Evaluation of Internal Control Systems: Adam & Co. - HA2042, T2 2019

VerifiedAdded on 2022/11/15

|10

|2437

|153

Case Study

AI Summary

This case study analyzes the internal control systems of Adam & Co., evaluating the purchasing, cash disbursements, and payroll departments. The assessment reveals significant weaknesses, including the purchasing clerk's autonomy, the cash disbursement clerk's inappropriate responsibilities, and the payroll department's lack of segregation of duties. The study highlights risks such as potential fraud and financial mismanagement due to these control failures. Recommendations are provided to strengthen internal controls, such as implementing a requisition process in purchasing, centralizing check writing, and separating payroll functions. The conclusion emphasizes the need for improved supervision and evaluation of employee duties to safeguard against financial losses and ensure organizational goals are met. The assignment follows the guidelines provided by Holmes Institute for the HA2042 Accounting Information Systems course.

CONTENTS

Executive Summary……………………………………………………..2

Introduction………………………………………………………………2

Purchase System………………………………………………………..3

Cash Disbursement System…………………………………………….5

Payroll System…………………………………………………………….6

Conclusion………………………………………………………………..

References………………………………………………………………..9

Page 1

Executive Summary……………………………………………………..2

Introduction………………………………………………………………2

Purchase System………………………………………………………..3

Cash Disbursement System…………………………………………….5

Payroll System…………………………………………………………….6

Conclusion………………………………………………………………..

References………………………………………………………………..9

Page 1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

EXECUTIVE SUMMARY

Adam & Co have very weak internal control systems. After a careful review, it is evident

that the company is exposed to great risks of losing money through the exploitation of

the existing loopholes by errant staff.

The entire internal control system requires a major haul so as to remove the

weaknesses inherent in the current set up. In almost all the departments clerks have

been left to make inventory orders or disburse payments without approval or even

knowledge of the accounts department and other relevant departments.

In the purchasing department where the clerk raises a purchase order and sends it

directly to the vendors without reference to anyone, it is recommended that a system be

put in place which allows the purchasing clerk to generate purchase orders finally after

a rigorous requisition process has been followed. It is also observed that it is not the

work of the cash disbursements clerk to update accounts payable subsidiary ledger and

the accounts payable control account. The purchasing clerk’s work is to write checks,

update the check register and raise journal vouchers after checks have been

processed.

The payroll department suffers from the same malady as the others. Payroll checks

should not be written by the payroll clerks. For sound internal control, check writing

must be centralized to be written by the company’s cash disbursements clerk only.

INTRODUCTION

This is an evaluation of the internal control systems of Adam & co. The purpose of this

review is to evaluate the soundness of the current internal control systems in place and

make recommendations.

Evaluations have been done on the purchase system, cash disbursements and payroll

system and recommendations have been made on the changes and improvements that

need to be put in place to correct the situation.

Page 2

Adam & Co have very weak internal control systems. After a careful review, it is evident

that the company is exposed to great risks of losing money through the exploitation of

the existing loopholes by errant staff.

The entire internal control system requires a major haul so as to remove the

weaknesses inherent in the current set up. In almost all the departments clerks have

been left to make inventory orders or disburse payments without approval or even

knowledge of the accounts department and other relevant departments.

In the purchasing department where the clerk raises a purchase order and sends it

directly to the vendors without reference to anyone, it is recommended that a system be

put in place which allows the purchasing clerk to generate purchase orders finally after

a rigorous requisition process has been followed. It is also observed that it is not the

work of the cash disbursements clerk to update accounts payable subsidiary ledger and

the accounts payable control account. The purchasing clerk’s work is to write checks,

update the check register and raise journal vouchers after checks have been

processed.

The payroll department suffers from the same malady as the others. Payroll checks

should not be written by the payroll clerks. For sound internal control, check writing

must be centralized to be written by the company’s cash disbursements clerk only.

INTRODUCTION

This is an evaluation of the internal control systems of Adam & co. The purpose of this

review is to evaluate the soundness of the current internal control systems in place and

make recommendations.

Evaluations have been done on the purchase system, cash disbursements and payroll

system and recommendations have been made on the changes and improvements that

need to be put in place to correct the situation.

Page 2

Purchase System

Shortcomings

The current purchase system in place has serious shortcomings which require urgent

attention. The system gives the purchasing clerk all the authority to make purchases

without reference to anyone else. From the analysis made of the purchasing process of

this organization, there is an important internal control tool which is missing- a

requisition form from the department which needs supplies. Currently, the department

which requires the materials or the supplies is not involved at all while the accounts

department only gets to know that there were purchases made at the time when it is

required to pay the vendor.

