Comprehensive Accounting Systems and Processes Analysis

VerifiedAdded on 2020/02/24

|36

|4795

|29

Homework Assignment

AI Summary

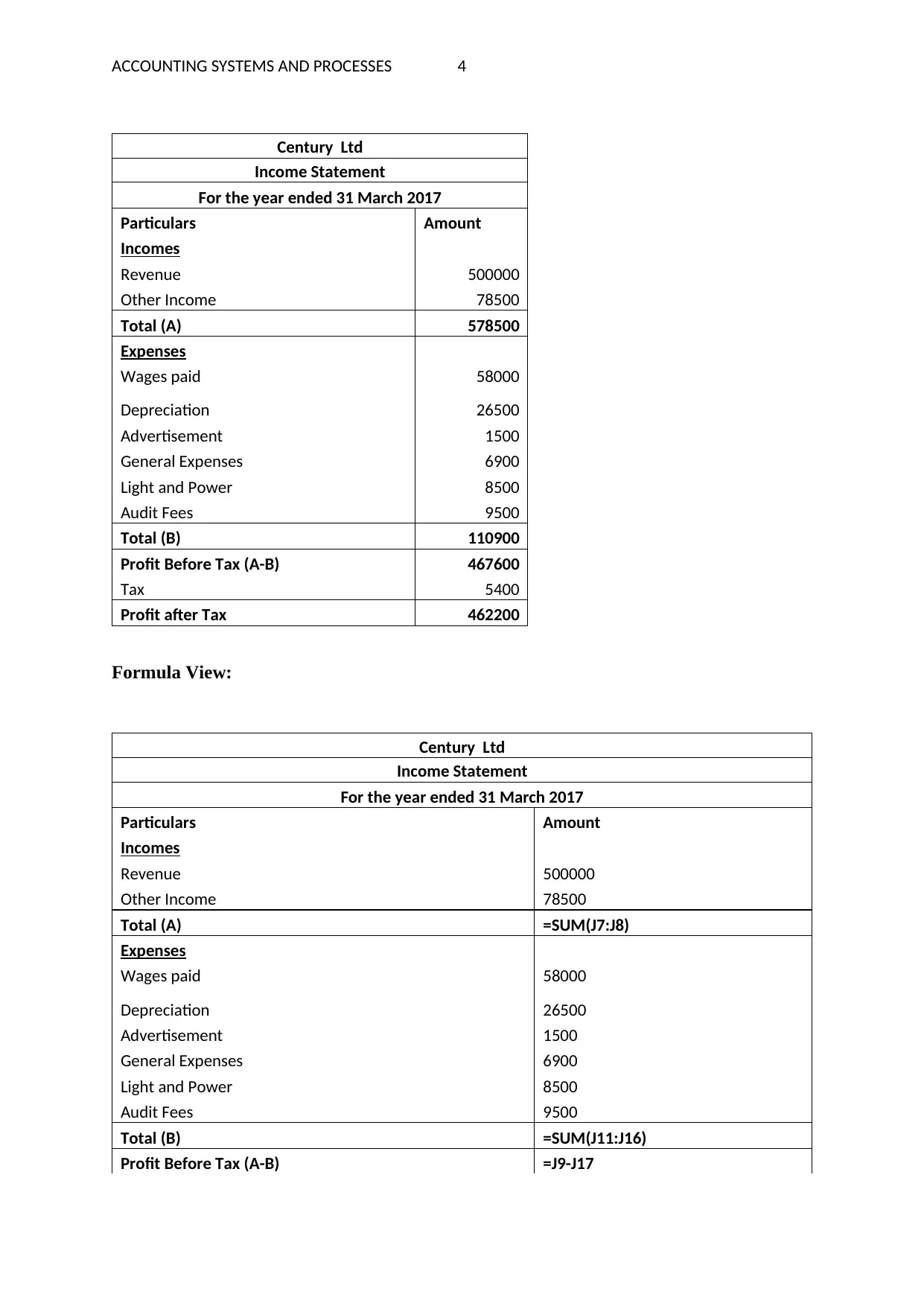

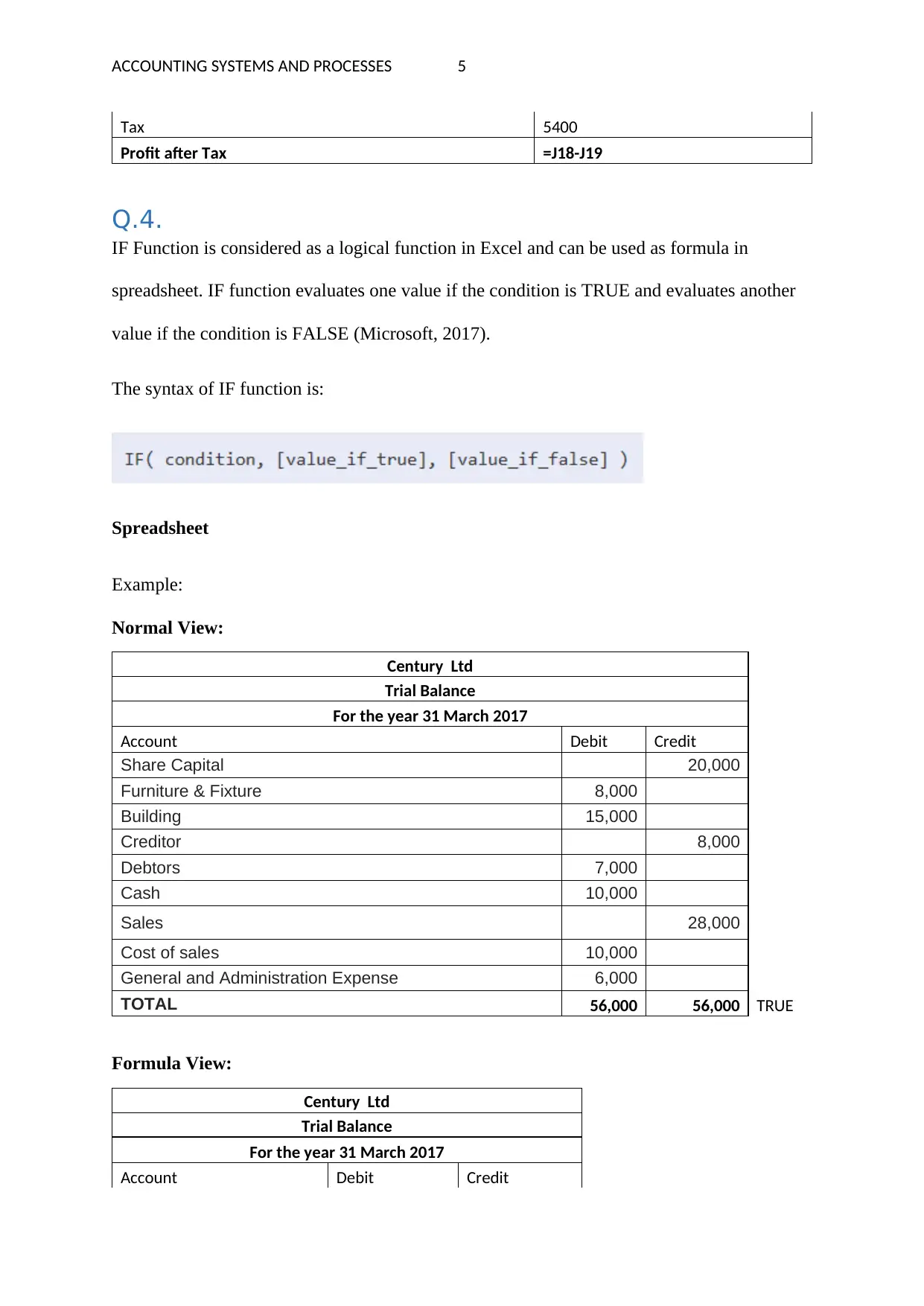

