Accounting Information Systems: Adam & Co. Expenditure Cycle

VerifiedAdded on 2022/11/13

|17

|3120

|447

Report

AI Summary

This report examines the internal control risks and processes within Adam & Co.'s expenditure cycle after centralizing its accounting system across multiple locations. The analysis focuses on the purchase, cash disbursement, and payroll systems, including system flowcharts and identification of control weaknesses. The report highlights the manual processes as the main issue, advocating for automation to save resources and time. Weaknesses are identified in the purchase system (manual inventory checks and hard copy orders), cash disbursement system (manual order monitoring and lack of supplier integration), and payroll system (manual data entry and hard copy document handling). The associated risks include errors, lack of supplier trust, and employee dissatisfaction. The report emphasizes the need for automated processes to improve accuracy, timeliness, and overall efficiency.

Running head: ACCOUNTING INFORMATION SYSTEMS

Accounting Information Systems

By Name of the Student

Group Number

Module Name

Accounting Information Systems

By Name of the Student

Group Number

Module Name

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

ACCOUNTING INFORMATION SYSTEMS

Executive Summary

The report enumerates the risks and processes of the internal control in the expenditure cycle

of Adam & Co. after it centralized its accounting system by using various network terminals

at different locations. The main risks and processes for the internal control have been

identified in “purchases system”, “cash disbursement system” and the “payroll system”

along with designing of the respective system flowcharts. The depiction of the control issues

has paved the way for effectively tracking the areas which need improvement. The findings

have revealed that the main issues are due to the manual process being followed in all the

three aforementioned systems. The organisation needs to innovate and develop an automated

process to eliminate the manual activities and save both resources and time.

ACCOUNTING INFORMATION SYSTEMS

Executive Summary

The report enumerates the risks and processes of the internal control in the expenditure cycle

of Adam & Co. after it centralized its accounting system by using various network terminals

at different locations. The main risks and processes for the internal control have been

identified in “purchases system”, “cash disbursement system” and the “payroll system”

along with designing of the respective system flowcharts. The depiction of the control issues

has paved the way for effectively tracking the areas which need improvement. The findings

have revealed that the main issues are due to the manual process being followed in all the

three aforementioned systems. The organisation needs to innovate and develop an automated

process to eliminate the manual activities and save both resources and time.

2

ACCOUNTING INFORMATION SYSTEMS

Table of Contents

Introduction................................................................................................................................3

System Flowchart of purchase systems......................................................................................4

Internal control weakness in the purchase systems....................................................................5

Risk associated with the weakness of purchase systems...........................................................5

System Flowchart of cash disbursement system........................................................................7

Internal control weakness in the cash disbursement system......................................................8

Risk associated with the weakness of the cash disbursement system........................................9

System Flowchart of payroll system........................................................................................10

Internal control weakness in the payroll system......................................................................11

Risk associated with the weakness in the payroll system........................................................12

Conclusion................................................................................................................................12

References................................................................................................................................14

ACCOUNTING INFORMATION SYSTEMS

Table of Contents

Introduction................................................................................................................................3

System Flowchart of purchase systems......................................................................................4

Internal control weakness in the purchase systems....................................................................5

Risk associated with the weakness of purchase systems...........................................................5

System Flowchart of cash disbursement system........................................................................7

Internal control weakness in the cash disbursement system......................................................8

Risk associated with the weakness of the cash disbursement system........................................9

System Flowchart of payroll system........................................................................................10

Internal control weakness in the payroll system......................................................................11

Risk associated with the weakness in the payroll system........................................................12

Conclusion................................................................................................................................12

References................................................................................................................................14

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

ACCOUNTING INFORMATION SYSTEMS

Introduction

The evaluation of operations is necessary for identifying the sub-processes. Similarly,

it is also customary to make assessment of the time and resources required for completion of

a task (Heizer, Render and Munson 2017). Process analysis plays a vital role in depicting the

needs of improvements in the operations activities (Mahadevan 2015). The study has focused

process assessment of “purchases systems”, “payroll process” and “cash disbursement

system” in Adam & Co. Some of the other excerpts will discuss about the weakness in

internal control and risk involved in each of the processes.

