000 260000

Value in use 810000 240000

Recoverable Amount (Higher of

both) 810000 260000

Less: Carrying Amount 872000 268000

Impairment Expenses 62000 8000

Journal Entries

Sr. No. Date Entries Amount ($)

1 30-06-

2018

Impairment Expenses Dr. 70,000

Accumulated Loss on

Impairment Cr. 70,000

(Being Impairment loss

recognized)

12 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.