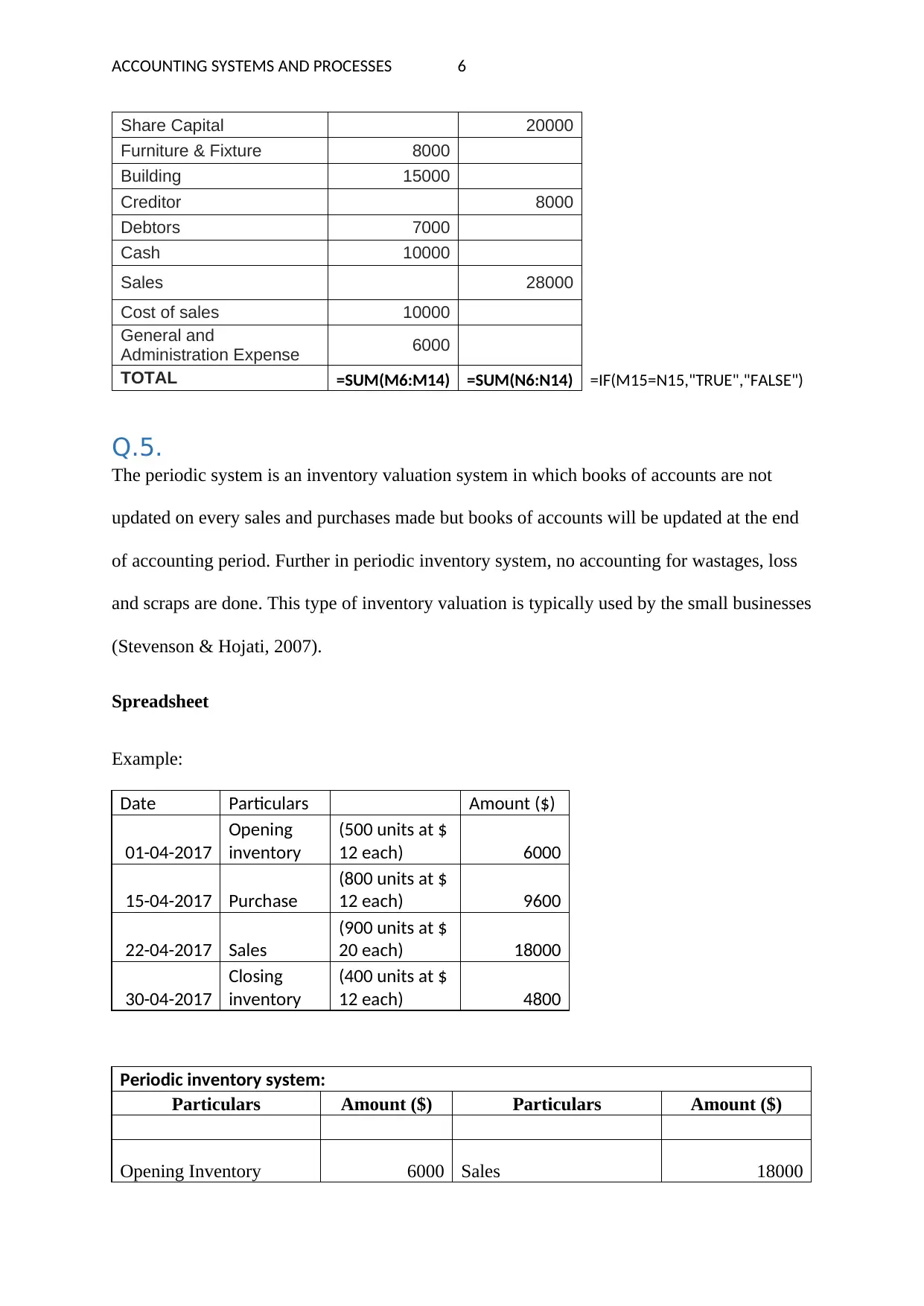

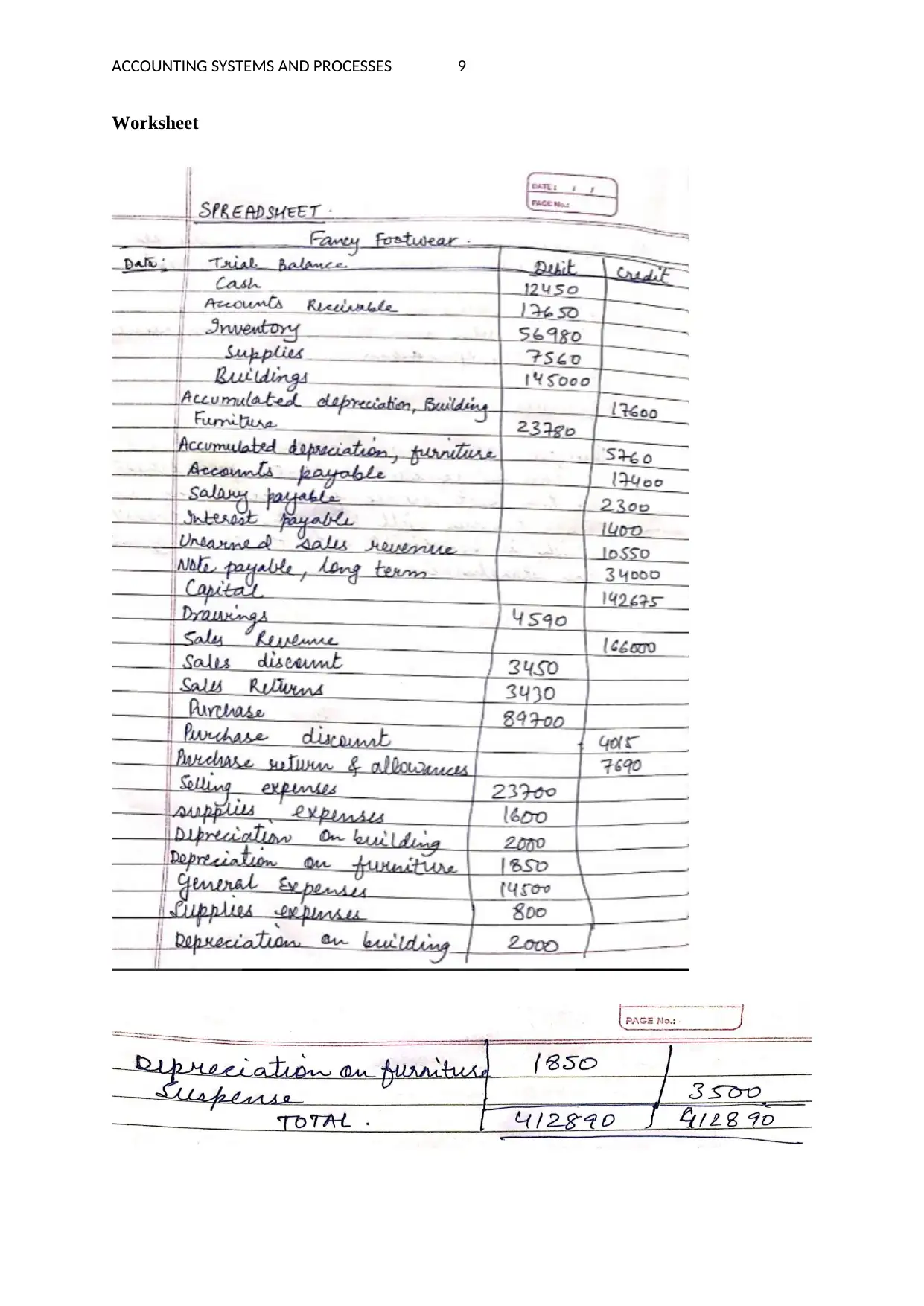

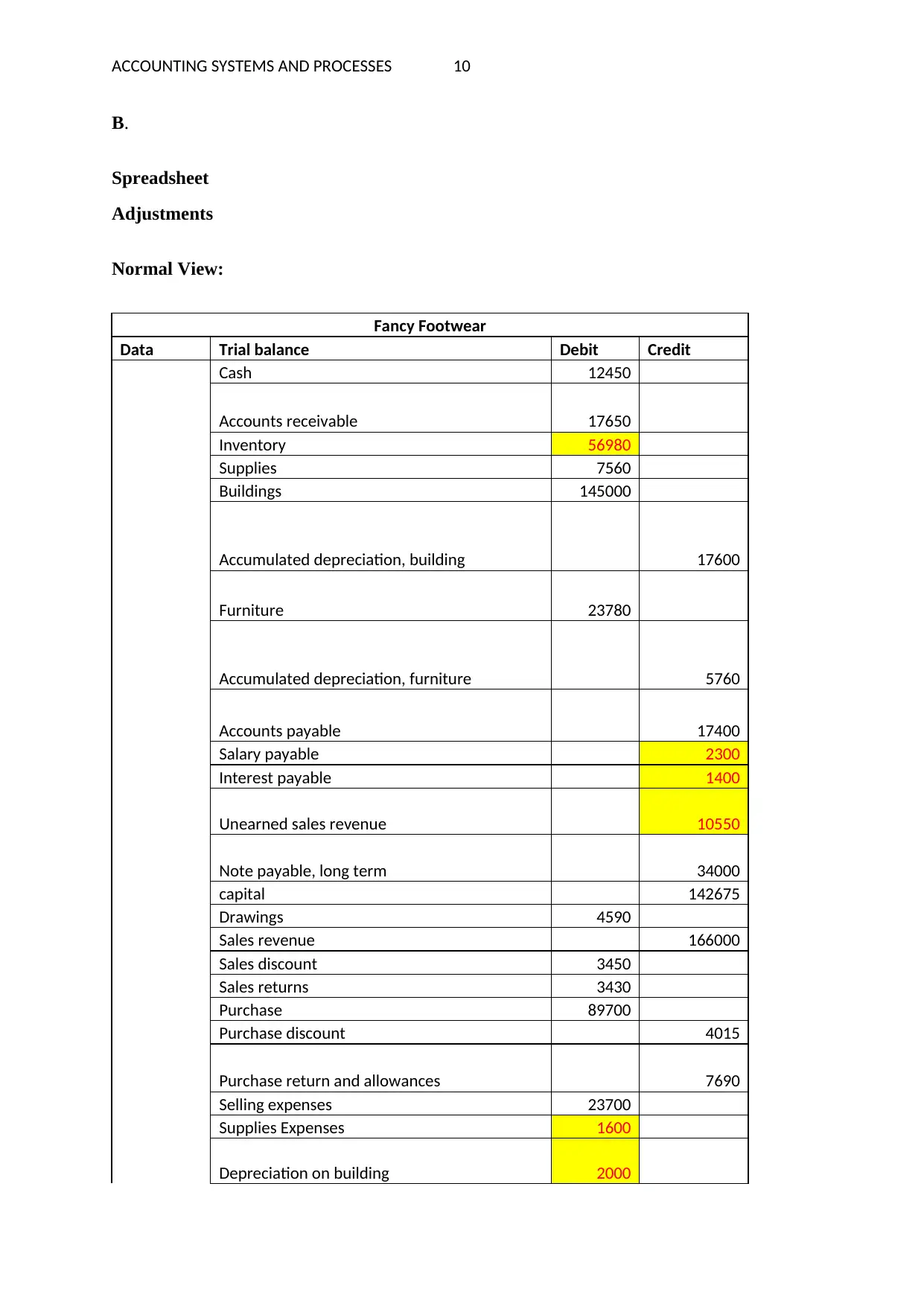

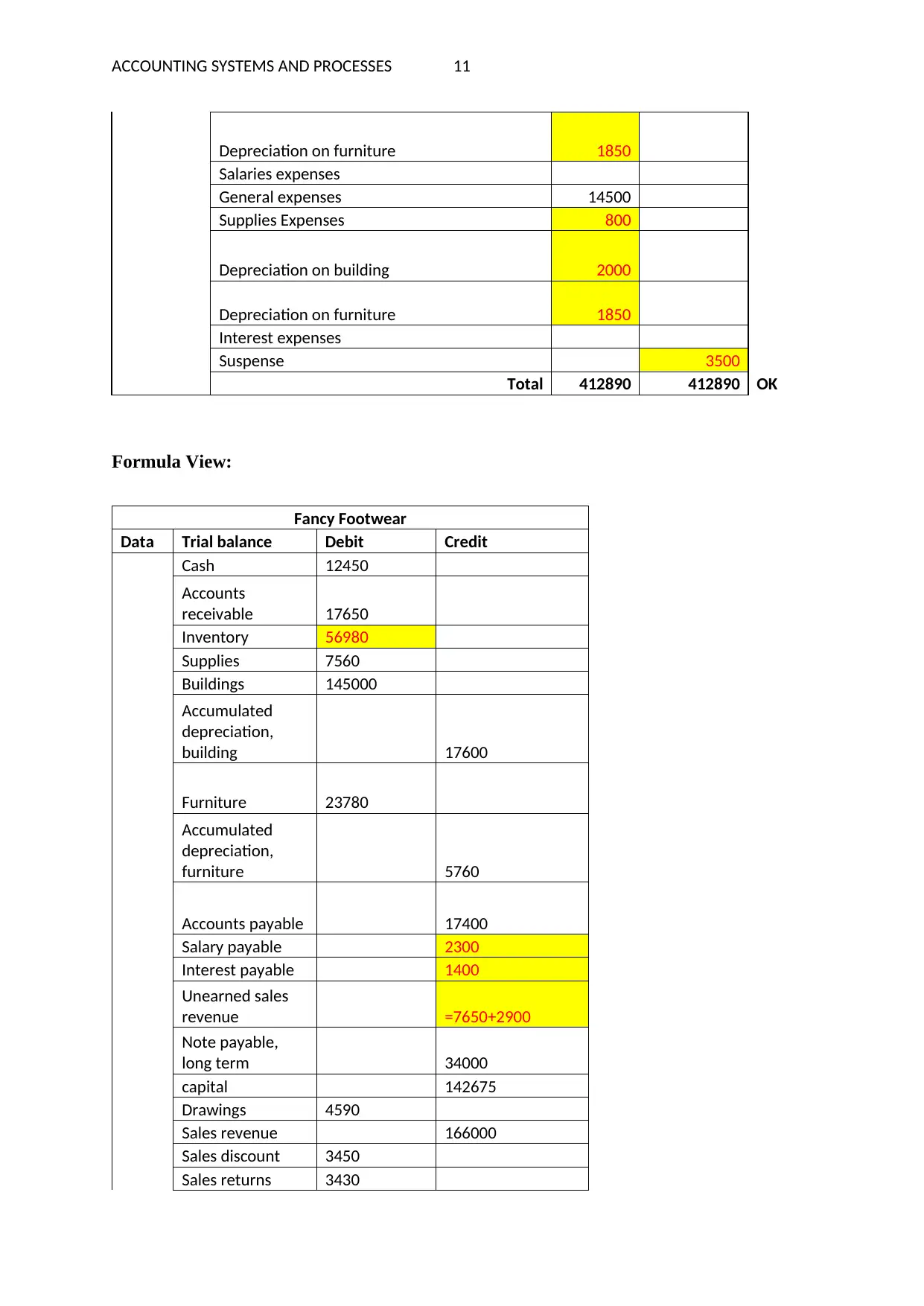

This assignment solution provides a comprehensive analysis of accounting systems and processes, covering various aspects such as cell referencing in Excel, the use of parentheses for negative numbers, designing spreadsheets with separate data entry and report areas, and the application of the IF function. It also delves into inventory valuation systems, specifically the periodic system, with examples. The solution includes a detailed spreadsheet for the trial balance, adjustments, and the benefits of using spreadsheets in accounting. Furthermore, the assignment explores inventory costing methods, including average cost, LIFO, and FIFO, with calculations and examples for a given scenario. The document presents both original and revised versions of the inventory costing problem, demonstrating the application of these methods in detail.

1 out of 36

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.