ACCOUNTING INFORMATION SYSTEMS

Introduction

The evaluation of operations is necessary for identifying the sub-processes. Similarly,

it is also customary to make assessment of the time and resources required for completion of

a task (Heizer, Render and Munson 2017). Process analysis plays a vital role in depicting the

needs of improvements in the operations activities (Mahadevan 2015). The study has focused

process assessment of “purchases systems”, “payroll process” and “cash disbursement

system” in Adam & Co. Some of the other excerpts will discuss about the weakness in

internal control and risk involved in each of the processes.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

ACCOUNTING INFORMATION SYSTEMS

Inventory

Ledger Inventory Clerk

Ledger Checking

and preparation of

orders

Forwarding printed

copy to vendor Digital Copy to

Purchase

Placing of order

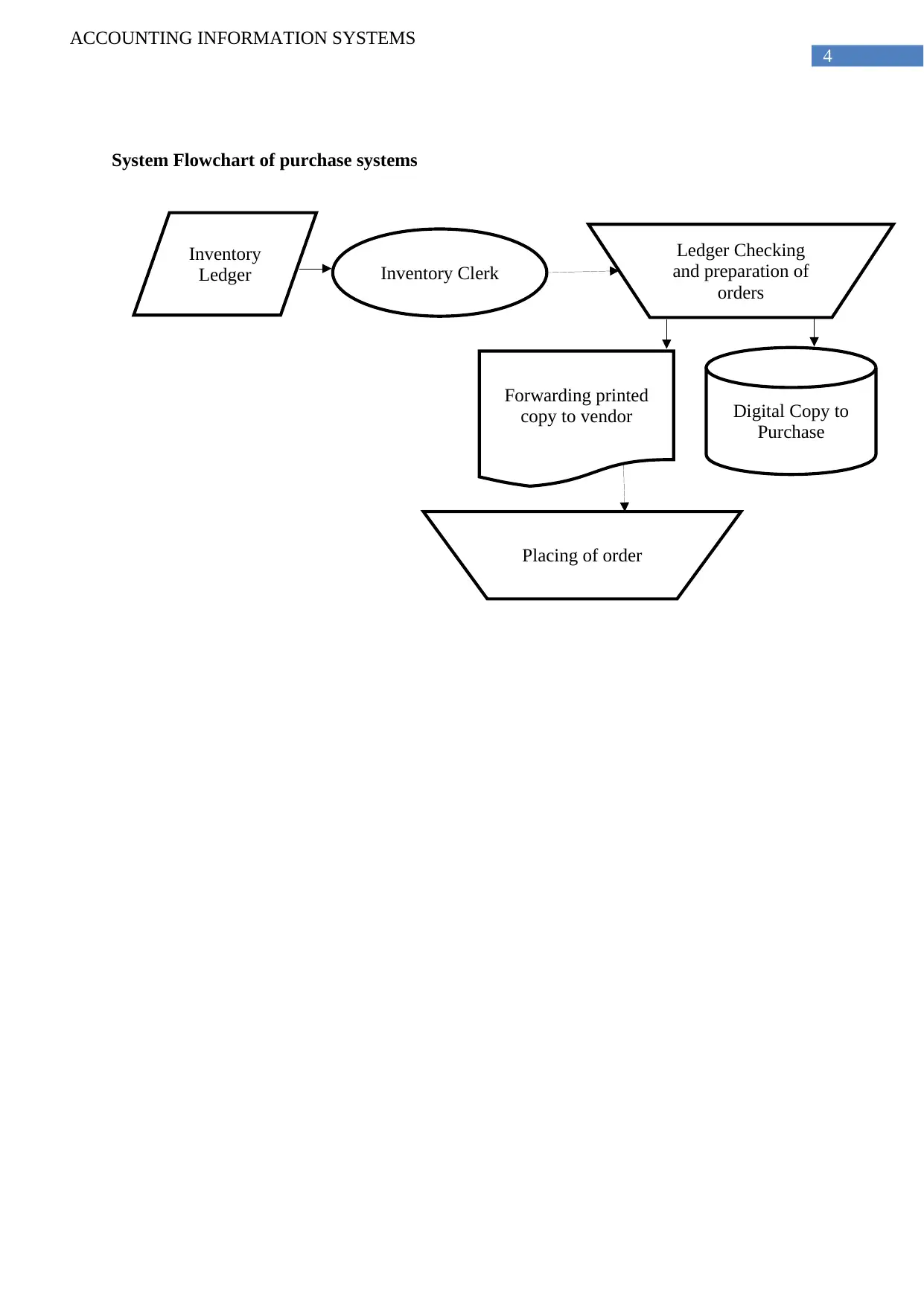

System Flowchart of purchase systems

ACCOUNTING INFORMATION SYSTEMS

Inventory

Ledger Inventory Clerk

Ledger Checking

and preparation of

orders

Forwarding printed

copy to vendor Digital Copy to

Purchase

Placing of order

System Flowchart of purchase systems

5

ACCOUNTING INFORMATION SYSTEMS

Internal control weakness in the purchase systems

Purchasing is defined as an activity conducted by any organisation for maintaining the

appropriate level of inventory. There are several tasks which are to be performed before or

after the purchase. In normal circumstances, the input is gathered from inventory information.

The purchase team processes the data so that the output can be produced and informed to the

vendors. (Koeppel and Perry 2019). The purchase process involves multiple stages such as

placing of an order, collecting inputs from inventory data and selecting the vendors (Hugos

2018). As soon as the data is collected on the inventory, it is processed with the support of

various teams and organizations. The output is further shared via different channels based on

the customer’s preference. The monitoring of the purchase process is done to ensure quality

based on the parameters such as accuracy and timeliness (Mukherjee 2017). The purchase

process may comprise of the following weaknesses:

1. Checking the Inventory Manually: The new orders requirement is checked manually in

the inventory. The manual monitoring process affects accuracy and requires more time.

2. Informing the Vendors through hard Copy of orders: The use of hard copy may

decrease the readability of data across different levels of the organization. This can

further negatively impact the level of collaboration and increase the chances of risks

(Mcmillion 2015).

Risk associated with the weakness of purchase systems

The challenges involved in the purchase process are listed as follows:

1. Complexity in collecting information from the inventory: The purchase quality is

dependent on the knowledge of inventory requirement. Ordering appropriate quantity

becomes easier for businesses which understands its inventory operations. However, in

ACCOUNTING INFORMATION SYSTEMS

Internal control weakness in the purchase systems

Purchasing is defined as an activity conducted by any organisation for maintaining the

appropriate level of inventory. There are several tasks which are to be performed before or

after the purchase. In normal circumstances, the input is gathered from inventory information.

The purchase team processes the data so that the output can be produced and informed to the

vendors. (Koeppel and Perry 2019). The purchase process involves multiple stages such as

placing of an order, collecting inputs from inventory data and selecting the vendors (Hugos

2018). As soon as the data is collected on the inventory, it is processed with the support of

various teams and organizations. The output is further shared via different channels based on

the customer’s preference. The monitoring of the purchase process is done to ensure quality

based on the parameters such as accuracy and timeliness (Mukherjee 2017). The purchase

process may comprise of the following weaknesses:

1. Checking the Inventory Manually: The new orders requirement is checked manually in

the inventory. The manual monitoring process affects accuracy and requires more time.

2. Informing the Vendors through hard Copy of orders: The use of hard copy may

decrease the readability of data across different levels of the organization. This can

further negatively impact the level of collaboration and increase the chances of risks

(Mcmillion 2015).

