Accounting Solutions

VerifiedAdded on 2019/11/25

|18

|1570

|493

Homework Assignment

AI Summary

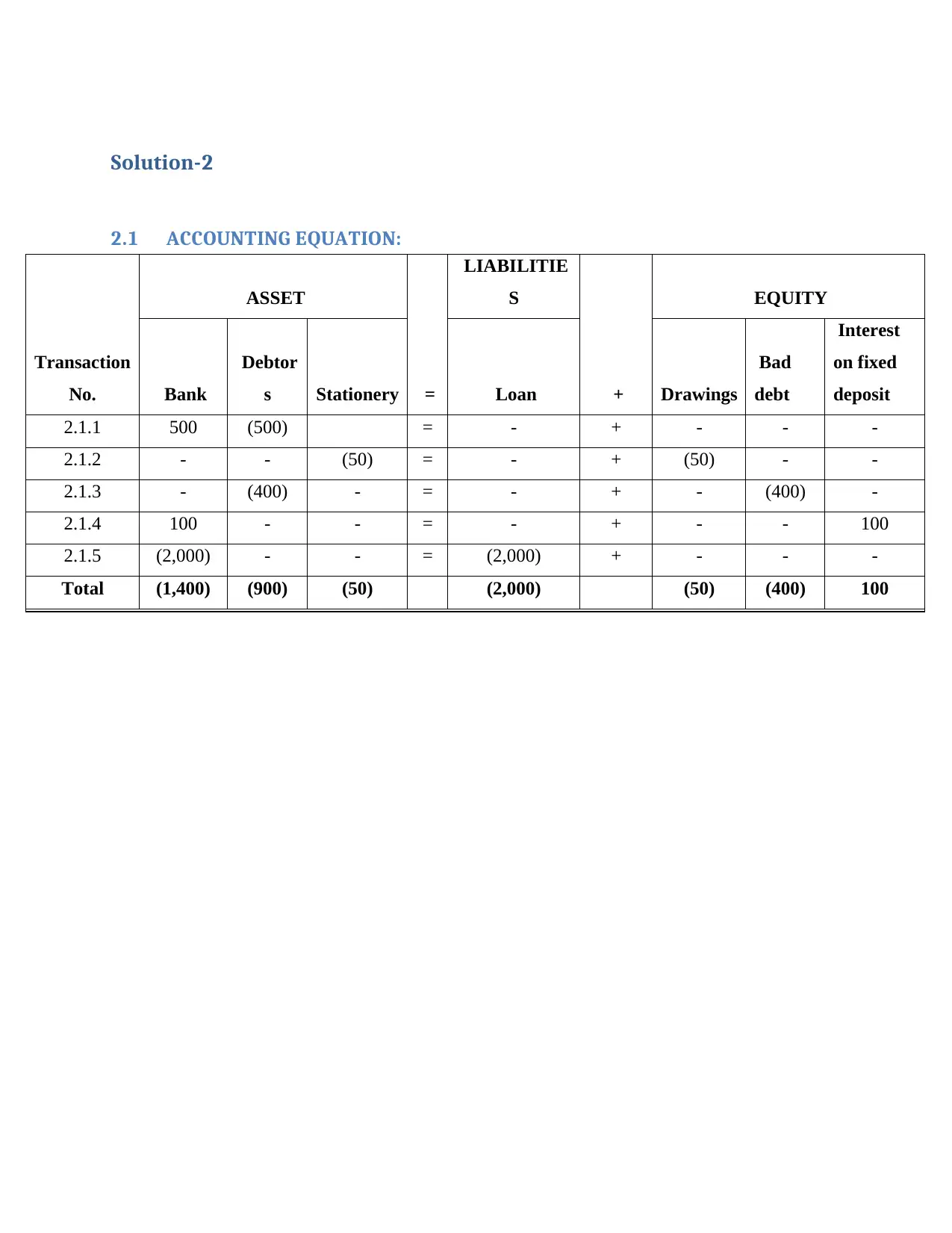

