Management Accounting: Cost Analysis, Reporting, and System Adoption

VerifiedAdded on 2024/05/16

|18

|4410

|303

Report

AI Summary

This report provides a comprehensive overview of management accounting, including cost analysis techniques and reporting methods. It begins with calculating costs using marginal and absorption costing to prepare income statements. It explains management accounting and its essential requirements, detailing different reporting methods. The report then discusses the advantages and disadvantages of planning tools for budgetary control and compares how organizations should adopt management accounting systems to address financial challenges. The analysis includes income statements prepared using both absorption and marginal costing methods, highlighting the differences in profit calculation and the impact of fixed cost allocation. The report also covers price optimization, cost accounting, inventory management, and job costing systems as crucial components of management accounting, alongside the significance of inventory, performance, and budget reports for effective management decision-making.

Management accounting

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Introduction......................................................................................................................................3

Task 1...............................................................................................................................................4

Part A...............................................................................................................................................4

P3 Calculate costs using appropriate techniques of cost analysis to prepare an income

statement using marginal and absorption costs...........................................................................4

Part B...............................................................................................................................................7

P1 Explain management accounting and give the essential requirements for different types of

management accounting systems.................................................................................................7

P2 Explain different methods used for management accounting reporting.................................8

Task 2.............................................................................................................................................11

P4 Explain the advantages and disadvantages of different types of planning tools that can be

used for budgetary control.........................................................................................................11

P5 Compare how organizations such as yours should adopt management accounting systems

to respond to financial problems................................................................................................13

Conclusion.....................................................................................................................................15

Bibliography..................................................................................................................................16

2

Introduction......................................................................................................................................3

Task 1...............................................................................................................................................4

Part A...............................................................................................................................................4

P3 Calculate costs using appropriate techniques of cost analysis to prepare an income

statement using marginal and absorption costs...........................................................................4

Part B...............................................................................................................................................7

P1 Explain management accounting and give the essential requirements for different types of

management accounting systems.................................................................................................7

P2 Explain different methods used for management accounting reporting.................................8

Task 2.............................................................................................................................................11

P4 Explain the advantages and disadvantages of different types of planning tools that can be

used for budgetary control.........................................................................................................11

P5 Compare how organizations such as yours should adopt management accounting systems

to respond to financial problems................................................................................................13

Conclusion.....................................................................................................................................15

Bibliography..................................................................................................................................16

2

Introduction

Management accounting is that technique which is needed in all types of organizations as by the

help of them it will be possible to ascertain all the required information. That will be taken into

consideration by the managers and other officials on the decision making process. In this

assignment, there will be a discussion in respect of the manner in which cost is to be calculated

and all the systems which are to be taken into account so that data which is needed is acquired.

With the help of them, their company will be able to make all the reports and all of this will be

performed in the first task of this assignment. Then in later part, all the planning will be made

with the use of the tools which are present such as budgets and in this section the techniques to

be used for resolving of all the financial problems will also be taken into consideration.

3

Management accounting is that technique which is needed in all types of organizations as by the

help of them it will be possible to ascertain all the required information. That will be taken into

consideration by the managers and other officials on the decision making process. In this

assignment, there will be a discussion in respect of the manner in which cost is to be calculated

and all the systems which are to be taken into account so that data which is needed is acquired.

With the help of them, their company will be able to make all the reports and all of this will be

performed in the first task of this assignment. Then in later part, all the planning will be made

with the use of the tools which are present such as budgets and in this section the techniques to

be used for resolving of all the financial problems will also be taken into consideration.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Task 1

Part A

P3 Calculate costs using appropriate techniques of cost analysis to prepare an income

statement using marginal and absorption costs.

Income statements are required to be prepared in order to identify the profits which are made and

for this, the methods which are present include marginal and absorption costing which is

discussed below.

Absorption costing: there is the need to use various types of cost in the production of the unit

and on this, they are classified as direct and indirect and also as the variable and fixed cost.

While the calculation of the total cost it is required that they are taken into account in a proper

manner. This is the method which is also known as the full cost method as in this all the cots

which are incurred will be included in the total cost (Aurora, 2013). There are various methods

which can be used for the allocation of the cost in an appropriate amount and one of them is

activity-based costing and in this, all the distribution is made by taking activities as the base and

in this cost pools and drivers are identified. There will also be an allocation of the fixed cost

which has been made in the particular period.

