Management Accounting: Systems, Reporting, and Problem Analysis

VerifiedAdded on 2020/06/04

|13

|4037

|148

Report

AI Summary

This report provides an analysis of management accounting and its importance in organizational decision-making. It examines various management accounting systems and reporting methods, including job cost reports, performance reports, account receivable reports, and inventory management reports. The report also discusses different cost accounting systems, such as absorption costing and marginal costing, used to evaluate net profit. Furthermore, it explores the benefits and disadvantages of planning tools used in budgetary control and analyzes financial problems and measures to overcome them, offering a comprehensive overview of management accounting techniques and their practical applications in managing business operations and finances.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

Table of Contents.............................................................................................................................2

INTRODUCTION...........................................................................................................................1

SECTION 1.....................................................................................................................................1

P1. Management accounting and its importance in decision making process.............................1

P2. Different type of management accounting systems used for management accoutring

reporting.......................................................................................................................................3

M1. Advantage of using management accounting system..........................................................4

D1. Critical evaluation of accounting and reporting system.......................................................5

P3. Types of cost accounting system used to evaluate net profit for the organisation................5

M2. Evaluation of type of management accounting techniques..................................................8

D2. Interpretation and reconciliation of income statement.........................................................8

SECTION 2.....................................................................................................................................8

PART A...........................................................................................................................................8

P4. Benefits and disadvantages of using planning tools used in budgetary control process.......8

M3. Analysing planning tools......................................................................................................9

D3. Critical analysis of financial problems.................................................................................9

PART B...........................................................................................................................................9

P5. Types of financial problems and measures to overcome financial problems........................9

M4. Evaluation of financial problem.........................................................................................10

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

Table of Contents.............................................................................................................................2

INTRODUCTION...........................................................................................................................1

SECTION 1.....................................................................................................................................1

P1. Management accounting and its importance in decision making process.............................1

P2. Different type of management accounting systems used for management accoutring

reporting.......................................................................................................................................3

M1. Advantage of using management accounting system..........................................................4

D1. Critical evaluation of accounting and reporting system.......................................................5

P3. Types of cost accounting system used to evaluate net profit for the organisation................5

M2. Evaluation of type of management accounting techniques..................................................8

D2. Interpretation and reconciliation of income statement.........................................................8

SECTION 2.....................................................................................................................................8

PART A...........................................................................................................................................8

P4. Benefits and disadvantages of using planning tools used in budgetary control process.......8

M3. Analysing planning tools......................................................................................................9

D3. Critical analysis of financial problems.................................................................................9

PART B...........................................................................................................................................9

P5. Types of financial problems and measures to overcome financial problems........................9

M4. Evaluation of financial problem.........................................................................................10

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION

Management accounting is a concept which is considered internal aspect of managing

operations and functions of organisation. Scope of accounting and reporting has been vast

subject in terms of exploring the business operations and management at large level. This is one

of the essential aspect which helps to consolidate the financial transactions and events subject to

make financial accounts of organisation. This report is prepared to analyse the importance of

management accounting subject to organise and manage business. There are primary objectives

and appropriateness of accounting techniques are defined in this context. Reporting methods are

also discussed which assist the accounting reporting (Boyns and Edwards, 2013).

There are sections are divided in this report. In which, first section define the vast

information and knowledge subject to both management accounting system and management

accounting reporting. Second sections examine various types of costing methods which are used

by organisation to manage and control cost. Advantages and disadvantages of types of planning

tools which are used in budgetary control process.

SECTION 1

P1. Management accounting and its importance in decision making process

It is seen that the changing business environment has changed the dimension of

accounting and reporting within the organisation. Accounting framework is adopted by business

organisations as per their nature and scope. It is required for organisations to manage and operate

the business operations in such a manner so that the effectiveness be maintained. A well

organised management accounting system is the only key to lead the operations and management

of organisation towards its desired success. There are appropriate accounting and reporting

systems are used by organisations in order to maintain effectiveness and the reliability among

internal parties of organisation. There are type of information remain essential in terms of

making financial plans and financial statements.

There is a use of primary sources and secondary sources used to make accurate finance

and accounting plans for management. Main objective and purpose of management accounting

system is to make strategies and plans as per defined structure and plan. These information not

only helpful for internal parties but also beneficial for outsiders of an organisation such as

stakeholders, investors, financiers, banks and financial institutions. More over these information

helps to align the structure in such a manner so that the managers of organisation be able to align

1

Management accounting is a concept which is considered internal aspect of managing

operations and functions of organisation. Scope of accounting and reporting has been vast

subject in terms of exploring the business operations and management at large level. This is one

of the essential aspect which helps to consolidate the financial transactions and events subject to

make financial accounts of organisation. This report is prepared to analyse the importance of

management accounting subject to organise and manage business. There are primary objectives

and appropriateness of accounting techniques are defined in this context. Reporting methods are

also discussed which assist the accounting reporting (Boyns and Edwards, 2013).

There are sections are divided in this report. In which, first section define the vast

information and knowledge subject to both management accounting system and management

accounting reporting. Second sections examine various types of costing methods which are used

by organisation to manage and control cost. Advantages and disadvantages of types of planning

tools which are used in budgetary control process.

SECTION 1

P1. Management accounting and its importance in decision making process

It is seen that the changing business environment has changed the dimension of

accounting and reporting within the organisation. Accounting framework is adopted by business

organisations as per their nature and scope. It is required for organisations to manage and operate

the business operations in such a manner so that the effectiveness be maintained. A well

organised management accounting system is the only key to lead the operations and management

of organisation towards its desired success. There are appropriate accounting and reporting

systems are used by organisations in order to maintain effectiveness and the reliability among

internal parties of organisation. There are type of information remain essential in terms of

making financial plans and financial statements.