Risks

The purchase system as it is currently has weak internal control mechanism and it is

open to abuse. The purchasing clerk might exploit this loophole and engage in fraud by

ordering goods for personal use.

To ensure that fraud is prevented the purchasing department in its entirety must

participate and supervise the whole process of ordering goods, supplies, and materials

for the organization. SIPMM (2018) emphasizes the need for coordination between the

company’s administration and the purchasing department.

Recommendation

There must be a requisition form emanating from the department where the goods

required will be used. Procurify (2018) underscores the critical value of a requisition to

the purchasing cycle. A department expresses the need for goods using an official

purchase requisition form which goes through approval processes before landing in the

hands of the purchasing clerk. With this system in place, the purchasing department is

precluded from making orders directly from the vendors and enables the organization to

have internal control over the whole process of requisitioning purchases.

Example

As an example, the IT requires reams of printing paper. The person in charge, upon

noticing that the supplies are low, will make an official request for the items by filling out

the requisition form. The form is approved by the head of the department and forwarded

to the purchasing department where it is scrutinized, approved and a purchase order

generated and sent to the vendor. A copy of the purchase order is forwarded to the

accounts payable section of the accounts department, a blind copy is sent to the

receiving department and the last copy is kept in the purchase order file.

Page 3

Shortcomings

The current purchase system in place has serious shortcomings which require urgent

attention. The system gives the purchasing clerk all the authority to make purchases

without reference to anyone else. From the analysis made of the purchasing process of

this organization, there is an important internal control tool which is missing- a

requisition form from the department which needs supplies. Currently, the department

which requires the materials or the supplies is not involved at all while the accounts

department only gets to know that there were purchases made at the time when it is

required to pay the vendor.

Risks

The purchase system as it is currently has weak internal control mechanism and it is

open to abuse. The purchasing clerk might exploit this loophole and engage in fraud by

ordering goods for personal use.

To ensure that fraud is prevented the purchasing department in its entirety must

participate and supervise the whole process of ordering goods, supplies, and materials

for the organization. SIPMM (2018) emphasizes the need for coordination between the

company’s administration and the purchasing department.

Recommendation

There must be a requisition form emanating from the department where the goods

required will be used. Procurify (2018) underscores the critical value of a requisition to

the purchasing cycle. A department expresses the need for goods using an official

purchase requisition form which goes through approval processes before landing in the

hands of the purchasing clerk. With this system in place, the purchasing department is

precluded from making orders directly from the vendors and enables the organization to

have internal control over the whole process of requisitioning purchases.

Example

As an example, the IT requires reams of printing paper. The person in charge, upon

noticing that the supplies are low, will make an official request for the items by filling out

the requisition form. The form is approved by the head of the department and forwarded

to the purchasing department where it is scrutinized, approved and a purchase order

generated and sent to the vendor. A copy of the purchase order is forwarded to the

accounts payable section of the accounts department, a blind copy is sent to the

receiving department and the last copy is kept in the purchase order file.

