Accounting Management Report: Systems, Reports, and Costing Analysis

VerifiedAdded on 2020/07/23

|15

|4203

|34

Report

AI Summary

This report provides a comprehensive overview of accounting management, encompassing various systems, reports, and costing methods. It begins with an introduction to management accounting and its significance in organizational decision-making, exploring different accounting systems such as inventory management, job costing, and cost accounting. The report then delves into the preparation and importance of various accounting reports, including target costing, sales reports, due account reports, and budget reports. Furthermore, it examines the concepts of marginal and absorption costing, comparing their methodologies and providing examples to illustrate their applications in financial analysis. The report also addresses budgetary control tools and the solving of financial problems, offering insights into effective financial management. Overall, the report serves as a valuable resource for understanding key accounting principles and their practical applications.

ACCOUNTING

MANAGEMENT

MANAGEMENT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Management accounting and its systems...............................................................................1

P2 Accounting reports.................................................................................................................3

TASK 2............................................................................................................................................4

P3 Marginal and absorption costing............................................................................................4

TASK 3............................................................................................................................................7

P4 Budgetary control tools..........................................................................................................7

P5 Solving of financial problems................................................................................................9

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Management accounting and its systems...............................................................................1

P2 Accounting reports.................................................................................................................3

TASK 2............................................................................................................................................4

P3 Marginal and absorption costing............................................................................................4

TASK 3............................................................................................................................................7

P4 Budgetary control tools..........................................................................................................7

P5 Solving of financial problems................................................................................................9

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION

Management accounting is a process through which decision taking process of an

enterprise become easy as quality information is provided by this section. It is a continuous

process in which various reports are prepared by the different departments which include all the

quality data which can help the user in getting the complete idea about that part so that

accordingly future judgement can be taken (Zimmerman and Yahya, 2011). Documents are

prepared on weekly or monthly basis which are of great help to the internal users for ensuring

effective control at work place. Hence a timely and statistical data is received which act as a base

for the department head to take corrective decisions. Following report will discuss different

accounting systems along with the variety of reports prepared under the same. This will help user

in understanding the whole concept of accountancy along with other related concepts.

TASK 1

P1 Management accounting and its systems

This is an important function of every organisation as it helps in the balanced functioning

of different departments which are part of an entity. With this concept the process of decision

making becomes easy as with the information provided by different systems degree of right

option selection increases and therefore goal of an organisation can be achieved effectively. It is

a different tool than that of financial system as in that only the statistical data is given which only

is not of greater use (Macintosh and Quattrone, 2010). Importance of management accounting

can be better understood under the different heads in the following manner:

1. Helps in forecasting the future – It is crucial for management to take the different

investment decision by the company for which decision regarding weather the investment

should be continue needs to be taken. During this course of action evaluation of available

opinion is done that weather it is effective or not? Should it be diversified into various

areas? Management accounting system gives answerer to these questions and forecast the

coming trend so that accordingly the best option is selected.

2. Assist in production or buying decision – when any company operates in the industry it

has both the choice weather to go for manufacturing or to opt for outsourcing. The

concern system will help in evaluating the positives and negatives of each variety which

will further aid in selecting the best alternative.

1

Management accounting is a process through which decision taking process of an

enterprise become easy as quality information is provided by this section. It is a continuous

process in which various reports are prepared by the different departments which include all the

quality data which can help the user in getting the complete idea about that part so that

accordingly future judgement can be taken (Zimmerman and Yahya, 2011). Documents are

prepared on weekly or monthly basis which are of great help to the internal users for ensuring

effective control at work place. Hence a timely and statistical data is received which act as a base

for the department head to take corrective decisions. Following report will discuss different

accounting systems along with the variety of reports prepared under the same. This will help user

in understanding the whole concept of accountancy along with other related concepts.

TASK 1

P1 Management accounting and its systems

This is an important function of every organisation as it helps in the balanced functioning

of different departments which are part of an entity. With this concept the process of decision

making becomes easy as with the information provided by different systems degree of right

option selection increases and therefore goal of an organisation can be achieved effectively. It is

a different tool than that of financial system as in that only the statistical data is given which only

is not of greater use (Macintosh and Quattrone, 2010). Importance of management accounting

can be better understood under the different heads in the following manner:

1. Helps in forecasting the future – It is crucial for management to take the different

investment decision by the company for which decision regarding weather the investment

should be continue needs to be taken. During this course of action evaluation of available

opinion is done that weather it is effective or not? Should it be diversified into various

areas? Management accounting system gives answerer to these questions and forecast the

coming trend so that accordingly the best option is selected.

