HA2042 Case Study: Evaluating Adam & Co.'s Accounting Systems

VerifiedAdded on 2022/11/25

|13

|3183

|441

Case Study

AI Summary

This case study examines the accounting information systems of Adam & Co., a wholesale industrial supplies business. The report analyzes the purchases, cash disbursements, and payroll systems using flowcharts to illustrate their processes. It identifies weaknesses in each system, such as excess staffing in purchases, lack of supervision in cash disbursements, and potential for fraud. The analysis includes risks associated with foreign suppliers, quality control, and budget allocation. The study concludes by offering recommendations to improve internal controls, address inefficiencies, and mitigate risks within each accounting system. The assignment emphasizes the importance of efficient accounting practices and robust internal controls for business operations. This analysis is provided by a student and available on Desklib, a platform offering AI-driven study tools.

Running head: ACCOUNTING INFORMATION SYSTEM

Accounting Information System

Name of the Student

Name of the University

Author Note

Accounting Information System

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1CASE STUDY – ADAM & CO.

Executive Summary

The primary purpose of this report is to conduct a thorough evaluation of the various internal

control systems of the company Adam &Co. These systems include the purchase, cash

disbursements and the payroll system. An overview of the systems is initially presented with the

help of flowcharts. This is useful in providing a brief and accurate analysis of the systems

implemented by the company. In order to obtain an idea of the strengths and weaknesses of

every type of internal system, an analysis of the available sources of literature is conducted.

After this, the report ends with providing advice to Adam &Co. about the ways in which their

existing weaknesses in each of the department can be overcome.

Executive Summary

The primary purpose of this report is to conduct a thorough evaluation of the various internal

control systems of the company Adam &Co. These systems include the purchase, cash

disbursements and the payroll system. An overview of the systems is initially presented with the

help of flowcharts. This is useful in providing a brief and accurate analysis of the systems

implemented by the company. In order to obtain an idea of the strengths and weaknesses of

every type of internal system, an analysis of the available sources of literature is conducted.

After this, the report ends with providing advice to Adam &Co. about the ways in which their

existing weaknesses in each of the department can be overcome.

2CASE STUDY – ADAM & CO.

Table of Contents

Introduction..................................................................................................................................3

System flowchart of purchases system........................................................................................4

System flowchart of cash disbursements system.........................................................................5

System flowchart of payroll system.............................................................................................6

Description of weaknesses and risks of the purchases system.....................................................7

Internal control weakness in the Cash Disbursements System....................................................8

Description of internal control weakness in the Payroll System.................................................9

Conclusion.................................................................................................................................10

List of References......................................................................................................................12

Table of Contents

Introduction..................................................................................................................................3

System flowchart of purchases system........................................................................................4

System flowchart of cash disbursements system.........................................................................5

System flowchart of payroll system.............................................................................................6

Description of weaknesses and risks of the purchases system.....................................................7

Internal control weakness in the Cash Disbursements System....................................................8

Description of internal control weakness in the Payroll System.................................................9

Conclusion.................................................................................................................................10

List of References......................................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3CASE STUDY – ADAM & CO.

Introduction

Adam & Co. is operating as a wholesale business in industrial supplies. It is based in

Perth. The inventories required for the production process are imported from manufacturers

operating in Thailand, Vietnam and China. The company has implemented a centralised

accounting system with various terminals in place at different points. The major accounting

systems that are prevalent in the organisation are called the Purchases system, Cash Distributions

system and the Payroll system. There is a well organised structure behind the implementation of

these systems within the organisation. At present, this system is considered to be very efficient

and duly meeting the requirements and necessities of the organisation. However, the

management acknowledges that the current system may be limited in certain aspects. These

systems are initially presented in the form of a flowchart to properly understand them and their

roles in the running of the business. After which, a robust study of these systems is conducted to

find whether there are any flaws in the particular systems and the methods that should be

implemented to overcome them.

