Analysis of Management Accounting Systems for R. L. Maynard Limited

VerifiedAdded on 2020/02/12

|25

|7011

|69

Report

AI Summary

This report provides an in-depth analysis of management accounting systems applicable to R. L. Maynard Limited, a property construction and development company. It explores various types of management accounting systems such as cost accounting, inventory management, job costing, and price optimization. The report also delves into specific systems like traditional cost accounting, lean accounting, throughput accounting, and transfer pricing, detailing their applications and benefits. Furthermore, it examines different methods of management accounting reporting, including cost reports, job cost reports, sales reports, and budget reports. The report also touches upon the benefits and limitations of planning tools used for budgetary control and the adaptation of management accounting systems in response to financial problems. The analysis provides a comprehensive overview of how management accounting principles are applied within R. L. Maynard Limited to aid decision-making, performance control, and financial reporting.

Unit 5. Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

P1 Types of Management accounting Systems that are required for R. L. Maynard Limited4

P2 Different methods of management accounting reporting..................................................7

M1...........................................................................................................................................9

TASK 2............................................................................................................................................9

P3 Income statement according to absorption and marginal costing.....................................9

M2.........................................................................................................................................12

TASK 3..........................................................................................................................................13

P4 Benefits and limitation of planning tools used for budgetary control.............................13

Capital Expenditure Budget:...............................................................................................19

M3.........................................................................................................................................19

P5 Adaption of management accounting systems for responding to financial problems.....20

CONCLUSION..............................................................................................................................22

M4.........................................................................................................................................22

REFERENCES..............................................................................................................................23

INTRODUCTION...........................................................................................................................3

P1 Types of Management accounting Systems that are required for R. L. Maynard Limited4

P2 Different methods of management accounting reporting..................................................7

M1...........................................................................................................................................9

TASK 2............................................................................................................................................9

P3 Income statement according to absorption and marginal costing.....................................9

M2.........................................................................................................................................12

TASK 3..........................................................................................................................................13

P4 Benefits and limitation of planning tools used for budgetary control.............................13

Capital Expenditure Budget:...............................................................................................19

M3.........................................................................................................................................19

P5 Adaption of management accounting systems for responding to financial problems.....20

CONCLUSION..............................................................................................................................22

M4.........................................................................................................................................22

REFERENCES..............................................................................................................................23

INTRODUCTION

The procedure of analysing, interpreting and presenting data related to accounting, that is

usually gathered with help of cost and financial accounting, to provide further assistance to

management in field of making decisions, creation of different policies and regular commercial

activity of organization is termed as Management Accounting (Management accounting - What

is management accounting? 2017). It measures the performance, provides assessment of the risks

involved, allocates the resources and gives presentation of different finance related statement to

the managing staff.

It allows to taking of corrective decisions for performance improvement. In the following

assessment R. L. Maynard Limited Company has been taken into consideration. The company

was incorporated on March 22 in year 1973. In Buckinghamshire its registered office is situated.

The organization has been flourishing efficiently for the past 43 years and 11 months. At present,

there are 3 progressive directors and 1 active secretaries as per the modish yearly return proposed

on June 10 in the year 2016. It has been engaged in the construction of property and

development. Emphasis is laid on the provision of employment agency services and on dwellings

which are private. The ultimate purpose of this assessment is to analyse information that how

Management Accounting will be applied to the wider business environment of R. L. Maynard

Limited.

3

The procedure of analysing, interpreting and presenting data related to accounting, that is

usually gathered with help of cost and financial accounting, to provide further assistance to

management in field of making decisions, creation of different policies and regular commercial

activity of organization is termed as Management Accounting (Management accounting - What

is management accounting? 2017). It measures the performance, provides assessment of the risks

involved, allocates the resources and gives presentation of different finance related statement to

the managing staff.

It allows to taking of corrective decisions for performance improvement. In the following

assessment R. L. Maynard Limited Company has been taken into consideration. The company

was incorporated on March 22 in year 1973. In Buckinghamshire its registered office is situated.

The organization has been flourishing efficiently for the past 43 years and 11 months. At present,

there are 3 progressive directors and 1 active secretaries as per the modish yearly return proposed

on June 10 in the year 2016. It has been engaged in the construction of property and

development. Emphasis is laid on the provision of employment agency services and on dwellings

which are private. The ultimate purpose of this assessment is to analyse information that how

Management Accounting will be applied to the wider business environment of R. L. Maynard

Limited.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TASK 1

P1 Types of Management accounting Systems that are required for R. L. Maynard Limited

Management Accounting is the process of evaluating, analysing, measuring, interpreting

and communicating information in order to pursue organisational objectives. The

objectives/benefits of Management Accounting are described below:

Help in planning and establishing future policies: The first objective of

management accounting is to plan in advance to eliminate future obstacles. It

includes forecasting on the basis of present and past conditions and framed future

policies and targets on the basis of it.

