Management Accounting: Systems, Reporting, Budgeting and Control

VerifiedAdded on 2023/01/13

|15

|3062

|57

Report

AI Summary

This report provides a detailed analysis of management accounting systems, reporting methods, and budgetary control techniques. It begins by defining management accounting and its functions, comparing it with financial accounting and cost accounting systems. Various reporting methods, including trading and profit & loss accounts, income statements, balance sheets, and cash flow statements, are discussed. The report explores cost calculation techniques, such as marginal costing and absorption costing, and their application in preparing income statements. Different planning tools used for budgetary control, including sales budgets, production budgets, cash budgets, and flexible budgets, are evaluated. Furthermore, the report compares adaptation methods like benchmarks, key performance indicators, balanced scorecards, and budgetary targets, adopted by organizations in response to financial systems. It concludes by highlighting the importance of financial governance for sustainable success, emphasizing compliance and disclosure norms. Desklib provides access to this and many other solved assignments to help students excel.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

P1 Management accounting and different types of management accounting system. ...............1

P2 Methods used in MA reporting...............................................................................................3

M1 Benefits of MA and its application........................................................................................4

D1 Relationship of MA systems and reporting within organisation process. .............................4

P3 Cost calculations using appropriate techniques in cost analysis for preparing income

statements. ...................................................................................................................................4

M2 Management accounting techniques.....................................................................................5

D2 Financial reports accurately applying & interpreting data for the complex businesses.........5

P4 Different types of planning tools used for budgetary control................................................6

M3 Application in budgetary control...........................................................................................8

P5 Comparison of different adaptation methods adopted by organization for responding to

financial systems..........................................................................................................................8

M4 Sustainable success..............................................................................................................10

D3 Planning tools used to solve the financial problems............................................................10

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

P1 Management accounting and different types of management accounting system. ...............1

P2 Methods used in MA reporting...............................................................................................3

M1 Benefits of MA and its application........................................................................................4

D1 Relationship of MA systems and reporting within organisation process. .............................4

P3 Cost calculations using appropriate techniques in cost analysis for preparing income

statements. ...................................................................................................................................4

M2 Management accounting techniques.....................................................................................5

D2 Financial reports accurately applying & interpreting data for the complex businesses.........5

P4 Different types of planning tools used for budgetary control................................................6

M3 Application in budgetary control...........................................................................................8

P5 Comparison of different adaptation methods adopted by organization for responding to

financial systems..........................................................................................................................8

M4 Sustainable success..............................................................................................................10

D3 Planning tools used to solve the financial problems............................................................10

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION

Management accounting helps in preparation of different financial reports that help in

analysing the operation and performance of the business. This report will identify the use of

costing methods for ascertaining the financial performance and the different types of

management accounting systems that can be used. The report will also evaluate different

budgetary options and conclude how the management accounting tools can be used in an

organization.

MAIN BODY

P1 Management accounting and different types of management accounting system.

Management accounting is also known as managerial accounting. It is defined as process

of analysing the business costs & operations for preparing internal financial records, reports and

the account for helping the managers of company in decision making for achieving the goals and

objectives of business.

Functions of management accounting

MA provides financial information to internal management for decision making.

MA analyses cause and effects of facts and figures presented in the accounting reports

(Lasyoud, Haslam and Roslender, 2018).

It uses special techniques & concepts for mitigating the variances and interpretation of

data.

It makes efforts for improving the efficiency of employees working in the organisation.

It analyses both quantitative and qualitative reasons of the variances.

Financial accounting system

It could be defined as specialised accounting branch for keeping track of the financial

transactions of company. With the use of standard guidelines, transaction are recorded, than

summarized & presented in the financial reports or the financial statements like income

statement or balance sheet (McLaren, Appleyard and Mitchell, 2016).

Rules and procedures

Financial accounting runs on the rules and procedures laid down by the government

authorities for recording and representing the financial transactions. They have to follow the set

accounting standards for presenting the financial statements.

1

Management accounting helps in preparation of different financial reports that help in

analysing the operation and performance of the business. This report will identify the use of

costing methods for ascertaining the financial performance and the different types of

management accounting systems that can be used. The report will also evaluate different

budgetary options and conclude how the management accounting tools can be used in an

organization.

MAIN BODY

P1 Management accounting and different types of management accounting system.

Management accounting is also known as managerial accounting. It is defined as process

of analysing the business costs & operations for preparing internal financial records, reports and

the account for helping the managers of company in decision making for achieving the goals and

objectives of business.

Functions of management accounting

MA provides financial information to internal management for decision making.

MA analyses cause and effects of facts and figures presented in the accounting reports

(Lasyoud, Haslam and Roslender, 2018).

It uses special techniques & concepts for mitigating the variances and interpretation of

data.

It makes efforts for improving the efficiency of employees working in the organisation.

It analyses both quantitative and qualitative reasons of the variances.

Financial accounting system

It could be defined as specialised accounting branch for keeping track of the financial

transactions of company. With the use of standard guidelines, transaction are recorded, than

summarized & presented in the financial reports or the financial statements like income

statement or balance sheet (McLaren, Appleyard and Mitchell, 2016).