Introduction

Adam & Co. is operating as a wholesale business in industrial supplies. It is based in

Perth. The inventories required for the production process are imported from manufacturers

operating in Thailand, Vietnam and China. The company has implemented a centralised

accounting system with various terminals in place at different points. The major accounting

systems that are prevalent in the organisation are called the Purchases system, Cash Distributions

system and the Payroll system. There is a well organised structure behind the implementation of

these systems within the organisation. At present, this system is considered to be very efficient

and duly meeting the requirements and necessities of the organisation. However, the

management acknowledges that the current system may be limited in certain aspects. These

systems are initially presented in the form of a flowchart to properly understand them and their

roles in the running of the business. After which, a robust study of these systems is conducted to

find whether there are any flaws in the particular systems and the methods that should be

implemented to overcome them.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4CASE STUDY – ADAM & CO.

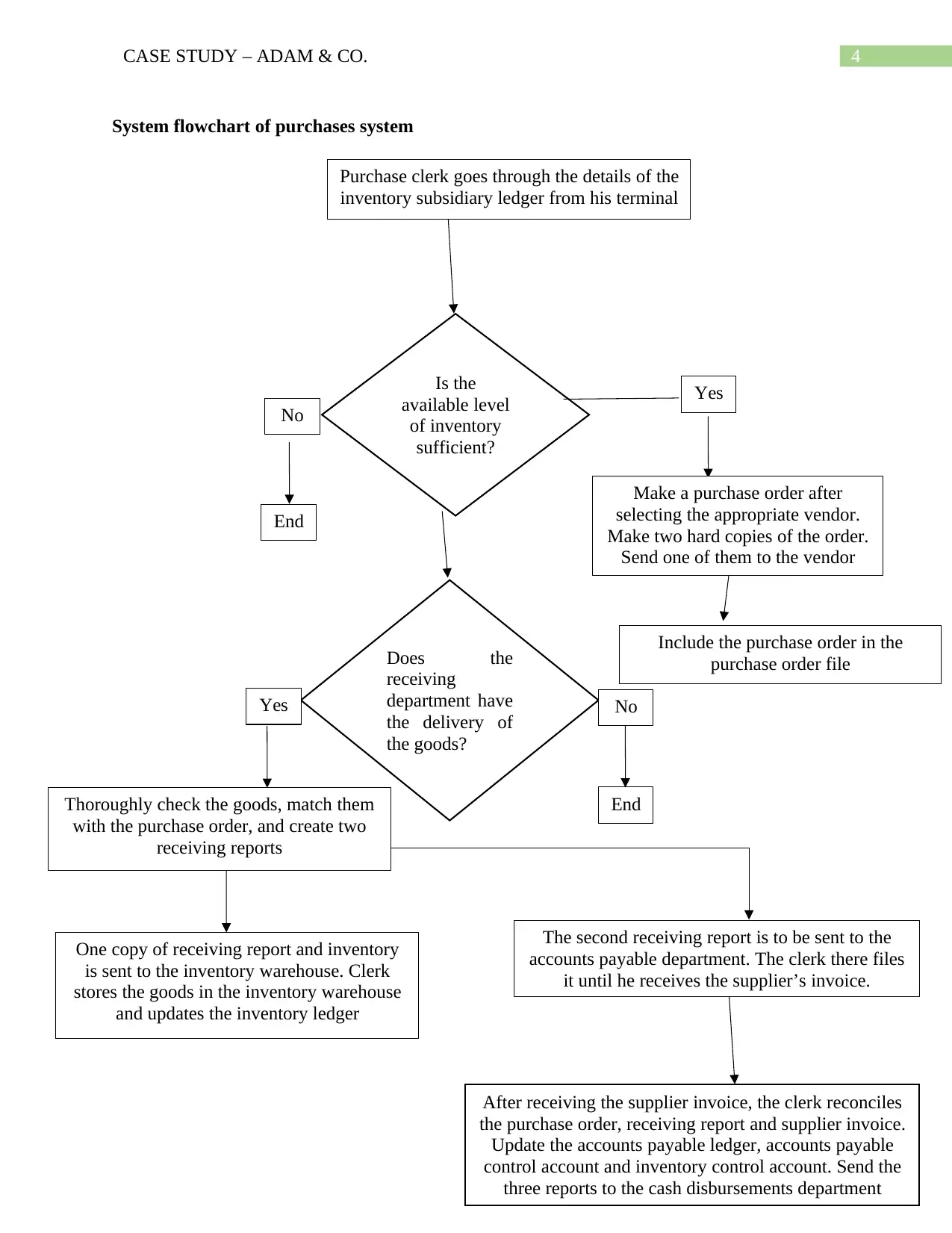

System flowchart of purchases system

Yes

No

Make a purchase order after

selecting the appropriate vendor.