Page 3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

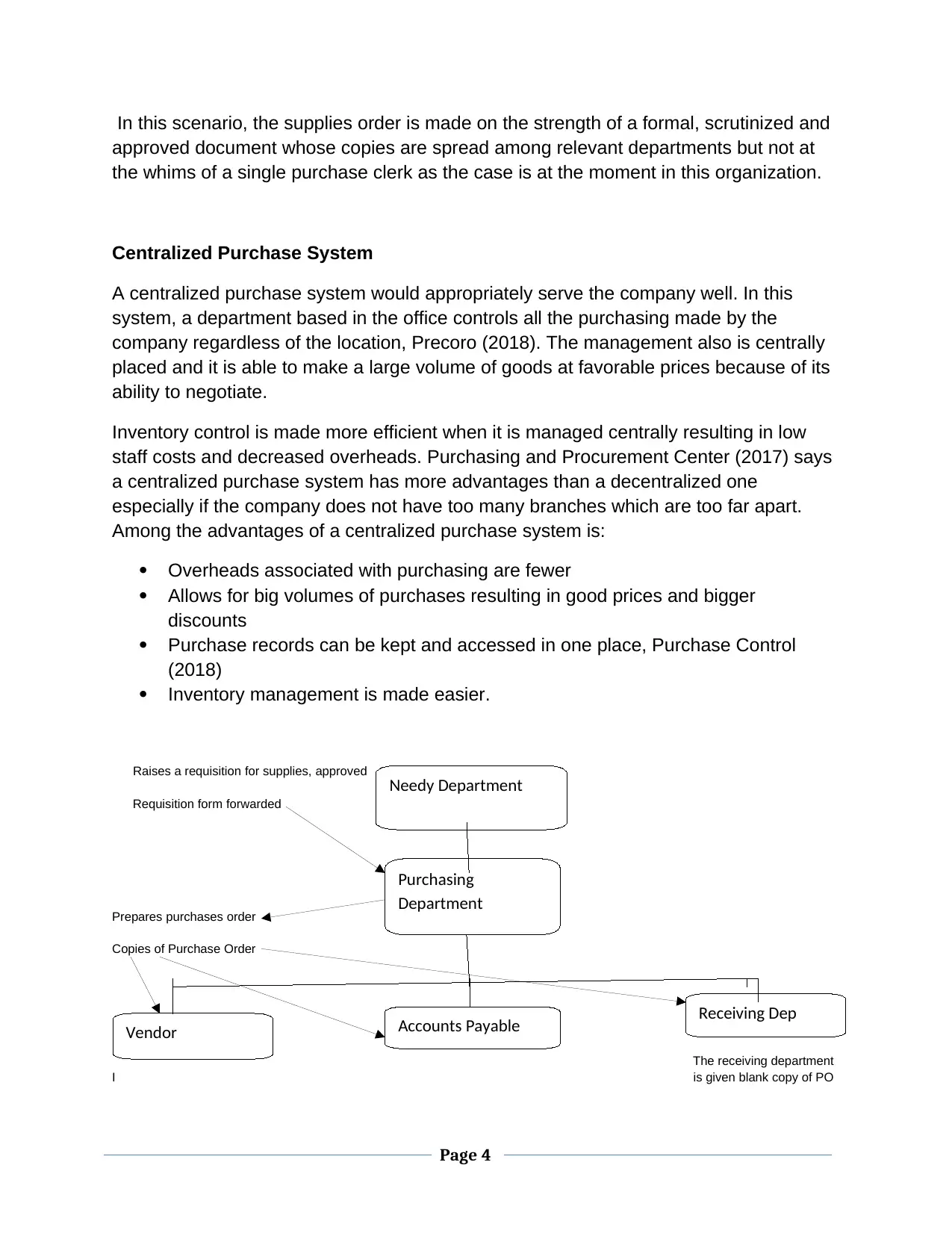

In this scenario, the supplies order is made on the strength of a formal, scrutinized and

approved document whose copies are spread among relevant departments but not at

the whims of a single purchase clerk as the case is at the moment in this organization.

Centralized Purchase System

A centralized purchase system would appropriately serve the company well. In this

system, a department based in the office controls all the purchasing made by the

company regardless of the location, Precoro (2018). The management also is centrally

placed and it is able to make a large volume of goods at favorable prices because of its

ability to negotiate.

Inventory control is made more efficient when it is managed centrally resulting in low

staff costs and decreased overheads. Purchasing and Procurement Center (2017) says

a centralized purchase system has more advantages than a decentralized one

especially if the company does not have too many branches which are too far apart.

Among the advantages of a centralized purchase system is:

Overheads associated with purchasing are fewer

Allows for big volumes of purchases resulting in good prices and bigger

discounts

Purchase records can be kept and accessed in one place, Purchase Control

(2018)

Inventory management is made easier.

Raises a requisition for supplies, approved

Requisition form forwarded

Prepares purchases order

Copies of Purchase Order

The receiving department

I is given blank copy of PO

Needy Department

Purchasing

Department

Vendor Accounts Payable

Dep

Receiving Dep

Page 4

approved document whose copies are spread among relevant departments but not at

the whims of a single purchase clerk as the case is at the moment in this organization.

Centralized Purchase System

A centralized purchase system would appropriately serve the company well. In this

system, a department based in the office controls all the purchasing made by the

company regardless of the location, Precoro (2018). The management also is centrally

placed and it is able to make a large volume of goods at favorable prices because of its

ability to negotiate.

Inventory control is made more efficient when it is managed centrally resulting in low

staff costs and decreased overheads. Purchasing and Procurement Center (2017) says

a centralized purchase system has more advantages than a decentralized one

especially if the company does not have too many branches which are too far apart.

