Accounting Systems and Processes Assignment - Course Code, University

VerifiedAdded on 2020/03/04

|30

|3726

|85

Homework Assignment

AI Summary

This accounting assignment solution addresses various aspects of accounting systems and processes. It begins by defining plagiarism and its impact. The solution then details methods for integrating Excel spreadsheets into Word documents, including both normal and formula views. It lists relevant accounting websites like AASB, IFRS, and ATO. The assignment also covers professional accounting organizations, work-integrated assessment experiences, and a case study on ABC Learning, highlighting ethical issues and financial statement analysis. The solution further provides a breakdown of account types, prepares an income statement and balance sheet, and demonstrates the balance sheet equation with different cases. The document also contains excel formulas for the balance sheet equation.

Running head: ACCOUNTS SYSTEMS & PROCESS

Accounting System & Process

Name of the Student:-

Name of the University:-

Author’s Note:-

Accounting System & Process

Name of the Student:-

Name of the University:-

Author’s Note:-

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ACCOUNTING SYSTEM & PROCESS

2ACCOUNTING SYSTEM & PROCESS

Table of Contents

Q 1:..................................................................................................................................................4

Q 2:..................................................................................................................................................4

Q 3:..................................................................................................................................................8

Q 4:..................................................................................................................................................9

Q 5:................................................................................................................................................10

Q 6:................................................................................................................................................11

Q 7:................................................................................................................................................12

Requirement 1:...........................................................................................................................12

Requirement 2:...........................................................................................................................13

Requirement 3:...........................................................................................................................14

Requirement 4:...........................................................................................................................14

Q 8:................................................................................................................................................16

Q 9:................................................................................................................................................17

Q 10:..............................................................................................................................................17

Q 12:..............................................................................................................................................19

Q 13:..............................................................................................................................................20

Q 14:..............................................................................................................................................20

Q 15:..............................................................................................................................................21

Reference & Bibliography:............................................................................................................29

Table of Contents

Q 1:..................................................................................................................................................4

Q 2:..................................................................................................................................................4

Q 3:..................................................................................................................................................8

Q 4:..................................................................................................................................................9

Q 5:................................................................................................................................................10

Q 6:................................................................................................................................................11

Q 7:................................................................................................................................................12

Requirement 1:...........................................................................................................................12

Requirement 2:...........................................................................................................................13

Requirement 3:...........................................................................................................................14

Requirement 4:...........................................................................................................................14

Q 8:................................................................................................................................................16

Q 9:................................................................................................................................................17

Q 10:..............................................................................................................................................17

Q 12:..............................................................................................................................................19

Q 13:..............................................................................................................................................20

Q 14:..............................................................................................................................................20

Q 15:..............................................................................................................................................21

Reference & Bibliography:............................................................................................................29

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ACCOUNTING SYSTEM & PROCESS

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ACCOUNTING SYSTEM & PROCESS

Q 1:

Plagiarism can be defined as the process of copying the ideas of others and describing the

idea with same words, used in the original source, without giving proper credit to it. The honest

students often get deprived due to the plagiarism. Many students use to copy others’ assignments

without changing a single word and get higher marks. On the other hand, the honest students

complete the assignments by fair means but may not such high marks. In such scenario, the

student, who has not studied the subject at all and given any effort, would get more advantage

than the honest student, who has worked hard to complete the assignment. Hence, plagiarism is

considered as one of the unfair ways to deprive honest students.

