ACCT 20074: Accounting Standards and Corporate Failures Analysis

VerifiedAdded on 2023/01/16

|11

|3272

|47

Report

AI Summary

This report provides a comprehensive analysis of the evolution of accounting standards in response to major corporate failures. It begins by highlighting the benefits of accounting standards, such as enhanced comparability and transparency, while also acknowledging the occurrence of corporate failures due to managerial misconduct and loopholes in the accounting standards. The report then details significant corporate crises, including Enron, Vivendi Universal, and One-Tel, and examines their impact on accounting regulations and standards. It explores the enactment of the Sarbanes-Oxley Act and the changes in accounting standards related to revenue recognition, measurement of leases, and property, plant, and equipment. Furthermore, the report critically evaluates the political lobbying and influences in the accounting standard-setting process, discussing the various forms of lobbying, the motivations of participants, and the impact of political pressure on standard-setting bodies like FASB, AASB, and IASB. The report concludes by emphasizing how corporate failures have shaped accounting standards, and the ongoing efforts to converge towards a comprehensive set of global accounting standards.

CONTEMPORARY ACCOUNTING 1

Introduction

The predictable advantages of the accounting standards are compelling. The

accounting standards are adopted by the entities across the world to enhance the comparisons

and transparency of the financial statements and an overall reduction in the financial

statement preparation costs. Further, the varied range of the stakeholder groups gain useful

insight about the management of affairs of an entity. For instance, it is significant to note that

the arguments presented in the favour of the adoption of the International Financial Reporting

Standards (IFRS), as cited by Brown, (2013) are advancing the quality and comparability of

financial reporting practices, promoting the expansion of national capital markets, thereby

leading to successful integration international markets. However, the corporate failures have

yet taken place in varied regions and industries owing to combination of the loopholes of the

accounting standards and misuse of the powers by those in the position.

The following assignment is aimed at analysing the progress of the accounting

standards over the years. The said evaluation will be done with the aid of the description of

the major corporate failures and how the same have shaped the accounting standards. Further,

the assignment will shed light on the complexity of the accounting standard setting process in

terms of the political lobbying.

Corporate crises and post-crisis developments in accounting

regulations/standards

The most significant characteristics of a corporate entity is the separate legal identity,

which separates the ownership from the management. Thus, the managerial body of an entity

has the prime responsibility to implement the relevant accounting standards in the business

functions and preparation and presentation of the financial information. Section 298(1) of the

Corporations Act accords the same as in case of the Australian context, likewise global

regulations state on the same lines. The accounting standards facilitate a framework within

which business entities are supposed to prepare the financial reports for the dissemination to

the public. The impacts of the accounting standards are considerable and the same lead to the

enhancement of the quality of financial reporting by entities as stated under Part 3.6 of the

Corporations Law. The primary benefits of the accounting standards can be deduced to be

provision of better picture, quality assurance, comparability and transparency. In spite of the

benefits as listed above, there have occurred numerous corporate failures owing to conflict of

Introduction

The predictable advantages of the accounting standards are compelling. The

accounting standards are adopted by the entities across the world to enhance the comparisons

and transparency of the financial statements and an overall reduction in the financial

statement preparation costs. Further, the varied range of the stakeholder groups gain useful

insight about the management of affairs of an entity. For instance, it is significant to note that

the arguments presented in the favour of the adoption of the International Financial Reporting

Standards (IFRS), as cited by Brown, (2013) are advancing the quality and comparability of

financial reporting practices, promoting the expansion of national capital markets, thereby

leading to successful integration international markets. However, the corporate failures have

yet taken place in varied regions and industries owing to combination of the loopholes of the

accounting standards and misuse of the powers by those in the position.

The following assignment is aimed at analysing the progress of the accounting

standards over the years. The said evaluation will be done with the aid of the description of

the major corporate failures and how the same have shaped the accounting standards. Further,

the assignment will shed light on the complexity of the accounting standard setting process in

terms of the political lobbying.

Corporate crises and post-crisis developments in accounting

regulations/standards

The most significant characteristics of a corporate entity is the separate legal identity,

which separates the ownership from the management. Thus, the managerial body of an entity

has the prime responsibility to implement the relevant accounting standards in the business

functions and preparation and presentation of the financial information. Section 298(1) of the

Corporations Act accords the same as in case of the Australian context, likewise global

regulations state on the same lines. The accounting standards facilitate a framework within

which business entities are supposed to prepare the financial reports for the dissemination to

the public. The impacts of the accounting standards are considerable and the same lead to the

enhancement of the quality of financial reporting by entities as stated under Part 3.6 of the

Corporations Law. The primary benefits of the accounting standards can be deduced to be

provision of better picture, quality assurance, comparability and transparency. In spite of the

benefits as listed above, there have occurred numerous corporate failures owing to conflict of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CONTEMPORARY ACCOUNTING 2

interest on the part of the owners or management leading to violation of rights of the other

stakeholder groups of businesses. Some of the chief corporate failures eras and their impact

on the accounting standards have been elaborated as follows.

