Financial Accounting 1: Detailed Analysis of Accounting Scenarios

VerifiedAdded on 2022/11/28

|26

|4819

|497

Homework Assignment

AI Summary

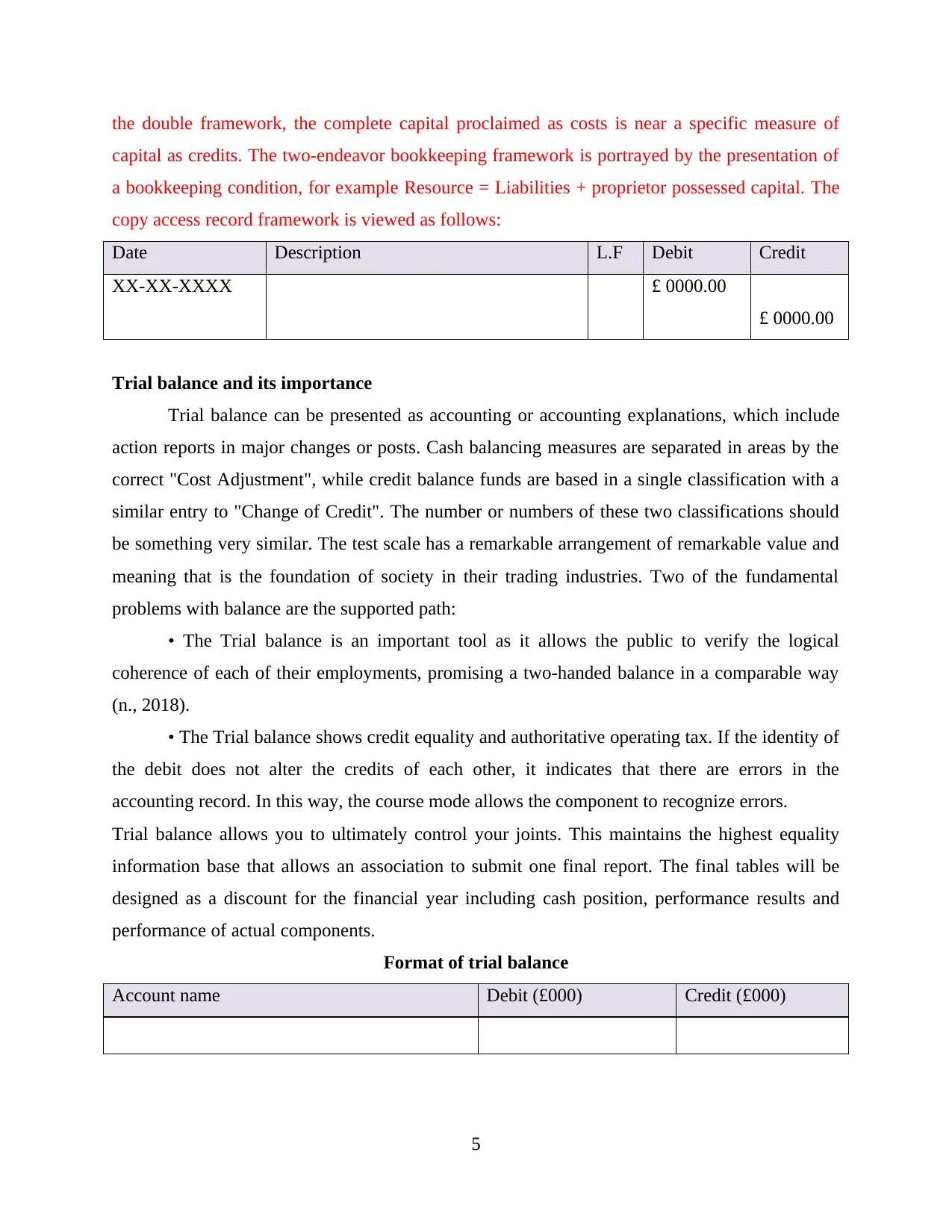

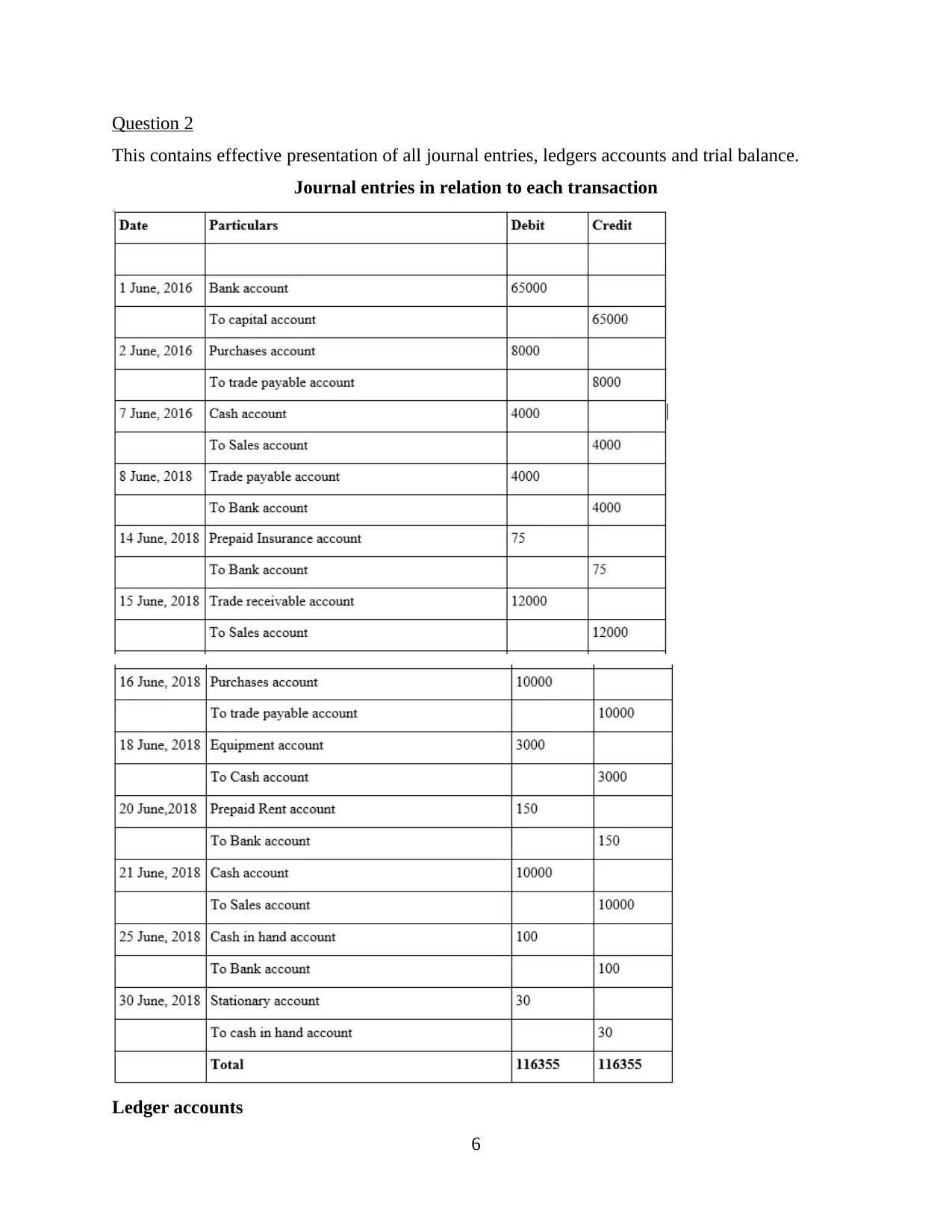

