Middlesex University ACC3125: Accounting Theory Report

VerifiedAdded on 2023/05/30

|12

|3028

|500

Report

AI Summary

This report delves into the core of accounting theory, examining the construction of accounting information, the evolution of accounting practices, and the importance of financial statements in communicating an organization's financial position. It explores the role of accounting concepts, such as the going concern assumption, accrual basis, prudence, and consistency, in ensuring the reliability and relevance of financial reporting. The report also analyzes the inductive and deductive approaches to gathering knowledge in accounting, the influence of International Financial Reporting Standards (IFRS) and Generally Accepted Accounting Principles (GAAP), and the significance of conceptual frameworks in enhancing the quality of financial information. Furthermore, it highlights the importance of qualitative characteristics, like relevance, reliability, comparability, and understandability, in meeting the needs of financial statement users and ensuring a true and fair view of an entity's financial performance. The report also discusses the historical development of accounting standards and the need for updates in response to the changing business environment.

Running head: ACCOUNTING THEORY

Accounting Theory

Name of the Student:

Name of the University:

Authors Note:

Accounting Theory

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

ACCOUNTING THEORY

Accounting concepts are central to the construction of accounting information. Critical

evaluation:

Communication of financial information of corporate and non-corporate entities by

measuring, processing and classifying financial transactions is what accounting is all about.

Accounting as a subject has evolved over the years to improve its ability to provide useful

information to the users of accounting information. It is based on the concept that the financial

transactions must be properly classified and recorded in the books of accounts to keep record of

all financial transactions to provide useful information to the stakeholders of an organization.

Communicating true and fair picture of an organization is the objective of accounting however,

there are number of limitations in accounting which make it almost impossible to achieve the

ultimate objective with 100% precision. Accounting concepts are the accumulation of

accounting rules and regulations to be followed in recording financial transactions in the books

of accounts to improve the ability of the financial statements to portray true and fair picture of

business organizations (Schrader and William, 1962). According to Walton, P (1993), “True and

fair representation of financial performance and position of an entity is essential to the

construction of accounting information”. As an example the financial information disclosed in

the financial statements of Enron did not reflected the actual financial state of the company

immediately prior to its collapse. Thus, it is important to ensure that financial statements reflect

the true and fair picture of an entity to be useful to the users of financial statements (Walton,

1993).

Knowledge is gathered and acquired over a period of time and it is the experience that one

receives from practical implementation of theoretical knowledge that helps the person to

understand about the subject better. Accounting is the underlying foundation on the basis of

ACCOUNTING THEORY

Accounting concepts are central to the construction of accounting information. Critical

evaluation:

Communication of financial information of corporate and non-corporate entities by

measuring, processing and classifying financial transactions is what accounting is all about.

Accounting as a subject has evolved over the years to improve its ability to provide useful

information to the users of accounting information. It is based on the concept that the financial

transactions must be properly classified and recorded in the books of accounts to keep record of

all financial transactions to provide useful information to the stakeholders of an organization.

Communicating true and fair picture of an organization is the objective of accounting however,

there are number of limitations in accounting which make it almost impossible to achieve the

ultimate objective with 100% precision. Accounting concepts are the accumulation of

accounting rules and regulations to be followed in recording financial transactions in the books

of accounts to improve the ability of the financial statements to portray true and fair picture of

business organizations (Schrader and William, 1962). According to Walton, P (1993), “True and

fair representation of financial performance and position of an entity is essential to the

construction of accounting information”. As an example the financial information disclosed in

the financial statements of Enron did not reflected the actual financial state of the company

immediately prior to its collapse. Thus, it is important to ensure that financial statements reflect

the true and fair picture of an entity to be useful to the users of financial statements (Walton,

1993).

Knowledge is gathered and acquired over a period of time and it is the experience that one

receives from practical implementation of theoretical knowledge that helps the person to

understand about the subject better. Accounting is the underlying foundation on the basis of

2

ACCOUNTING THEORY

which the financial information about an organization is provided to different stakeholders.

Financial statements include Balance sheet, profit and loss account, cash flow statement and

notes to accounts (Tinker, 1991).