Make two hard copies of the order.

Send one of them to the vendor

Purchase clerk goes through the details of the

inventory subsidiary ledger from his terminal

Is the

available level

of inventory

sufficient?

Include the purchase order in the

purchase order file

End

Does the

receiving

department have

the delivery of

the goods?

Yes

Thoroughly check the goods, match them

with the purchase order, and create two

receiving reports

One copy of receiving report and inventory

is sent to the inventory warehouse. Clerk

stores the goods in the inventory warehouse

and updates the inventory ledger

The second receiving report is to be sent to the

accounts payable department. The clerk there files

it until he receives the supplier’s invoice.

No

End

After receiving the supplier invoice, the clerk reconciles

the purchase order, receiving report and supplier invoice.

Update the accounts payable ledger, accounts payable

control account and inventory control account. Send the

three reports to the cash disbursements department

System flowchart of purchases system

Yes

No

Make a purchase order after

selecting the appropriate vendor.

Make two hard copies of the order.

Send one of them to the vendor

Purchase clerk goes through the details of the

inventory subsidiary ledger from his terminal

Is the

available level

of inventory

sufficient?

Include the purchase order in the

purchase order file

End

Does the

receiving

department have

the delivery of

the goods?

Yes

Thoroughly check the goods, match them

with the purchase order, and create two

receiving reports

One copy of receiving report and inventory

is sent to the inventory warehouse. Clerk

stores the goods in the inventory warehouse

and updates the inventory ledger

The second receiving report is to be sent to the

accounts payable department. The clerk there files

it until he receives the supplier’s invoice.

No

End

After receiving the supplier invoice, the clerk reconciles

the purchase order, receiving report and supplier invoice.

Update the accounts payable ledger, accounts payable

control account and inventory control account. Send the

three reports to the cash disbursements department

5CASE STUDY – ADAM & CO.