Rules and procedures

Financial accounting runs on the rules and procedures laid down by the government

authorities for recording and representing the financial transactions. They have to follow the set

accounting standards for presenting the financial statements.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Accounting information systems

Accounting information systems are the structures that business uses for collecting,

storing, managing, processing, retrieving and reporting the financial data so that it could be used

by consultants, accountants, business analysts, CFO regulators and auditors.

Internal control

There should be strong internal control within the organisation so that all the information

provided by accounts is accurate and reliable. The control should be laid at every level from

where the information is being received. It is the duty of executives to ensure that all the

information are being provided are correct.

Auditing

In financial accounting all the financial information is audited by the auditors (Burritt,

2017). They ensure that all the information is being recorded using the appropriate accounting

standards. They also ensure that the information provided in the financial statements is free from

material misstatements.

Cost Accounting systems

It refers to business practice where the organisations are concerned with recording,

summarizing and studying the cost spent by company over any service, process, products or

anything in organisation. Such kind of financial statements give management visibility of their

cost informations.

Product costing

Product costing refers to costs incurred for manufacturing the product item. These cost

includes direct materials, direct labour, consumable production supply and factory overheads.

Product costs are presented in financial statements as it includes manufacturing overheads as

required by IFRS.

Activity Based Costing

ABC refers to costing method identifying the activities in organisation and assigning cost

of every activity to the products & services as per actual consumption by every activity. The

model assigns indirect costs to direct costs in comparison with conventional costings.

Management accounting system

2

Accounting information systems are the structures that business uses for collecting,

storing, managing, processing, retrieving and reporting the financial data so that it could be used

by consultants, accountants, business analysts, CFO regulators and auditors.

Internal control

There should be strong internal control within the organisation so that all the information

provided by accounts is accurate and reliable. The control should be laid at every level from

where the information is being received. It is the duty of executives to ensure that all the

information are being provided are correct.

Auditing

In financial accounting all the financial information is audited by the auditors (Burritt,

2017). They ensure that all the information is being recorded using the appropriate accounting

standards. They also ensure that the information provided in the financial statements is free from

material misstatements.

Cost Accounting systems

It refers to business practice where the organisations are concerned with recording,

summarizing and studying the cost spent by company over any service, process, products or

anything in organisation. Such kind of financial statements give management visibility of their

cost informations.

Product costing

Product costing refers to costs incurred for manufacturing the product item. These cost

includes direct materials, direct labour, consumable production supply and factory overheads.

Product costs are presented in financial statements as it includes manufacturing overheads as

required by IFRS.

Activity Based Costing

ABC refers to costing method identifying the activities in organisation and assigning cost

of every activity to the products & services as per actual consumption by every activity. The

model assigns indirect costs to direct costs in comparison with conventional costings.

Management accounting system

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Management accounting is used by organisations for helping them in making effective

decision making process. By making budgets for processes they keep control over costs. By

applying various concepts and techniques management accounting maintain the profitability.

P2 Methods used in MA reporting.

The purpose and uses ;

Trading and profit or loss account - Trading account is prepared by entities for showing results

of the trading activities that are purchases and sale of goods. Profit & loss account is prepared for

identifying the profits actually earned or sustained loss from business. It is used for decision

making.

COGS - It is prepared for knowing the actual costs of the goods that are sold by business during

the year considering opening and closing inventory.

Income Statement – It is prepared for knowing the profits left with company after incurring all

the costs associated with business. It is used for knowing the profitability of business (Ameen,

Ahmed and Hafez, 2018).

Balance sheet – Balance sheet is prepared for representing the assets and liabilities of business.

It is used for identifying the financial position of business.

Cash flow statement – Cash flow statements is prepared for recording the cash inflow and

outflow from business. It is used to know the liquidity of company.

Inventory management system

Inventory management refers to the management of inventory within organisation.

Organisations incur costs for implementing inventory management system. This ensures the

availability of inventory for the production and keeps track record of all the finished goods

inventory. Inventory management systems installed in the warehouses.

Job Costing

In job costing all the costs incurred for the job are identified separately. All the costs

associated with job are recorded by the organisations. It is the most useful method of MA as it

helps in knowing the cost of each job in manufacturing the product (Järvinen, 2016). It provides

for optimum use of the resources so that less wastage is resulted with high level of the

production. Like the cost of dying the c

3

decision making process. By making budgets for processes they keep control over costs. By

applying various concepts and techniques management accounting maintain the profitability.

P2 Methods used in MA reporting.

The purpose and uses ;

Trading and profit or loss account - Trading account is prepared by entities for showing results

of the trading activities that are purchases and sale of goods. Profit & loss account is prepared for

identifying the profits actually earned or sustained loss from business. It is used for decision

making.

COGS - It is prepared for knowing the actual costs of the goods that are sold by business during

the year considering opening and closing inventory.

Income Statement – It is prepared for knowing the profits left with company after incurring all

the costs associated with business. It is used for knowing the profitability of business (Ameen,

Ahmed and Hafez, 2018).

Balance sheet – Balance sheet is prepared for representing the assets and liabilities of business.

It is used for identifying the financial position of business.

Cash flow statement – Cash flow statements is prepared for recording the cash inflow and

outflow from business. It is used to know the liquidity of company.

Inventory management system

Inventory management refers to the management of inventory within organisation.