Assist in interpreting financial information: It helps management of R. L.

Maynard Limited to interpret financial and technical data in efficient way, so that

it can benefit in decision-making policy of company.

Assist in performance control: Management accounting of organisation aid in

controlling performance of different responsibility centres and departments of R.

L. Maynard Limited.

Management accounting system is the process of gathering financial data from various

departments such as sales, inventory, production, etc. Than converts the information to formulate

reports. There are many type of management accounting systems are available, such as:

1. Cost Accounting System: Used for estimation of cost of products, raw materials,

inventory valuation and cost control.

2. Inventory Management System: Assist in tracking and estimating level of inventory,

orders and sales.

3. Job costing System: This system is used by R.L. enterprise to value the cost of

manufacturing of commodities in accordance to competitors and market demand

4. Price Optimisation: It is analytical and mathematical method that provide idea to

company that how customers will react on different pricing methods.

Management Accounting encapsulates those accounts which serve managerial purpose.

They provide timely piece of data in accordance with financial status of the organization on a

day-to-day basis (Brandau, Endenich and Trapp, 2013). The departmental managers make short

term decisions with the help of these. It is an accumulation management, finance and accounts.

4

P1 Types of Management accounting Systems that are required for R. L. Maynard Limited

Management Accounting is the process of evaluating, analysing, measuring, interpreting

and communicating information in order to pursue organisational objectives. The

objectives/benefits of Management Accounting are described below:

Help in planning and establishing future policies: The first objective of

management accounting is to plan in advance to eliminate future obstacles. It

includes forecasting on the basis of present and past conditions and framed future

policies and targets on the basis of it.

Assist in interpreting financial information: It helps management of R. L.

Maynard Limited to interpret financial and technical data in efficient way, so that

it can benefit in decision-making policy of company.

Assist in performance control: Management accounting of organisation aid in

controlling performance of different responsibility centres and departments of R.

L. Maynard Limited.

Management accounting system is the process of gathering financial data from various

departments such as sales, inventory, production, etc. Than converts the information to formulate

reports. There are many type of management accounting systems are available, such as:

1. Cost Accounting System: Used for estimation of cost of products, raw materials,

inventory valuation and cost control.

2. Inventory Management System: Assist in tracking and estimating level of inventory,

orders and sales.

3. Job costing System: This system is used by R.L. enterprise to value the cost of

manufacturing of commodities in accordance to competitors and market demand

4. Price Optimisation: It is analytical and mathematical method that provide idea to

company that how customers will react on different pricing methods.

Management Accounting encapsulates those accounts which serve managerial purpose.

They provide timely piece of data in accordance with financial status of the organization on a

day-to-day basis (Brandau, Endenich and Trapp, 2013). The departmental managers make short

term decisions with the help of these. It is an accumulation management, finance and accounts.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

All the kind of information that is related to tasks like business strategy, financial accounts, etc.

It provides great boon to the small-scale business.

The company R. L. Maynard Limited is basically a property construction company and

management accounting system is followed in their organization. This has caused efficient and

effective running of the organization. For the sake of company's internal people such as

functional or departmental heads, operational officers and board of directors, management

accounting needs to be done on a daily, weekly or monthly basis.

Management Accounting systems require some necessities that are followed by R. L.

Maynard Limited:

The costings which are related to the production of different types of goods and services

provided by company have been covered in management accounting. The frequently preferred

management accounting systems are mentioned below:

Transfer of Pricing

Throughput Accounting

Traditional cost accounting

Lean accounting

The above-mentioned accounting systems have been further discussed below: Traditional cost Accounting System: The costs of production overheads are allocated to

the products that are generally manufactured by the company in this system. This

traditional method is often referred to as Conventional method. Per current statistics

mostly traditional way of cost accounting is preferred by companies like R. L. Maynard

Limited. The indirect costs of the manufacturing units get distributed over the units of

production. This procedure is carried out based on criteria involving volume or quantity

of the units that are produced, over-head production and direct labour over-head. It

considers Process and Job Order costings (Salehi, Rostami and Mogadam, 2010). Where

costings can be easily identified for individual projects in case of large or big projects,

there the Job order costings finds applications. But allocating the costs individually on

homogeneous products, which undergo through various processes, becomes difficult to

handle. Lean Accounting: It’s a fresh term or one could say that it serving as a revolutionary to

the management accounting system. This is so because management accounting only

5

It provides great boon to the small-scale business.

The company R. L. Maynard Limited is basically a property construction company and

management accounting system is followed in their organization. This has caused efficient and

effective running of the organization. For the sake of company's internal people such as

functional or departmental heads, operational officers and board of directors, management

accounting needs to be done on a daily, weekly or monthly basis.