Sources of knowledge is equally important to the proper accumulation of financial information.

PRIMFIT analysis shall be helpful in understanding knowledge and the sources of knowledge.

Accounting is a mix of arts and science and thus, there are certain characteristics of both

which makes it neither completely scientific nor completely artistic. Accounting is a process

which helps in recording financial transactions properly. It creates a perception about an

organization and its performance by constructing reality by recording all financial transactions

(Trochim and Donnelly, 2006).

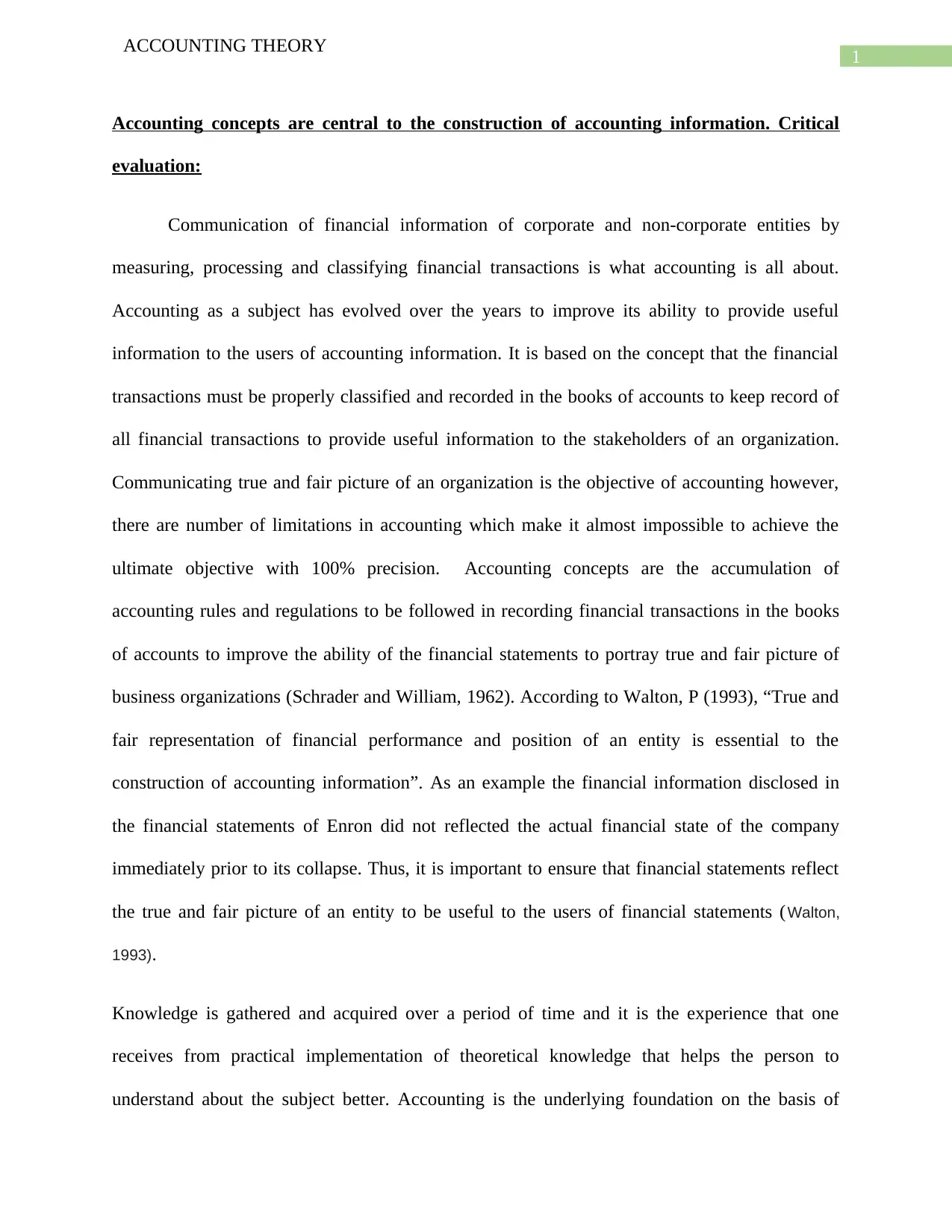

The observation made from various financial data provided about an entity helps the