Marginal costing: There is certain cost which will be changing in direct proportion to the

change in the volume and they all are known as a variable cost which is to be taken into

consideration in the marginal costing. In this, they will be used and by that, the contribution

which has been earned is ascertained which then helps in calculation of the final amount which

has been earned by the business. Under this, the apportionment of fixed expenses is not made.

In the making of these reports there is the need for the various types of information and also the

methods are to be used so that correct amount is included in the cost sheet. The one tool which

can be used is budget in which standards of all the costs are determined. By the use of them the

best cost will be determined and then they will have to be compared with the actuals so that the

deviations which are present can be calculated and for this variance analysis will have to be used.

4

Part A

P3 Calculate costs using appropriate techniques of cost analysis to prepare an income

statement using marginal and absorption costs.

Income statements are required to be prepared in order to identify the profits which are made and

for this, the methods which are present include marginal and absorption costing which is

discussed below.

Absorption costing: there is the need to use various types of cost in the production of the unit

and on this, they are classified as direct and indirect and also as the variable and fixed cost.

While the calculation of the total cost it is required that they are taken into account in a proper

manner. This is the method which is also known as the full cost method as in this all the cots

which are incurred will be included in the total cost (Aurora, 2013). There are various methods

which can be used for the allocation of the cost in an appropriate amount and one of them is

activity-based costing and in this, all the distribution is made by taking activities as the base and

in this cost pools and drivers are identified. There will also be an allocation of the fixed cost

which has been made in the particular period.

Marginal costing: There is certain cost which will be changing in direct proportion to the

change in the volume and they all are known as a variable cost which is to be taken into

consideration in the marginal costing. In this, they will be used and by that, the contribution

which has been earned is ascertained which then helps in calculation of the final amount which

has been earned by the business. Under this, the apportionment of fixed expenses is not made.

In the making of these reports there is the need for the various types of information and also the

methods are to be used so that correct amount is included in the cost sheet. The one tool which

can be used is budget in which standards of all the costs are determined. By the use of them the

best cost will be determined and then they will have to be compared with the actuals so that the

deviations which are present can be calculated and for this variance analysis will have to be used.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