Risk associated with the weakness of purchase systems

The challenges involved in the purchase process are listed as follows:

1. Complexity in collecting information from the inventory: The purchase quality is

dependent on the knowledge of inventory requirement. Ordering appropriate quantity

becomes easier for businesses which understands its inventory operations. However, in

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

ACCOUNTING INFORMATION SYSTEMS

many cases knowing the inventory requirement can be cumbersome. The inventory clerk

may fail to depict the appropriate quantity required and share it accurately with the

company (Pauker and Spies 2017).

2. Timely placing of the order: In most situations, organizations expect swift processing of

purchase systems. However, sometimes the orders might take more time than elected. In

the given scenario of Adam & Co. The delay in purchase process may negatively impact

on the entire efficiency of the organisation.

3. Using the existing data inappropriately: The appropriate usage of existing data decides

whether the purchase has been executed efficiently. In this context, the businesses are

needed to assess their inventory for ensuring quality of purchasing activities.

4. Complying with expectations- The main target of purchasing service is to ensure

smooth flow of raw materials. The business needs to consider their personal production

schedule while executing the activities associated with inventory. The teams are needed

to collaborate among themselves for fulfilling the inventory requirements on time.

ACCOUNTING INFORMATION SYSTEMS

many cases knowing the inventory requirement can be cumbersome. The inventory clerk

may fail to depict the appropriate quantity required and share it accurately with the

company (Pauker and Spies 2017).

2. Timely placing of the order: In most situations, organizations expect swift processing of

purchase systems. However, sometimes the orders might take more time than elected. In

the given scenario of Adam & Co. The delay in purchase process may negatively impact

on the entire efficiency of the organisation.

3. Using the existing data inappropriately: The appropriate usage of existing data decides

whether the purchase has been executed efficiently. In this context, the businesses are

needed to assess their inventory for ensuring quality of purchasing activities.

4. Complying with expectations- The main target of purchasing service is to ensure

smooth flow of raw materials. The business needs to consider their personal production

schedule while executing the activities associated with inventory. The teams are needed

to collaborate among themselves for fulfilling the inventory requirements on time.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

ACCOUNTING INFORMATION SYSTEMS

Information related to vendor list

Lower inventory

information in ledger Purchasing Clerk Purchase

Making hard copies for vendorsForwarding digital copy to purchase departm

Specification of the supplies at the

receiving department

Manually preparing two hard copiesPacking slipOrder’s arrival at receiving side

Inventory Accounts Payable

Inventory shelving

Computer

Invoice of supplier

Printing invoice and forwarding to cash disbursement along with other two

Entering

information on

Computer

Due date checking by the clerk at cash disbursement

Invoice sent and signed by treasurer

Mailing to vendor

Updating the subsidiary ledger of

accounts payable, cheque register

and control account of accounts

payable from computer

Filing the copies of

cheque, invoice, purchase

order and receiving report

by receiving clerk

System Flowchart of cash disbursement system

ACCOUNTING INFORMATION SYSTEMS

Information related to vendor list

Lower inventory

information in ledger Purchasing Clerk Purchase

Making hard copies for vendorsForwarding digital copy to purchase departm

Specification of the supplies at the

receiving department

Manually preparing two hard copiesPacking slipOrder’s arrival at receiving side

Inventory Accounts Payable

Inventory shelving

Computer

Invoice of supplier

Printing invoice and forwarding to cash disbursement along with other two

Entering

information on

Computer

Due date checking by the clerk at cash disbursement

Invoice sent and signed by treasurer

Mailing to vendor

Updating the subsidiary ledger of

accounts payable, cheque register

and control account of accounts

payable from computer

Filing the copies of

cheque, invoice, purchase

order and receiving report

by receiving clerk

System Flowchart of cash disbursement system

8

ACCOUNTING INFORMATION SYSTEMS

Internal control weakness in the cash disbursement system

The cash disbursement process involves processing of the cash flows associated to

procurement activities which involves payments to be made for purchase obligations (DeVan

et al. 2015). The designing of such a system is done to ensure that an organisation is able to

process the payments appropriately in its accounts payable over red whenever it is due.

