Comprehensive Analysis of Management Accounting Systems & Tools

VerifiedAdded on 2024/05/16

|26

|4327

|224

Report

AI Summary

This report provides a comprehensive overview of management accounting systems and techniques. It begins by defining management accounting and differentiating it from financial accounting, highlighting key functions and various types of management accounting systems, including financial, cost, tax, and inventory management. The report discusses methods of reporting management accounting information, such as income statements, balance sheets, and cash flow statements. It also explores cost computation techniques, including marginal and absorption costing, and illustrates these with a cost report and reconciliation statement. Furthermore, the document examines planning tools like budgets, discussing their advantages and disadvantages, and how organizations adapt management accounting systems to respond to financial problems. The report concludes by emphasizing how management accounting can lead an organization to sustainable success through informed decision-making and strategic planning. Desklib offers students access to this and other solved assignments for academic support.

Management Accounting

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Introduction...................................................................................................................................4

LO1 Systems of Management Accounting (P1, P2, M1, D1).................................................5

P1 Management Accounting and Types................................................................................5

P2 Methods of the reporting of the management accounting...........................................7

M1 Benefits of the system of the management accounting................................................8

D1 Management Accounting system and reporting integration with the organization 9

LO2 Techniques range for management accounting (P3, M2, D2)....................................10

P3 Cost computation and income statement......................................................................10

LO3...............................................................................................................................................13

P4. Advantages and disadvantages of types of planning tools........................................13

M3 Use of planning tools and their application................................................................14

LO4...............................................................................................................................................18

P5 Organizations adapting management accounting systems to respond to financial

problems..................................................................................................................................18

M4 How management accounting can lead an organization to sustainable success...19

D3 How planning tools respond appropriately in solving problems.............................21

2

Introduction...................................................................................................................................4

LO1 Systems of Management Accounting (P1, P2, M1, D1).................................................5

P1 Management Accounting and Types................................................................................5

P2 Methods of the reporting of the management accounting...........................................7

M1 Benefits of the system of the management accounting................................................8

D1 Management Accounting system and reporting integration with the organization 9

LO2 Techniques range for management accounting (P3, M2, D2)....................................10

P3 Cost computation and income statement......................................................................10

LO3...............................................................................................................................................13

P4. Advantages and disadvantages of types of planning tools........................................13

M3 Use of planning tools and their application................................................................14

LO4...............................................................................................................................................18

P5 Organizations adapting management accounting systems to respond to financial

problems..................................................................................................................................18

M4 How management accounting can lead an organization to sustainable success...19

D3 How planning tools respond appropriately in solving problems.............................21

2

Conclusion...................................................................................................................................22

Bibliography................................................................................................................................23

3

Bibliography................................................................................................................................23

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Introduction

The main part of any organization is the accounting which helps in the understanding of the

performance of the company for the current scenario as well as the future. The management

accounting is the part of the accounting where the internal holders will be able to know the

performance. In the assignment below the theories of management accounting and different

calculations will be shown along with the responsibilities and methods of management

accounting are explained in the report below. The assignment will further explain the

reporting methods of the management accounting and the planning tools used for the

budgetary control. Further, the budget, variance calculation and the ways the company

respond to the financial problems will be discussed.

4

The main part of any organization is the accounting which helps in the understanding of the

performance of the company for the current scenario as well as the future. The management

accounting is the part of the accounting where the internal holders will be able to know the

performance. In the assignment below the theories of management accounting and different

calculations will be shown along with the responsibilities and methods of management

accounting are explained in the report below. The assignment will further explain the

reporting methods of the management accounting and the planning tools used for the

budgetary control. Further, the budget, variance calculation and the ways the company

respond to the financial problems will be discussed.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

LO1 Systems of Management Accounting (P1, P2, M1, D1)

P1 Management Accounting and Types

Management Accounting- Management accounting is a very important tool which helps the

company in taking the decision. The various tools which management accounting uses are

the budgets, variance, break-even Point and Cost-volume Profit analysis. The management

will be able to properly plan and control the company and the management accounting can

be used at every kind of organization. The organization will be able to use the resources

efficiently and effectively (Borad, 2017).

The management accounting and financial accounting are two different concepts for the

organization in terms of:

Reporting- Management accounting reports in a detailed way than the financial

accounting whereas the financial accounting reports on the business as a whole.

Use of Standards- Management accounting does not use any standards while the

financial accounting uses the accounting standards.

