Accounting Standards Report: Case Studies on Australian Standards

VerifiedAdded on 2020/02/24

|9

|2381

|345

Report

AI Summary

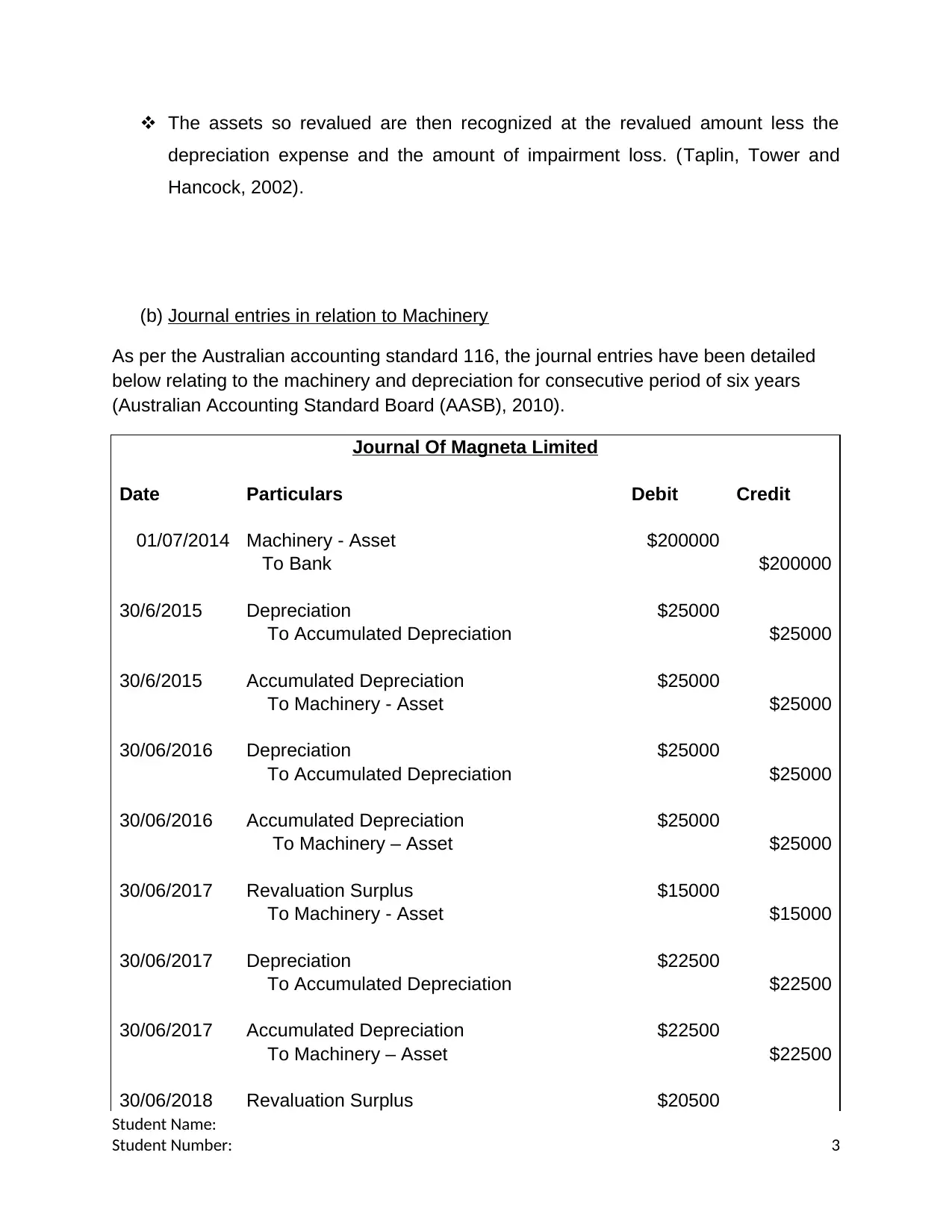

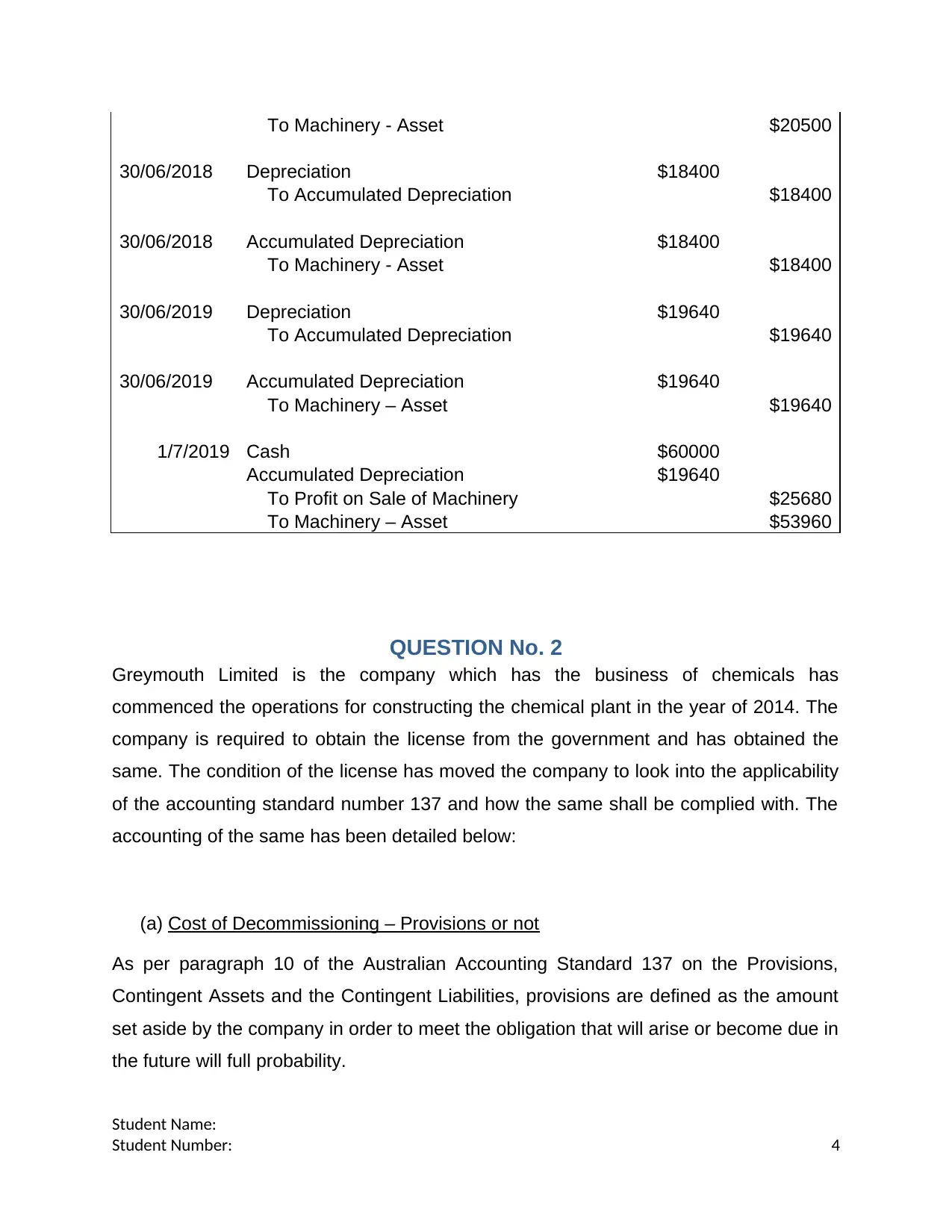

This report provides a comprehensive analysis of accounting standards, focusing on practical application through case studies. The executive summary introduces the importance of accounting standards for companies and their alignment with government policies. The report delves into specific standards, including accounting policies, property, plant, and equipment, and provisions and contingent liabilities. The first case study examines Magenta Company's change in valuation method from cost to revaluation model, referencing AASB 108 and AASB 116 and providing journal entries. The second case study analyzes Greymouth Limited's chemical plant decommissioning, applying AASB 137 to determine the provision for decommissioning costs, including calculations and journal entries. The third case study evaluates the recognition of intangible assets, particularly computer software, based on AASB 138. The report concludes with recommendations for companies to correctly adopt and apply accounting standards, emphasizing their significance for stakeholders. The report uses Australian Accounting Standards as a reference and provides detailed calculations and journal entries for each case study. The report is designed to help students understand the practical aspects of accounting standards.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.