Case Study Analysis: Adam & Co. Accounting Information System - HA2042

VerifiedAdded on 2022/11/09

|12

|2680

|346

Case Study

AI Summary

This case study analyzes the accounting information system of Adam & Co., focusing on its inventory management and cost management systems. The assignment provides flowcharts for the purchase, cash disbursement, and payroll systems, illustrating the processes within the company. It also identifies and discusses potential internal control weaknesses within these systems, such as inefficiencies in the management system and security risks within the payroll system. The analysis emphasizes the importance of strategic approaches and the need for constant monitoring and improvement in the expenditure cycle, including the implementation of machine learning tools for detecting potential threats. The study also highlights the role of supervisors in the payroll system and the need for automation to enhance business efficiency.

Running head: ACCOUNTING INFORMATION SYSTEM

ACCOUNTING INFORMATION SYSTEM

Name of the student:

Name of the university:

Author Note:

ACCOUNTING INFORMATION SYSTEM

Name of the student:

Name of the university:

Author Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING INFORMATION SYSTEM 1

Table of Contents

Introduction................................................................................................................................3

Discussions.................................................................................................................................3

Flowchart of the purchase system..........................................................................................3

Flowchart of Cash disbursement system................................................................................5

Flowchart of payroll system...................................................................................................6

Estimation of the Internal Control Weakness........................................................................7

Conclusion..................................................................................................................................9

References................................................................................................................................10

Table of Contents

Introduction................................................................................................................................3

Discussions.................................................................................................................................3

Flowchart of the purchase system..........................................................................................3

Flowchart of Cash disbursement system................................................................................5

Flowchart of payroll system...................................................................................................6

Estimation of the Internal Control Weakness........................................................................7

Conclusion..................................................................................................................................9

References................................................................................................................................10

2ACCOUNTING INFORMATION SYSTEM

Executive Summary

The current topic is concentrating on the flow chart of the entity along with the purchase

department, cash disbursement system and the payroll system of the entity. It is actually

important for the entity to identify the internal control weakness in the flow chart system and

also the various aspects which are associated with it are further taken into consideration in the

conducted study. Along with that the detailed analysis of the entity is performed and further

the loopholes or rather the weakness in the system has also been highlighted in this conducted

assignment.

Executive Summary

The current topic is concentrating on the flow chart of the entity along with the purchase

department, cash disbursement system and the payroll system of the entity. It is actually

important for the entity to identify the internal control weakness in the flow chart system and

also the various aspects which are associated with it are further taken into consideration in the

conducted study. Along with that the detailed analysis of the entity is performed and further

the loopholes or rather the weakness in the system has also been highlighted in this conducted

assignment.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ACCOUNTING INFORMATION SYSTEM