The timing of Reporting- The management accounting reports whenever the

requirement arises while the financial accounting reports at the end of the year.

Orientation- The management accounting has the future orientation whereas the

financial accounting has the historical orientation.

Information- Management accounting does not provide accurate or precise

information while the financial accounting is required to provide accurate information

(Bragg, 2017).

The management accounting requires to follow the mandatory principles of the

communication where the departments are required to be communicated, the information

provided should be relevant with the help of which the decisions can be taken, the

management accounting should help the companies in creating their value and the

management accounting should be developed so that the trust is created by the employees

and the staff. The management accounting has many key functions which include the

providing of the data, changing the data, interpreting of the data, helps in communication,

provides qualitative and quantitative information, etc.

The different types of the system of the management accounting are as follows:

1. Financial Accounting- The financial accounting is a system which helps in the

analysis and the reporting of the information of the business and the financial

accounting is required to prepare the reports in financial terms through which the

decisions can be taken.

2. Cost Accounting- The cost of the product for the company is predicted and the profit

can be estimated on the basis of the cost. The system will help the company in

controlling the cost where the cost accounting system is divided into two parts which

are the job order costing and the process cost.

5

P1 Management Accounting and Types

Management Accounting- Management accounting is a very important tool which helps the

company in taking the decision. The various tools which management accounting uses are

the budgets, variance, break-even Point and Cost-volume Profit analysis. The management

will be able to properly plan and control the company and the management accounting can

be used at every kind of organization. The organization will be able to use the resources

efficiently and effectively (Borad, 2017).

The management accounting and financial accounting are two different concepts for the

organization in terms of:

Reporting- Management accounting reports in a detailed way than the financial

accounting whereas the financial accounting reports on the business as a whole.

Use of Standards- Management accounting does not use any standards while the

financial accounting uses the accounting standards.

The timing of Reporting- The management accounting reports whenever the

requirement arises while the financial accounting reports at the end of the year.

Orientation- The management accounting has the future orientation whereas the

financial accounting has the historical orientation.

Information- Management accounting does not provide accurate or precise

information while the financial accounting is required to provide accurate information

(Bragg, 2017).

The management accounting requires to follow the mandatory principles of the

communication where the departments are required to be communicated, the information

provided should be relevant with the help of which the decisions can be taken, the

management accounting should help the companies in creating their value and the

management accounting should be developed so that the trust is created by the employees

and the staff. The management accounting has many key functions which include the

providing of the data, changing the data, interpreting of the data, helps in communication,

provides qualitative and quantitative information, etc.

The different types of the system of the management accounting are as follows:

1. Financial Accounting- The financial accounting is a system which helps in the

analysis and the reporting of the information of the business and the financial

accounting is required to prepare the reports in financial terms through which the

decisions can be taken.

2. Cost Accounting- The cost of the product for the company is predicted and the profit

can be estimated on the basis of the cost. The system will help the company in

controlling the cost where the cost accounting system is divided into two parts which

are the job order costing and the process cost.

5

3. Management Accounting- The management at all the levels uses the system of

management accounting and the financial and non-financial information is used by

the system of management accounting. The indicators can be identified with the help

of the management accounting systems.

4. Tax Accounting- The system whose main focus area is taxation and not the financial

statements. The tax accounting system follows the generally accepted principles and

helps in the preparation of the tax returns and the payment of tax amounts.

6

management accounting and the financial and non-financial information is used by

the system of management accounting. The indicators can be identified with the help

of the management accounting systems.

4. Tax Accounting- The system whose main focus area is taxation and not the financial

statements. The tax accounting system follows the generally accepted principles and

helps in the preparation of the tax returns and the payment of tax amounts.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

P2 Methods of the reporting of the management accounting

The reports prepared are the trading and profit and loss which shows the profitability

position of the company and the decision on making the payment of the dividend can be

taken. Cost of goods sold is prepared so that the deduction can be claimed and the tax can be

reduced (Murray, 2017). The income statement is prepared so that the income and expenses

of the company can be analysed. The balance sheet is prepared to interpret the position of

the company and the cash flow statement helps in the analysing the cash flow of the

company (Kumar, 2011).

The different systems of management accounting are:

1. Cost Accounting System- The system which is used to control the cost and based

on which the profit is earned. The main types are the job order and process costing.

Example- when the material move from one location to another then the system

helps in tracking the progress.

2. Inventory Management System- The main component of the company is

managed with the help of this system which is inventory. Example- when the

inventory is sold by the business and it reaches danger level then the system will

automatically order the inventory.