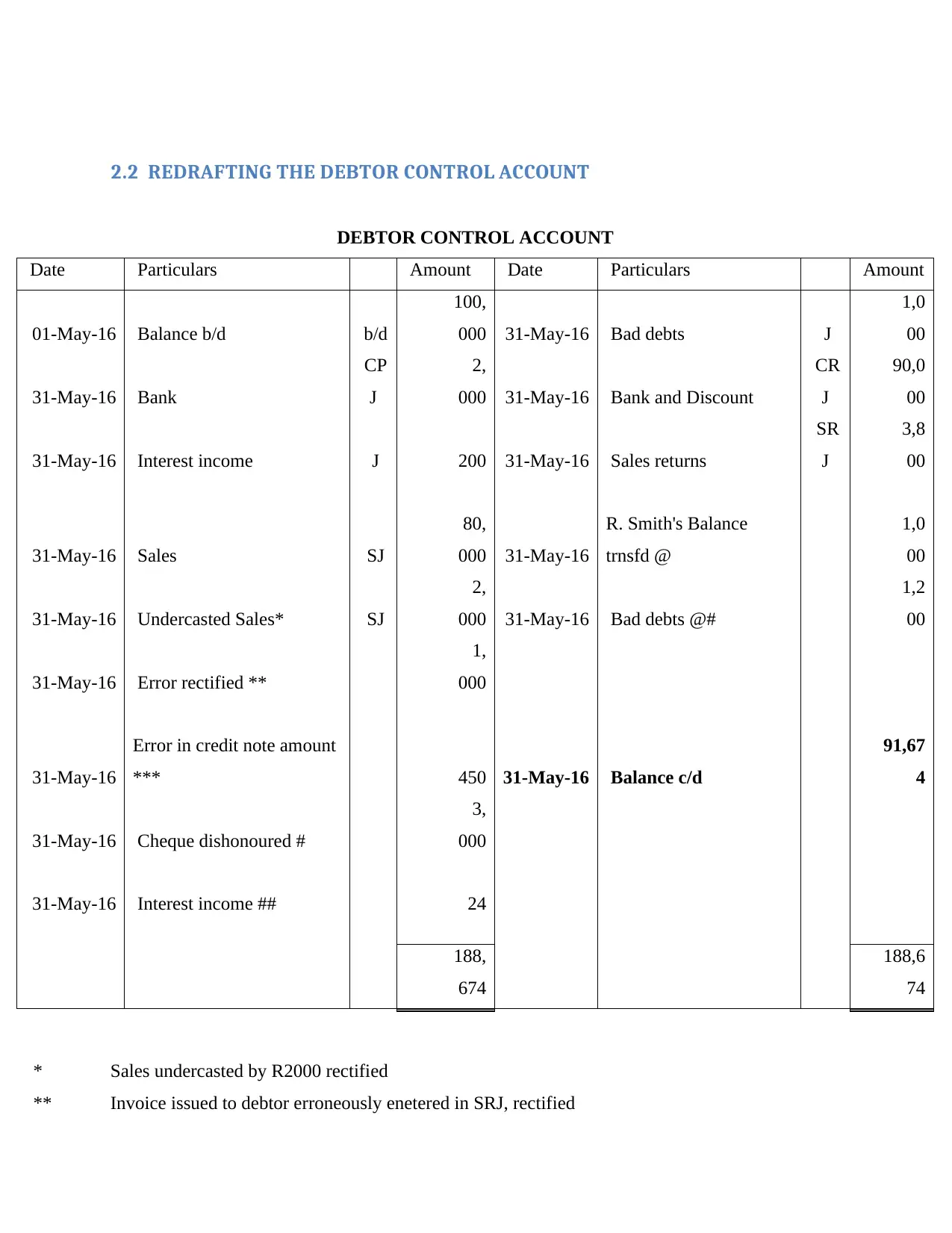

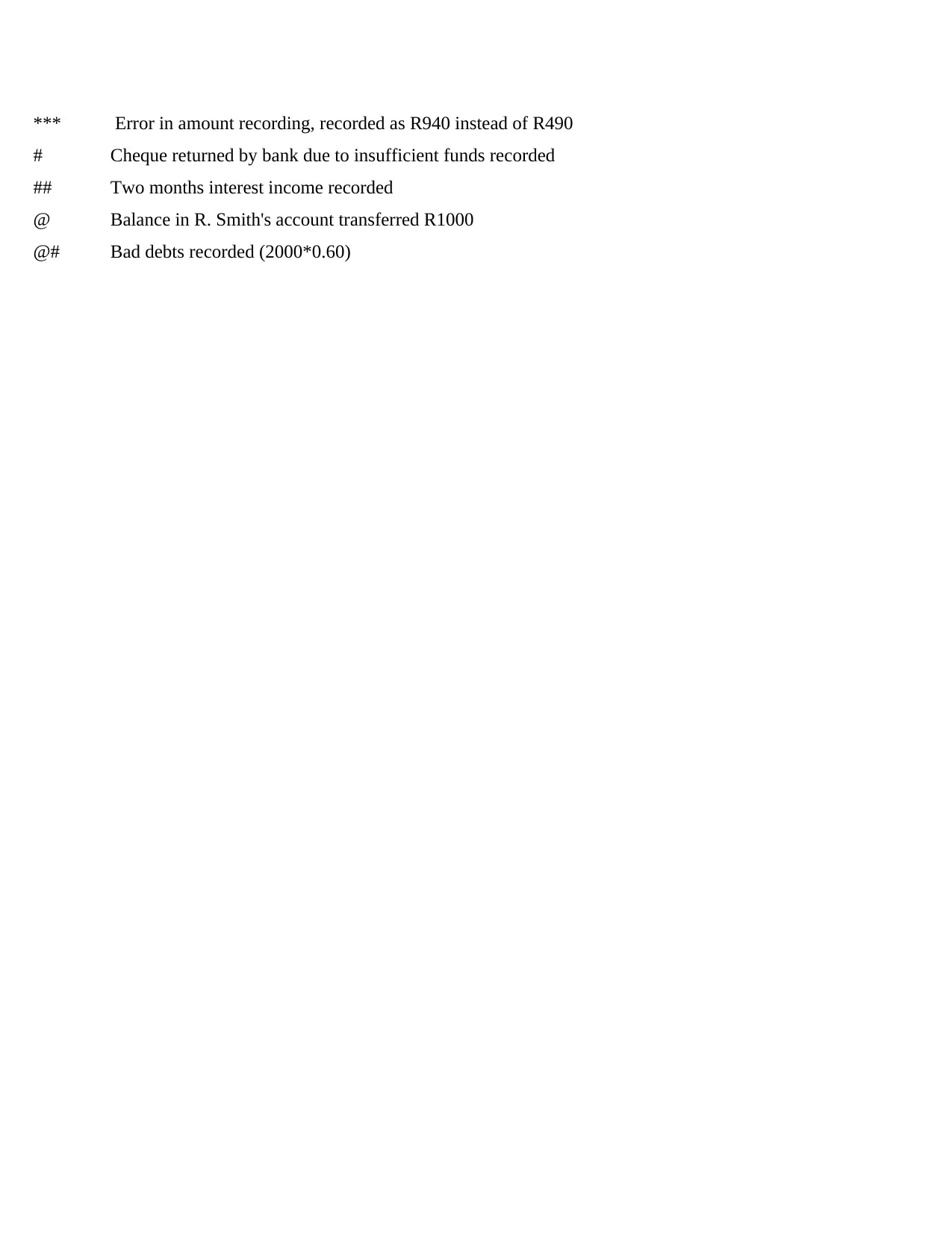

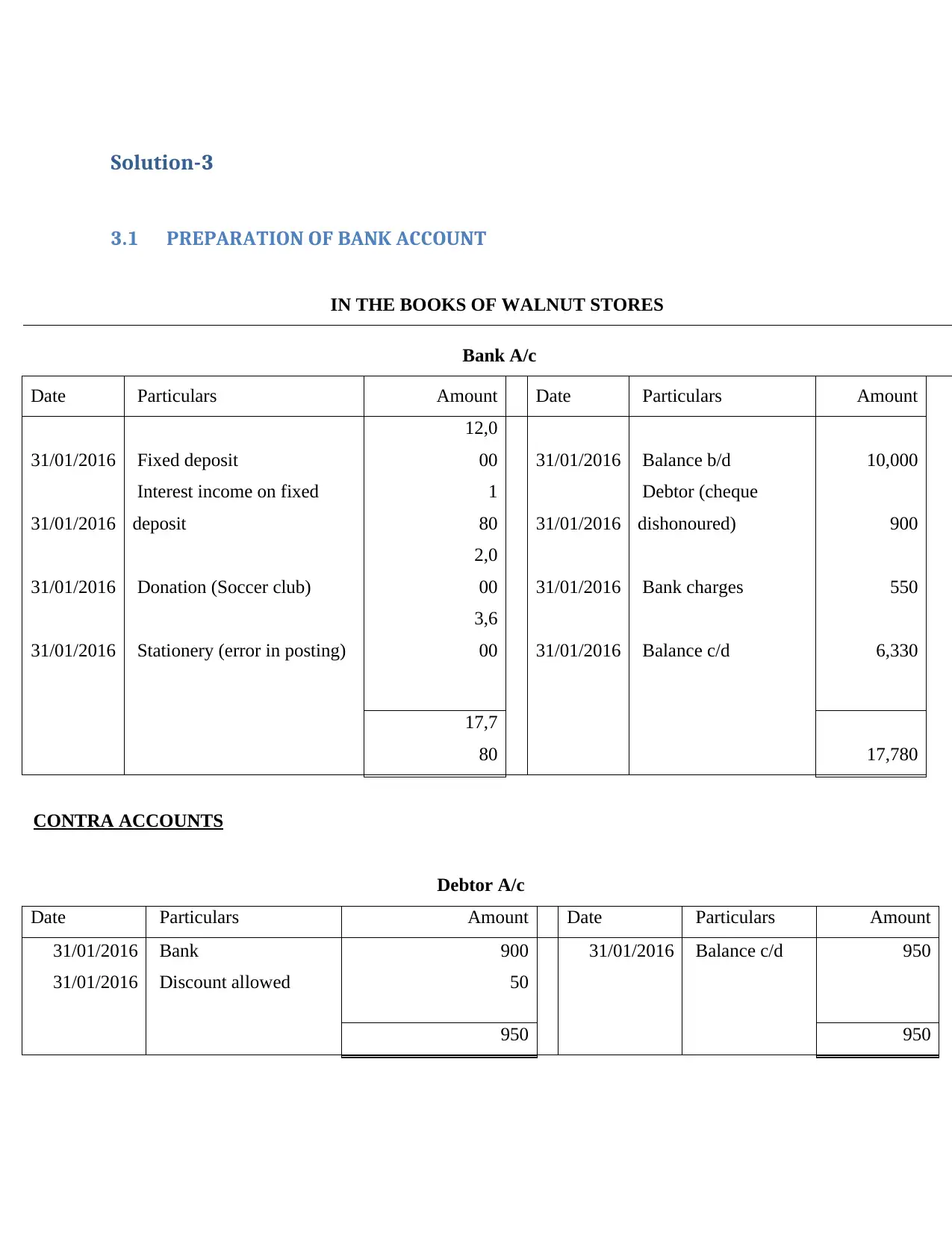

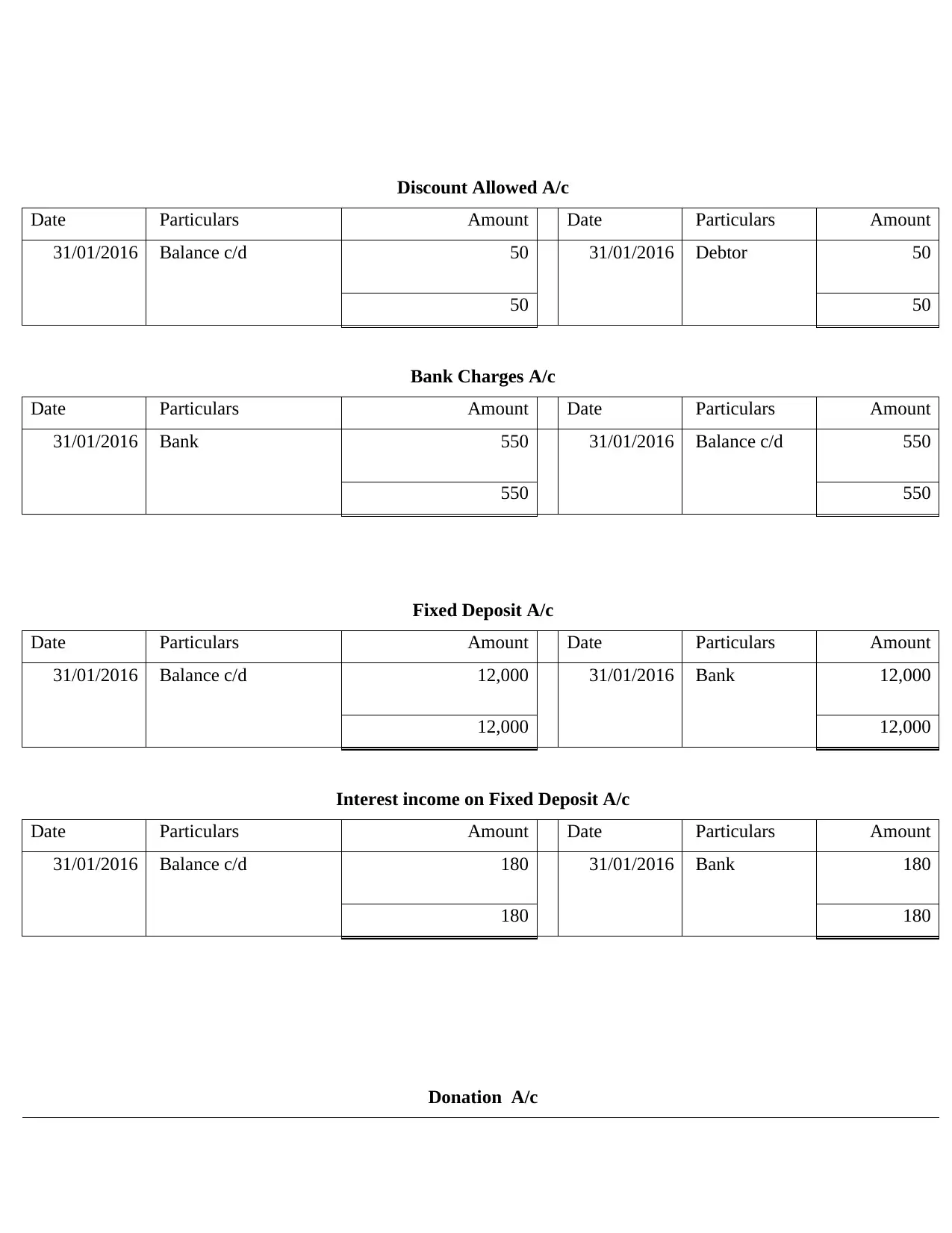