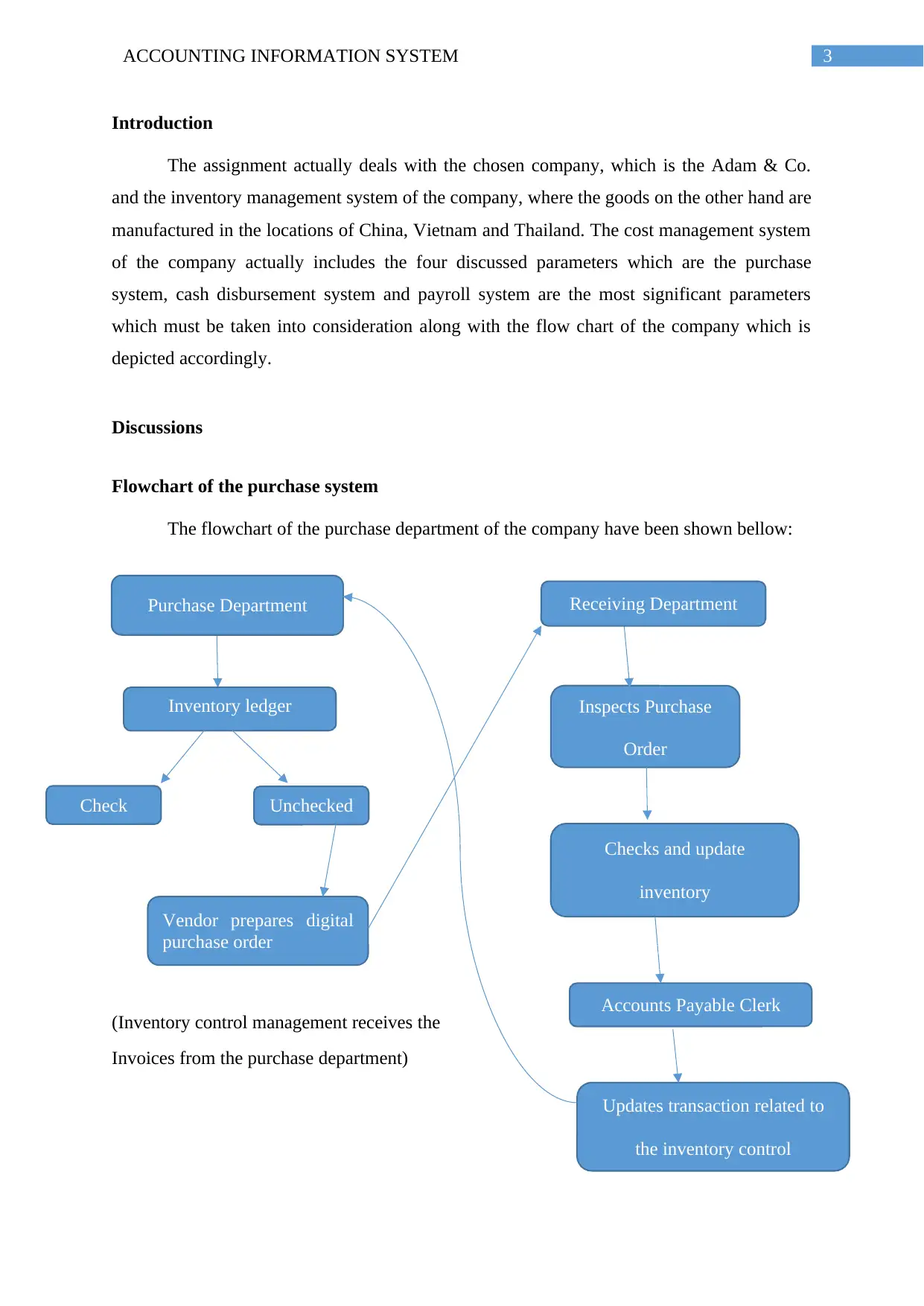

Introduction

The assignment actually deals with the chosen company, which is the Adam & Co.

and the inventory management system of the company, where the goods on the other hand are

manufactured in the locations of China, Vietnam and Thailand. The cost management system

of the company actually includes the four discussed parameters which are the purchase

system, cash disbursement system and payroll system are the most significant parameters

which must be taken into consideration along with the flow chart of the company which is

depicted accordingly.

Discussions

Flowchart of the purchase system

The flowchart of the purchase department of the company have been shown bellow:

(Inventory control management receives the

Invoices from the purchase department)

Inventory ledger

Check

Inspects Purchase

Order

Checks and update

inventory

Accounts Payable Clerk

Updates transaction related to

the inventory control

Purchase Department Receiving Department

Unchecked

Vendor prepares digital

purchase order

Introduction

The assignment actually deals with the chosen company, which is the Adam & Co.

and the inventory management system of the company, where the goods on the other hand are

manufactured in the locations of China, Vietnam and Thailand. The cost management system

of the company actually includes the four discussed parameters which are the purchase

system, cash disbursement system and payroll system are the most significant parameters

which must be taken into consideration along with the flow chart of the company which is

depicted accordingly.

Discussions

Flowchart of the purchase system

The flowchart of the purchase department of the company have been shown bellow:

(Inventory control management receives the

Invoices from the purchase department)

Inventory ledger

Check

Inspects Purchase

Order

Checks and update

inventory

Accounts Payable Clerk

Updates transaction related to

the inventory control

Purchase Department Receiving Department

Unchecked

Vendor prepares digital

purchase order

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ACCOUNTING INFORMATION SYSTEM