3. Price Optimisation System- The analysis of the customer response is done

through the mathematical analysis and the price will be decided. Example- the

price for the newly innovated product can be decided (McCormick, 2017).

4. Job-Costing System- The Cost of each job or the product can be identified which

will include the material, overhead and the labour. Example- the cost of the product

is £ 2,00,000, then the system will allocate the cost to the job proportionately in job

cost sheet (Bragg, 2018).

7

The reports prepared are the trading and profit and loss which shows the profitability

position of the company and the decision on making the payment of the dividend can be

taken. Cost of goods sold is prepared so that the deduction can be claimed and the tax can be

reduced (Murray, 2017). The income statement is prepared so that the income and expenses

of the company can be analysed. The balance sheet is prepared to interpret the position of

the company and the cash flow statement helps in the analysing the cash flow of the

company (Kumar, 2011).

The different systems of management accounting are:

1. Cost Accounting System- The system which is used to control the cost and based

on which the profit is earned. The main types are the job order and process costing.

Example- when the material move from one location to another then the system

helps in tracking the progress.

2. Inventory Management System- The main component of the company is

managed with the help of this system which is inventory. Example- when the

inventory is sold by the business and it reaches danger level then the system will

automatically order the inventory.

3. Price Optimisation System- The analysis of the customer response is done

through the mathematical analysis and the price will be decided. Example- the

price for the newly innovated product can be decided (McCormick, 2017).

4. Job-Costing System- The Cost of each job or the product can be identified which

will include the material, overhead and the labour. Example- the cost of the product

is £ 2,00,000, then the system will allocate the cost to the job proportionately in job

cost sheet (Bragg, 2018).