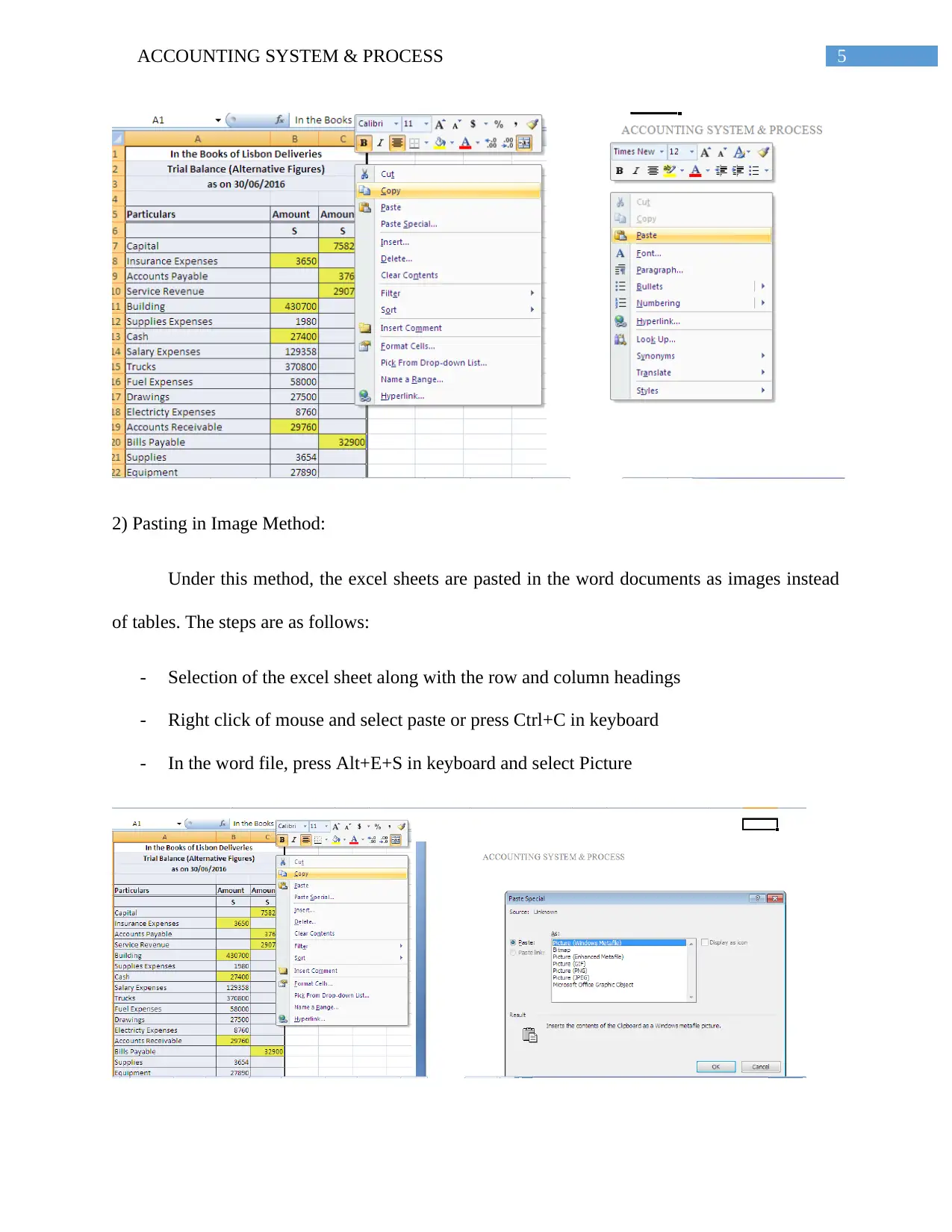

Q 2:

The computer spreadsheet, for example, Excel sheets can be copied and pasted in the

word documents through various methods. However, there are two most widely-used methods of

pasting excel sheets are described below:

1) Simple Pasting Method:

The steps of simple pasting method are stated below:

- Selection of the excel sheet along with the row and column headings

- Right click of mouse and select paste or press Ctrl+C in keyboard

- In the word file, right click of mouse and select paste or press Ctrl+V in keyboard

Q 1:

Plagiarism can be defined as the process of copying the ideas of others and describing the

idea with same words, used in the original source, without giving proper credit to it. The honest

students often get deprived due to the plagiarism. Many students use to copy others’ assignments

without changing a single word and get higher marks. On the other hand, the honest students

complete the assignments by fair means but may not such high marks. In such scenario, the

student, who has not studied the subject at all and given any effort, would get more advantage

than the honest student, who has worked hard to complete the assignment. Hence, plagiarism is

considered as one of the unfair ways to deprive honest students.

