Management Accounting for Financial Problem Solving and Planning

VerifiedAdded on 2024/05/17

|21

|3410

|305

Report

AI Summary

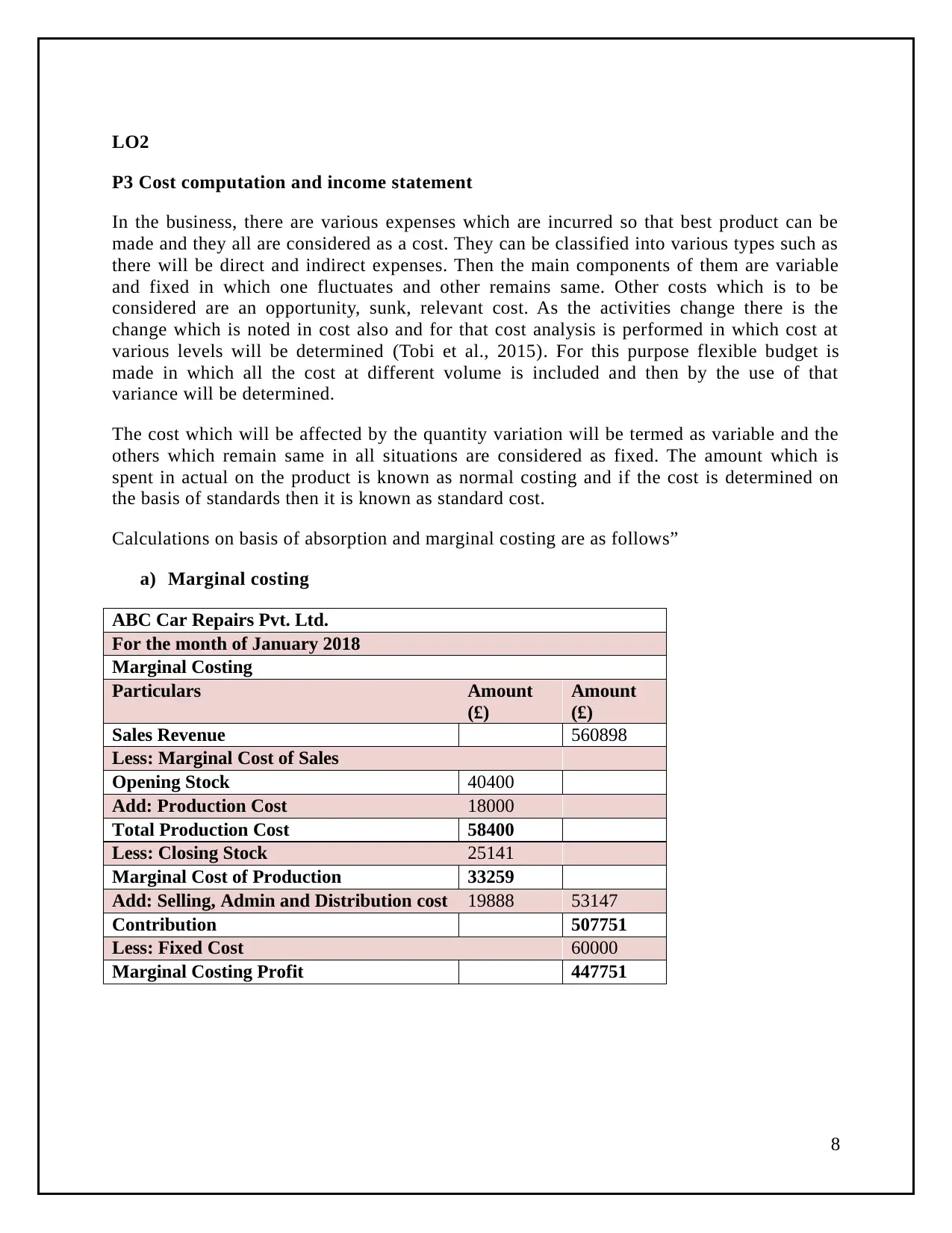

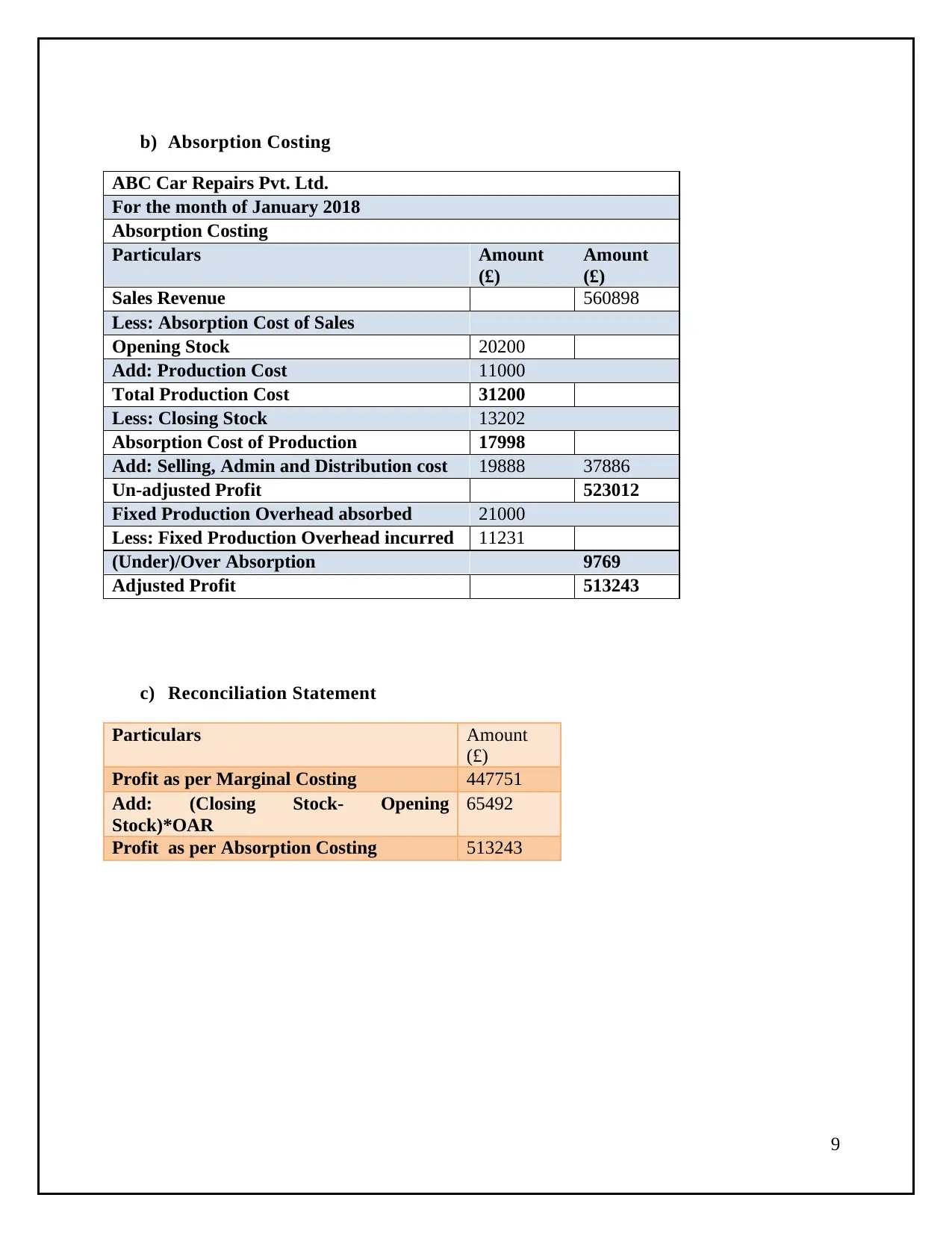

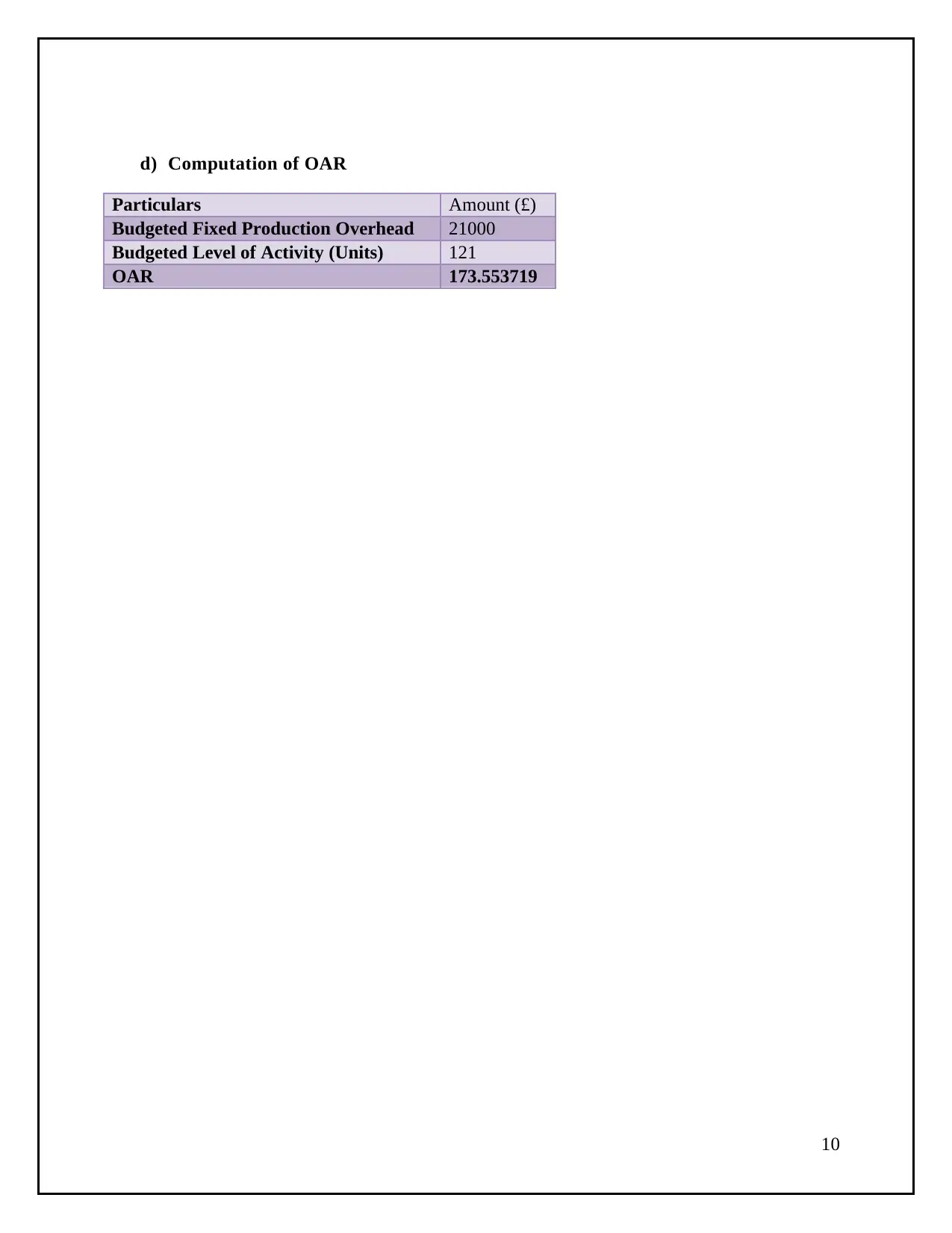

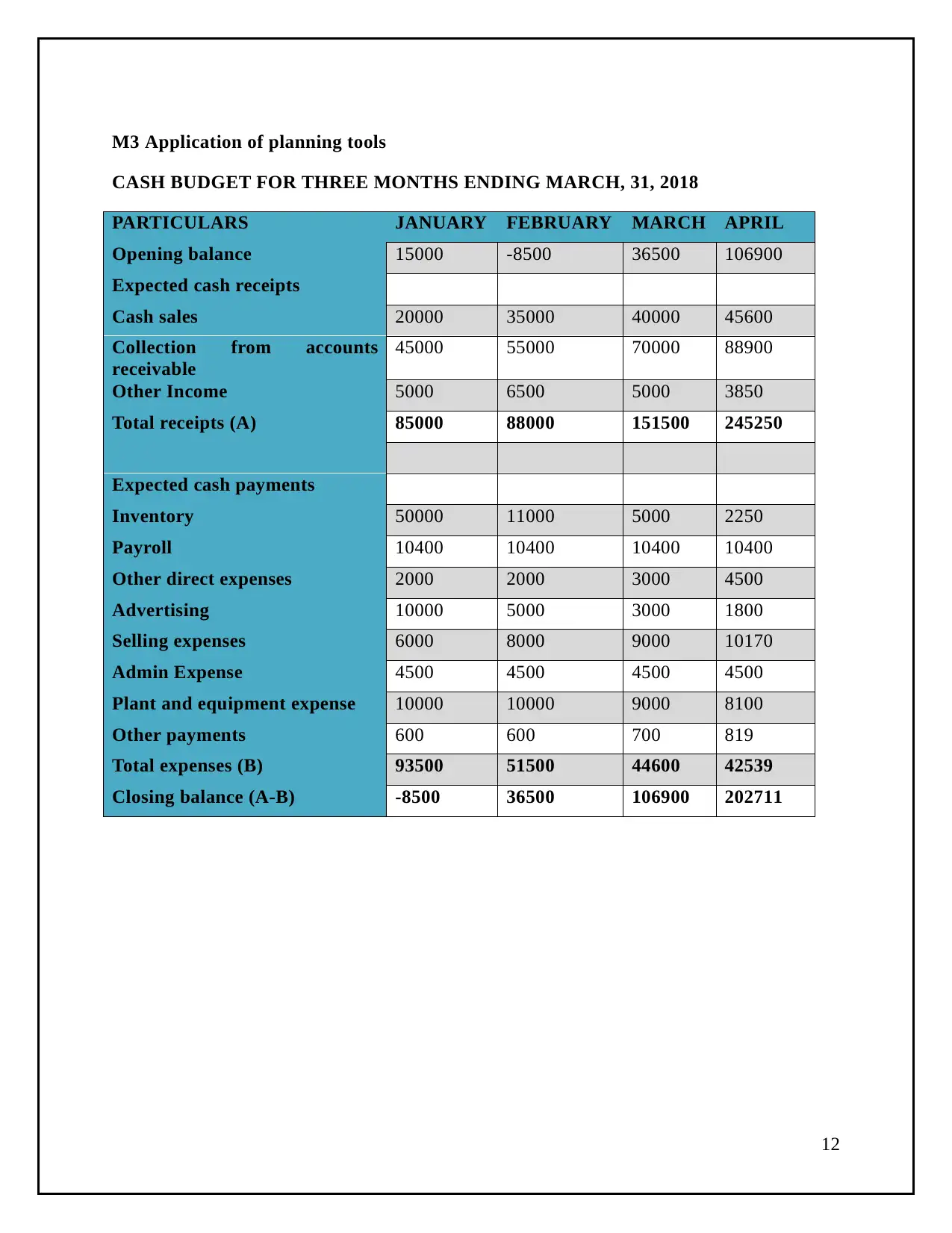

This report provides a comprehensive overview of management accounting principles and their application in resolving financial problems and achieving sustainable success. It begins by defining management accounting and its various systems, including financial accounting, cost accounting, and tax accounting. The report then explores different methods of reporting management accounting information, such as income statements, cost of goods sold reports, and cash flow statements. It delves into cost computation, distinguishing between direct and indirect costs, variable and fixed costs, and relevant and irrelevant costs, with calculations based on absorption and marginal costing. The report also examines the advantages and disadvantages of various planning tools, including incremental budgets, zero-based budgets, and cash budgets, and applies these tools in a practical cash budget scenario, identifying percentage deviations. Finally, it discusses how management accounting can be adapted to resolve financial problems and lead an organization to sustainable success, emphasizing the integration of management accounting systems and reporting within the organization.

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.