Management Accounting Report: Methods and Analysis for Ovation Systems

VerifiedAdded on 2020/12/30

|20

|5226

|26

Report

AI Summary

This report delves into the realm of management accounting, providing a comprehensive analysis applicable to a small to medium enterprise (SME) like Ovation Systems. It begins by defining management accounting and its importance, highlighting the requirements of various accounting systems, including inventory management and job costing, and their benefits. The report then examines different management accounting reports utilized by Ovation Systems, such as cost reports, performance reports, and budget reports, emphasizing their significance in managerial decision-making. The core of the report focuses on the application of absorption and marginal costing methods, including the preparation of income statements and break-even analysis. It further explores the advantages and disadvantages of various planning tools used for budgetary control, their application in analysis, forecasting, and budget preparation. A comparative analysis of management accounting methods is conducted to address financial problems, with an evaluation of management accounting techniques for effective financial problem-solving. The report concludes with a synthesis of the findings, offering insights into how management accounting can be leveraged to enhance financial performance and support sustainable business growth.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

A. Management accounting and requirements of different management accounting system.....1

B. Various accounting management reports used by Ovation system and importance of such

reports..........................................................................................................................................2

C. Benefits of types of inventory management and job costing system.....................................3

D. Integrated features of management accounting system and management accounting reports

in organization.............................................................................................................................4

TASK 2............................................................................................................................................4

A1. Absorption and marginal costing methods...........................................................................4

A2. Preparation of income statements........................................................................................6

C. Significance of Prepared Financial Statements....................................................................10

D. Interpretation of Financial Reports for Ovation Systems.....................................................11

TASK 3..........................................................................................................................................12

A. Advantages and disadvantages of various planning tools for budgetary controlled............12

B. Application of planning tools for analysis, forecasting and preparation..............................13

C. Comparing methods of management accounting systems with regard to financial problems

...................................................................................................................................................14

D. Analysis of management accounting techniques for financial problems.............................14

E. Evaluation of management accounting techniques for financial problems..........................15

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................17

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

A. Management accounting and requirements of different management accounting system.....1

B. Various accounting management reports used by Ovation system and importance of such

reports..........................................................................................................................................2

C. Benefits of types of inventory management and job costing system.....................................3

D. Integrated features of management accounting system and management accounting reports

in organization.............................................................................................................................4

TASK 2............................................................................................................................................4

A1. Absorption and marginal costing methods...........................................................................4

A2. Preparation of income statements........................................................................................6

C. Significance of Prepared Financial Statements....................................................................10

D. Interpretation of Financial Reports for Ovation Systems.....................................................11

TASK 3..........................................................................................................................................12

A. Advantages and disadvantages of various planning tools for budgetary controlled............12

B. Application of planning tools for analysis, forecasting and preparation..............................13

C. Comparing methods of management accounting systems with regard to financial problems

...................................................................................................................................................14

D. Analysis of management accounting techniques for financial problems.............................14

E. Evaluation of management accounting techniques for financial problems..........................15

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................17

INTRODUCTION

Management accounting is analysis of business costs and operations that help in

preparation of internal financial reports, accounts, records which aid managers in making

decisions. It is an important responsibility and its financial data is required in order to determine

various information which can be beneficial for management of an organisation. This report will

give an understanding of management accounting systems and their different methods that are

been used. It will evaluate its benefits and application in Ovation systems, an SME which has 23

employees and is located in UK. Calculations of costs with the help of appropriate cost analysis

will be done and determine income statements using marginal and absorption costs. It will also

explain uses of planning tools, its application while preparing forecasting budgets and their

advantages and disadvantages. Comparison of methods that can solve financial problems and

how they respond to them will be done, which will lead organisation in sustaining its growth

successfully.

TASK 1

A. Management accounting and requirements of different management accounting system

Management accounting is a tool used by managers to manage financial position of the

enterprise and provide accurate report of financial and economic status of a company.

Management refers to advising company for the best use of provision of financial data. In simple

words it is also defined as identifying company's cost and operations and preparing financial

report (Quinn and et.al., 2018). Management is analysing, identifying, planning and managing

activities according to needs of the business.

Accounting management has a selective nature of selecting the limited information out of

wide range of data.