Organisations incur costs for implementing inventory management system. This ensures the

availability of inventory for the production and keeps track record of all the finished goods

inventory. Inventory management systems installed in the warehouses.

Job Costing

In job costing all the costs incurred for the job are identified separately. All the costs

associated with job are recorded by the organisations. It is the most useful method of MA as it

helps in knowing the cost of each job in manufacturing the product (Järvinen, 2016). It provides

for optimum use of the resources so that less wastage is resulted with high level of the

production. Like the cost of dying the c

3

M1 Benefits of MA and its application.

MA helps in maintaining and improving the profitability of company. They are applied in

the internal management of company. They are applied in the production processes for reducing

the costs of product and increasing profit margins.

D1 Relationship of MA systems and reporting within organisation process.

Both systems and reporting are integrated as the reports are prepared on the basis of

accounting systems being followed. In each accounting systems different expenses are incurred

requiring separate cash flows that are reported in the accounting reports (Bento, Mertins and

White, 2018). Therefore reports cannot be prepared without the information in management

accounting systems

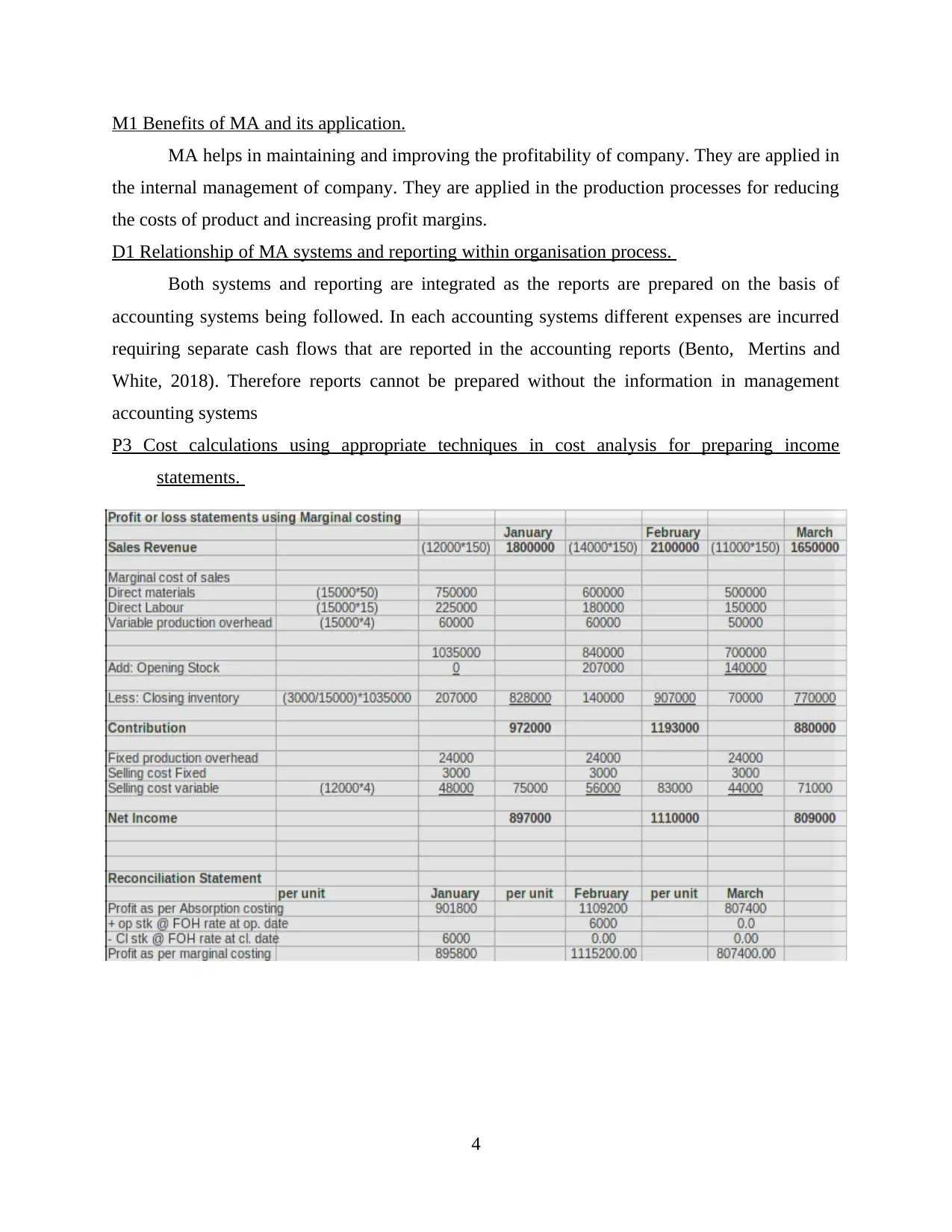

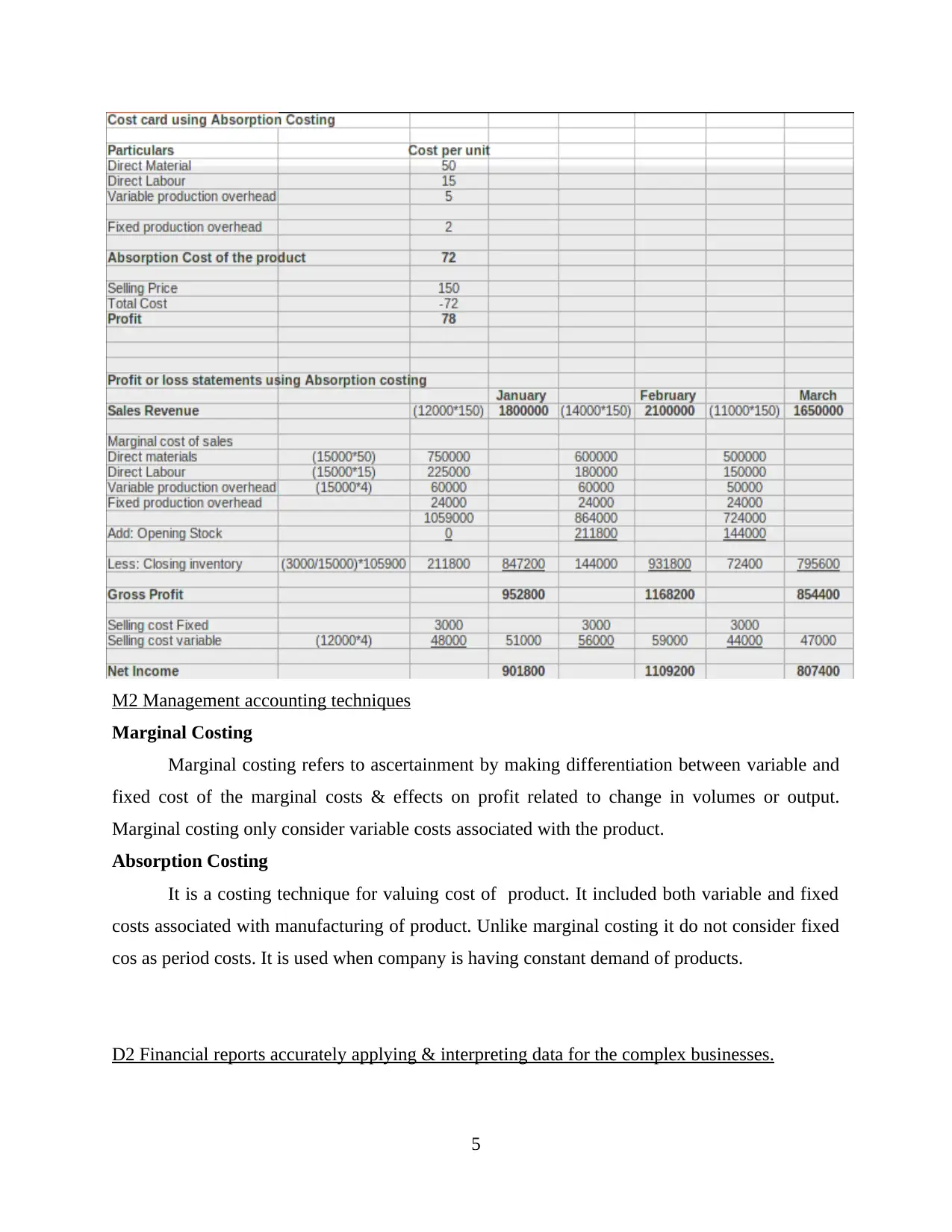

P3 Cost calculations using appropriate techniques in cost analysis for preparing income

statements.

4

MA helps in maintaining and improving the profitability of company. They are applied in

the internal management of company. They are applied in the production processes for reducing

the costs of product and increasing profit margins.

D1 Relationship of MA systems and reporting within organisation process.

Both systems and reporting are integrated as the reports are prepared on the basis of