As the FASB began its operations in 1973, initially the Board considered twenty-

seven initial agenda items, out of which only seven were pursued. The initial objectives of the

conceptual framework project did not comprise of the resolution of the accounting issues, but

included the setting of stage for future problem solutions (Detzen, 2014). Pre Enron era of

corporate failures is popularly termed as the era of the creative corporate failures. It is

significant to note that the corporate pictures reveal information to the extent the same are

painted, as there is also been left a room for the enhancing of considerations taken into

account as per the financial policies, exercise of professional judgements. Thus, financial

performance is achieved by exploiting breaches within legislation. This was followed by the

most popular failure that is widely remembered and lessons have been learned from the same

is that of the United States most popular energy company namely Enron. The company is in

news and literary works since the publication of its financial results in October 2001, which

disclosed a loss of a $638m in the income statement (da Silveira, 2013). Further, the debts

amounting to $1.2bn were highlighted that were previously not part of the balance sheet of

the entity. Some of the chief reasons that contributed to the said scandal are the mark to

market accounting approach for revenue recognition from the sale of natural gas contracts,

simultaneously inflating the current earnings; creation of the special purpose entities, off

balance sheet financing arrangements and others (Li, 2010). The company had established 12

business entities to abuse the US accounting rules in relation to the special purpose entities,

and facilitate the debt to be shifted off the balance sheet. Yet another major corporate failure

was that of the Vivendi Universal (France) where the Vivendi Universal’s (VU) had aimed at

obtaining approval for a further corporate acquisition from the European Commission, and

thus forced disposal of BskyB shares. It is significant to note that while the US GAAP

addressed the accounting rules for such a transaction, the same were missing specifically

from the French GAAP. Thus, the incident highlights the corporate failure in France. Yet

another incidents are related to the Australian corporate climate concerning the entity One

Tel. The major reasons for the said corporate failure were inefficient corporate governance

practices, the financial statements comprised of errors, low quality earnings of the entity,

combined with the low audit quality.

interest on the part of the owners or management leading to violation of rights of the other

stakeholder groups of businesses. Some of the chief corporate failures eras and their impact

on the accounting standards have been elaborated as follows.

As the FASB began its operations in 1973, initially the Board considered twenty-

seven initial agenda items, out of which only seven were pursued. The initial objectives of the

conceptual framework project did not comprise of the resolution of the accounting issues, but

included the setting of stage for future problem solutions (Detzen, 2014). Pre Enron era of

corporate failures is popularly termed as the era of the creative corporate failures. It is

significant to note that the corporate pictures reveal information to the extent the same are

painted, as there is also been left a room for the enhancing of considerations taken into

account as per the financial policies, exercise of professional judgements. Thus, financial

performance is achieved by exploiting breaches within legislation. This was followed by the

most popular failure that is widely remembered and lessons have been learned from the same

is that of the United States most popular energy company namely Enron. The company is in

news and literary works since the publication of its financial results in October 2001, which

disclosed a loss of a $638m in the income statement (da Silveira, 2013). Further, the debts

amounting to $1.2bn were highlighted that were previously not part of the balance sheet of

the entity. Some of the chief reasons that contributed to the said scandal are the mark to

market accounting approach for revenue recognition from the sale of natural gas contracts,

simultaneously inflating the current earnings; creation of the special purpose entities, off

balance sheet financing arrangements and others (Li, 2010). The company had established 12

business entities to abuse the US accounting rules in relation to the special purpose entities,

and facilitate the debt to be shifted off the balance sheet. Yet another major corporate failure

was that of the Vivendi Universal (France) where the Vivendi Universal’s (VU) had aimed at

obtaining approval for a further corporate acquisition from the European Commission, and

thus forced disposal of BskyB shares. It is significant to note that while the US GAAP

addressed the accounting rules for such a transaction, the same were missing specifically

from the French GAAP. Thus, the incident highlights the corporate failure in France. Yet

another incidents are related to the Australian corporate climate concerning the entity One

Tel. The major reasons for the said corporate failure were inefficient corporate governance

practices, the financial statements comprised of errors, low quality earnings of the entity,

combined with the low audit quality.

