Accounting Systems and Processes: July 2019 Transactions

VerifiedAdded on 2022/10/04

|19

|3894

|311

Homework Assignment

AI Summary

This assignment solution covers accounting systems and processes for Pete's Handyman Services. It begins with preparing journal entries for July 2019 transactions, followed by creating T-accounts and an adjusted trial balance. The solution then includes the preparation of an income statement, balance sheet, and statement of owner's equity. Furthermore, the assignment calculates and evaluates the business's current and debt ratios. The solution also delves into the history of accounting and explores ethical principles in the code of ethics, along with measures to be taken in ethical dilemmas. The document provides detailed workings, including adjusting entries, and analyzes the financial performance and position of the business based on the provided transactions.

Running head: ACCOUNTING SYSTEMS AND PROCESSES

Accounting Systems and Processes

Name of the Student:

Name of the University:

Authors Note:

Accounting Systems and Processes

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING SYSTEMS AND PROCESSES

1

Table of Contents

Question 1:.................................................................................................................................2

i) Preparing journal entries for July 2019 transactions:.............................................................2

ii) Preparing the T-account for the transactions:........................................................................4

iii) Preparing the Adjusted Trial Balance:.................................................................................7

iv) Preparing the income statement, Balance sheet and statement of equity changes:..............8

v) Calculating and evaluating the business current ratio and debt ratio:.................................10

Question 2:...............................................................................................................................10

Analysing the history of accounting:.......................................................................................10

Question 3:...............................................................................................................................15

i) Listing and explaining each of the ethical principles in the code of ethics:.........................15

ii) Indicating the measures that need to be taken by the accountant in ethical dilemma:........16

References and Bibliography:..................................................................................................17

1

Table of Contents

Question 1:.................................................................................................................................2

i) Preparing journal entries for July 2019 transactions:.............................................................2

ii) Preparing the T-account for the transactions:........................................................................4

iii) Preparing the Adjusted Trial Balance:.................................................................................7

iv) Preparing the income statement, Balance sheet and statement of equity changes:..............8

v) Calculating and evaluating the business current ratio and debt ratio:.................................10

Question 2:...............................................................................................................................10

Analysing the history of accounting:.......................................................................................10

Question 3:...............................................................................................................................15

i) Listing and explaining each of the ethical principles in the code of ethics:.........................15

ii) Indicating the measures that need to be taken by the accountant in ethical dilemma:........16

References and Bibliography:..................................................................................................17

ACCOUNTING SYSTEMS AND PROCESSES

2

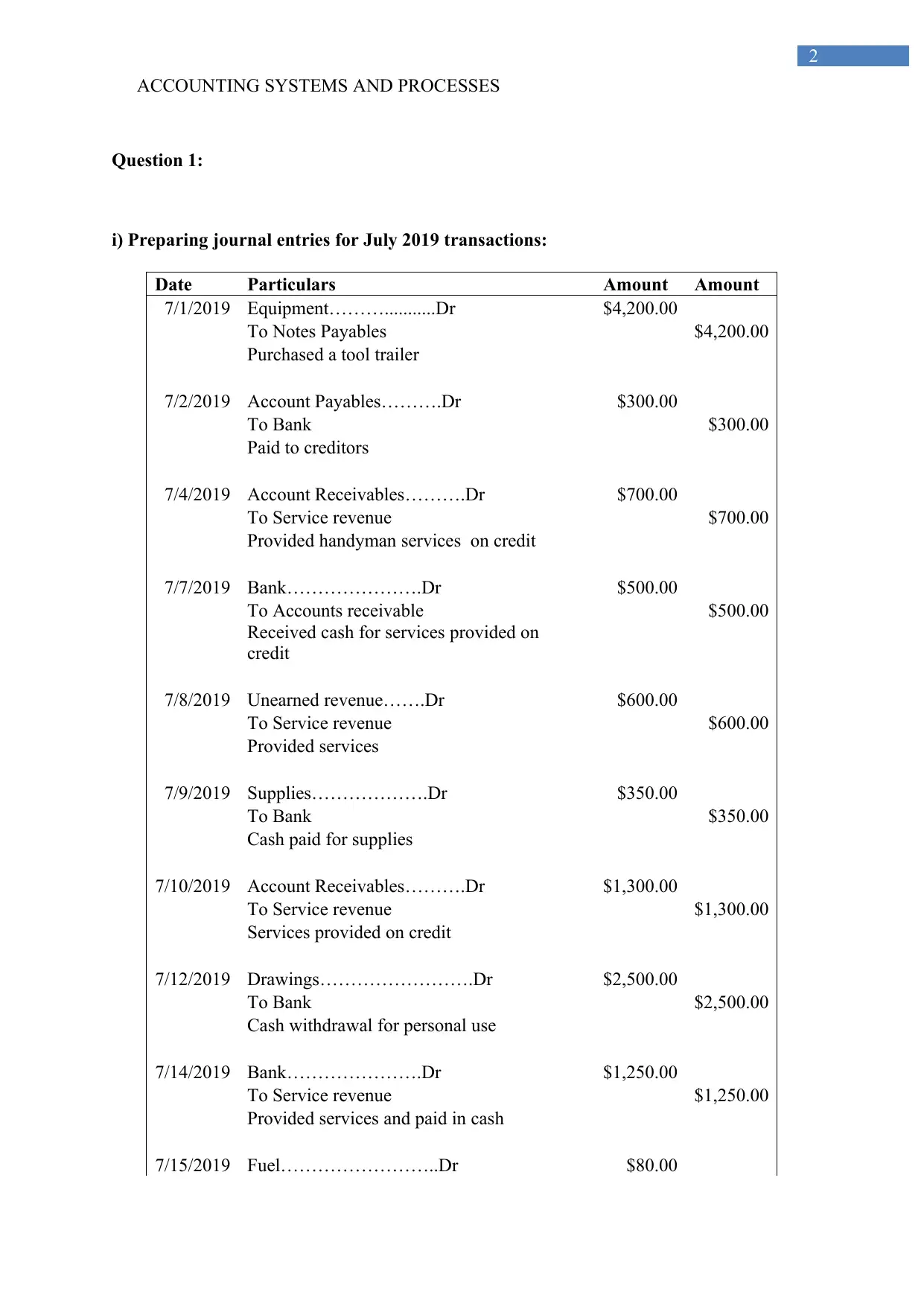

Question 1:

i) Preparing journal entries for July 2019 transactions:

Date Particulars Amount Amount

7/1/2019 Equipment………...........Dr $4,200.00

To Notes Payables $4,200.00

Purchased a tool trailer

7/2/2019 Account Payables……….Dr $300.00

To Bank $300.00

Paid to creditors

7/4/2019 Account Receivables……….Dr $700.00

To Service revenue $700.00

Provided handyman services on credit

7/7/2019 Bank………………….Dr $500.00

To Accounts receivable $500.00

Received cash for services provided on

credit

7/8/2019 Unearned revenue…….Dr $600.00

To Service revenue $600.00

Provided services

7/9/2019 Supplies……………….Dr $350.00

To Bank $350.00

Cash paid for supplies

7/10/2019 Account Receivables……….Dr $1,300.00

To Service revenue $1,300.00

Services provided on credit

7/12/2019 Drawings…………………….Dr $2,500.00

To Bank $2,500.00

Cash withdrawal for personal use

7/14/2019 Bank………………….Dr $1,250.00

To Service revenue $1,250.00

Provided services and paid in cash

7/15/2019 Fuel……………………..Dr $80.00

2

Question 1:

i) Preparing journal entries for July 2019 transactions:

Date Particulars Amount Amount

7/1/2019 Equipment………...........Dr $4,200.00

To Notes Payables $4,200.00

Purchased a tool trailer

7/2/2019 Account Payables……….Dr $300.00

To Bank $300.00

Paid to creditors

7/4/2019 Account Receivables……….Dr $700.00

To Service revenue $700.00

Provided handyman services on credit

7/7/2019 Bank………………….Dr $500.00

To Accounts receivable $500.00

Received cash for services provided on

credit

7/8/2019 Unearned revenue…….Dr $600.00

To Service revenue $600.00

Provided services

7/9/2019 Supplies……………….Dr $350.00

To Bank $350.00

Cash paid for supplies

7/10/2019 Account Receivables……….Dr $1,300.00

To Service revenue $1,300.00

Services provided on credit

7/12/2019 Drawings…………………….Dr $2,500.00

To Bank $2,500.00

Cash withdrawal for personal use

7/14/2019 Bank………………….Dr $1,250.00

To Service revenue $1,250.00

Provided services and paid in cash

7/15/2019 Fuel……………………..Dr $80.00

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ACCOUNTING SYSTEMS AND PROCESSES