accounting systems being followed. In each accounting systems different expenses are incurred

requiring separate cash flows that are reported in the accounting reports (Bento, Mertins and

White, 2018). Therefore reports cannot be prepared without the information in management

accounting systems

P3 Cost calculations using appropriate techniques in cost analysis for preparing income

statements.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

M2 Management accounting techniques

Marginal Costing

Marginal costing refers to ascertainment by making differentiation between variable and

fixed cost of the marginal costs & effects on profit related to change in volumes or output.

Marginal costing only consider variable costs associated with the product.

Absorption Costing

It is a costing technique for valuing cost of product. It included both variable and fixed

costs associated with manufacturing of product. Unlike marginal costing it do not consider fixed

cos as period costs. It is used when company is having constant demand of products.

D2 Financial reports accurately applying & interpreting data for the complex businesses.

5

Marginal Costing

Marginal costing refers to ascertainment by making differentiation between variable and

fixed cost of the marginal costs & effects on profit related to change in volumes or output.

Marginal costing only consider variable costs associated with the product.

Absorption Costing

It is a costing technique for valuing cost of product. It included both variable and fixed

costs associated with manufacturing of product. Unlike marginal costing it do not consider fixed

cos as period costs. It is used when company is having constant demand of products.

D2 Financial reports accurately applying & interpreting data for the complex businesses.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Cost

Cost in business refers to the monetary valuation for efforts, material, resources, time and

the utilities consumed, risks and opportunity forgone for producing or delivering goods or

services.