CONTEMPORARY ACCOUNTING 3

The events in the Enron, WorldCom, Vivendi Universal, One-Tel, Xerox and others

have led to the far reaching repercussions in the form of fall of the stock markets, entities

been declared as bankrupt, shattering of the investor confidence, and regulators being

encouraged to devise and propose more stringent means of preparation and dissemination of

the financial information (Markham, 2015). Consistent questions were raised regarding the

effectiveness of the existing rules and institutions in terms of corporate governance and

disclosure of information, not only in United States, but also at global level including

Australia. One of the major transformations that have been witnessed pose the Enron scandal

was the enactment of the Sarbanes Oxley Act. The effect is such that efforts have been made

to hasten the global regulation of the world’s capital markets. Accordingly, from the

discussions conducted above, it can be stated that over the years, the accounting profession

has evolved tremendously from the initial establishment of the regulatory bodies to the

convergence interests. The corporate failures like above, have shaped the various aspects of

the accounting standards. For instance, some of the accounting standards that have been in

highlight owing to the stated corporate failures are on lines of revenue recognition,

measurement and presentation of leases, measurement of the Property, plant and Equipment

and others. The chief accounting standard that underwent transformation, post the political,

regulatory, media and expert scrutiny was the IFRS 15 in international context and AASB

115 in the Australian context for the recognition of the revenues.

Thus, the above stated eras of the corporate failures have led to the various

developments in the various accounting standards. The current set of accounting standards

have started following the convergence approach, though the full convergence has yet not

been achieved, yet the efforts and the projects are on the said lines only. The modern set of

revised standards cover numerous business aspects such as the transactions with the related

parties, maintenance and the disclosure of apt corporate disclosure structure, establishment of

the sound internal control system and likewise. In addition, the regional corporate laws,

securities exchange commission, stock authorities have increasingly requiring the corporates

to abide by their duties and responsibilities of maintenance and preparation of the account

books and financial statements.

The events in the Enron, WorldCom, Vivendi Universal, One-Tel, Xerox and others

have led to the far reaching repercussions in the form of fall of the stock markets, entities

been declared as bankrupt, shattering of the investor confidence, and regulators being

encouraged to devise and propose more stringent means of preparation and dissemination of

the financial information (Markham, 2015). Consistent questions were raised regarding the

effectiveness of the existing rules and institutions in terms of corporate governance and

disclosure of information, not only in United States, but also at global level including

Australia. One of the major transformations that have been witnessed pose the Enron scandal

was the enactment of the Sarbanes Oxley Act. The effect is such that efforts have been made

to hasten the global regulation of the world’s capital markets. Accordingly, from the

discussions conducted above, it can be stated that over the years, the accounting profession

has evolved tremendously from the initial establishment of the regulatory bodies to the

convergence interests. The corporate failures like above, have shaped the various aspects of

the accounting standards. For instance, some of the accounting standards that have been in

highlight owing to the stated corporate failures are on lines of revenue recognition,

measurement and presentation of leases, measurement of the Property, plant and Equipment

and others. The chief accounting standard that underwent transformation, post the political,

regulatory, media and expert scrutiny was the IFRS 15 in international context and AASB

115 in the Australian context for the recognition of the revenues.

Thus, the above stated eras of the corporate failures have led to the various

developments in the various accounting standards. The current set of accounting standards

have started following the convergence approach, though the full convergence has yet not

been achieved, yet the efforts and the projects are on the said lines only. The modern set of

revised standards cover numerous business aspects such as the transactions with the related

parties, maintenance and the disclosure of apt corporate disclosure structure, establishment of

the sound internal control system and likewise. In addition, the regional corporate laws,

securities exchange commission, stock authorities have increasingly requiring the corporates

to abide by their duties and responsibilities of maintenance and preparation of the account

books and financial statements.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CONTEMPORARY ACCOUNTING 4

Critical evaluation of the lobbies/influences in the accounting

standard setting process

The term political lobbying or influence is referred to as the decisive intervention by

an economic entity in the several of processes of accounting standard-setting. The outcome of

that process is the focus of the said intervention, so as to facilitate an increment in the

economic value of that particular entity. The yet another aim is the accomplishment of other

purposes that are not on the same lines as that of the objectives of the standard setting

controllers such as FASB, AASB, and others (Königsgruber, 2010). It is significant to note

that the accounting standard setting process is a comprehensive process which involves a

series of steps such as the public discussions, invitation of commentary letters, consultations,

discussion by the experts and other related activities. Such a comprehensive framework not

only indicates importance and expected impact of the new standards, but also ensures the

legitimacy of the processes. The lobbying occurs in various forms such as the submission of a

comment letter by the interested party in the process. It is vital to note that the conflict of the

limited number of resources available for the satisfaction of the stakeholders and the

unlimited number of consumer needs; is also applicable in the accounting profession as well

(Stenka & Taylor, 2010). With the existence of the various definitions of income and capital

and methods for their measurement, the onus to make the choice from the options available

lies with the preparers of financial statements in relation to provision of the useful

information to the users of the financial statements (Zeff, 2012). It must be noted that the

smallest of change in the accounting standards may lead to the substantial alteration in the

flow of the economic benefits to affected stakeholders. Thus, the comprehensive standard

setting process lead to the reduction of the risk of conflicts among various stakeholder groups

such as that of auditors, users, prepares, regulators and others, as the same are invited in the

participation in the preparation stage of the new accounting standards (Hansen, 2011).