2. Assist in production or buying decision – when any company operates in the industry it

has both the choice weather to go for manufacturing or to opt for outsourcing. The

concern system will help in evaluating the positives and negatives of each variety which

will further aid in selecting the best alternative.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

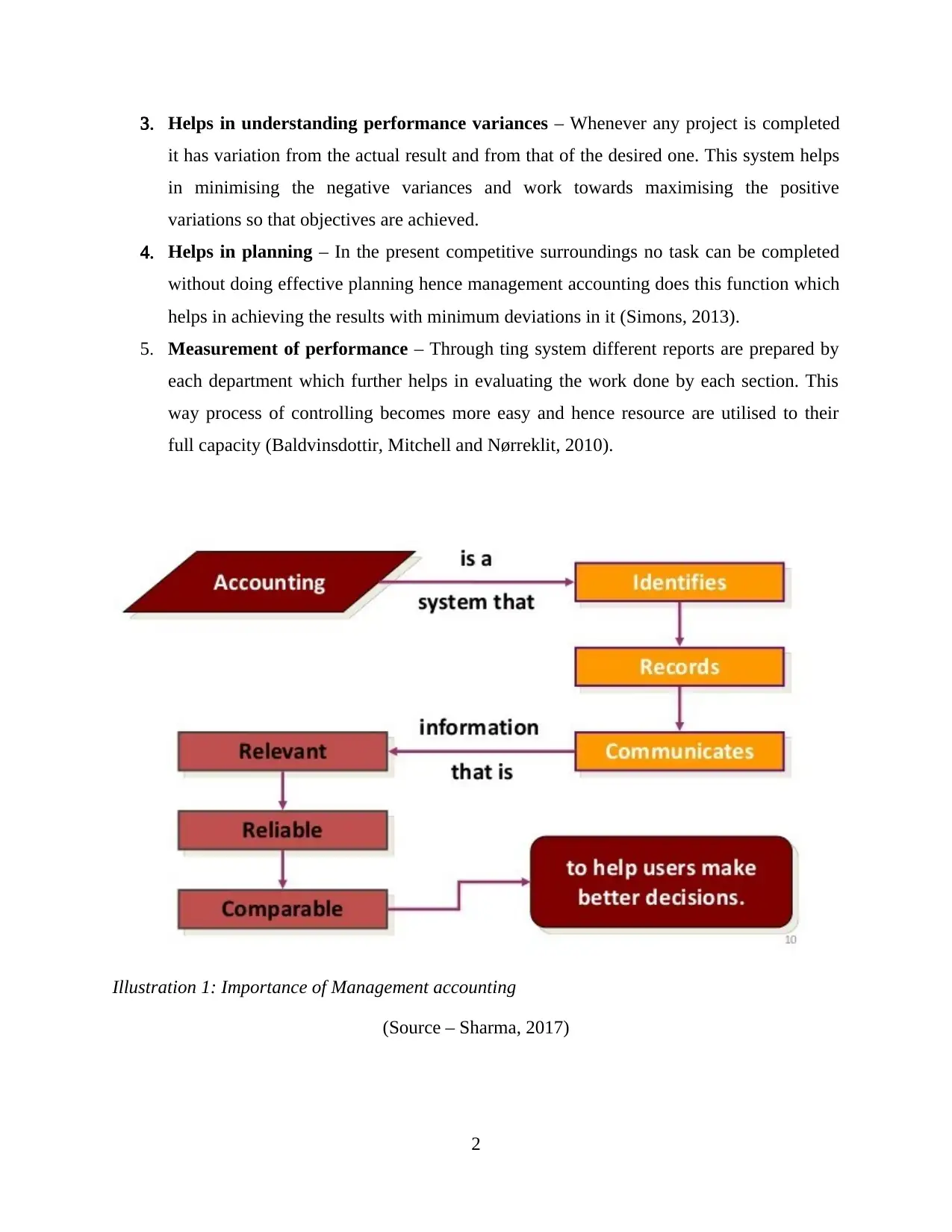

3. Helps in understanding performance variances – Whenever any project is completed

it has variation from the actual result and from that of the desired one. This system helps

in minimising the negative variances and work towards maximising the positive

variations so that objectives are achieved.

4. Helps in planning – In the present competitive surroundings no task can be completed

without doing effective planning hence management accounting does this function which

helps in achieving the results with minimum deviations in it (Simons, 2013).

5. Measurement of performance – Through ting system different reports are prepared by

each department which further helps in evaluating the work done by each section. This

way process of controlling becomes more easy and hence resource are utilised to their

full capacity (Baldvinsdottir, Mitchell and Nørreklit, 2010).

(Source – Sharma, 2017)

2

Illustration 1: Importance of Management accounting

it has variation from the actual result and from that of the desired one. This system helps

in minimising the negative variances and work towards maximising the positive

variations so that objectives are achieved.

4. Helps in planning – In the present competitive surroundings no task can be completed

without doing effective planning hence management accounting does this function which

helps in achieving the results with minimum deviations in it (Simons, 2013).

5. Measurement of performance – Through ting system different reports are prepared by

each department which further helps in evaluating the work done by each section. This

way process of controlling becomes more easy and hence resource are utilised to their

full capacity (Baldvinsdottir, Mitchell and Nørreklit, 2010).

(Source – Sharma, 2017)

2

Illustration 1: Importance of Management accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Different systems which are performed under the management accounting system has their own

significance and are utilised at various levels of the firm. Some of those scheme are discussed

below in detail:

Inventory management system – In order to reach at the final output stock is required

which is used as an input throughout the production process. For this it is important that

the required level of inventory is made available so that the manufacturing process does

not get effected. This system of management accounting provide useful information

regarding the present level of available stock so that decision regarding further purchase

can be taken properly(Ward, 2012).

Job costing system – While carrying out business different activities are perform by

distinct departments. For this departmentalization is done according to nature of job done

by each. Mentioned system of accounting helps in measuring the level of efficiency of

each job so that the required improvements can be done and overall results are achieved.