Product costing

It provides the costs that are incurred for producing a product. It includes both variable

and fixed costs. Variable costs includes cost of material, labour and variable production

overheads. Fixed costs are the factory rent, power and heat. Cost are allocated to products as

variables and fixed. Variable cost changes with change in volume where the fixed costs remain

fixed irrespective of volume.

Normal costing

It is used for deriving costs. In this costing method actual data are used for derivation of cost of

product with exceptions to manufacturing overheads rate.

Standard costing

Standard costing helps in ascertaining the ideal cost within which the production of the related

goods or service must be completed and this is then compared with the actual cost.

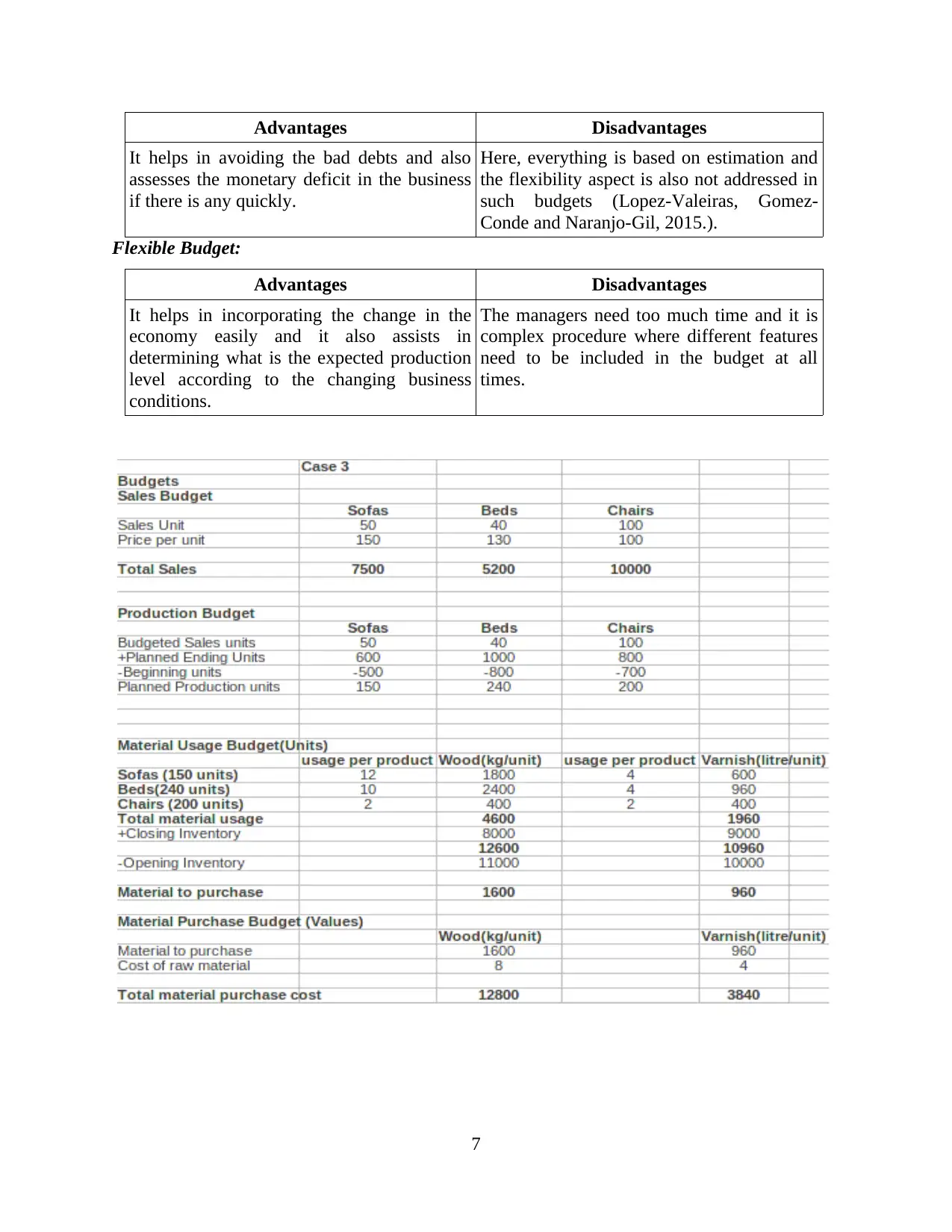

P4 Different types of planning tools used for budgetary control

Sales Budget:

Advantages Disadvantages

Sales budget helps in estimating the revenue

that the company will earn and it also helps

in planning for the resources in advance

(Maas, Schaltegger and Crutzen, 2016).

Sales budget is not an adequate budget as it

does not take into consideration the changing

trends on which sales is based.

Production Budget:

Advantages Disadvantages

The major advantage of production budget is

that it helps in ascertaining what will be the

production level and therefore helps in

revenue prediction as well.

The disadvantage of this budget is that it is a

time-consuming process where the managers

have to take into account different associated

products in order to estimate the production

units.