The literature on the political lobbying has evaluated the motivation of participants

which comprises of varied attitudes, objections, opinions, and suggestions. In context of

lobbying, the submission of the comment letter depicts the fact that expected benefits are

more than incurred costs. This means that there is an existing belief in the minds of the

lobbyist that they can potentially influence the attitude of a standard setter in a particular

scenario (Orens, Jorissen, Lybaert & Van Der Tas, 2011). The model devised by (Sutton

1984) in context of lobbying indicates that the pressure of lobbying in the form of comment

Critical evaluation of the lobbies/influences in the accounting

standard setting process

The term political lobbying or influence is referred to as the decisive intervention by

an economic entity in the several of processes of accounting standard-setting. The outcome of

that process is the focus of the said intervention, so as to facilitate an increment in the

economic value of that particular entity. The yet another aim is the accomplishment of other

purposes that are not on the same lines as that of the objectives of the standard setting

controllers such as FASB, AASB, and others (Königsgruber, 2010). It is significant to note

that the accounting standard setting process is a comprehensive process which involves a

series of steps such as the public discussions, invitation of commentary letters, consultations,

discussion by the experts and other related activities. Such a comprehensive framework not

only indicates importance and expected impact of the new standards, but also ensures the

legitimacy of the processes. The lobbying occurs in various forms such as the submission of a

comment letter by the interested party in the process. It is vital to note that the conflict of the

limited number of resources available for the satisfaction of the stakeholders and the

unlimited number of consumer needs; is also applicable in the accounting profession as well

(Stenka & Taylor, 2010). With the existence of the various definitions of income and capital

and methods for their measurement, the onus to make the choice from the options available

lies with the preparers of financial statements in relation to provision of the useful

information to the users of the financial statements (Zeff, 2012). It must be noted that the

smallest of change in the accounting standards may lead to the substantial alteration in the

flow of the economic benefits to affected stakeholders. Thus, the comprehensive standard

setting process lead to the reduction of the risk of conflicts among various stakeholder groups

such as that of auditors, users, prepares, regulators and others, as the same are invited in the

participation in the preparation stage of the new accounting standards (Hansen, 2011).

The literature on the political lobbying has evaluated the motivation of participants

which comprises of varied attitudes, objections, opinions, and suggestions. In context of

lobbying, the submission of the comment letter depicts the fact that expected benefits are

more than incurred costs. This means that there is an existing belief in the minds of the

lobbyist that they can potentially influence the attitude of a standard setter in a particular

scenario (Orens, Jorissen, Lybaert & Van Der Tas, 2011). The model devised by (Sutton

1984) in context of lobbying indicates that the pressure of lobbying in the form of comment

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CONTEMPORARY ACCOUNTING 5

letter, in the case major and controversial accounting standards and projects is higher than the

lobbying in the case of the minor adjustments of existing practices (Procházka, 2015). In

terms of the cost benefit analysis, the cost of the preparation of the comment letter is much

lower than the benefits obtained to the economic users of the said standards. There has been

additionally wide literature available in which the lobbyists have been successful in the

achievement of their objective in the standard setting process. It must be noted that the

intensity of the controversy surrounding an accounting standard is evident from the number

of the comments as received by the board. Further, the increment in the controversy leads to

the invitation of the greater attention from parties that are affected, as a result of which the

regulatory bodies such as the AASB, IASB, and FASB are exposed to the greater amount of

pressure. The greater amount of pressure from the stakeholders leads to the weakening of the

power of the IASB, AASB and others, while attempting to defend its position. The result of

the same is that in the standard-setting process, the regulatory bodies succumb to lobbyists

leading to the significant revisions in the projects being discussed or even the projects being

stopped in between that were once started (Gipper, Lombardi & Skinner, 2013). As stated in

the previous parts, the accounting standard that was exposed to intensive media scrutiny,

expert examination after the corporate failures like that of Enron, One Tel and other was in

relation to the revenue recognition by the entities. Consequently, the amendment of the IFRS

15 on the Revenue from Contracts with Customers, in the United States was initiated. As per