users of such financial data to make assertion about the entity and its financial performance as

per the induction process. The assertions are made on the basis of generalized theory and

concepts of accounting. Inductive approach enables the users of accounting information to create

perception about an entity by using the monetary information of the entity. Deductive reasoning

on the other hand does not allow the imaginations of the users of financial information to create

perception as the approach starts with established theory. The approach of deductive reasoning

allows the users to ascertain the true and fair nature of financial information with its logical

explanation and reasoning.

ACCOUNTING THEORY

which the financial information about an organization is provided to different stakeholders.

Financial statements include Balance sheet, profit and loss account, cash flow statement and

notes to accounts (Tinker, 1991).

Sources of knowledge is equally important to the proper accumulation of financial information.

PRIMFIT analysis shall be helpful in understanding knowledge and the sources of knowledge.

Accounting is a mix of arts and science and thus, there are certain characteristics of both

which makes it neither completely scientific nor completely artistic. Accounting is a process

which helps in recording financial transactions properly. It creates a perception about an

organization and its performance by constructing reality by recording all financial transactions

(Trochim and Donnelly, 2006).

The observation made from various financial data provided about an entity helps the

users of such financial data to make assertion about the entity and its financial performance as

per the induction process. The assertions are made on the basis of generalized theory and

concepts of accounting. Inductive approach enables the users of accounting information to create

perception about an entity by using the monetary information of the entity. Deductive reasoning

on the other hand does not allow the imaginations of the users of financial information to create

perception as the approach starts with established theory. The approach of deductive reasoning

allows the users to ascertain the true and fair nature of financial information with its logical

explanation and reasoning.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

ACCOUNTING THEORY

The conceptual framework in accounting is essential to the understanding of users of

financial statements as it is based on the theoretical aspect of accounting. The objective of

accounting information to correctly disclose the financial information of an organization is

possible to be achieved only if the core principles of accounting developed in the conceptual

framework are followed in preparation and presentation of financial statements. The

inconsistency in financial reporting standards and accounting policies have been reduced

significantly subsequent to the development of conceptual framework in accounting. Morgan, G.,

1988 stated that “the importance of conceptual framework in accounting is immense to enhance the

quality of financial information”.

Financial statements are prepared in accordance with financial information accumulated

in the books of accounts as per accounting concepts include Balance sheet, profit and loss

account, cash flow statement and notes to accounts. According to Atrill & Mclaney (1995, page

21), “The purpose of the b/s is simply to set out the financial position of a business at a

particular moment in time” (Atrill and Mclaney, 1995). The accounting concepts if not

ACCOUNTING THEORY

The conceptual framework in accounting is essential to the understanding of users of

financial statements as it is based on the theoretical aspect of accounting. The objective of

accounting information to correctly disclose the financial information of an organization is

possible to be achieved only if the core principles of accounting developed in the conceptual

framework are followed in preparation and presentation of financial statements. The

inconsistency in financial reporting standards and accounting policies have been reduced

significantly subsequent to the development of conceptual framework in accounting. Morgan, G.,

1988 stated that “the importance of conceptual framework in accounting is immense to enhance the

quality of financial information”.

Financial statements are prepared in accordance with financial information accumulated

in the books of accounts as per accounting concepts include Balance sheet, profit and loss

account, cash flow statement and notes to accounts. According to Atrill & Mclaney (1995, page

21), “The purpose of the b/s is simply to set out the financial position of a business at a

particular moment in time” (Atrill and Mclaney, 1995). The accounting concepts if not

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

ACCOUNTING THEORY

followed properly then it would be not possible to construct useful accounting information for

the users of financial statements. Solomons talked about importance of neutrality and

representation of faithfulness in accounting information to be useful. The accounting concepts

must be followed properly in order ensure that the accounting information have these qualitative

characteristics necessary to help the users of financial statements to assess the financial

performance and position of an organization properly (Solomons, 1991).