There is a use of primary sources and secondary sources used to make accurate finance

and accounting plans for management. Main objective and purpose of management accounting

system is to make strategies and plans as per defined structure and plan. These information not

only helpful for internal parties but also beneficial for outsiders of an organisation such as

stakeholders, investors, financiers, banks and financial institutions. More over these information

helps to align the structure in such a manner so that the managers of organisation be able to align

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

and sort out the plan in effective manner. Enhancing and increasing the appropriateness and

affectivity of management and operation is also one of the prime objectives of management

accounting (Zoni, Dossi and Morelli, 2012).

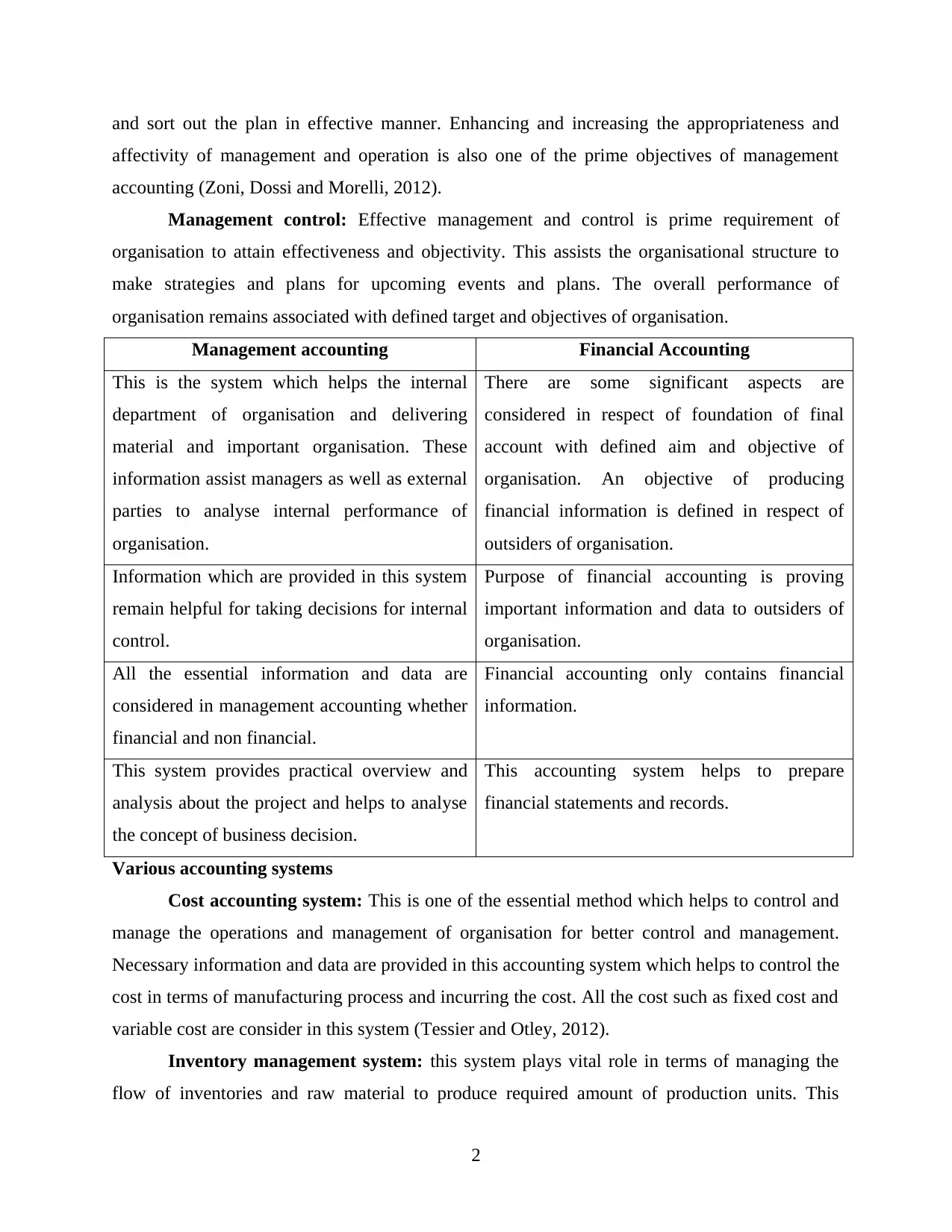

Management control: Effective management and control is prime requirement of

organisation to attain effectiveness and objectivity. This assists the organisational structure to

make strategies and plans for upcoming events and plans. The overall performance of

organisation remains associated with defined target and objectives of organisation.

Management accounting Financial Accounting

This is the system which helps the internal

department of organisation and delivering

material and important organisation. These

information assist managers as well as external

parties to analyse internal performance of

organisation.

There are some significant aspects are

considered in respect of foundation of final

account with defined aim and objective of

organisation. An objective of producing

financial information is defined in respect of

outsiders of organisation.

Information which are provided in this system

remain helpful for taking decisions for internal

control.

Purpose of financial accounting is proving

important information and data to outsiders of

organisation.

All the essential information and data are

considered in management accounting whether

financial and non financial.

Financial accounting only contains financial

information.

This system provides practical overview and

analysis about the project and helps to analyse

the concept of business decision.

This accounting system helps to prepare

financial statements and records.

Various accounting systems

Cost accounting system: This is one of the essential method which helps to control and

manage the operations and management of organisation for better control and management.

Necessary information and data are provided in this accounting system which helps to control the

cost in terms of manufacturing process and incurring the cost. All the cost such as fixed cost and

variable cost are consider in this system (Tessier and Otley, 2012).