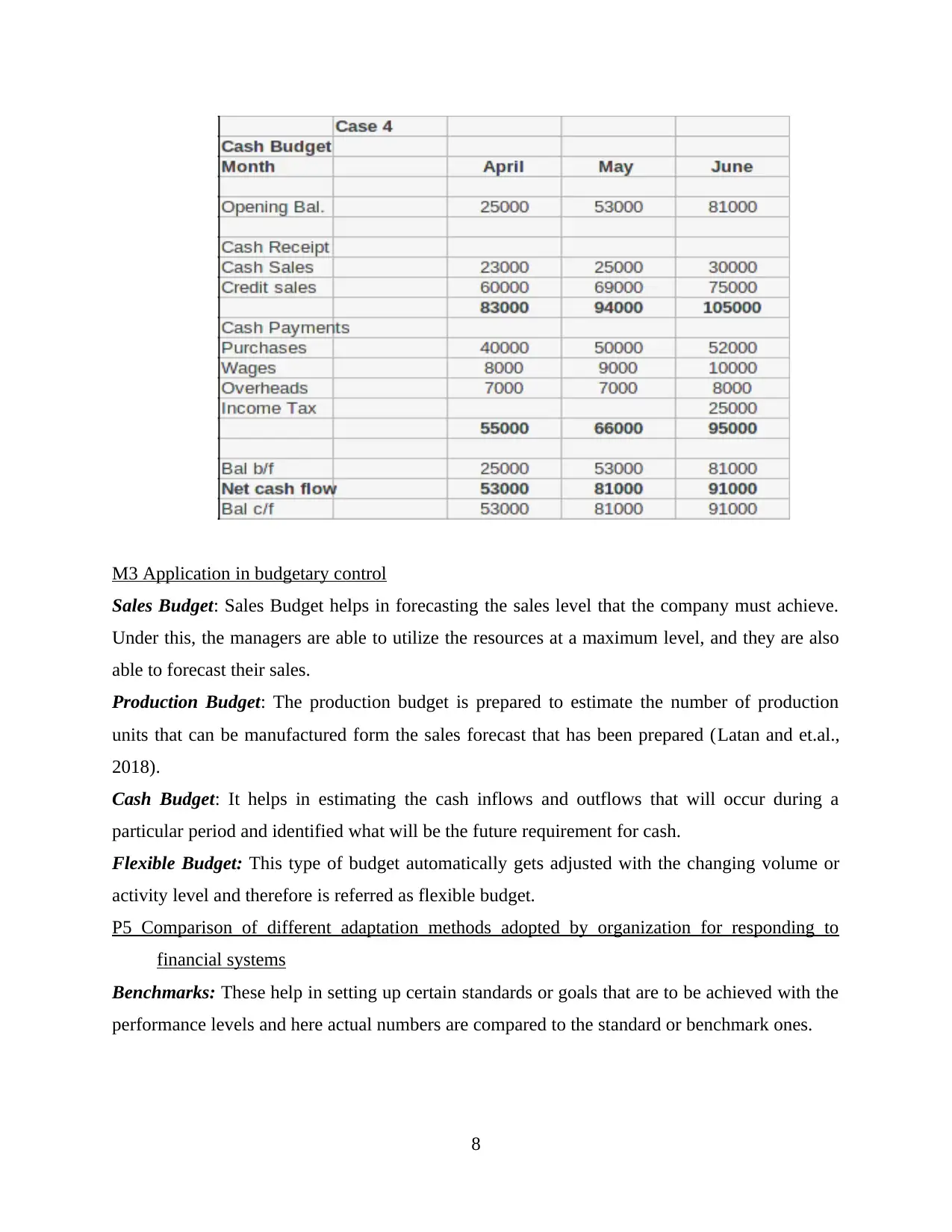

Cash Budget:

6

Cost in business refers to the monetary valuation for efforts, material, resources, time and

the utilities consumed, risks and opportunity forgone for producing or delivering goods or

services.

Product costing

It provides the costs that are incurred for producing a product. It includes both variable

and fixed costs. Variable costs includes cost of material, labour and variable production

overheads. Fixed costs are the factory rent, power and heat. Cost are allocated to products as

variables and fixed. Variable cost changes with change in volume where the fixed costs remain

fixed irrespective of volume.

Normal costing

It is used for deriving costs. In this costing method actual data are used for derivation of cost of

product with exceptions to manufacturing overheads rate.

Standard costing

Standard costing helps in ascertaining the ideal cost within which the production of the related

goods or service must be completed and this is then compared with the actual cost.

P4 Different types of planning tools used for budgetary control

Sales Budget:

Advantages Disadvantages

Sales budget helps in estimating the revenue

that the company will earn and it also helps

in planning for the resources in advance

(Maas, Schaltegger and Crutzen, 2016).

Sales budget is not an adequate budget as it

does not take into consideration the changing

trends on which sales is based.

Production Budget:

Advantages Disadvantages

The major advantage of production budget is

that it helps in ascertaining what will be the

production level and therefore helps in

revenue prediction as well.

The disadvantage of this budget is that it is a

time-consuming process where the managers

have to take into account different associated

products in order to estimate the production

units.

Cash Budget:

6

Advantages Disadvantages

It helps in avoiding the bad debts and also

assesses the monetary deficit in the business

if there is any quickly.

Here, everything is based on estimation and

the flexibility aspect is also not addressed in

such budgets (Lopez-Valeiras, Gomez-

Conde and Naranjo-Gil, 2015.).