Management Accounting systems require some necessities that are followed by R. L.

Maynard Limited:

The costings which are related to the production of different types of goods and services

provided by company have been covered in management accounting. The frequently preferred

management accounting systems are mentioned below:

Transfer of Pricing

Throughput Accounting

Traditional cost accounting

Lean accounting

The above-mentioned accounting systems have been further discussed below: Traditional cost Accounting System: The costs of production overheads are allocated to

the products that are generally manufactured by the company in this system. This

traditional method is often referred to as Conventional method. Per current statistics

mostly traditional way of cost accounting is preferred by companies like R. L. Maynard

Limited. The indirect costs of the manufacturing units get distributed over the units of

production. This procedure is carried out based on criteria involving volume or quantity

of the units that are produced, over-head production and direct labour over-head. It

considers Process and Job Order costings (Salehi, Rostami and Mogadam, 2010). Where

costings can be easily identified for individual projects in case of large or big projects,

there the Job order costings finds applications. But allocating the costs individually on

homogeneous products, which undergo through various processes, becomes difficult to

handle. Lean Accounting: It’s a fresh term or one could say that it serving as a revolutionary to

the management accounting system. This is so because management accounting only

5

takes costings into consideration but this brand-new concepts puts focus on cost reduction

methods by excluding the waste material caused in production. Accounts coming under

this category provide data that is related to value streams assessing, profits measurement

and making of decisions to the assigned officers. Excess of any of the costs provided will

be cut down in system based on information provided through above mentioned

categories. Increase in sale revenue by reduction of cost of wastage materials, eliminating

the waste generated availability of plant's capacity, money saving by cost step-down; are

included in the advantages provided by Lean accounting. Throughput Accounting: The volume of the raw material or the product that is passed

through a system or process is usually termed as throughput. In management accounting

system, the throughput accounting cannot be seen as a activity for costing. This happens

because it mainly lays its focus on determining the constraints that arise when units are

being manufactured (Abrahamsson, Englund and Gerdin, 2011). Constraints are not

enough in relation to raw material, turnover of labour, waste of plant's capacity

requirement; and are provided from organization. Therefore, this category of accounting

system eliminates such type of constraints in organization and lead to insisting of more

throughputs for enhancing the quantity and quality of production. This will ensure that

for each of the units produced, the costing will remain low through these ways.

Transfer Pricing: When the commodities are being transferred from one department/ to

another or from holding company to subsidiary one, then transfer pricing is evaluated.

Moving and transferring of products from one place to another generally adds up some

extra costs to it for every single process of transfer. The costs that are being generated in

transfer pricing are generally shifting price and opportunity price. Amount of money that

will be bared by company in the case of outsourcing of goods to firm outside, comes

under the category of opportunity cost (Frezatti, Guerreiro and Gouvea, 2011). While

dependence on production cost is shown by variable cost. This type of management

accounting system provides flexibility to the company and hence this is a benefit

provided through it.

Essential requirements of different types of management accounting systems

It is necessary for RL Maynard to implement management accounting system in its retail

stores in order to establish stability between management and workforce.

6

methods by excluding the waste material caused in production. Accounts coming under

this category provide data that is related to value streams assessing, profits measurement

and making of decisions to the assigned officers. Excess of any of the costs provided will

be cut down in system based on information provided through above mentioned

categories. Increase in sale revenue by reduction of cost of wastage materials, eliminating

the waste generated availability of plant's capacity, money saving by cost step-down; are

included in the advantages provided by Lean accounting. Throughput Accounting: The volume of the raw material or the product that is passed

through a system or process is usually termed as throughput. In management accounting

system, the throughput accounting cannot be seen as a activity for costing. This happens

because it mainly lays its focus on determining the constraints that arise when units are

being manufactured (Abrahamsson, Englund and Gerdin, 2011). Constraints are not

enough in relation to raw material, turnover of labour, waste of plant's capacity

requirement; and are provided from organization. Therefore, this category of accounting

system eliminates such type of constraints in organization and lead to insisting of more

throughputs for enhancing the quantity and quality of production. This will ensure that

for each of the units produced, the costing will remain low through these ways.

Transfer Pricing: When the commodities are being transferred from one department/ to

another or from holding company to subsidiary one, then transfer pricing is evaluated.

Moving and transferring of products from one place to another generally adds up some

extra costs to it for every single process of transfer. The costs that are being generated in

transfer pricing are generally shifting price and opportunity price. Amount of money that

will be bared by company in the case of outsourcing of goods to firm outside, comes

under the category of opportunity cost (Frezatti, Guerreiro and Gouvea, 2011). While

dependence on production cost is shown by variable cost. This type of management

accounting system provides flexibility to the company and hence this is a benefit

provided through it.