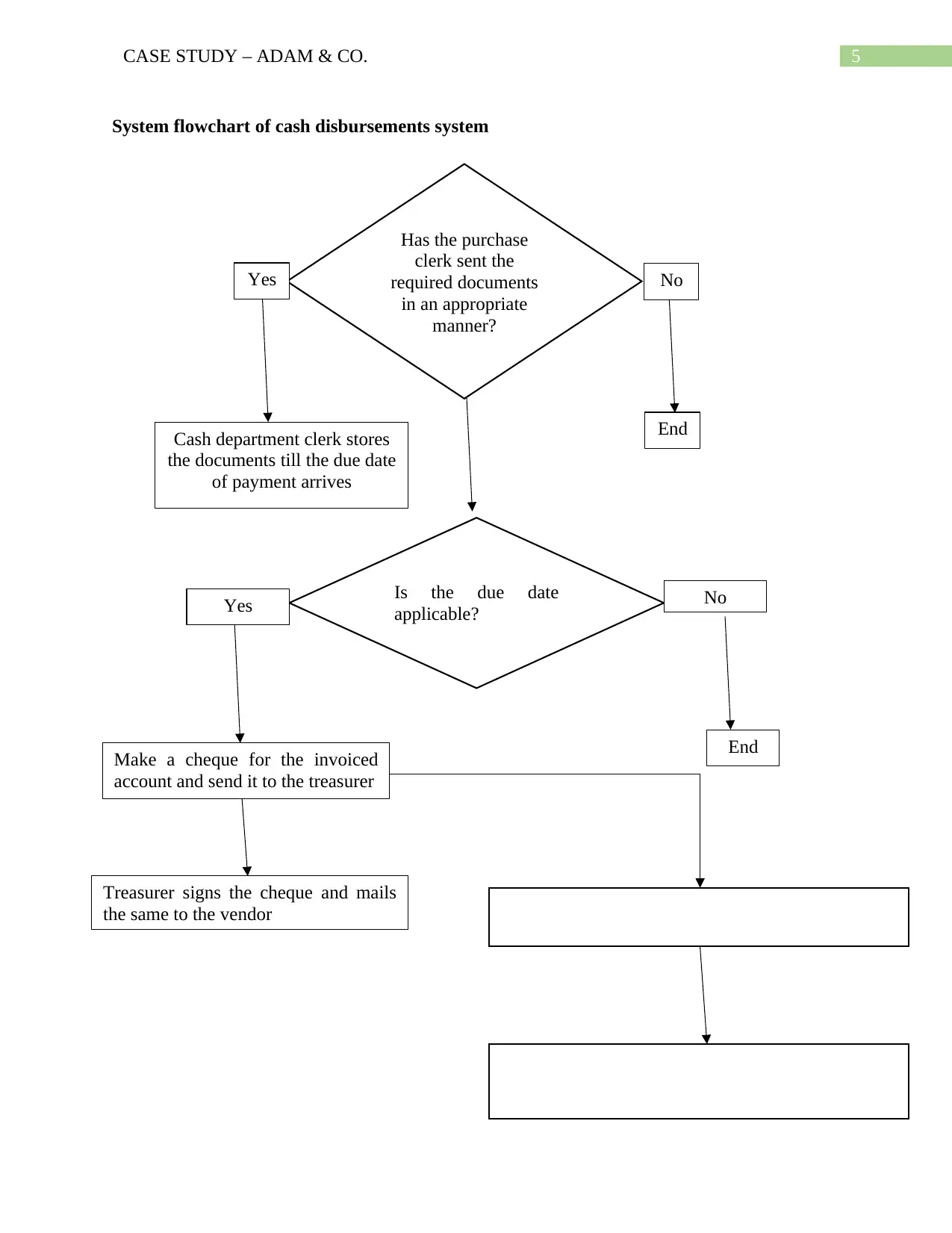

System flowchart of cash disbursements system

Has the purchase

clerk sent the

required documents

in an appropriate

manner?

Yes No

Cash department clerk stores

the documents till the due date

of payment arrives

End

Is the due date

applicable?Yes No

Make a cheque for the invoiced

account and send it to the treasurer

End

Treasurer signs the cheque and mails

the same to the vendor Update the cheque register, accounts payable ledger

and the accounts payable control account.

File the invoice, purchase order copy, receiving

report and cheque copy in the department

System flowchart of cash disbursements system

Has the purchase

clerk sent the

required documents

in an appropriate

manner?

Yes No

Cash department clerk stores

the documents till the due date

of payment arrives

End

Is the due date

applicable?Yes No

Make a cheque for the invoiced

account and send it to the treasurer

End

Treasurer signs the cheque and mails

the same to the vendor Update the cheque register, accounts payable ledger

and the accounts payable control account.

File the invoice, purchase order copy, receiving

report and cheque copy in the department

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6CASE STUDY – ADAM & CO.