Inventory management system: this system plays vital role in terms of managing the

flow of inventories and raw material to produce required amount of production units. This

2

affectivity of management and operation is also one of the prime objectives of management

accounting (Zoni, Dossi and Morelli, 2012).

Management control: Effective management and control is prime requirement of

organisation to attain effectiveness and objectivity. This assists the organisational structure to

make strategies and plans for upcoming events and plans. The overall performance of

organisation remains associated with defined target and objectives of organisation.

Management accounting Financial Accounting

This is the system which helps the internal

department of organisation and delivering

material and important organisation. These

information assist managers as well as external

parties to analyse internal performance of

organisation.

There are some significant aspects are

considered in respect of foundation of final

account with defined aim and objective of

organisation. An objective of producing

financial information is defined in respect of

outsiders of organisation.

Information which are provided in this system

remain helpful for taking decisions for internal

control.

Purpose of financial accounting is proving

important information and data to outsiders of

organisation.

All the essential information and data are

considered in management accounting whether

financial and non financial.

Financial accounting only contains financial

information.

This system provides practical overview and

analysis about the project and helps to analyse

the concept of business decision.

This accounting system helps to prepare

financial statements and records.

Various accounting systems

Cost accounting system: This is one of the essential method which helps to control and

manage the operations and management of organisation for better control and management.

Necessary information and data are provided in this accounting system which helps to control the

cost in terms of manufacturing process and incurring the cost. All the cost such as fixed cost and

variable cost are consider in this system (Tessier and Otley, 2012).

Inventory management system: this system plays vital role in terms of managing the

flow of inventories and raw material to produce required amount of production units. This

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

accounting system assists managers to determine the optimum level of requirement of raw

material and finished goods for fulfilling the supply and demand. This system basically helps to

determine the level of inventory to be retained in stores for producing goods. With the changing

trends it is seen that there are type of inventory management systems are used in organisational

context to control the level of outcomes inventories.

Price optimisation: this is one of the essential system which assist managers to make

effective pricing strategies and plans. This process not only assist the pricing structure but also

helps the decision making process. Price and cost are determined on the basis of overall cost of

production of manufacturing production process.

Job costing system: there are type of functions and operations remain bifurcated in

defining the structure of organisation. Aim and objective of this accounting basically remain

associated with analysing the cost of each department and section. This accounting system

remain beneficial for those organisation which deals in multiple process and sections

P2. Different type of management accounting systems used for management accoutring reporting

Reporting is one of the essential element which helps management and senior level

authorities subject to understand the essential aspects and elements which remain associated with

financial planning and process. Moreover, this information helps to analyse the sustainability and

effectiveness of management and operations for better application management. There are type

of information are considered and produced under this system which helps to sort out the plans

and management of operations for better understanding (Van der Stede, 2015). There is a

systematic procedure is followed in terms of managing and operation the essential aspect in

terms of managing the operations and system of organisation. Reporting work is very important

element in organisational context which helps to align the structure of organisation with effective

management and operations. Planning, decision making and the distribution of financial aspects

are the main aspects which are considered essential in organisational context. It is very important

for organisations to manage the flow of operations and management for getting desired results.

There are types of reporting methods used by organisation to determine the essential

aspect in terms of managing and determining the knowledge and skills of employees parallel to

organisation's performance. Job cost, budget performance and inventory management reporting

system is basically remain associated with making the profitability and management in such an

manner so that good image of business can be reflected. This basically helps to mange and

3

material and finished goods for fulfilling the supply and demand. This system basically helps to

determine the level of inventory to be retained in stores for producing goods. With the changing

trends it is seen that there are type of inventory management systems are used in organisational

context to control the level of outcomes inventories.

Price optimisation: this is one of the essential system which assist managers to make

effective pricing strategies and plans. This process not only assist the pricing structure but also

helps the decision making process. Price and cost are determined on the basis of overall cost of

production of manufacturing production process.

Job costing system: there are type of functions and operations remain bifurcated in

defining the structure of organisation. Aim and objective of this accounting basically remain

associated with analysing the cost of each department and section. This accounting system

remain beneficial for those organisation which deals in multiple process and sections

P2. Different type of management accounting systems used for management accoutring reporting

Reporting is one of the essential element which helps management and senior level

authorities subject to understand the essential aspects and elements which remain associated with

financial planning and process. Moreover, this information helps to analyse the sustainability and

effectiveness of management and operations for better application management. There are type

of information are considered and produced under this system which helps to sort out the plans

and management of operations for better understanding (Van der Stede, 2015). There is a

systematic procedure is followed in terms of managing and operation the essential aspect in

terms of managing the operations and system of organisation. Reporting work is very important

element in organisational context which helps to align the structure of organisation with effective

management and operations. Planning, decision making and the distribution of financial aspects

are the main aspects which are considered essential in organisational context. It is very important

for organisations to manage the flow of operations and management for getting desired results.

There are types of reporting methods used by organisation to determine the essential

aspect in terms of managing and determining the knowledge and skills of employees parallel to

organisation's performance. Job cost, budget performance and inventory management reporting

system is basically remain associated with making the profitability and management in such an

manner so that good image of business can be reflected. This basically helps to mange and

3

operating the business for building goodwill for the company. There are communications and

coordination need to set between the accounting system and management is one of the essential

aspects in organisational context. There are types of reporting methods are analysed in

organisational context which are defined as follows;

Job cost reports: these are the reports which help to determine the report in terms of cost

of each department. There are types of analysing the cost of production and manufacturing the

details related to expanding the projects and process of manufacturing. Overall activities and

plans are defined subject to analysing the cost incurred at particular cost centre.