Essential requirements of different types of management accounting systems

It is necessary for RL Maynard to implement management accounting system in its retail

stores in order to establish stability between management and workforce.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

It is not bound by accounting standards and therefore helps R.L Maynard in analyzing

past data in accordance to make changes in current business operations to make them

more effective and efficient.

It will help the enterprise in serving best services to its customers.

The system helps the management in gathering specific and appropriate information

regarding plant, product, process and all the organisational departments.

It benefits in making effective planning and decisions regarding business operations.

P2 Different methods of management accounting reporting

Management accounting is termed as the process preparing management and accounts reports

which provides timely and accurate information on financial and statistical matters which are

required by the managers to make decisions on short – term or on day to day basis. There are

various methods used by the cited organisation for management accounting reporting such as

cost accounting, job costs reports, sales report, budget report and payroll report. These are

explained as follows: Cost reports: Cost accounting is determined as a process in which information related to

cost is provided to the management which monitors the future costs. It calculates costs of

items produced by considering costs of raw material, labour, overheads and any other

additional costs. The total amount is divided by number of products produced to get cost

per unit (Merchant, 2012). All this information is summarized in the cost report. It aids in

decision – the internal report system represents the per unit cost of manufactured

products This assists the managers of R.L. Maynard Ltd. to compare the cost prices of

goods with that of the selling price. Moreover, it facilitates them to report on cost of

goods in firm's balance sheet and cost of goods sold in Profit & Loss A/C. Thus, cost

accounting provides, Standard costing, transfer pricing, variance analysis, marginal

costing, activity-based costing, etc. which aids the manager in planning and controlling

profit margins. Job cost reports: It provides an overall statement of the firm's profit and loss in relation

to specific jobs which are assigned to the individuals. Moreover, it makes it easier to get

relevant data in context of job costs that enables greater efficiency for long term period.

In this report, direct costs and overheads related to job are allocated, recorded in the

7

past data in accordance to make changes in current business operations to make them

more effective and efficient.

It will help the enterprise in serving best services to its customers.

The system helps the management in gathering specific and appropriate information

regarding plant, product, process and all the organisational departments.

It benefits in making effective planning and decisions regarding business operations.

P2 Different methods of management accounting reporting

Management accounting is termed as the process preparing management and accounts reports

which provides timely and accurate information on financial and statistical matters which are

required by the managers to make decisions on short – term or on day to day basis. There are

various methods used by the cited organisation for management accounting reporting such as

cost accounting, job costs reports, sales report, budget report and payroll report. These are

explained as follows: Cost reports: Cost accounting is determined as a process in which information related to

cost is provided to the management which monitors the future costs. It calculates costs of

items produced by considering costs of raw material, labour, overheads and any other

additional costs. The total amount is divided by number of products produced to get cost

per unit (Merchant, 2012). All this information is summarized in the cost report. It aids in

decision – the internal report system represents the per unit cost of manufactured

products This assists the managers of R.L. Maynard Ltd. to compare the cost prices of

goods with that of the selling price. Moreover, it facilitates them to report on cost of

goods in firm's balance sheet and cost of goods sold in Profit & Loss A/C. Thus, cost

accounting provides, Standard costing, transfer pricing, variance analysis, marginal

costing, activity-based costing, etc. which aids the manager in planning and controlling

profit margins. Job cost reports: It provides an overall statement of the firm's profit and loss in relation

to specific jobs which are assigned to the individuals. Moreover, it makes it easier to get

relevant data in context of job costs that enables greater efficiency for long term period.

In this report, direct costs and overheads related to job are allocated, recorded in the

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ledger accounts and then they are summarized in trial balance. This helps the

management in preparing batch manufacturing statements. Sales report: It helps in determining the increase or decrease in sales of a company that

enables the managers in identifying areas having market opportunity to increase the sales

volume (Hiebl, 2014). A sales analysis report shows sales for a specific period that may

be on quarterly basis or yearly basis or any other time frame which management

considers significant. Typically, this report may contain data relating to – volume of sales

for per item or group of item, number and place of new and current accounts and costs

incurred in promotion or sale of products. Sales manager of R.L. Maynard Ltd. can

analyse the trends in the report at any time during the fiscal year and determine the best

course of action. This type of management report assists the management to ascertain the

buying behaviour of customers in relation to products or services which enables them to

evaluate the turnover of company as well as discount offers to the clients. Budget report: Preparation of budget is one of the main elements of managerial

accounting. The budget report is an internal part which is used by the management to

make comparison between the actual and estimated performance to ascertain the

company’s achievements over a period. It is prepared by using budgets of previous years

and adjusting them as per the future projections (Jansen, 2011). It helps the management

of cited organisation in comparing the related to the sales data so that various decisions of

the company can be taken. It is essential for the firm to keep a control over its activities

and make decisions regarding financial resources so that it can operate effectively and

smoothly. Along with this, a budget report aids the management to find out deviations

and identify the cause and effect relationship. The cited firm tries to achieve its objectives

while staying within the amounts specified in the budget. Payroll report: This report is prepared in relation to compensation salary of employees

that help management to ascertain financial position of the company. A payroll report

shows reputation of the firm and assists the managers in evaluating of employee's

performance by analysing increment in salary and number of bonus. R.L. Maynard Ltd.

uses software which is updated with the legislative changes and automatically generates

the reports which saves costs of the organisation for a longer period.