Solomon and Tinker used different perspectives to explain the role of accountants. Both

have agreed on the importance of neutrality of accounting information by comparing the job of

accountants with that of journalists and telephone. According to Solomon accountants shall be

more like journalists to report information and not to make information. Importance of neutrality

and reliability in ensuring that true and correct information is provided about an entity is

essential in accounting.

Tony Tinker on the other has questioned the integrity of journalists. According to Tinker

journalists often use biased reporting to distort reality. Also with the objective of attracting

maximum eye balls and public attention journalists often use untrue and sensational reporting.

Accountants often do the same for business organizations by using favourable and manipulative

accounting guidelines to portray a better or worst picture for an organization than the actual

reality to support the objectives of executive management.

International Financial Reporting Standards (IFRS) and Generally Accepted Accounting

Principles (GAAP) have provided relevant accounting standards to be followed by companies

and other forms of business organizations operating in and around the world to ensure that the

books of accounts and financial statements are correctly complied and prepared to show the true

ACCOUNTING THEORY

followed properly then it would be not possible to construct useful accounting information for

the users of financial statements. Solomons talked about importance of neutrality and

representation of faithfulness in accounting information to be useful. The accounting concepts

must be followed properly in order ensure that the accounting information have these qualitative

characteristics necessary to help the users of financial statements to assess the financial

performance and position of an organization properly (Solomons, 1991).

Solomon and Tinker used different perspectives to explain the role of accountants. Both

have agreed on the importance of neutrality of accounting information by comparing the job of

accountants with that of journalists and telephone. According to Solomon accountants shall be

more like journalists to report information and not to make information. Importance of neutrality

and reliability in ensuring that true and correct information is provided about an entity is

essential in accounting.

Tony Tinker on the other has questioned the integrity of journalists. According to Tinker

journalists often use biased reporting to distort reality. Also with the objective of attracting

maximum eye balls and public attention journalists often use untrue and sensational reporting.

Accountants often do the same for business organizations by using favourable and manipulative

accounting guidelines to portray a better or worst picture for an organization than the actual

reality to support the objectives of executive management.

International Financial Reporting Standards (IFRS) and Generally Accepted Accounting

Principles (GAAP) have provided relevant accounting standards to be followed by companies

and other forms of business organizations operating in and around the world to ensure that the

books of accounts and financial statements are correctly complied and prepared to show the true

5

ACCOUNTING THEORY

and fair picture of business organizations. Accounting concepts are essential to the construction

of useful information and must be given due importance in maintaining the books of accounts of

an organization. IFRSs and GAAP have been developed as per the accounting concepts to be

followed in preparation and presentation of financial statements (Nagengast and Stehrer, 2016).

“There is only one reason for misleading financial statements. It is the failure or the

unwillingness of the public accounting profession to square the principles of accounting with its

professional responsibility to the public.” Quoted by Spacek thus, the lack of coherence among

accounting professional have certainly contributed to the disagreement between different

accounting standards IFRSs and GAAP. With the objective of resolving these issues in

accounting SSAP 2 was introduced. The qualitative characteristics of both GAAP and FASB

have been merged to formulate SSAP 2 with the objective of resolving the accounting issues.

SSAP 2 was based on the foundation of four concepts, also referred to as fundamental

accounting principles, discussed below.

One of the fundamental concepts of accounting is the going concern assumptions. The

presumption of an entity continuing its operations in the long run without any intention or reason

to cease operation is the fundamental concept of accounting. Financial accounting as well as

other branches of accounting are primarily founded on the above presumption. It is important to

state here, that going concern assumption is fundamental accounting assumption thus, in case it

has not been followed appropriate note shall be attached with the accounting information and

financial statements that the concept has not been followed along with reason for such non-

compliance. In going concern basis the valuation technique used to value inventories, other

current assets, fixed assets and liabilities are significantly different as compared to the valuation

technique used to value these under liquidation basis of accounting. Thus, the true and fair view

ACCOUNTING THEORY

and fair picture of business organizations. Accounting concepts are essential to the construction

of useful information and must be given due importance in maintaining the books of accounts of

an organization. IFRSs and GAAP have been developed as per the accounting concepts to be

followed in preparation and presentation of financial statements (Nagengast and Stehrer, 2016).