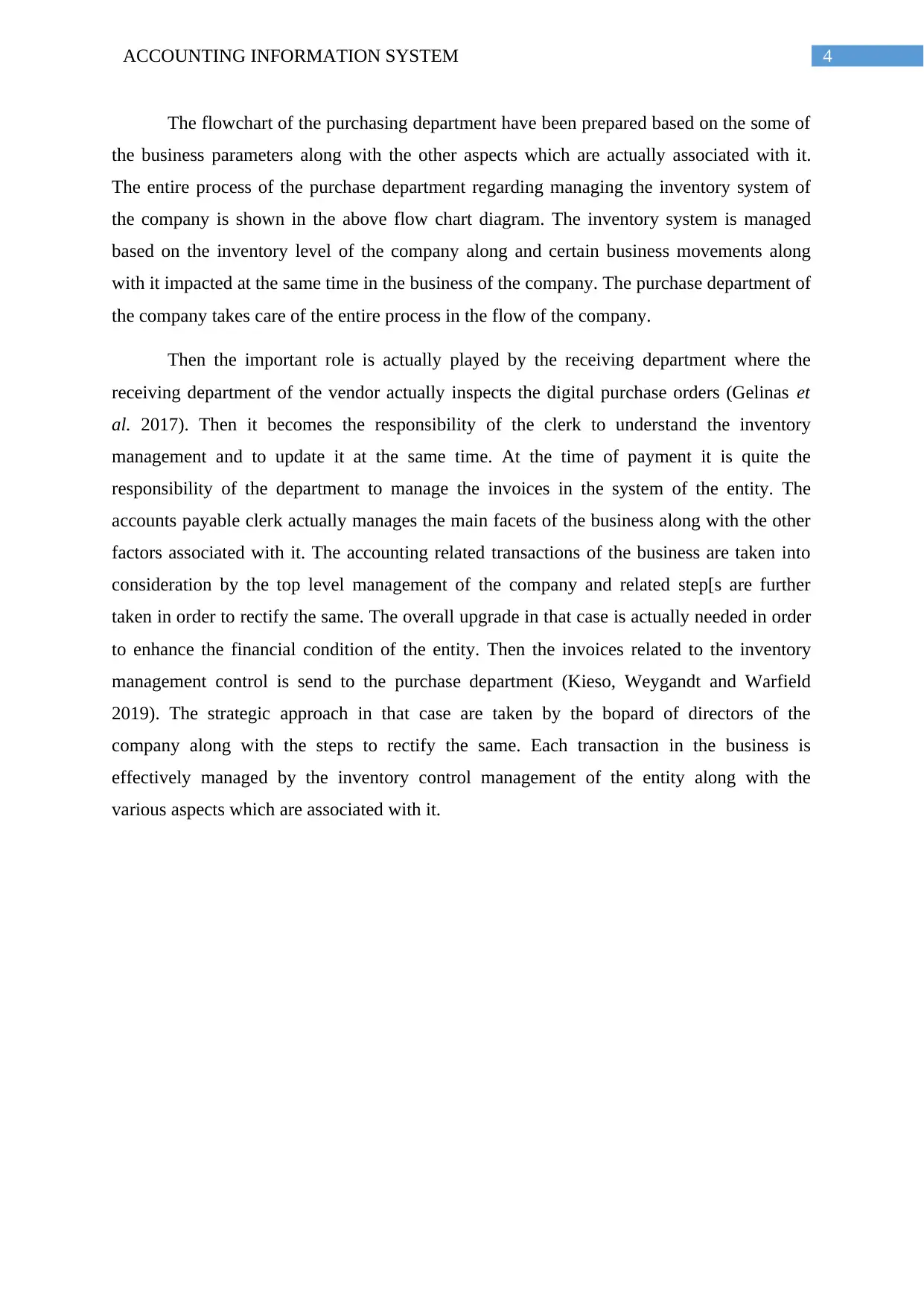

The flowchart of the purchasing department have been prepared based on the some of

the business parameters along with the other aspects which are actually associated with it.

The entire process of the purchase department regarding managing the inventory system of

the company is shown in the above flow chart diagram. The inventory system is managed

based on the inventory level of the company along and certain business movements along

with it impacted at the same time in the business of the company. The purchase department of

the company takes care of the entire process in the flow of the company.

Then the important role is actually played by the receiving department where the

receiving department of the vendor actually inspects the digital purchase orders (Gelinas et

al. 2017). Then it becomes the responsibility of the clerk to understand the inventory

management and to update it at the same time. At the time of payment it is quite the

responsibility of the department to manage the invoices in the system of the entity. The

accounts payable clerk actually manages the main facets of the business along with the other

factors associated with it. The accounting related transactions of the business are taken into

consideration by the top level management of the company and related step[s are further

taken in order to rectify the same. The overall upgrade in that case is actually needed in order

to enhance the financial condition of the entity. Then the invoices related to the inventory

management control is send to the purchase department (Kieso, Weygandt and Warfield

2019). The strategic approach in that case are taken by the bopard of directors of the

company along with the steps to rectify the same. Each transaction in the business is

effectively managed by the inventory control management of the entity along with the

various aspects which are associated with it.

The flowchart of the purchasing department have been prepared based on the some of

the business parameters along with the other aspects which are actually associated with it.

The entire process of the purchase department regarding managing the inventory system of

the company is shown in the above flow chart diagram. The inventory system is managed

based on the inventory level of the company along and certain business movements along

with it impacted at the same time in the business of the company. The purchase department of

the company takes care of the entire process in the flow of the company.

Then the important role is actually played by the receiving department where the

receiving department of the vendor actually inspects the digital purchase orders (Gelinas et

al. 2017). Then it becomes the responsibility of the clerk to understand the inventory

management and to update it at the same time. At the time of payment it is quite the

responsibility of the department to manage the invoices in the system of the entity. The

accounts payable clerk actually manages the main facets of the business along with the other

factors associated with it. The accounting related transactions of the business are taken into

consideration by the top level management of the company and related step[s are further

taken in order to rectify the same. The overall upgrade in that case is actually needed in order

to enhance the financial condition of the entity. Then the invoices related to the inventory

management control is send to the purchase department (Kieso, Weygandt and Warfield

2019). The strategic approach in that case are taken by the bopard of directors of the

company along with the steps to rectify the same. Each transaction in the business is

effectively managed by the inventory control management of the entity along with the

various aspects which are associated with it.