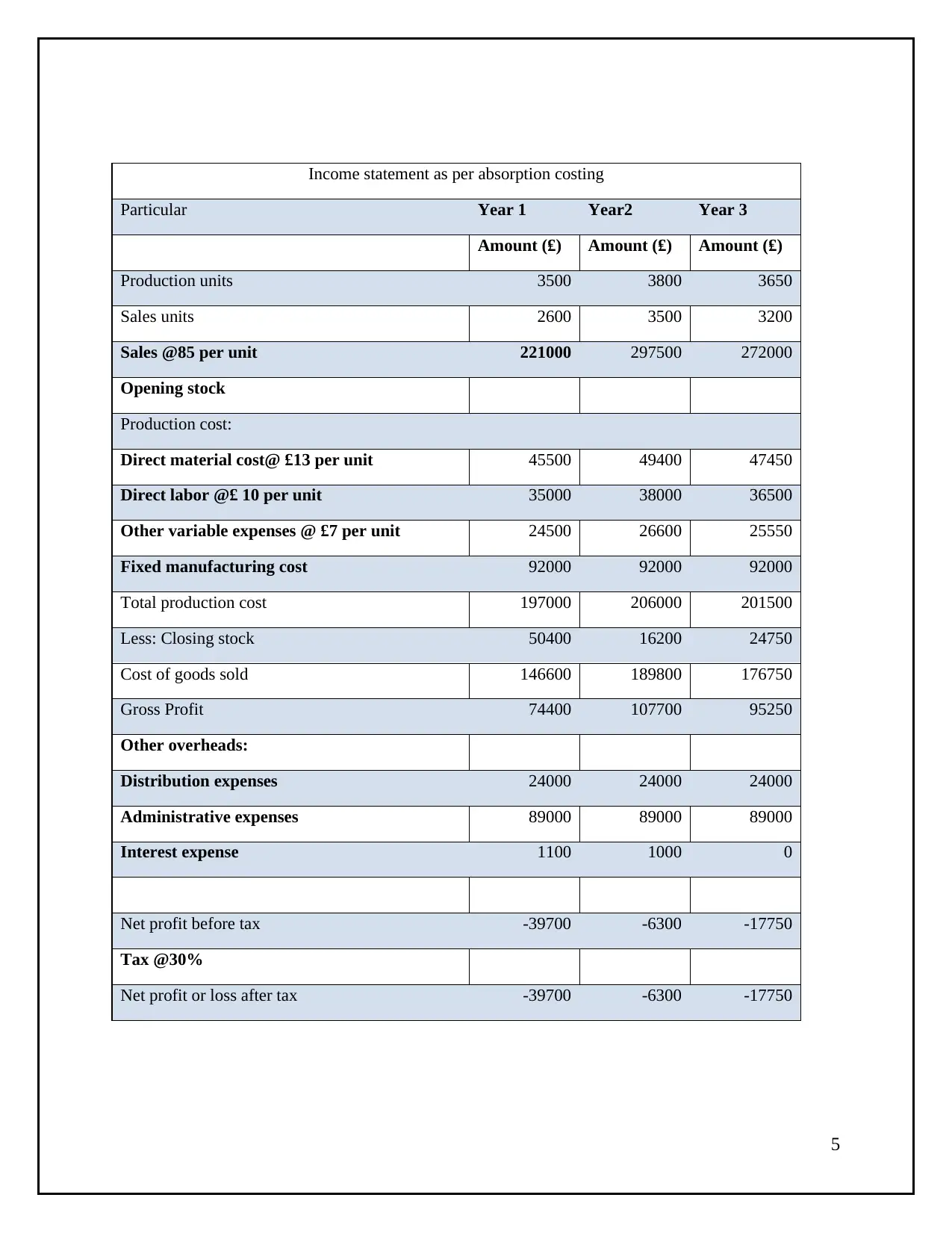

Income statement as per absorption costing

Particular Year 1 Year2 Year 3

Amount (₤) Amount (₤) Amount (₤)

Production units 3500 3800 3650

Sales units 2600 3500 3200

Sales @85 per unit 221000 297500 272000

Opening stock

Production cost:

Direct material cost@ £13 per unit 45500 49400 47450

Direct labor @£ 10 per unit 35000 38000 36500

Other variable expenses @ £7 per unit 24500 26600 25550

Fixed manufacturing cost 92000 92000 92000

Total production cost 197000 206000 201500

Less: Closing stock 50400 16200 24750

Cost of goods sold 146600 189800 176750

Gross Profit 74400 107700 95250

Other overheads:

Distribution expenses 24000 24000 24000

Administrative expenses 89000 89000 89000

Interest expense 1100 1000 0

Net profit before tax -39700 -6300 -17750

Tax @30%

Net profit or loss after tax -39700 -6300 -17750

5

Particular Year 1 Year2 Year 3

Amount (₤) Amount (₤) Amount (₤)

Production units 3500 3800 3650

Sales units 2600 3500 3200

Sales @85 per unit 221000 297500 272000

Opening stock

Production cost:

Direct material cost@ £13 per unit 45500 49400 47450

Direct labor @£ 10 per unit 35000 38000 36500

Other variable expenses @ £7 per unit 24500 26600 25550

Fixed manufacturing cost 92000 92000 92000

Total production cost 197000 206000 201500

Less: Closing stock 50400 16200 24750

Cost of goods sold 146600 189800 176750

Gross Profit 74400 107700 95250

Other overheads:

Distribution expenses 24000 24000 24000

Administrative expenses 89000 89000 89000

Interest expense 1100 1000 0

Net profit before tax -39700 -6300 -17750

Tax @30%

Net profit or loss after tax -39700 -6300 -17750

5

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

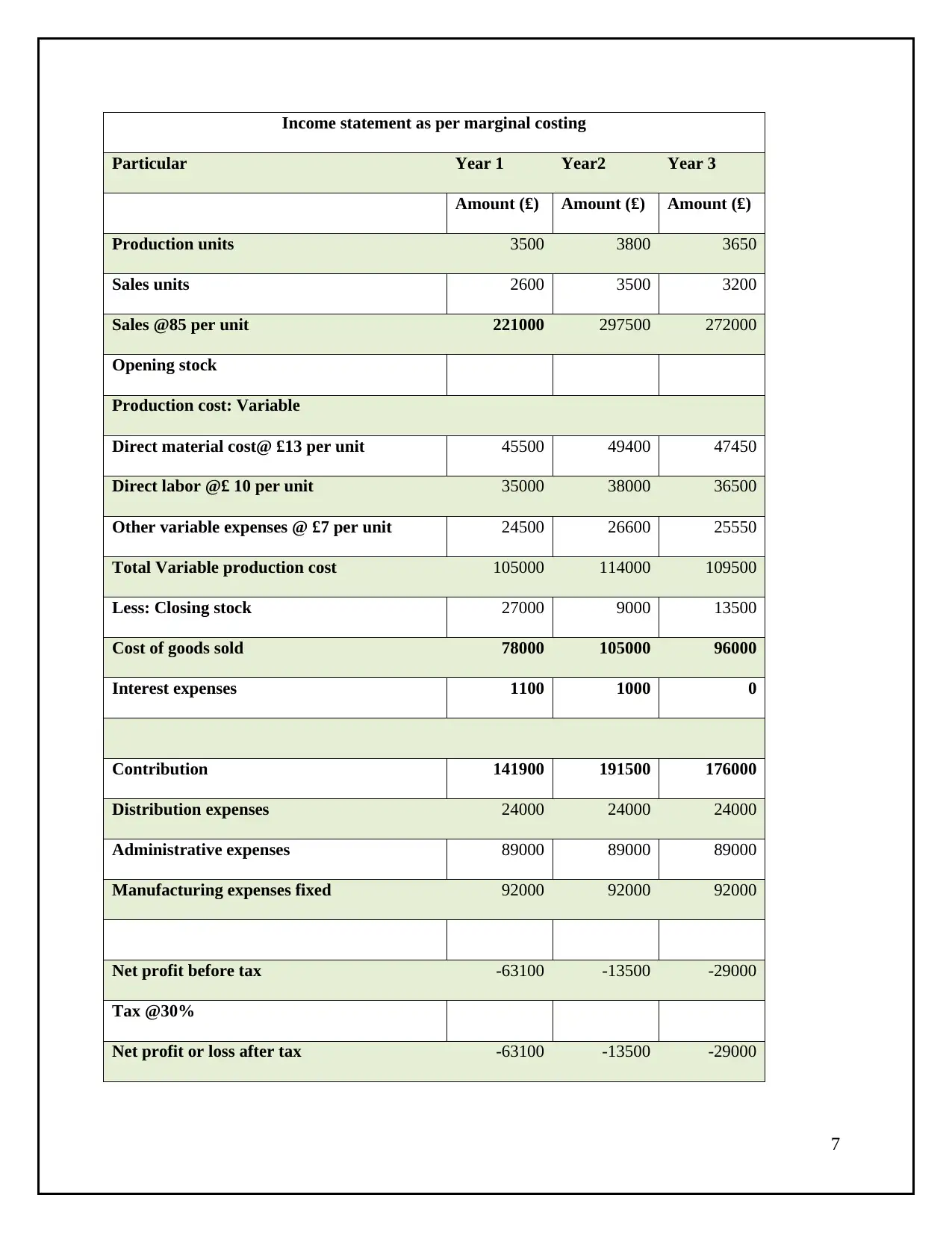

Income statement as per marginal costing

Particular Year 1 Year2 Year 3

Amount (₤) Amount (₤) Amount (₤)

Production units 3500 3800 3650

Sales units 2600 3500 3200

Sales @85 per unit 221000 297500 272000

Opening stock

Production cost: Variable

Direct material cost@ £13 per unit 45500 49400 47450

Direct labor @£ 10 per unit 35000 38000 36500

Other variable expenses @ £7 per unit 24500 26600 25550

Total Variable production cost 105000 114000 109500

Less: Closing stock 27000 9000 13500

Cost of goods sold 78000 105000 96000

Interest expenses 1100 1000 0

Contribution 141900 191500 176000

Distribution expenses 24000 24000 24000

Administrative expenses 89000 89000 89000

Manufacturing expenses fixed 92000 92000 92000

Net profit before tax -63100 -13500 -29000

Tax @30%

Net profit or loss after tax -63100 -13500 -29000

7

Particular Year 1 Year2 Year 3

Amount (₤) Amount (₤) Amount (₤)