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

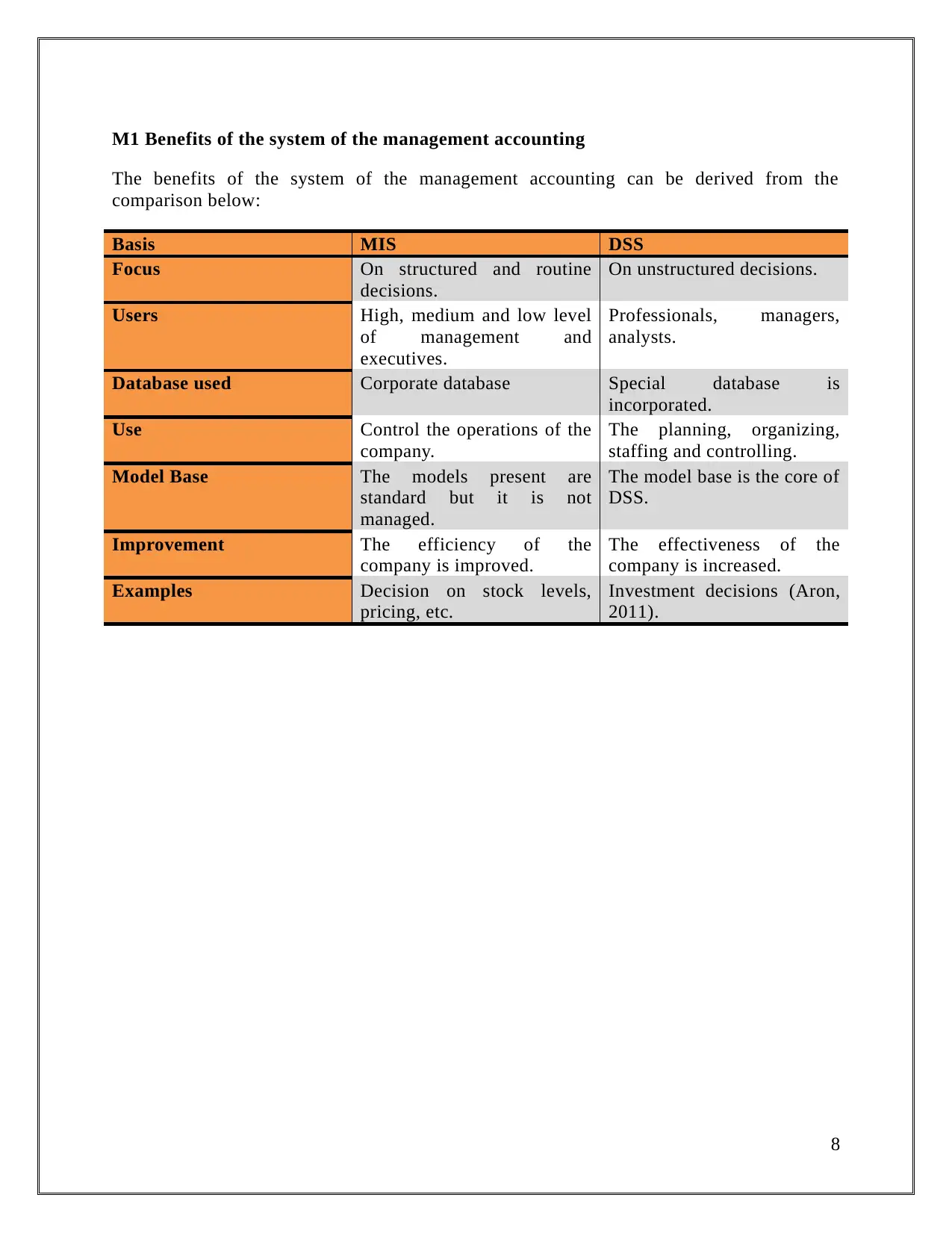

M1 Benefits of the system of the management accounting

The benefits of the system of the management accounting can be derived from the

comparison below:

Basis MIS DSS

Focus On structured and routine

decisions.

On unstructured decisions.

Users High, medium and low level

of management and

executives.

Professionals, managers,

analysts.

Database used Corporate database Special database is

incorporated.

Use Control the operations of the

company.

The planning, organizing,

staffing and controlling.

Model Base The models present are

standard but it is not

managed.

The model base is the core of

DSS.

Improvement The efficiency of the

company is improved.

The effectiveness of the

company is increased.

Examples Decision on stock levels,

pricing, etc.

Investment decisions (Aron,

2011).

8

The benefits of the system of the management accounting can be derived from the

comparison below:

Basis MIS DSS

Focus On structured and routine

decisions.

On unstructured decisions.

Users High, medium and low level

of management and

executives.

Professionals, managers,

analysts.

Database used Corporate database Special database is

incorporated.

Use Control the operations of the

company.

The planning, organizing,

staffing and controlling.

Model Base The models present are

standard but it is not

managed.

The model base is the core of

DSS.

Improvement The efficiency of the

company is improved.

The effectiveness of the

company is increased.

Examples Decision on stock levels,

pricing, etc.

Investment decisions (Aron,

2011).

