HA2032 Corporate & Financial Accounting: Reporting Regulations 2018

VerifiedAdded on 2023/06/04

|17

|3209

|495

Report

AI Summary

This report examines the crucial role of corporate regulations and accounting standards in enhancing financial reporting disclosures. It delves into the Australian context, highlighting the Corporations Act 2001 and the influence of the Australian Securities and Investments Commission (ASIC). The report emphasizes the importance of regulations in mitigating accounting limitations, reducing manipulation, and improving comparability in financial statements. It also explores the Australian Accounting Standards Board's (AASB) contribution to setting international accounting standards. Furthermore, the report analyzes the owners' equity of four ASX-listed companies—Telstra Corporation, Queste Communications Limited, TPG Telecom Limited, and Vodafone Australia—discussing share capital, reserves, accumulated losses, and retained earnings, and comparing their debt-to-equity positions.

Running head: CORPORATE ACCOUNTING

Corporate Accounting

Name of the Student:

Name of the University:

Authors Note:

Corporate Accounting

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

CORPORATE ACCOUNTING

Executive summary:

The auspicious objectives of corporate regulations include regulation of the disclosure

requirements in financial statements of corporates as well as to regulate the financial reporting

framework of corporates operating in a country. The purpose of this document is to understand

the importance of corporate regulations and accounting standards in improving the disclosures

made in financial reports of organizations. Apart from that a brief discussion shall also be made

on owners’ equity and various elements of it.

CORPORATE ACCOUNTING

Executive summary:

The auspicious objectives of corporate regulations include regulation of the disclosure

requirements in financial statements of corporates as well as to regulate the financial reporting

framework of corporates operating in a country. The purpose of this document is to understand

the importance of corporate regulations and accounting standards in improving the disclosures

made in financial reports of organizations. Apart from that a brief discussion shall also be made

on owners’ equity and various elements of it.

2

CORPORATE ACCOUNTING

Contents

Executive summary:........................................................................................................................1

Introduction:....................................................................................................................................3

Corporate regulations:.....................................................................................................................3

Australian Accounting Standards Board’s role in setting International accounting standards:......5

Owners’ Equity:...............................................................................................................................6

Conclusion:....................................................................................................................................13

References:....................................................................................................................................14

CORPORATE ACCOUNTING

Contents

Executive summary:........................................................................................................................1

Introduction:....................................................................................................................................3

Corporate regulations:.....................................................................................................................3

Australian Accounting Standards Board’s role in setting International accounting standards:......5

Owners’ Equity:...............................................................................................................................6

Conclusion:....................................................................................................................................13

References:....................................................................................................................................14

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

CORPORATE ACCOUNTING

Introduction:

Corporate regulations have been made and issued to ensure there is proper regulation in

operations of corporations in the country. In Australia, the corporates are governed in accordance

with the provisions of Corporations Act, 2001. The corporate regulations are also enumerated in

the act. Apart from that the entities are also bound by the regulations of Australian Securities and

Investments Commission (ASIC) for certain matters. A detailed discussion on the relevance of

the corporate regulations to financial reporting process of entities operating in the country shall

be made in the document. In addition four companies listed in the Australian Securities

Exchange (ASX) shall be selected to discuss various elements of equity in these entities.

Corporate regulations:

Financial accounting and reporting is the process of maintaining proper books of

accounts of an organization & preparation and presentation of financial statements to disclose

true and fair picture of the organization. Corporations Act, 2001 provides requirements in

relation to the financial reporting and audit of such reports for entities operating in the country.

ASIC is the corporate regulatory body governing the compliance requirements for corporates

while reporting their financial information (Ioannou & Serafeim, 2017). Importance of corporate

regulations in financial reporting is immensely important. The inherent limitations of accounting

and financial reporting makes it compulsory to have mandatory corporate regulations for entities

to comply while preparing and presenting the financial statements. Brief discussion about the

importance of corporate regulations and their benefits on financial reporting would be essential

to determine the necessity of having such corporate regulations (Armstrong, Guay, Mehran &

Weber, 2015).

CORPORATE ACCOUNTING

Introduction:

Corporate regulations have been made and issued to ensure there is proper regulation in

operations of corporations in the country. In Australia, the corporates are governed in accordance

with the provisions of Corporations Act, 2001. The corporate regulations are also enumerated in

the act. Apart from that the entities are also bound by the regulations of Australian Securities and

Investments Commission (ASIC) for certain matters. A detailed discussion on the relevance of

the corporate regulations to financial reporting process of entities operating in the country shall

be made in the document. In addition four companies listed in the Australian Securities

Exchange (ASX) shall be selected to discuss various elements of equity in these entities.

