Accounting Systems and Processes: Financial Analysis, A2 Milk Company

VerifiedAdded on 2023/04/20

|22

|3384

|234

Report

AI Summary

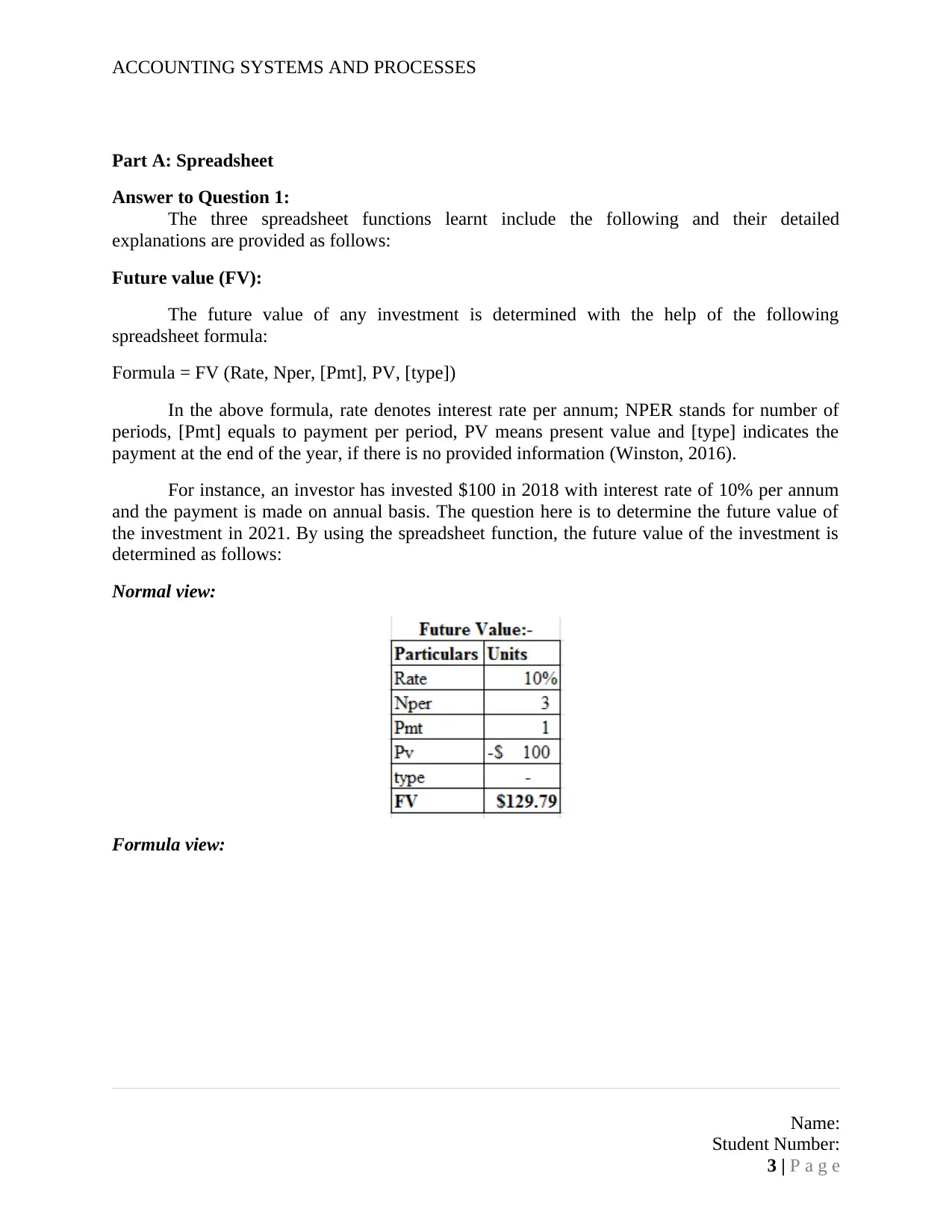

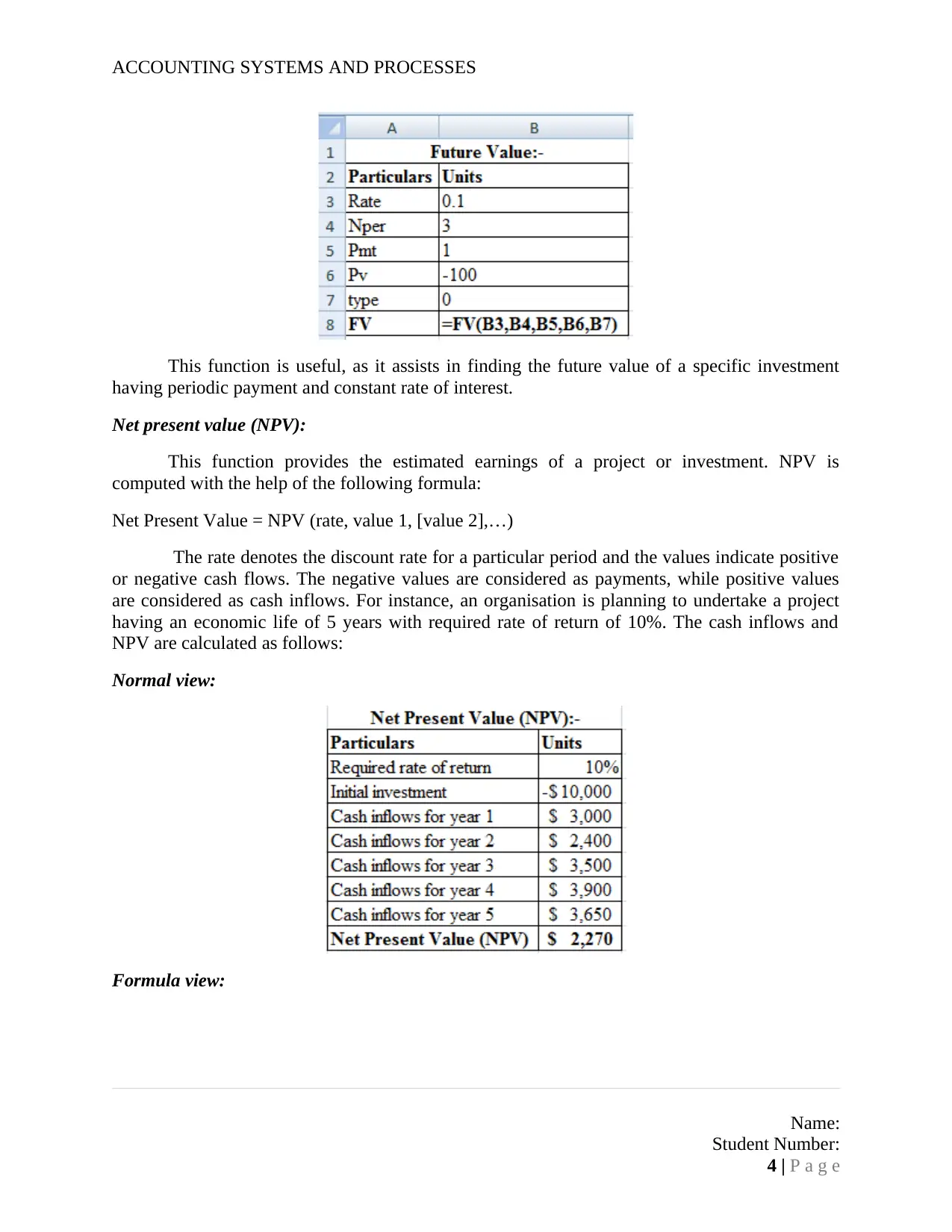