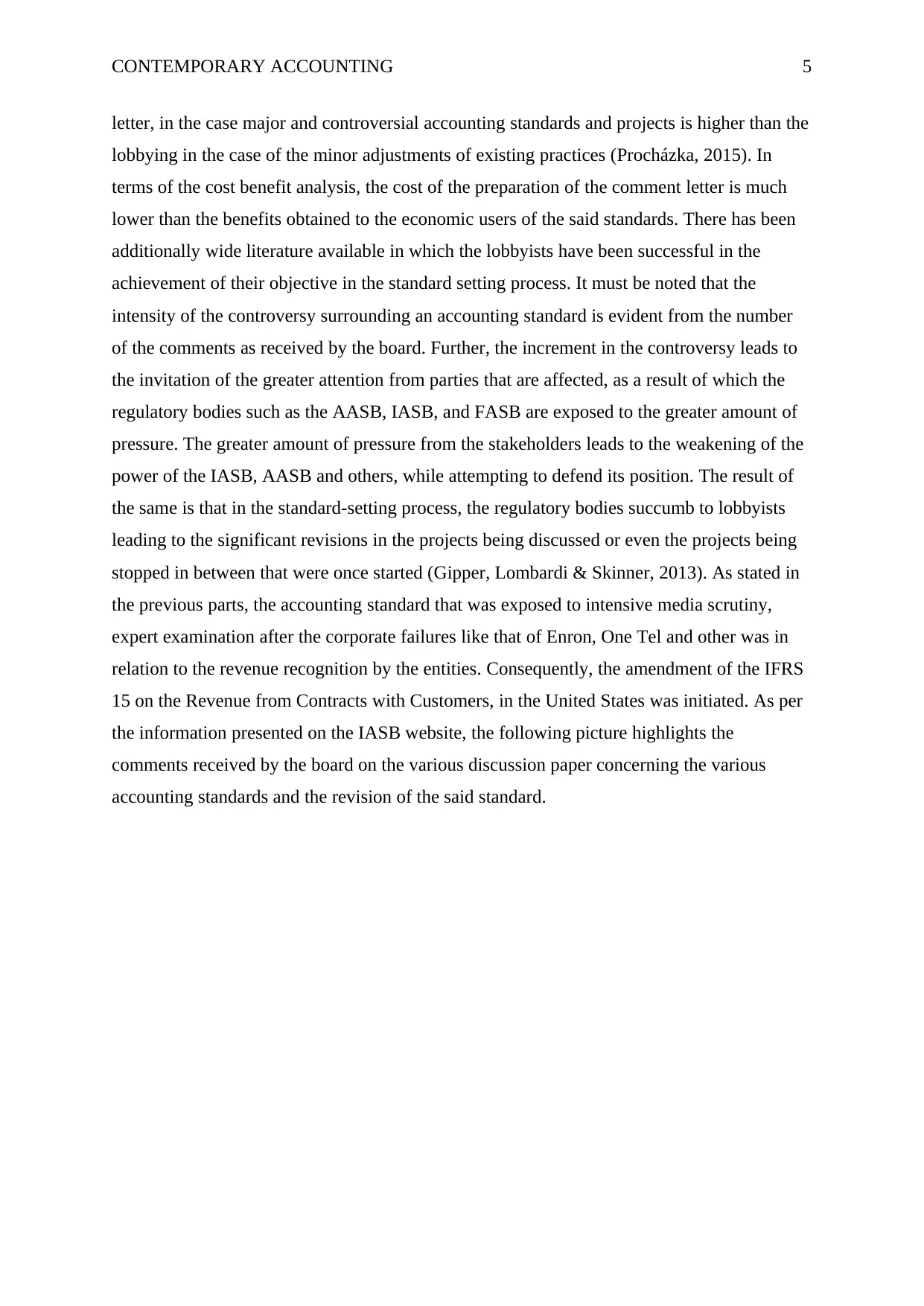

the information presented on the IASB website, the following picture highlights the

comments received by the board on the various discussion paper concerning the various

accounting standards and the revision of the said standard.

letter, in the case major and controversial accounting standards and projects is higher than the

lobbying in the case of the minor adjustments of existing practices (Procházka, 2015). In

terms of the cost benefit analysis, the cost of the preparation of the comment letter is much

lower than the benefits obtained to the economic users of the said standards. There has been

additionally wide literature available in which the lobbyists have been successful in the

achievement of their objective in the standard setting process. It must be noted that the

intensity of the controversy surrounding an accounting standard is evident from the number

of the comments as received by the board. Further, the increment in the controversy leads to

the invitation of the greater attention from parties that are affected, as a result of which the

regulatory bodies such as the AASB, IASB, and FASB are exposed to the greater amount of

pressure. The greater amount of pressure from the stakeholders leads to the weakening of the

power of the IASB, AASB and others, while attempting to defend its position. The result of

the same is that in the standard-setting process, the regulatory bodies succumb to lobbyists

leading to the significant revisions in the projects being discussed or even the projects being

stopped in between that were once started (Gipper, Lombardi & Skinner, 2013). As stated in

the previous parts, the accounting standard that was exposed to intensive media scrutiny,

expert examination after the corporate failures like that of Enron, One Tel and other was in

relation to the revenue recognition by the entities. Consequently, the amendment of the IFRS

15 on the Revenue from Contracts with Customers, in the United States was initiated. As per

the information presented on the IASB website, the following picture highlights the

comments received by the board on the various discussion paper concerning the various

accounting standards and the revision of the said standard.