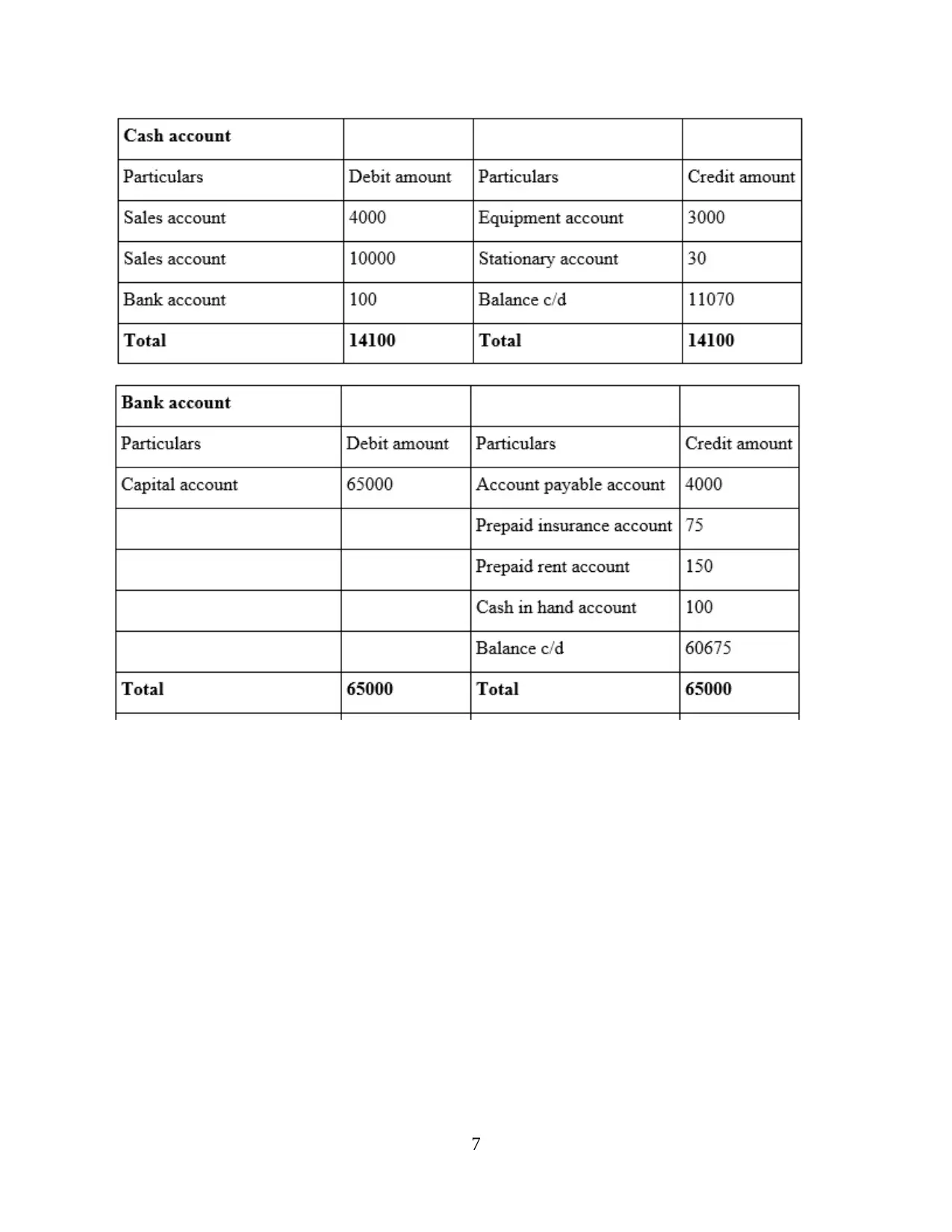

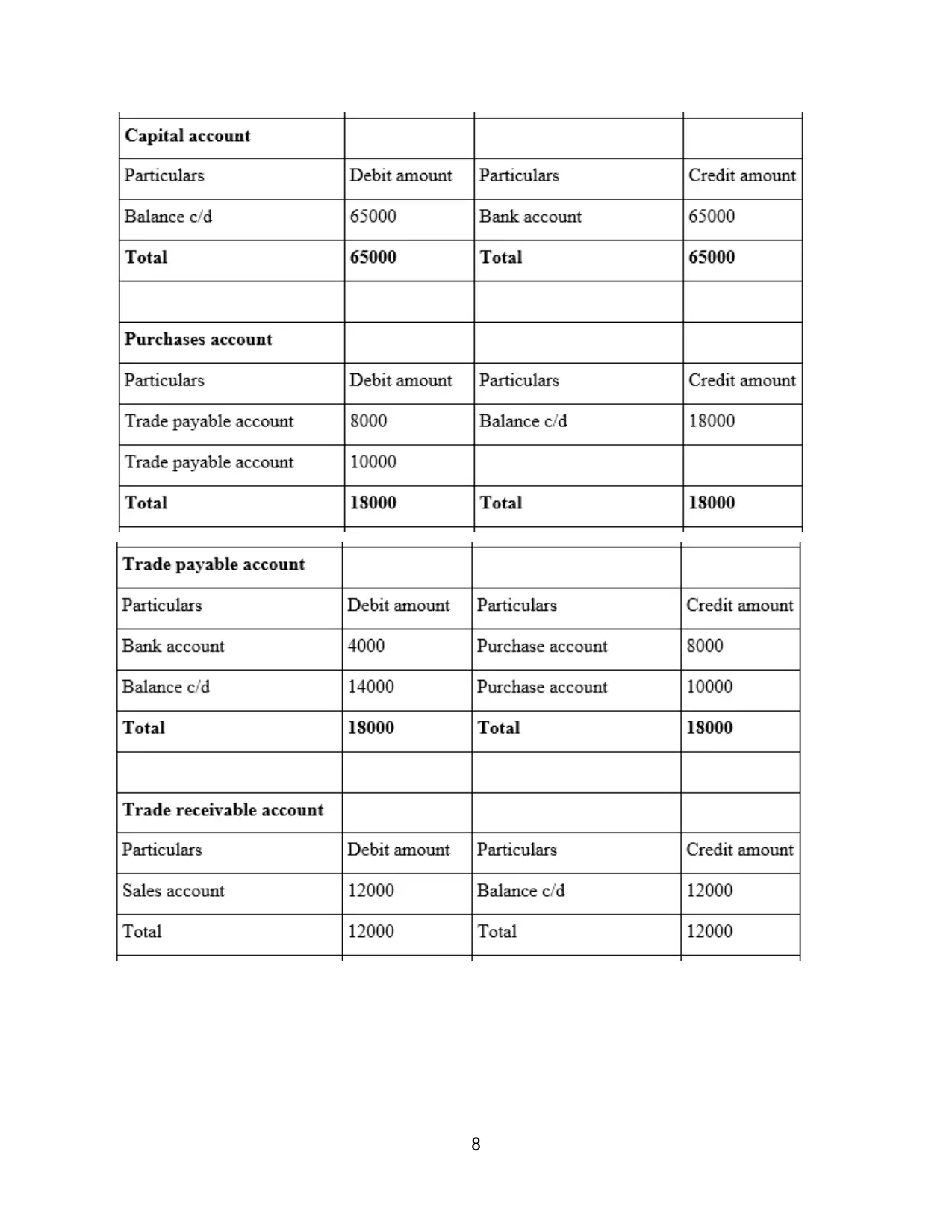

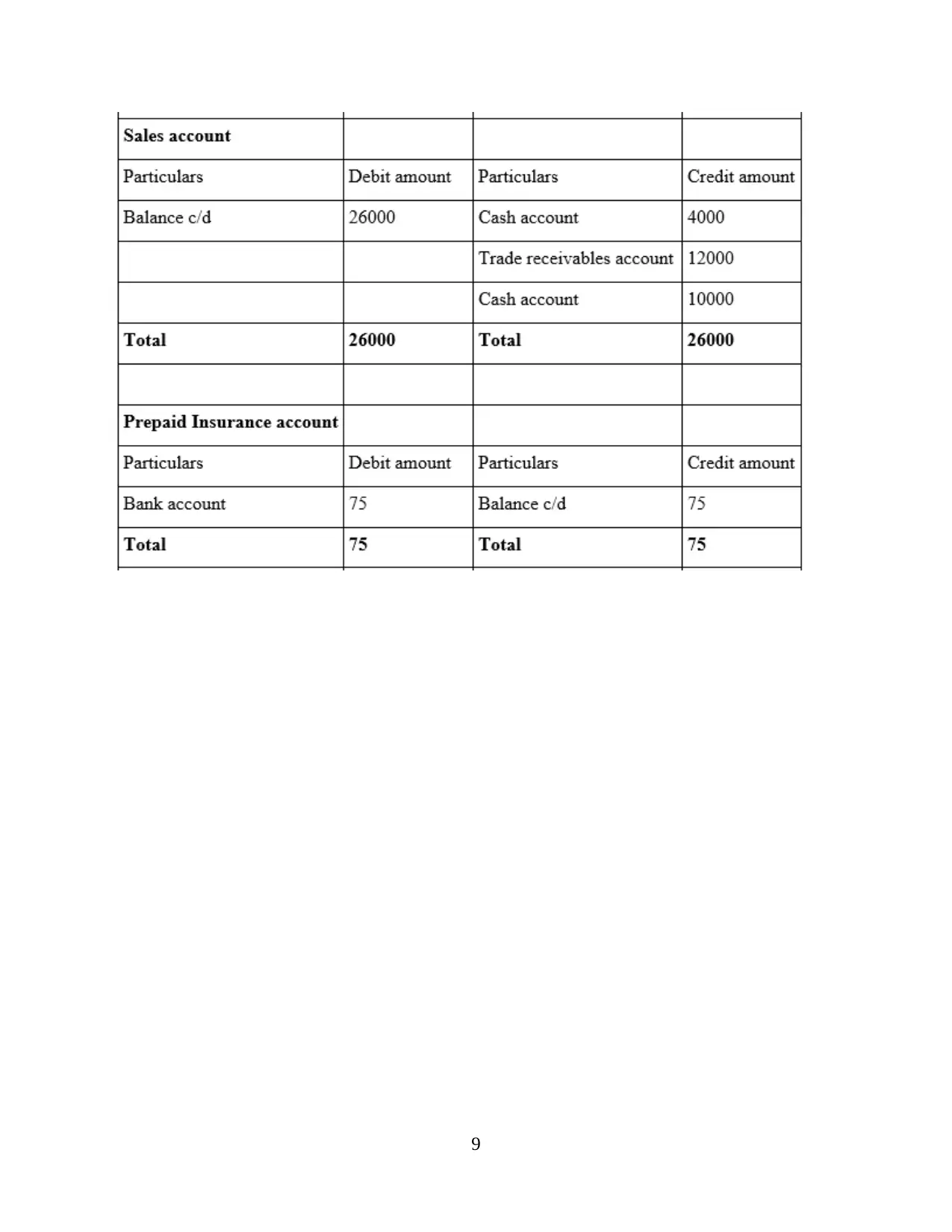

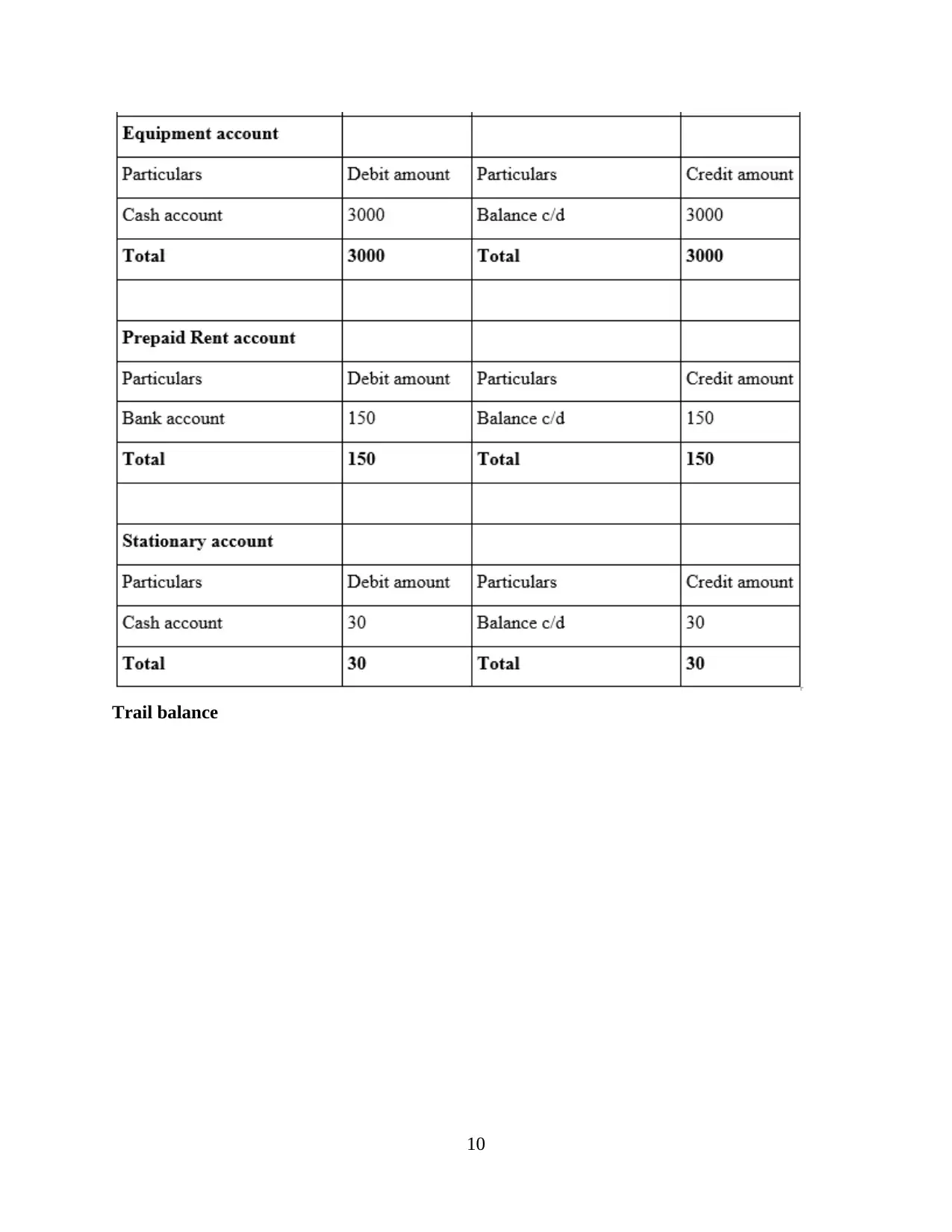

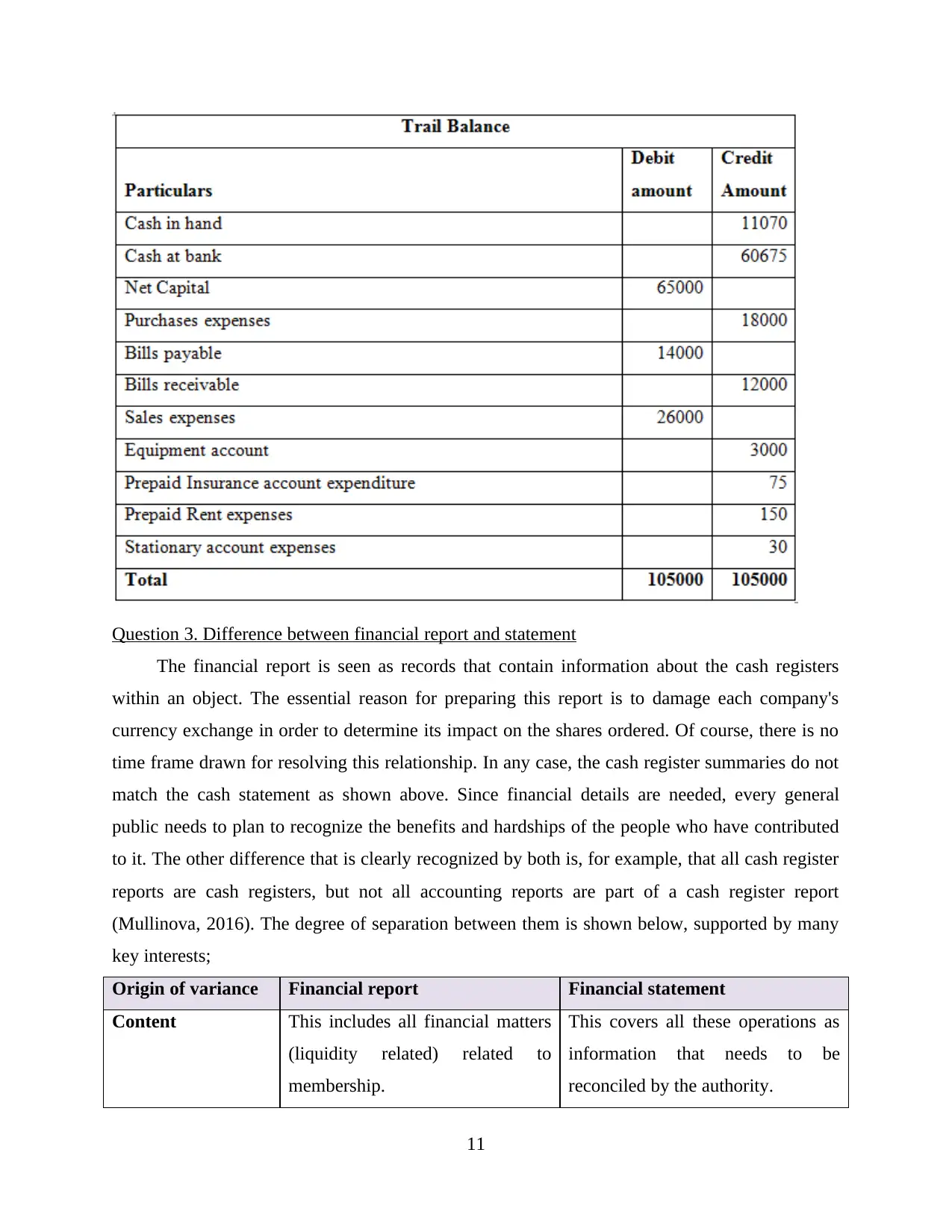