8

management in preparing batch manufacturing statements. Sales report: It helps in determining the increase or decrease in sales of a company that

enables the managers in identifying areas having market opportunity to increase the sales

volume (Hiebl, 2014). A sales analysis report shows sales for a specific period that may

be on quarterly basis or yearly basis or any other time frame which management

considers significant. Typically, this report may contain data relating to – volume of sales

for per item or group of item, number and place of new and current accounts and costs

incurred in promotion or sale of products. Sales manager of R.L. Maynard Ltd. can

analyse the trends in the report at any time during the fiscal year and determine the best

course of action. This type of management report assists the management to ascertain the

buying behaviour of customers in relation to products or services which enables them to

evaluate the turnover of company as well as discount offers to the clients. Budget report: Preparation of budget is one of the main elements of managerial

accounting. The budget report is an internal part which is used by the management to

make comparison between the actual and estimated performance to ascertain the

company’s achievements over a period. It is prepared by using budgets of previous years

and adjusting them as per the future projections (Jansen, 2011). It helps the management

of cited organisation in comparing the related to the sales data so that various decisions of

the company can be taken. It is essential for the firm to keep a control over its activities

and make decisions regarding financial resources so that it can operate effectively and

smoothly. Along with this, a budget report aids the management to find out deviations

and identify the cause and effect relationship. The cited firm tries to achieve its objectives

while staying within the amounts specified in the budget. Payroll report: This report is prepared in relation to compensation salary of employees

that help management to ascertain financial position of the company. A payroll report

shows reputation of the firm and assists the managers in evaluating of employee's

performance by analysing increment in salary and number of bonus. R.L. Maynard Ltd.

uses software which is updated with the legislative changes and automatically generates

the reports which saves costs of the organisation for a longer period.

8

Performance report: A performance reports list out differences calculated in the budget

and this information is analysed for developing the new budgets. Generally, these reports

are calculated on a yearly basis but companies may create them quarterly or monthly. It

helps the managers of the cited organisation in planning for future demand in production

and increment in costs.

M1

Benefits of different management accounting systems are given below. Cost accounting: There are number of benefits of cost accounting system and one of

them is that by using cost accounting systems overall costing of product is done in

different manner. Thus, overall reporting quality is better in case of cost accounting. Lean accounting: Main advantage of lean accounting system is that it is less complex

and costly than traditional accounting system. Due to this reason lean accounting is

adopted by most of firms. Throughput accounting: It is another management accounting system and have its own

strong points relative to other accounting systems. Throughput accounting system help

managers in measurement and making business decisions. This accounting system

changes the way in which organization think about determining revenue and costing as

well as profitability of product. Thus, it can be said that throughput accounting give

different and better picture of costing and revenue that is associated with product. Transfer pricing: Transfer pricing reflect pricing of product that happened when it is

transferred from one department to another. Usually, such kind of transfer cost is not

included in cost accounting systems but this accounting system consider it and it is its

major advantage.

TASK 2

P3 Income statement according to absorption and marginal costing

Income statement is a form of financial statement which shows profitability of an organisation at

the end of specific time (Setthasakko, 2010). Such performance is assessed by analysing

revenues generated and expenses incurred because of operating and non-operating activities. In

this context, income statement is prepared and presented below based on marginal and

absorption costing method:

9

and this information is analysed for developing the new budgets. Generally, these reports

are calculated on a yearly basis but companies may create them quarterly or monthly. It

helps the managers of the cited organisation in planning for future demand in production

and increment in costs.

M1

Benefits of different management accounting systems are given below. Cost accounting: There are number of benefits of cost accounting system and one of

them is that by using cost accounting systems overall costing of product is done in

different manner. Thus, overall reporting quality is better in case of cost accounting. Lean accounting: Main advantage of lean accounting system is that it is less complex

and costly than traditional accounting system. Due to this reason lean accounting is

adopted by most of firms. Throughput accounting: It is another management accounting system and have its own

strong points relative to other accounting systems. Throughput accounting system help

managers in measurement and making business decisions. This accounting system

changes the way in which organization think about determining revenue and costing as

well as profitability of product. Thus, it can be said that throughput accounting give

different and better picture of costing and revenue that is associated with product. Transfer pricing: Transfer pricing reflect pricing of product that happened when it is

transferred from one department to another. Usually, such kind of transfer cost is not

included in cost accounting systems but this accounting system consider it and it is its

major advantage.