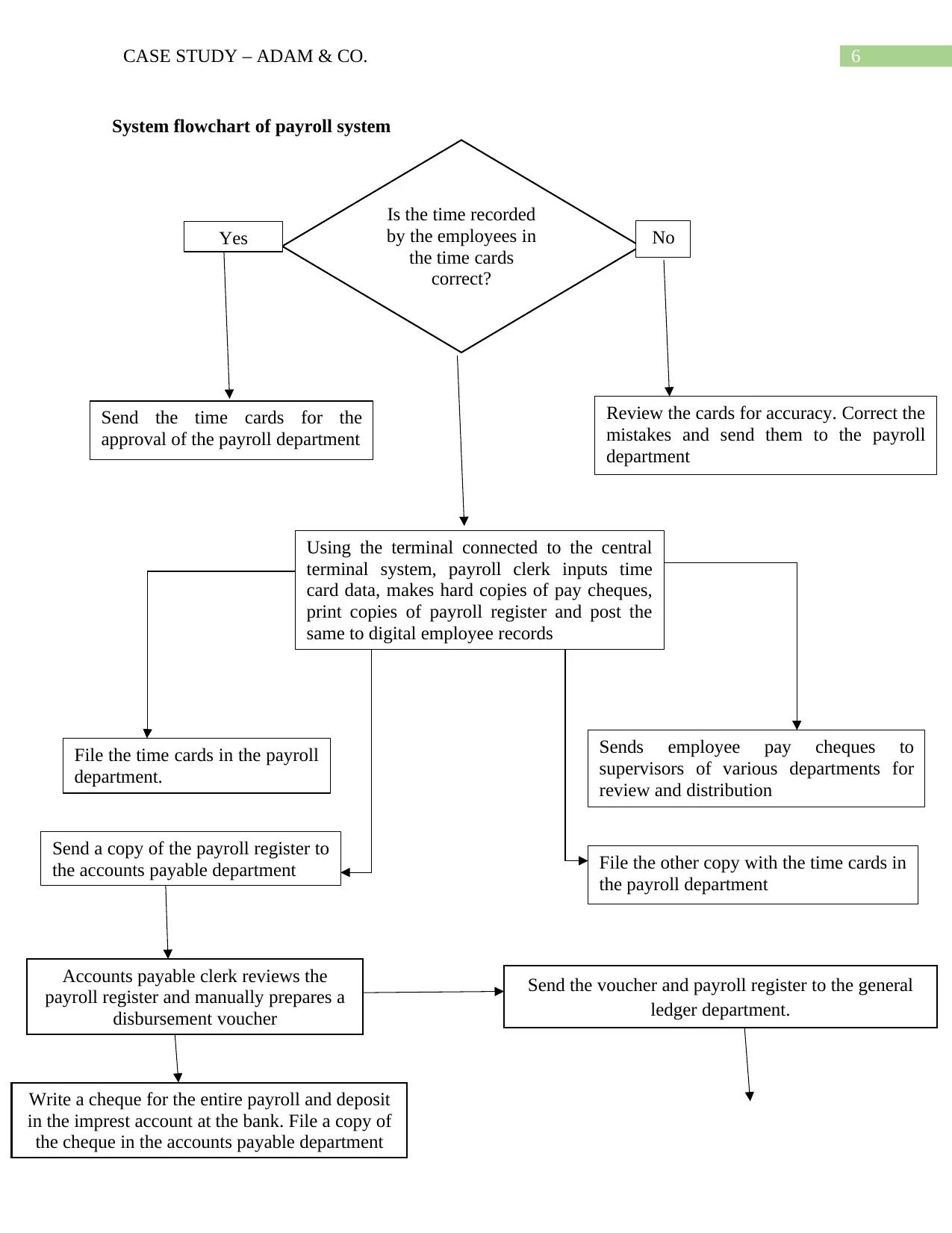

System flowchart of payroll system

Review the cards for accuracy. Correct the

mistakes and send them to the payroll

department

Send the time cards for the

approval of the payroll department

Is the time recorded

by the employees in

the time cards

correct?

Yes No

Using the terminal connected to the central

terminal system, payroll clerk inputs time

card data, makes hard copies of pay cheques,

print copies of payroll register and post the

same to digital employee records

Send a copy of the payroll register to

the accounts payable department

Sends employee pay cheques to

supervisors of various departments for

review and distribution

File the other copy with the time cards in

the payroll department

File the time cards in the payroll

department.

Accounts payable clerk reviews the

payroll register and manually prepares a

disbursement voucher

Send the voucher and payroll register to the general

ledger department.

Write a cheque for the entire payroll and deposit

in the imprest account at the bank. File a copy of

the cheque in the accounts payable department

System flowchart of payroll system

Review the cards for accuracy. Correct the

mistakes and send them to the payroll

department

Send the time cards for the

approval of the payroll department

Is the time recorded

by the employees in

the time cards

correct?

Yes No

Using the terminal connected to the central

terminal system, payroll clerk inputs time

card data, makes hard copies of pay cheques,

print copies of payroll register and post the

same to digital employee records

Send a copy of the payroll register to

the accounts payable department

Sends employee pay cheques to

supervisors of various departments for

review and distribution

File the other copy with the time cards in

the payroll department

File the time cards in the payroll

department.

Accounts payable clerk reviews the

payroll register and manually prepares a

disbursement voucher

Send the voucher and payroll register to the general

ledger department.

Write a cheque for the entire payroll and deposit

in the imprest account at the bank. File a copy of

the cheque in the accounts payable department

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7CASE STUDY – ADAM & CO.

