Detailed Accounting Systems & Processes Assignment Solution - Finance

VerifiedAdded on 2020/04/07

|38

|2799

|39

Homework Assignment

AI Summary

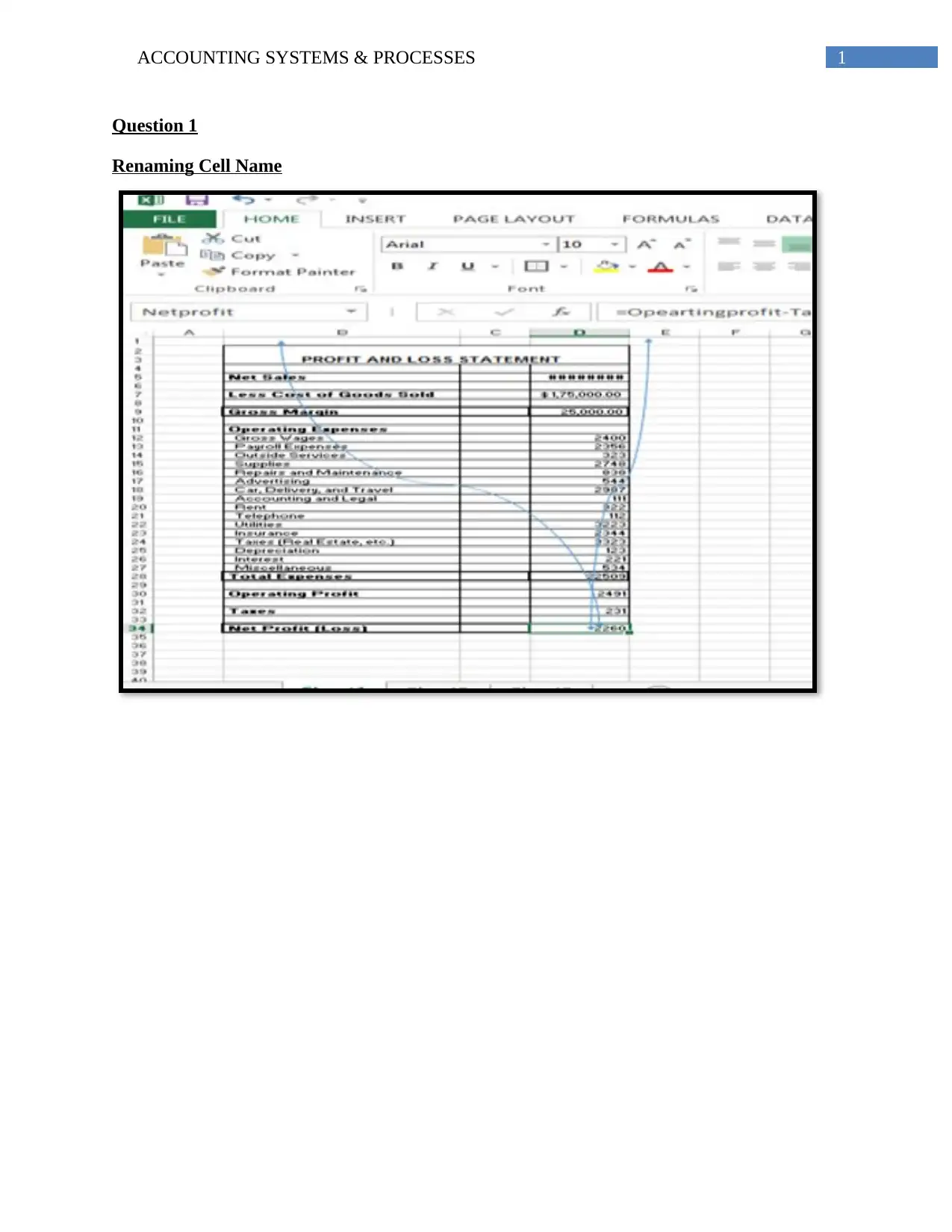

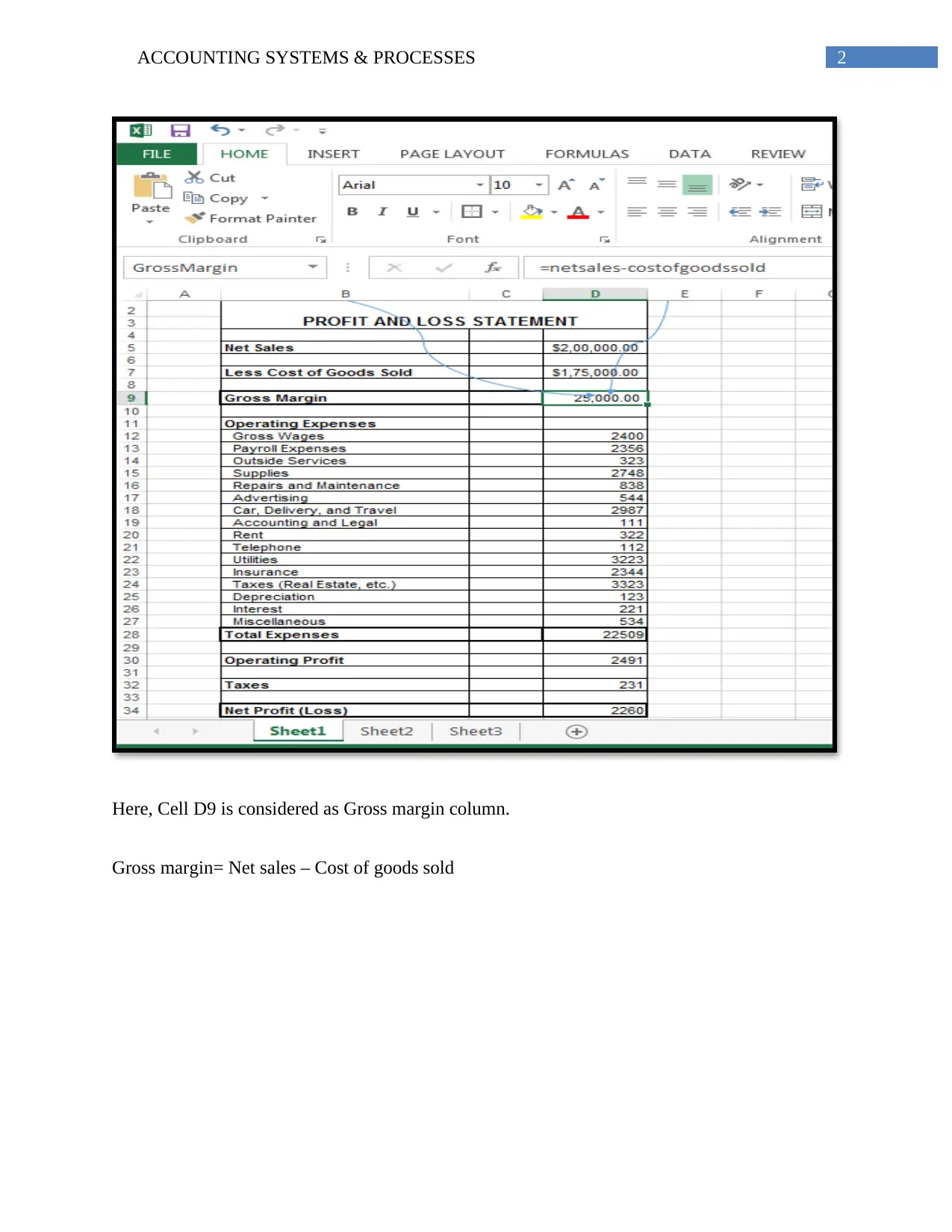

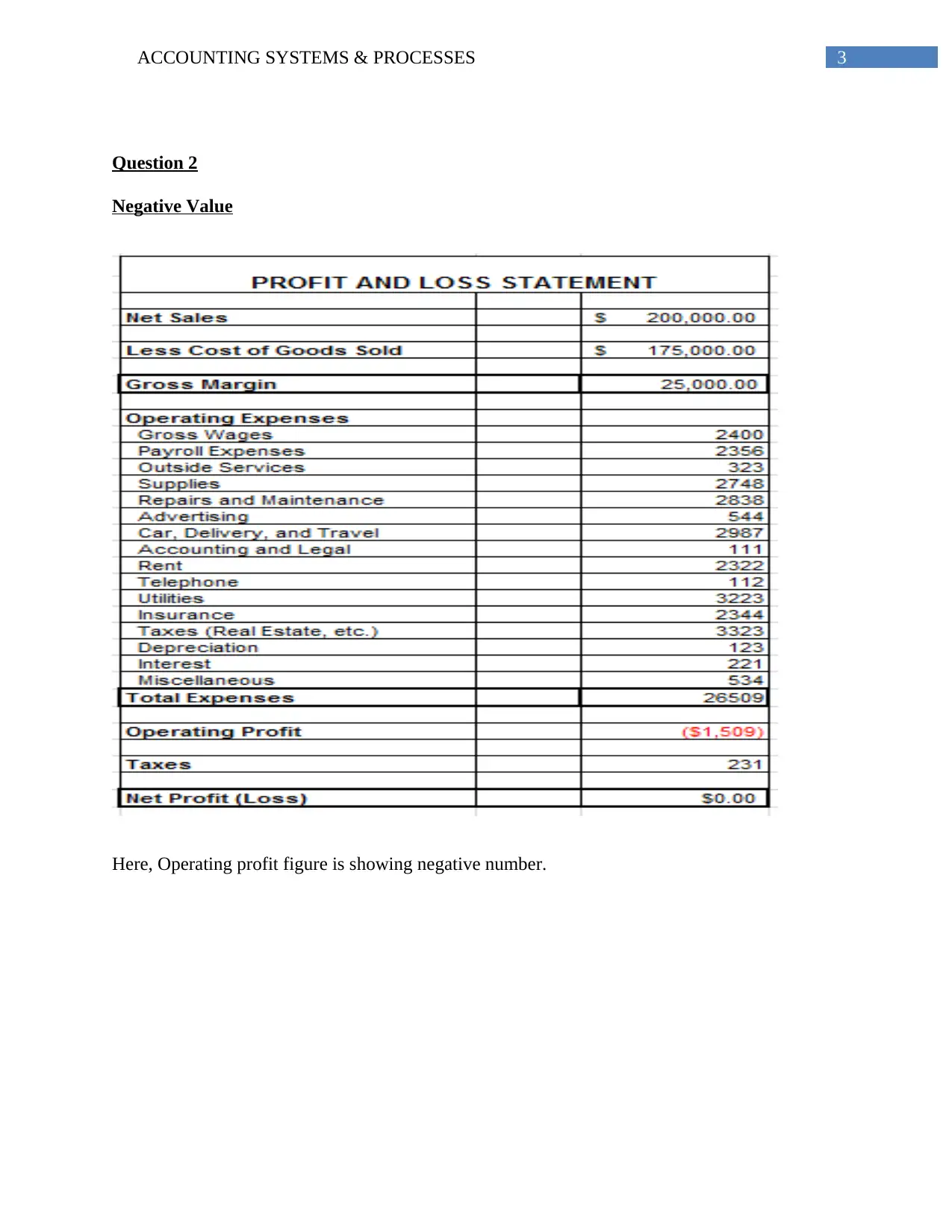