Corporate regulations:

Financial accounting and reporting is the process of maintaining proper books of

accounts of an organization & preparation and presentation of financial statements to disclose

true and fair picture of the organization. Corporations Act, 2001 provides requirements in

relation to the financial reporting and audit of such reports for entities operating in the country.

ASIC is the corporate regulatory body governing the compliance requirements for corporates

while reporting their financial information (Ioannou & Serafeim, 2017). Importance of corporate

regulations in financial reporting is immensely important. The inherent limitations of accounting

and financial reporting makes it compulsory to have mandatory corporate regulations for entities

to comply while preparing and presenting the financial statements. Brief discussion about the

importance of corporate regulations and their benefits on financial reporting would be essential

to determine the necessity of having such corporate regulations (Armstrong, Guay, Mehran &

Weber, 2015).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

CORPORATE ACCOUNTING

Number of areas where accounting provides alternative accounting principles and policies:

Due to the inherent limitations of accounting there are number of areas such as accounting for

inventory, depreciation, calculation of cost of goods sold, valuation of intangible assets,

measurement of assets, etc. where accounting provides more than one alternative to the

management and accountants. Corporate regulations help in reducing the number of alternatives

to minimum to ensure that the financial statements are prepared in accordance with appropriate

accounting principles and policies (Eccles & Serafeim, 2015).

Reducing the scope manipulation by the accountants and management:

Corporate regulations restrict the scope of manipulation in the financial reporting and accounting

by the management and accountants as they have to abide by the corporate regulations in

preparing and presenting the financial statements (Bhasin, 2015).

Comparability:

Due to reduction in number of alternatives for financial reporting the financial accounting and

reporting must be in accordance with the corporate regulations. This increase the comparability

of financial information.

Disclosure of true and fair picture:

Compulsory compliance requirements with corporate regulations improves financial accounting

and reporting to disclose true and fair picture of corporates.

If the disclosure requirements in financial reporting are made voluntary and the managers are

allowed to disclose financial information as per their choice then there would be huge scope of

manipulation in accounting and financial reporting. As a result the financial statements will end

CORPORATE ACCOUNTING

Number of areas where accounting provides alternative accounting principles and policies:

Due to the inherent limitations of accounting there are number of areas such as accounting for

inventory, depreciation, calculation of cost of goods sold, valuation of intangible assets,

measurement of assets, etc. where accounting provides more than one alternative to the

management and accountants. Corporate regulations help in reducing the number of alternatives

to minimum to ensure that the financial statements are prepared in accordance with appropriate

accounting principles and policies (Eccles & Serafeim, 2015).

Reducing the scope manipulation by the accountants and management:

Corporate regulations restrict the scope of manipulation in the financial reporting and accounting

by the management and accountants as they have to abide by the corporate regulations in

preparing and presenting the financial statements (Bhasin, 2015).

Comparability:

Due to reduction in number of alternatives for financial reporting the financial accounting and

reporting must be in accordance with the corporate regulations. This increase the comparability

of financial information.

Disclosure of true and fair picture:

Compulsory compliance requirements with corporate regulations improves financial accounting

and reporting to disclose true and fair picture of corporates.

If the disclosure requirements in financial reporting are made voluntary and the managers are

allowed to disclose financial information as per their choice then there would be huge scope of

manipulation in accounting and financial reporting. As a result the financial statements will end

5

CORPORATE ACCOUNTING

up becoming a tool in the hands of the management to disclose the desired picture of an

organization as per their preference instead of disclosing true and fair picture of corporates

(Bhasin, 2015). Thus, the corporate regulations must be there to regulate financial accounting

and reporting with a continuous objective to improve financial reporting. Management should

never be allowed to only disclose information voluntarily as per their choice.