3

To Bank $80.00

Paid cash for fuel

7/16/2019 Bank………………….Dr $1,300.00

To Accounts receivable $1,300.00

Received cash for services provided on

credit

7/22/2019 Account Receivables……….Dr $500.00

To Service revenue $500.00

Services provided on credit

7/23/2019 Unearned revenue…….Dr $2,600.00

To Bank $2,600.00

Received cash for services provided on

credit

7/23/2019 Prepaid advertisement………………….Dr $1,200.00

To Bank $1,200.00

Paid in advance for advertisement

7/23/2019 Bank………………….Dr $700.00

To Accounts receivable $700.00

Received cash for services provided on

credit

7/26/2019 Drawings…………………….Dr $2,500.00

To Bank $2,500.00

Cash withdrawal for personal use

7/26/2019 Bank………………….Dr $280.00

To Service revenue $280.00

Received cash for services provided

7/30/2019 Prepaid Insurance………………….Dr $320.00

To Bank $320.00

Paid in advance for Insurance

7/31/2019 Notes Payable…..................Dr $350.00

Interest expense….............Dr $50.00

To Bank $400.00

Payment for loan instalment

7/31/2019 Repairs…............................Dr $320.00

To Accounts payable $320.00

Expenses accrued on repairs

3

To Bank $80.00

Paid cash for fuel

7/16/2019 Bank………………….Dr $1,300.00

To Accounts receivable $1,300.00

Received cash for services provided on

credit

7/22/2019 Account Receivables……….Dr $500.00

To Service revenue $500.00

Services provided on credit

7/23/2019 Unearned revenue…….Dr $2,600.00

To Bank $2,600.00

Received cash for services provided on

credit

7/23/2019 Prepaid advertisement………………….Dr $1,200.00

To Bank $1,200.00

Paid in advance for advertisement

7/23/2019 Bank………………….Dr $700.00

To Accounts receivable $700.00

Received cash for services provided on

credit

7/26/2019 Drawings…………………….Dr $2,500.00

To Bank $2,500.00

Cash withdrawal for personal use

7/26/2019 Bank………………….Dr $280.00

To Service revenue $280.00

Received cash for services provided

7/30/2019 Prepaid Insurance………………….Dr $320.00

To Bank $320.00

Paid in advance for Insurance

7/31/2019 Notes Payable…..................Dr $350.00

Interest expense….............Dr $50.00

To Bank $400.00

Payment for loan instalment

7/31/2019 Repairs…............................Dr $320.00

To Accounts payable $320.00

Expenses accrued on repairs

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING SYSTEMS AND PROCESSES

4

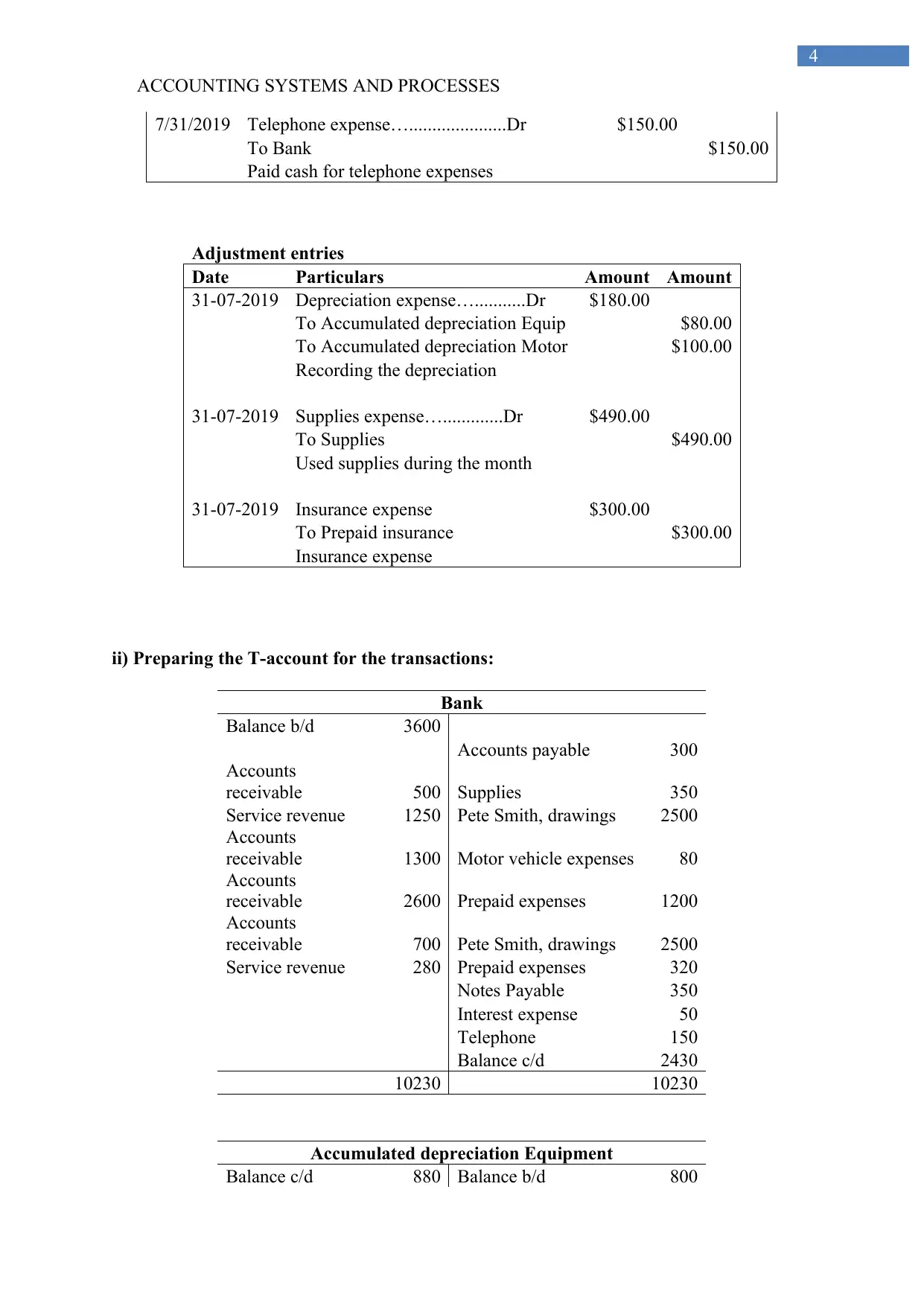

7/31/2019 Telephone expense….....................Dr $150.00

To Bank $150.00

Paid cash for telephone expenses

Adjustment entries

Date Particulars Amount Amount

31-07-2019 Depreciation expense…...........Dr $180.00

To Accumulated depreciation Equip $80.00

To Accumulated depreciation Motor $100.00

Recording the depreciation

31-07-2019 Supplies expense….............Dr $490.00

To Supplies $490.00

Used supplies during the month

31-07-2019 Insurance expense $300.00

To Prepaid insurance $300.00

Insurance expense

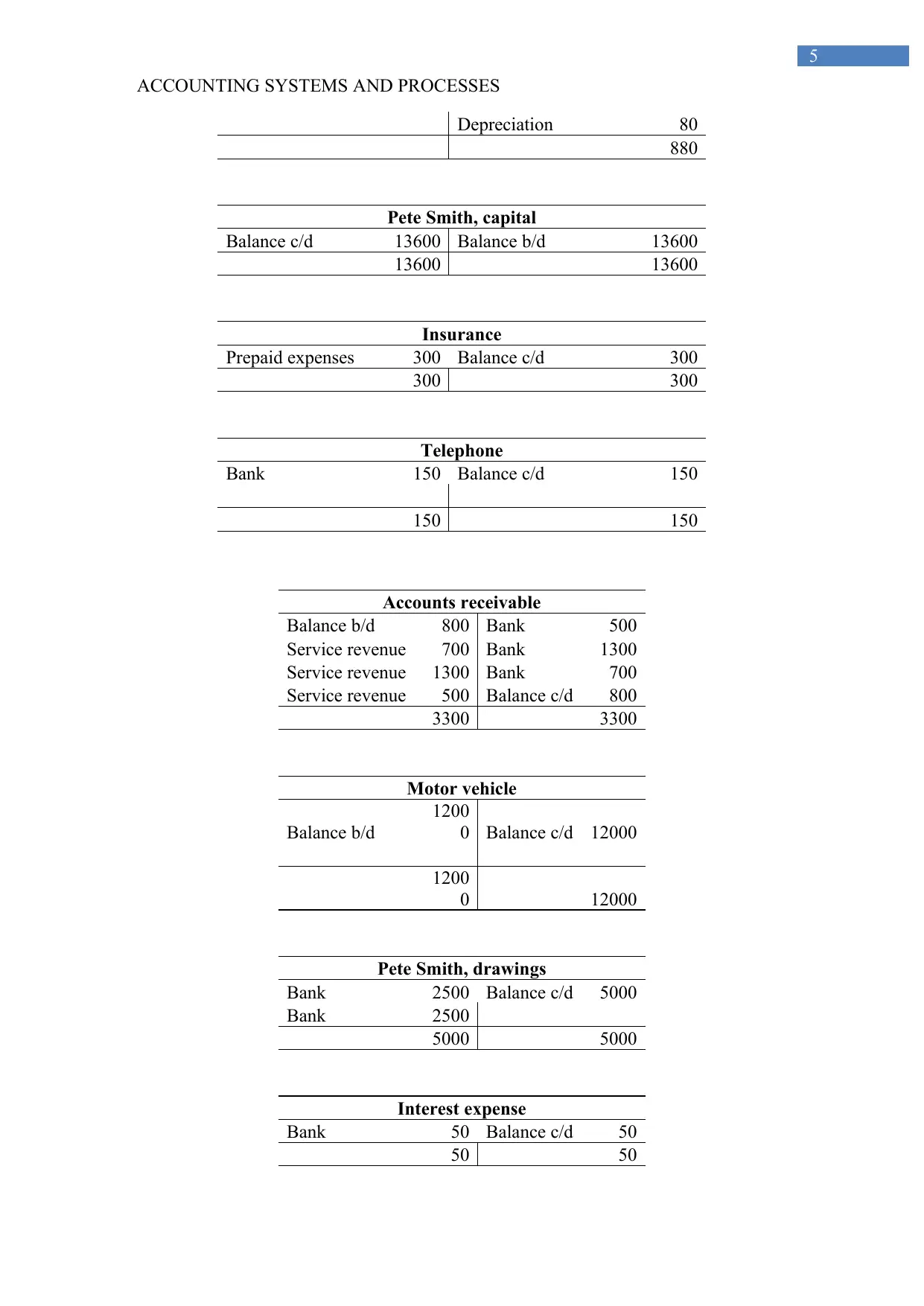

ii) Preparing the T-account for the transactions:

Bank

Balance b/d 3600

Accounts payable 300

Accounts

receivable 500 Supplies 350

Service revenue 1250 Pete Smith, drawings 2500

Accounts

receivable 1300 Motor vehicle expenses 80

Accounts

receivable 2600 Prepaid expenses 1200

Accounts

receivable 700 Pete Smith, drawings 2500

Service revenue 280 Prepaid expenses 320

Notes Payable 350

Interest expense 50

Telephone 150

Balance c/d 2430

10230 10230

Accumulated depreciation Equipment

Balance c/d 880 Balance b/d 800

4

7/31/2019 Telephone expense….....................Dr $150.00

To Bank $150.00

Paid cash for telephone expenses

Adjustment entries

Date Particulars Amount Amount

31-07-2019 Depreciation expense…...........Dr $180.00

To Accumulated depreciation Equip $80.00

To Accumulated depreciation Motor $100.00

Recording the depreciation

31-07-2019 Supplies expense….............Dr $490.00

To Supplies $490.00

Used supplies during the month

31-07-2019 Insurance expense $300.00

To Prepaid insurance $300.00

Insurance expense

ii) Preparing the T-account for the transactions:

Bank

Balance b/d 3600

Accounts payable 300

Accounts

receivable 500 Supplies 350

Service revenue 1250 Pete Smith, drawings 2500

Accounts

receivable 1300 Motor vehicle expenses 80

Accounts

receivable 2600 Prepaid expenses 1200

Accounts

receivable 700 Pete Smith, drawings 2500

Service revenue 280 Prepaid expenses 320

Notes Payable 350

Interest expense 50

Telephone 150

Balance c/d 2430

10230 10230

Accumulated depreciation Equipment

Balance c/d 880 Balance b/d 800

ACCOUNTING SYSTEMS AND PROCESSES

5

Depreciation 80

880

Pete Smith, capital

Balance c/d 13600 Balance b/d 13600

13600 13600

Insurance

Prepaid expenses 300 Balance c/d 300

300 300

Telephone

Bank 150 Balance c/d 150

150 150

Accounts receivable

Balance b/d 800 Bank 500

Service revenue 700 Bank 1300

Service revenue 1300 Bank 700

Service revenue 500 Balance c/d 800

3300 3300

Motor vehicle

Balance b/d

1200

0 Balance c/d 12000

1200

0 12000

Pete Smith, drawings

Bank 2500 Balance c/d 5000

Bank 2500

5000 5000

Interest expense

Bank 50 Balance c/d 50

50 50

5

Depreciation 80

880

Pete Smith, capital

Balance c/d 13600 Balance b/d 13600

13600 13600

Insurance

Prepaid expenses 300 Balance c/d 300

300 300

Telephone

Bank 150 Balance c/d 150

150 150

Accounts receivable

Balance b/d 800 Bank 500

Service revenue 700 Bank 1300

Service revenue 1300 Bank 700

Service revenue 500 Balance c/d 800

3300 3300

Motor vehicle

Balance b/d

1200

0 Balance c/d 12000

1200

0 12000

Pete Smith, drawings

Bank 2500 Balance c/d 5000

Bank 2500

5000 5000

Interest expense

Bank 50 Balance c/d 50

50 50

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ACCOUNTING SYSTEMS AND PROCESSES