CONTEMPORARY ACCOUNTING 6

Thus, as depicted in the picture, the highest number of comments received were in

relation to the IFRS 15 “Revenue from contracts with customer,” followed by the IAS 17 on

Leases. The information depicts that a total of 211 comments were received on the discussion

paper stage, 986 comments were received on the Exposure Draft stage. In addition to the

above, 357 comments were also received in the Revised Exposure Draft stage as well.

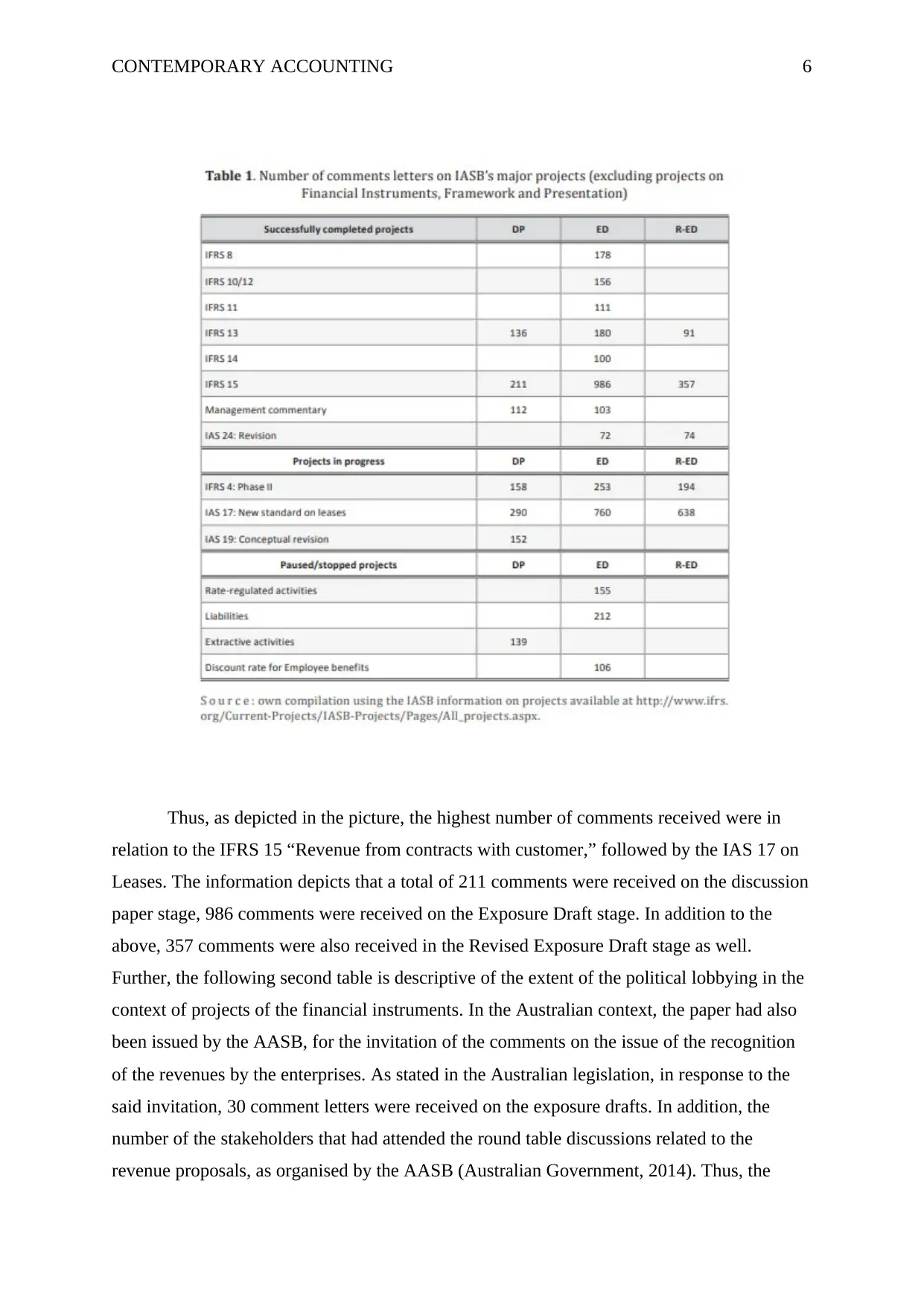

Further, the following second table is descriptive of the extent of the political lobbying in the

context of projects of the financial instruments. In the Australian context, the paper had also

been issued by the AASB, for the invitation of the comments on the issue of the recognition

of the revenues by the enterprises. As stated in the Australian legislation, in response to the

said invitation, 30 comment letters were received on the exposure drafts. In addition, the

number of the stakeholders that had attended the round table discussions related to the

revenue proposals, as organised by the AASB (Australian Government, 2014). Thus, the

Thus, as depicted in the picture, the highest number of comments received were in

relation to the IFRS 15 “Revenue from contracts with customer,” followed by the IAS 17 on

Leases. The information depicts that a total of 211 comments were received on the discussion

paper stage, 986 comments were received on the Exposure Draft stage. In addition to the

above, 357 comments were also received in the Revised Exposure Draft stage as well.