Performance reports: As per the performance reports overall activities and performance

of departments are defined in this context. There are type of reports prepared on periodic basis to

analyse the essential aspect remain associated with reducing the structure of cost and analysis.

There is an comparison done between actual and budgeted results for making the essential

aspects to determine the performance of organisation. These reports are prepared on regular basis

to track regular performance of organisation (Klemstine and Maher, 2014).

Account receivable report: Account receivable reports are considered in respect of

analyse the reports and invoice. There is a proper record retained in respect of tracking the

details of debtors to be maid and remain unpaid for the particular period. Reports which are

produced under this reporting method help to resolve and sort out the plans for better

management and coordination with suppliers and managers. These reports also plays vital role in

terms of decision making process.

Inventory management report: To manage the operation and management it is require

aligning the effective management. This method helps to bifurcate the level of inventories as per

requirement of business. There is overall step is analysed in this reporting method subject to

manage the flow of operation. Types of inventory methods are used such as LIFO, EOQ and

FIFO (Lim, 2011).

M1. Advantage of using management accounting system

There are various crucial benefits of using appropriate accounting system. All of them are

equally important for the company. With the use of price optimisation overall perception of

customers can be determine in effective manner. While inventory management system used to

track overall position of stock that is being kept by the company. Similarly all other types of

systems are more reliable for the company.

4

coordination need to set between the accounting system and management is one of the essential

aspects in organisational context. There are types of reporting methods are analysed in

organisational context which are defined as follows;

Job cost reports: these are the reports which help to determine the report in terms of cost

of each department. There are types of analysing the cost of production and manufacturing the

details related to expanding the projects and process of manufacturing. Overall activities and

plans are defined subject to analysing the cost incurred at particular cost centre.

Performance reports: As per the performance reports overall activities and performance

of departments are defined in this context. There are type of reports prepared on periodic basis to

analyse the essential aspect remain associated with reducing the structure of cost and analysis.

There is an comparison done between actual and budgeted results for making the essential

aspects to determine the performance of organisation. These reports are prepared on regular basis

to track regular performance of organisation (Klemstine and Maher, 2014).

Account receivable report: Account receivable reports are considered in respect of

analyse the reports and invoice. There is a proper record retained in respect of tracking the

details of debtors to be maid and remain unpaid for the particular period. Reports which are

produced under this reporting method help to resolve and sort out the plans for better

management and coordination with suppliers and managers. These reports also plays vital role in

terms of decision making process.

Inventory management report: To manage the operation and management it is require

aligning the effective management. This method helps to bifurcate the level of inventories as per

requirement of business. There is overall step is analysed in this reporting method subject to

manage the flow of operation. Types of inventory methods are used such as LIFO, EOQ and

FIFO (Lim, 2011).

M1. Advantage of using management accounting system

There are various crucial benefits of using appropriate accounting system. All of them are

equally important for the company. With the use of price optimisation overall perception of

customers can be determine in effective manner. While inventory management system used to

track overall position of stock that is being kept by the company. Similarly all other types of

systems are more reliable for the company.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

D1. Critical evaluation of accounting and reporting system

According to the above discussed all kind of reports those are essential for increasing

overall growth and performance of an organisation in more effective manner. Some of them are

performance report which is used to make comparison of actual performance with the standard

one. While account receivable report are use to analyse total time needed to collect necessary