Among the advantages of a centralized purchase system is:

Overheads associated with purchasing are fewer

Allows for big volumes of purchases resulting in good prices and bigger

discounts

Purchase records can be kept and accessed in one place, Purchase Control

(2018)

Inventory management is made easier.

Raises a requisition for supplies, approved

Requisition form forwarded

Prepares purchases order

Copies of Purchase Order

The receiving department

I is given blank copy of PO

Needy Department

Purchasing

Department

Vendor Accounts Payable

Dep

Receiving Dep

Page 4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

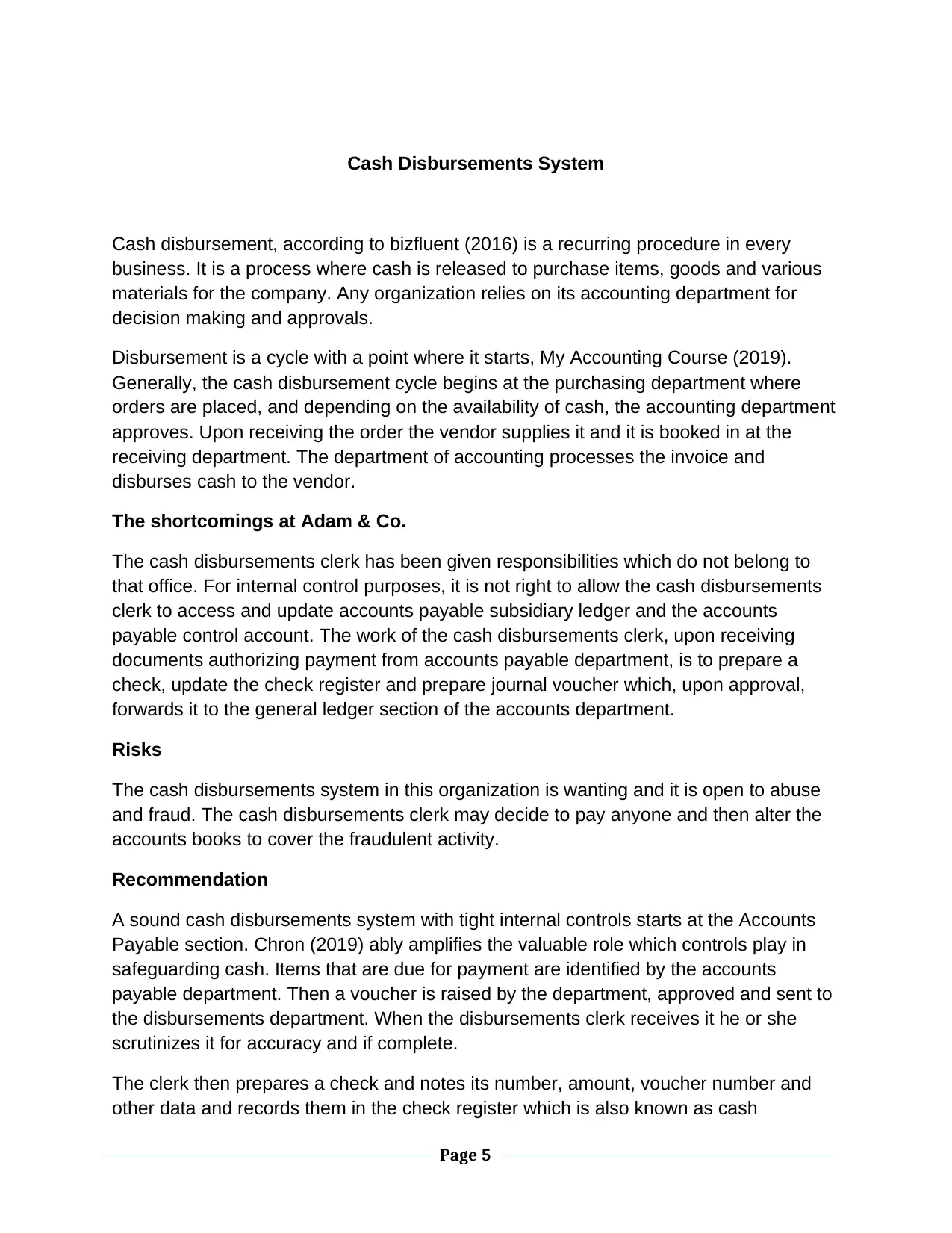

Cash Disbursements System

Cash disbursement, according to bizfluent (2016) is a recurring procedure in every

business. It is a process where cash is released to purchase items, goods and various

materials for the company. Any organization relies on its accounting department for

decision making and approvals.