Flexible Budget:

Advantages Disadvantages

It helps in incorporating the change in the

economy easily and it also assists in

determining what is the expected production

level according to the changing business

conditions.

The managers need too much time and it is

complex procedure where different features

need to be included in the budget at all

times.

7

It helps in avoiding the bad debts and also

assesses the monetary deficit in the business

if there is any quickly.

Here, everything is based on estimation and

the flexibility aspect is also not addressed in

such budgets (Lopez-Valeiras, Gomez-

Conde and Naranjo-Gil, 2015.).

Flexible Budget:

Advantages Disadvantages

It helps in incorporating the change in the

economy easily and it also assists in

determining what is the expected production

level according to the changing business

conditions.

The managers need too much time and it is

complex procedure where different features

need to be included in the budget at all

times.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

M3 Application in budgetary control

Sales Budget: Sales Budget helps in forecasting the sales level that the company must achieve.

Under this, the managers are able to utilize the resources at a maximum level, and they are also

able to forecast their sales.

Production Budget: The production budget is prepared to estimate the number of production

units that can be manufactured form the sales forecast that has been prepared (Latan and et.al.,

2018).

Cash Budget: It helps in estimating the cash inflows and outflows that will occur during a

particular period and identified what will be the future requirement for cash.

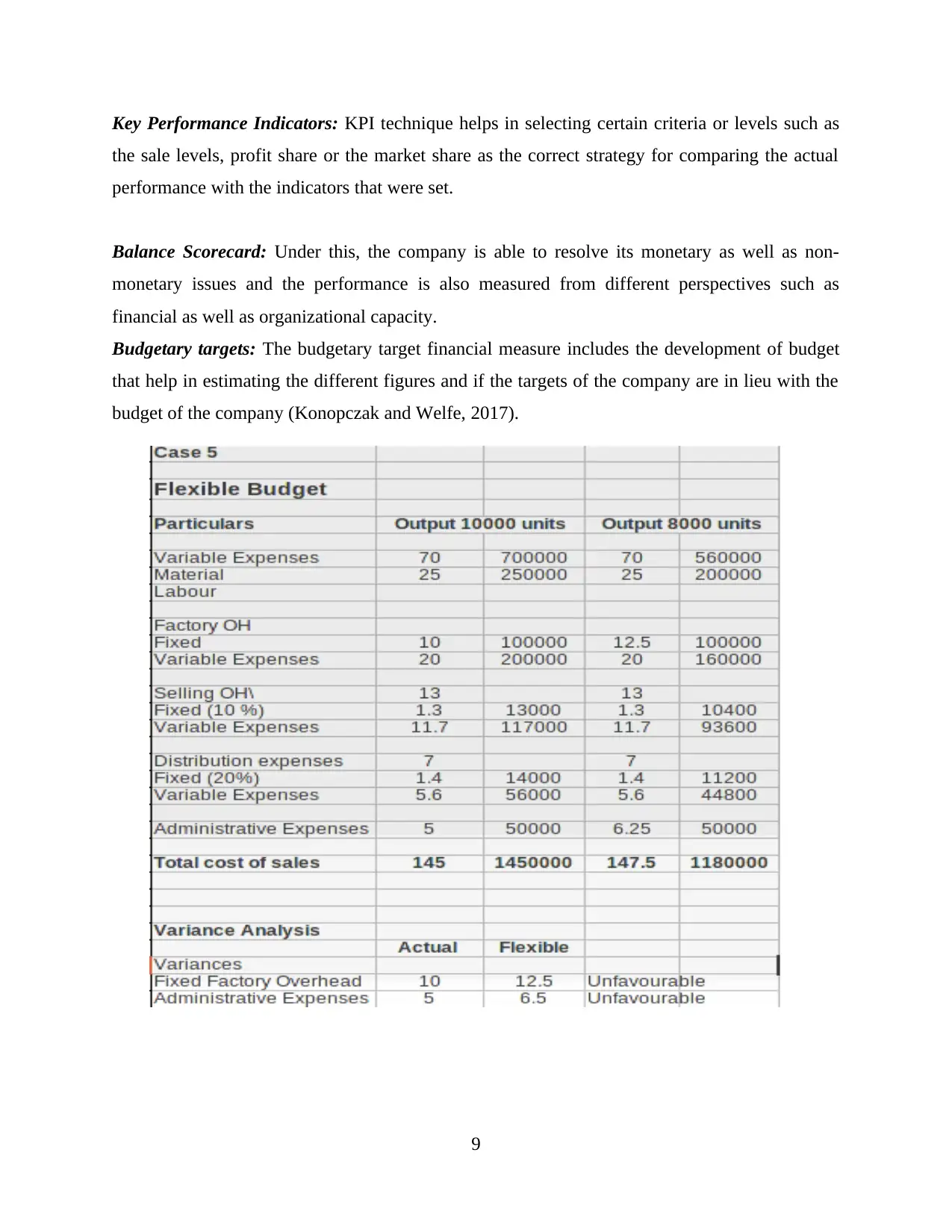

Flexible Budget: This type of budget automatically gets adjusted with the changing volume or

activity level and therefore is referred as flexible budget.