Q 2:

The computer spreadsheet, for example, Excel sheets can be copied and pasted in the

word documents through various methods. However, there are two most widely-used methods of

pasting excel sheets are described below:

1) Simple Pasting Method:

The steps of simple pasting method are stated below:

- Selection of the excel sheet along with the row and column headings

- Right click of mouse and select paste or press Ctrl+C in keyboard

- In the word file, right click of mouse and select paste or press Ctrl+V in keyboard

5ACCOUNTING SYSTEM & PROCESS

2) Pasting in Image Method:

Under this method, the excel sheets are pasted in the word documents as images instead

of tables. The steps are as follows:

- Selection of the excel sheet along with the row and column headings

- Right click of mouse and select paste or press Ctrl+C in keyboard

- In the word file, press Alt+E+S in keyboard and select Picture

2) Pasting in Image Method:

Under this method, the excel sheets are pasted in the word documents as images instead

of tables. The steps are as follows:

- Selection of the excel sheet along with the row and column headings

- Right click of mouse and select paste or press Ctrl+C in keyboard

- In the word file, press Alt+E+S in keyboard and select Picture

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ACCOUNTING SYSTEM & PROCESS

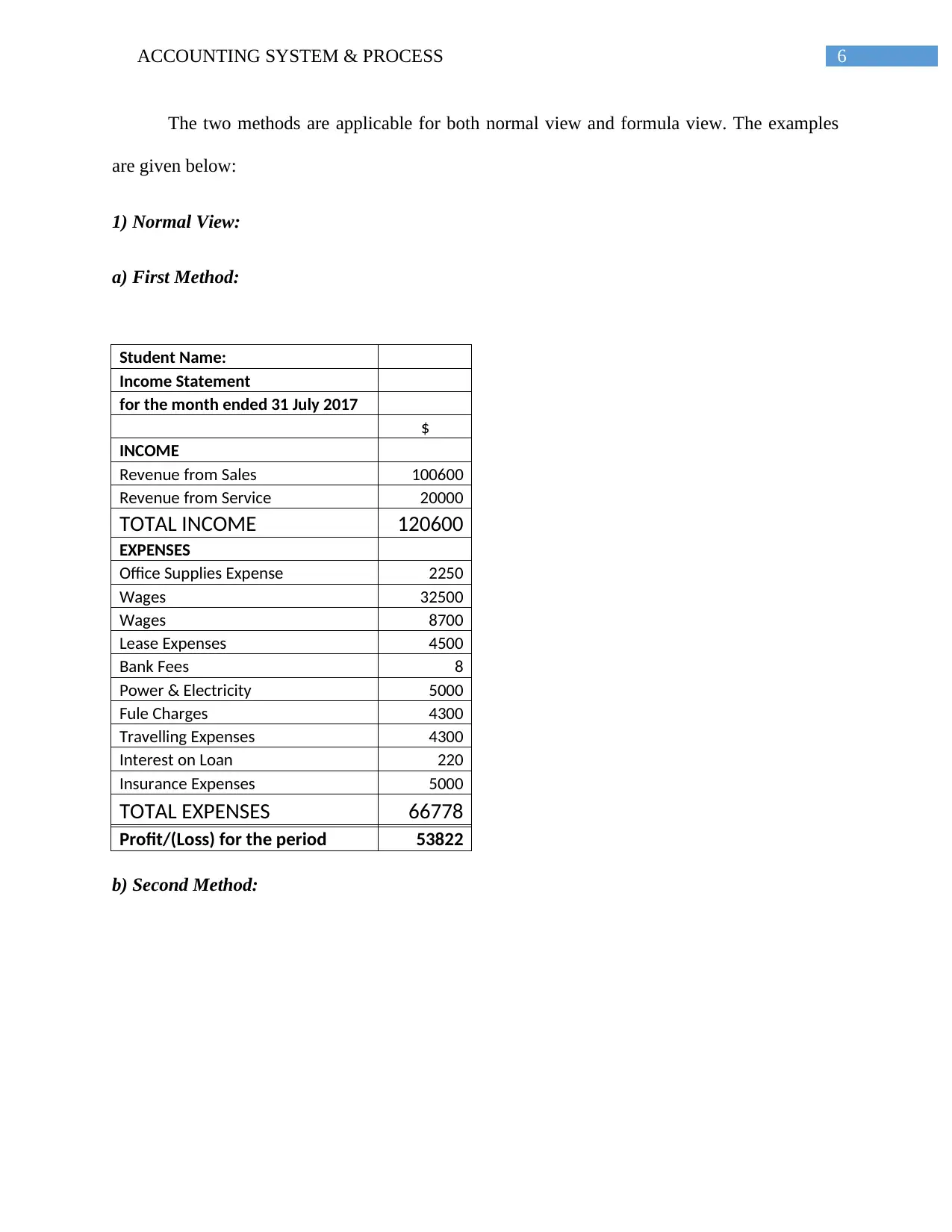

The two methods are applicable for both normal view and formula view. The examples

are given below:

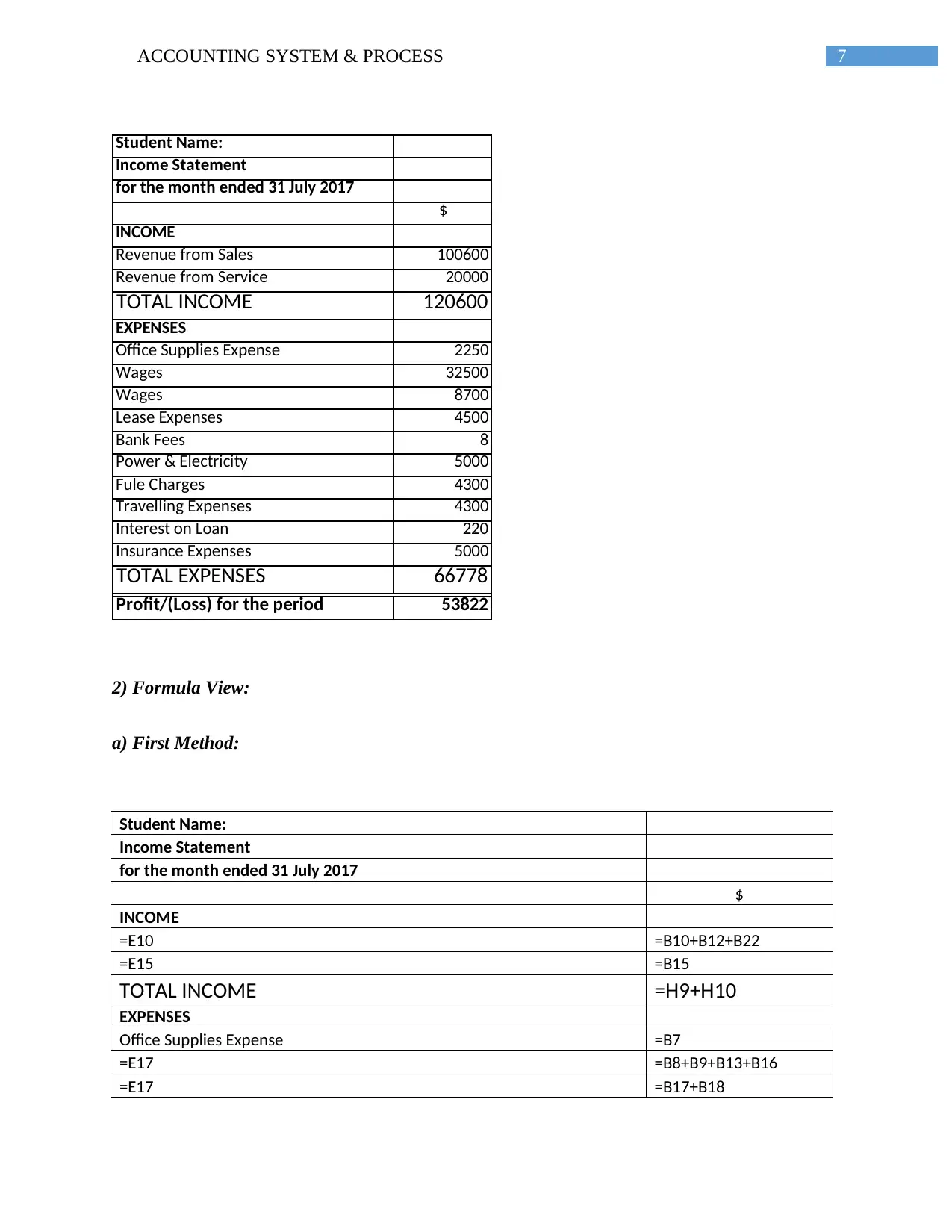

1) Normal View:

a) First Method:

Student Name:

Income Statement

for the month ended 31 July 2017

$

INCOME

Revenue from Sales 100600

Revenue from Service 20000

TOTAL INCOME 120600

EXPENSES

Office Supplies Expense 2250

Wages 32500

Wages 8700

Lease Expenses 4500

Bank Fees 8

Power & Electricity 5000

Fule Charges 4300

Travelling Expenses 4300

Interest on Loan 220

Insurance Expenses 5000

TOTAL EXPENSES 66778

Profit/(Loss) for the period 53822

b) Second Method:

The two methods are applicable for both normal view and formula view. The examples

are given below:

1) Normal View:

a) First Method:

Student Name:

Income Statement

for the month ended 31 July 2017

$

INCOME

Revenue from Sales 100600

Revenue from Service 20000

TOTAL INCOME 120600

EXPENSES

Office Supplies Expense 2250

Wages 32500

Wages 8700

Lease Expenses 4500

Bank Fees 8

Power & Electricity 5000

Fule Charges 4300

Travelling Expenses 4300

Interest on Loan 220

Insurance Expenses 5000

TOTAL EXPENSES 66778

Profit/(Loss) for the period 53822

b) Second Method:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ACCOUNTING SYSTEM & PROCESS

Student Name:

Income Statement

for the month ended 31 July 2017

$

INCOME

Revenue from Sales 100600

Revenue from Service 20000

TOTAL INCOME 120600

EXPENSES

Office Supplies Expense 2250

Wages 32500

Wages 8700

Lease Expenses 4500

Bank Fees 8

Power & Electricity 5000

Fule Charges 4300

Travelling Expenses 4300

Interest on Loan 220

Insurance Expenses 5000

TOTAL EXPENSES 66778

Profit/(Loss) for the period 53822

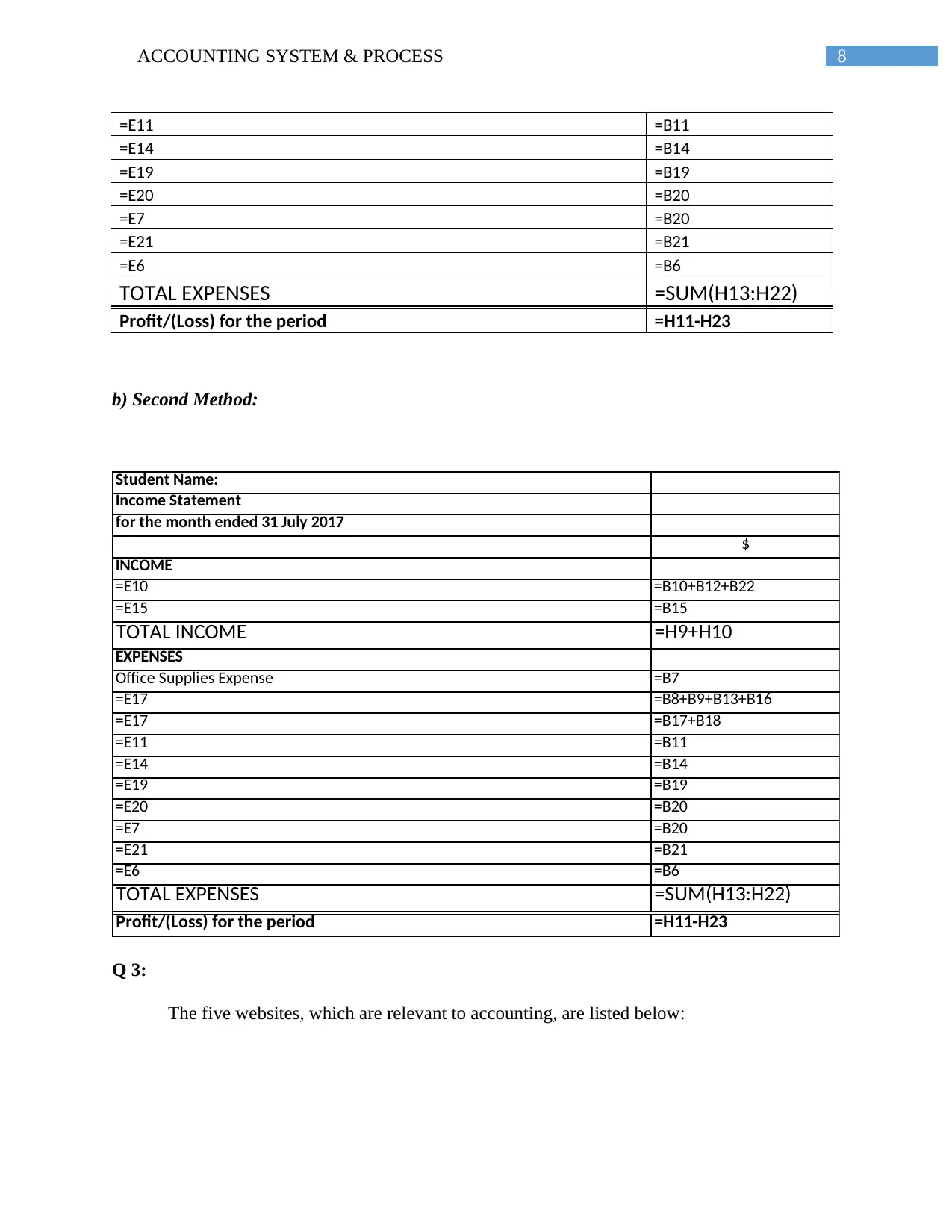

2) Formula View:

a) First Method:

Student Name:

Income Statement

for the month ended 31 July 2017

$

INCOME

=E10 =B10+B12+B22

=E15 =B15

TOTAL INCOME =H9+H10

EXPENSES

Office Supplies Expense =B7

=E17 =B8+B9+B13+B16

=E17 =B17+B18

Student Name:

Income Statement

for the month ended 31 July 2017

$

INCOME

Revenue from Sales 100600

Revenue from Service 20000

TOTAL INCOME 120600

EXPENSES

Office Supplies Expense 2250

Wages 32500

Wages 8700

Lease Expenses 4500

Bank Fees 8

Power & Electricity 5000

Fule Charges 4300

Travelling Expenses 4300

Interest on Loan 220

Insurance Expenses 5000

TOTAL EXPENSES 66778

Profit/(Loss) for the period 53822

2) Formula View:

a) First Method:

Student Name:

Income Statement

for the month ended 31 July 2017

$

INCOME

=E10 =B10+B12+B22

=E15 =B15

TOTAL INCOME =H9+H10

EXPENSES

Office Supplies Expense =B7

=E17 =B8+B9+B13+B16

=E17 =B17+B18

8ACCOUNTING SYSTEM & PROCESS

=E11 =B11

=E14 =B14

=E19 =B19

=E20 =B20

=E7 =B20

=E21 =B21

=E6 =B6

TOTAL EXPENSES =SUM(H13:H22)

Profit/(Loss) for the period =H11-H23

b) Second Method:

Student Name:

Income Statement

for the month ended 31 July 2017

$

INCOME

=E10 =B10+B12+B22

=E15 =B15

TOTAL INCOME =H9+H10

EXPENSES

Office Supplies Expense =B7

=E17 =B8+B9+B13+B16

=E17 =B17+B18

=E11 =B11

=E14 =B14

=E19 =B19

=E20 =B20

=E7 =B20

=E21 =B21

=E6 =B6

TOTAL EXPENSES =SUM(H13:H22)

Profit/(Loss) for the period =H11-H23

Q 3:

The five websites, which are relevant to accounting, are listed below:

=E11 =B11

=E14 =B14

=E19 =B19

=E20 =B20

=E7 =B20

=E21 =B21

=E6 =B6

TOTAL EXPENSES =SUM(H13:H22)

