ACC 566: Accounting System and Procedure: Detailed Analysis

VerifiedAdded on 2020/05/28

|23

|2794

|36

Homework Assignment

AI Summary

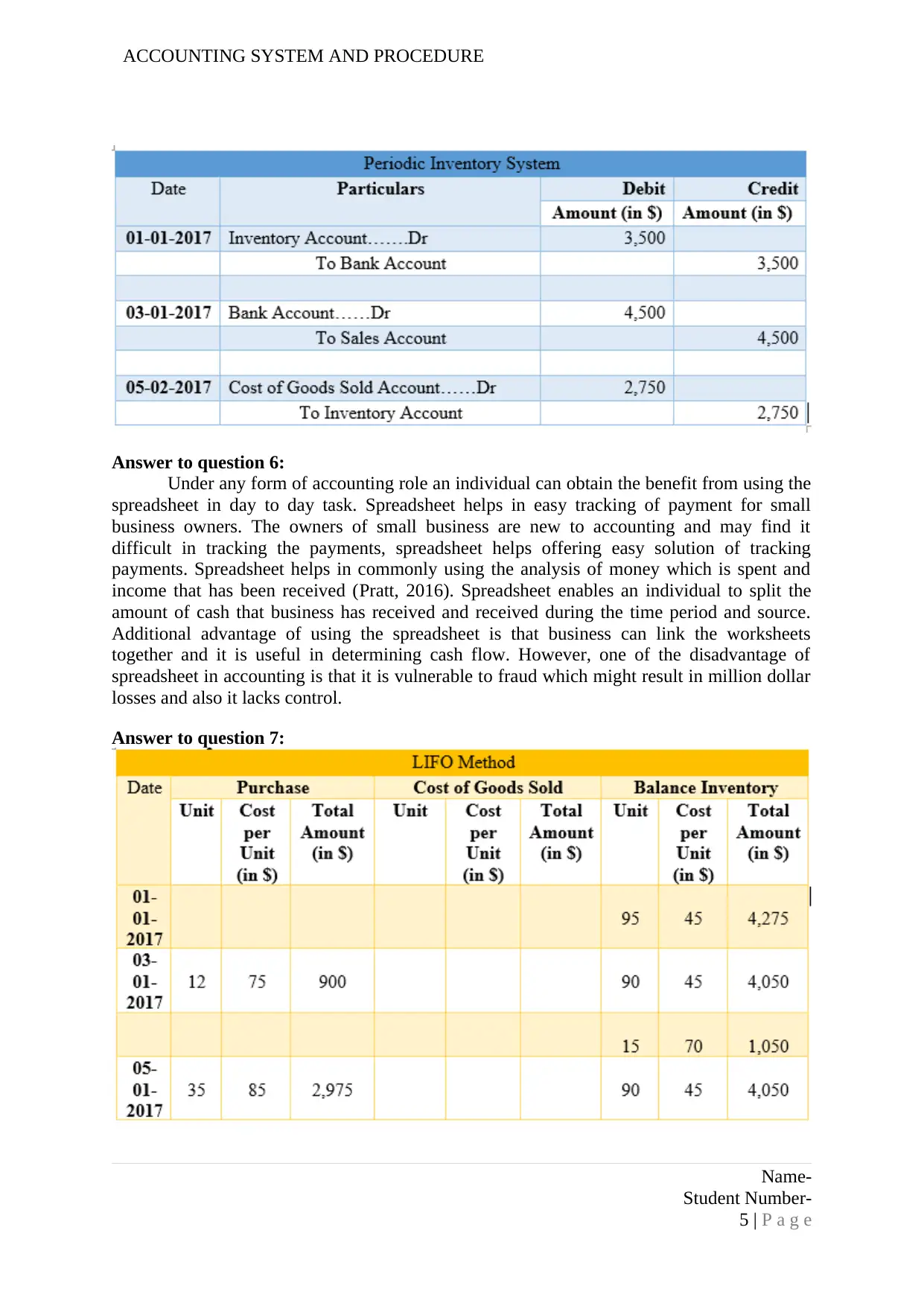