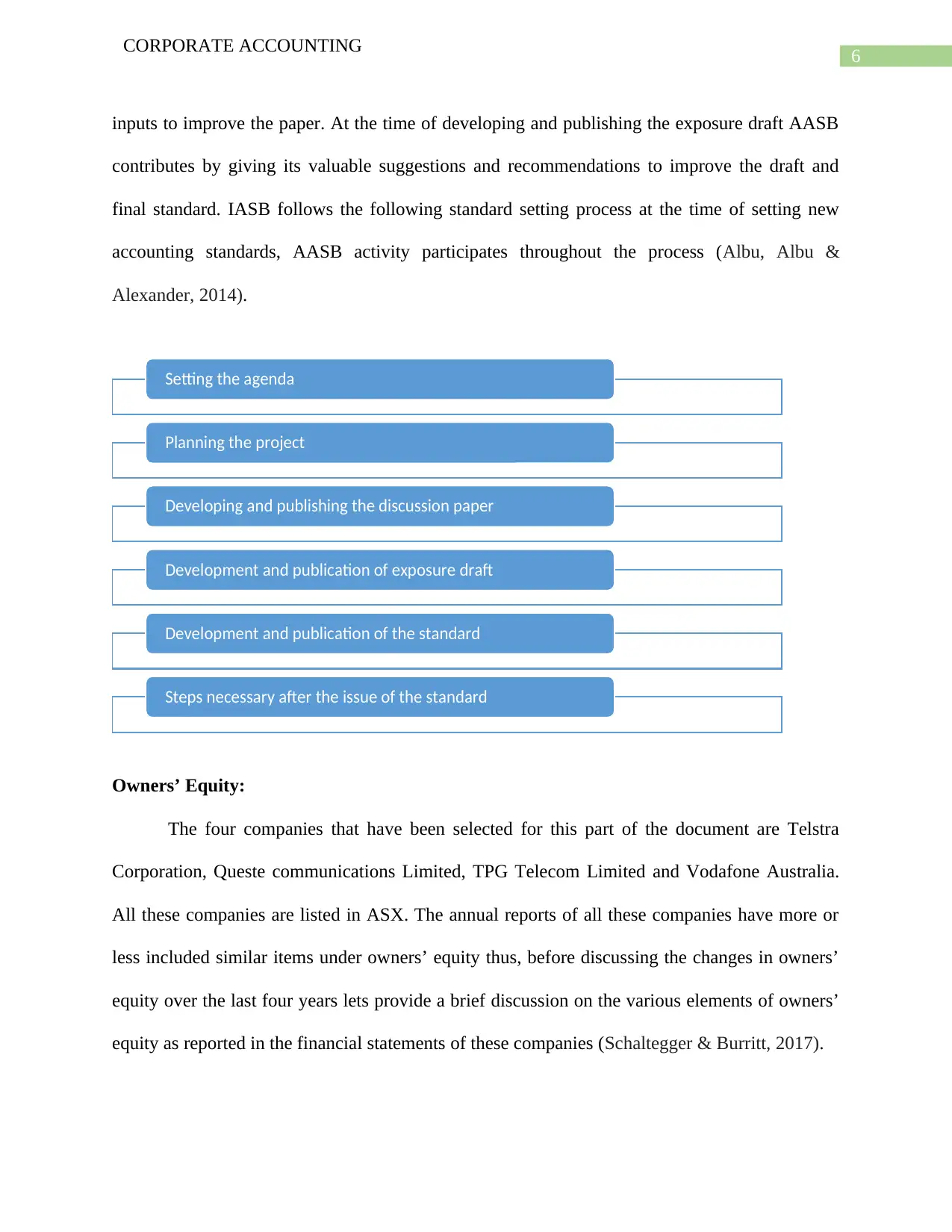

Australian Accounting Standards Board’s role in setting International accounting

standards:

Australian Accounting Standards Board (AASB) is one of the members of International

Accounting Standards Board (IASB) and plays an important role in the processing of setting

global accounting standards. At the time of drafting new standards or proposing amendments for

existing standards (IFRSs) the members of IASB including AASB is consulted. The preliminary

drafts of new standards and amendment standards are provided to the members of the Board

including AASB (Crane & Matten, 2016). The comments, suggestions, recommendations of all

the members are invited on the drafts. Based on the comments, suggestions and

recommendations necessary changes are made in the drafts. Once the final draft is ready the

same is formulated as new standard or amended standard as per the standard process of the

IASB.

AASB participates in the global accounting standards setting process by providing its

independent view on different matters while developing a new standard or IASB is in the process

of issuing amendments to the existing standard / standards. AASB is one of the premier members

of IASB and plays a pivotal role in the process of setting global accounting standards (Ntim,

Opong & Danbolt, 2015). AASB participates in all the stages of accounting standards process.

At the time of developing and publishing the discussion paper AASB provides its important

CORPORATE ACCOUNTING

up becoming a tool in the hands of the management to disclose the desired picture of an

organization as per their preference instead of disclosing true and fair picture of corporates

(Bhasin, 2015). Thus, the corporate regulations must be there to regulate financial accounting

and reporting with a continuous objective to improve financial reporting. Management should

never be allowed to only disclose information voluntarily as per their choice.

Australian Accounting Standards Board’s role in setting International accounting

standards:

Australian Accounting Standards Board (AASB) is one of the members of International

Accounting Standards Board (IASB) and plays an important role in the processing of setting

global accounting standards. At the time of drafting new standards or proposing amendments for

existing standards (IFRSs) the members of IASB including AASB is consulted. The preliminary

drafts of new standards and amendment standards are provided to the members of the Board

including AASB (Crane & Matten, 2016). The comments, suggestions, recommendations of all

the members are invited on the drafts. Based on the comments, suggestions and

recommendations necessary changes are made in the drafts. Once the final draft is ready the

same is formulated as new standard or amended standard as per the standard process of the

IASB.