Profit/(Loss) for the period =H11-H23

b) Second Method:

Student Name:

Income Statement

for the month ended 31 July 2017

$

INCOME

=E10 =B10+B12+B22

=E15 =B15

TOTAL INCOME =H9+H10

EXPENSES

Office Supplies Expense =B7

=E17 =B8+B9+B13+B16

=E17 =B17+B18

=E11 =B11

=E14 =B14

=E19 =B19

=E20 =B20

=E7 =B20

=E21 =B21

=E6 =B6

TOTAL EXPENSES =SUM(H13:H22)

Profit/(Loss) for the period =H11-H23

Q 3:

The five websites, which are relevant to accounting, are listed below:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ACCOUNTING SYSTEM & PROCESS

1) Australian Accounting Standard Board (http://www.aasb.gov.au ) : This website provides the

accounting standards, which have to be followed for recording any accounting transactions and

preparing accounting reports.

2) International Financial Reporting Standards (http://www.ifrs.org/ ) : This website describes

the international standards for preparing financial reports.

3) Australian Taxation Office (https://www.ato.gov.au ): This is the website, where all the

information, related to accounting for taxation in Australia, are available.

4) Financial Accounting Standard Board (http://www.fasb.org ): The accounting standards of

AASB are based on the FASB standards. Therefore, apart from AASB website, this website can

also be helpful for the relevant information on accounting standards.

5) Generally Accepted Accounting Principles (http://gaap.com.au ): GAAP is another popular

accounting principles, followed in any countries, especially in USA. Hence, for international

financial reporting, this website can be very beneficial to understand the accounting policies,

adopted by foreign companies.

Q 4:

Amongst the various professional accounting organizations, Association of International

Accountants is one of the most revered organizations. The organization helps the people, who

wish to have training in accountancy, financially. Moreover, the professional accountants and the

business firms can also get various type of financial and accounting information from the website

of this organization.

1) Australian Accounting Standard Board (http://www.aasb.gov.au ) : This website provides the

accounting standards, which have to be followed for recording any accounting transactions and

preparing accounting reports.

2) International Financial Reporting Standards (http://www.ifrs.org/ ) : This website describes

the international standards for preparing financial reports.

3) Australian Taxation Office (https://www.ato.gov.au ): This is the website, where all the

information, related to accounting for taxation in Australia, are available.

4) Financial Accounting Standard Board (http://www.fasb.org ): The accounting standards of

AASB are based on the FASB standards. Therefore, apart from AASB website, this website can

also be helpful for the relevant information on accounting standards.

5) Generally Accepted Accounting Principles (http://gaap.com.au ): GAAP is another popular

accounting principles, followed in any countries, especially in USA. Hence, for international

financial reporting, this website can be very beneficial to understand the accounting policies,

adopted by foreign companies.

Q 4:

Amongst the various professional accounting organizations, Association of International

Accountants is one of the most revered organizations. The organization helps the people, who

wish to have training in accountancy, financially. Moreover, the professional accountants and the

business firms can also get various type of financial and accounting information from the website

of this organization.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ACCOUNTING SYSTEM & PROCESS

Q 5:

Work Integrated Assessment

My previous work was in educational institute where they had to prepare the students for

the entrance examination of engineering as well as medical background. In that, we had

computing work environment that my existing workplace. My key responsibility computer was

to handle the administration as well as documentation work for the educational institutes. I had to

perform all the documentation work by using computers and system need to be updated as well.

In my computer, information was saved in data saving file as well as protected by uploading on

the computer. The use of network was easily accessible and reliable because it was linked with

the computer (Williams, 2014). In my computer, Microsoft office programs were present that I

used to work like Microsoft PowerPoint, Microsoft word, Microsoft Excel and Microsoft

Outlook. While working in these educational institutions, I was aware of various courses and

programs that are provided for the students so that they can score well in their entrance

examination. I was responsible to handle the administration department where I noted that this

educational institution was running their business in a profitable way.