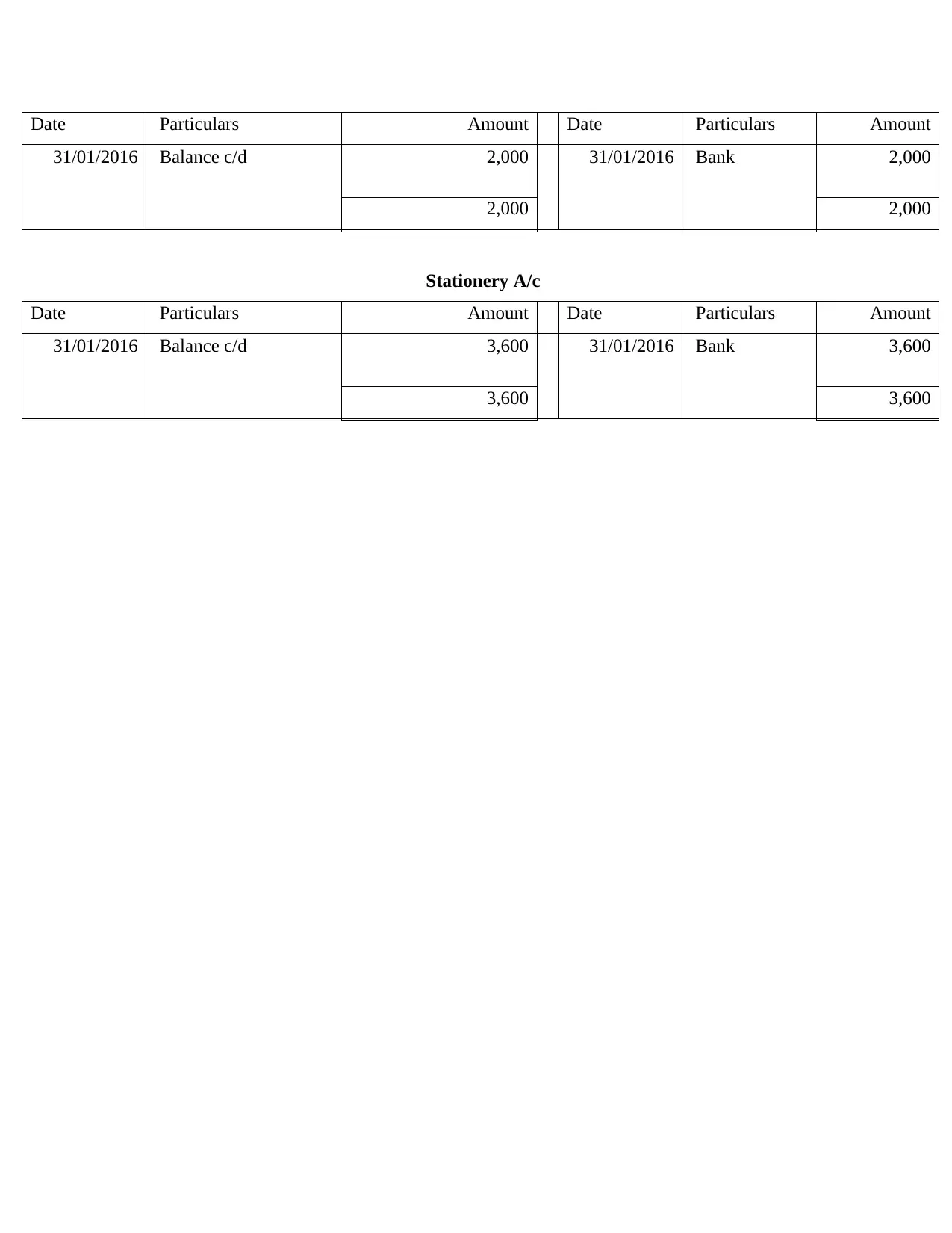

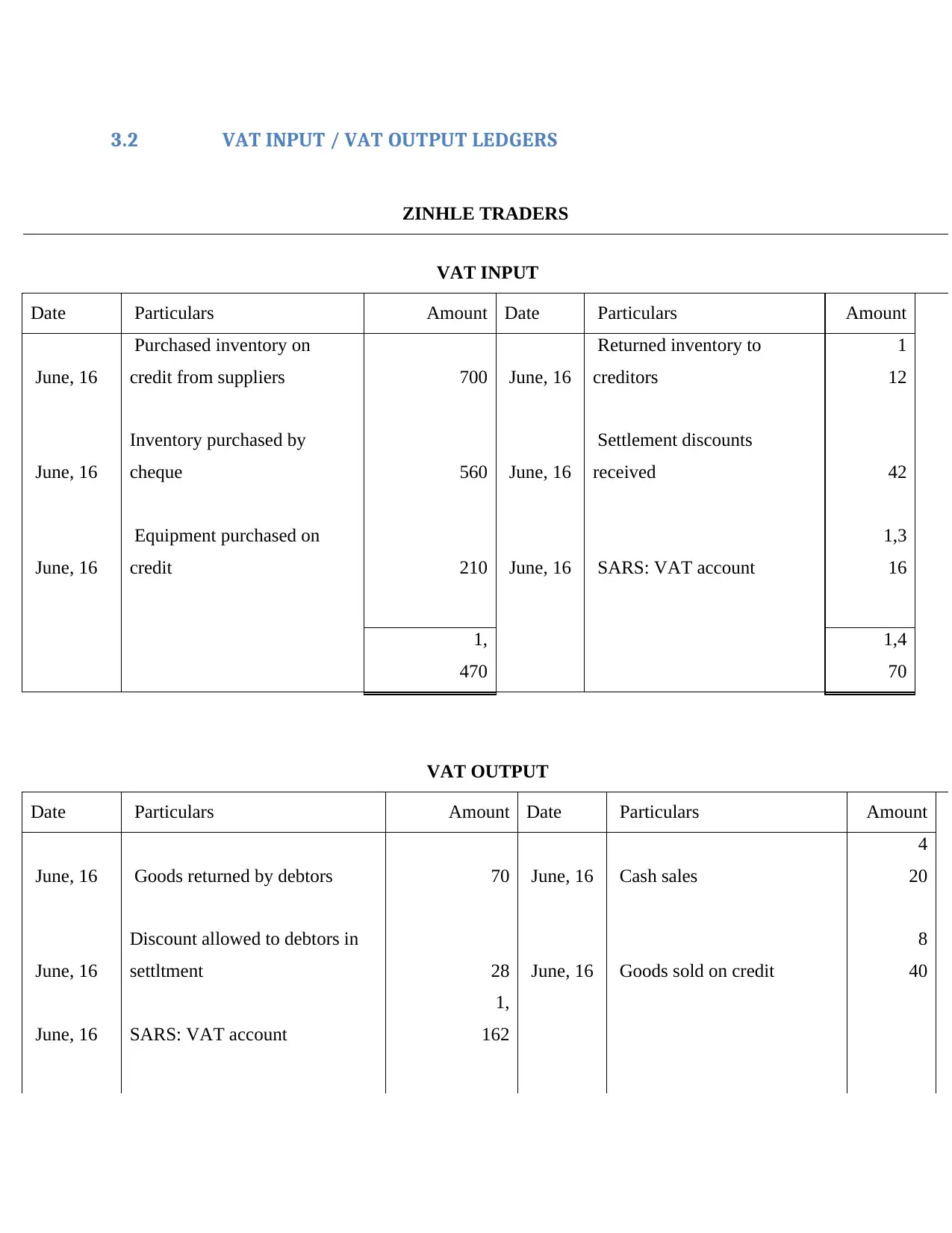

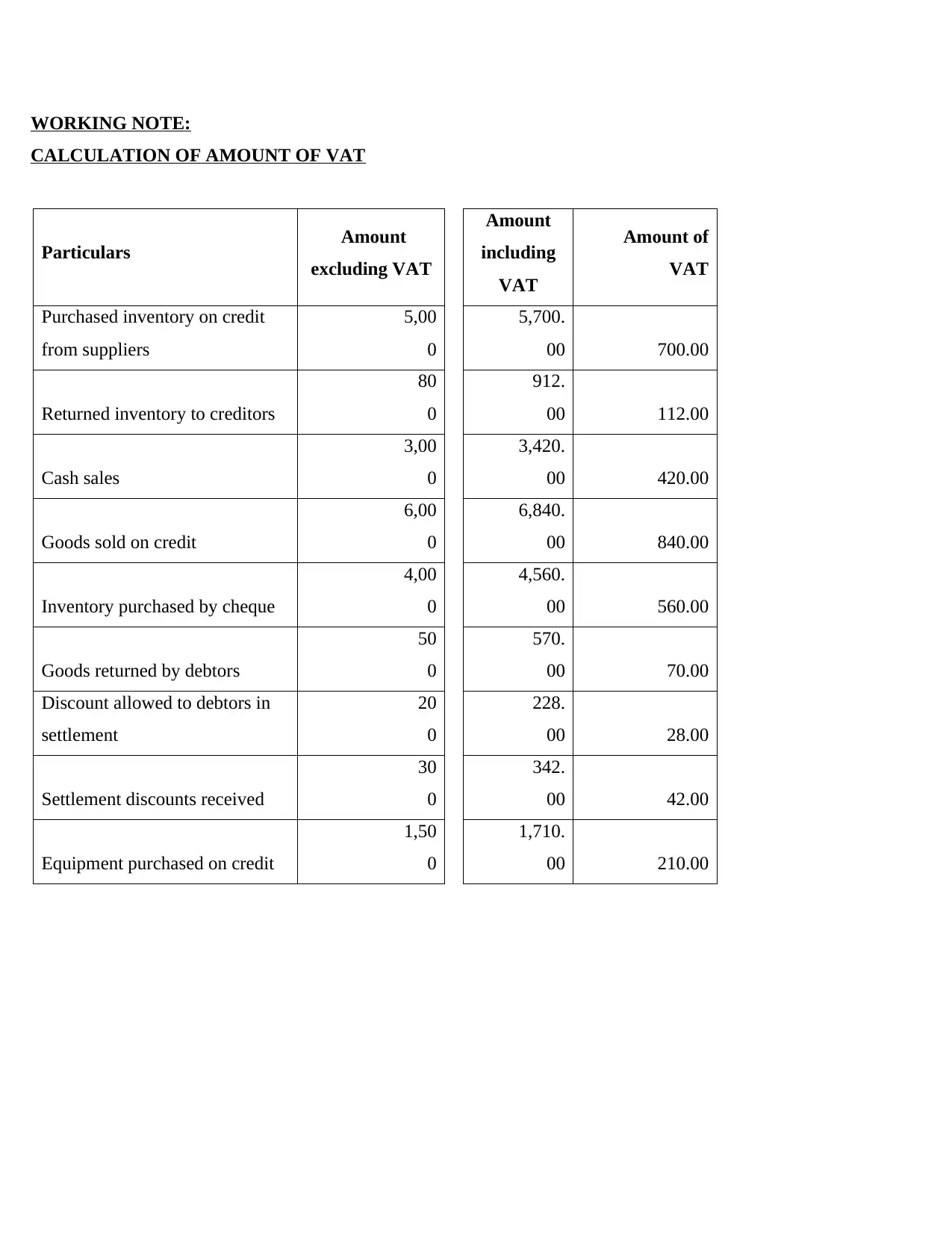

