Accounting System and Process Assignment for Finance Students

VerifiedAdded on 2023/06/04

|19

|2548

|360

Homework Assignment

AI Summary

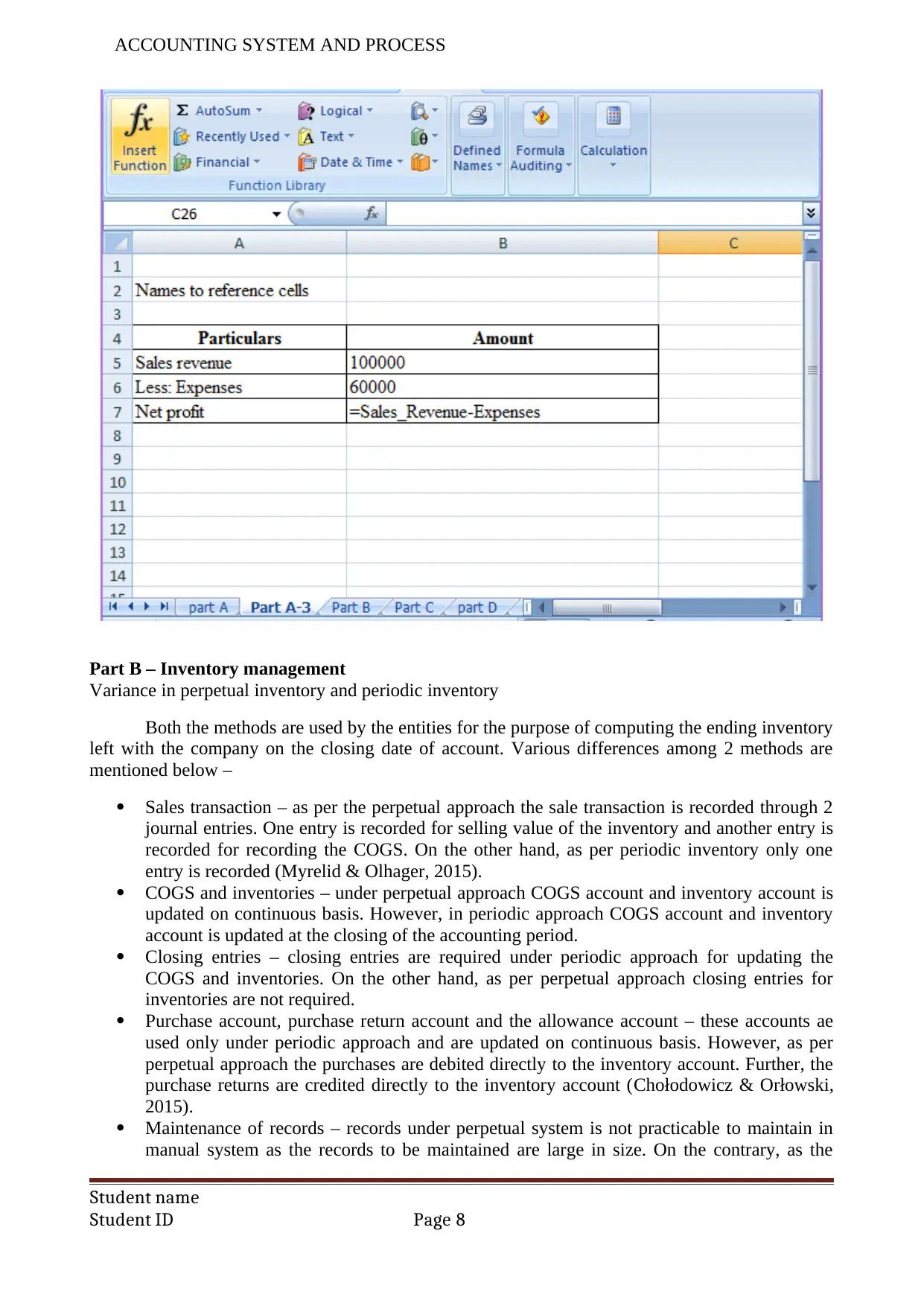

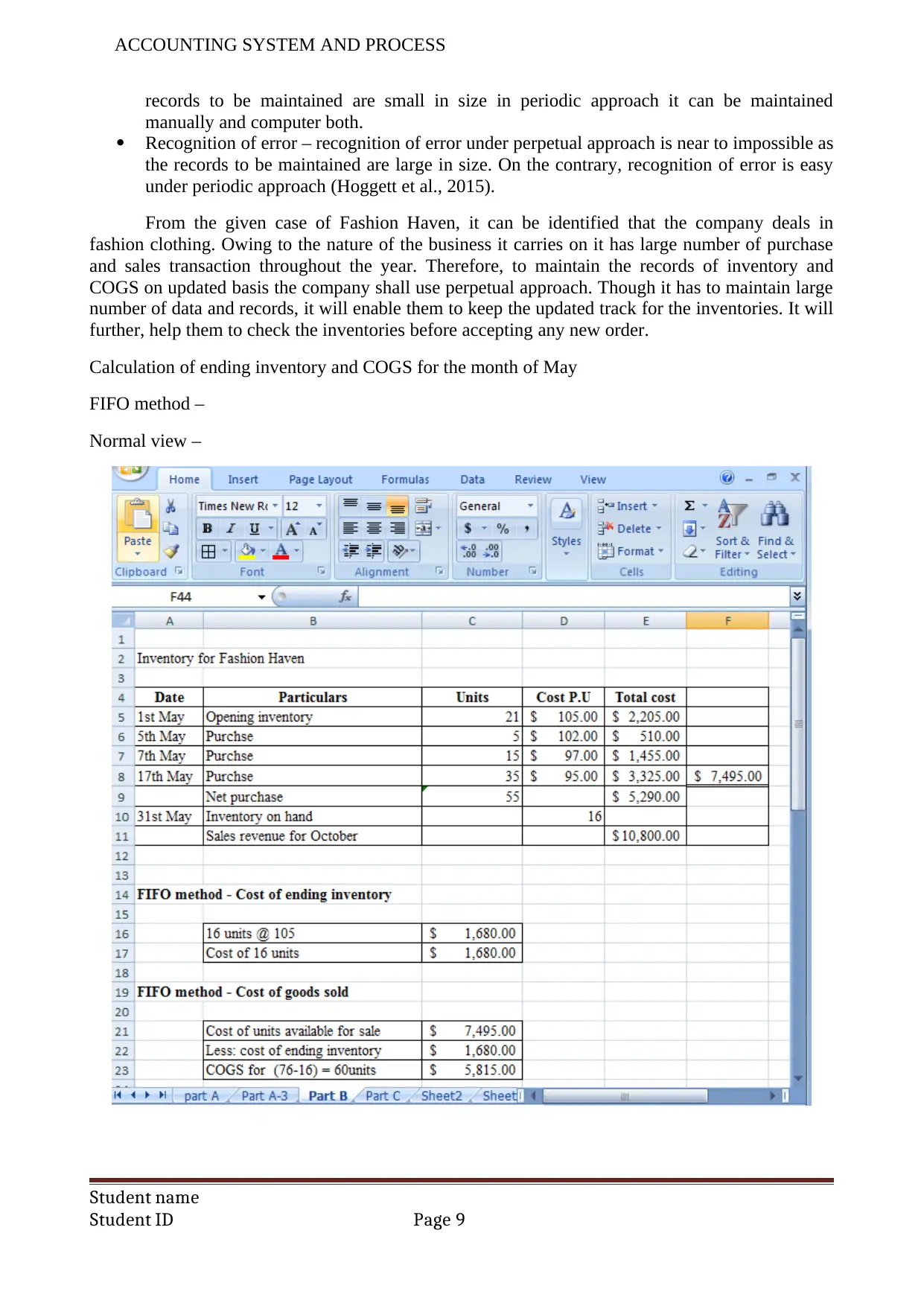

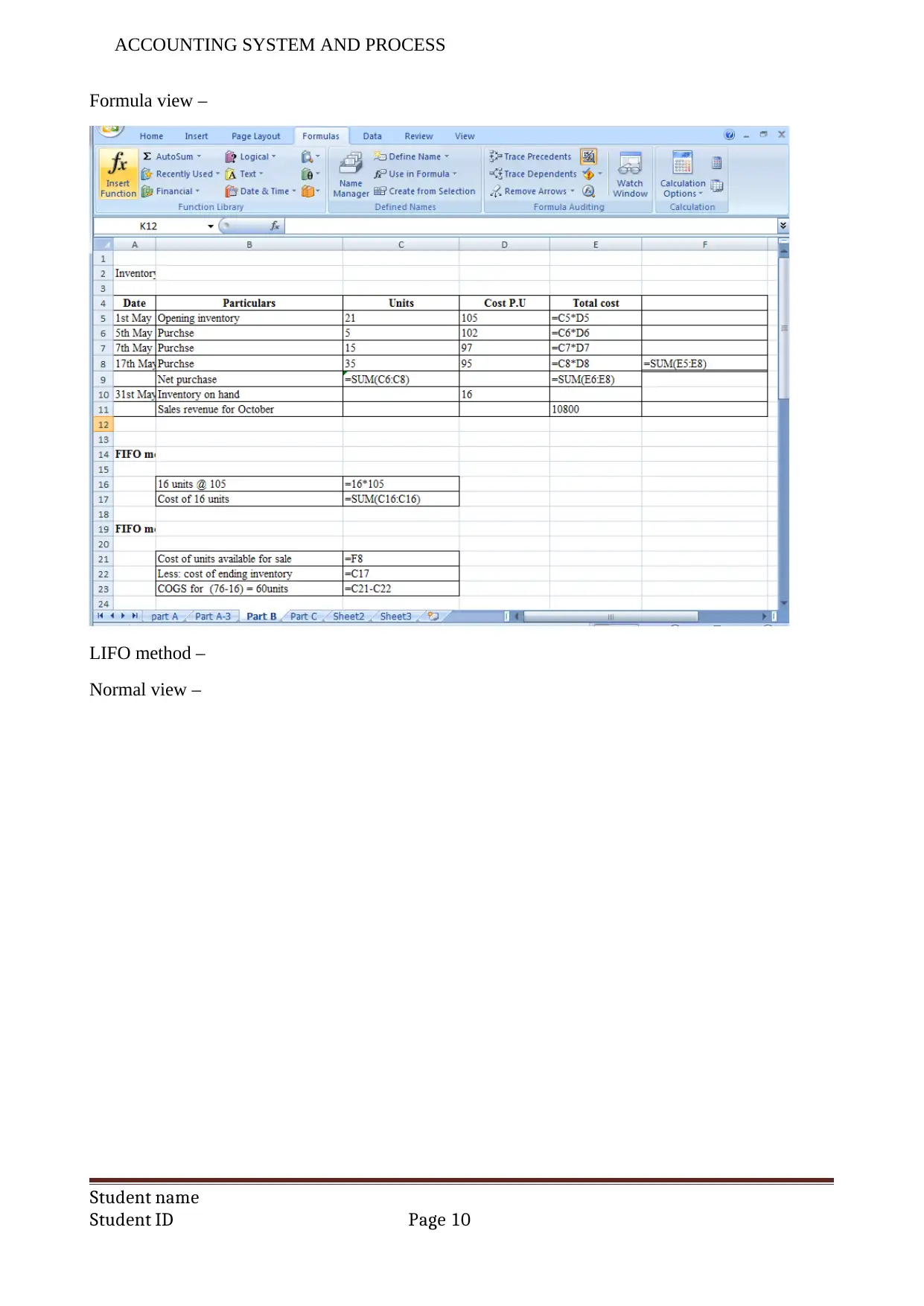

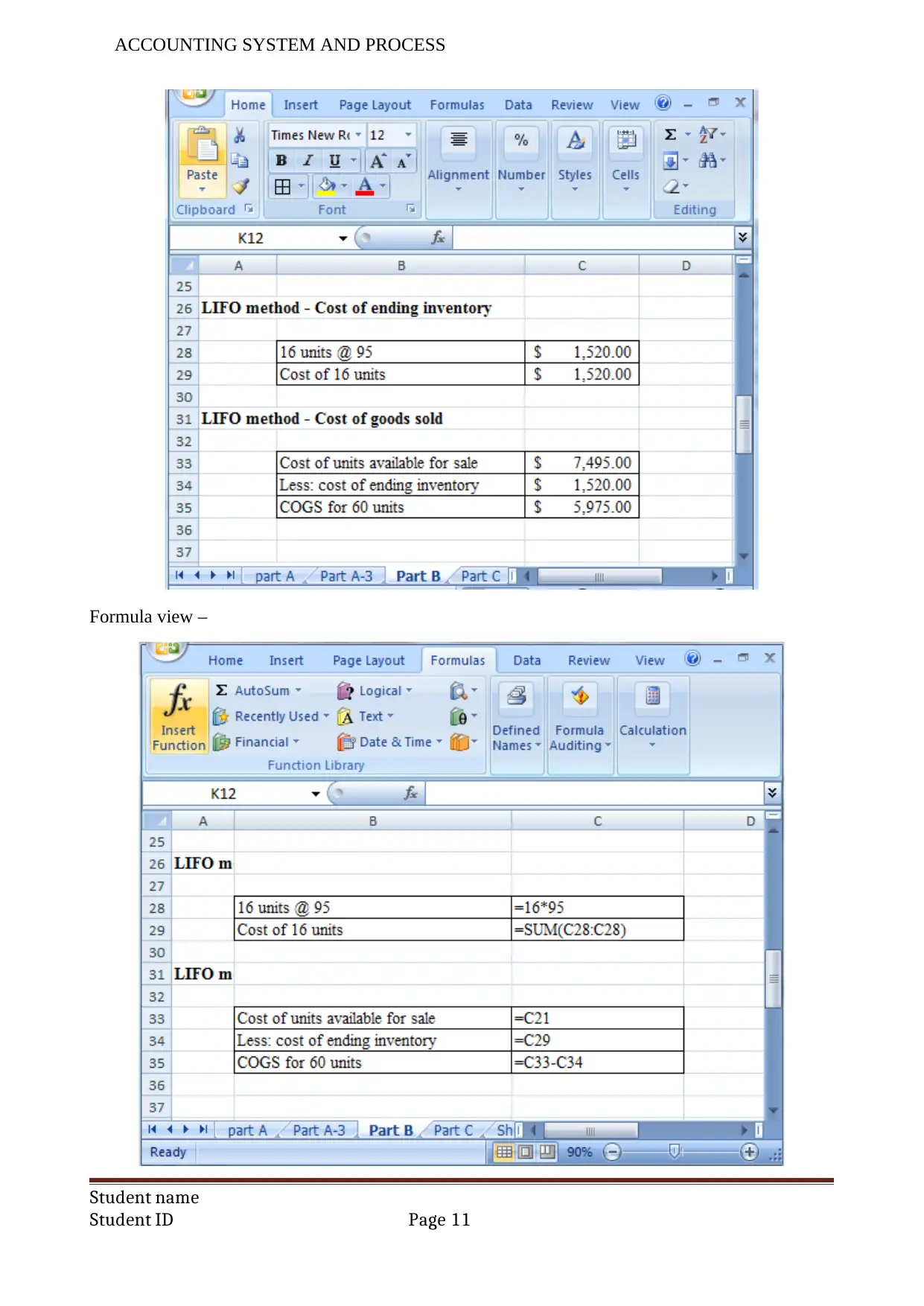

This accounting assignment solution provides a detailed analysis of various accounting concepts and processes. Part A focuses on the advantages and disadvantages of using spreadsheets in accounting, including data organization, computations, and security concerns. Part B delves into inventory management, comparing perpetual and periodic inventory systems, and applying FIFO, LIFO, and average cost methods to calculate ending inventory and cost of goods sold for Fashion Haven. Part C addresses bank reconciliation, including correcting bank errors and preparing journal entries. Finally, Part D explores bad debt management, comparing the allowance and write-off methods, and analyzing financial ratios (net profit, current, and debt-equity) and profitability charts to assess a company's financial performance and position, ultimately recommending investment decisions based on the analysis of Coca-Cola Amatil.

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.