Apart from this through this method it can also be evaluated that which job is important

and which can be discontinued if that is not of much importance (Lukka and Modell,

2010).

Cost accounting system – Customer is very much price sensitive hence it is necessary

that the total cost is controlled so that overall organisation expenditure can be controlled.

Through this system of accounting monitoring over the cost is kept to maintain a balance.

P2 Accounting reports

In order to maintain effective control over the organisation performance different reports

are prepared which gives the details of projects status and results of each departments. This way

proper monitoring can be done and also the required corrective actions can be taken in the

sections which are found to be less efficient. Apart from this with the help of reporting system

comparison process also become easy as the results of particular year or any time frame can be

compare with the previous frame and accordingly standards can be set. Some of the important

reports are explained below which are formed in the organisation:

Target costing report – According to this document the required amount of resource are

determined which will be required to accomplish the given project. This way it become

easy to keep control over the usage of different resources and it is assured that budget do

not cross the set limits.

3

significance and are utilised at various levels of the firm. Some of those scheme are discussed

below in detail:

Inventory management system – In order to reach at the final output stock is required

which is used as an input throughout the production process. For this it is important that

the required level of inventory is made available so that the manufacturing process does

not get effected. This system of management accounting provide useful information

regarding the present level of available stock so that decision regarding further purchase

can be taken properly(Ward, 2012).

Job costing system – While carrying out business different activities are perform by

distinct departments. For this departmentalization is done according to nature of job done

by each. Mentioned system of accounting helps in measuring the level of efficiency of

each job so that the required improvements can be done and overall results are achieved.

Apart from this through this method it can also be evaluated that which job is important

and which can be discontinued if that is not of much importance (Lukka and Modell,

2010).

Cost accounting system – Customer is very much price sensitive hence it is necessary

that the total cost is controlled so that overall organisation expenditure can be controlled.

Through this system of accounting monitoring over the cost is kept to maintain a balance.

P2 Accounting reports

In order to maintain effective control over the organisation performance different reports

are prepared which gives the details of projects status and results of each departments. This way

proper monitoring can be done and also the required corrective actions can be taken in the

sections which are found to be less efficient. Apart from this with the help of reporting system

comparison process also become easy as the results of particular year or any time frame can be

compare with the previous frame and accordingly standards can be set. Some of the important

reports are explained below which are formed in the organisation:

Target costing report – According to this document the required amount of resource are

determined which will be required to accomplish the given project. This way it become

easy to keep control over the usage of different resources and it is assured that budget do

not cross the set limits.

3

Sales report – It is another variety of reporting system in which sales is the subject

matter. This document gives the knowledge regarding present and past sales records so

that a proper track record is maintained which cane further utilised to set limits for future

targets. The efficiency of the sales department can also be judged through the information

provided by it and hence deviations in the actual and set standards can be determined.

This will help in improving the overall performance of the company (Bodie, 2013).

Due account report – This is another variety of records which are related to the amount

against which services are given but amount is not received. It is necessary that the

management keeps proper record of all those from whom the amount is due so that at the

time of doing collection no difficulty is faced and also this way no party is missed from

with whom the bill is due. Apart from this knowledge regarding the time span for which a

party hold the unpaid amount can also be recorded (Otley and Emmanuel, 2013).

Budget report – It is another file which is related to setting limits for distinct

department. This helps in controlling the cash inflow and outflow as in order to achieve

success the most important tool is that the funds of an enterprise are used to their

maximum limit. Budget helps in providing standards to the different departments so that

they learn to finish the project with the provided resources which further helps in

achieving competitive advantage (Garrison and et. al., 2010).

M1

With the help of management accounting management will be able to do a better

business. Systems discussed will be of great help to achieve organisation goals and objectives.

D1

The reports which are discussed will help organisation in keeping effective control and

will provide the required information relevant in decision making and doing the comparison of

each department.

TASK 2

P3 Marginal and absorption costing

In order to get the final output a product has to go through various stages. At every a cost

is incurred which is a combination of both fixed and variable. In order to calculate the cost of

4

matter. This document gives the knowledge regarding present and past sales records so

that a proper track record is maintained which cane further utilised to set limits for future

targets. The efficiency of the sales department can also be judged through the information

provided by it and hence deviations in the actual and set standards can be determined.

This will help in improving the overall performance of the company (Bodie, 2013).

Due account report – This is another variety of records which are related to the amount

against which services are given but amount is not received. It is necessary that the

management keeps proper record of all those from whom the amount is due so that at the

time of doing collection no difficulty is faced and also this way no party is missed from

with whom the bill is due. Apart from this knowledge regarding the time span for which a

party hold the unpaid amount can also be recorded (Otley and Emmanuel, 2013).

Budget report – It is another file which is related to setting limits for distinct

department. This helps in controlling the cash inflow and outflow as in order to achieve

success the most important tool is that the funds of an enterprise are used to their

maximum limit. Budget helps in providing standards to the different departments so that

they learn to finish the project with the provided resources which further helps in

achieving competitive advantage (Garrison and et. al., 2010).

M1

With the help of management accounting management will be able to do a better

business. Systems discussed will be of great help to achieve organisation goals and objectives.

D1

The reports which are discussed will help organisation in keeping effective control and

will provide the required information relevant in decision making and doing the comparison of

each department.