Therefore, the Accounts Payable department is usually responsible for notifying the need for

maintaining vendor accounts and making cash disbursements (O’Reilly 2019).

The challenges identified in the cash disbursement system are as follows:

1. Monitoring the received orders manually- In general, the suppliers are paid as per the

quality of the products received. In the given case study of Adam & Co. The quality

checking of the products is done manually, based on which the payment is initiated. This

increases the consumption time of the entire process. In addition to this, manual labour is

itself more risk prone in nature (Potts and Everi Payments 2015).

2. Infrastructure lacks supplier integration- In order to ensure transparency in the

payment process, there needs to be an integration of the suppliers. As for the given case

study, there are two distinct systems used for communicating with the internal and

external stakeholders. The suppliers are notified about the payment with the use of hard

copies, while the digital records are regulated for the purpose of internal teams within the

business. This shows the lack of digital infrastructure for communicating with the

supplier which acts as an obstacle to transparency for the organisation (Klapper and

Singer 2017).

ACCOUNTING INFORMATION SYSTEMS

Internal control weakness in the cash disbursement system

The cash disbursement process involves processing of the cash flows associated to

procurement activities which involves payments to be made for purchase obligations (DeVan

et al. 2015). The designing of such a system is done to ensure that an organisation is able to

process the payments appropriately in its accounts payable over red whenever it is due.

Therefore, the Accounts Payable department is usually responsible for notifying the need for

maintaining vendor accounts and making cash disbursements (O’Reilly 2019).

The challenges identified in the cash disbursement system are as follows:

1. Monitoring the received orders manually- In general, the suppliers are paid as per the

quality of the products received. In the given case study of Adam & Co. The quality

checking of the products is done manually, based on which the payment is initiated. This

increases the consumption time of the entire process. In addition to this, manual labour is

itself more risk prone in nature (Potts and Everi Payments 2015).

2. Infrastructure lacks supplier integration- In order to ensure transparency in the

payment process, there needs to be an integration of the suppliers. As for the given case

study, there are two distinct systems used for communicating with the internal and

external stakeholders. The suppliers are notified about the payment with the use of hard

copies, while the digital records are regulated for the purpose of internal teams within the

business. This shows the lack of digital infrastructure for communicating with the

supplier which acts as an obstacle to transparency for the organisation (Klapper and

Singer 2017).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

ACCOUNTING INFORMATION SYSTEMS

Risk associated with the weakness of the cash disbursement system

The risk associated with the cash disbursement system is listed below as follows:

1. Erroneous payment- The organizations are required to use the financial resources

optimally. It needs to also ensure that accurate payments are being made to the suppliers

for preventing any waste of the financial resources. The given case suggests that the

payment process relies on tasks which are manual in nature. This leads to increased risk

of errors while making payment to the suppliers (Rachlin 2019).

2. Lack of trusted relationship with the suppliers- In order to ensure that the supply of

raw materials is done efficiently, it is important to ensure that the organisation has

maintained a trusted relationship with the suppliers. In the given scenario, there is clearly

an absence of sufficient digital infrastructure which is mainly responsible for negatively

impacting the transparency in the transactions. Due to this, the business may face several

issues to maintain its trustworthiness with the suppliers (Hay, Schaefers and Thomas,

Union Supply Group 2019).

ACCOUNTING INFORMATION SYSTEMS

Risk associated with the weakness of the cash disbursement system

The risk associated with the cash disbursement system is listed below as follows:

1. Erroneous payment- The organizations are required to use the financial resources

optimally. It needs to also ensure that accurate payments are being made to the suppliers

for preventing any waste of the financial resources. The given case suggests that the

payment process relies on tasks which are manual in nature. This leads to increased risk

of errors while making payment to the suppliers (Rachlin 2019).