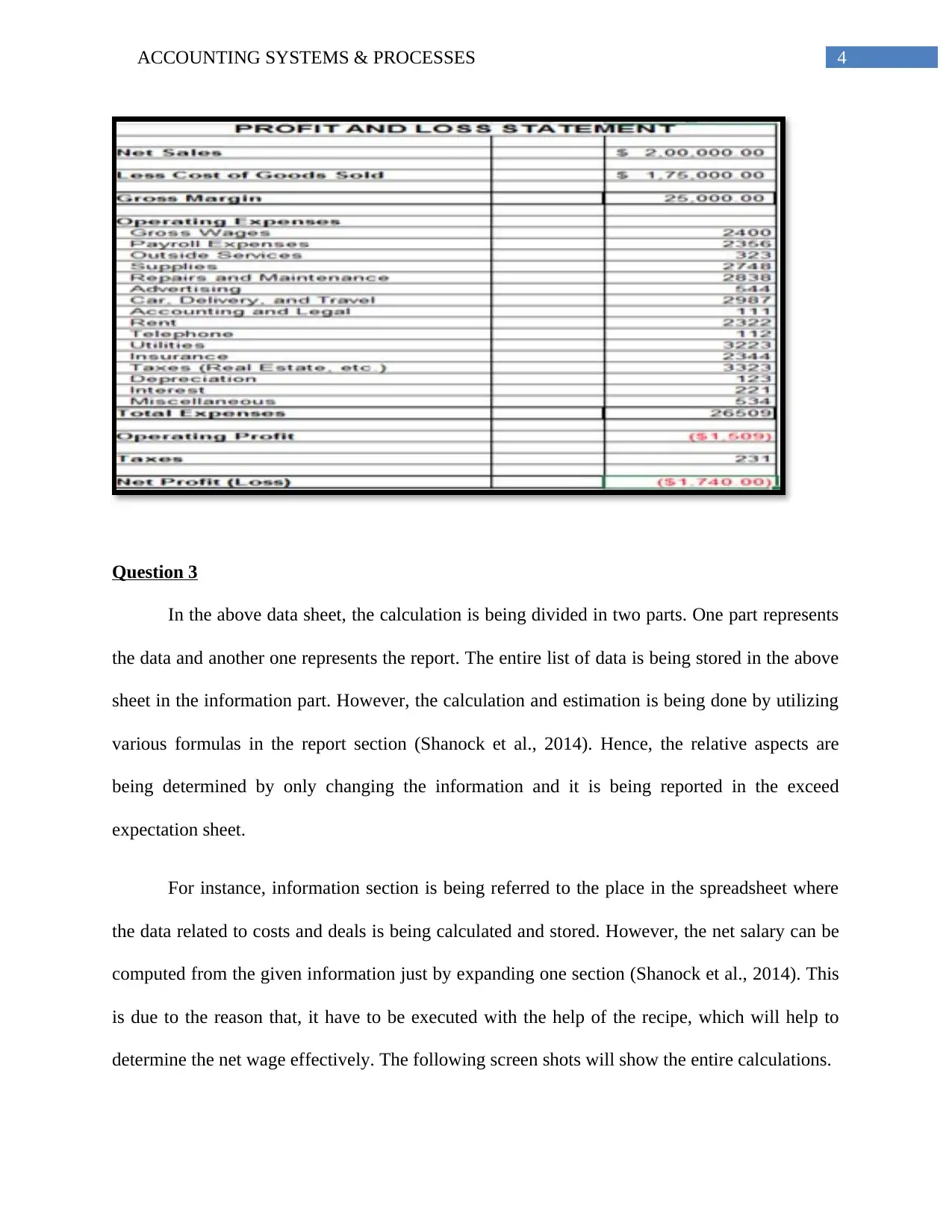

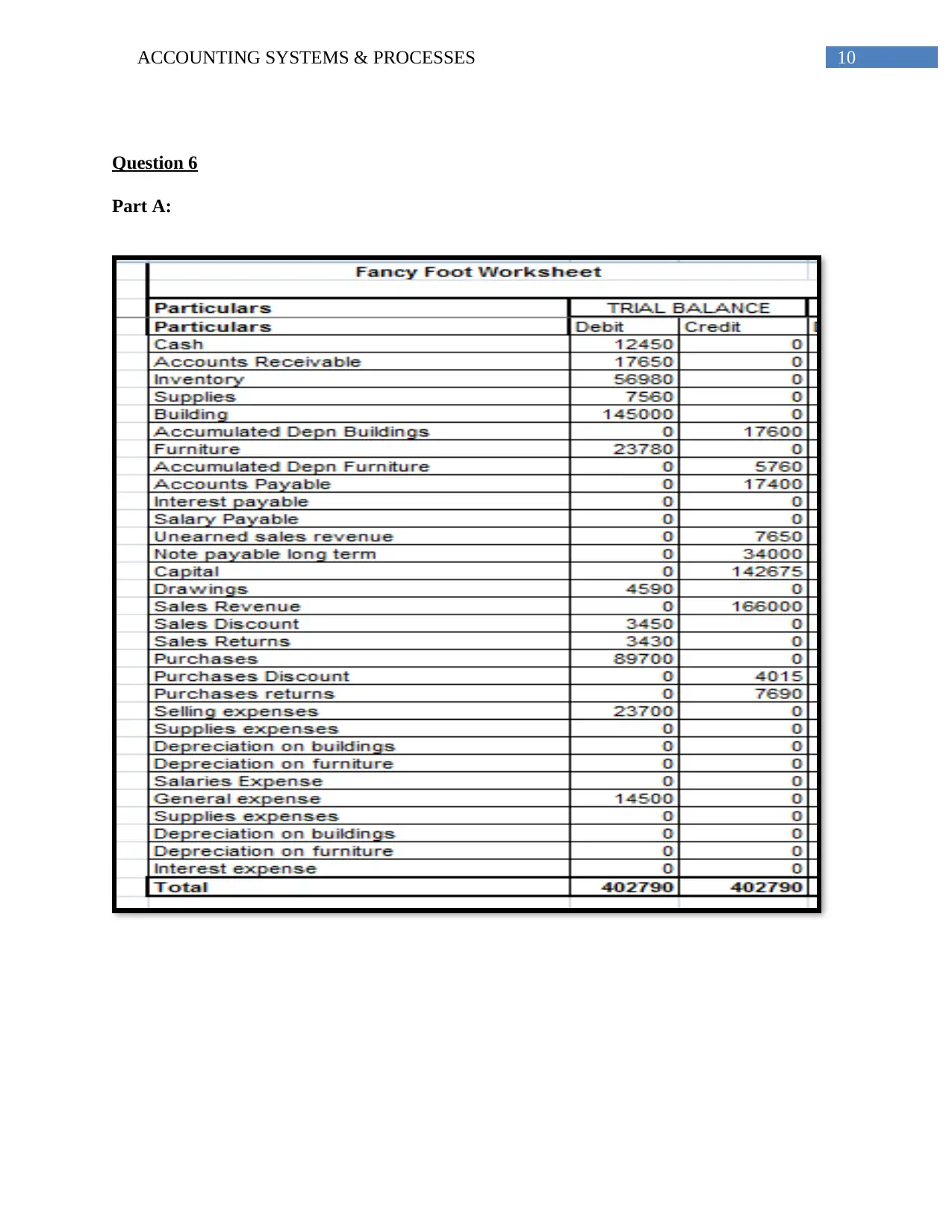

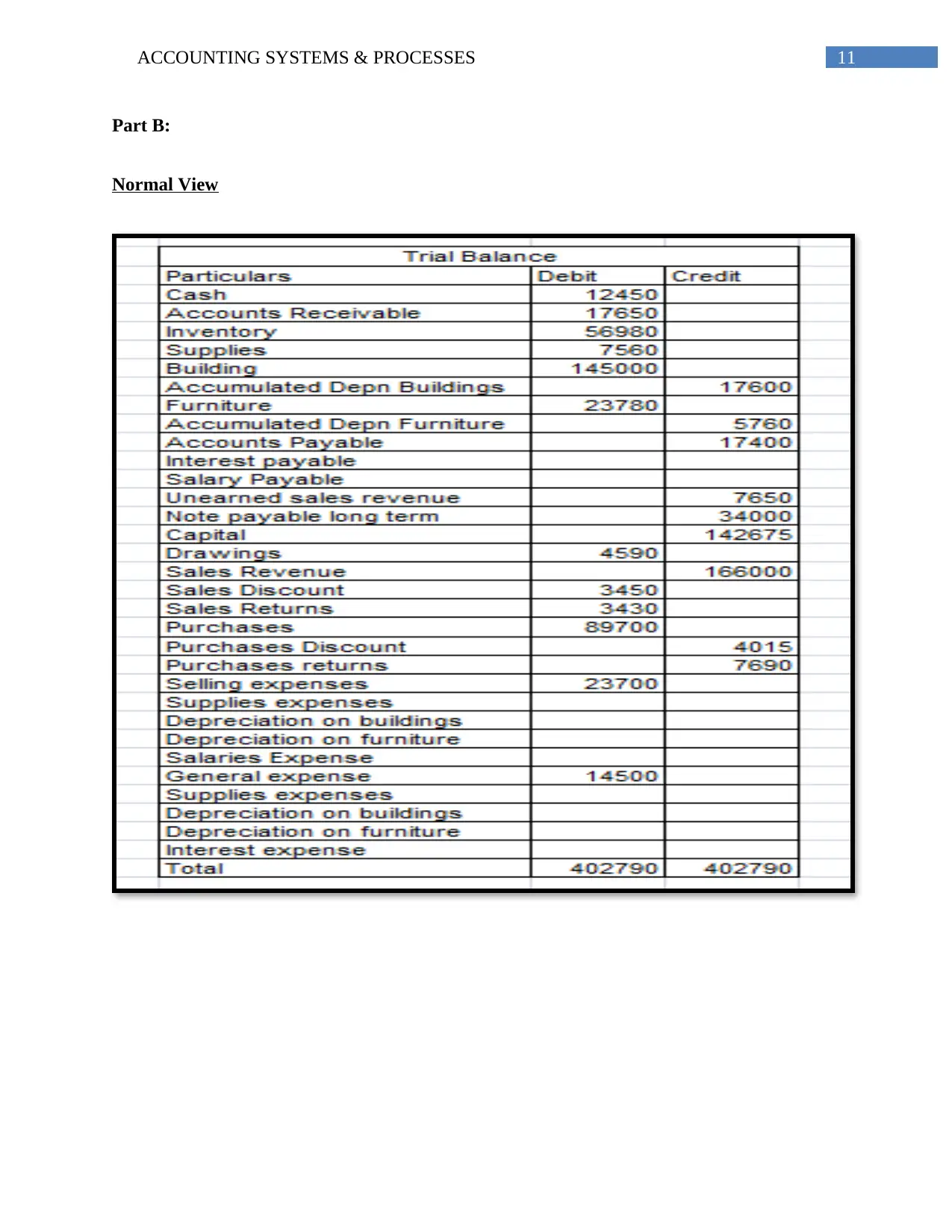

This document provides a comprehensive solution to an accounting systems and processes assignment. It covers various aspects of accounting, including calculating gross margin, analyzing operating profit, and understanding data organization within spreadsheets. The assignment delves into the use of IF functions, periodic inventory systems, and the identification of errors in corporate spreadsheets, along with recommendations for improvement. It includes detailed inventory ledgers using average, FIFO, and LIFO methods, along with calculations for gross profit. Furthermore, the assignment addresses bank reconciliation, journal entries, and the estimation of bad debts using both direct write-off and allowance methods. It also explores the evaluation of a firm's financial position, the handling of dishonored notes receivable, and a case study of Wesfarmers Limited, including financial ratio analysis and insights from its annual report. The solution provides both normal and formula views of data, as well as revised calculations, offering a complete and detailed analysis of the accounting concepts covered.

1 out of 38

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.