Production units 3500 3800 3650

Sales units 2600 3500 3200

Sales @85 per unit 221000 297500 272000

Opening stock

Production cost: Variable

Direct material cost@ £13 per unit 45500 49400 47450

Direct labor @£ 10 per unit 35000 38000 36500

Other variable expenses @ £7 per unit 24500 26600 25550

Total Variable production cost 105000 114000 109500

Less: Closing stock 27000 9000 13500

Cost of goods sold 78000 105000 96000

Interest expenses 1100 1000 0

Contribution 141900 191500 176000

Distribution expenses 24000 24000 24000

Administrative expenses 89000 89000 89000

Manufacturing expenses fixed 92000 92000 92000

Net profit before tax -63100 -13500 -29000

Tax @30%

Net profit or loss after tax -63100 -13500 -29000

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

From the calculations which are made above it can be noted that the profits which are made in

both the methods are different and this is due to various reasons. The manner in which allocation

of fixed assets is made in them is different and due to this, there is deviation which is identified.

As the distribution of fixed cost is done in case of absorption so in this the amount of loss is less

in that in comparison to what is ascertained in marginal costing.

Part B

P1 Explain management accounting and give the essential requirements for different types

of management accounting systems.

In the business, there are various processes which are to be performed such as collection,

interpretation, and analyzation of the information and all of these are performed under

management accounting. By the help of this, all the managers are able to make the proper

decisions as the data which is required will be made available to them on time. All of this will be

beneficial for the business as the processes will be performed in an appropriate manner. There

are certain principles which are to be used in this and they include the principle of casualty and

analogy. Management accounting plays a very important role in the business as by the help of

this all the issues which are there can be dealt in the proper way with the use of the processes and

tools that are available (Mongiello, 2016). The management will be able to use them and perform

the operations in such way which is best in the interest of the company. Some of the most

important systems which will be included in this are as follows:

1. Price optimization system: this is the system in which information in relation to price setting

will be collected. All the entities are required to set such price by which the company will be

able to make the maximum amount of profits. There is the various method which is available in

this regard. Some of them are penetration pricing, cost-plus pricing, market-led pricing. In the

undertaking of them, there will be a requirement of a lot of information and that will be collected

under this system and this will be done in such manner by which all the information is taken into

use.

2. Cost accounting system: Under this, the company will be required to undertake such process

by which the optimum cot will be ascertained. This can be done with the help of the methods and

8

both the methods are different and this is due to various reasons. The manner in which allocation

of fixed assets is made in them is different and due to this, there is deviation which is identified.

As the distribution of fixed cost is done in case of absorption so in this the amount of loss is less

in that in comparison to what is ascertained in marginal costing.

Part B

P1 Explain management accounting and give the essential requirements for different types

of management accounting systems.

In the business, there are various processes which are to be performed such as collection,

interpretation, and analyzation of the information and all of these are performed under

management accounting. By the help of this, all the managers are able to make the proper

decisions as the data which is required will be made available to them on time. All of this will be

beneficial for the business as the processes will be performed in an appropriate manner. There

are certain principles which are to be used in this and they include the principle of casualty and

analogy. Management accounting plays a very important role in the business as by the help of

this all the issues which are there can be dealt in the proper way with the use of the processes and

tools that are available (Mongiello, 2016). The management will be able to use them and perform

the operations in such way which is best in the interest of the company. Some of the most

important systems which will be included in this are as follows:

1. Price optimization system: this is the system in which information in relation to price setting

will be collected. All the entities are required to set such price by which the company will be

able to make the maximum amount of profits. There is the various method which is available in

this regard. Some of them are penetration pricing, cost-plus pricing, market-led pricing. In the

undertaking of them, there will be a requirement of a lot of information and that will be collected

under this system and this will be done in such manner by which all the information is taken into

use.

2. Cost accounting system: Under this, the company will be required to undertake such process

by which the optimum cot will be ascertained. This can be done with the help of the methods and

8

then it will be possible for the company to know that whether overspending is done by the

company (Wiedemann , 2014). For this proper plan will be made so that this can be reduced and

then the company will be collecting the information by which this can be achieved.

3. Inventory management system: In this system, all the aspects in respect of the inventory will

be taken into account. There will be various materials which are used in the process of

production of the goods. All of them will be determined and the information about them such as

the quantity and the time at which order is required to be placed is also collected. Then they will

be used in the business so that there are no problems which are faced by the company. This is the

man component and so it is important that they shall be taken into account and this will be

possible with the help of this. The manner in which the allocation is to be made of all the stock

will also be identified in this system.