Disbursement is a cycle with a point where it starts, My Accounting Course (2019).

Generally, the cash disbursement cycle begins at the purchasing department where

orders are placed, and depending on the availability of cash, the accounting department

approves. Upon receiving the order the vendor supplies it and it is booked in at the

receiving department. The department of accounting processes the invoice and

disburses cash to the vendor.

The shortcomings at Adam & Co.

The cash disbursements clerk has been given responsibilities which do not belong to

that office. For internal control purposes, it is not right to allow the cash disbursements

clerk to access and update accounts payable subsidiary ledger and the accounts

payable control account. The work of the cash disbursements clerk, upon receiving

documents authorizing payment from accounts payable department, is to prepare a

check, update the check register and prepare journal voucher which, upon approval,

forwards it to the general ledger section of the accounts department.

Risks

The cash disbursements system in this organization is wanting and it is open to abuse

and fraud. The cash disbursements clerk may decide to pay anyone and then alter the

accounts books to cover the fraudulent activity.

Recommendation

A sound cash disbursements system with tight internal controls starts at the Accounts

Payable section. Chron (2019) ably amplifies the valuable role which controls play in

safeguarding cash. Items that are due for payment are identified by the accounts

payable department. Then a voucher is raised by the department, approved and sent to

the disbursements department. When the disbursements clerk receives it he or she

scrutinizes it for accuracy and if complete.

The clerk then prepares a check and notes its number, amount, voucher number and

other data and records them in the check register which is also known as cash

Page 5

Cash disbursement, according to bizfluent (2016) is a recurring procedure in every

business. It is a process where cash is released to purchase items, goods and various

materials for the company. Any organization relies on its accounting department for

decision making and approvals.

Disbursement is a cycle with a point where it starts, My Accounting Course (2019).

Generally, the cash disbursement cycle begins at the purchasing department where

orders are placed, and depending on the availability of cash, the accounting department

approves. Upon receiving the order the vendor supplies it and it is booked in at the

receiving department. The department of accounting processes the invoice and

disburses cash to the vendor.

The shortcomings at Adam & Co.

The cash disbursements clerk has been given responsibilities which do not belong to

that office. For internal control purposes, it is not right to allow the cash disbursements

clerk to access and update accounts payable subsidiary ledger and the accounts

payable control account. The work of the cash disbursements clerk, upon receiving

documents authorizing payment from accounts payable department, is to prepare a

check, update the check register and prepare journal voucher which, upon approval,

forwards it to the general ledger section of the accounts department.

Risks

The cash disbursements system in this organization is wanting and it is open to abuse

and fraud. The cash disbursements clerk may decide to pay anyone and then alter the

accounts books to cover the fraudulent activity.

Recommendation

A sound cash disbursements system with tight internal controls starts at the Accounts

Payable section. Chron (2019) ably amplifies the valuable role which controls play in

safeguarding cash. Items that are due for payment are identified by the accounts

payable department. Then a voucher is raised by the department, approved and sent to

the disbursements department. When the disbursements clerk receives it he or she

scrutinizes it for accuracy and if complete.

The clerk then prepares a check and notes its number, amount, voucher number and

other data and records them in the check register which is also known as cash

Page 5

disbursements journal. The clerk also prepares a journal voucher to capture this

transaction and sends it to the general ledger section for posting.

The journal voucher shows the updated cash balances and reduction of debt as a result

of this transaction. The disbursements clerk then writes the check number on the

payment voucher and returns it with its attachments to accounts payable section where

it is used to update the accounts payable subsidiary account.

Accounts payable department initiates

Payment by raising a payment voucher

Upon approval it is forwarded

Scrutinized, check written

Journal voucher prepared

Forwarded for posting

The payroll System

The balance small business (2019) defines a payroll as a series of actions carried out

by a company for its employees which culminates in the payment of wages. A payroll

has some parts and definition:

Physical or electronic calculation and the handing out of checks

Records of employees showing wages, bonuses, deductions, and other details

A payroll is the record of total wages earned by all employees of a company in a

financial year.

After an employee’s wages have been calculated, it is a legal requirement for the

employer to withhold taxes and other deductions from each employee. After the wages

are paid out the employer must segregate the amounts deducted from employees’

wages for later disbursement to various agencies. Every employee has his or her own

record showing the amount of wages earned in each period, Cloudpay (2018). A

control record showing details of wage payments for every employee is known as

payroll register.