5ACCOUNTING INFORMATION SYSTEM

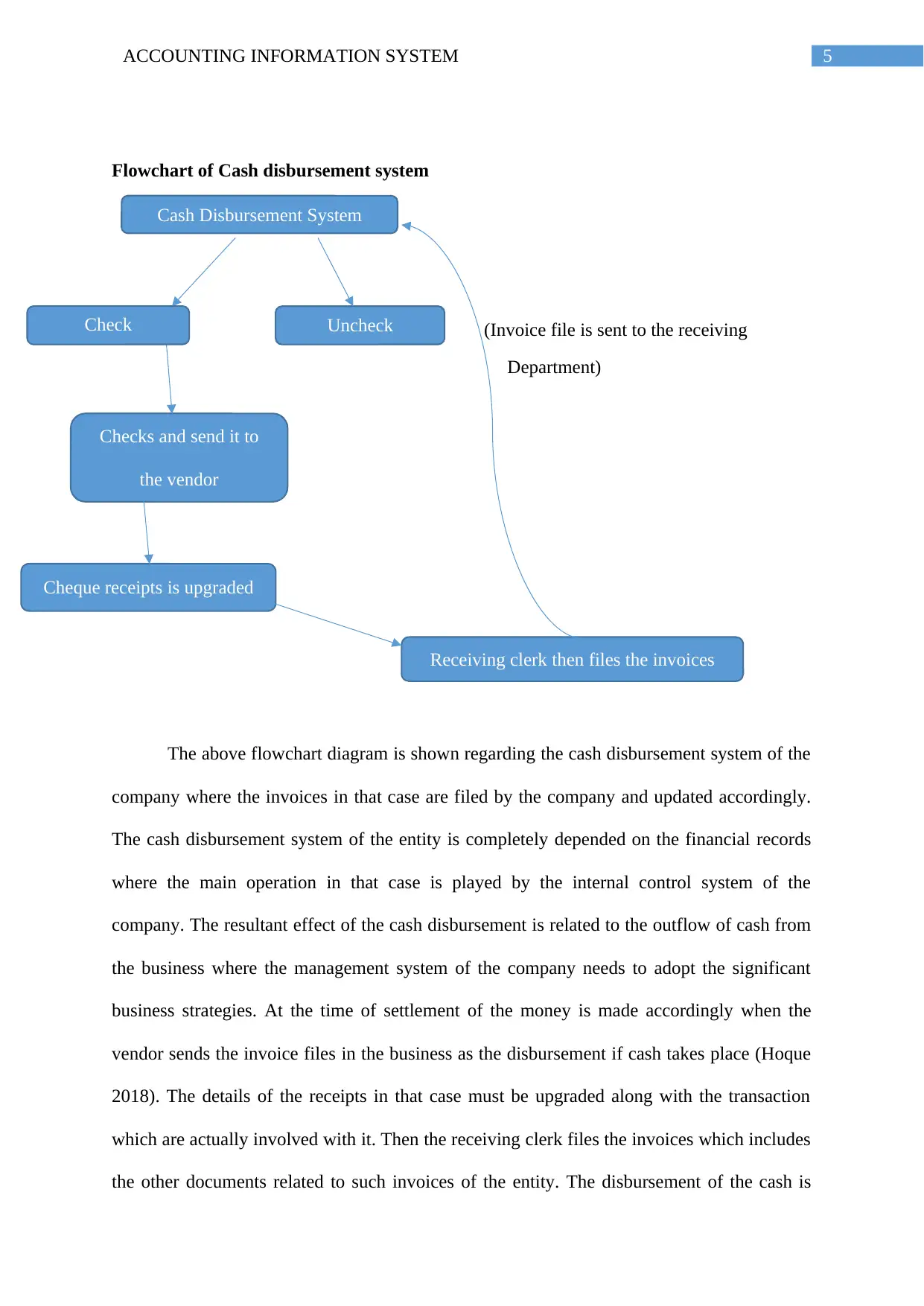

Flowchart of Cash disbursement system

(Invoice file is sent to the receiving

Department)

The above flowchart diagram is shown regarding the cash disbursement system of the

company where the invoices in that case are filed by the company and updated accordingly.

The cash disbursement system of the entity is completely depended on the financial records

where the main operation in that case is played by the internal control system of the

company. The resultant effect of the cash disbursement is related to the outflow of cash from

the business where the management system of the company needs to adopt the significant

business strategies. At the time of settlement of the money is made accordingly when the

vendor sends the invoice files in the business as the disbursement if cash takes place (Hoque

2018). The details of the receipts in that case must be upgraded along with the transaction

which are actually involved with it. Then the receiving clerk files the invoices which includes

the other documents related to such invoices of the entity. The disbursement of the cash is

Checks and send it to

the vendor

Cheque receipts is upgraded

Receiving clerk then files the invoices

Cash Disbursement System

Check Uncheck

Flowchart of Cash disbursement system

(Invoice file is sent to the receiving

Department)

The above flowchart diagram is shown regarding the cash disbursement system of the

company where the invoices in that case are filed by the company and updated accordingly.