“There is only one reason for misleading financial statements. It is the failure or the

unwillingness of the public accounting profession to square the principles of accounting with its

professional responsibility to the public.” Quoted by Spacek thus, the lack of coherence among

accounting professional have certainly contributed to the disagreement between different

accounting standards IFRSs and GAAP. With the objective of resolving these issues in

accounting SSAP 2 was introduced. The qualitative characteristics of both GAAP and FASB

have been merged to formulate SSAP 2 with the objective of resolving the accounting issues.

SSAP 2 was based on the foundation of four concepts, also referred to as fundamental

accounting principles, discussed below.

One of the fundamental concepts of accounting is the going concern assumptions. The

presumption of an entity continuing its operations in the long run without any intention or reason

to cease operation is the fundamental concept of accounting. Financial accounting as well as

other branches of accounting are primarily founded on the above presumption. It is important to

state here, that going concern assumption is fundamental accounting assumption thus, in case it

has not been followed appropriate note shall be attached with the accounting information and

financial statements that the concept has not been followed along with reason for such non-

compliance. In going concern basis the valuation technique used to value inventories, other

current assets, fixed assets and liabilities are significantly different as compared to the valuation

technique used to value these under liquidation basis of accounting. Thus, the true and fair view

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

ACCOUNTING THEORY

of an organization in the form of financial information is certainly affected due to the accounting

concept. Hence, accountants as well as management which is responsible for the maintenance of

books of accounts of an entity must ensure that the fundamental accounting concepts and

principles are complied with in maintenance of books of accounts of the entity (Tinker, 1991).

Another fundamental accounting principle is accrual basis of accounting. As per the

concept, items of income and expenditures in the books of accounts shall be recorded as per

accrual basis and not in accordance to the receipts and payment basis. Thus, even if revenue not

received in a particular accounting period, it shall still be considered in the income statement of

an entity as per the accrual basis of accounting if the same has been earned in the accounting

period. Similarly, payment even if not made in an accounting year but the expenditure has been

incurred in the period then the income statement shall include such item of expenditure as per

accrual basis of accounting. Hence, the concept of accrual basis of accounting must be followed

in preparation and presentation of financial statements of the company (Morgan, 1988).

Prudence is another fundamental accounting concept that illustrates the importance of

not to overstate the amount of revenue and not to understate the amount of expenditures in the

books of accounts of an organization. It is a conservative concept where the assets are not

overstated and liabilities are not understated (Hendriksen, 1965). The objective of prudence is to

ensure that the financial statements are conservative in its disclosure of revenue and assets and

prudent to provide for all expenditures and liabilities. Thus, the objective behind the concept is to

ensure that until unless there is absolute certainty about final recovery of revenue it shall not be

recognized similarly asset shall only be recognized when there is significant certainty about the

future economic benefits accruing to the company from such assets. The concept ensures that the

ACCOUNTING THEORY

of an organization in the form of financial information is certainly affected due to the accounting

concept. Hence, accountants as well as management which is responsible for the maintenance of

books of accounts of an entity must ensure that the fundamental accounting concepts and

principles are complied with in maintenance of books of accounts of the entity (Tinker, 1991).

Another fundamental accounting principle is accrual basis of accounting. As per the

concept, items of income and expenditures in the books of accounts shall be recorded as per

accrual basis and not in accordance to the receipts and payment basis. Thus, even if revenue not

received in a particular accounting period, it shall still be considered in the income statement of

an entity as per the accrual basis of accounting if the same has been earned in the accounting

period. Similarly, payment even if not made in an accounting year but the expenditure has been

incurred in the period then the income statement shall include such item of expenditure as per

accrual basis of accounting. Hence, the concept of accrual basis of accounting must be followed

in preparation and presentation of financial statements of the company (Morgan, 1988).