Description of weaknesses and risks of the purchases system

Excess staffing is the main problem that can be observed in the purchases system. There

are way too many people who are charged with the responsibility of ensuring that the system

runs in a smooth manner. The responsibility of understanding and determining whether the stock

levels are too low is vested with one clerk. When this clerk thinks that the available stock levels

are too low, then he places an order for the goods from a particular vendor and receives the

goods from the particular vendor. After receiving the goods, he sends them to another clerk in

the department who undertakes the responsibility of safeguarding the goods and maintaining

them properly for future usage. Out of the two receiving reports prepared by the clerk in the

purchase department, one of them is sent to the clerk operating in the accounts payable

department. The other report has to be safeguarded by him until he receives the invoice from the

supplier. On receiving the invoice from the supplier, another temporary file has to be created and

the purchase order, receiving report and the supplier’s invoice are to be reconciled together.

There are not many aspects in this system to suggest that the system being implemented in the

organisation is not efficient. However, it is evident that the costs involved in the maintenance of

the department and its procedures are extremely expensive. With regards to the purchases

system, the biggest risk is the committing of frauds by suppliers. Other identifiable risks are

related to the delivery of goods from a foreign country and the problems that arise on receiving

low quality goods from those suppliers (Sandberg and Mena 2015). Risks also provide further

evidence about the presence of inefficiencies in the system implemented by Adam & Co. One of

them is the lack of a proper mechanism to quickly identify the quality of the goods received from

the suppliers. Receiving low quality products leads to a delay in the production of the goods and

Post to the general ledger from the computer

terminal and file them in the department

Description of weaknesses and risks of the purchases system

Excess staffing is the main problem that can be observed in the purchases system. There

are way too many people who are charged with the responsibility of ensuring that the system

runs in a smooth manner. The responsibility of understanding and determining whether the stock

levels are too low is vested with one clerk. When this clerk thinks that the available stock levels

are too low, then he places an order for the goods from a particular vendor and receives the

goods from the particular vendor. After receiving the goods, he sends them to another clerk in

the department who undertakes the responsibility of safeguarding the goods and maintaining

them properly for future usage. Out of the two receiving reports prepared by the clerk in the

purchase department, one of them is sent to the clerk operating in the accounts payable

department. The other report has to be safeguarded by him until he receives the invoice from the

supplier. On receiving the invoice from the supplier, another temporary file has to be created and

the purchase order, receiving report and the supplier’s invoice are to be reconciled together.

There are not many aspects in this system to suggest that the system being implemented in the

organisation is not efficient. However, it is evident that the costs involved in the maintenance of

the department and its procedures are extremely expensive. With regards to the purchases

system, the biggest risk is the committing of frauds by suppliers. Other identifiable risks are

related to the delivery of goods from a foreign country and the problems that arise on receiving

low quality goods from those suppliers (Sandberg and Mena 2015). Risks also provide further

evidence about the presence of inefficiencies in the system implemented by Adam & Co. One of

them is the lack of a proper mechanism to quickly identify the quality of the goods received from

the suppliers. Receiving low quality products leads to a delay in the production of the goods and

Post to the general ledger from the computer

terminal and file them in the department

8CASE STUDY – ADAM & CO.

causes a delay in conducting the business as a whole. Having a separate person each for ordering

the goods and receiving those causes information asymmetry in the organisation. There has to be

constant communication between both the clerks to understand that the goods ordered and

received are the same. Another identifiable risk in the department is the estimations of the ideal

quantity by the purchase clerks. It has been suggested that they place a new order when they

think that the quantity of inventories is too low. However, it has been found that these estimates

tend to be very conservative in most of the situations. The other area that can cause problems is

the allocation of the budget available (Dai and Gao 2014). Inappropriate allocation measures in

terms of budgets leads the organisation to suffer losses from the business. Another significant

weakness present in the purchases system is the authorisation of purchases. While the clerks in

every department perform their jobs according to a strict system, the lack of proper supervising

authority in the purchases department signifies the potential of frauds in the department.

Internal control weakness in the Cash Disbursements System

The lack of a credible supervising authority is the problem that is most likely to impact

the cash disbursements system and its functioning. The efficiency of this system is also heavily

dependent on the operating styles and efficiency of the people involved in the accounts payable

department. Any motive to commit a fraud on their part is likely to cause serious problems in the

cash disbursements system as a whole. The involvement of the purchasing clerk in this process

dilutes the powers of the cash system (Attom 2013). The accounts payable department should

always undertake the responsibility of maintaining the cheques related to a particular payment.