The cash disbursement system of the entity is completely depended on the financial records

where the main operation in that case is played by the internal control system of the

company. The resultant effect of the cash disbursement is related to the outflow of cash from

the business where the management system of the company needs to adopt the significant

business strategies. At the time of settlement of the money is made accordingly when the

vendor sends the invoice files in the business as the disbursement if cash takes place (Hoque

2018). The details of the receipts in that case must be upgraded along with the transaction

which are actually involved with it. Then the receiving clerk files the invoices which includes

the other documents related to such invoices of the entity. The disbursement of the cash is

Checks and send it to

the vendor

Cheque receipts is upgraded

Receiving clerk then files the invoices

Cash Disbursement System

Check Uncheck

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ACCOUNTING INFORMATION SYSTEM

then prepared and further the purchase order copy along with the receiving report is send to

the purchase department from whim the material is obtained (Smith 2017). After the

disbursement of the cash, it is quite important for the entity to keep the relevant records and

verify the relevant transaction which took place in the business along with the impact of it in

the organization.

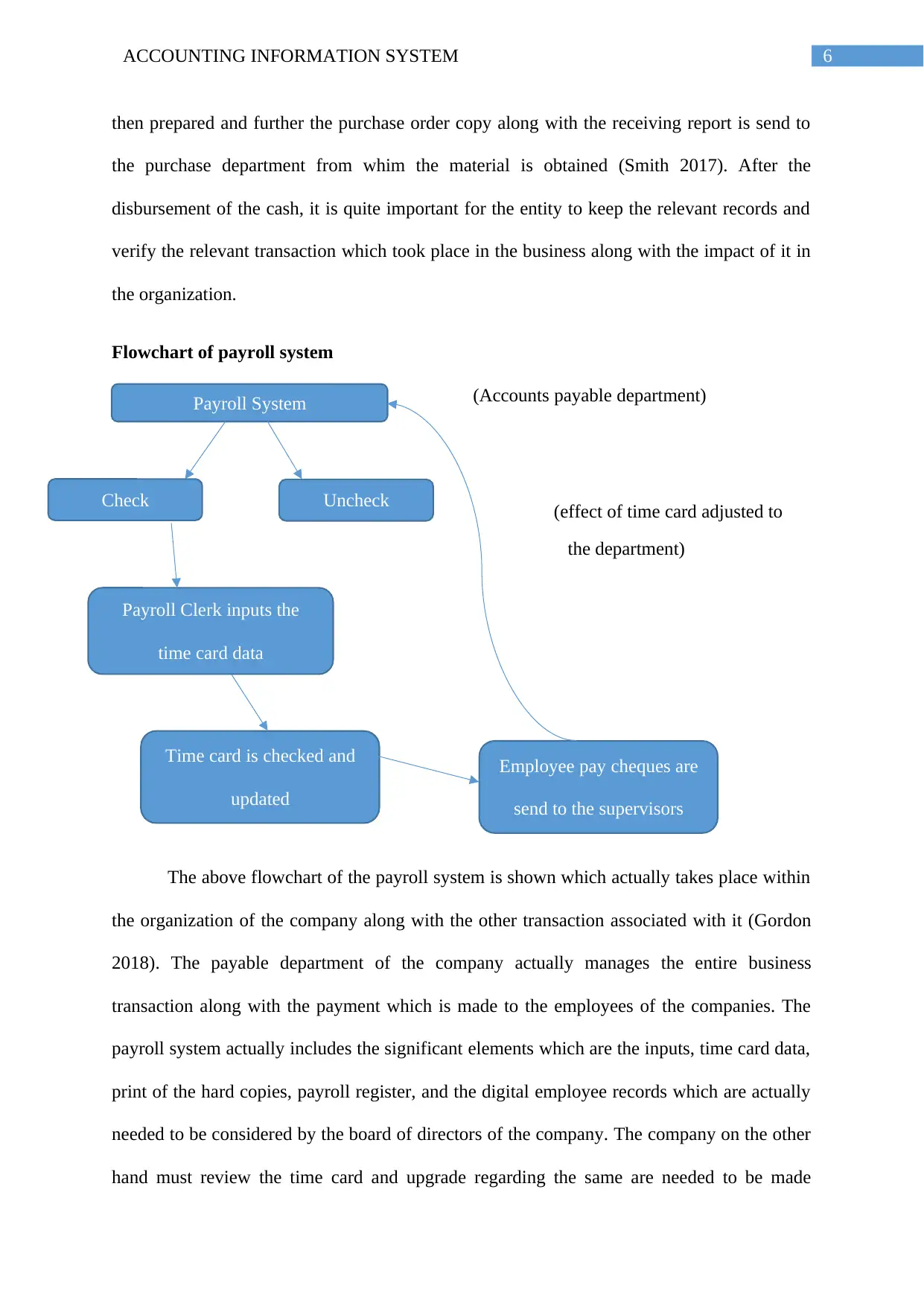

Flowchart of payroll system

(Accounts payable department)