TASK 2

P3 Income statement according to absorption and marginal costing

Income statement is a form of financial statement which shows profitability of an organisation at

the end of specific time (Setthasakko, 2010). Such performance is assessed by analysing

revenues generated and expenses incurred because of operating and non-operating activities. In

this context, income statement is prepared and presented below based on marginal and

absorption costing method:

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

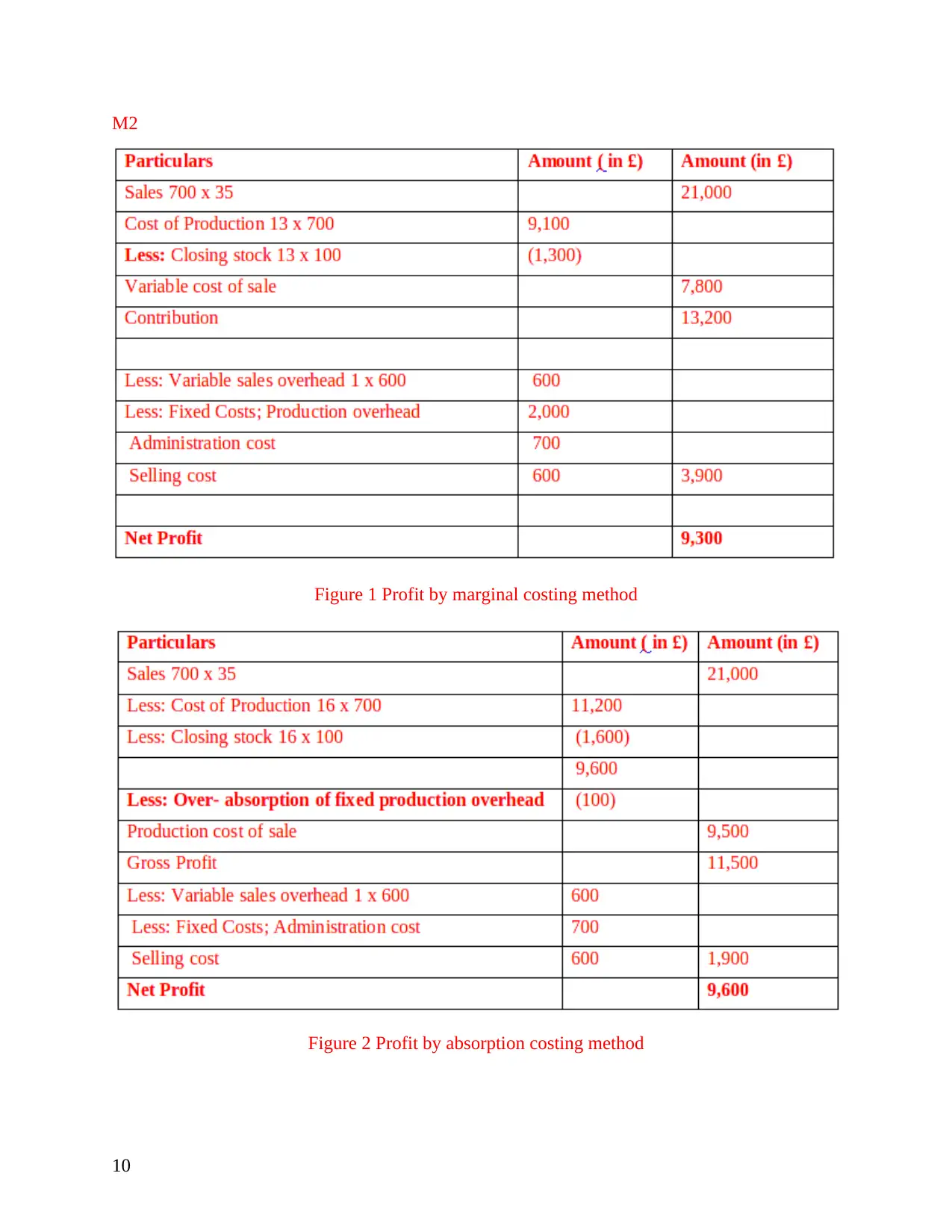

M2

Figure 1 Profit by marginal costing method

Figure 2 Profit by absorption costing method

10

Figure 1 Profit by marginal costing method

Figure 2 Profit by absorption costing method

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

It can be articulated from the above income statements that better net profits are generated by the

company at the month end. The value of net profit calculated under these two methods is

different – net profit as per marginal costing is £12600 which is higher as calculated under

absorption costing i.e. £9300. The main reason of difference in net profit amount is that both

methods take into consideration different types of costs (Sánchez-Rodríguez and Spraakman,

2012). Further, it can be interpreted that as per P&L a/c under marginal costing expenses are

£1800 as it considers only variable costs while under absorption costing it is £5100 as it takes

into account both variable as well as fixed costs.