Accounts Payable Dep

Disbursements Dep

General ledger Section

Page 6

transaction and sends it to the general ledger section for posting.

The journal voucher shows the updated cash balances and reduction of debt as a result

of this transaction. The disbursements clerk then writes the check number on the

payment voucher and returns it with its attachments to accounts payable section where

it is used to update the accounts payable subsidiary account.

Accounts payable department initiates

Payment by raising a payment voucher

Upon approval it is forwarded

Scrutinized, check written

Journal voucher prepared

Forwarded for posting

The payroll System

The balance small business (2019) defines a payroll as a series of actions carried out

by a company for its employees which culminates in the payment of wages. A payroll

has some parts and definition:

Physical or electronic calculation and the handing out of checks

Records of employees showing wages, bonuses, deductions, and other details

A payroll is the record of total wages earned by all employees of a company in a

financial year.

After an employee’s wages have been calculated, it is a legal requirement for the

employer to withhold taxes and other deductions from each employee. After the wages

are paid out the employer must segregate the amounts deducted from employees’

wages for later disbursement to various agencies. Every employee has his or her own

record showing the amount of wages earned in each period, Cloudpay (2018). A

control record showing details of wage payments for every employee is known as

payroll register.

Accounts Payable Dep

Disbursements Dep

General ledger Section

Page 6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Shortcomings

The payroll system at Adam’s & co lacks sound internal control checks and it can be

abused. The payroll department has been given all the authority and the final say in the

approval and payment of wages. The authority to pay should come from the accounts

department, and the person writing checks is the cash disbursements clerk, not the

payroll clerk. It is also wrong for the payroll clerk to send the payroll register to the

Accounts Payable department after checks have been written and distributed.

Risks

Without the involvement of the accounts department in the approval and processing of

payroll payments, there is a danger for the payroll staff to collude and make payments

to themselves in the name of non-existent workers. This situation is made even more

likely to happen because the payroll clerk initiates and completes the process of writing

and issuing checks without any supervision.