(effect of time card adjusted to

the department)

The above flowchart of the payroll system is shown which actually takes place within

the organization of the company along with the other transaction associated with it (Gordon

2018). The payable department of the company actually manages the entire business

transaction along with the payment which is made to the employees of the companies. The

payroll system actually includes the significant elements which are the inputs, time card data,

print of the hard copies, payroll register, and the digital employee records which are actually

needed to be considered by the board of directors of the company. The company on the other

hand must review the time card and upgrade regarding the same are needed to be made

Payroll Clerk inputs the

time card data

Time card is checked and

updated

Employee pay cheques are

send to the supervisors

Payroll System

Check Uncheck

then prepared and further the purchase order copy along with the receiving report is send to

the purchase department from whim the material is obtained (Smith 2017). After the

disbursement of the cash, it is quite important for the entity to keep the relevant records and

verify the relevant transaction which took place in the business along with the impact of it in

the organization.

Flowchart of payroll system

(Accounts payable department)

(effect of time card adjusted to

the department)

The above flowchart of the payroll system is shown which actually takes place within

the organization of the company along with the other transaction associated with it (Gordon

2018). The payable department of the company actually manages the entire business

transaction along with the payment which is made to the employees of the companies. The

payroll system actually includes the significant elements which are the inputs, time card data,

print of the hard copies, payroll register, and the digital employee records which are actually

needed to be considered by the board of directors of the company. The company on the other

hand must review the time card and upgrade regarding the same are needed to be made

Payroll Clerk inputs the

time card data

Time card is checked and

updated

Employee pay cheques are

send to the supervisors

Payroll System

Check Uncheck

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ACCOUNTING INFORMATION SYSTEM

accordingly (Maskell, Baggaley and Grasso 2017). At the end the pay checks on the other

hand are sent to the supervisors of the company along with the potential information which

are associated with it. The payroll system of the company is then sent the files to the upper

level management of the company for further update of the same.

Estimation of the Internal Control Weakness

The weakness in the internal control system of the company is actually related to the

inefficiency in the management system of the company. The fluctuation in the management

system of the company also needed to be taken into consideration by the management system

along with the other parameters which are involved in that case (Hoyle, Schaefer and

Doupnik 2015). The potential glitches and threat in the system must be taken care of by

internal management of the entity and accordingly the significant steps are needed to be

taken. There are threats regarding the security related risk in the business and tit is the

responsibility of the management heads to mitigate the risk in the business.

The clusters of the payroll system of the company is not effective enough to mitigate

the potential risks and threats involved in that case. Security plays a significant role in the

business of the entity as it also ensures the effectiveness in the business operation, which is

actually conducted within the entity. If the head of the management manages the system or

rather it is needed to upgrade the entire system of the payroll department then certain steps in

that case are needed to be taken. Based on the presentation of the flowcharts in case of every

system which are the purchase department, cash disbursement and payroll system of the

entity (Kranacher and Riley 2019). The functions of each and every departments are different

along with that it is the duty of the upper level management of the entity to decentralize the

entire system. The record of each and every system must be taken care of by the management

and further responsibilities in that case are embedded on the departmental head of the

business.

accordingly (Maskell, Baggaley and Grasso 2017). At the end the pay checks on the other

hand are sent to the supervisors of the company along with the potential information which

are associated with it. The payroll system of the company is then sent the files to the upper

level management of the company for further update of the same.

Estimation of the Internal Control Weakness

The weakness in the internal control system of the company is actually related to the

inefficiency in the management system of the company. The fluctuation in the management

system of the company also needed to be taken into consideration by the management system

along with the other parameters which are involved in that case (Hoyle, Schaefer and

Doupnik 2015). The potential glitches and threat in the system must be taken care of by

internal management of the entity and accordingly the significant steps are needed to be

taken. There are threats regarding the security related risk in the business and tit is the

responsibility of the management heads to mitigate the risk in the business.

The clusters of the payroll system of the company is not effective enough to mitigate

the potential risks and threats involved in that case. Security plays a significant role in the

business of the entity as it also ensures the effectiveness in the business operation, which is

actually conducted within the entity. If the head of the management manages the system or

rather it is needed to upgrade the entire system of the payroll department then certain steps in

that case are needed to be taken. Based on the presentation of the flowcharts in case of every

system which are the purchase department, cash disbursement and payroll system of the

entity (Kranacher and Riley 2019). The functions of each and every departments are different

along with that it is the duty of the upper level management of the entity to decentralize the

entire system. The record of each and every system must be taken care of by the management

and further responsibilities in that case are embedded on the departmental head of the

business.