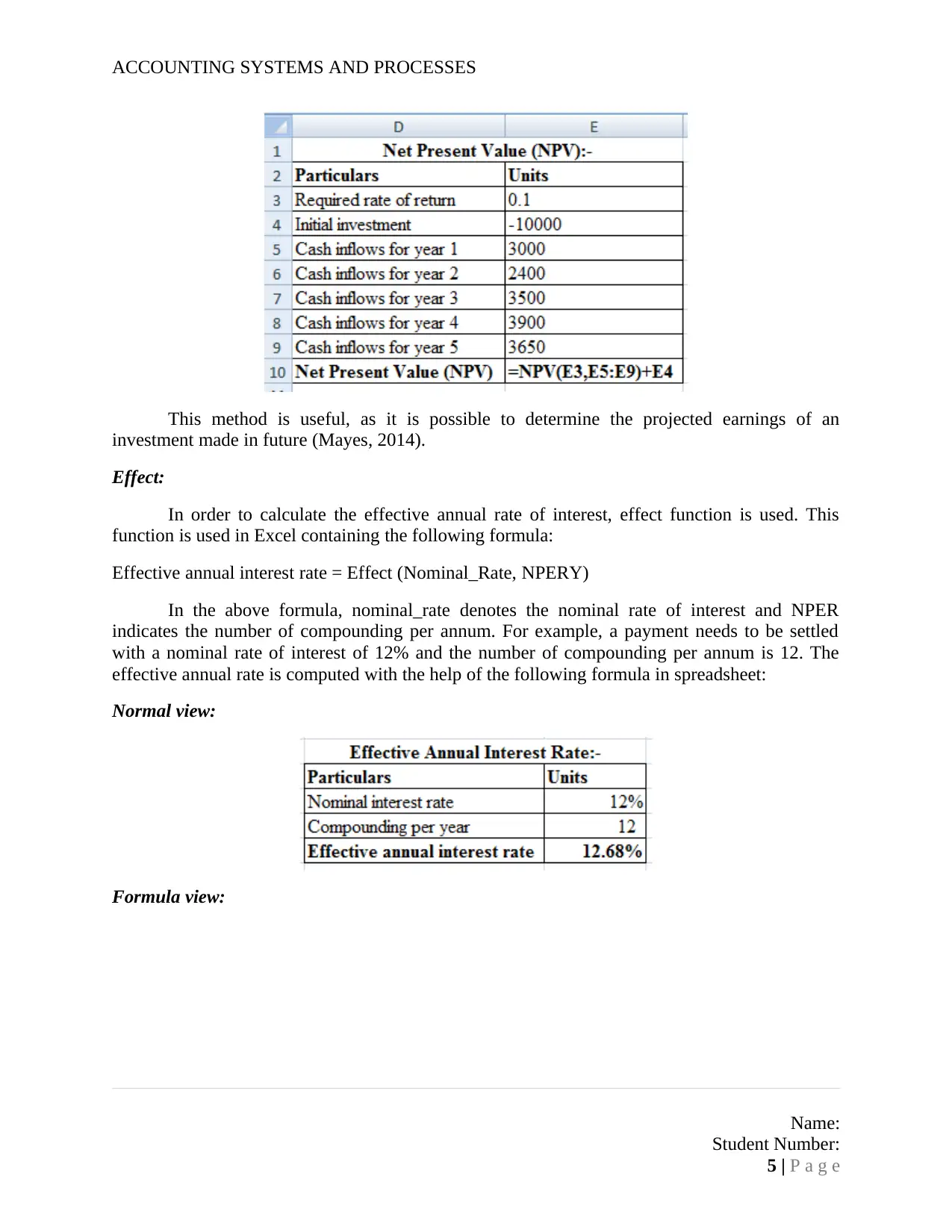

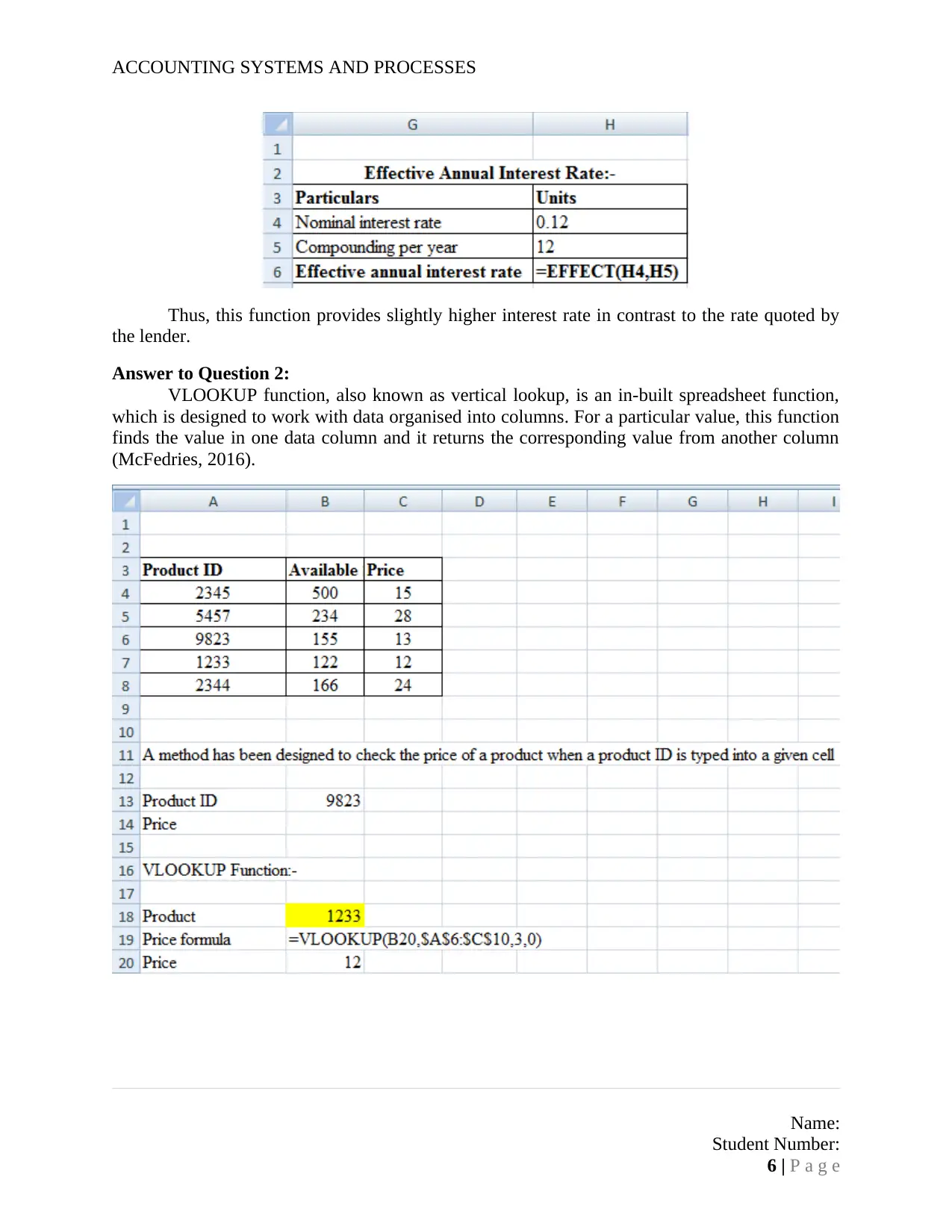

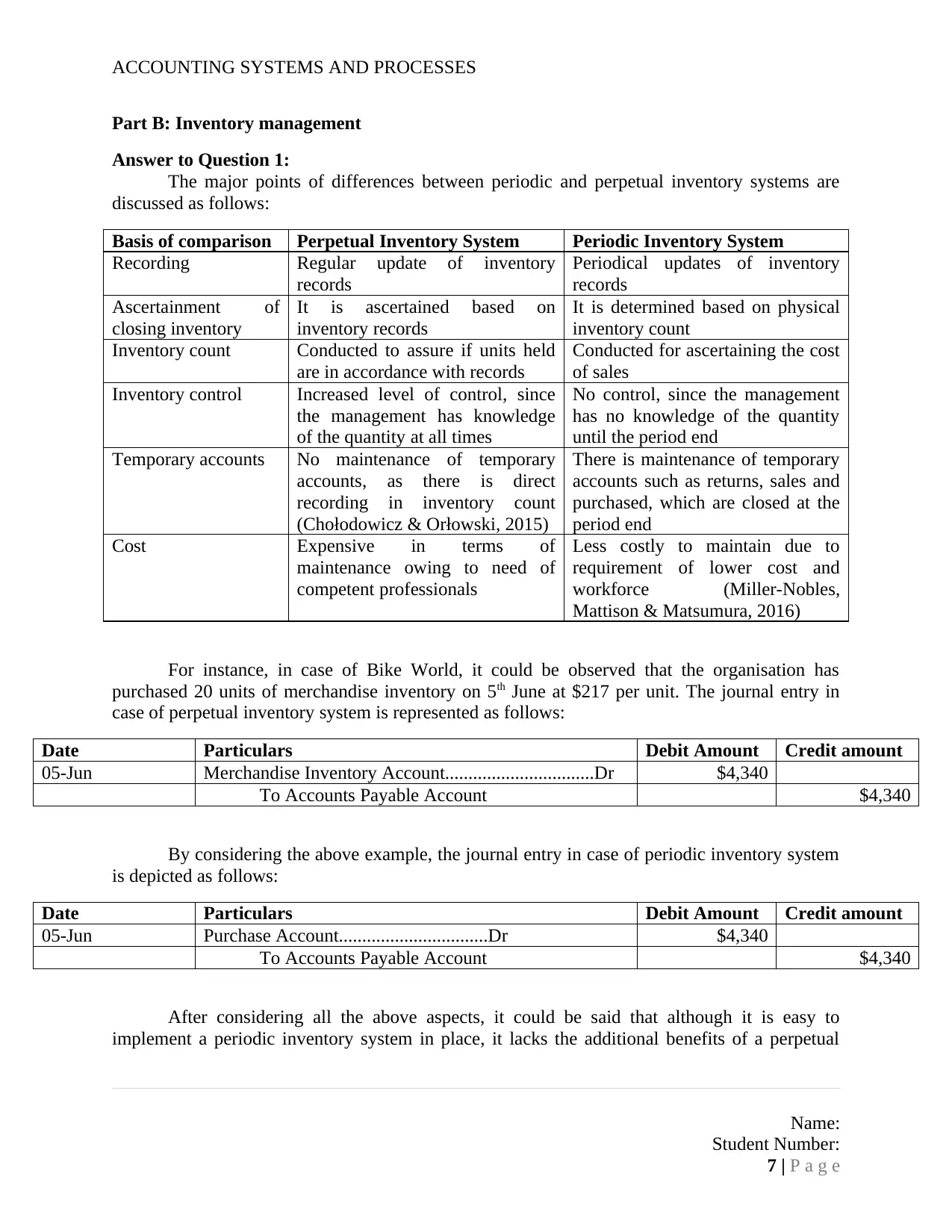

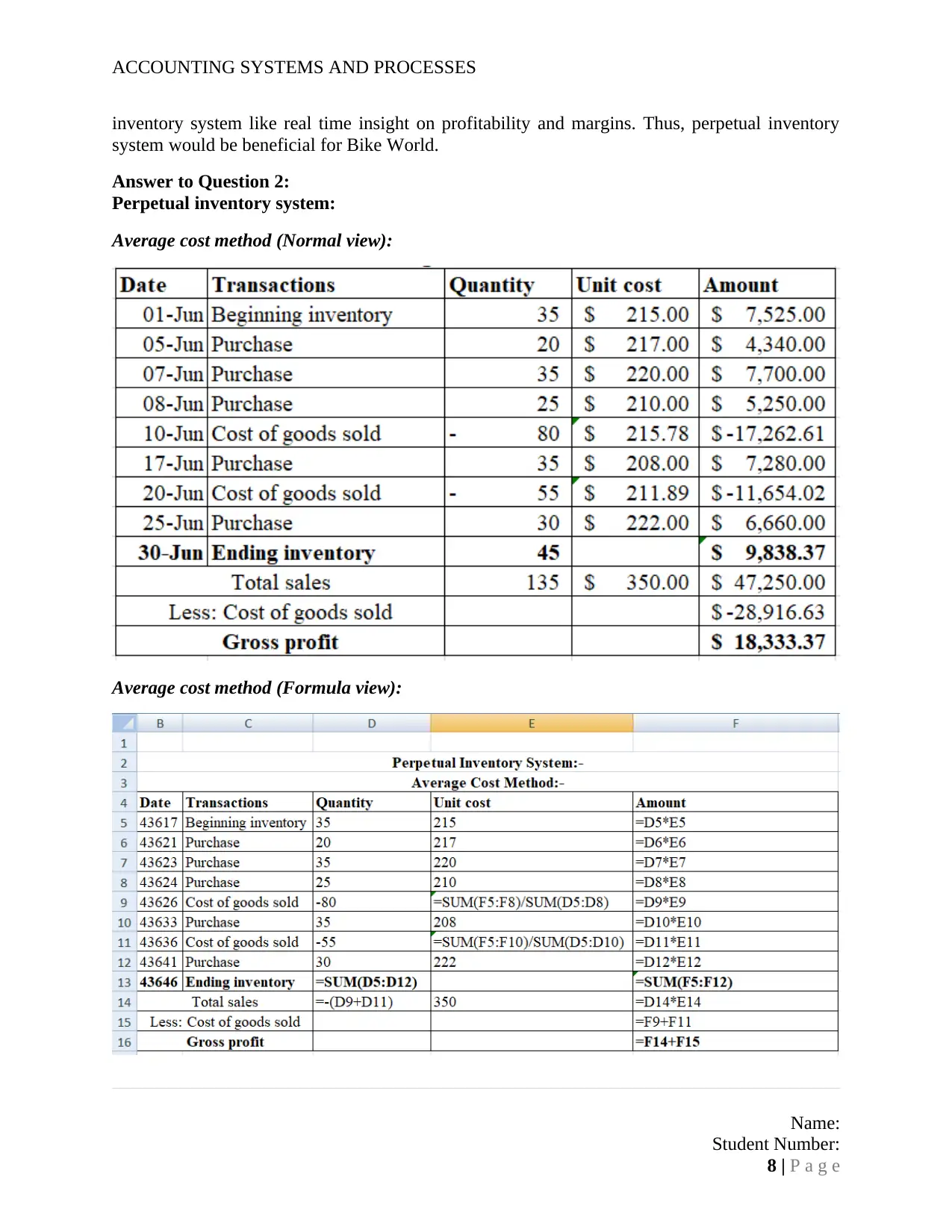

