Detailed Analysis of Accounting Systems and Processes Assignment

VerifiedAdded on 2020/05/28

|19

|2069

|38

Homework Assignment

AI Summary

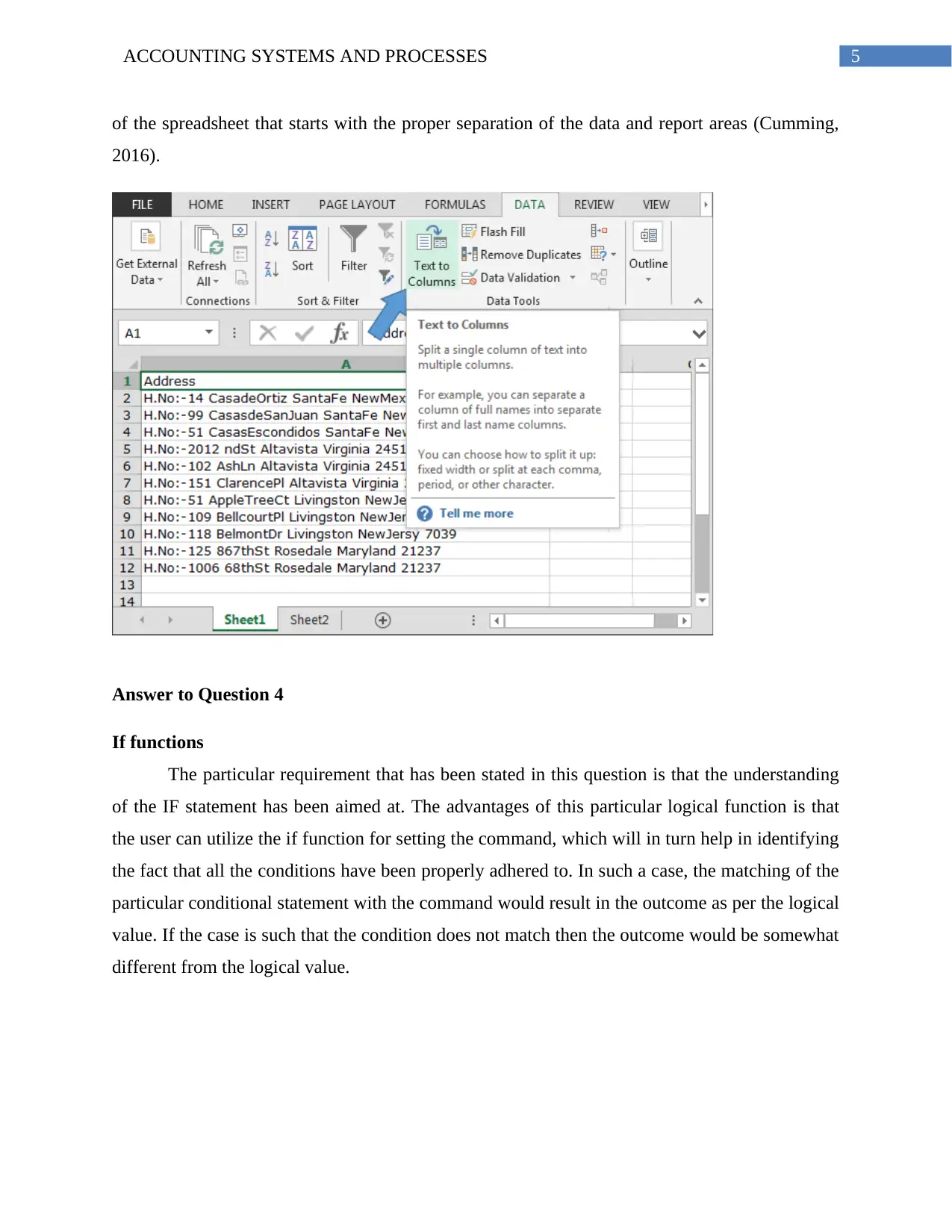

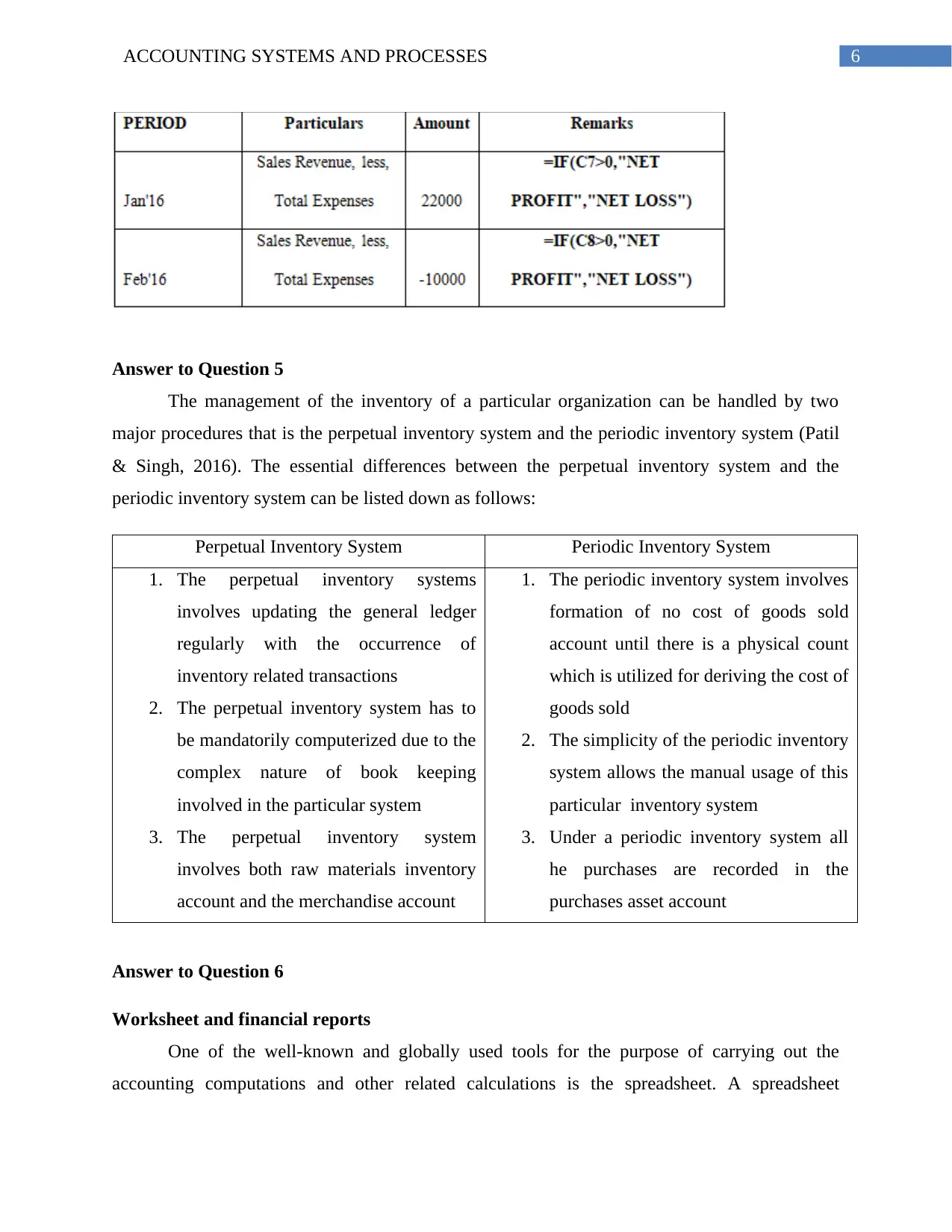

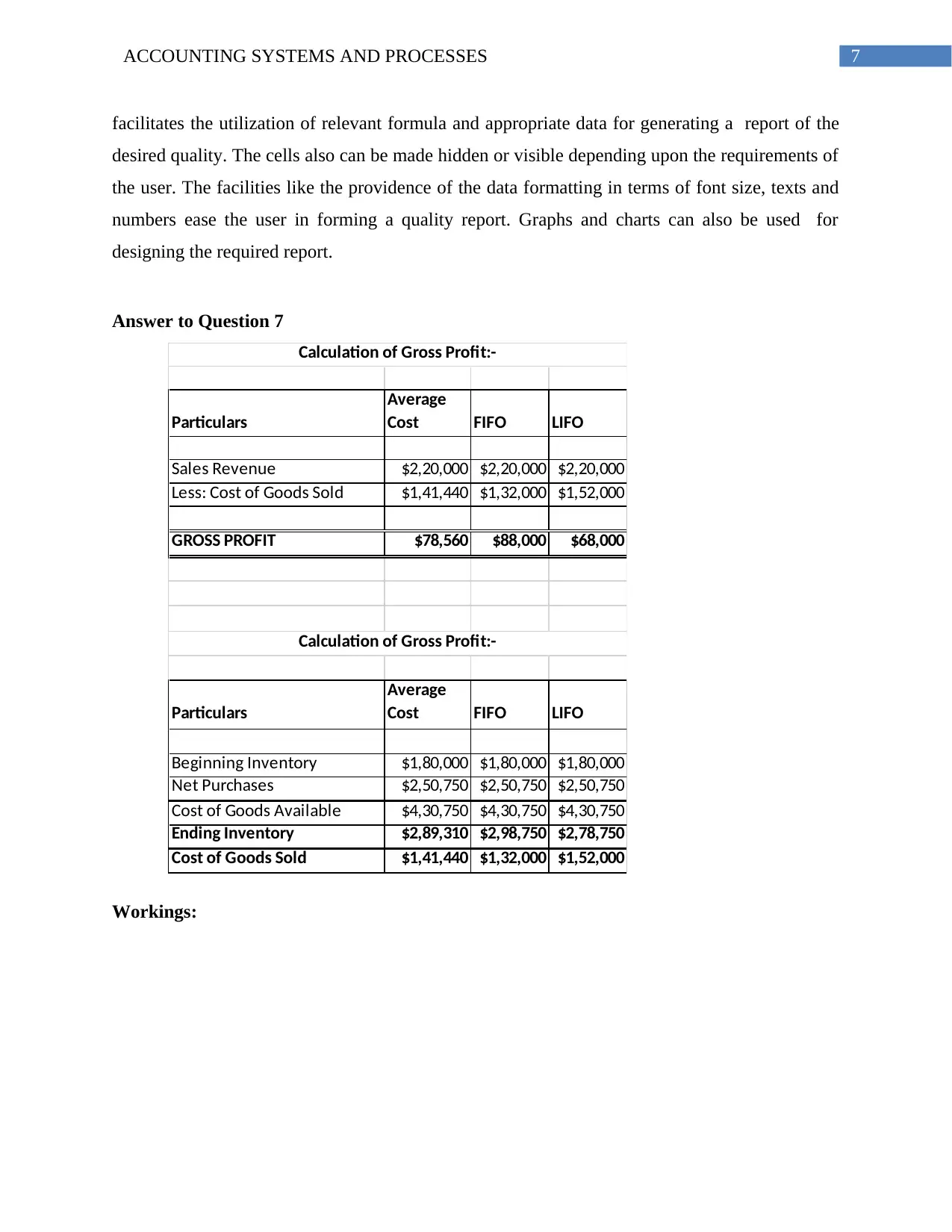

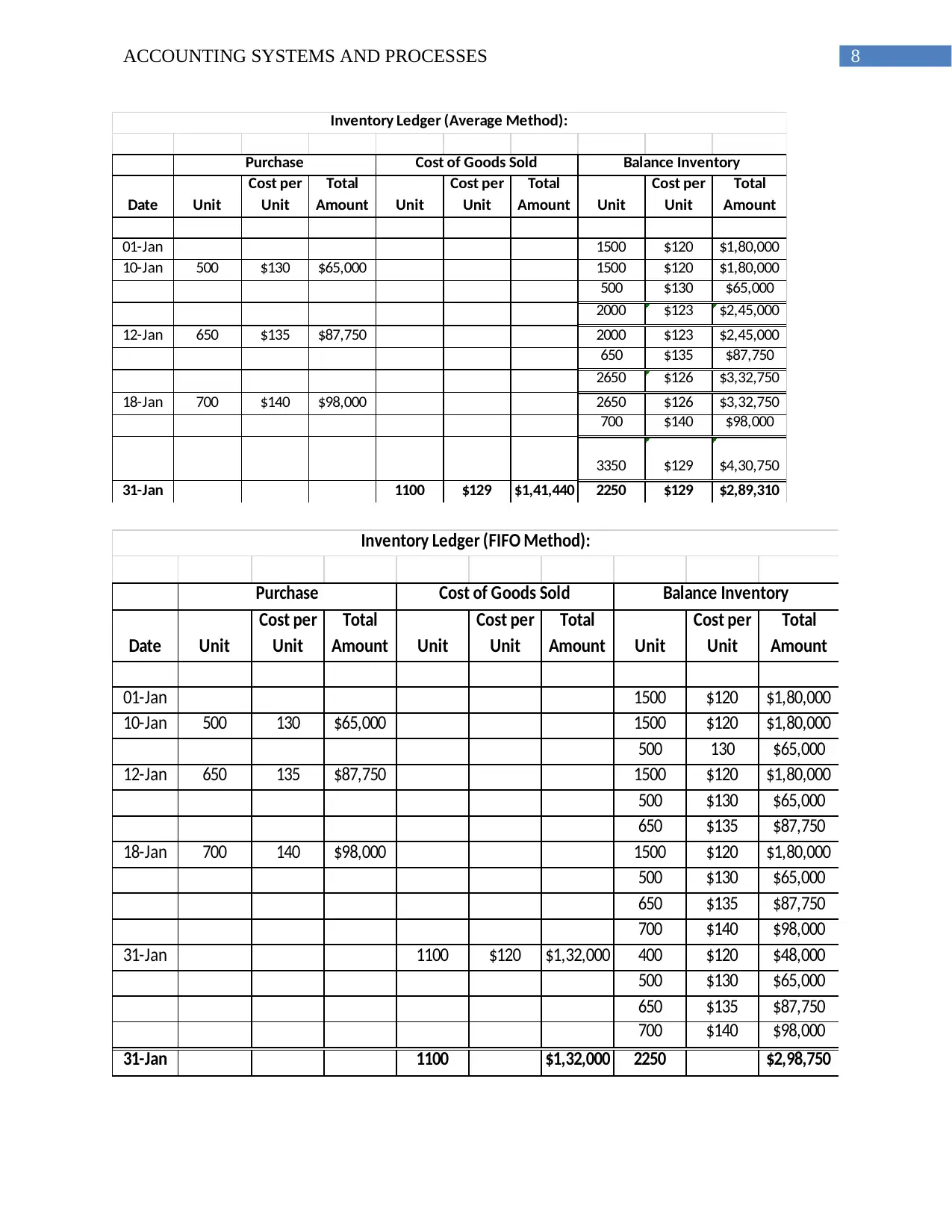

This document presents a comprehensive solution to an accounting systems and processes assignment. It begins by addressing cell naming in spreadsheets, the representation of negative numbers, and the importance of separating data and report areas. The solution then explores the application of IF functions and contrasts perpetual and periodic inventory systems. It further explains the use of spreadsheets for financial reporting and provides detailed workings and revised data for specific questions. The assignment also delves into the impact of computers on online retail, using eBay as an example. A significant portion of the assignment is dedicated to a case study on Qantas Airways, analyzing its financial statements from 2012 to 2017, including key financial ratios such as Return on Investment, Return on Equity, and Net Profit Margin, to assess its suitability for shareholder investment. The document concludes with a recommendation to postpone investment consideration until the company's profit trend stabilizes. The document includes references to academic sources.

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.