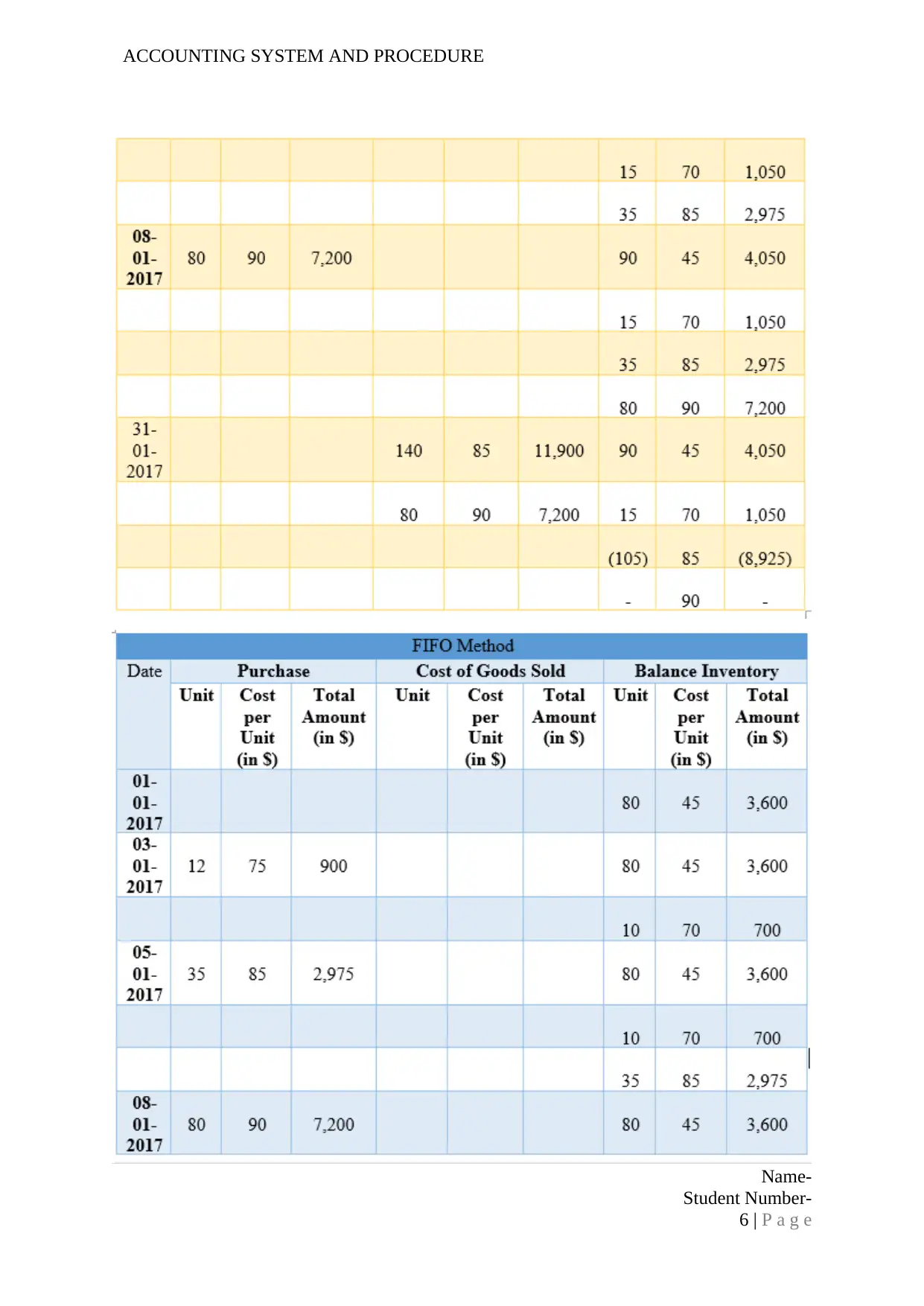

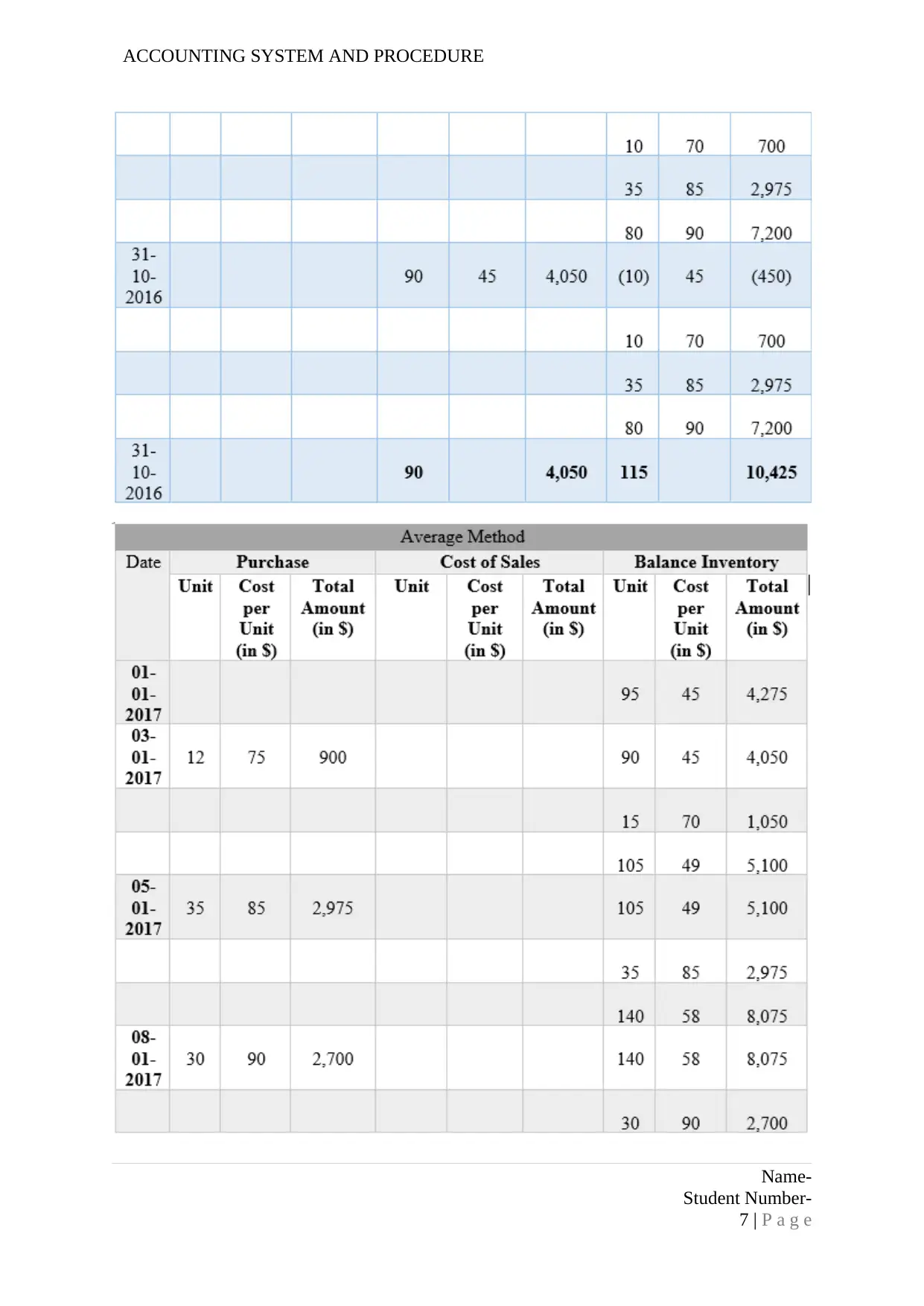

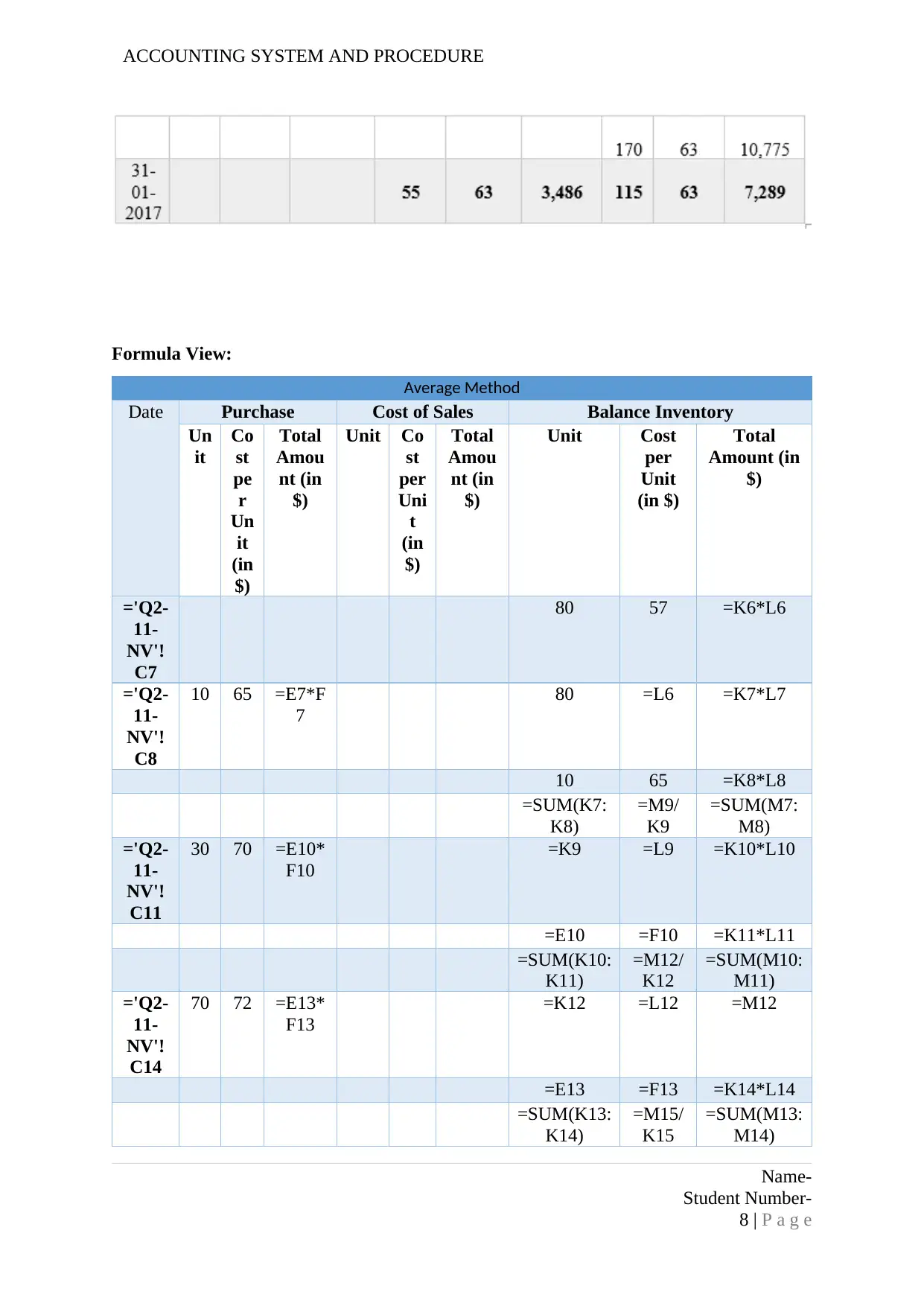

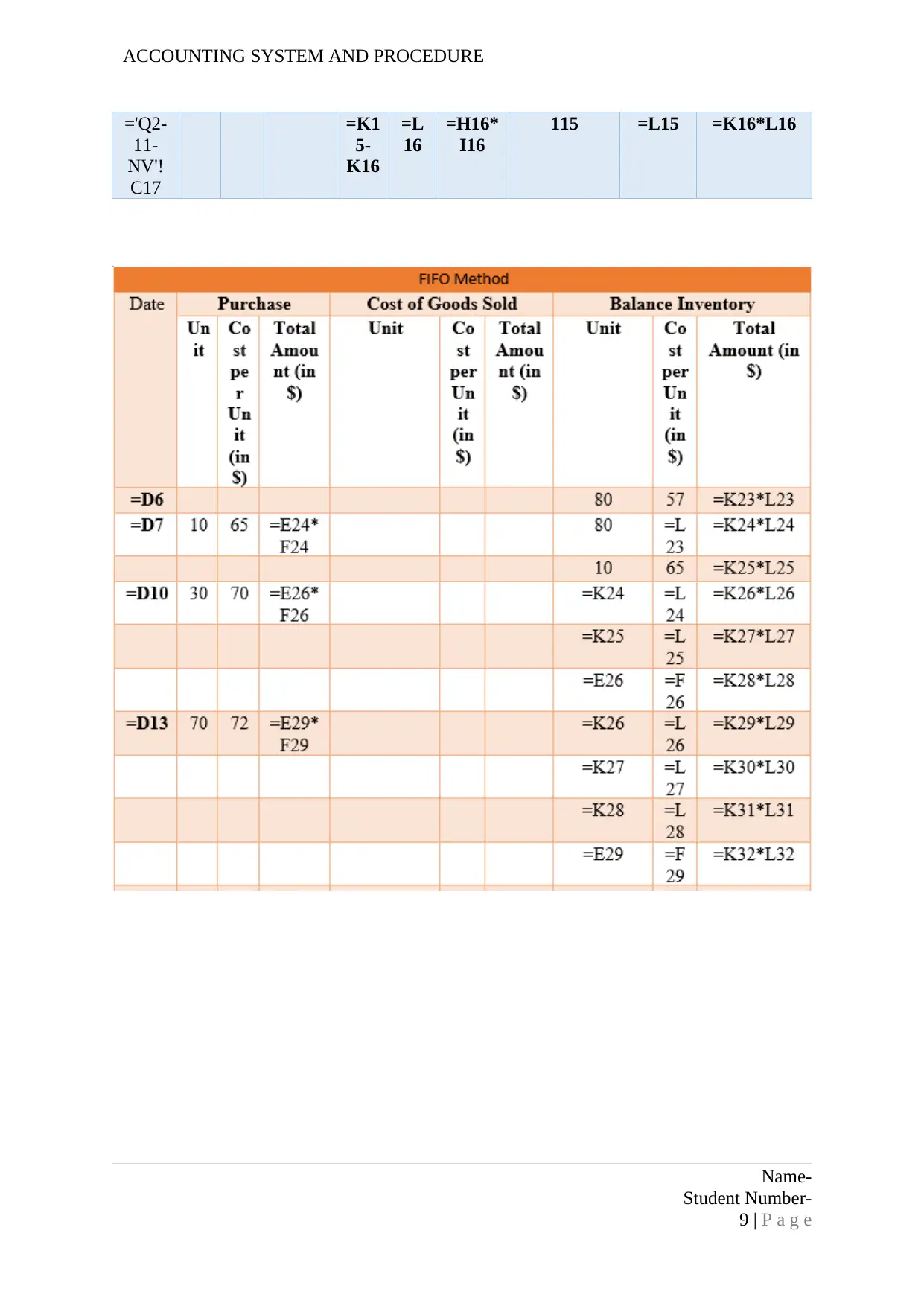