Prudence is another fundamental accounting concept that illustrates the importance of

not to overstate the amount of revenue and not to understate the amount of expenditures in the

books of accounts of an organization. It is a conservative concept where the assets are not

overstated and liabilities are not understated (Hendriksen, 1965). The objective of prudence is to

ensure that the financial statements are conservative in its disclosure of revenue and assets and

prudent to provide for all expenditures and liabilities. Thus, the objective behind the concept is to

ensure that until unless there is absolute certainty about final recovery of revenue it shall not be

recognized similarly asset shall only be recognized when there is significant certainty about the

future economic benefits accruing to the company from such assets. The concept ensures that the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

ACCOUNTING THEORY

management regularly reviews the value of assets and liabilities to state these in correct values in

the books of accounts of an organization (Hines, 1988).

Consistency is the concept of accounting where an entity uses similar accounting

principles and policies year after year until unless a change is necessary as per the law and

regulations or change in accounting policies or principles will improve the true and fair view

characteristics of accounting information complied for an entity. Thus, for example an entity

using straight line method of depreciation shall continue to use the same method year after until

unless an alternative method such as written down value method will reflect more accurate

amount of depreciation in the books of accounts or a change in recent law makes it compulsory

for the organization to use written down value method to record depreciation in the books of

accounts (Schaltegger and Burritt, 2017).

With the ever evolving subject SSAP 2 was also updated by introduction of FRED 21.

With the changes in business world there was a need to make necessary changes to the existing

accounting concepts and hence, FRED 21 was introduced. Going concern and accruals concepts

have played pervasive role in accounting with consistency and prudence reduced to desirable

qualities in accounting information. Replacement of FRED 21 by FRS 18 however was an

important stepping stone in the right direction with formulation of accounting standard

“Disclosure of Accounting Policies” in 1971. The need for changes in accounting estimates,

importance of going concern and selection of accounting policies have been included in FRS 18.

The importance of relevance, reliability, comparability and understandability have been

explained by Henry Lent in the article, “The Fab Four’s Solo Careers”. The accounting

information must have these four qualitative characteristics to fulfil the requirements of the users

ACCOUNTING THEORY

management regularly reviews the value of assets and liabilities to state these in correct values in

the books of accounts of an organization (Hines, 1988).

Consistency is the concept of accounting where an entity uses similar accounting

principles and policies year after year until unless a change is necessary as per the law and

regulations or change in accounting policies or principles will improve the true and fair view

characteristics of accounting information complied for an entity. Thus, for example an entity

using straight line method of depreciation shall continue to use the same method year after until

unless an alternative method such as written down value method will reflect more accurate

amount of depreciation in the books of accounts or a change in recent law makes it compulsory

for the organization to use written down value method to record depreciation in the books of

accounts (Schaltegger and Burritt, 2017).

With the ever evolving subject SSAP 2 was also updated by introduction of FRED 21.

With the changes in business world there was a need to make necessary changes to the existing

accounting concepts and hence, FRED 21 was introduced. Going concern and accruals concepts

have played pervasive role in accounting with consistency and prudence reduced to desirable

qualities in accounting information. Replacement of FRED 21 by FRS 18 however was an

important stepping stone in the right direction with formulation of accounting standard

“Disclosure of Accounting Policies” in 1971. The need for changes in accounting estimates,

importance of going concern and selection of accounting policies have been included in FRS 18.

The importance of relevance, reliability, comparability and understandability have been

explained by Henry Lent in the article, “The Fab Four’s Solo Careers”. The accounting

information must have these four qualitative characteristics to fulfil the requirements of the users

8

ACCOUNTING THEORY

of financial statements. Conceptual guidelines is the framework within which the accounting

information must be compiled by the accountants in order to be relevant, reliable comparable and

understandable (Trochim and Donnelly, 2006). Further Lunt has classified users of accounting

information into 2 categories, internal users and external users of information. The reliability of

information to these users is primarily dependant on the ability of the accounting system to

correctly summarize and process financial transactions. Both internal and external users of

information will be benefitted from the accounting information only when the accounting

concepts such as going concern, accrual basis, prudence and consistency are followed (Lunt,

2016).