8

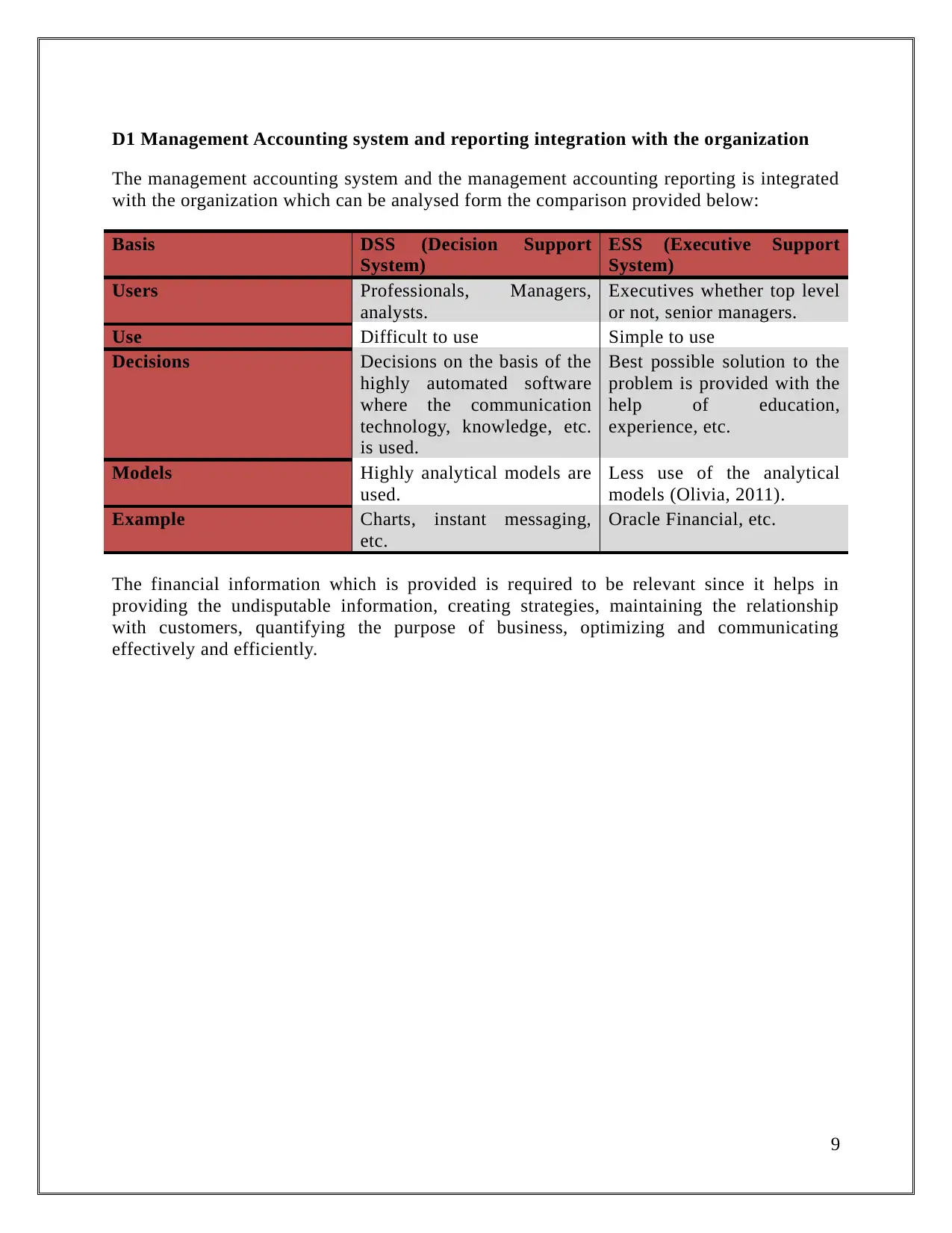

D1 Management Accounting system and reporting integration with the organization

The management accounting system and the management accounting reporting is integrated

with the organization which can be analysed form the comparison provided below:

Basis DSS (Decision Support

System)

ESS (Executive Support

System)

Users Professionals, Managers,

analysts.

Executives whether top level

or not, senior managers.

Use Difficult to use Simple to use

Decisions Decisions on the basis of the

highly automated software

where the communication

technology, knowledge, etc.

is used.

Best possible solution to the

problem is provided with the

help of education,

experience, etc.

Models Highly analytical models are

used.

Less use of the analytical

models (Olivia, 2011).

Example Charts, instant messaging,

etc.

Oracle Financial, etc.

The financial information which is provided is required to be relevant since it helps in

providing the undisputable information, creating strategies, maintaining the relationship

with customers, quantifying the purpose of business, optimizing and communicating

effectively and efficiently.

9

The management accounting system and the management accounting reporting is integrated

with the organization which can be analysed form the comparison provided below:

Basis DSS (Decision Support

System)

ESS (Executive Support

System)

Users Professionals, Managers,

analysts.

Executives whether top level

or not, senior managers.

Use Difficult to use Simple to use

Decisions Decisions on the basis of the

highly automated software

where the communication

technology, knowledge, etc.

is used.

Best possible solution to the

problem is provided with the

help of education,

experience, etc.

Models Highly analytical models are

used.

Less use of the analytical

models (Olivia, 2011).

Example Charts, instant messaging,

etc.

Oracle Financial, etc.

The financial information which is provided is required to be relevant since it helps in

providing the undisputable information, creating strategies, maintaining the relationship

with customers, quantifying the purpose of business, optimizing and communicating

effectively and efficiently.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

LO2 Techniques range for management accounting (P3, M2, D2)

P3 Cost computation and income statement

The amount incurred in the product or the service by the company is termed as the cost and

this will be increased to a certain extent and will be charged from the customer. The cost is

divided into different types which are variable, fixed, semi-variable, indirect, period cost,

product cost, direct cost, etc. For the analysis of the cost the different cost can be classified

in various forms like social cost, opportunity, relevant, sunk, implicit, explicit cost, past,

future cost, etc. To determine the change in cost and its effect on the volume of the company

will be possible with the help of the cost-volume-profit analysis. The change in the

environment requires the change in the level of activity and it can be done with the help of

the flexible budget. The difference in the actual and the budgeted cost is the variance of the

cost.

The absorption costing is the method which determines the cost and the profit by

considering the total cost of the product or the service. In absorption costing the cost of the

product or the service is taken on the basis of the average and then that cost is added to the

selling price of the service or the product. The cost will include the fixed and variable and

the profit will be calculated by calculating the gross profit (S, 2015).