6

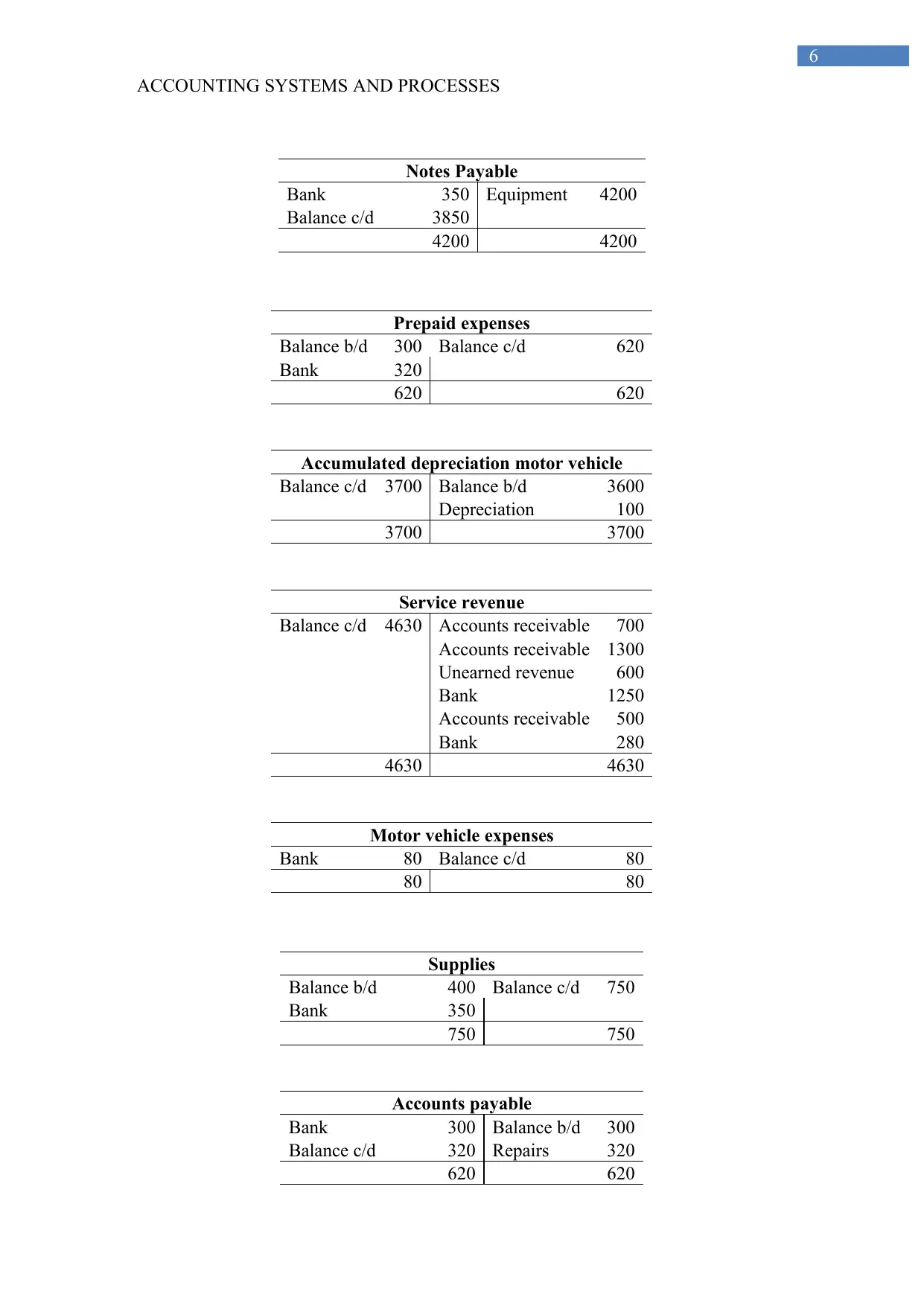

Notes Payable

Bank 350 Equipment 4200

Balance c/d 3850

4200 4200

Prepaid expenses

Balance b/d 300 Balance c/d 620

Bank 320

620 620

Accumulated depreciation motor vehicle

Balance c/d 3700 Balance b/d 3600

Depreciation 100

3700 3700

Service revenue

Balance c/d 4630 Accounts receivable 700

Accounts receivable 1300

Unearned revenue 600

Bank 1250

Accounts receivable 500

Bank 280

4630 4630

Motor vehicle expenses

Bank 80 Balance c/d 80

80 80

Supplies

Balance b/d 400 Balance c/d 750

Bank 350

750 750

Accounts payable

Bank 300 Balance b/d 300

Balance c/d 320 Repairs 320

620 620

6

Notes Payable

Bank 350 Equipment 4200

Balance c/d 3850

4200 4200

Prepaid expenses

Balance b/d 300 Balance c/d 620

Bank 320

620 620

Accumulated depreciation motor vehicle

Balance c/d 3700 Balance b/d 3600

Depreciation 100

3700 3700

Service revenue

Balance c/d 4630 Accounts receivable 700

Accounts receivable 1300

Unearned revenue 600

Bank 1250

Accounts receivable 500

Bank 280

4630 4630

Motor vehicle expenses

Bank 80 Balance c/d 80

80 80

Supplies

Balance b/d 400 Balance c/d 750

Bank 350

750 750

Accounts payable

Bank 300 Balance b/d 300

Balance c/d 320 Repairs 320

620 620

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING SYSTEMS AND PROCESSES

7

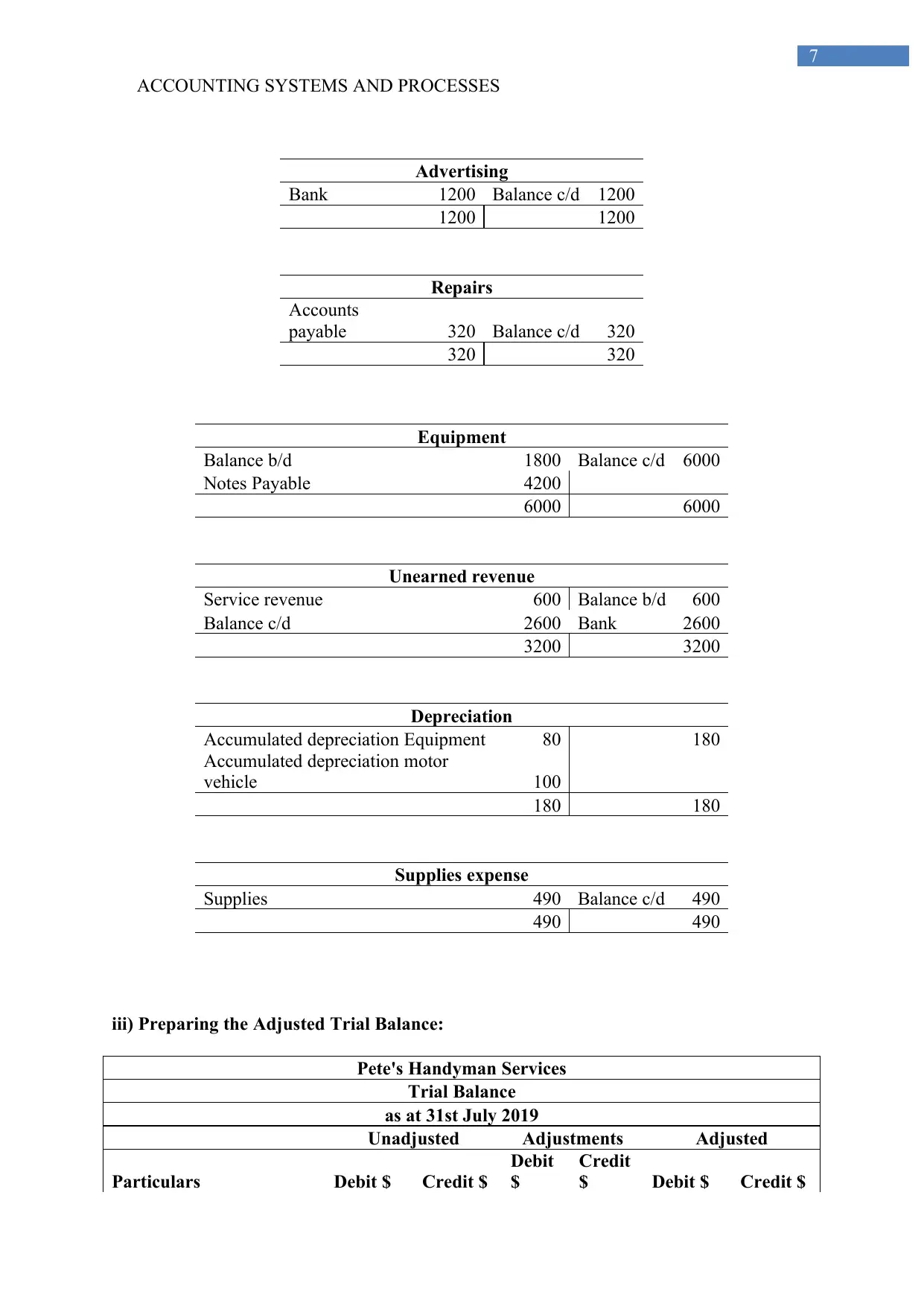

Advertising

Bank 1200 Balance c/d 1200

1200 1200

Repairs

Accounts

payable 320 Balance c/d 320

320 320

Equipment

Balance b/d 1800 Balance c/d 6000

Notes Payable 4200

6000 6000

Unearned revenue

Service revenue 600 Balance b/d 600

Balance c/d 2600 Bank 2600

3200 3200

Depreciation

Accumulated depreciation Equipment 80 180

Accumulated depreciation motor

vehicle 100

180 180

Supplies expense

Supplies 490 Balance c/d 490

490 490

iii) Preparing the Adjusted Trial Balance:

Pete's Handyman Services

Trial Balance

as at 31st July 2019

Unadjusted Adjustments Adjusted

Particulars Debit $ Credit $

Debit

$

Credit

$ Debit $ Credit $

7

Advertising

Bank 1200 Balance c/d 1200

1200 1200

Repairs

Accounts

payable 320 Balance c/d 320

320 320

Equipment

Balance b/d 1800 Balance c/d 6000

Notes Payable 4200

6000 6000

Unearned revenue

Service revenue 600 Balance b/d 600

Balance c/d 2600 Bank 2600

3200 3200

Depreciation

Accumulated depreciation Equipment 80 180

Accumulated depreciation motor

vehicle 100

180 180

Supplies expense

Supplies 490 Balance c/d 490

490 490

iii) Preparing the Adjusted Trial Balance:

Pete's Handyman Services

Trial Balance

as at 31st July 2019

Unadjusted Adjustments Adjusted

Particulars Debit $ Credit $

Debit

$

Credit

$ Debit $ Credit $

ACCOUNTING SYSTEMS AND PROCESSES

8

Bank

$2,430.0

0

$2,430.0

0

Accounts receivable $800.00 $800.00

Prepaid expenses $620.00

$300.0

0 $320.00

Supplies $750.00

$490.0

0 $260.00

Equipment

$6,000.0

0

$6,000.0

0

Less: Accumulated

depreciation $800.00 $80.00 $880.00

Motor vehicle

$12,000.

00

$12,000.

00

Less: Accumulated

depreciation

$3,600.0

0

$100.0

0

$3,700.0

0

Accounts payable $320.00 $320.00

Unearned revenue

$2,600.0

0

$2,600.0

0

Notes Payable

$3,850.0

0

$3,850.0

0

Pete Smith, capital

$13,600.

00

$13,600.

00

Pete Smith, drawings

$5,000.0

0

$5,000.0

0

Service revenue

$4,630.0

0

$4,630.0

0

Advertising

$1,200.0

0

$1,200.0

0

Depreciation

$180.0

0 $180.00

Insurance

$300.0

0 $300.00

Interest expense $50.00 $50.00

Motor vehicle expenses $80.00 $80.00

Repairs $320.00 $320.00

Supplies expense

$490.0

0 $490.00

Telephone $150.00 $150.00

Total

$29,400.

00

$29,400.

00

$970.0

0

$970.0

0

$29,580.

00

$29,580.

00

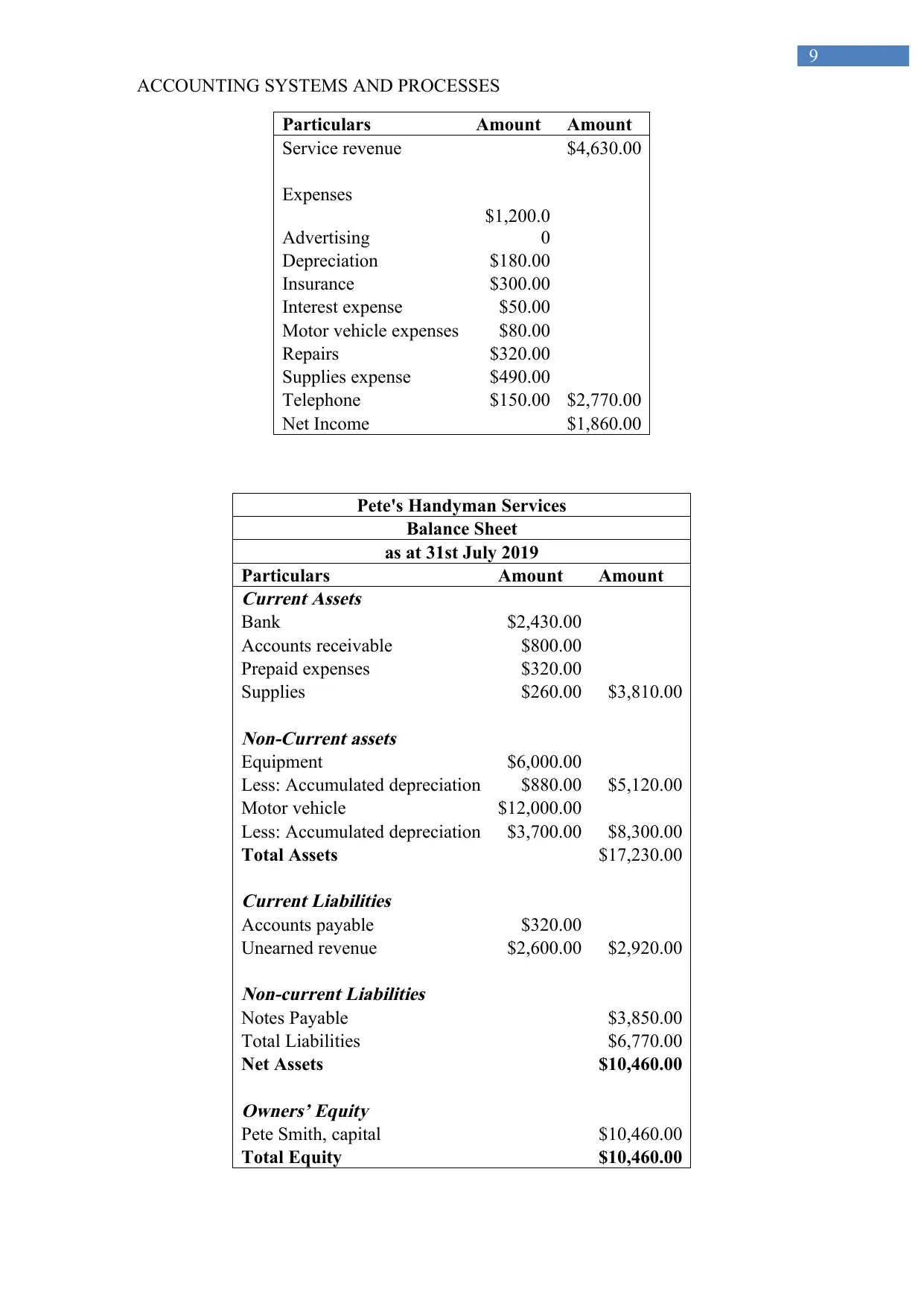

iv) Preparing the income statement, Balance sheet and statement of equity changes:

Pete's Handyman Services

Statement of Income

as at 31st July 2019

8

Bank

$2,430.0

0

$2,430.0

0

Accounts receivable $800.00 $800.00

Prepaid expenses $620.00

$300.0

0 $320.00

Supplies $750.00

$490.0

0 $260.00

Equipment

$6,000.0

0

$6,000.0

0

Less: Accumulated

depreciation $800.00 $80.00 $880.00

Motor vehicle

$12,000.