payments from debtors

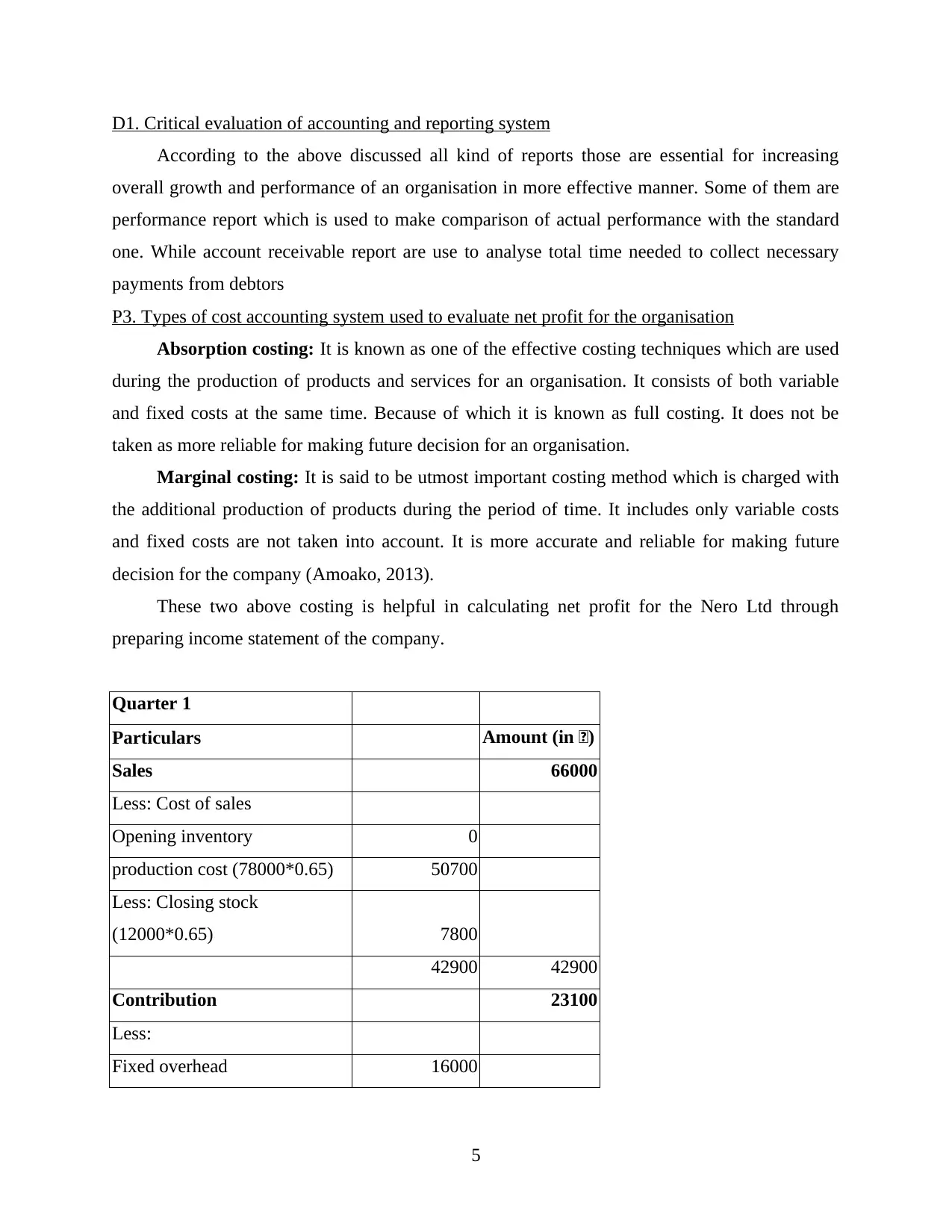

P3. Types of cost accounting system used to evaluate net profit for the organisation

Absorption costing: It is known as one of the effective costing techniques which are used

during the production of products and services for an organisation. It consists of both variable

and fixed costs at the same time. Because of which it is known as full costing. It does not be

taken as more reliable for making future decision for an organisation.

Marginal costing: It is said to be utmost important costing method which is charged with

the additional production of products during the period of time. It includes only variable costs

and fixed costs are not taken into account. It is more accurate and reliable for making future

decision for the company (Amoako, 2013).

These two above costing is helpful in calculating net profit for the Nero Ltd through

preparing income statement of the company.

Quarter 1

Particulars Amount (in £)

Sales 66000

Less: Cost of sales

Opening inventory 0

production cost (78000*0.65) 50700

Less: Closing stock

(12000*0.65) 7800

42900 42900

Contribution 23100

Less:

Fixed overhead 16000

5

According to the above discussed all kind of reports those are essential for increasing

overall growth and performance of an organisation in more effective manner. Some of them are

performance report which is used to make comparison of actual performance with the standard

one. While account receivable report are use to analyse total time needed to collect necessary

payments from debtors

P3. Types of cost accounting system used to evaluate net profit for the organisation

Absorption costing: It is known as one of the effective costing techniques which are used

during the production of products and services for an organisation. It consists of both variable

and fixed costs at the same time. Because of which it is known as full costing. It does not be

taken as more reliable for making future decision for an organisation.

Marginal costing: It is said to be utmost important costing method which is charged with

the additional production of products during the period of time. It includes only variable costs

and fixed costs are not taken into account. It is more accurate and reliable for making future

decision for the company (Amoako, 2013).

These two above costing is helpful in calculating net profit for the Nero Ltd through

preparing income statement of the company.

Quarter 1

Particulars Amount (in £)

Sales 66000

Less: Cost of sales

Opening inventory 0

production cost (78000*0.65) 50700

Less: Closing stock

(12000*0.65) 7800

42900 42900

Contribution 23100

Less:

Fixed overhead 16000

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

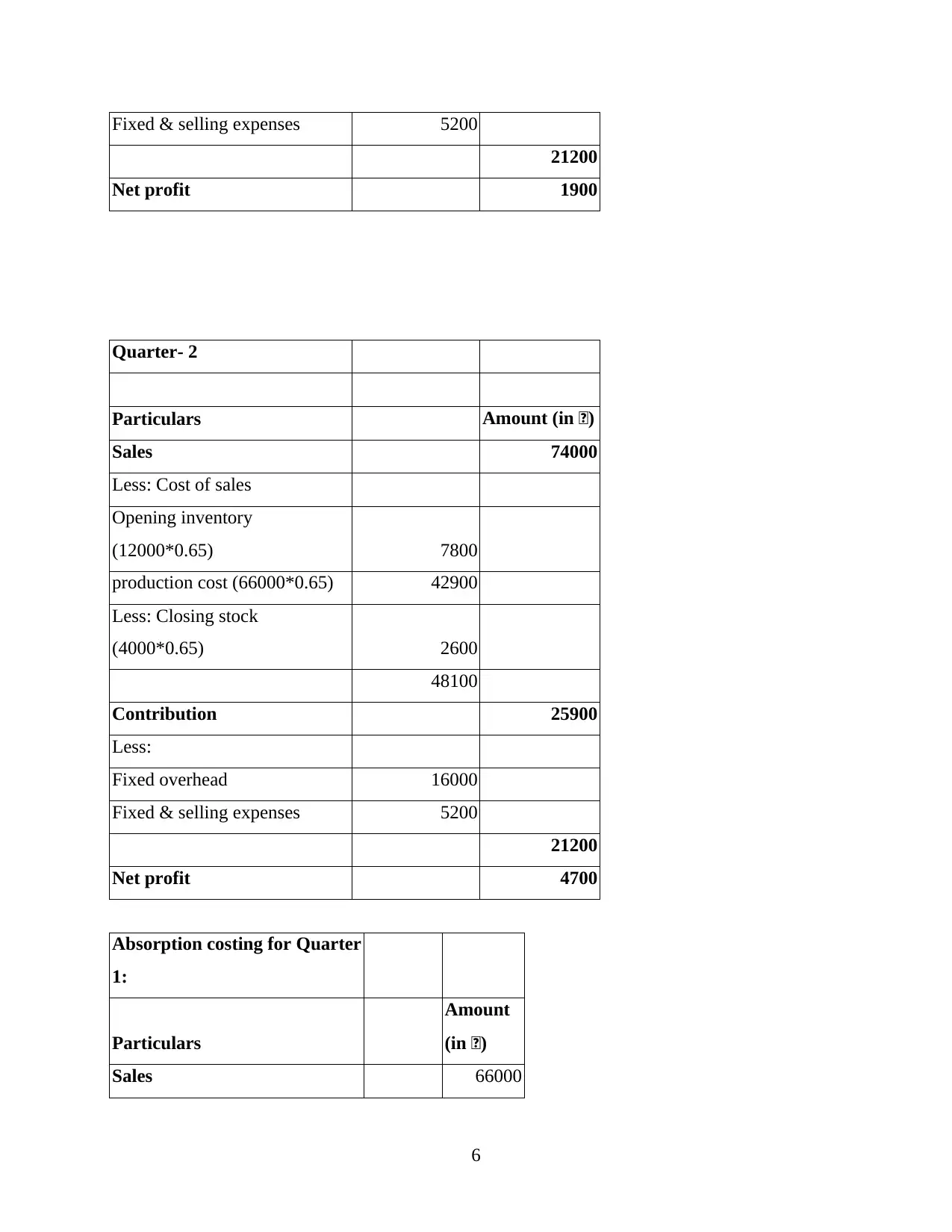

Fixed & selling expenses 5200

21200

Net profit 1900

Quarter- 2

Particulars Amount (in £)

Sales 74000

Less: Cost of sales

Opening inventory

(12000*0.65) 7800

production cost (66000*0.65) 42900

Less: Closing stock

(4000*0.65) 2600

48100

Contribution 25900

Less:

Fixed overhead 16000

Fixed & selling expenses 5200

21200

Net profit 4700

Absorption costing for Quarter

1:

Particulars

Amount

(in £)

Sales 66000

6

21200

Net profit 1900

Quarter- 2

Particulars Amount (in £)

Sales 74000

Less: Cost of sales

Opening inventory

(12000*0.65) 7800

production cost (66000*0.65) 42900

Less: Closing stock

(4000*0.65) 2600

48100

Contribution 25900

Less:

Fixed overhead 16000

Fixed & selling expenses 5200

21200

Net profit 4700

Absorption costing for Quarter

1:

Particulars

Amount

(in £)