8ACCOUNTING INFORMATION SYSTEM

In case of internal weakness within the system it is needed by the entity to understand

the facts, which are associated with the potential business loopholes, and to solve it with the

help of the critical analytical approach which must be adopted by the entity. The internal

control in the expenditure cycle must be optimized in an interval basis and accordingly the

top-level management of the entity must take the decisions (Laudon and Laudon 2016). The

facts and figures must be considered by the company at time of evaluating the potential

business facets The relevant tools and techniques in that case are needed by the entity in order

to understand or rather calibrate the facts and figures associated with the potential facets of

the business. The various kinds of the internal weakness of risk, which are associated with the

entity, are the technical, operational, administrative and architectural control regarding the

weakness of the entity (Libby 2017).

The parameters of the risk management must be taken into consideration along with

that the changes in the system of the company must be made accordingly. On the other hand

actually supports the relevant facts associated with the entity along with the various business

impact of the entity based on the objectives of the firm. The current flow regarding the

expenditure cycle, which is adopted by the entity, are taken care of by the management

system which is quite perfect (Schaltegger and Burritt 2017). The reason behind that is the

entity maintains the flow in the system of the entity as it is producing a positive impact in the

business of the entity based on the long run objectives. The another significant facets is that

the organization needs to constantly monitor the expenditure control and implementation of

the machine learning tools will further help the management to detect the malware and the

ransom ware in the system (Kaplan and Atkinson 2015). In case of any potential changes,

which must further be taken care of by the management, system of the company and the

potential weakness in the system must be altered. The policies and strategies regarding the

In case of internal weakness within the system it is needed by the entity to understand

the facts, which are associated with the potential business loopholes, and to solve it with the

help of the critical analytical approach which must be adopted by the entity. The internal

control in the expenditure cycle must be optimized in an interval basis and accordingly the

top-level management of the entity must take the decisions (Laudon and Laudon 2016). The

facts and figures must be considered by the company at time of evaluating the potential

business facets The relevant tools and techniques in that case are needed by the entity in order

to understand or rather calibrate the facts and figures associated with the potential facets of

the business. The various kinds of the internal weakness of risk, which are associated with the

entity, are the technical, operational, administrative and architectural control regarding the

weakness of the entity (Libby 2017).

The parameters of the risk management must be taken into consideration along with

that the changes in the system of the company must be made accordingly. On the other hand

actually supports the relevant facts associated with the entity along with the various business

impact of the entity based on the objectives of the firm. The current flow regarding the

expenditure cycle, which is adopted by the entity, are taken care of by the management

system which is quite perfect (Schaltegger and Burritt 2017). The reason behind that is the

entity maintains the flow in the system of the entity as it is producing a positive impact in the

business of the entity based on the long run objectives. The another significant facets is that

the organization needs to constantly monitor the expenditure control and implementation of

the machine learning tools will further help the management to detect the malware and the

ransom ware in the system (Kaplan and Atkinson 2015). In case of any potential changes,

which must further be taken care of by the management, system of the company and the

potential weakness in the system must be altered. The policies and strategies regarding the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ACCOUNTING INFORMATION SYSTEM

expenditure cycle of the company must be made adopted by the company with the systematic

approach associated with it.

In case of the expenditure cycle of the entity it is actually needed by the entity to

secure the transaction related data so that the security realted facts of the company can be

taken into consideration. The payroll system of the entity includes the payment structure

which must be revised by the company and the supervisors in that case plays the significant

business role (Lara, Osma and Penalva 2016). In case of any manipulation within the system

of the entity it is quite important for the supervisors of the entity to report it to the top level

management of the entity along with the other business parameters which are associated in

that case. The internal control system of the entity must be automated so that the entity will

be able to enhance the efficiency of the business based on the long-term approach of the

entity. At the time of audit of the entity it is quite needed by the entity to adopt the strategies

in the system so that the business of the entity is free from the material misstatement or

frauds which actually takes place in the business (Prasad and Green 2015).

Conclusion

From the above discussion it can be concluded that the flowchart of the Adam and Co.

has been prepared and the potential risk along with threats in the business of the company

must be identified by the company. The data of the company must be updated at the time

along with the other factors which are associated in the business of the company. Based on

the criticality of the analysis it is quite noticeable that the preparation of the flowchart will

help the management system of the entity to get into the right track in the business. The

implementation in the operations of the entity will further help the business to accomplish the

main objectives. On the other hand the internal control weakness of the entity have been

expenditure cycle of the company must be made adopted by the company with the systematic

approach associated with it.

In case of the expenditure cycle of the entity it is actually needed by the entity to

secure the transaction related data so that the security realted facts of the company can be

taken into consideration. The payroll system of the entity includes the payment structure

which must be revised by the company and the supervisors in that case plays the significant

business role (Lara, Osma and Penalva 2016). In case of any manipulation within the system

of the entity it is quite important for the supervisors of the entity to report it to the top level

management of the entity along with the other business parameters which are associated in

that case. The internal control system of the entity must be automated so that the entity will

be able to enhance the efficiency of the business based on the long-term approach of the

entity. At the time of audit of the entity it is quite needed by the entity to adopt the strategies

in the system so that the business of the entity is free from the material misstatement or

frauds which actually takes place in the business (Prasad and Green 2015).