TASK 2

P3 Marginal and absorption costing

In order to get the final output a product has to go through various stages. At every a cost

is incurred which is a combination of both fixed and variable. In order to calculate the cost of

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

product different methods are used which further presents the final reports to the management.

Among the different tools absorption and marginal costing is the most effective one.

Marginal costing – It is a tool that that helps in controlling or conducting the decision

taking process effectively. Under this process the change in cost take place due to one unit

addition in the total quantity of production. Fixed cost is that that remain same at every level of

production and variable value consists of those which fluctuates with the units of output. In

marginal costing the total value is sub divided into fixed and variable. While calculating the cost

of products only variable costs are included and valuation of inventory is done. Cost per unit

under this system remains constant as only variable cost are considered for calculation (Cinquini

and Tenucci, 2010).

Absorption costing – Working of this method is different from that of the one discussed

before. Under this system both the costs are considered while calculating the cost of inventory.

through this method the net profit is determined after deducting the firm cost with the variable

cost too (Luft and Shields, 2010).

Comparison between Marginal and absorption costing

Basis Marginal Absorption

Meaning A tool that assist in taking

decisions

Helps in doing apportionment

of total cost

Cost Recognition Variable is taken as the value

of product and fixed is taken

as the cost of period.

Variable and fixed both the

cost are taken in care while

calculating product cost

Highlights Share per component Final Profits pter component

An example of each method is given below which will show how calculaion of income is

different in both the cases.

Statement of financial gain and failure using absorption cost accounting

Quarter 1

No. Of units £/unit £ £

Sales value 66.000 1 66.000

less Value of sales

5

Among the different tools absorption and marginal costing is the most effective one.

Marginal costing – It is a tool that that helps in controlling or conducting the decision

taking process effectively. Under this process the change in cost take place due to one unit

addition in the total quantity of production. Fixed cost is that that remain same at every level of

production and variable value consists of those which fluctuates with the units of output. In

marginal costing the total value is sub divided into fixed and variable. While calculating the cost

of products only variable costs are included and valuation of inventory is done. Cost per unit

under this system remains constant as only variable cost are considered for calculation (Cinquini

and Tenucci, 2010).

Absorption costing – Working of this method is different from that of the one discussed

before. Under this system both the costs are considered while calculating the cost of inventory.

through this method the net profit is determined after deducting the firm cost with the variable

cost too (Luft and Shields, 2010).

Comparison between Marginal and absorption costing

Basis Marginal Absorption

Meaning A tool that assist in taking

decisions

Helps in doing apportionment

of total cost

Cost Recognition Variable is taken as the value

of product and fixed is taken

as the cost of period.

Variable and fixed both the

cost are taken in care while

calculating product cost

Highlights Share per component Final Profits pter component

An example of each method is given below which will show how calculaion of income is

different in both the cases.