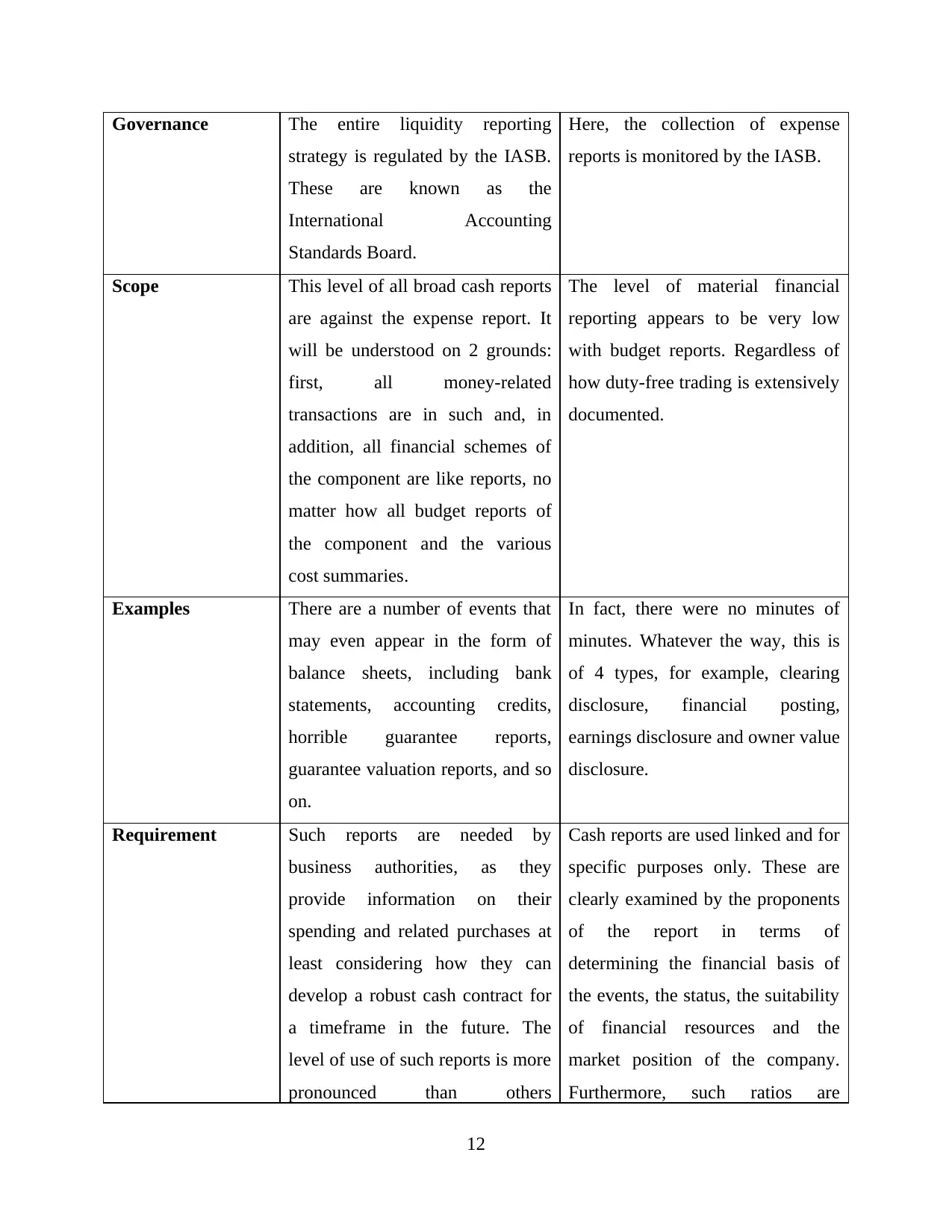

This assignment provides a detailed analysis of financial accounting concepts through two distinct scenarios. The content covers the definition and types of business transactions, including currency exchange, credit exchange, internal and external exchanges, and the difference between single-entry and double-entry bookkeeping systems. It explores journal entries, ledger accounts, and the trial balance, highlighting its importance in verifying the logical coherence of accounting records. The assignment also distinguishes between financial reports and financial statements, detailing their differences in content, governance, scope, and users. Furthermore, it describes the fundamental principles of accounting, such as the traditionalism standard, traditional management, consistency standard, cost management, and management of financial materials. Scenario 2 delves into bank reconciliation and control accounts, providing a comprehensive understanding of these crucial accounting processes. The document includes journal entries, ledger accounts, trial balance and financial statements to offer a complete view of the accounting cycle.

1 out of 26

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.