Detailed Explanation of Reserves, Dividends, and Accounting Practices

VerifiedAdded on 2023/04/25

|3

|1078

|144

Homework Assignment

AI Summary

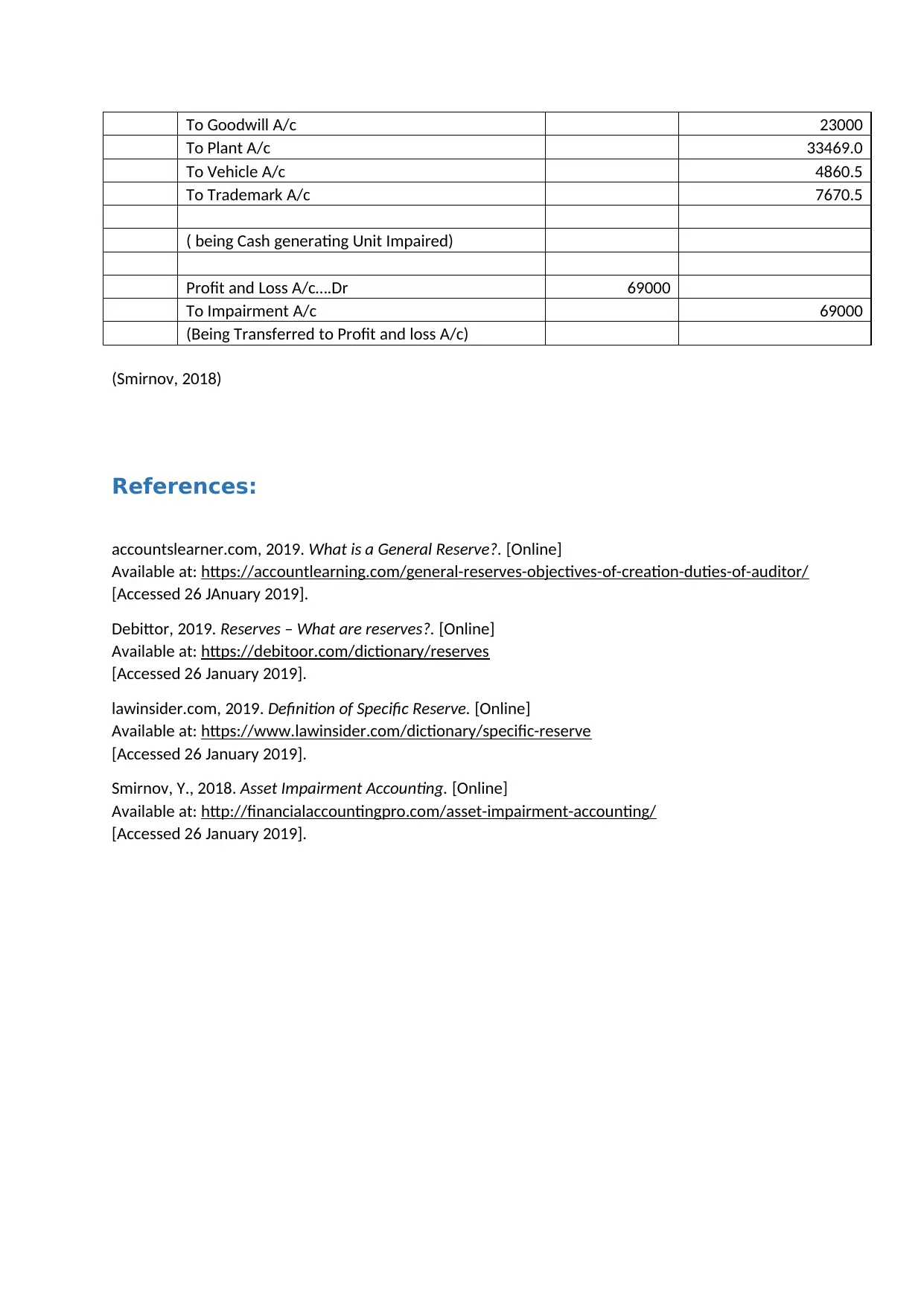

This assignment delves into the nature of reserves, defining them as funds set aside for specific purposes or future needs, and accounting for their movements within a company's financial records. It differentiates between general and specific reserves, providing examples such as general revenue reserves, investment fluctuation reserves, and debt redemption reserves. The document explains how reserves are created and utilized through journal entries, demonstrating the debiting of retained earnings and crediting of reserve accounts. It also addresses the impact of dividends, both cash and stock, on reserves, highlighting how cash dividends reduce liquid assets and retained earnings, while stock dividends transfer surplus to company stock without impacting cash flow. The assignment further discusses impairment, illustrating relevant journal entries, and concludes with a list of references used for the explanation.

1 out of 3

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.