2. Lack of trusted relationship with the suppliers- In order to ensure that the supply of

raw materials is done efficiently, it is important to ensure that the organisation has

maintained a trusted relationship with the suppliers. In the given scenario, there is clearly

an absence of sufficient digital infrastructure which is mainly responsible for negatively

impacting the transparency in the transactions. Due to this, the business may face several

issues to maintain its trustworthiness with the suppliers (Hay, Schaefers and Thomas,

Union Supply Group 2019).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

ACCOUNTING INFORMATION SYSTEMS

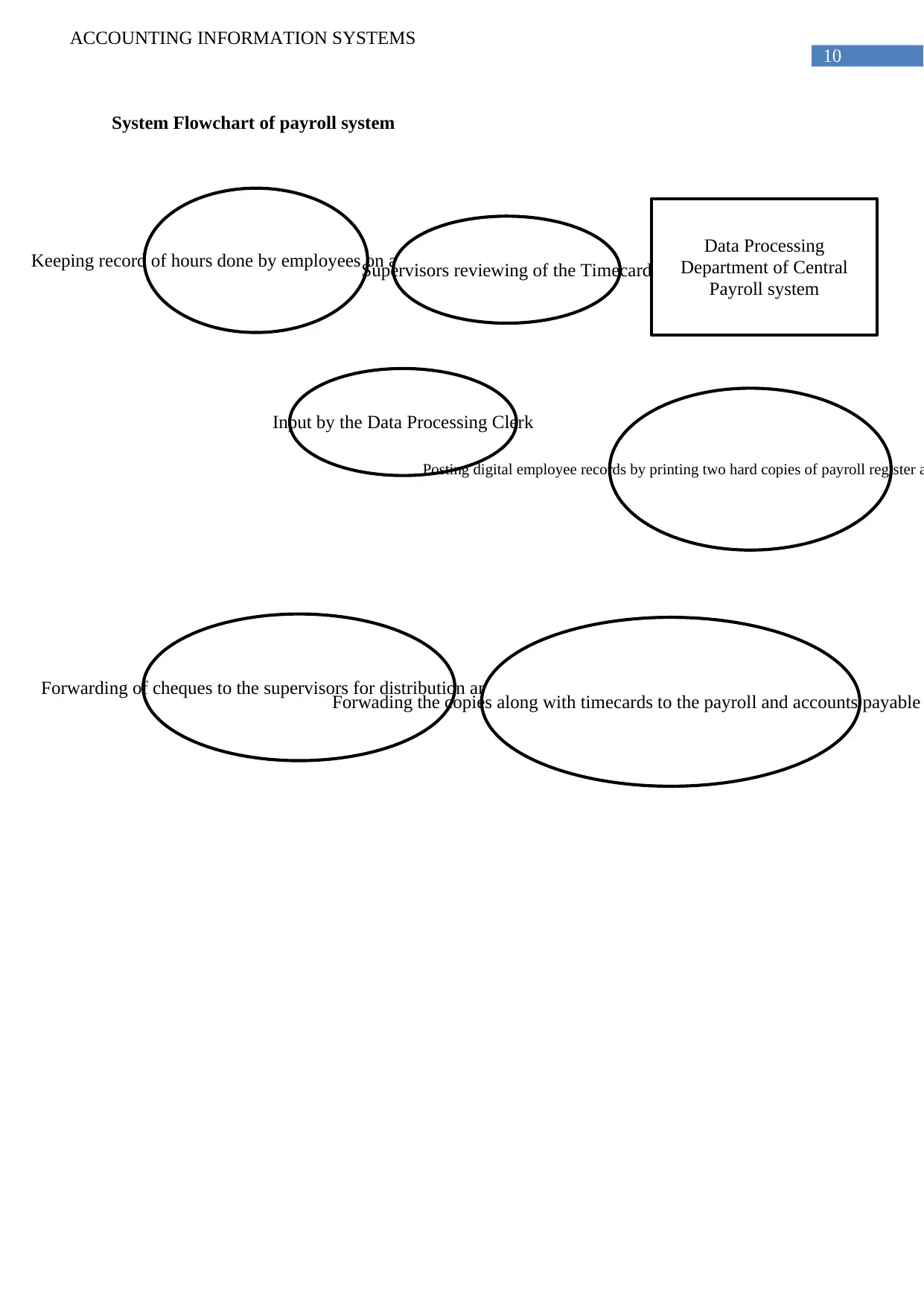

Keeping record of hours done by employees on a daily basisSupervisors reviewing of the Timecard