Conclusion

From the above discussion it can be concluded that the flowchart of the Adam and Co.

has been prepared and the potential risk along with threats in the business of the company

must be identified by the company. The data of the company must be updated at the time

along with the other factors which are associated in the business of the company. Based on

the criticality of the analysis it is quite noticeable that the preparation of the flowchart will

help the management system of the entity to get into the right track in the business. The

implementation in the operations of the entity will further help the business to accomplish the

main objectives. On the other hand the internal control weakness of the entity have been

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ACCOUNTING INFORMATION SYSTEM

highlighted which is less and further changes regarding the same have highlighted in the

conducted study.

References

Duska, R.F., Duska, B.S. and Kury, K.W., 2018. Accounting ethics. Wiley-Blackwell.

Gelinas, U.J., Dull, R.B., Wheeler, P. and Hill, M.C., 2017. Accounting Information Systems.

Cengage Learning.

Gordon, S., 2018. Technology Advancement Influence in Accounting and Information

System Fields.

Hoque, Z., 2018. Methodological issues in accounting research. Spiramus Press Ltd.

Hoyle, J.B., Schaefer, T. and Doupnik, T., 2015. Advanced accounting. McGraw Hill.

Kaplan, R.S. and Atkinson, A.A., 2015. Advanced management accounting. PHI Learning.

Kieso, D.E., Weygandt, J.J. and Warfield, T.D., 2019. Intermediate accounting. John Wiley

& Sons.

Kieso, D.E., Weygandt, J.J. and Warfield, T.D., 2019. Intermediate accounting. John Wiley

& Sons.

Kranacher, M.J. and Riley, R., 2019. Forensic accounting and fraud examination. John Wiley

& Sons.

highlighted which is less and further changes regarding the same have highlighted in the

conducted study.

References

Duska, R.F., Duska, B.S. and Kury, K.W., 2018. Accounting ethics. Wiley-Blackwell.

Gelinas, U.J., Dull, R.B., Wheeler, P. and Hill, M.C., 2017. Accounting Information Systems.

Cengage Learning.

Gordon, S., 2018. Technology Advancement Influence in Accounting and Information

System Fields.

Hoque, Z., 2018. Methodological issues in accounting research. Spiramus Press Ltd.

Hoyle, J.B., Schaefer, T. and Doupnik, T., 2015. Advanced accounting. McGraw Hill.

Kaplan, R.S. and Atkinson, A.A., 2015. Advanced management accounting. PHI Learning.

Kieso, D.E., Weygandt, J.J. and Warfield, T.D., 2019. Intermediate accounting. John Wiley

& Sons.

Kieso, D.E., Weygandt, J.J. and Warfield, T.D., 2019. Intermediate accounting. John Wiley

& Sons.

Kranacher, M.J. and Riley, R., 2019. Forensic accounting and fraud examination. John Wiley

& Sons.

11ACCOUNTING INFORMATION SYSTEM

Lara, J.M.G., Osma, B.G. and Penalva, F., 2016. Accounting conservatism and firm

investment efficiency. Journal of Accounting and Economics, 61(1), pp.221-238.

Laudon, K.C. and Laudon, J.P., 2016. Management information system. Pearson Education

India.

Libby, R., 2017. Accounting and human information processing. In The Routledge

Companion to Behavioural Accounting Research (pp. 42-54). Routledge.

Maskell, B.H., Baggaley, B. and Grasso, L., 2017. Practical lean accounting: a proven system

for measuring and managing the lean enterprise. Productivity Press.

Prasad, A. and Green, P., 2015. Organizational competencies and dynamic accounting

information system capability: impact on AIS processes and firm performance. Journal of

Information Systems, 29(3), pp.123-149.

Schaltegger, S. and Burritt, R., 2017. Contemporary environmental accounting: issues,

concepts and practice. Routledge.

Smith, M., 2017. Research methods in accounting. Sage.

Lara, J.M.G., Osma, B.G. and Penalva, F., 2016. Accounting conservatism and firm

investment efficiency. Journal of Accounting and Economics, 61(1), pp.221-238.

Laudon, K.C. and Laudon, J.P., 2016. Management information system. Pearson Education

India.

Libby, R., 2017. Accounting and human information processing. In The Routledge

Companion to Behavioural Accounting Research (pp. 42-54). Routledge.

Maskell, B.H., Baggaley, B. and Grasso, L., 2017. Practical lean accounting: a proven system

for measuring and managing the lean enterprise. Productivity Press.

Prasad, A. and Green, P., 2015. Organizational competencies and dynamic accounting

information system capability: impact on AIS processes and firm performance. Journal of

Information Systems, 29(3), pp.123-149.

Schaltegger, S. and Burritt, R., 2017. Contemporary environmental accounting: issues,

concepts and practice. Routledge.

Smith, M., 2017. Research methods in accounting. Sage.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.