00

$12,000.

00

Less: Accumulated

depreciation

$3,600.0

0

$100.0

0

$3,700.0

0

Accounts payable $320.00 $320.00

Unearned revenue

$2,600.0

0

$2,600.0

0

Notes Payable

$3,850.0

0

$3,850.0

0

Pete Smith, capital

$13,600.

00

$13,600.

00

Pete Smith, drawings

$5,000.0

0

$5,000.0

0

Service revenue

$4,630.0

0

$4,630.0

0

Advertising

$1,200.0

0

$1,200.0

0

Depreciation

$180.0

0 $180.00

Insurance

$300.0

0 $300.00

Interest expense $50.00 $50.00

Motor vehicle expenses $80.00 $80.00

Repairs $320.00 $320.00

Supplies expense

$490.0

0 $490.00

Telephone $150.00 $150.00

Total

$29,400.

00

$29,400.

00

$970.0

0

$970.0

0

$29,580.

00

$29,580.

00

iv) Preparing the income statement, Balance sheet and statement of equity changes:

Pete's Handyman Services

Statement of Income

as at 31st July 2019

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ACCOUNTING SYSTEMS AND PROCESSES

9

Particulars Amount Amount

Service revenue $4,630.00

Expenses

Advertising

$1,200.0

0

Depreciation $180.00

Insurance $300.00

Interest expense $50.00

Motor vehicle expenses $80.00

Repairs $320.00

Supplies expense $490.00

Telephone $150.00 $2,770.00

Net Income $1,860.00

Pete's Handyman Services

Balance Sheet

as at 31st July 2019

Particulars Amount Amount

Current Assets

Bank $2,430.00

Accounts receivable $800.00

Prepaid expenses $320.00

Supplies $260.00 $3,810.00

Non-Current assets

Equipment $6,000.00

Less: Accumulated depreciation $880.00 $5,120.00

Motor vehicle $12,000.00

Less: Accumulated depreciation $3,700.00 $8,300.00

Total Assets $17,230.00

Current Liabilities

Accounts payable $320.00

Unearned revenue $2,600.00 $2,920.00

Non-current Liabilities

Notes Payable $3,850.00

Total Liabilities $6,770.00

Net Assets $10,460.00

Owners’ Equity

Pete Smith, capital $10,460.00

Total Equity $10,460.00

9

Particulars Amount Amount

Service revenue $4,630.00

Expenses

Advertising

$1,200.0

0

Depreciation $180.00

Insurance $300.00

Interest expense $50.00

Motor vehicle expenses $80.00

Repairs $320.00

Supplies expense $490.00

Telephone $150.00 $2,770.00

Net Income $1,860.00

Pete's Handyman Services

Balance Sheet

as at 31st July 2019

Particulars Amount Amount

Current Assets

Bank $2,430.00

Accounts receivable $800.00

Prepaid expenses $320.00

Supplies $260.00 $3,810.00

Non-Current assets

Equipment $6,000.00

Less: Accumulated depreciation $880.00 $5,120.00

Motor vehicle $12,000.00

Less: Accumulated depreciation $3,700.00 $8,300.00

Total Assets $17,230.00

Current Liabilities

Accounts payable $320.00

Unearned revenue $2,600.00 $2,920.00

Non-current Liabilities

Notes Payable $3,850.00

Total Liabilities $6,770.00

Net Assets $10,460.00

Owners’ Equity

Pete Smith, capital $10,460.00

Total Equity $10,460.00

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING SYSTEMS AND PROCESSES

10

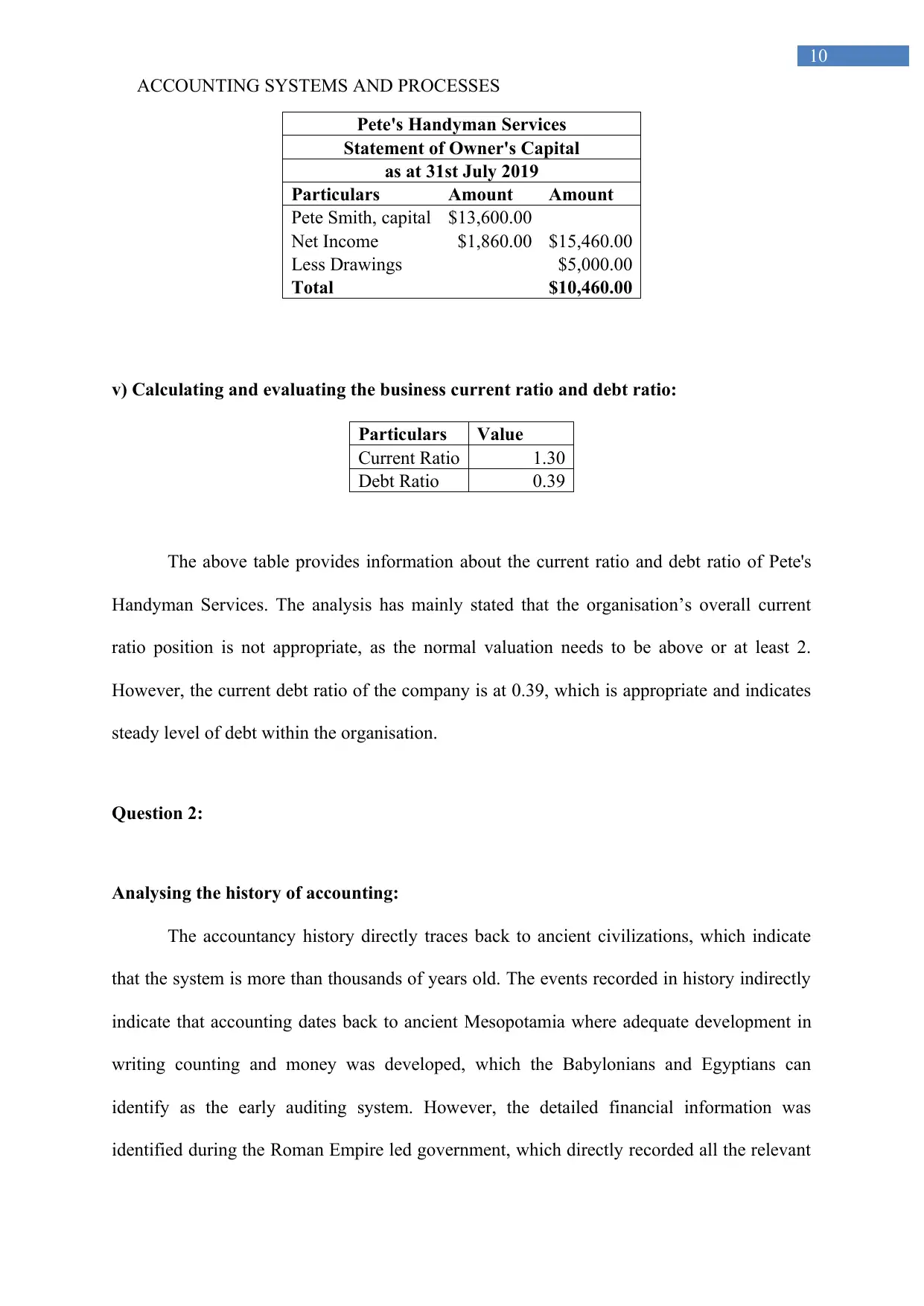

Pete's Handyman Services

Statement of Owner's Capital

as at 31st July 2019

Particulars Amount Amount

Pete Smith, capital $13,600.00

Net Income $1,860.00 $15,460.00

Less Drawings $5,000.00

Total $10,460.00

v) Calculating and evaluating the business current ratio and debt ratio:

Particulars Value

Current Ratio 1.30

Debt Ratio 0.39

The above table provides information about the current ratio and debt ratio of Pete's

Handyman Services. The analysis has mainly stated that the organisation’s overall current

ratio position is not appropriate, as the normal valuation needs to be above or at least 2.

However, the current debt ratio of the company is at 0.39, which is appropriate and indicates

steady level of debt within the organisation.

Question 2:

Analysing the history of accounting:

The accountancy history directly traces back to ancient civilizations, which indicate

that the system is more than thousands of years old. The events recorded in history indirectly

indicate that accounting dates back to ancient Mesopotamia where adequate development in

writing counting and money was developed, which the Babylonians and Egyptians can

identify as the early auditing system. However, the detailed financial information was

identified during the Roman Empire led government, which directly recorded all the relevant

10

Pete's Handyman Services

Statement of Owner's Capital

as at 31st July 2019

Particulars Amount Amount

Pete Smith, capital $13,600.00

Net Income $1,860.00 $15,460.00

Less Drawings $5,000.00

Total $10,460.00

v) Calculating and evaluating the business current ratio and debt ratio:

Particulars Value

Current Ratio 1.30

Debt Ratio 0.39

The above table provides information about the current ratio and debt ratio of Pete's

Handyman Services. The analysis has mainly stated that the organisation’s overall current

ratio position is not appropriate, as the normal valuation needs to be above or at least 2.

However, the current debt ratio of the company is at 0.39, which is appropriate and indicates

steady level of debt within the organisation.

Question 2:

Analysing the history of accounting:

The accountancy history directly traces back to ancient civilizations, which indicate

that the system is more than thousands of years old. The events recorded in history indirectly

indicate that accounting dates back to ancient Mesopotamia where adequate development in

writing counting and money was developed, which the Babylonians and Egyptians can

identify as the early auditing system. However, the detailed financial information was

identified during the Roman Empire led government, which directly recorded all the relevant

ACCOUNTING SYSTEMS AND PROCESSES

11

events and financial transactions to depict the financial conditions of a town. The manuscripts

that was similar to the financial management book was written by Chanakya during the

Mauryan empire where the book name Arthashasthra containing the detailed aspects of

maintaining the financial books of accounts for a Sovereign state. The detailed information

that was provided in the book during the Mauryan Empire directly related the progress that

has been made throughout history in accounting. Therefore, it has been detected that the

maintenance of financial accounts or accountancy has been present in human history for a

longer duration where it allowed Sovereign Nations to detect the level of their financial

capability and treasury amount. Thus, detailed financial accounting was an essential part of

maintaining and creating an empire since ancient times (Brown, 2014).

The progress of accounting is directly e sub divided in four different aspects, which

contains Ancient History, Roman Empire, Mediaeval or Renaissance period, and Modern

Professional Accounting. The different segments of the accounting history directly indicate

about the progress and the improvements that were conducted in the field of accountancy to

improve the financial management and accounting conditions of both servant missions and

companies in later years. There were adequate early developments of accounting and

expansion of the role of an accountant, which was laid during the ancient times. The timeline

or the time period of the accounting development are depicted as follows.

Ancient History: One of the accounting records that is dated back for more than 7000 years

ago was found in Mesopotamia where are all the relevant documents from the ancient

civilization directly identifies the list of expenditures and goods received during trade. The

development of accounting directly indicates about the add element money and numbers that

work directly indicating the trading activities that were conducted in the civilization during

the era (D. Carnegie, 2014). The development of accounting is closely related to the

improvements that were conducted with money, writing and counting that have been

11

events and financial transactions to depict the financial conditions of a town. The manuscripts

that was similar to the financial management book was written by Chanakya during the

Mauryan empire where the book name Arthashasthra containing the detailed aspects of

maintaining the financial books of accounts for a Sovereign state. The detailed information

that was provided in the book during the Mauryan Empire directly related the progress that

has been made throughout history in accounting. Therefore, it has been detected that the

maintenance of financial accounts or accountancy has been present in human history for a

longer duration where it allowed Sovereign Nations to detect the level of their financial

capability and treasury amount. Thus, detailed financial accounting was an essential part of

maintaining and creating an empire since ancient times (Brown, 2014).

The progress of accounting is directly e sub divided in four different aspects, which

contains Ancient History, Roman Empire, Mediaeval or Renaissance period, and Modern

Professional Accounting. The different segments of the accounting history directly indicate

about the progress and the improvements that were conducted in the field of accountancy to

improve the financial management and accounting conditions of both servant missions and

companies in later years. There were adequate early developments of accounting and

expansion of the role of an accountant, which was laid during the ancient times. The timeline

or the time period of the accounting development are depicted as follows.

Ancient History: One of the accounting records that is dated back for more than 7000 years

ago was found in Mesopotamia where are all the relevant documents from the ancient

civilization directly identifies the list of expenditures and goods received during trade. The

development of accounting directly indicates about the add element money and numbers that

work directly indicating the trading activities that were conducted in the civilization during

the era (D. Carnegie, 2014). The development of accounting is closely related to the

improvements that were conducted with money, writing and counting that have been

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.