The marginal costing is the method where the cost and the profit are calculated by

considering the variable cost only. In the marginal costing technique, the marginal cost is

calculated by adding the one unit extra cost to the one unit extra produced. The cost includes

only variable cost and hence the contribution is firstly calculated then the net profit is

calculated (S, 2015).

The cost which remains fixed irrespective of the change in the level of the activity is the

fixed cost while the cost which changes as per the change in the level of activity is termed

as a variable cost. Normal cost includes the cost of manufacturing i.e. the material, labour

cost and overhead and the expected cost when substituted for the actual cost is termed as the

standard cost.

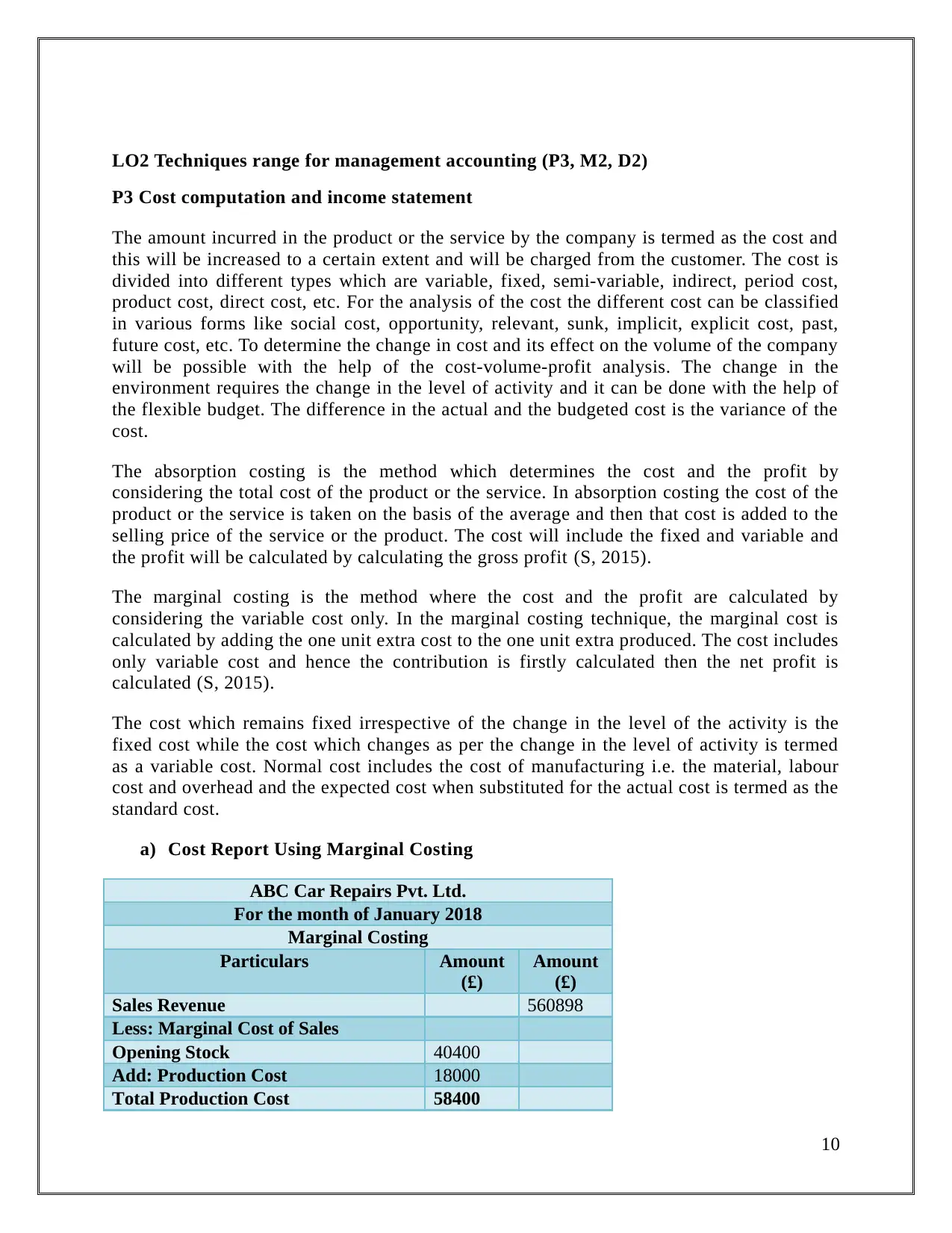

a) Cost Report Using Marginal Costing

ABC Car Repairs Pvt. Ltd.