Most of the companies use absorption costing method as it covers all the expenditures incurred

by the firm as against marginal costing which takes into account only variable expenses. Thus,

an appropriate and clear financial performance in terms of profitability at the end of the period is

provided by absorption costing.

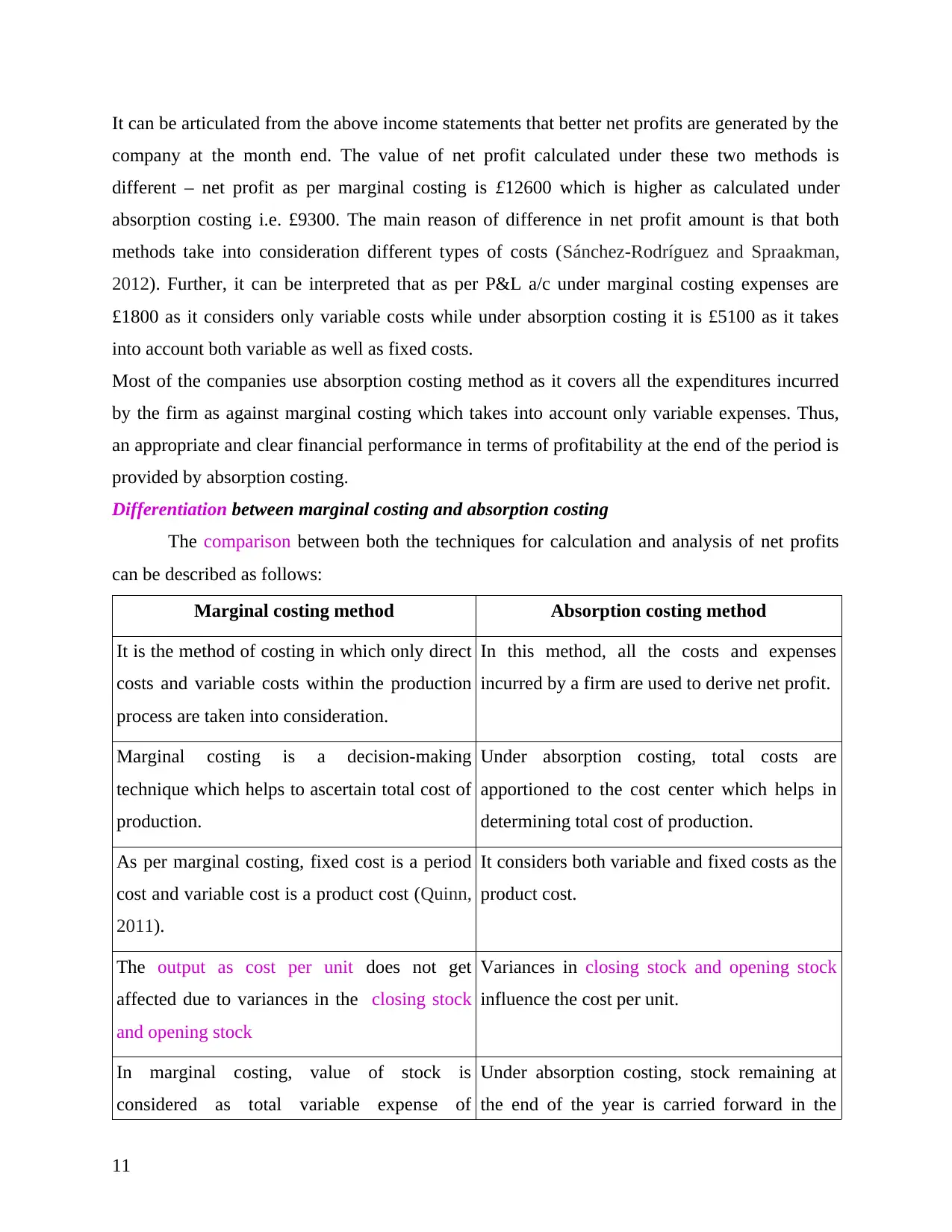

Differentiation between marginal costing and absorption costing

The comparison between both the techniques for calculation and analysis of net profits

can be described as follows:

Marginal costing method Absorption costing method

It is the method of costing in which only direct

costs and variable costs within the production

process are taken into consideration.

In this method, all the costs and expenses

incurred by a firm are used to derive net profit.

Marginal costing is a decision-making

technique which helps to ascertain total cost of

production.

Under absorption costing, total costs are

apportioned to the cost center which helps in

determining total cost of production.