AASB participates in the global accounting standards setting process by providing its

independent view on different matters while developing a new standard or IASB is in the process

of issuing amendments to the existing standard / standards. AASB is one of the premier members

of IASB and plays a pivotal role in the process of setting global accounting standards (Ntim,

Opong & Danbolt, 2015). AASB participates in all the stages of accounting standards process.

At the time of developing and publishing the discussion paper AASB provides its important

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

CORPORATE ACCOUNTING

inputs to improve the paper. At the time of developing and publishing the exposure draft AASB

contributes by giving its valuable suggestions and recommendations to improve the draft and

final standard. IASB follows the following standard setting process at the time of setting new

accounting standards, AASB activity participates throughout the process (Albu, Albu &

Alexander, 2014).

Owners’ Equity:

The four companies that have been selected for this part of the document are Telstra

Corporation, Queste communications Limited, TPG Telecom Limited and Vodafone Australia.

All these companies are listed in ASX. The annual reports of all these companies have more or

less included similar items under owners’ equity thus, before discussing the changes in owners’

equity over the last four years lets provide a brief discussion on the various elements of owners’

equity as reported in the financial statements of these companies (Schaltegger & Burritt, 2017).

Setting the agenda

Planning the project

Developing and publishing the discussion paper

Development and publication of exposure draft

Development and publication of the standard

Steps necessary after the issue of the standard

CORPORATE ACCOUNTING

inputs to improve the paper. At the time of developing and publishing the exposure draft AASB

contributes by giving its valuable suggestions and recommendations to improve the draft and

final standard. IASB follows the following standard setting process at the time of setting new

accounting standards, AASB activity participates throughout the process (Albu, Albu &

Alexander, 2014).

Owners’ Equity:

The four companies that have been selected for this part of the document are Telstra

Corporation, Queste communications Limited, TPG Telecom Limited and Vodafone Australia.

All these companies are listed in ASX. The annual reports of all these companies have more or

less included similar items under owners’ equity thus, before discussing the changes in owners’

equity over the last four years lets provide a brief discussion on the various elements of owners’

equity as reported in the financial statements of these companies (Schaltegger & Burritt, 2017).

Setting the agenda

Planning the project

Developing and publishing the discussion paper

Development and publication of exposure draft

Development and publication of the standard

Steps necessary after the issue of the standard

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

CORPORATE ACCOUNTING

Share capital: It is the face value received by these companies from issue of ordinary shares in

the market. The represent the ownership right of the shareholders in an organization.

Called up capital: Called up capital is another metaphor used for share capital.

Additional paid up capital: It is the excess amount over and above the face value of shares issued

by an organization.

Reserves: Reserves are the accumulated amount of funds provided for specific future liabilities.

No amount from such reserves should be used to pay dividend (Morris, 2017).

Accumulated losses: The amount of loss accumulated over the years is termed as accumulated

losses.

Retained earnings: It is the accumulated amount of profit over the years that have remained after

payment of dividend from profits earned by a company.

Changes in owners’ equity:

In order to assess the changes in owners’ equity over the last four years period it is imperative to

have the table showing the balances in owners’ equity and different elements of owners’ equity.

Queste Communications Limited: The following table contains the balances in owners’ equity

account over the last four years:

Queste communications Limited

Amount in $

Year 2017 2016 2015 2014

CORPORATE ACCOUNTING

Share capital: It is the face value received by these companies from issue of ordinary shares in

the market. The represent the ownership right of the shareholders in an organization.

Called up capital: Called up capital is another metaphor used for share capital.

Additional paid up capital: It is the excess amount over and above the face value of shares issued

by an organization.

Reserves: Reserves are the accumulated amount of funds provided for specific future liabilities.

No amount from such reserves should be used to pay dividend (Morris, 2017).

Accumulated losses: The amount of loss accumulated over the years is termed as accumulated

losses.

Retained earnings: It is the accumulated amount of profit over the years that have remained after

payment of dividend from profits earned by a company.

Changes in owners’ equity:

In order to assess the changes in owners’ equity over the last four years period it is imperative to

have the table showing the balances in owners’ equity and different elements of owners’ equity.

Queste Communications Limited: The following table contains the balances in owners’ equity

account over the last four years:

Queste communications Limited

Amount in $

Year 2017 2016 2015 2014

8

CORPORATE ACCOUNTING

Equity:

Issued capital 6,149,888.

00

6,149,888.

00

6,268,445.

00

6,268,445.