Statement of financial gain and failure using absorption cost accounting

Quarter 1

No. Of units £/unit £ £

Sales value 66.000 1 66.000

less Value of sales

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

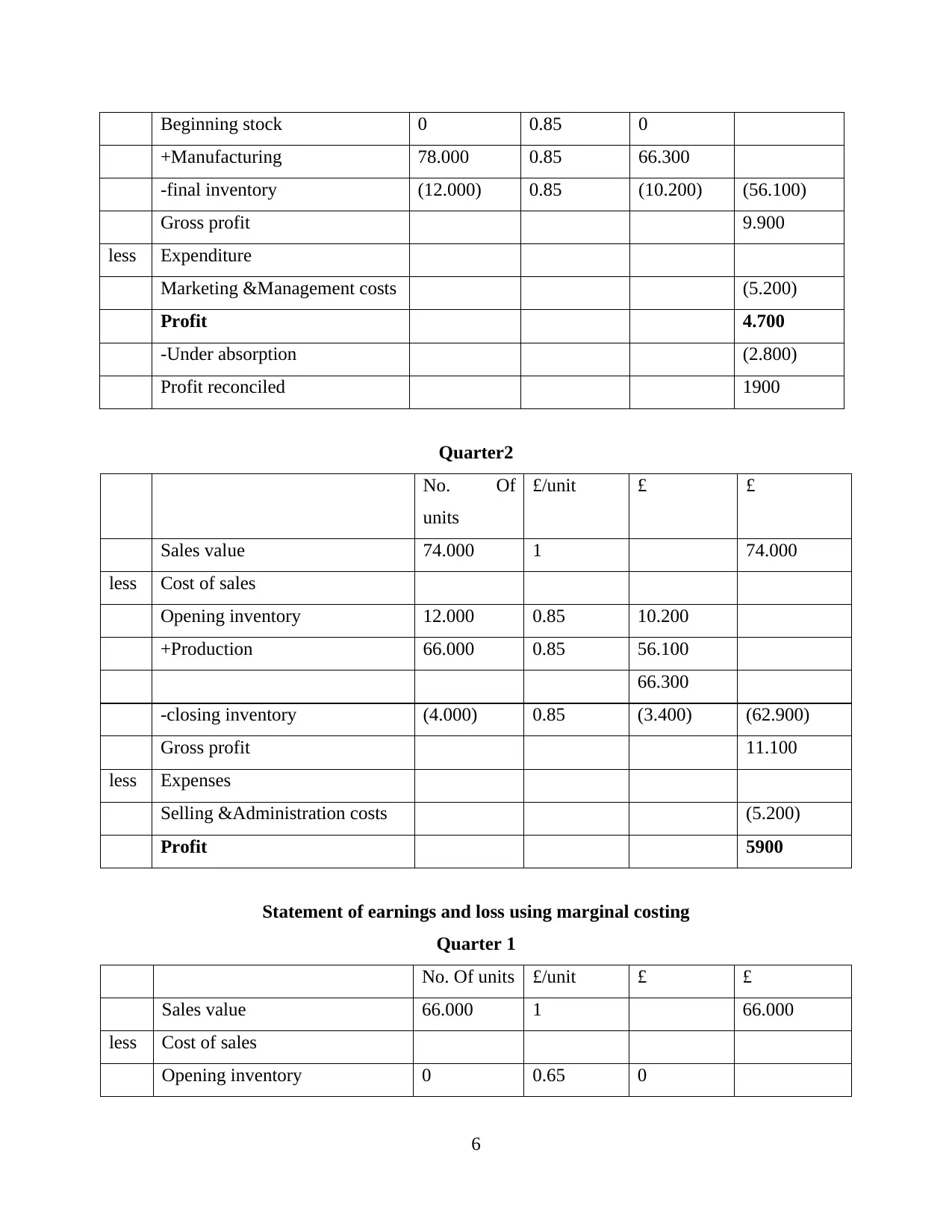

Beginning stock 0 0.85 0

+Manufacturing 78.000 0.85 66.300

-final inventory (12.000) 0.85 (10.200) (56.100)

Gross profit 9.900

less Expenditure

Marketing &Management costs (5.200)

Profit 4.700

-Under absorption (2.800)

Profit reconciled 1900

Quarter2

No. Of

units

£/unit £ £

Sales value 74.000 1 74.000

less Cost of sales

Opening inventory 12.000 0.85 10.200

+Production 66.000 0.85 56.100

66.300

-closing inventory (4.000) 0.85 (3.400) (62.900)

Gross profit 11.100

less Expenses

Selling &Administration costs (5.200)

Profit 5900

Statement of earnings and loss using marginal costing

Quarter 1

No. Of units £/unit £ £

Sales value 66.000 1 66.000

less Cost of sales

Opening inventory 0 0.65 0

6

+Manufacturing 78.000 0.85 66.300

-final inventory (12.000) 0.85 (10.200) (56.100)

Gross profit 9.900

less Expenditure

Marketing &Management costs (5.200)

Profit 4.700

-Under absorption (2.800)

Profit reconciled 1900

Quarter2

No. Of

units

£/unit £ £

Sales value 74.000 1 74.000

less Cost of sales

Opening inventory 12.000 0.85 10.200

+Production 66.000 0.85 56.100

66.300

-closing inventory (4.000) 0.85 (3.400) (62.900)

Gross profit 11.100

less Expenses

Selling &Administration costs (5.200)