4. Job costing system: In the company tee are various processes and jobs which are undertaken

and it is required that they are carried out in the best possible manner. For this, all the required

data will be collected by the company and this will then be used to perform all the actions. Under

the manner in which performance s to be made and the ones who will be responsible in this

regard will also be identified and they will be told about the task which is to be completed by

them. By this, the work will be completed in the specified and manner and there will be no

confusion which will be made in this respect.

P2 Explain different methods used for management accounting reporting.

In the company there is a lot of the data which is collected by the use of the systems and that will

be recorded when it is not possible to use it in the perfect manner. For this various reports are

required to be prepared. There are several types which are involved in this and it is essential to

follow this as of this is not done then the chances are there that data may be modified and

misused. Some of the reports which will be made are as follows:

Inventory report: In this report, all the data which is related to inventory and has been collected

in the above procedure will be recorded so that it can be used in the coming period. The

managers are required to use that in their processes so that they can deal with all the issues in

such manner by which no harm will be made to it (Zaleha Abdul Rasid et al., 2014). The

9

company (Wiedemann , 2014). For this proper plan will be made so that this can be reduced and

then the company will be collecting the information by which this can be achieved.

3. Inventory management system: In this system, all the aspects in respect of the inventory will

be taken into account. There will be various materials which are used in the process of

production of the goods. All of them will be determined and the information about them such as

the quantity and the time at which order is required to be placed is also collected. Then they will

be used in the business so that there are no problems which are faced by the company. This is the

man component and so it is important that they shall be taken into account and this will be

possible with the help of this. The manner in which the allocation is to be made of all the stock

will also be identified in this system.

4. Job costing system: In the company tee are various processes and jobs which are undertaken

and it is required that they are carried out in the best possible manner. For this, all the required

data will be collected by the company and this will then be used to perform all the actions. Under

the manner in which performance s to be made and the ones who will be responsible in this

regard will also be identified and they will be told about the task which is to be completed by

them. By this, the work will be completed in the specified and manner and there will be no

confusion which will be made in this respect.

P2 Explain different methods used for management accounting reporting.

In the company there is a lot of the data which is collected by the use of the systems and that will

be recorded when it is not possible to use it in the perfect manner. For this various reports are

required to be prepared. There are several types which are involved in this and it is essential to

follow this as of this is not done then the chances are there that data may be modified and

misused. Some of the reports which will be made are as follows:

Inventory report: In this report, all the data which is related to inventory and has been collected

in the above procedure will be recorded so that it can be used in the coming period. The

managers are required to use that in their processes so that they can deal with all the issues in

such manner by which no harm will be made to it (Zaleha Abdul Rasid et al., 2014). The

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

shortage or bulk stock problems which are faced will be eliminated and company will be able to

save the cost which is incurred due to this and also the goodwill is made of they are working in a

proper manner.

Performance report: Under this, all the information by the use of which performance can be

evaluated will be recorded. There are various aspects which are involved in this process and all

the actors which are to be checked for the determination of this will be mentioned in the report.

by this employees will feel motivated as they will be required to achieve the targets which are

specified otherwise they will not be able to prove themselves. For this, they will be working with

the full potential and by this company will also be obtaining benefits. The overall performance of

the company will be improved and this will lead to the attainment of the success and this the

main objective for which working is made.

Budgets: This is also a kind of report in which plans are made in respect of all the incomes and

expenses which are made in the business and this will help them in obtaining the required

targets. There are standards which are set in this and they are the marks which are to be achieved

and so the company will be required to incur all the expenses in such manner by which they can

be maintained and this will be in the interest of the company (Wang et al., 2015). By the use of

the overall reduction in cost will be made which is needed to increase the level of profits.

Job reports: in this report, all the information which is related to the jobs will be entered. The

persons who will be responsible for this will be mentioned in the report so that they know that

what is to be done by them and also the manner in which they will be required to perform all of

these tasks. The time within which it is to be completed and provided will also be mentioned in

this report. By this there will best result’s which will be obtained and also the data will be used

for future reference.

By the use of all the reports and systems, it will be possible for the company to attain the

required results. Then they will also be useful for the management as they will be able to take

such decisions which will bring the additional benefits for the business (Zinyama & Nhema,

2016). All the departments will be able to establish a proper plan with the help of this and this

will lead to carrying out of the operations in the best manner which will lead to increase in

satisfaction among all.

10

save the cost which is incurred due to this and also the goodwill is made of they are working in a

proper manner.