At present, there are too many copies of a cheque that are being distributed within the

organisation. There is a problem of misplacement of records and the risk of frauds associated

with this system. Matching the available records is also a time-taking process which consumes a

causes a delay in conducting the business as a whole. Having a separate person each for ordering

the goods and receiving those causes information asymmetry in the organisation. There has to be

constant communication between both the clerks to understand that the goods ordered and

received are the same. Another identifiable risk in the department is the estimations of the ideal

quantity by the purchase clerks. It has been suggested that they place a new order when they

think that the quantity of inventories is too low. However, it has been found that these estimates

tend to be very conservative in most of the situations. The other area that can cause problems is

the allocation of the budget available (Dai and Gao 2014). Inappropriate allocation measures in

terms of budgets leads the organisation to suffer losses from the business. Another significant

weakness present in the purchases system is the authorisation of purchases. While the clerks in

every department perform their jobs according to a strict system, the lack of proper supervising

authority in the purchases department signifies the potential of frauds in the department.

Internal control weakness in the Cash Disbursements System

The lack of a credible supervising authority is the problem that is most likely to impact

the cash disbursements system and its functioning. The efficiency of this system is also heavily

dependent on the operating styles and efficiency of the people involved in the accounts payable

department. Any motive to commit a fraud on their part is likely to cause serious problems in the

cash disbursements system as a whole. The involvement of the purchasing clerk in this process

dilutes the powers of the cash system (Attom 2013). The accounts payable department should

always undertake the responsibility of maintaining the cheques related to a particular payment.

At present, there are too many copies of a cheque that are being distributed within the

organisation. There is a problem of misplacement of records and the risk of frauds associated

with this system. Matching the available records is also a time-taking process which consumes a

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9CASE STUDY – ADAM & CO.

lot of efforts and time of the employees present in the system. There is also no restriction on the

funds available within the system and they are being spent as per the wishes of the clerks. Their

activities are not being controlled by the organisation. There should be an allocation of restricted

funds within the organisation and clear instructions should be passed on to the clerks about the

purposes and manner in which the funds should be spent. These practices are very common in

the operations of not-for-profit organisations (Herrera and Ibeas 2015). Another problem is the

presence of a single authority with signing powers within the entity. Although having a

minimum number of signing authorities is beneficial, the entity has no alternative option in

which the treasurer is unavailable to sign the cheque. A person that can step up in the absence of

the treasurer is essential for increasing the efficiency of the cash disbursements system. The

company also does not have any regulations against the advanced signing of cheques. This

practice can lead to the usage of the cheque for a different purpose than it was intended to.

Separation of cheques on the basis of the amount contained within them should also be

undertaken by the organisation to make sure that misappropriation of funds does not take place

within the payments authorised by the clerks and approved by the treasurer.

Description of internal control weakness in the Payroll System

The main problem that is pretty evident in the system implemented by the organisation is

the outdated practice of using time cards for the maintenance of records of the employees. The

inefficiency of these cards has been well documented and proven time and again by the

researchers (Oloyede, Adedoyin and Adewole 2013). The number of cards that are being

circulated within the system are also extremely huge in number and they need to be kept within

the organisation for future usage by any of the concerned parties. There is a good chance of these

cards getting misplaced in no time. The misplacement can lead to false claims being made by the

lot of efforts and time of the employees present in the system. There is also no restriction on the

funds available within the system and they are being spent as per the wishes of the clerks. Their

activities are not being controlled by the organisation. There should be an allocation of restricted

funds within the organisation and clear instructions should be passed on to the clerks about the

purposes and manner in which the funds should be spent. These practices are very common in

the operations of not-for-profit organisations (Herrera and Ibeas 2015). Another problem is the

presence of a single authority with signing powers within the entity. Although having a

minimum number of signing authorities is beneficial, the entity has no alternative option in

which the treasurer is unavailable to sign the cheque. A person that can step up in the absence of

the treasurer is essential for increasing the efficiency of the cash disbursements system. The

company also does not have any regulations against the advanced signing of cheques. This

practice can lead to the usage of the cheque for a different purpose than it was intended to.

Separation of cheques on the basis of the amount contained within them should also be

undertaken by the organisation to make sure that misappropriation of funds does not take place

within the payments authorised by the clerks and approved by the treasurer.