Profit 5900

Statement of earnings and loss using marginal costing

Quarter 1

No. Of units £/unit £ £

Sales value 66.000 1 66.000

less Cost of sales

Opening inventory 0 0.65 0

6

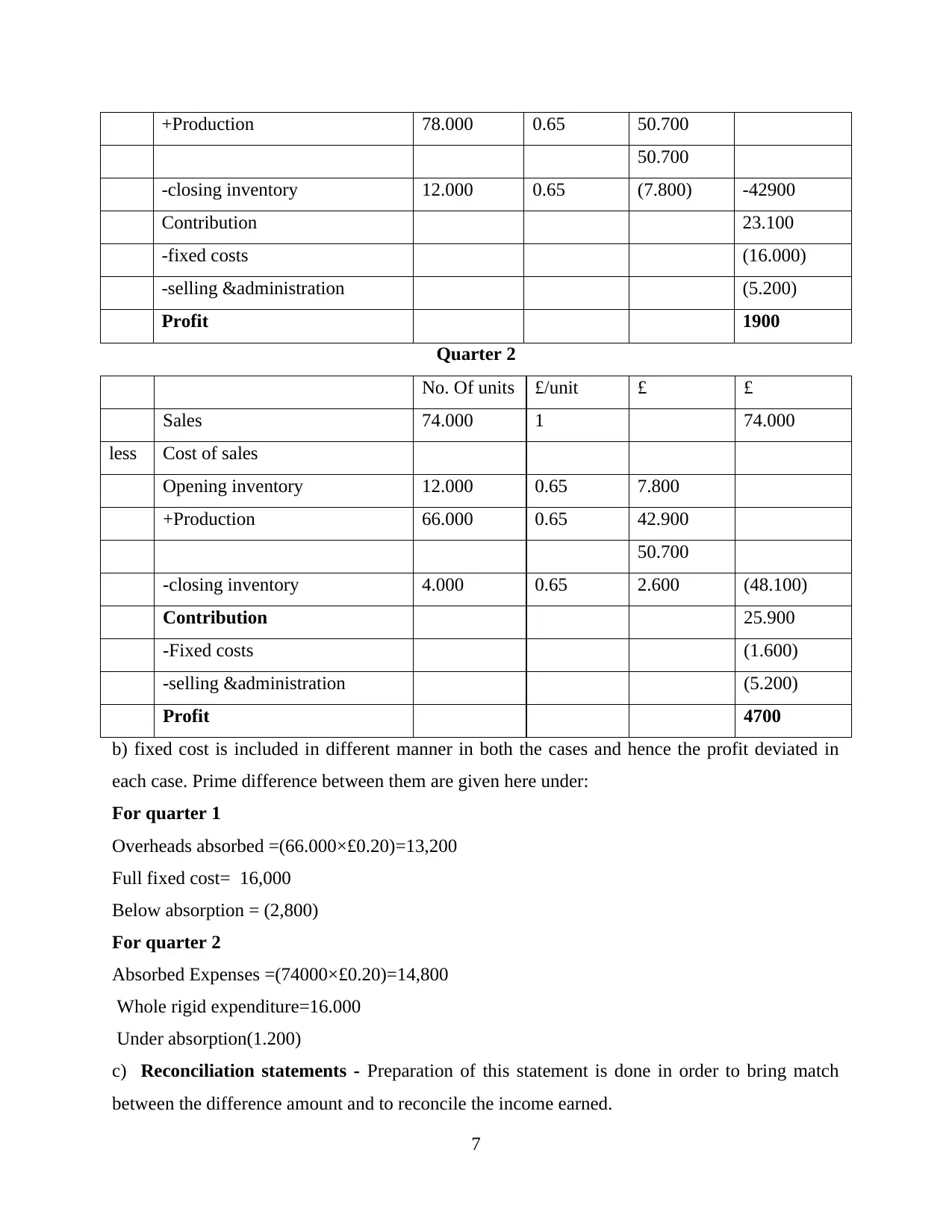

+Production 78.000 0.65 50.700

50.700

-closing inventory 12.000 0.65 (7.800) -42900

Contribution 23.100

-fixed costs (16.000)

-selling &administration (5.200)

Profit 1900

Quarter 2

No. Of units £/unit £ £

Sales 74.000 1 74.000

less Cost of sales

Opening inventory 12.000 0.65 7.800

+Production 66.000 0.65 42.900

50.700

-closing inventory 4.000 0.65 2.600 (48.100)

Contribution 25.900

-Fixed costs (1.600)

-selling &administration (5.200)

Profit 4700

b) fixed cost is included in different manner in both the cases and hence the profit deviated in

each case. Prime difference between them are given here under:

For quarter 1

Overheads absorbed =(66.000×£0.20)=13,200

Full fixed cost= 16,000

Below absorption = (2,800)

For quarter 2

Absorbed Expenses =(74000×£0.20)=14,800

Whole rigid expenditure=16.000

Under absorption(1.200)

c) Reconciliation statements - Preparation of this statement is done in order to bring match

between the difference amount and to reconcile the income earned.

7

50.700

-closing inventory 12.000 0.65 (7.800) -42900

Contribution 23.100

-fixed costs (16.000)

-selling &administration (5.200)

Profit 1900

Quarter 2

No. Of units £/unit £ £

Sales 74.000 1 74.000

less Cost of sales

Opening inventory 12.000 0.65 7.800

+Production 66.000 0.65 42.900

50.700

-closing inventory 4.000 0.65 2.600 (48.100)

Contribution 25.900

-Fixed costs (1.600)

-selling &administration (5.200)

Profit 4700

b) fixed cost is included in different manner in both the cases and hence the profit deviated in

each case. Prime difference between them are given here under:

For quarter 1

Overheads absorbed =(66.000×£0.20)=13,200

Full fixed cost= 16,000

Below absorption = (2,800)

For quarter 2

Absorbed Expenses =(74000×£0.20)=14,800

Whole rigid expenditure=16.000

Under absorption(1.200)

c) Reconciliation statements - Preparation of this statement is done in order to bring match

between the difference amount and to reconcile the income earned.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

