Management Accounting Report: Analysis of Vispring Plc's Accounting

VerifiedAdded on 2021/02/20

|16

|2555

|52

Report

AI Summary

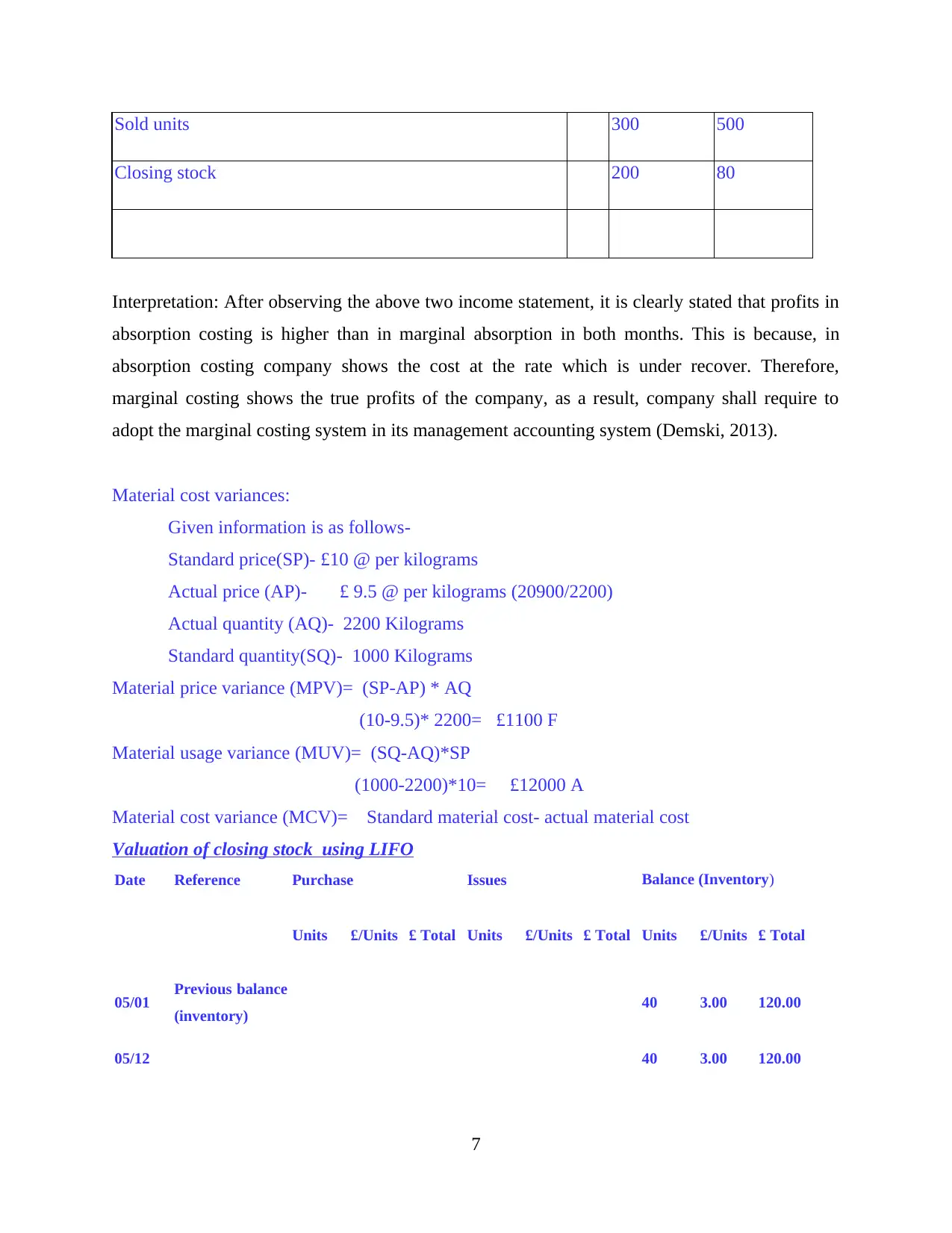

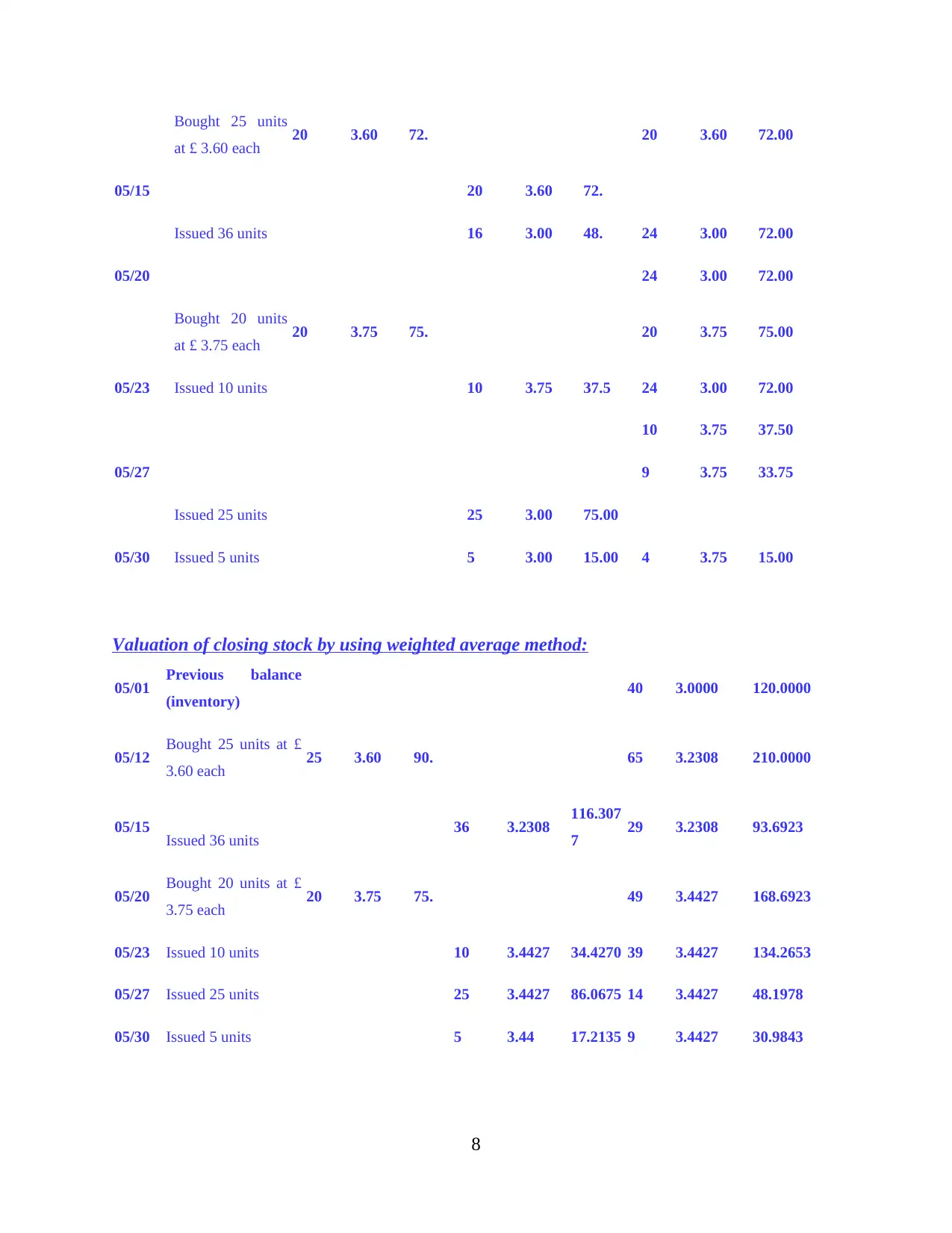

This report provides a comprehensive analysis of management accounting, focusing on the application of various systems and techniques within the context of Vispring Plc, a bed and furniture manufacturer. It explores different types of management accounting systems, including inventory management, cost accounting, job costing, and price optimization, and discusses their benefits. The report then delves into different methods of management accounting reporting, such as job cost reports and budget reports, and explains their significance. A key section compares and contrasts income statements prepared using absorption and marginal costing, highlighting their impact on profitability and the importance of choosing the appropriate method. Furthermore, it includes calculations of material cost variances and the valuation of closing stock using LIFO. The report also addresses a specific financial issue faced by the company—a lack of liquidity—and suggests the adoption of an inventory management system to mitigate this problem. Finally, it provides a conclusion summarizing the key findings and recommendations for effective management accounting practices.

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.