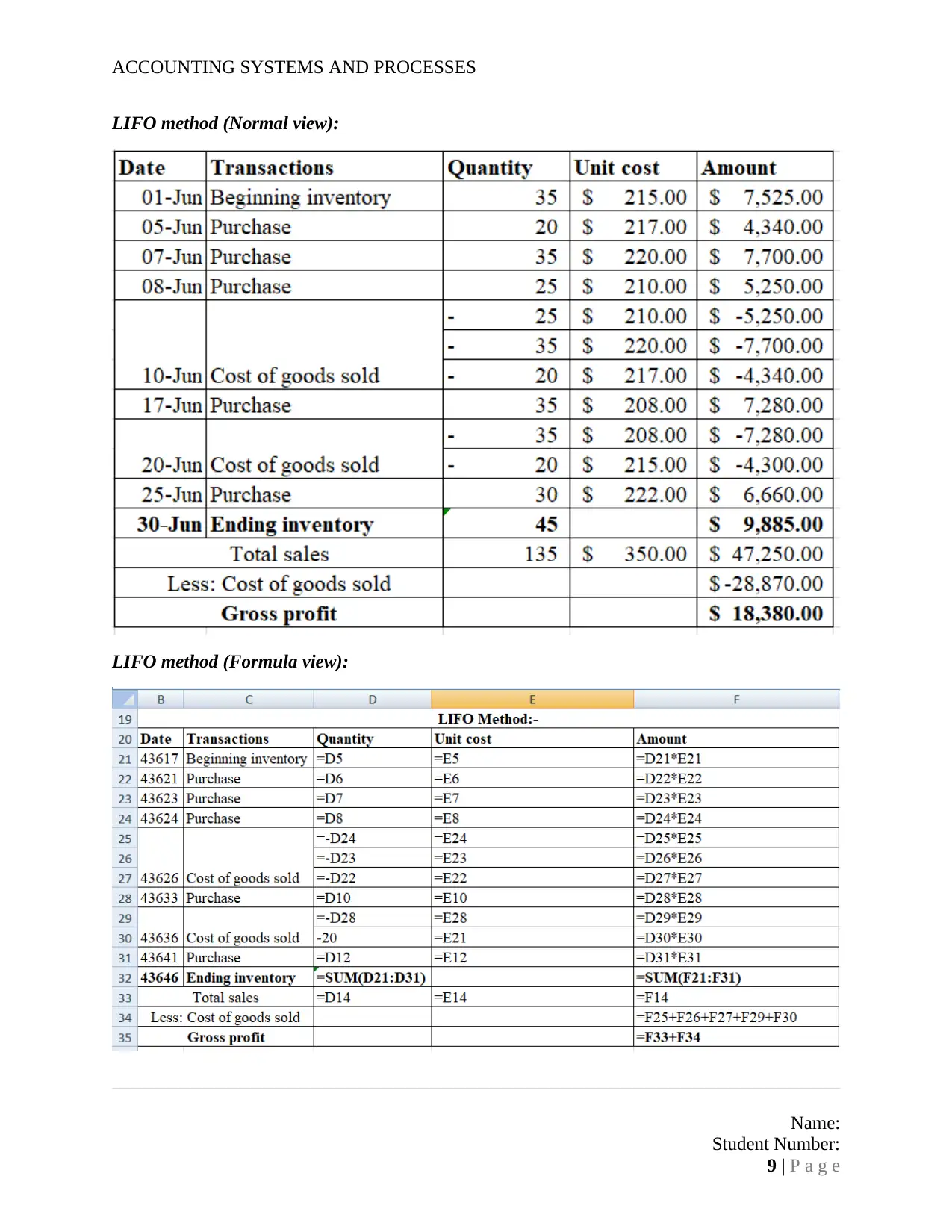

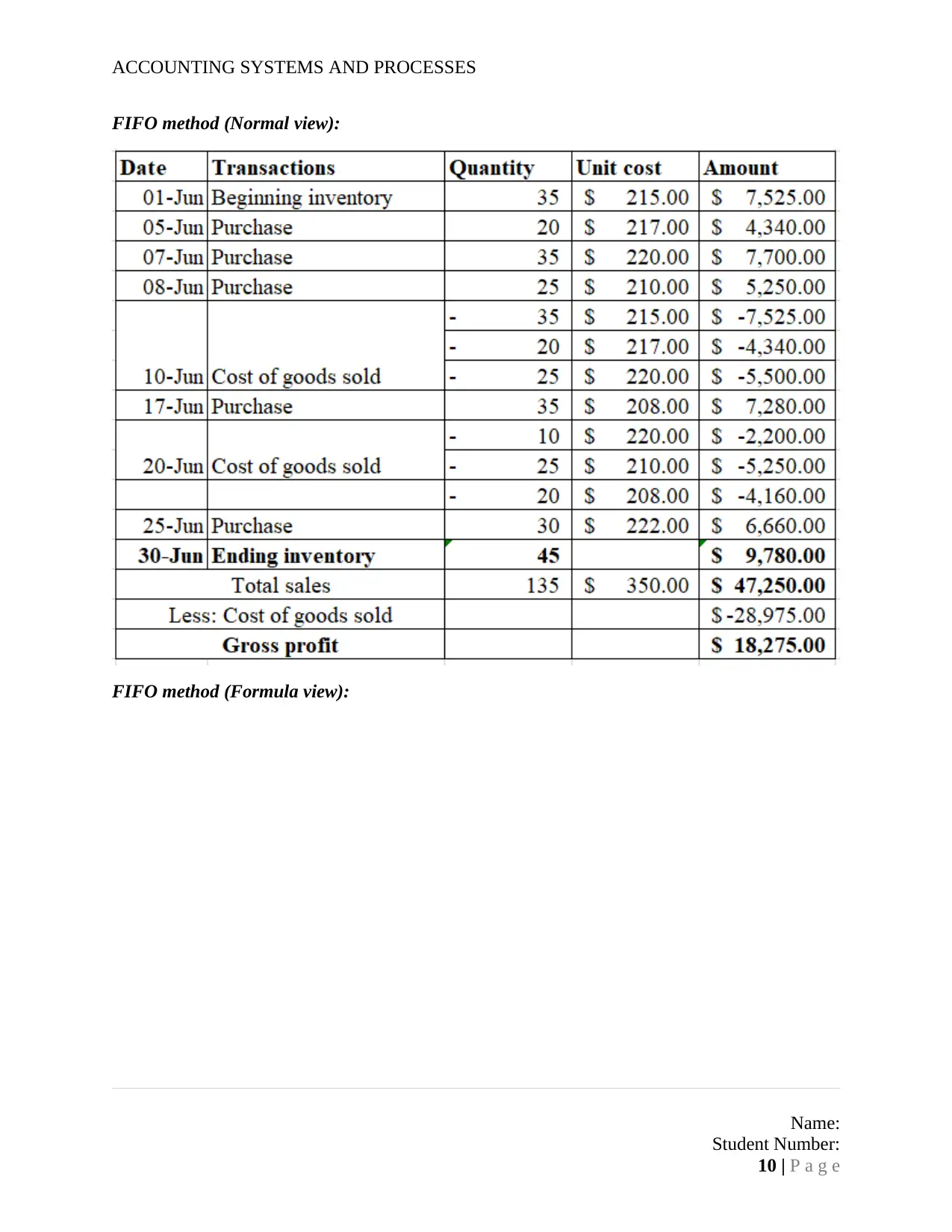

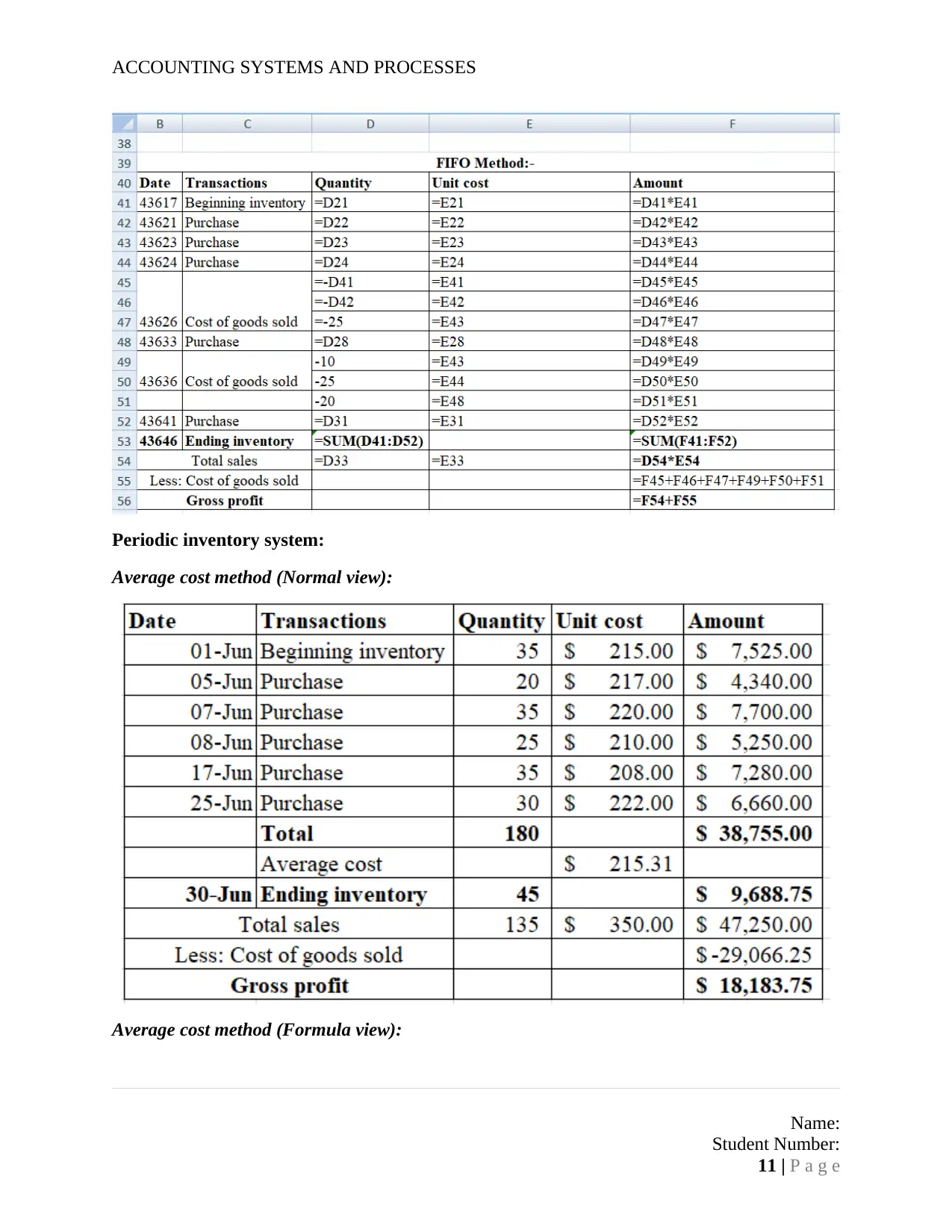

This report provides a detailed analysis of accounting systems and processes, covering spreadsheet functions, inventory management, bank reconciliation, and bad debt management. It begins with an explanation of spreadsheet functions such as future value (FV), net present value (NPV), and effective interest rate. The report then discusses the differences between periodic and perpetual inventory systems, applying various costing methods like average cost, LIFO, and FIFO to Bike World's inventory. Furthermore, it includes a bank reconciliation statement and journal entries. The final section focuses on bad debt management and financial decisions related to the A2 Milk Company, analyzing its financial performance using ratios like net margin, quick ratio, and debt-to-equity ratio, and evaluating its sustainability performance. The report concludes with a recommendation regarding investment decisions based on these analyses. This student-contributed assignment is available on Desklib, a platform offering study tools and resources for students.

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.