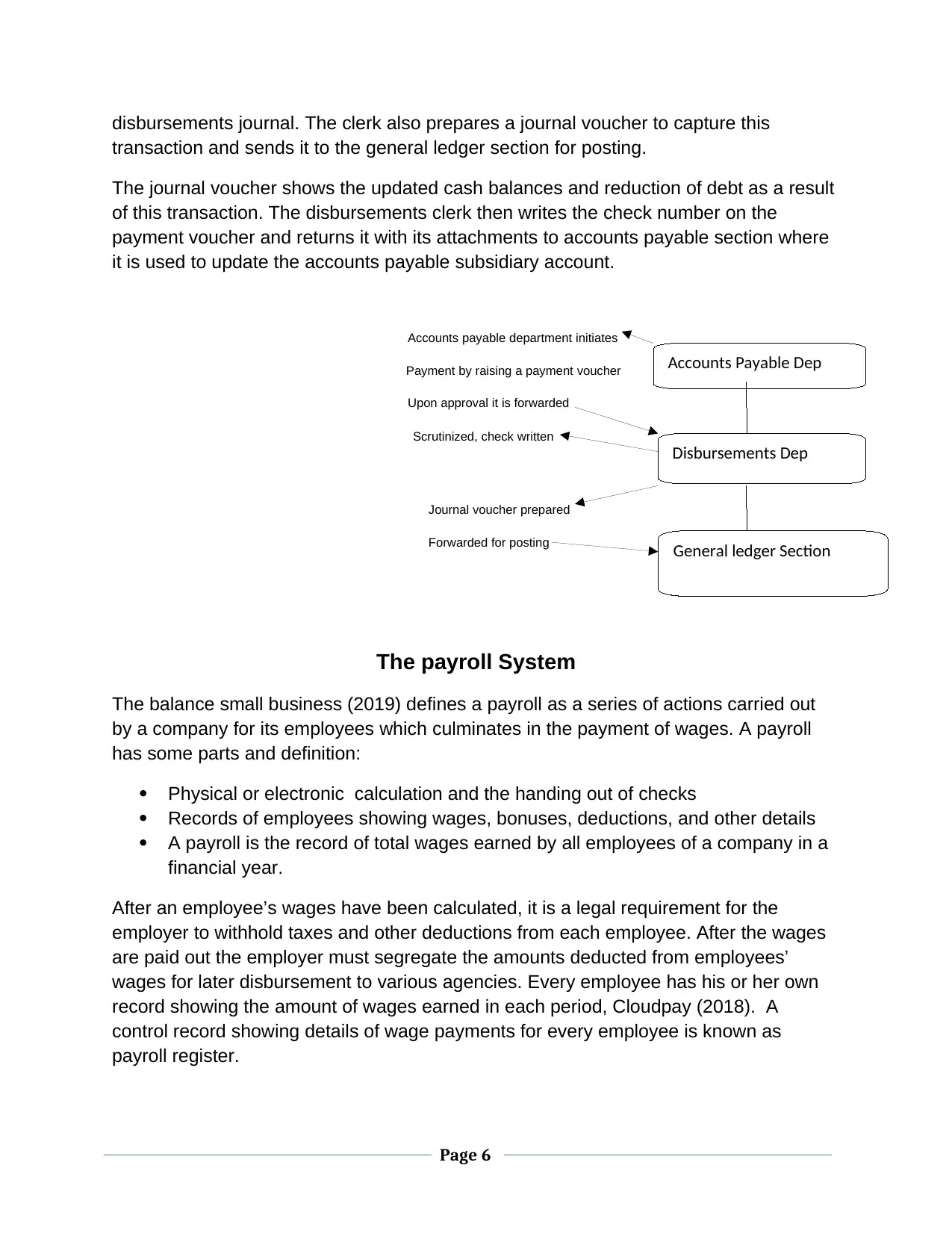

Recommendation

For good internal control, the payroll department should process the raw data and

forward the payroll register to Accounts Payable where it is scrutinized and approved for

payment. Fitsmallbusiness (2019) suggests the use of a payroll system software to

simplify the process.

The cash disbursements clerk then writes checks and distributes them. The accounts

payable department will also deduct workers taxes and other statutory deductions and

forward them to relevant authorities.

Processes wages data

Prepares payroll register

Scrutinizes payroll register, approves

Writes checks for workers

Payroll Department

Accounts Payable Dep

Cash Disbursements

Page 7

The payroll system at Adam’s & co lacks sound internal control checks and it can be

abused. The payroll department has been given all the authority and the final say in the

approval and payment of wages. The authority to pay should come from the accounts

department, and the person writing checks is the cash disbursements clerk, not the

payroll clerk. It is also wrong for the payroll clerk to send the payroll register to the

Accounts Payable department after checks have been written and distributed.

Risks

Without the involvement of the accounts department in the approval and processing of

payroll payments, there is a danger for the payroll staff to collude and make payments

to themselves in the name of non-existent workers. This situation is made even more

likely to happen because the payroll clerk initiates and completes the process of writing

and issuing checks without any supervision.

Recommendation

For good internal control, the payroll department should process the raw data and

forward the payroll register to Accounts Payable where it is scrutinized and approved for

payment. Fitsmallbusiness (2019) suggests the use of a payroll system software to

simplify the process.

The cash disbursements clerk then writes checks and distributes them. The accounts

payable department will also deduct workers taxes and other statutory deductions and

forward them to relevant authorities.

Processes wages data

Prepares payroll register

Scrutinizes payroll register, approves

Writes checks for workers

Payroll Department

Accounts Payable Dep

Cash Disbursements

Page 7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CONCLUSION

Adam & co are operating with very weak internal control systems which expose the

company to fraudulent activities.

In the three departments of purchasing, cash disbursements and payroll loopholes exist

which could easily be exploited by some staff to defraud the company.

In each of those departments changes that will strengthen the control function are

recommended. All clerks should be stripped of the authority they now have of making

purchase orders or writing and issuing checks without following the requisition process.

Payroll clerks should cease from writing and issuing checks. All checks should be

written and issued from cash disbursements department only.

The company also, as a matter of urgency, should put in place a control system which

ensures that employees are supervised and evaluated on the duties they were assigned

because a company without such controls, according to iedunote (2015) might not

achieve its goals.

Page 8

Adam & co are operating with very weak internal control systems which expose the

company to fraudulent activities.

In the three departments of purchasing, cash disbursements and payroll loopholes exist

which could easily be exploited by some staff to defraud the company.

In each of those departments changes that will strengthen the control function are

recommended. All clerks should be stripped of the authority they now have of making

purchase orders or writing and issuing checks without following the requisition process.

Payroll clerks should cease from writing and issuing checks. All checks should be

written and issued from cash disbursements department only.

The company also, as a matter of urgency, should put in place a control system which

ensures that employees are supervised and evaluated on the duties they were assigned

because a company without such controls, according to iedunote (2015) might not

achieve its goals.