For the month of January 2018

Marginal Costing

Particulars Amount

(£)

Amount

(£)

Sales Revenue 560898

Less: Marginal Cost of Sales

Opening Stock 40400

Add: Production Cost 18000

Total Production Cost 58400

10

P3 Cost computation and income statement

The amount incurred in the product or the service by the company is termed as the cost and

this will be increased to a certain extent and will be charged from the customer. The cost is

divided into different types which are variable, fixed, semi-variable, indirect, period cost,

product cost, direct cost, etc. For the analysis of the cost the different cost can be classified

in various forms like social cost, opportunity, relevant, sunk, implicit, explicit cost, past,

future cost, etc. To determine the change in cost and its effect on the volume of the company

will be possible with the help of the cost-volume-profit analysis. The change in the

environment requires the change in the level of activity and it can be done with the help of

the flexible budget. The difference in the actual and the budgeted cost is the variance of the

cost.

The absorption costing is the method which determines the cost and the profit by

considering the total cost of the product or the service. In absorption costing the cost of the

product or the service is taken on the basis of the average and then that cost is added to the

selling price of the service or the product. The cost will include the fixed and variable and

the profit will be calculated by calculating the gross profit (S, 2015).

The marginal costing is the method where the cost and the profit are calculated by

considering the variable cost only. In the marginal costing technique, the marginal cost is

calculated by adding the one unit extra cost to the one unit extra produced. The cost includes

only variable cost and hence the contribution is firstly calculated then the net profit is

calculated (S, 2015).

The cost which remains fixed irrespective of the change in the level of the activity is the

fixed cost while the cost which changes as per the change in the level of activity is termed

as a variable cost. Normal cost includes the cost of manufacturing i.e. the material, labour

cost and overhead and the expected cost when substituted for the actual cost is termed as the

standard cost.

a) Cost Report Using Marginal Costing

ABC Car Repairs Pvt. Ltd.

For the month of January 2018

Marginal Costing

Particulars Amount

(£)

Amount

(£)

Sales Revenue 560898

Less: Marginal Cost of Sales

Opening Stock 40400

Add: Production Cost 18000

Total Production Cost 58400

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Less: Closing Stock 25141

Marginal Cost of Production 33259

Add: Selling, Admin and Distribution

cost

19888 53147

Contribution 507751

Less: Fixed Cost 60000

Marginal Costing Profit 447751

b) Cost Report Using Absorption Costing

ABC Car Repairs Pvt. Ltd.

For the month of January 2018

Absorption Costing

Particulars Amount

(£)

Amount

(£)

Sales Revenue 560898

Less: Absorption Cost of Sales

Opening Stock 20200

Add: Production Cost 11000

Total Production Cost 31200

Less: Closing Stock 13202

Absorption Cost of Production 17998

Add: Selling, Admin and

Distribution cost

19888 37886

Un-adjusted Profit 523012

Fixed Production Overhead

absorbed

21000

Less: Fixed Production Overhead

incurred

11231

(Under)/Over Absorption 9769

Adjusted Profit 513243

c) Reconciliation Statement of Absorption and Marginal Costing Profits

Reconciliation Statement For Marginal and

Absorption Costing Profit

Particulars Amount

(£)