00

Reserves 3,182,215.

00

3,270,684.

00

3,200,408.

00

3,106,232.

00

Accumulated loss (6,281,531.0

0)

(4,769,667.0

0)

(4,057,596.0

0)

(3,313,407.0

0)

Non-controlling

interests

2,088,208.

00

3,011,476.

00

3,313,099.

00

3,520,654.

00

Total equity 5,138,780.

00

7,662,381.

00

8,724,356.

00

9,581,924.

00

One of the most important characteristics that can be identified from the above balances in

owners’ equity of the company is that each year the amount of equity has reduced. It almost

seems like a trend for the company (Camfferman & Zeff, 2015). The main reason for such

reduction in owners’ equity of the company is ever increasing accumulating losses of the

company. In 2014 the accumulated losses of the company was $3,520,654. Within a period of

three years the same has increased to $6,281,531.

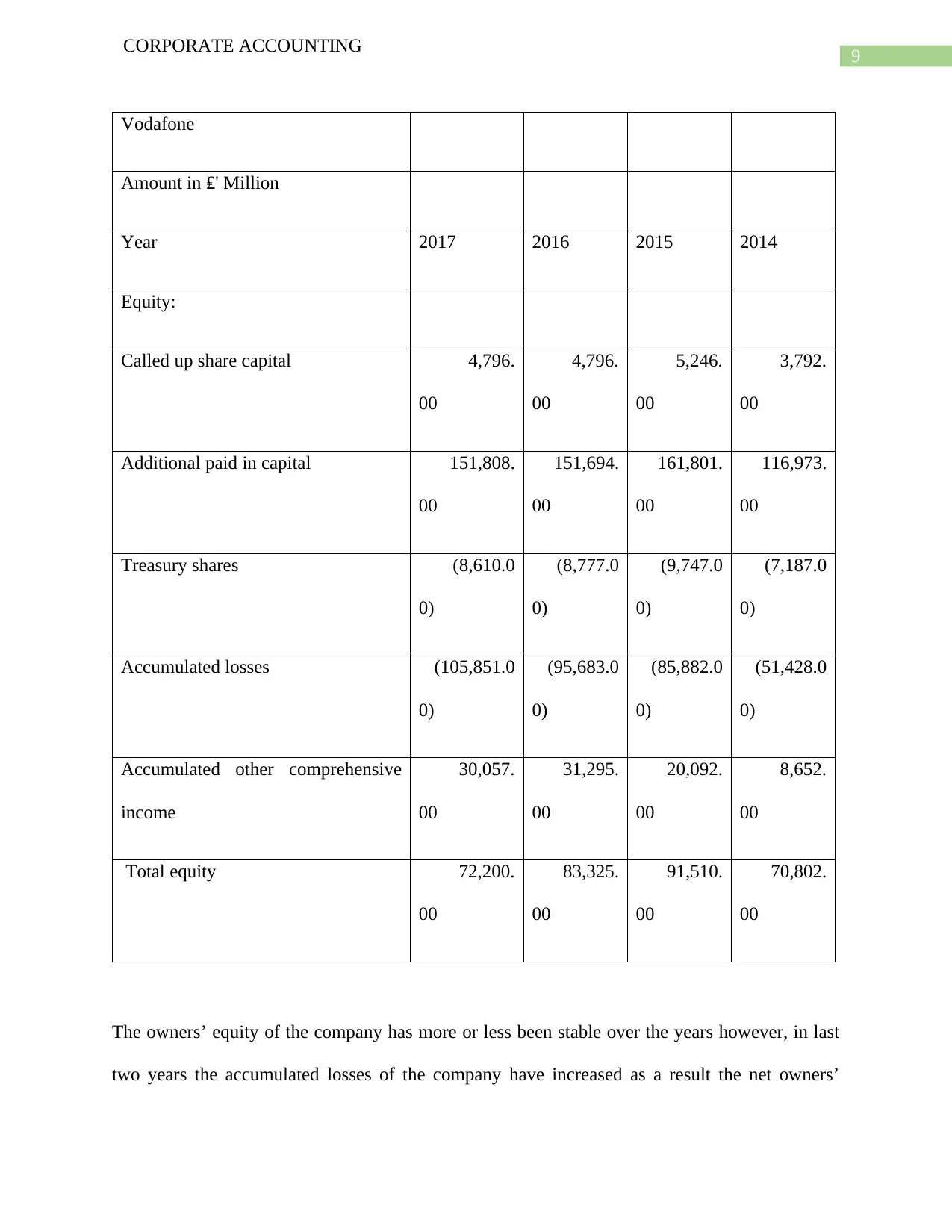

Vodafone Australia: The following figures contained in the table below represent the amount of

owners’’ equity in last 4 years ended in 2017.