Page 8

REFERENCES

Bizfluent (2017) Objectives of accounting information system [online]. Available from:

https://bizfluent.com/list-6818819-objectives-accounting-information-systems.html

[Accessed on 18 September 2019]

Chron (2019) What is a cash disbursement system? [online]. Available from:

https://smallbusiness.chron.com/cash-disbursement-system-47911.html [Accessed 17

[September 2019].

Cloudpay (2018) The strategic importance of payroll [online]. Available from:

https://www.cloudpay.net/resources/the-strategic-importance-of-payroll/ [Accessed on

18 September 2019).

FitSmallBusiness (2019) Payroll processing: what happens during the payroll process

[online]. Available from: https://fitsmallbusiness.com/payroll-processing/

iEdunote (2015) Internal controlsystem:5 components of internal control system [online].

Available from: https://iedunote.com/internal-control-system [Accessed 17 September

2019].

My Accounting Course (2019) What is a cash disbursement [online]. Available from:

https://www.myaccountingcourse.com/accounting-dictionary/cash-disbursement

[Accessed on 18September 2018].

Precoro (2018) What is centralized purchasing [online]. Available from:

https://blog.precoro.com/en/2017/01/what-is-centralized-purchasing/ [ Accessed on 18

September 2019]/

Purchase Control (2018) Centralized vs decentralized purchasing [online]. Available

from: https://www.purchasecontrol.com/blog/centralized-vs-decentralized-purchasing/

[Accessed on 18September 2019].

Purchasing Procurement Center (2017) Centralized purchasing-good or bad [online].

Available from: https://www.purchasing-procurement-center.com/centralized-

purchasing.html [Accessed on 18 September 2019].

Procurify (2018) What is a purchase requisition and why it is important for your business

[online]. Available from: https://blog.procurify.com/2018/01/30/purchase-requisition-

important-business/ [Accessed 17September 2019].

Page 9

Bizfluent (2017) Objectives of accounting information system [online]. Available from:

https://bizfluent.com/list-6818819-objectives-accounting-information-systems.html

[Accessed on 18 September 2019]

Chron (2019) What is a cash disbursement system? [online]. Available from:

https://smallbusiness.chron.com/cash-disbursement-system-47911.html [Accessed 17

[September 2019].

Cloudpay (2018) The strategic importance of payroll [online]. Available from:

https://www.cloudpay.net/resources/the-strategic-importance-of-payroll/ [Accessed on

18 September 2019).

FitSmallBusiness (2019) Payroll processing: what happens during the payroll process

[online]. Available from: https://fitsmallbusiness.com/payroll-processing/

iEdunote (2015) Internal controlsystem:5 components of internal control system [online].

Available from: https://iedunote.com/internal-control-system [Accessed 17 September

2019].

My Accounting Course (2019) What is a cash disbursement [online]. Available from:

https://www.myaccountingcourse.com/accounting-dictionary/cash-disbursement

[Accessed on 18September 2018].

Precoro (2018) What is centralized purchasing [online]. Available from:

https://blog.precoro.com/en/2017/01/what-is-centralized-purchasing/ [ Accessed on 18

September 2019]/

Purchase Control (2018) Centralized vs decentralized purchasing [online]. Available

from: https://www.purchasecontrol.com/blog/centralized-vs-decentralized-purchasing/

[Accessed on 18September 2019].

Purchasing Procurement Center (2017) Centralized purchasing-good or bad [online].

Available from: https://www.purchasing-procurement-center.com/centralized-

purchasing.html [Accessed on 18 September 2019].

Procurify (2018) What is a purchase requisition and why it is important for your business

[online]. Available from: https://blog.procurify.com/2018/01/30/purchase-requisition-

important-business/ [Accessed 17September 2019].

Page 9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

SIPMM (2018) Key Performance Indicators for Evaluating Purchasing Performance

[online]. Available from: https://sipmm.edu.sg/key-performance-indicators-evaluating-

purchasing-performance/ [Accessed on 16 September 2019].

The balance small business (2019) What is the definition of payroll [online]. Available

from: https://www.thebalancesmb.com/what-is-payroll-398399 [Accessed on 18

September 2019]

Page

10

[online]. Available from: https://sipmm.edu.sg/key-performance-indicators-evaluating-

purchasing-performance/ [Accessed on 16 September 2019].

The balance small business (2019) What is the definition of payroll [online]. Available

from: https://www.thebalancesmb.com/what-is-payroll-398399 [Accessed on 18

September 2019]

Page

10

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.