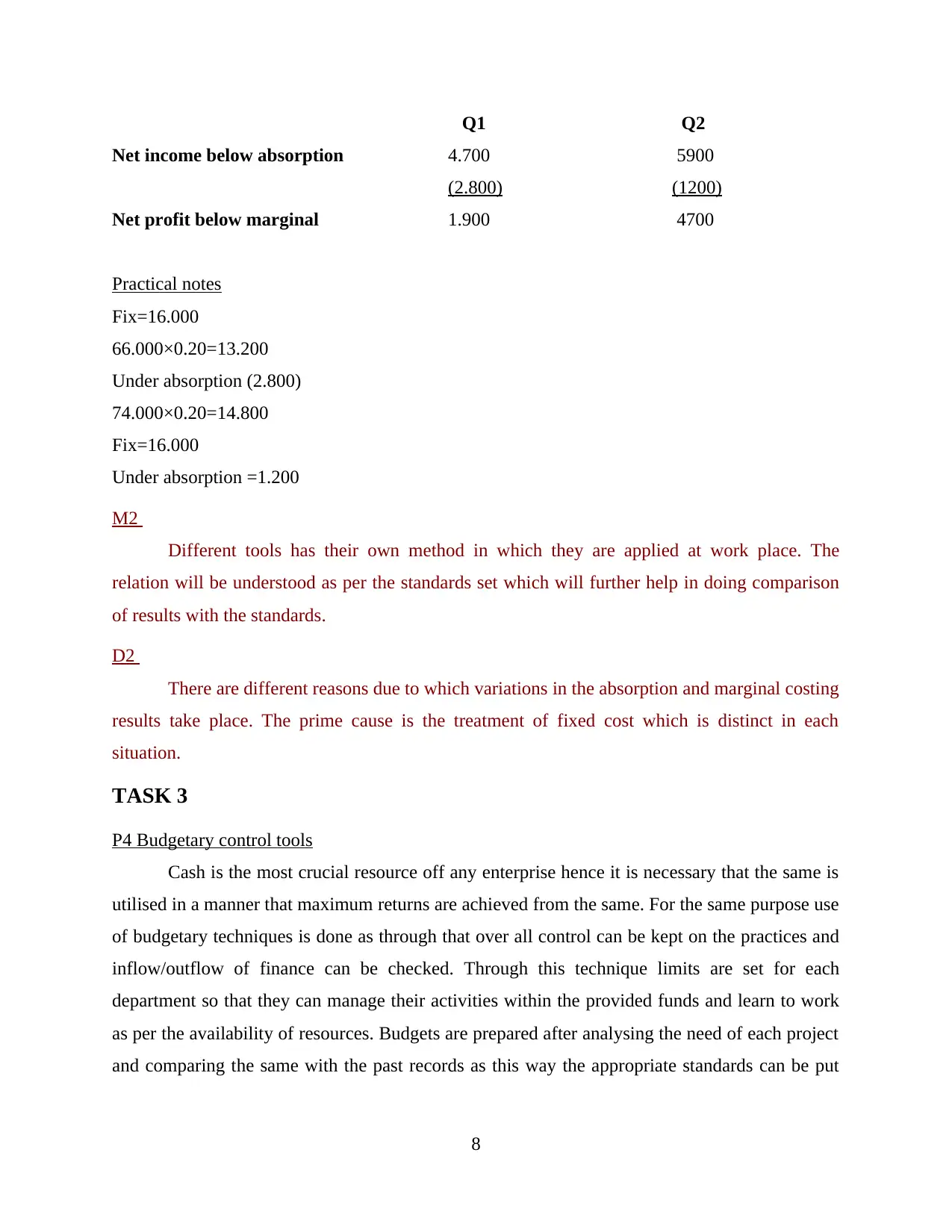

Q1 Q2

Net income below absorption 4.700 5900

(2.800) (1200)

Net profit below marginal 1.900 4700

Practical notes

Fix=16.000

66.000×0.20=13.200

Under absorption (2.800)

74.000×0.20=14.800

Fix=16.000

Under absorption =1.200

M2

Different tools has their own method in which they are applied at work place. The

relation will be understood as per the standards set which will further help in doing comparison

of results with the standards.

D2

There are different reasons due to which variations in the absorption and marginal costing

results take place. The prime cause is the treatment of fixed cost which is distinct in each

situation.

TASK 3

P4 Budgetary control tools

Cash is the most crucial resource off any enterprise hence it is necessary that the same is

utilised in a manner that maximum returns are achieved from the same. For the same purpose use

of budgetary techniques is done as through that over all control can be kept on the practices and

inflow/outflow of finance can be checked. Through this technique limits are set for each

department so that they can manage their activities within the provided funds and learn to work

as per the availability of resources. Budgets are prepared after analysing the need of each project

and comparing the same with the past records as this way the appropriate standards can be put

8

Net income below absorption 4.700 5900

(2.800) (1200)

Net profit below marginal 1.900 4700

Practical notes

Fix=16.000

66.000×0.20=13.200

Under absorption (2.800)

74.000×0.20=14.800

Fix=16.000

Under absorption =1.200

M2

Different tools has their own method in which they are applied at work place. The

relation will be understood as per the standards set which will further help in doing comparison

of results with the standards.

D2

There are different reasons due to which variations in the absorption and marginal costing

results take place. The prime cause is the treatment of fixed cost which is distinct in each

situation.

TASK 3

P4 Budgetary control tools

Cash is the most crucial resource off any enterprise hence it is necessary that the same is

utilised in a manner that maximum returns are achieved from the same. For the same purpose use

of budgetary techniques is done as through that over all control can be kept on the practices and

inflow/outflow of finance can be checked. Through this technique limits are set for each

department so that they can manage their activities within the provided funds and learn to work

as per the availability of resources. Budgets are prepared after analysing the need of each project

and comparing the same with the past records as this way the appropriate standards can be put

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

forward against the concern department (Scapens and Bromwich, , 2010). As per the nature,

department and scale of project distinct budgets are prepared among which the most popular are:

Master budget

Cash budget

Sales budget

Zero budget

Operating financial plan

Statics estimates

Cash flow forecast report

Each one of the tool given above has their own pros and cons as the business

environment is dynamic and budgets are prepared on the basis of predictions which can is

difficult to be correct purely. Given below is the detail of the different advantages and

disadvantages of the budgetary control technique (Giovannoni, Maraghini and Riccaboni, 2011).

Positives

1. Facilitate control - With the help of this technique effective control can be practised

over the various functions of the company as through this system limits are set against

each function. This way the whole department work in a manner that it has only the

available amount of resource to utilise and hence use it to its maximum potentiality.