CORPORATE ACCOUNTING

Equity:

Issued capital 6,149,888.

00

6,149,888.

00

6,268,445.

00

6,268,445.

00

Reserves 3,182,215.

00

3,270,684.

00

3,200,408.

00

3,106,232.

00

Accumulated loss (6,281,531.0

0)

(4,769,667.0

0)

(4,057,596.0

0)

(3,313,407.0

0)

Non-controlling

interests

2,088,208.

00

3,011,476.

00

3,313,099.

00

3,520,654.

00

Total equity 5,138,780.

00

7,662,381.

00

8,724,356.

00

9,581,924.

00

One of the most important characteristics that can be identified from the above balances in

owners’ equity of the company is that each year the amount of equity has reduced. It almost

seems like a trend for the company (Camfferman & Zeff, 2015). The main reason for such

reduction in owners’ equity of the company is ever increasing accumulating losses of the

company. In 2014 the accumulated losses of the company was $3,520,654. Within a period of

three years the same has increased to $6,281,531.

Vodafone Australia: The following figures contained in the table below represent the amount of

owners’’ equity in last 4 years ended in 2017.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

CORPORATE ACCOUNTING

Vodafone

Amount in ₤' Million

Year 2017 2016 2015 2014

Equity:

Called up share capital 4,796.

00

4,796.

00

5,246.

00

3,792.

00

Additional paid in capital 151,808.

00

151,694.

00

161,801.

00

116,973.

00

Treasury shares (8,610.0

0)

(8,777.0

0)

(9,747.0

0)

(7,187.0

0)

Accumulated losses (105,851.0

0)

(95,683.0

0)

(85,882.0

0)

(51,428.0

0)

Accumulated other comprehensive

income

30,057.

00

31,295.

00

20,092.

00

8,652.

00

Total equity 72,200.

00

83,325.

00

91,510.

00

70,802.

00

The owners’ equity of the company has more or less been stable over the years however, in last

two years the accumulated losses of the company have increased as a result the net owners’

CORPORATE ACCOUNTING

Vodafone

Amount in ₤' Million

Year 2017 2016 2015 2014

Equity:

Called up share capital 4,796.

00

4,796.

00

5,246.

00

3,792.

00

Additional paid in capital 151,808.

00

151,694.

00

161,801.

00

116,973.

00

Treasury shares (8,610.0

0)

(8,777.0

0)

(9,747.0

0)

(7,187.0

0)

Accumulated losses (105,851.0

0)

(95,683.0

0)

(85,882.0

0)

(51,428.0

0)

Accumulated other comprehensive

income

30,057.

00

31,295.

00

20,092.

00

8,652.

00

Total equity 72,200.

00

83,325.

00

91,510.

00

70,802.

00

The owners’ equity of the company has more or less been stable over the years however, in last

two years the accumulated losses of the company have increased as a result the net owners’

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

CORPORATE ACCOUNTING

equity in 2017 is GBP 72,200 million (Martínez‐Ferrero, Garcia‐Sanchez & Cuadrado‐

Ballesteros, 2015).