The concepts of accounting is the core of the subject and the profession. The value of

information as well as the purpose of the subject would be lost if the concepts as mentioned in

this document are not followed while summarizing, classifying and processing accounting

transactions. “Disclosure of accounting principles” is an accounting standard which illustrates

the significance of disclosing the accounting principles in case fundamental accounting concepts,

going concern, accrual, prudence, and consistency, are not followed. Thus, when an organization

does not follow any of the fundamental accounting concepts then it is necessary to make

necessary disclosure in the financial statements that any particular concept has not been followed

(Zeff, 2016).

In conclusion it is safe to say that the accounting concepts is certainly central to the

construction of true and correct accounting information. The books of accounts prepared in

accordance with the concepts of accounting, going concern, consistency, prudence and accrual,

will provide the correct underlying information on the basis of which financial statements of an

organization shall be prepared to show the true and fair picture of the organization. It is

ACCOUNTING THEORY

of financial statements. Conceptual guidelines is the framework within which the accounting

information must be compiled by the accountants in order to be relevant, reliable comparable and

understandable (Trochim and Donnelly, 2006). Further Lunt has classified users of accounting

information into 2 categories, internal users and external users of information. The reliability of

information to these users is primarily dependant on the ability of the accounting system to

correctly summarize and process financial transactions. Both internal and external users of

information will be benefitted from the accounting information only when the accounting

concepts such as going concern, accrual basis, prudence and consistency are followed (Lunt,

2016).

The concepts of accounting is the core of the subject and the profession. The value of

information as well as the purpose of the subject would be lost if the concepts as mentioned in

this document are not followed while summarizing, classifying and processing accounting

transactions. “Disclosure of accounting principles” is an accounting standard which illustrates

the significance of disclosing the accounting principles in case fundamental accounting concepts,

going concern, accrual, prudence, and consistency, are not followed. Thus, when an organization

does not follow any of the fundamental accounting concepts then it is necessary to make

necessary disclosure in the financial statements that any particular concept has not been followed

(Zeff, 2016).

In conclusion it is safe to say that the accounting concepts is certainly central to the

construction of true and correct accounting information. The books of accounts prepared in

accordance with the concepts of accounting, going concern, consistency, prudence and accrual,

will provide the correct underlying information on the basis of which financial statements of an

organization shall be prepared to show the true and fair picture of the organization. It is

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

ACCOUNTING THEORY

important to keep in mind that there are certain inherent limitations in accounting which make it

impossible to achieve absolute true and fair picture of an organization such as different methods

of depreciation, inventory valuation, estimates to make provision and others. However, despite

all these the concepts of accounting if followed properly will enable the accountants to make a

proper foundation for an organization to correctly report its financial performance and position

by preparing financial statements properly (Simkin, Norman and Rose, 2014).

ACCOUNTING THEORY

important to keep in mind that there are certain inherent limitations in accounting which make it

impossible to achieve absolute true and fair picture of an organization such as different methods

of depreciation, inventory valuation, estimates to make provision and others. However, despite

all these the concepts of accounting if followed properly will enable the accountants to make a

proper foundation for an organization to correctly report its financial performance and position

by preparing financial statements properly (Simkin, Norman and Rose, 2014).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

ACCOUNTING THEORY

References:

Atrill, P and Mclaney, E 2013. Financial Accounting for Decision Makers, 18(7), pp.21-129.

Davis, S.W., Menon, K. and Morgan, G., 1982. The images that have shaped accounting

theory. Accounting, Organizations and Society, 7(4), pp.307-318.

Deegan, C., and Unerman, J 2011. Financial accounting theory (2nd European ed.). London:

McGraw-Hill.

Dyckman, R., Thomas & A. Zeff, Stephen. (1985). Two Decades of The Journal of Accounting

Research. Journal of Accounting Research.

Hendriksen, E. (1965). Accounting Theory. Washington: Homewood Illinois.