Performance report: Under this, all the information by the use of which performance can be

evaluated will be recorded. There are various aspects which are involved in this process and all

the actors which are to be checked for the determination of this will be mentioned in the report.

by this employees will feel motivated as they will be required to achieve the targets which are

specified otherwise they will not be able to prove themselves. For this, they will be working with

the full potential and by this company will also be obtaining benefits. The overall performance of

the company will be improved and this will lead to the attainment of the success and this the

main objective for which working is made.

Budgets: This is also a kind of report in which plans are made in respect of all the incomes and

expenses which are made in the business and this will help them in obtaining the required

targets. There are standards which are set in this and they are the marks which are to be achieved

and so the company will be required to incur all the expenses in such manner by which they can

be maintained and this will be in the interest of the company (Wang et al., 2015). By the use of

the overall reduction in cost will be made which is needed to increase the level of profits.

Job reports: in this report, all the information which is related to the jobs will be entered. The

persons who will be responsible for this will be mentioned in the report so that they know that

what is to be done by them and also the manner in which they will be required to perform all of

these tasks. The time within which it is to be completed and provided will also be mentioned in

this report. By this there will best result’s which will be obtained and also the data will be used

for future reference.

By the use of all the reports and systems, it will be possible for the company to attain the

required results. Then they will also be useful for the management as they will be able to take

such decisions which will bring the additional benefits for the business (Zinyama & Nhema,

2016). All the departments will be able to establish a proper plan with the help of this and this

will lead to carrying out of the operations in the best manner which will lead to increase in

satisfaction among all.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

All the reports and systems which are made in the business are integrated with each other and

this is because of the fact that they cannot be used in the business without each other. This is

because all the data which will be required in order to prepare the reports will be collected by the

use of the systems as they are responsible for this (Mayeli & Bakhoda, 2016). Then if the entry

will not be made then the collection process will not be used as in order to use the information it

is required that it is presented in the proper manner.

11

this is because of the fact that they cannot be used in the business without each other. This is

because all the data which will be required in order to prepare the reports will be collected by the

use of the systems as they are responsible for this (Mayeli & Bakhoda, 2016). Then if the entry

will not be made then the collection process will not be used as in order to use the information it

is required that it is presented in the proper manner.

11

Task 2

Report:

Introduction

In this report, all the components which are required in the planning will be discussed and

together with them the techniques by the use of which it will be possible for the company to

eliminate the issues which are present will be discussed.

P4 Explain the advantages and disadvantages of different types of planning tools that can

be used for budgetary control.

Budgetary control is required to be undertaken in the business so that all the operations can be

controlled in an appropriate manner and for this, it is required that proper planning shall be

undertaken. There are various tools which can be used such as budgets can be made in then it

will be required that the best costing method is used as by the help of that proper cost will be

ascertained that will have to be used in the formulation of the budget (Kovalevaa et al., 2016).

There are some of the merits and limitation which are present in relation to them and they are as

follows:

Advantages of budgetary control:

There will be the availability of the information in them which is required in order to

carry out the process in such manner by which wastage which is currently made will be

reduced.

As in this research is performed so the resources which are available will be identified

and then they will be distributed among all the sections as per their requirements by which

they will be able to improve the performance.

Risk factors which are present will be identified and then the manner in which they can

be reduced will be considered in the making if the budget.

12

Report:

Introduction

In this report, all the components which are required in the planning will be discussed and

together with them the techniques by the use of which it will be possible for the company to

eliminate the issues which are present will be discussed.

P4 Explain the advantages and disadvantages of different types of planning tools that can

be used for budgetary control.

Budgetary control is required to be undertaken in the business so that all the operations can be

controlled in an appropriate manner and for this, it is required that proper planning shall be

undertaken. There are various tools which can be used such as budgets can be made in then it

will be required that the best costing method is used as by the help of that proper cost will be

ascertained that will have to be used in the formulation of the budget (Kovalevaa et al., 2016).

There are some of the merits and limitation which are present in relation to them and they are as

follows:

Advantages of budgetary control:

There will be the availability of the information in them which is required in order to

carry out the process in such manner by which wastage which is currently made will be

reduced.

As in this research is performed so the resources which are available will be identified

and then they will be distributed among all the sections as per their requirements by which

they will be able to improve the performance.

Risk factors which are present will be identified and then the manner in which they can

be reduced will be considered in the making if the budget.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.