2. Incorporates efficiency – When the work staff is made to work with limits they work

with greater duty as they know if the project assigned is not finished with the provided

resource than their performance will be questioned. Hence everyone work with greater

efficiency to remain free from any negative interrogation (Soin and Collier, 2013).

3. Improve communication – At the time of budget formulation, interaction between the

head authority and the concern department take place which further improves the

communication level. It is a positive move as while communicating with one another a

better relation is set at the work place which is a positive move for companies growth.

4. Improve employee morale – When the top authority prepares budgets they interact with

their subordinates and this way every individual gets a feeling of belongingness with the

company. They find themselves worth and hence feel motivated and accordingly give

their performance (DRURY, 2013).

Disadvantages / Negatives

9

department and scale of project distinct budgets are prepared among which the most popular are:

Master budget

Cash budget

Sales budget

Zero budget

Operating financial plan

Statics estimates

Cash flow forecast report

Each one of the tool given above has their own pros and cons as the business

environment is dynamic and budgets are prepared on the basis of predictions which can is

difficult to be correct purely. Given below is the detail of the different advantages and

disadvantages of the budgetary control technique (Giovannoni, Maraghini and Riccaboni, 2011).

Positives

1. Facilitate control - With the help of this technique effective control can be practised

over the various functions of the company as through this system limits are set against

each function. This way the whole department work in a manner that it has only the

available amount of resource to utilise and hence use it to its maximum potentiality.

2. Incorporates efficiency – When the work staff is made to work with limits they work

with greater duty as they know if the project assigned is not finished with the provided

resource than their performance will be questioned. Hence everyone work with greater

efficiency to remain free from any negative interrogation (Soin and Collier, 2013).

3. Improve communication – At the time of budget formulation, interaction between the

head authority and the concern department take place which further improves the

communication level. It is a positive move as while communicating with one another a

better relation is set at the work place which is a positive move for companies growth.

4. Improve employee morale – When the top authority prepares budgets they interact with

their subordinates and this way every individual gets a feeling of belongingness with the

company. They find themselves worth and hence feel motivated and accordingly give

their performance (DRURY, 2013).

Disadvantages / Negatives

9

1. Time taking activity – Although budgets has various positive effects on an organisations

it has some limitations too. In order to reach at correct planning enough time is consumed

and hence much time is wasted in case of budget failure.

2. High value procedure – In order to formulate an effective budget management has to

ensure that right person with adequate knowledge is appointed. To get such person good

cost has to be paid which makes it an expensive process cost of which is added to the

ultimate product of the company and hence the value increases.

3. Complex Operation – As various functions are performed at the work place it becomes

difficult to determine each and every aspect which needs to be considered while

formulating the particular financial limit (Li and et. al., 2012).

4. Decrease flexibility – When budgets are set by the higher authorities it reduces the

flexibility at the work place.

M3

Budgetary techniques help in solving the different issues that take place at the work

place. This concept helps in reaching to the desired level of accuracy in management.

D3

The budget system helps in achieving substantial growth in the long run. This is due to

the reason that problems can be better resolved by applying these techniques in organisation.

P5 Solving of financial problems

Various factors and elements which exist in the business environment and which gave

rise to the unnecessary issues should taken into consideration for planning future activities of a

business and to take necessary actions in order to solve them. One of the main issue which exist

in today's business environment is lack of communication. So it comes under the responsibility

of managers to ensure effective and proper communication at various level of firms so that

enterprise can formulate effective policies for the business. By this coordination and cooperation

can be maintain among various operations. It is very necessary that all the required information

should be made available to the managers so that loopholes can be avoided in the process of

business. In this way business can be conducted in an effective manner and strategies can be

implemented in short duration of time and proper functioning of business can be ensured.

Main techniques which are involved in this are stated below:

10

it has some limitations too. In order to reach at correct planning enough time is consumed

and hence much time is wasted in case of budget failure.

2. High value procedure – In order to formulate an effective budget management has to

ensure that right person with adequate knowledge is appointed. To get such person good

cost has to be paid which makes it an expensive process cost of which is added to the

ultimate product of the company and hence the value increases.

3. Complex Operation – As various functions are performed at the work place it becomes

difficult to determine each and every aspect which needs to be considered while

formulating the particular financial limit (Li and et. al., 2012).

4. Decrease flexibility – When budgets are set by the higher authorities it reduces the

flexibility at the work place.

M3

Budgetary techniques help in solving the different issues that take place at the work

place. This concept helps in reaching to the desired level of accuracy in management.

D3

The budget system helps in achieving substantial growth in the long run. This is due to

the reason that problems can be better resolved by applying these techniques in organisation.

P5 Solving of financial problems

Various factors and elements which exist in the business environment and which gave

rise to the unnecessary issues should taken into consideration for planning future activities of a

business and to take necessary actions in order to solve them. One of the main issue which exist

in today's business environment is lack of communication. So it comes under the responsibility

of managers to ensure effective and proper communication at various level of firms so that

enterprise can formulate effective policies for the business. By this coordination and cooperation

can be maintain among various operations. It is very necessary that all the required information

should be made available to the managers so that loopholes can be avoided in the process of

business. In this way business can be conducted in an effective manner and strategies can be

implemented in short duration of time and proper functioning of business can be ensured.

Main techniques which are involved in this are stated below:

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.