Analyzing IFRS 9 & IAS 39 Amendments: Interest Rate Benchmark Reform

VerifiedAdded on 2022/11/27

|10

|1508

|198

Report

AI Summary

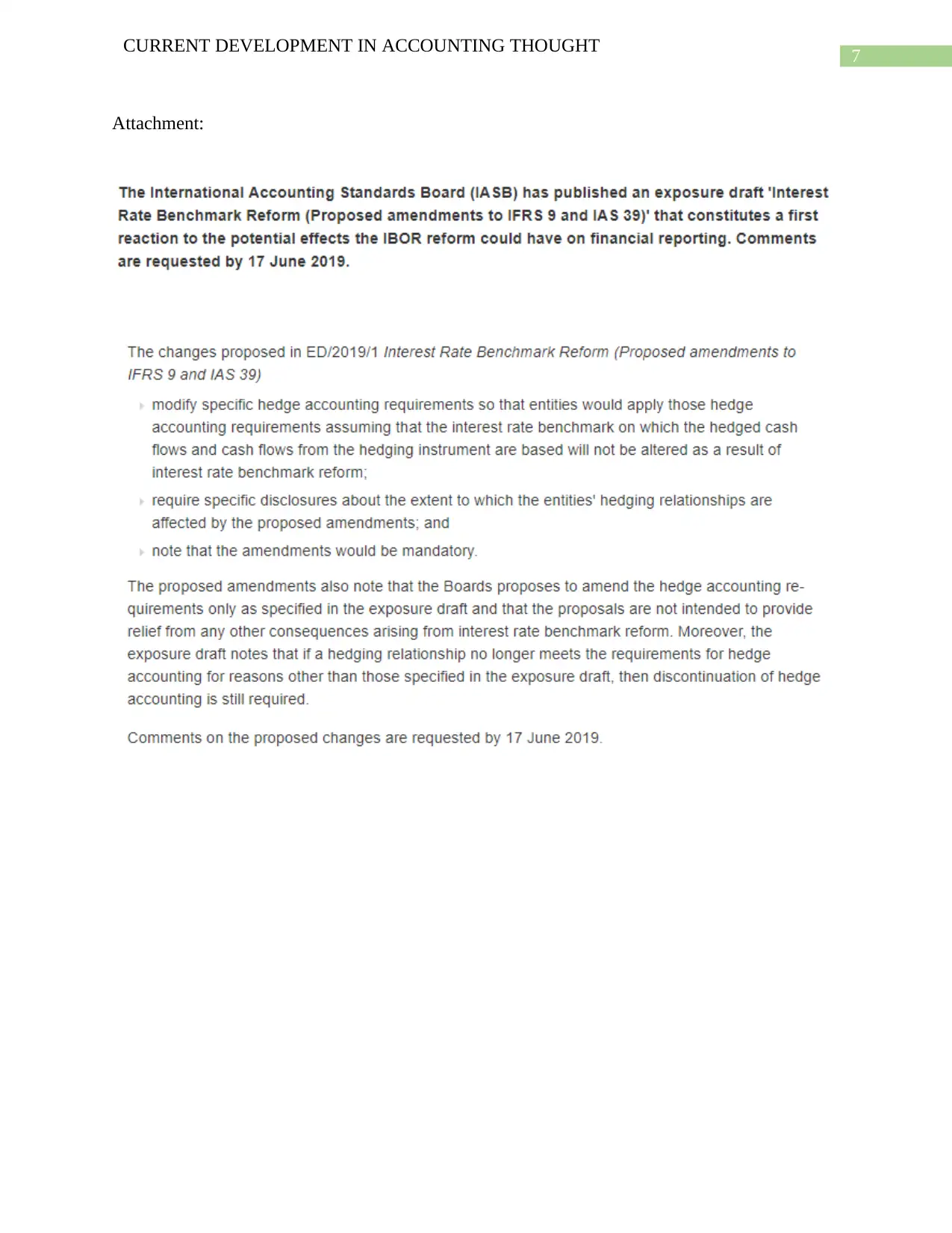

This report provides an analysis of the exposure draft ‘interest rate benchmark reform’ and amendments to IFRS 9 and IAS 39, focusing on the implications for financial reporting. It discusses the challenges posed by the potential cessation of interbank offered rates (IBORs) and the proposed amendments to address these challenges. The report examines the regulator's behavior through the lens of public interest theory, highlighting the aim to improve financial reporting quality. It also explores areas of agreement and disagreement with the exposure draft, including the scope of hedging accounting changes and disclosure requirements. Furthermore, the application of public and private interest theories is considered in relation to the amendments. The report concludes that public interest theory best explains the rationale behind the amendments, as they enhance the transparency and accuracy of financial reporting concerning hedging accounting and benchmark interest rates.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.