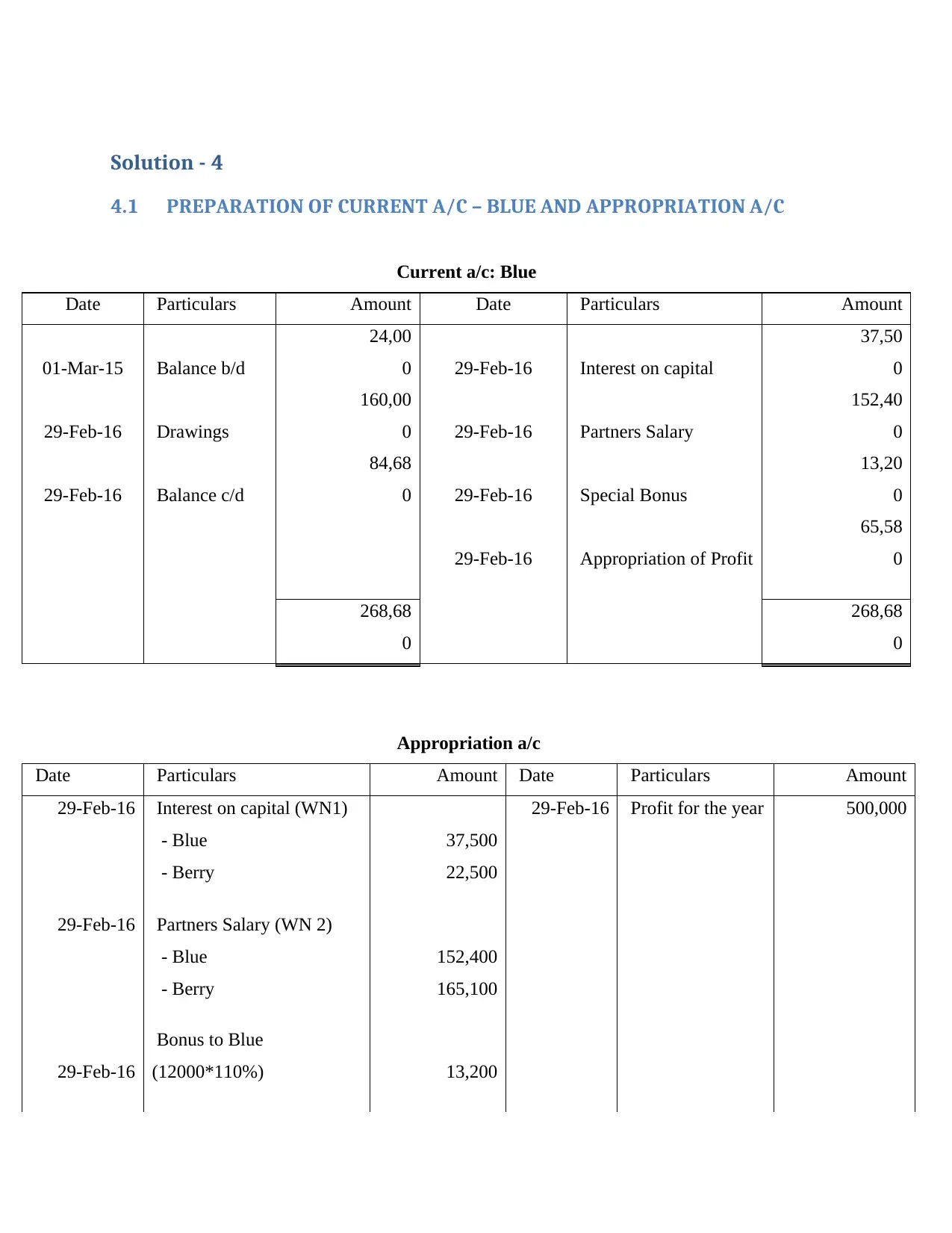

This document provides solutions to various accounting problems. It covers topics such as the accounting equation, debtor control accounts, bank account preparation, VAT input/output ledgers, current and appropriation accounts, and the equity section of the statement of financial position. Detailed solutions with explanations and working notes are included for each problem. The solutions demonstrate the preparation of financial statements and the application of accounting principles. The document also includes a trial balance and the calculation of net profit, showcasing a comprehensive approach to accounting problem-solving.

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.