Currently, I am working in a bank where I am employed as manager. In the bank, I was

provided with materials that I need on daily basis like task lamp, document holder, phone head

set as well as computer to work. We are given comfortable desk and chair where we can sit and

work without any problem. Secrecy and confidentiality of information need to be maintained at

banks as there are so many transactions related to money that we have to handle. I really enjoy

working in this friendly and productive environment where we are given enough freedom to

work as we like and utilize the resources as far as possible.

Q 5:

Work Integrated Assessment

My previous work was in educational institute where they had to prepare the students for

the entrance examination of engineering as well as medical background. In that, we had

computing work environment that my existing workplace. My key responsibility computer was

to handle the administration as well as documentation work for the educational institutes. I had to

perform all the documentation work by using computers and system need to be updated as well.

In my computer, information was saved in data saving file as well as protected by uploading on

the computer. The use of network was easily accessible and reliable because it was linked with

the computer (Williams, 2014). In my computer, Microsoft office programs were present that I

used to work like Microsoft PowerPoint, Microsoft word, Microsoft Excel and Microsoft

Outlook. While working in these educational institutions, I was aware of various courses and

programs that are provided for the students so that they can score well in their entrance

examination. I was responsible to handle the administration department where I noted that this

educational institution was running their business in a profitable way.

Currently, I am working in a bank where I am employed as manager. In the bank, I was

provided with materials that I need on daily basis like task lamp, document holder, phone head

set as well as computer to work. We are given comfortable desk and chair where we can sit and

work without any problem. Secrecy and confidentiality of information need to be maintained at

banks as there are so many transactions related to money that we have to handle. I really enjoy

working in this friendly and productive environment where we are given enough freedom to

work as we like and utilize the resources as far as possible.

11ACCOUNTING SYSTEM & PROCESS

Q 6:

ABC Learning and ethics- ABC Learning Case study

In this particular question, ABC Learning was explained where it experiences a slow but

stable start especially in the first year of operations (Weil, Schipper & Francis, 2013). On

introducing the role of Federal Government, it was considered as the main factor that needs

development at that point of time. It was all about the company who actually has access to

fantastic media coverage but the government was even purchasing the centers of ABC by using

indirect means. In addition, the company even was capable for international expansion in the

near future. The company enjoys high share price as well as valuation of assets that was

increasing at a faster pace because of financial inclusions. After gathering information from the

reports of the company, it is noted that the financial performance as well as cash flow shows the

scenario that it is about to collapse in short time (Deegan, 2013). There was a need for ABC

Learning on urgent basis and this could be realized because of astronomical debt as well as

valuation of assets at given inflated and the cross assets liquidity at the same time. The company

even suffered from huge debt crisis during the Global Financial Crisis 2008 where the company

owned more than dollar in debt at 30% in equity.

There are three major ethical issues that were the reason for the collapse of ABC

Learning and these are as follows:

There was wrong information given about the company to the public because of which

shareholders had lost money in the business.

There was constant accounting irregularities as well as company had used margin loan

for financing purpose.

Q 6:

ABC Learning and ethics- ABC Learning Case study

In this particular question, ABC Learning was explained where it experiences a slow but

stable start especially in the first year of operations (Weil, Schipper & Francis, 2013). On

introducing the role of Federal Government, it was considered as the main factor that needs

development at that point of time. It was all about the company who actually has access to

fantastic media coverage but the government was even purchasing the centers of ABC by using

indirect means. In addition, the company even was capable for international expansion in the

near future. The company enjoys high share price as well as valuation of assets that was

increasing at a faster pace because of financial inclusions. After gathering information from the

reports of the company, it is noted that the financial performance as well as cash flow shows the

scenario that it is about to collapse in short time (Deegan, 2013). There was a need for ABC

Learning on urgent basis and this could be realized because of astronomical debt as well as

valuation of assets at given inflated and the cross assets liquidity at the same time. The company

even suffered from huge debt crisis during the Global Financial Crisis 2008 where the company

owned more than dollar in debt at 30% in equity.

There are three major ethical issues that were the reason for the collapse of ABC

Learning and these are as follows:

There was wrong information given about the company to the public because of which

shareholders had lost money in the business.

There was constant accounting irregularities as well as company had used margin loan

for financing purpose.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 30

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.