Data Processing

Department of Central

Payroll system

Input by the Data Processing Clerk

Posting digital employee records by printing two hard copies of payroll register a

Forwarding of cheques to the supervisors for distribution and review

Forwading the copies along with timecards to the payroll and accounts payable

System Flowchart of payroll system

ACCOUNTING INFORMATION SYSTEMS

Keeping record of hours done by employees on a daily basisSupervisors reviewing of the Timecard

Data Processing

Department of Central

Payroll system

Input by the Data Processing Clerk

Posting digital employee records by printing two hard copies of payroll register a

Forwarding of cheques to the supervisors for distribution and review

Forwading the copies along with timecards to the payroll and accounts payable

System Flowchart of payroll system

11

ACCOUNTING INFORMATION SYSTEMS

Internal control weakness in the payroll system

Payroll system deals with all the activities which is needed for filing of employment

taxes and making payment to the implies (DeWitt 2017). Such an information system is

conducive in tracking the total working hours, delivering cheques, printing cheques,

withholding taxes and also managing other deductions (Mahajan, Shukla and Soni 2015). The

initiation of payroll system is done when a company hires its first employee. There can be

several mistakes in the payroll which can originate from the source of income. This can occur

during collecting payroll inputs, distributing payslips, defining of the components and setting

pay policies (Sople 2016).

Some of the most notable weakness of the payroll system for Adam & Co. is listed as

follows:

1. Manually entering and reviewing the data- Based on the facts of the case study, the

employees at Adam & Co. record the working hours manually on the time cards every

day. Additionally, the supervisors are responsible for reviewing the time cards manually

for ensuring correctness in the time cards and forwarding the same to the payroll

department every week. This makes the payroll system not only inefficient but also time

consuming in nature (Gupta, Kundu and Das 2019).

2. Sending hard copies of the payroll documents to the accounts payable department -

As per the given information, the payroll clerk is responsible for filing the time cards in

the payroll department and sending the hard copies of employee paychecks to the

different supervisors for distribution and review of the retrospective department

employees. This takes up a lot of time for the organisation in filing the time cards in a

manual procedure. The copy of payroll register is also sent in a hard copy format to the

Accounts Payable department which is a time-consuming process.

ACCOUNTING INFORMATION SYSTEMS

Internal control weakness in the payroll system

Payroll system deals with all the activities which is needed for filing of employment

taxes and making payment to the implies (DeWitt 2017). Such an information system is

conducive in tracking the total working hours, delivering cheques, printing cheques,

withholding taxes and also managing other deductions (Mahajan, Shukla and Soni 2015). The

initiation of payroll system is done when a company hires its first employee. There can be

several mistakes in the payroll which can originate from the source of income. This can occur

during collecting payroll inputs, distributing payslips, defining of the components and setting

pay policies (Sople 2016).

Some of the most notable weakness of the payroll system for Adam & Co. is listed as

follows:

1. Manually entering and reviewing the data- Based on the facts of the case study, the

employees at Adam & Co. record the working hours manually on the time cards every

day. Additionally, the supervisors are responsible for reviewing the time cards manually

for ensuring correctness in the time cards and forwarding the same to the payroll

department every week. This makes the payroll system not only inefficient but also time

consuming in nature (Gupta, Kundu and Das 2019).

2. Sending hard copies of the payroll documents to the accounts payable department -

As per the given information, the payroll clerk is responsible for filing the time cards in

the payroll department and sending the hard copies of employee paychecks to the

different supervisors for distribution and review of the retrospective department

employees. This takes up a lot of time for the organisation in filing the time cards in a

manual procedure. The copy of payroll register is also sent in a hard copy format to the

Accounts Payable department which is a time-consuming process.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.