Sales 66000

6

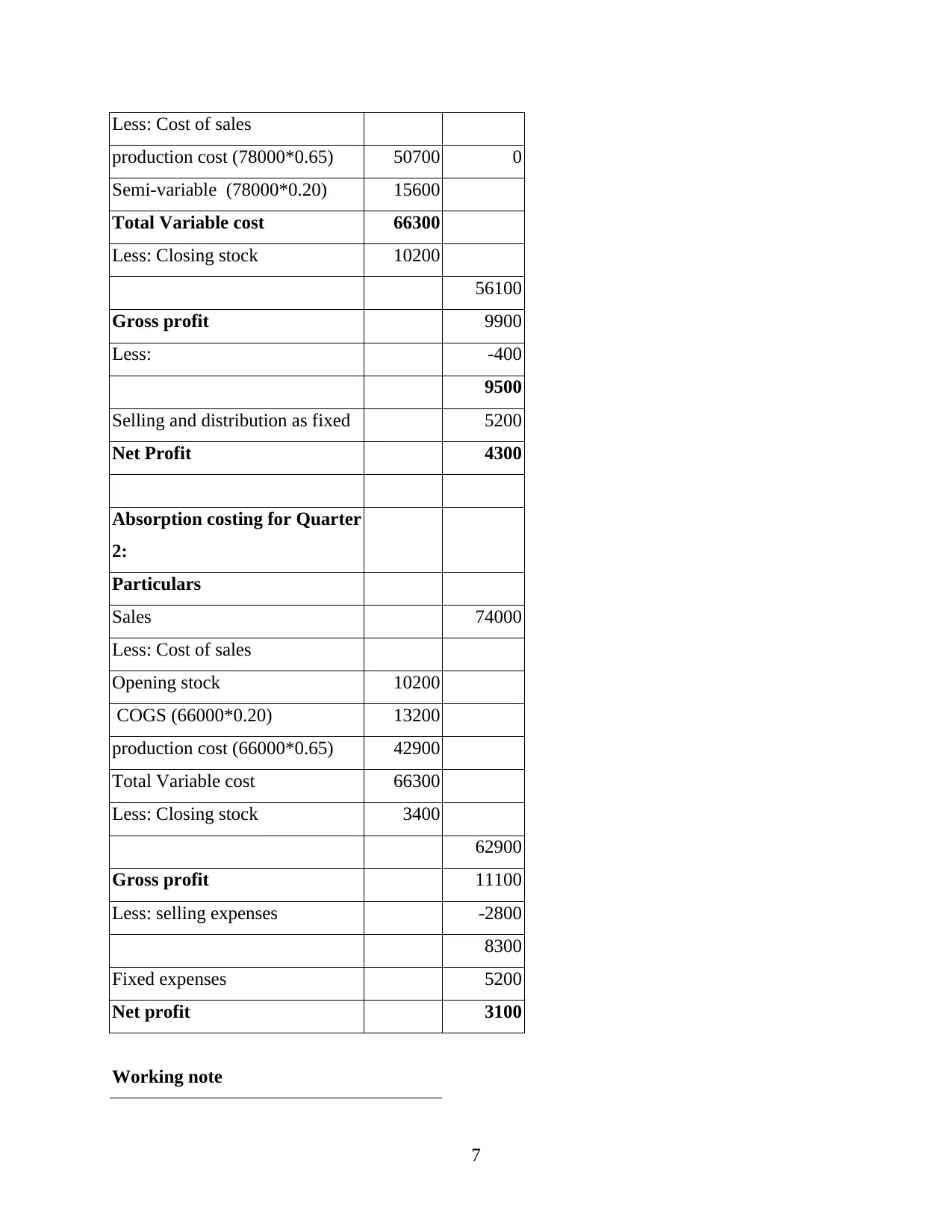

Less: Cost of sales

production cost (78000*0.65) 50700 0

Semi-variable (78000*0.20) 15600

Total Variable cost 66300

Less: Closing stock 10200

56100

Gross profit 9900

Less: -400

9500

Selling and distribution as fixed 5200

Net Profit 4300

Absorption costing for Quarter

2:

Particulars

Sales 74000

Less: Cost of sales

Opening stock 10200

COGS (66000*0.20) 13200

production cost (66000*0.65) 42900

Total Variable cost 66300

Less: Closing stock 3400

62900

Gross profit 11100

Less: selling expenses -2800

8300

Fixed expenses 5200

Net profit 3100

Working note

7

production cost (78000*0.65) 50700 0

Semi-variable (78000*0.20) 15600

Total Variable cost 66300

Less: Closing stock 10200

56100

Gross profit 9900

Less: -400

9500

Selling and distribution as fixed 5200

Net Profit 4300

Absorption costing for Quarter

2:

Particulars

Sales 74000

Less: Cost of sales

Opening stock 10200

COGS (66000*0.20) 13200

production cost (66000*0.65) 42900

Total Variable cost 66300

Less: Closing stock 3400

62900

Gross profit 11100

Less: selling expenses -2800

8300

Fixed expenses 5200

Net profit 3100

Working note

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Fixed costs 16000

Budgeted cost of production

80000

per units

Budgeted fixed cost 0.2

Variable cost per units 0.65

M2. Evaluation of type of management accounting techniques

There are various types of accounting techniques which are essential for increasing overall

performance of an organisation. Some of them are standard costing tools which are used to make

comparison of actual financial position of the company. Whereas marginal costing is helpful in

evaluating total cost incur on production of additional units.

D2. Interpretation and reconciliation of income statement

In accordance with above data calculated with the use of absorption and marginal costing, it

has been seen that with the total fixed cost of 16000 they are able to earn net profit of 3100 and

4700 during the time.

SECTION 2

PART A

P4. Benefits and disadvantages of using planning tools used in budgetary control process

There are various types of planning tools which are essential for increase overall growth

for Nero Plc (Klychova and et. al., 2015). It is essential make use of right tools so that budgets

can be made in more effective and accurate manner. Some of them are discussed underneath:

Forecasting tools: According to these particular planning tools managers will used to

estimate future costs and expenditure a company is going in incur with the available resources. It

is vital to enhance overall growth and financial stability in effective manner. There are certain

benefits of using these tools.

Advantage: This seems too effective enough to make planning for future growth as future

is more beneficial for the company to increase overall revenue at the same point of time.

Disadvantage: The major limitation of these type of tools is mostly relies on future

prediction which is uncertain to estimate.

Contingency tools: As per this tools which are used to analyse and control total risk

factors that are associated with the company’s internal as well as external department of an

8

Budgeted cost of production

80000

per units

Budgeted fixed cost 0.2

Variable cost per units 0.65

M2. Evaluation of type of management accounting techniques

There are various types of accounting techniques which are essential for increasing overall

performance of an organisation. Some of them are standard costing tools which are used to make

comparison of actual financial position of the company. Whereas marginal costing is helpful in

evaluating total cost incur on production of additional units.

D2. Interpretation and reconciliation of income statement

In accordance with above data calculated with the use of absorption and marginal costing, it

has been seen that with the total fixed cost of 16000 they are able to earn net profit of 3100 and

4700 during the time.

SECTION 2

PART A

P4. Benefits and disadvantages of using planning tools used in budgetary control process

There are various types of planning tools which are essential for increase overall growth

for Nero Plc (Klychova and et. al., 2015). It is essential make use of right tools so that budgets

can be made in more effective and accurate manner. Some of them are discussed underneath:

Forecasting tools: According to these particular planning tools managers will used to

estimate future costs and expenditure a company is going in incur with the available resources. It

is vital to enhance overall growth and financial stability in effective manner. There are certain

benefits of using these tools.

Advantage: This seems too effective enough to make planning for future growth as future

is more beneficial for the company to increase overall revenue at the same point of time.

Disadvantage: The major limitation of these type of tools is mostly relies on future

prediction which is uncertain to estimate.

Contingency tools: As per this tools which are used to analyse and control total risk

factors that are associated with the company’s internal as well as external department of an

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

organisation. Risk free data would be helpful for the company to increase overall growth and

sustainability in more effective and reliable manner.

Advantage: As per this Nero Ltd would easily be able to make modification in public

relation. By the help of this, company can deal with all kind of competition that are exist with an

organisation (JOSHI and et. al., 2011).

Disadvantage: In accordance with this, it is very hard to detect all kind of risk because of

its quantitative nature. The future risks are not be able to address in the allotted time period.