Further, the following second table is descriptive of the extent of the political lobbying in the

context of projects of the financial instruments. In the Australian context, the paper had also

been issued by the AASB, for the invitation of the comments on the issue of the recognition

of the revenues by the enterprises. As stated in the Australian legislation, in response to the

said invitation, 30 comment letters were received on the exposure drafts. In addition, the

number of the stakeholders that had attended the round table discussions related to the

revenue proposals, as organised by the AASB (Australian Government, 2014). Thus, the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CONTEMPORARY ACCOUNTING 7

overall consultations organised by the IASB and the FASB together had led to the receipt of

the 1,500 comment letters by the stakeholders.

The above table highlights the fact that the hedge accounting is one prime method of

concern of the stakeholders, the highest number of comment letters receipt sheds light on the

same. As depicted above, the exposure draft on hedge accounting had received 216 comment

letters. The following points are additionally noteworthy in relation to the minor changes

concerning the present projects.

overall consultations organised by the IASB and the FASB together had led to the receipt of

the 1,500 comment letters by the stakeholders.

The above table highlights the fact that the hedge accounting is one prime method of

concern of the stakeholders, the highest number of comment letters receipt sheds light on the

same. As depicted above, the exposure draft on hedge accounting had received 216 comment

letters. The following points are additionally noteworthy in relation to the minor changes

concerning the present projects.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CONTEMPORARY ACCOUNTING 8

The table describes the difference between the major and the minor projects. Only for

some major projects, there is an exercise of the publication of the Discussion papers. Further,

if the exposure drafts faces strong objections, in relation to the major projects, the same are

sometimes revised.

Conclusion

The discussions conducted in the previous parts, aid to conclude that accounting

standards and guidelines serves as the framework within which the entities must prepare and

disseminate the financial information. The corporate failures have nevertheless taken place

due to the loopholes being abused sometimes and misuse of the powers by the senior

management and employees of the entity. The major corporate failures such as that of the

Enron, Xerox, One-Tel have been highlighted in the work to study the impact of the same on

the accounting standards in the subsequent periods. Further, the work highlighted that the

accounting standards setting procedure is a complex process with the existence of a number

of stakeholders. Accordingly, the regulatory bodies face a great deal of the political lobbying,

and the same leads to the significant impacts on the progress and formation of the accounting

standards at regional and global levels. The work highlighted the details of the excessive

political influence in the global and the Australian context in relation to the development of

the IASB and AASB standards. The figures presented in the various tables are indicative of

the facts that the external commenting bodies hold the potential capacity to influence the

The table describes the difference between the major and the minor projects. Only for

some major projects, there is an exercise of the publication of the Discussion papers. Further,

if the exposure drafts faces strong objections, in relation to the major projects, the same are

sometimes revised.

Conclusion

The discussions conducted in the previous parts, aid to conclude that accounting

standards and guidelines serves as the framework within which the entities must prepare and

disseminate the financial information. The corporate failures have nevertheless taken place

due to the loopholes being abused sometimes and misuse of the powers by the senior

management and employees of the entity. The major corporate failures such as that of the

Enron, Xerox, One-Tel have been highlighted in the work to study the impact of the same on

the accounting standards in the subsequent periods. Further, the work highlighted that the

accounting standards setting procedure is a complex process with the existence of a number

of stakeholders. Accordingly, the regulatory bodies face a great deal of the political lobbying,

and the same leads to the significant impacts on the progress and formation of the accounting

standards at regional and global levels. The work highlighted the details of the excessive

political influence in the global and the Australian context in relation to the development of

the IASB and AASB standards. The figures presented in the various tables are indicative of

the facts that the external commenting bodies hold the potential capacity to influence the

CONTEMPORARY ACCOUNTING 9

decisions taken by the regulatory bodies. While the major projects face a lot of comments

letters, the case is opposite in the case of the minor amendments for the existing projects.

decisions taken by the regulatory bodies. While the major projects face a lot of comments

letters, the case is opposite in the case of the minor amendments for the existing projects.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CONTEMPORARY ACCOUNTING 10

References

Australian Government (2014). Regulation Impact Statement- AASB 15 Revenue from

Contracts with Customers Retrieved from:

https://www.legislation.gov.au/Details/F2015L00115/Supporting%20Material/

Text#_Toc405543469

Brown, P. (2013). Some observations on research on the benefits to nations of adopting

IFRS. The Japanese Accounting Review, 3(2013), 1-19.

da Silveira, A. (2013). The Enron Scandal a Decade Later: Lessons Learned?. SSRN

Electronic Journal. doi: 10.2139/ssrn.2310114

Detzen, D. (2014). Inflation, exchange rates, and the conceptual framework: The FASB's

debates from 1973 to 1984. Accounting Horizons, 28(3), 673-694.