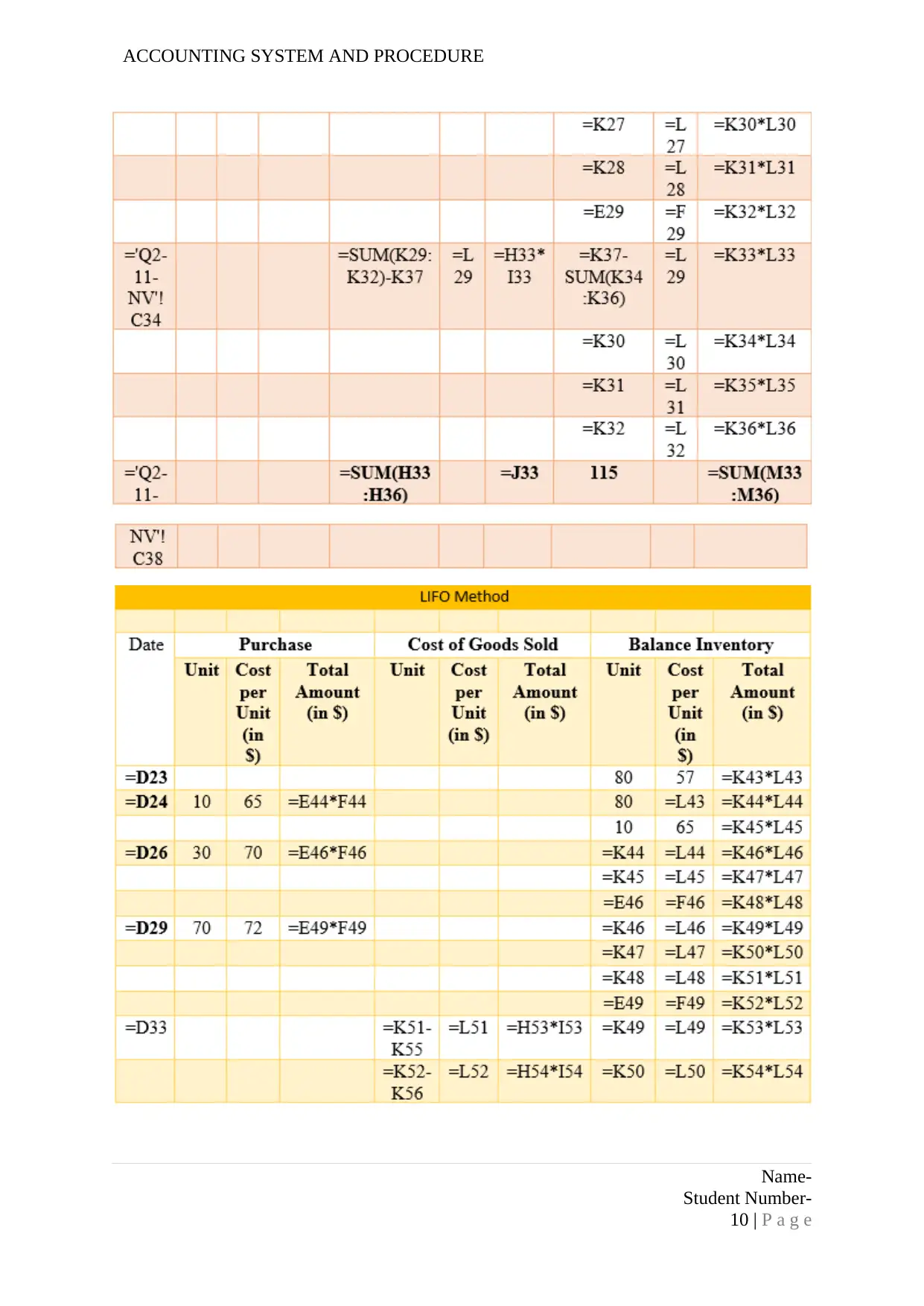

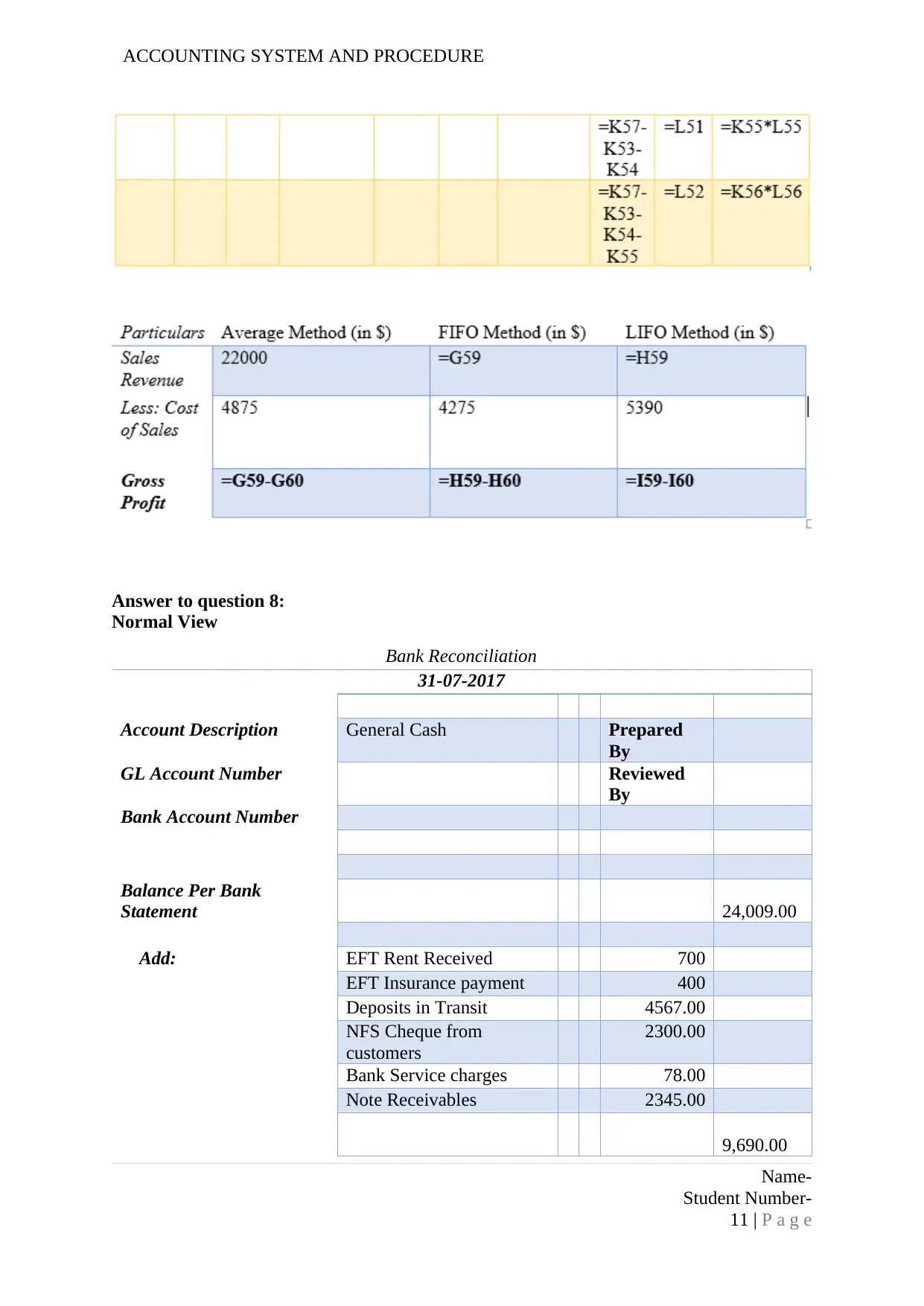

This assignment, prepared by a student, addresses various aspects of accounting systems and procedures. The solution begins with spreadsheet analysis, including the use of "IF" functions, and then delves into the differences between perpetual and periodic inventory systems. It covers how spreadsheets are used in accounting, including their advantages and disadvantages. The assignment includes a bank reconciliation exercise, providing both normal and formula views. Furthermore, it explores bad debt methods, comparing the direct write-off and allowance methods. The assignment also touches on the role of computers in online retailing and concludes with an analysis of the balance scorecard, using Qantas as a case study to evaluate its financial performance and non-current assets.

1 out of 23

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.