M3. Analysing planning tools

In respect to all above discussed budgetary control tools, managers can make use of

various planning techniques. Such as by the help of forecasting techniques they are able to

predict total amount of cost which is being invested by Nero Ltd on the production of products

and services. Contingency techniques can lead to analyse total risk factors those are affecting

growth and financial position at the same period of time.

D3. Critical analysis of financial problems

According to all necessary issues those are arises in an organisation. Some financial issues

are more dynamic which will increase maximum burden over the company’s overall goodwill.

Issues can be related with profitability level, product and services quality that are exist for an

organisation. These issues can be overcome through using key performance indicators and

financial governance.

PART B

P5. Types of financial problems and measures to overcome financial problems

In accordance with total financial problems that are affecting the overall profitability for an

organisation. These issues are affecting total sustainability and growth during the period of time.

It can be use to analyse overall gain by using resources in more reliable and accurate manner

(Abdel-Kader, 2011). Some of the issues can increase maximum chances of mistakes that is

more crucial concern for accountant while evaluating financial statements of an organisation.

There are certain issues those are associated with the companies are:

Profit level: It is known as effective issues which will directly make impacts on the future

growth of the company. In case owner will not be able to generate more funds then they are not

being able to earn maximum profit during the time (Bobryshev and et. al., 2015).

9

sustainability in more effective and reliable manner.

Advantage: As per this Nero Ltd would easily be able to make modification in public

relation. By the help of this, company can deal with all kind of competition that are exist with an

organisation (JOSHI and et. al., 2011).

Disadvantage: In accordance with this, it is very hard to detect all kind of risk because of

its quantitative nature. The future risks are not be able to address in the allotted time period.

M3. Analysing planning tools

In respect to all above discussed budgetary control tools, managers can make use of

various planning techniques. Such as by the help of forecasting techniques they are able to

predict total amount of cost which is being invested by Nero Ltd on the production of products

and services. Contingency techniques can lead to analyse total risk factors those are affecting

growth and financial position at the same period of time.

D3. Critical analysis of financial problems

According to all necessary issues those are arises in an organisation. Some financial issues

are more dynamic which will increase maximum burden over the company’s overall goodwill.

Issues can be related with profitability level, product and services quality that are exist for an

organisation. These issues can be overcome through using key performance indicators and

financial governance.

PART B

P5. Types of financial problems and measures to overcome financial problems

In accordance with total financial problems that are affecting the overall profitability for an

organisation. These issues are affecting total sustainability and growth during the period of time.

It can be use to analyse overall gain by using resources in more reliable and accurate manner

(Abdel-Kader, 2011). Some of the issues can increase maximum chances of mistakes that is

more crucial concern for accountant while evaluating financial statements of an organisation.

There are certain issues those are associated with the companies are:

Profit level: It is known as effective issues which will directly make impacts on the future

growth of the company. In case owner will not be able to generate more funds then they are not

being able to earn maximum profit during the time (Bobryshev and et. al., 2015).

9

Product and services quality: Another big issue is associated with the product

manufactured by the company. While at the same point of time services which is provided to the

customers. It can enhance maximum loss in case they are dealing with low capital.

In order to resolve all the above issues, manager need to make use of some effective

financial tools that are liable to deal with those in well organise manner. Some of them are

discussed underneath:

Key Performance indicators: It is known as one of the primary tools that are liable to

control the impacts that are associated with the company. These issues can leads to make

comparison of actual data with the standard one.

Financial governance: It is said to be appropriate rules and regulations that are being

made by local government in order to operate business in well planned manner. These policies

can assist an organisation to regulate their operations as per the mentioned accounting guidelines

(Sisaye and Birnberg, 2012).

M4. Evaluation of financial problem

According to the above financial issues a company would not be able to attain their aims and

objective in systematic manner. In respect to deal with them managers need to make use of well

appropriate tools such as key performance indicators, budgetary techniques and benchmarking.

All these are useful to increase productivity as well as efficiency of an organisation in more

effectively.

CONCLUSION

From the above project report, it has been articulated that management need to make proper

understanding of all essential requirements those are effective in future planning for a Nero Ltd.

There are certain tools and techniques which are helpful for the company to record the

accounting data into their respective format. With the use of accounting and reporting system

they are able to make plan in order to increase their goodwill. Various costing techniques are

used to analyse total net incomes they are earning for the company. All of these are discussed in

effective manner to increase future growth and sustainability.

10

manufactured by the company. While at the same point of time services which is provided to the

customers. It can enhance maximum loss in case they are dealing with low capital.

In order to resolve all the above issues, manager need to make use of some effective

financial tools that are liable to deal with those in well organise manner. Some of them are

discussed underneath:

Key Performance indicators: It is known as one of the primary tools that are liable to

control the impacts that are associated with the company. These issues can leads to make

comparison of actual data with the standard one.

Financial governance: It is said to be appropriate rules and regulations that are being

made by local government in order to operate business in well planned manner. These policies

can assist an organisation to regulate their operations as per the mentioned accounting guidelines

(Sisaye and Birnberg, 2012).

M4. Evaluation of financial problem

According to the above financial issues a company would not be able to attain their aims and

objective in systematic manner. In respect to deal with them managers need to make use of well

appropriate tools such as key performance indicators, budgetary techniques and benchmarking.

All these are useful to increase productivity as well as efficiency of an organisation in more

effectively.

CONCLUSION

From the above project report, it has been articulated that management need to make proper

understanding of all essential requirements those are effective in future planning for a Nero Ltd.

There are certain tools and techniques which are helpful for the company to record the

accounting data into their respective format. With the use of accounting and reporting system

they are able to make plan in order to increase their goodwill. Various costing techniques are

used to analyse total net incomes they are earning for the company. All of these are discussed in

effective manner to increase future growth and sustainability.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.