Gipper, B., Lombardi, B. J., & Skinner, D. J. (2013). The politics of accounting standard-

setting: A review of empirical research. Australian Journal of Management, 38(3),

523-551.

Hansen, T. B. (2011). Lobbying of the IASB: an empirical investigation. Journal of

International Accounting Research, 10(2), 57-75.

Jones, S. (Ed.). (2015). The Routledge companion to financial accounting theory. UK:

Routledge.

Königsgruber, R. (2010). A Political Economy of Accounting Standard Setting. Journal of

Management & Governance, 14(4), 277–295. http://doi.org/10.1007/s10997-009-

9101-1.

Li, Y. (2010). The case analysis of the scandal of Enron. International Journal of Business

and Management, 5(10), 37.

Markham, J. W. (2015). A financial history of the United States: From Enron-era scandals to

the subprime crisis (2004-2006); From the subprime crisis to the Great Recession

(2006-2009). Oxon: Routledge.

References

Australian Government (2014). Regulation Impact Statement- AASB 15 Revenue from

Contracts with Customers Retrieved from:

https://www.legislation.gov.au/Details/F2015L00115/Supporting%20Material/

Text#_Toc405543469

Brown, P. (2013). Some observations on research on the benefits to nations of adopting

IFRS. The Japanese Accounting Review, 3(2013), 1-19.

da Silveira, A. (2013). The Enron Scandal a Decade Later: Lessons Learned?. SSRN

Electronic Journal. doi: 10.2139/ssrn.2310114

Detzen, D. (2014). Inflation, exchange rates, and the conceptual framework: The FASB's

debates from 1973 to 1984. Accounting Horizons, 28(3), 673-694.

Gipper, B., Lombardi, B. J., & Skinner, D. J. (2013). The politics of accounting standard-

setting: A review of empirical research. Australian Journal of Management, 38(3),

523-551.

Hansen, T. B. (2011). Lobbying of the IASB: an empirical investigation. Journal of

International Accounting Research, 10(2), 57-75.

Jones, S. (Ed.). (2015). The Routledge companion to financial accounting theory. UK:

Routledge.

Königsgruber, R. (2010). A Political Economy of Accounting Standard Setting. Journal of

Management & Governance, 14(4), 277–295. http://doi.org/10.1007/s10997-009-

9101-1.

Li, Y. (2010). The case analysis of the scandal of Enron. International Journal of Business

and Management, 5(10), 37.

Markham, J. W. (2015). A financial history of the United States: From Enron-era scandals to

the subprime crisis (2004-2006); From the subprime crisis to the Great Recession

(2006-2009). Oxon: Routledge.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CONTEMPORARY ACCOUNTING 11

Orens, R., Jorissen, A., Lybaert, N., & Van Der Tas, L. (2011). Corporate lobbying in private

accounting standard setting: does the IASB have to reckon with national

differences?. Accounting in Europe, 8(2), 211-234.

Procházka, D. (2015). Lobbying on the IASB Standards: An analysis of the Lobbyists’

Behaviour over Period 2006–2014. Copernican Journal Of Finance &

Accounting, 4(2), 129. doi: 10.12775/cjfa.2015.020

Stenka, R., & Taylor, P. (2010). Setting UK Standards on the Concept of Control: An

Analysis of Lobbying Behaviour. Accounting and Business Research, 40(2), 109–

130. http://doi.org/10.1080/00014788.2010.9663387

Orens, R., Jorissen, A., Lybaert, N., & Van Der Tas, L. (2011). Corporate lobbying in private

accounting standard setting: does the IASB have to reckon with national

differences?. Accounting in Europe, 8(2), 211-234.

Procházka, D. (2015). Lobbying on the IASB Standards: An analysis of the Lobbyists’

Behaviour over Period 2006–2014. Copernican Journal Of Finance &

Accounting, 4(2), 129. doi: 10.12775/cjfa.2015.020

Stenka, R., & Taylor, P. (2010). Setting UK Standards on the Concept of Control: An

Analysis of Lobbying Behaviour. Accounting and Business Research, 40(2), 109–

130. http://doi.org/10.1080/00014788.2010.9663387

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.