As per marginal costing, fixed cost is a period

cost and variable cost is a product cost (Quinn,

2011).

It considers both variable and fixed costs as the

product cost.

The output as cost per unit does not get

affected due to variances in the closing stock

and opening stock

Variances in closing stock and opening stock

influence the cost per unit.

In marginal costing, value of stock is

considered as total variable expense of

Under absorption costing, stock remaining at

the end of the year is carried forward in the

11

company at the month end. The value of net profit calculated under these two methods is

different – net profit as per marginal costing is £12600 which is higher as calculated under

absorption costing i.e. £9300. The main reason of difference in net profit amount is that both

methods take into consideration different types of costs (Sánchez-Rodríguez and Spraakman,

2012). Further, it can be interpreted that as per P&L a/c under marginal costing expenses are

£1800 as it considers only variable costs while under absorption costing it is £5100 as it takes

into account both variable as well as fixed costs.

Most of the companies use absorption costing method as it covers all the expenditures incurred

by the firm as against marginal costing which takes into account only variable expenses. Thus,

an appropriate and clear financial performance in terms of profitability at the end of the period is

provided by absorption costing.

Differentiation between marginal costing and absorption costing

The comparison between both the techniques for calculation and analysis of net profits

can be described as follows:

Marginal costing method Absorption costing method

It is the method of costing in which only direct

costs and variable costs within the production

process are taken into consideration.

In this method, all the costs and expenses

incurred by a firm are used to derive net profit.

Marginal costing is a decision-making

technique which helps to ascertain total cost of

production.

Under absorption costing, total costs are

apportioned to the cost center which helps in

determining total cost of production.

As per marginal costing, fixed cost is a period

cost and variable cost is a product cost (Quinn,

2011).

It considers both variable and fixed costs as the

product cost.

The output as cost per unit does not get

affected due to variances in the closing stock

and opening stock

Variances in closing stock and opening stock

influence the cost per unit.

In marginal costing, value of stock is

considered as total variable expense of

Under absorption costing, stock remaining at

the end of the year is carried forward in the

11

production cost so; it is not carried forward in

next financial year.

next accounting period because inventory is

valued as total cost of production at the end of

financial year (Meer-Kooistra and Vosselman,

2012).

Overheads are classified on the basis of fixed

and variable cost.

The basis of classification of overheads is

under administration, production, selling and

distribution heads.

The amount of net profit is higher under this

method as compared to other methods.

As all expenses and costs are considered in this

costing method, so net profit is comparatively

low.

When variable expenses are involved , per unit

cost of fixed overhead differs at every level of

production. So marginal cost method serve this

purpose of determining any sort of additional

costs required at every level of production.

On the other hand, the main purpose of

absorption costs is to determine the overall

expenses in accordance with a particular

product or more. It includes the direct as well

as overhead costs.

M2

There are different type of management accounting system some of them are as follows:

Capital budget: This can be determined to be the techniques or the process through which

business plans for their long term investment. R.L. Maynard Ltd. is able plan their future so that

they will be able to make investment for their business. Capital budgets are maintained and

documented by the finance and account manager of the organization efficiently.

Ratio analysis: It is beneficial for R.L. Maynard Ltd. to make evaluation of various

aspects of financial performance and operations. In this context, it includes liquidity, solvency,

etc.

There are financial reporting documents that are helpful for the firm to determine the

business position. In this context it consists of profit and loss account, balance sheet in which

assets and liability are determined.

12

next financial year.

next accounting period because inventory is

valued as total cost of production at the end of

financial year (Meer-Kooistra and Vosselman,

2012).

Overheads are classified on the basis of fixed

and variable cost.

The basis of classification of overheads is

under administration, production, selling and

distribution heads.

The amount of net profit is higher under this

method as compared to other methods.

As all expenses and costs are considered in this

costing method, so net profit is comparatively

low.

When variable expenses are involved , per unit

cost of fixed overhead differs at every level of

production. So marginal cost method serve this

purpose of determining any sort of additional

costs required at every level of production.

On the other hand, the main purpose of

absorption costs is to determine the overall

expenses in accordance with a particular

product or more. It includes the direct as well

as overhead costs.

M2

There are different type of management accounting system some of them are as follows:

Capital budget: This can be determined to be the techniques or the process through which

business plans for their long term investment. R.L. Maynard Ltd. is able plan their future so that

they will be able to make investment for their business. Capital budgets are maintained and

documented by the finance and account manager of the organization efficiently.

Ratio analysis: It is beneficial for R.L. Maynard Ltd. to make evaluation of various

aspects of financial performance and operations. In this context, it includes liquidity, solvency,

etc.

There are financial reporting documents that are helpful for the firm to determine the

business position. In this context it consists of profit and loss account, balance sheet in which

assets and liability are determined.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 25

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.