P5 Comparison of different adaptation methods adopted by organization for responding to

financial systems

Benchmarks: These help in setting up certain standards or goals that are to be achieved with the

performance levels and here actual numbers are compared to the standard or benchmark ones.

8

Sales Budget: Sales Budget helps in forecasting the sales level that the company must achieve.

Under this, the managers are able to utilize the resources at a maximum level, and they are also

able to forecast their sales.

Production Budget: The production budget is prepared to estimate the number of production

units that can be manufactured form the sales forecast that has been prepared (Latan and et.al.,

2018).

Cash Budget: It helps in estimating the cash inflows and outflows that will occur during a

particular period and identified what will be the future requirement for cash.

Flexible Budget: This type of budget automatically gets adjusted with the changing volume or

activity level and therefore is referred as flexible budget.

P5 Comparison of different adaptation methods adopted by organization for responding to

financial systems

Benchmarks: These help in setting up certain standards or goals that are to be achieved with the

performance levels and here actual numbers are compared to the standard or benchmark ones.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Key Performance Indicators: KPI technique helps in selecting certain criteria or levels such as

the sale levels, profit share or the market share as the correct strategy for comparing the actual

performance with the indicators that were set.

Balance Scorecard: Under this, the company is able to resolve its monetary as well as non-

monetary issues and the performance is also measured from different perspectives such as

financial as well as organizational capacity.

Budgetary targets: The budgetary target financial measure includes the development of budget

that help in estimating the different figures and if the targets of the company are in lieu with the

budget of the company (Konopczak and Welfe, 2017).

9

the sale levels, profit share or the market share as the correct strategy for comparing the actual

performance with the indicators that were set.

Balance Scorecard: Under this, the company is able to resolve its monetary as well as non-

monetary issues and the performance is also measured from different perspectives such as

financial as well as organizational capacity.

Budgetary targets: The budgetary target financial measure includes the development of budget

that help in estimating the different figures and if the targets of the company are in lieu with the

budget of the company (Konopczak and Welfe, 2017).

9

M4 Sustainable success

Financial governance: This indicates the manner in which the monetary or financial information

is gathered stored, managed, monitored and controlled by the organization or its management

team. There are various compliance as well as disclosure norms that are attained under the

financial governance and this can be used to identify and root out the loopholes that exist in the

managerial process of the company. The company is able to expand their profitability level along

with the goodwill and managerial efficiency but the compliance norms are very rigid in nature.

Characteristics of management accountant: A management accountant needs to be prudent in

their role and responsibilities where they need to evaluate the performance of the businesses, the

different budgeting techniques, the various accounting strategy development and implementation

and also the usage of the information systems that are linked to the management accounting

systems (Granlund and Lukka, 2017). There are various skills that the management accountant

needs to possess and these include quick decision-making, adept in using different analytical

tools, capable of developing useful insights etc. and these will help in improving the efficiency

of the company collectively.

D3 Planning tools used to solve the financial problems

Benchmarks:

Advantages Disadvantages

It helps in improving the performance and

motivates the employees to meet the standards

that have been set.

The information that is provided under this is

insufficient for predicting the future and the

customer might not be completely satisfied.

Key Performance Indicators:

Advantages Disadvantages

It helps in easily identifying the key

performance of the employees and ultimately

the progress of organization can also be

tracked.

The technique does not incorporate innovation

into its practices and ultimately the quality gets

compromised due to the achievement of key

level that has been set.

Balance Scorecard:

Advantages Disadvantages

This technique shows the performance of the

company and it also helps in integrating the

performance with the vision and mission of the

It is an extremely time-consuming process and

the technique is also expensive because it

involves both financial and non-financial

10

Financial governance: This indicates the manner in which the monetary or financial information

is gathered stored, managed, monitored and controlled by the organization or its management

team. There are various compliance as well as disclosure norms that are attained under the

financial governance and this can be used to identify and root out the loopholes that exist in the

managerial process of the company. The company is able to expand their profitability level along

with the goodwill and managerial efficiency but the compliance norms are very rigid in nature.

Characteristics of management accountant: A management accountant needs to be prudent in

their role and responsibilities where they need to evaluate the performance of the businesses, the

different budgeting techniques, the various accounting strategy development and implementation

and also the usage of the information systems that are linked to the management accounting

systems (Granlund and Lukka, 2017). There are various skills that the management accountant

needs to possess and these include quick decision-making, adept in using different analytical

tools, capable of developing useful insights etc. and these will help in improving the efficiency

of the company collectively.

D3 Planning tools used to solve the financial problems

Benchmarks:

Advantages Disadvantages

It helps in improving the performance and

motivates the employees to meet the standards

that have been set.

The information that is provided under this is

insufficient for predicting the future and the

customer might not be completely satisfied.

Key Performance Indicators:

Advantages Disadvantages

It helps in easily identifying the key

performance of the employees and ultimately

the progress of organization can also be

tracked.

The technique does not incorporate innovation

into its practices and ultimately the quality gets

compromised due to the achievement of key

level that has been set.

Balance Scorecard:

Advantages Disadvantages

This technique shows the performance of the

company and it also helps in integrating the

performance with the vision and mission of the

It is an extremely time-consuming process and

the technique is also expensive because it

involves both financial and non-financial

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.