Hines, R.D., 1988. Financial accounting: in communicating reality, we construct

reality. Accounting, organizations and society, 13(3), pp.251-261.

Lunt, H., 2006. The Fab Four’s Solo Careers: Relevance, Reliability, comparability and

understandability. 16(3), pp.2-12.

Morgan, G., 1988. Accounting as reality construction: towards a new epistemology for

accounting practice. Accounting, Organizations and Society, 13(5), pp.477-485.

Nagengast, A.J. and Stehrer, R., 2016. Accounting for the differences between gross and value

added trade balances. The World Economy, 39(9), pp.1276-1306.

Schaltegger, S. and Burritt, R., 2017. Contemporary environmental accounting: issues, concepts

and practice. Routledge.

ACCOUNTING THEORY

References:

Atrill, P and Mclaney, E 2013. Financial Accounting for Decision Makers, 18(7), pp.21-129.

Davis, S.W., Menon, K. and Morgan, G., 1982. The images that have shaped accounting

theory. Accounting, Organizations and Society, 7(4), pp.307-318.

Deegan, C., and Unerman, J 2011. Financial accounting theory (2nd European ed.). London:

McGraw-Hill.

Dyckman, R., Thomas & A. Zeff, Stephen. (1985). Two Decades of The Journal of Accounting

Research. Journal of Accounting Research.

Hendriksen, E. (1965). Accounting Theory. Washington: Homewood Illinois.

Hines, R.D., 1988. Financial accounting: in communicating reality, we construct

reality. Accounting, organizations and society, 13(3), pp.251-261.

Lunt, H., 2006. The Fab Four’s Solo Careers: Relevance, Reliability, comparability and

understandability. 16(3), pp.2-12.

Morgan, G., 1988. Accounting as reality construction: towards a new epistemology for

accounting practice. Accounting, Organizations and Society, 13(5), pp.477-485.

Nagengast, A.J. and Stehrer, R., 2016. Accounting for the differences between gross and value

added trade balances. The World Economy, 39(9), pp.1276-1306.

Schaltegger, S. and Burritt, R., 2017. Contemporary environmental accounting: issues, concepts

and practice. Routledge.

11

ACCOUNTING THEORY

Schrader, William J. "An Inductive Approach to Accounting Theory," Accounting Review, Vol.

XXXVII (October 1962), pp. 645-49.

Simkin, M.G., Norman, C.S. and Rose, J.M., 2014. Core concepts of accounting information

systems. John Wiley & Sons.

Solomons, D., 1991. Accounting and social change: a neutralist view. Accounting, Organizations

and Society, 16(3), pp.287-295.

Tinker, T., 1991. The accountant as partisan. Accounting, Organizations and Society, 16(3),

pp.297-310.

Trochim, W.M. and Donnelly, J.P. (2006) The Research Methods Knowledge Base. 3rd Edition,

Atomic Dog, Cincinnati, OH.

Walton, P., 1993. Introduction: the true and fair view in British accounting. European

Accounting Review, 2(1), pp.49-58.

Zeff, S.A., 2016. Forging accounting principles in five countries: A history and an analysis of

trends. Routledge.

ACCOUNTING THEORY

Schrader, William J. "An Inductive Approach to Accounting Theory," Accounting Review, Vol.

XXXVII (October 1962), pp. 645-49.

Simkin, M.G., Norman, C.S. and Rose, J.M., 2014. Core concepts of accounting information

systems. John Wiley & Sons.

Solomons, D., 1991. Accounting and social change: a neutralist view. Accounting, Organizations

and Society, 16(3), pp.287-295.

Tinker, T., 1991. The accountant as partisan. Accounting, Organizations and Society, 16(3),

pp.297-310.

Trochim, W.M. and Donnelly, J.P. (2006) The Research Methods Knowledge Base. 3rd Edition,

Atomic Dog, Cincinnati, OH.

Walton, P., 1993. Introduction: the true and fair view in British accounting. European

Accounting Review, 2(1), pp.49-58.

Zeff, S.A., 2016. Forging accounting principles in five countries: A history and an analysis of

trends. Routledge.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.