Marginal Costing Profit 447751

Add: (Closing Stock- Opening

Stock)*OAR

65492

Absorption Costing Profit 513243

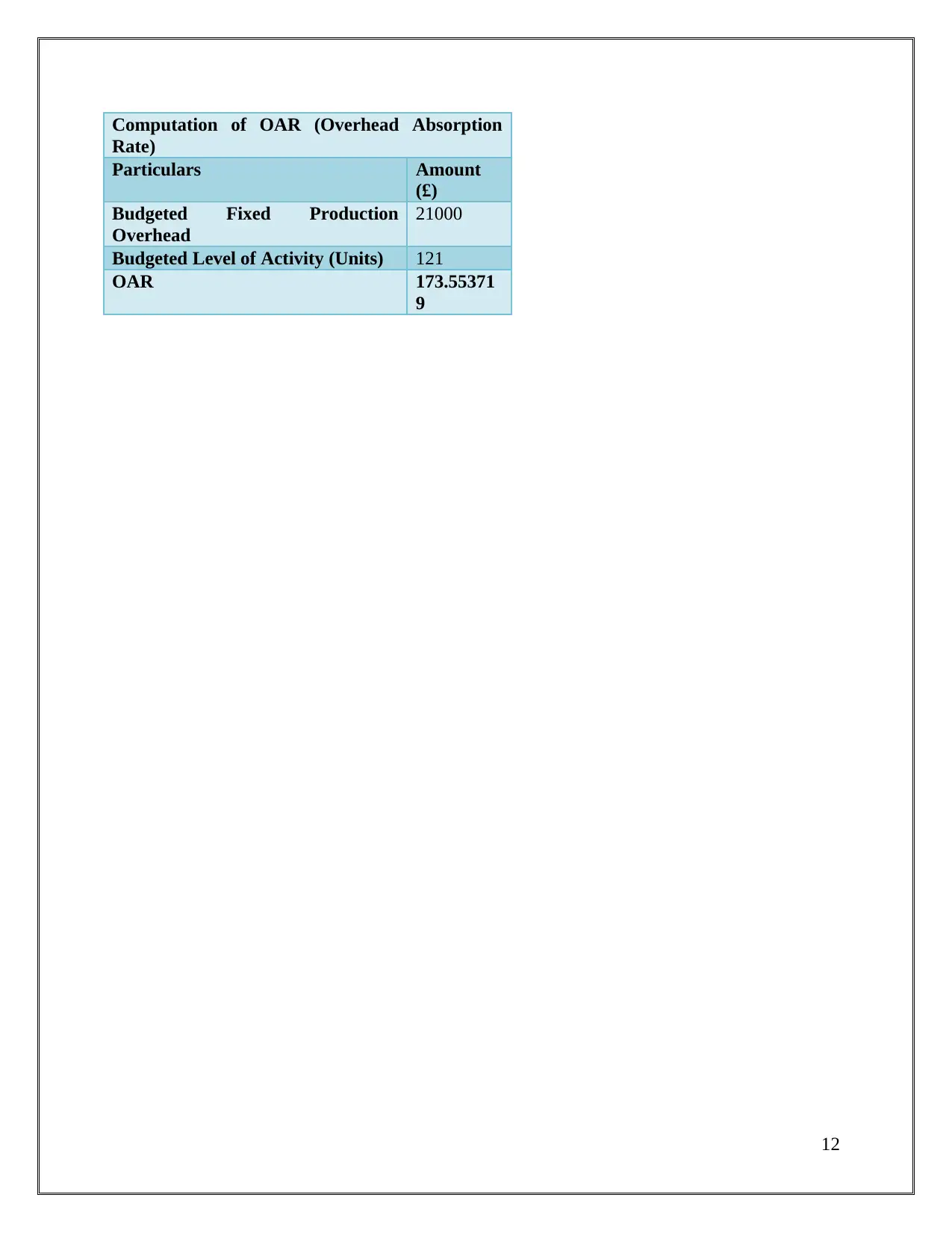

d) Compute OAR

11

Marginal Cost of Production 33259

Add: Selling, Admin and Distribution

cost

19888 53147

Contribution 507751

Less: Fixed Cost 60000

Marginal Costing Profit 447751

b) Cost Report Using Absorption Costing

ABC Car Repairs Pvt. Ltd.

For the month of January 2018

Absorption Costing

Particulars Amount

(£)

Amount

(£)

Sales Revenue 560898

Less: Absorption Cost of Sales

Opening Stock 20200

Add: Production Cost 11000

Total Production Cost 31200

Less: Closing Stock 13202

Absorption Cost of Production 17998

Add: Selling, Admin and

Distribution cost

19888 37886

Un-adjusted Profit 523012

Fixed Production Overhead

absorbed

21000

Less: Fixed Production Overhead

incurred

11231

(Under)/Over Absorption 9769

Adjusted Profit 513243

c) Reconciliation Statement of Absorption and Marginal Costing Profits

Reconciliation Statement For Marginal and

Absorption Costing Profit

Particulars Amount

(£)

Marginal Costing Profit 447751

Add: (Closing Stock- Opening

Stock)*OAR

65492

Absorption Costing Profit 513243

d) Compute OAR

11

Computation of OAR (Overhead Absorption

Rate)

Particulars Amount

(£)

Budgeted Fixed Production

Overhead

21000

Budgeted Level of Activity (Units) 121

OAR 173.55371

9

12

Rate)

Particulars Amount

(£)

Budgeted Fixed Production

Overhead

21000

Budgeted Level of Activity (Units) 121

OAR 173.55371

9

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 26

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.