Description of internal control weakness in the Payroll System

The main problem that is pretty evident in the system implemented by the organisation is

the outdated practice of using time cards for the maintenance of records of the employees. The

inefficiency of these cards has been well documented and proven time and again by the

researchers (Oloyede, Adedoyin and Adewole 2013). The number of cards that are being

circulated within the system are also extremely huge in number and they need to be kept within

the organisation for future usage by any of the concerned parties. There is a good chance of these

cards getting misplaced in no time. The misplacement can lead to false claims being made by the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10CASE STUDY – ADAM & CO.

employees about the amounts they should receive from the company as a part of their salary or

incentives (Sullivan 2014). Unethical agreements between supervisors and the employees in a

particular department can lead to the overpayment of wages and improper records being accepted

by the supervisors. There is no audit of the authority being used by the supervisors. The payroll

system involves a lot of people from different departments and follows an extremely complex

pattern. Any misjudgement or error committed by any one of the parties is likely to effect the

entity altogether. The pressure on the accounts payable system is very high as it also has to

properly maintain and supervise the records of the purchasing system and the cash disbursements

system (Thite and Sandhu 2014). While the clerk writes a cheque for the entire payroll system as

a whole, any changes occurring within the payment details are unlikely to be changed at a quick

notice. There is also no authorisation of the cheques written by the payroll clerk. Other inherent

risks faced by the system are the loss, embezzlement or theft of documents which increases the

chances for misappropriation or loss of funds available for usage. The documents are also

processed by the single clerk. Any inaccuracy on his part is another risk faced by the system. The

number of accounts that need to be updated and the number of documents that are to be

reconciled together are very large in number and create a lot of pressure on the clerks responsible

for processing them. The time required to complete the processing of a week’s payroll is much

higher than the time taken by other organisations of similar functions.

Conclusion

To summarise the above findings and discussion, it can be suggested that the present

systems that the organisation in place are undoubtedly efficient. However, sustaining the same

level of efficiency over a period of time is dependent on a lot of variables whose accuracy

remains questionable. The main problem with the system implemented by Adam & Co. is its

employees about the amounts they should receive from the company as a part of their salary or

incentives (Sullivan 2014). Unethical agreements between supervisors and the employees in a

particular department can lead to the overpayment of wages and improper records being accepted

by the supervisors. There is no audit of the authority being used by the supervisors. The payroll

system involves a lot of people from different departments and follows an extremely complex

pattern. Any misjudgement or error committed by any one of the parties is likely to effect the

entity altogether. The pressure on the accounts payable system is very high as it also has to

properly maintain and supervise the records of the purchasing system and the cash disbursements

system (Thite and Sandhu 2014). While the clerk writes a cheque for the entire payroll system as

a whole, any changes occurring within the payment details are unlikely to be changed at a quick

notice. There is also no authorisation of the cheques written by the payroll clerk. Other inherent

risks faced by the system are the loss, embezzlement or theft of documents which increases the

chances for misappropriation or loss of funds available for usage. The documents are also

processed by the single clerk. Any inaccuracy on his part is another risk faced by the system. The

number of accounts that need to be updated and the number of documents that are to be

reconciled together are very large in number and create a lot of pressure on the clerks responsible

for processing them. The time required to complete the processing of a week’s payroll is much

higher than the time taken by other organisations of similar functions.

Conclusion

To summarise the above findings and discussion, it can be suggested that the present

systems that the organisation in place are undoubtedly efficient. However, sustaining the same

level of efficiency over a period of time is dependent on a lot of variables whose accuracy

remains questionable. The main problem with the system implemented by Adam & Co. is its

11CASE STUDY – ADAM & CO.

dependence on a selected few persons and lack of proper supervision in the individual

departments. This absence can cause false claims, embezzlement and manipulation of documents

while also causing the entity to suffer losses. There is a need for the company to employ more

people within the organisation to ensure that the processes remain efficient. However, adopting a

business intelligence system in their assistance is also a useful measure that can be followed.

dependence on a selected few persons and lack of proper supervision in the individual

departments. This absence can cause false claims, embezzlement and manipulation of documents

while also causing the entity to suffer losses. There is a need for the company to employ more

people within the organisation to ensure that the processes remain efficient. However, adopting a

business intelligence system in their assistance is also a useful measure that can be followed.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.