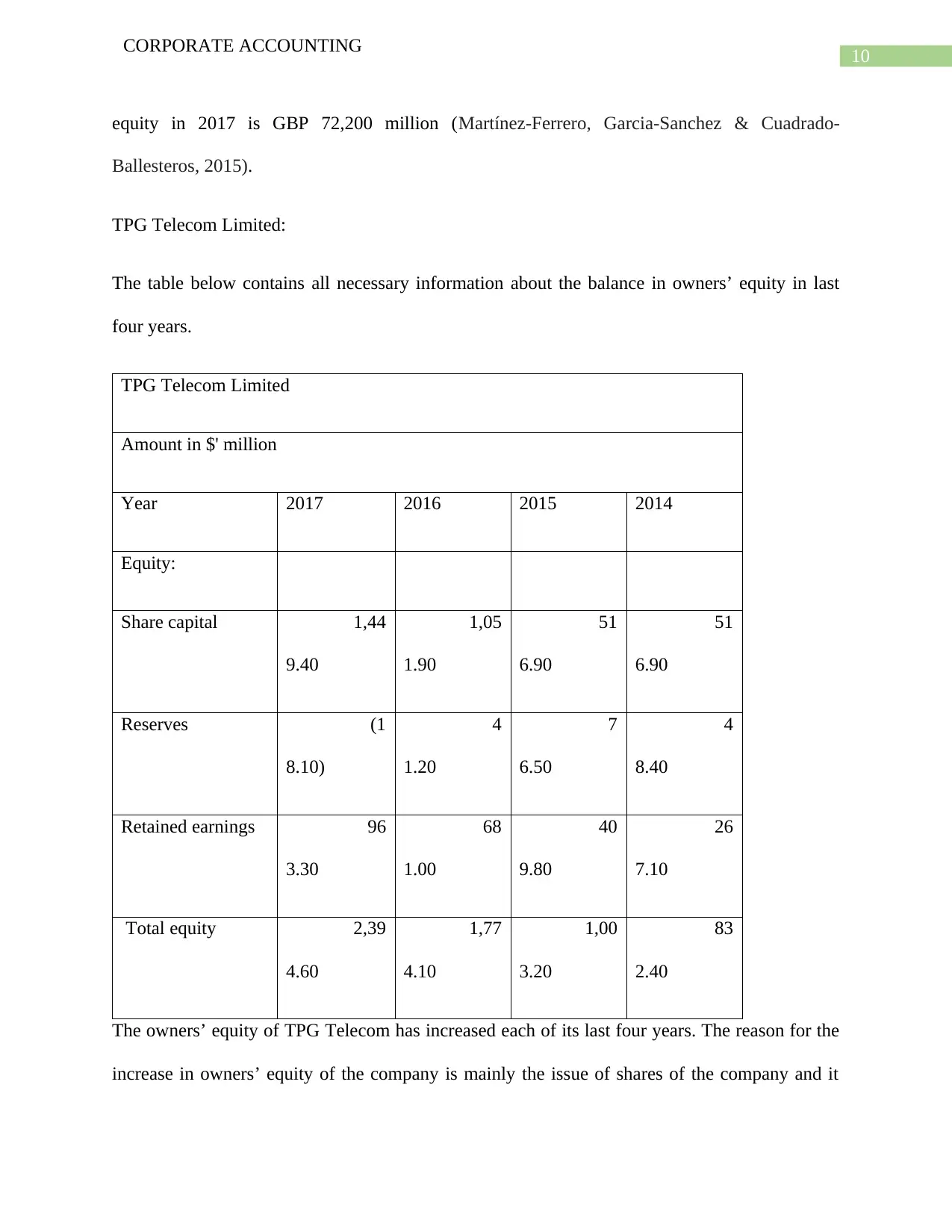

TPG Telecom Limited:

The table below contains all necessary information about the balance in owners’ equity in last

four years.

TPG Telecom Limited

Amount in $' million

Year 2017 2016 2015 2014

Equity:

Share capital 1,44

9.40

1,05

1.90

51

6.90

51

6.90

Reserves (1

8.10)

4

1.20

7

6.50

4

8.40

Retained earnings 96

3.30

68

1.00

40

9.80

26

7.10

Total equity 2,39

4.60

1,77

4.10

1,00

3.20

83

2.40

The owners’ equity of TPG Telecom has increased each of its last four years. The reason for the

increase in owners’ equity of the company is mainly the issue of shares of the company and it

CORPORATE ACCOUNTING

equity in 2017 is GBP 72,200 million (Martínez‐Ferrero, Garcia‐Sanchez & Cuadrado‐

Ballesteros, 2015).

TPG Telecom Limited:

The table below contains all necessary information about the balance in owners’ equity in last

four years.

TPG Telecom Limited

Amount in $' million

Year 2017 2016 2015 2014

Equity:

Share capital 1,44

9.40

1,05

1.90

51

6.90

51

6.90

Reserves (1

8.10)

4

1.20

7

6.50

4

8.40

Retained earnings 96

3.30

68

1.00

40

9.80

26

7.10

Total equity 2,39

4.60

1,77

4.10

1,00

3.20

83

2.40

The owners’ equity of TPG Telecom has increased each of its last four years. The reason for the

increase in owners’ equity of the company is mainly the issue of shares of the company and it

11

CORPORATE ACCOUNTING

ever increasing retained earnings. In 2017 the company has a net owners’ equity of $2,394.6

million compared to $832.40 million in 2014 (Griffin, 2015).

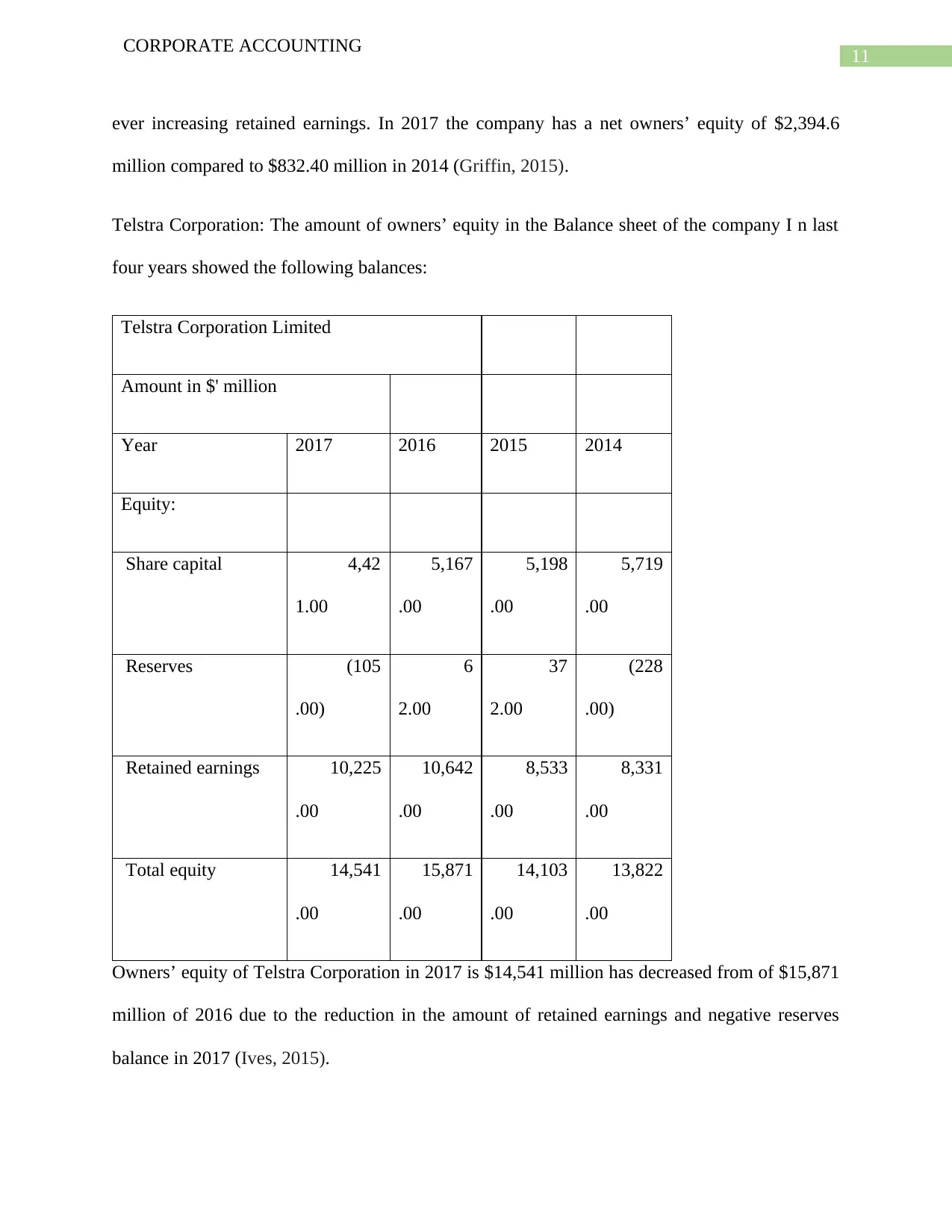

Telstra Corporation: The amount of owners’ equity in the Balance sheet of the company I n last

four years showed the following balances:

Telstra Corporation Limited

Amount in $' million

Year 2017 2016 2015 2014

Equity:

Share capital 4,42

1.00

5,167

.00

5,198

.00

5,719

.00

Reserves (105

.00)

6

2.00

37

2.00

(228

.00)

Retained earnings 10,225

.00

10,642

.00

8,533

.00

8,331

.00

Total equity 14,541

.00

15,871

.00

14,103

.00

13,822

.00

Owners’ equity of Telstra Corporation in 2017 is $14,541 million has decreased from of $15,871

million of 2016 due to the reduction in the amount of retained earnings and negative reserves

balance in 2017 (Ives, 2015).

CORPORATE ACCOUNTING

ever increasing retained earnings. In 2017 the company has a net owners’ equity of $2,394.6

million compared to $832.40 million in 2014 (Griffin, 2015).

Telstra Corporation: The amount of owners’ equity in the Balance sheet of the company I n last

four years showed the following balances:

Telstra Corporation Limited

Amount in $' million

Year 2017 2016 2015 2014

Equity:

Share capital 4,42

1.00

5,167

.00

5,198

.00

5,719

.00

Reserves (105

.00)

6

2.00

37

2.00

(228

.00)

Retained earnings 10,225

.00

10,642

.00

8,533

.00

8,331

.00

Total equity 14,541

.00

15,871

.00

14,103

.00

13,822

.00

Owners’ equity of Telstra Corporation in 2017 is $14,541 million has decreased from of $15,871

million of 2016 due to the reduction in the amount of retained earnings and negative reserves

balance in 2017 (Ives, 2015).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.