It emphasis on future planning and growth of business.

It only provides large amount of data but no decision.

Wide variety of options available to solve a particular problem.

Reports focuses on preparing a financial information for external parties, such as

stockholders, public regulators etc.

Requirements of Management accounting system are:

1

Management accounting is analysis of business costs and operations that help in

preparation of internal financial reports, accounts, records which aid managers in making

decisions. It is an important responsibility and its financial data is required in order to determine

various information which can be beneficial for management of an organisation. This report will

give an understanding of management accounting systems and their different methods that are

been used. It will evaluate its benefits and application in Ovation systems, an SME which has 23

employees and is located in UK. Calculations of costs with the help of appropriate cost analysis

will be done and determine income statements using marginal and absorption costs. It will also

explain uses of planning tools, its application while preparing forecasting budgets and their

advantages and disadvantages. Comparison of methods that can solve financial problems and

how they respond to them will be done, which will lead organisation in sustaining its growth

successfully.

TASK 1

A. Management accounting and requirements of different management accounting system

Management accounting is a tool used by managers to manage financial position of the

enterprise and provide accurate report of financial and economic status of a company.

Management refers to advising company for the best use of provision of financial data. In simple

words it is also defined as identifying company's cost and operations and preparing financial

report (Quinn and et.al., 2018). Management is analysing, identifying, planning and managing

activities according to needs of the business.

Accounting management has a selective nature of selecting the limited information out of

wide range of data.

It emphasis on future planning and growth of business.

It only provides large amount of data but no decision.

Wide variety of options available to solve a particular problem.

Reports focuses on preparing a financial information for external parties, such as

stockholders, public regulators etc.

Requirements of Management accounting system are:

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Inventory management: Managers of Ovation system requires lot of information regarding the

management of accounting. Inventory is also a kind of management which needs to be managed

properly to get the correct financial reports of the business. Inventory management refers to

keeping the records of production and sale of goods. Stock management identifies the

availability of raw material and finished product in company (Otley, 2015). It deals with demand

and supply of products. Stock of the Ovation system required to be properly managed. Inventory

management consists of keeping information about sale of products and services and stock which

is still available in storage.

Job costing system: It is termed as assigning different cost structure to different products. This

system focuses on the cost of individual product. In small companies like Ovation system, cost

of product and their selling rate plays an important role in generating the profits of the company.

So this costing system ultimately affects the activities which are involved in managing the

financial reports of the business entity. This system is concerned with manufacturing cost of the

product. Different types of products vary in their costs and this variation in costs effects job

costing system of the organization.

B. Various accounting management reports used by Ovation system and importance of such

reports

Business entity uses different types of reports for the company. These reports provide

information regarding cost of product, performance of an employee and budget stated for the

production. The managers of Ovation system require Accounting management reports because

this provides them information’s about various kinds of financial activities (Melnyk and et.al.,

2014). Such reports can be concluded from various departments of an organization. This is

helpful in decision making of the management. Different reports provides comprehensive view

about the management of financial status in business. Following such reports are described

below:

Cost report: This report gives a view about the total cost incurred of a product. This includes

cost of raw material, labour expanses and extra costs in manufacturing the product. Cost report

gives an extracted orientation of all this information in respect with a manufacturing of

commodity. This report is used to ascertain the actual cost of the commodity. This report tells

about the overhead expanses of a product.

2

management of accounting. Inventory is also a kind of management which needs to be managed

properly to get the correct financial reports of the business. Inventory management refers to

keeping the records of production and sale of goods. Stock management identifies the

availability of raw material and finished product in company (Otley, 2015). It deals with demand

and supply of products. Stock of the Ovation system required to be properly managed. Inventory

management consists of keeping information about sale of products and services and stock which

is still available in storage.

Job costing system: It is termed as assigning different cost structure to different products. This

system focuses on the cost of individual product. In small companies like Ovation system, cost

of product and their selling rate plays an important role in generating the profits of the company.

So this costing system ultimately affects the activities which are involved in managing the

financial reports of the business entity. This system is concerned with manufacturing cost of the

product. Different types of products vary in their costs and this variation in costs effects job

costing system of the organization.

B. Various accounting management reports used by Ovation system and importance of such

reports

Business entity uses different types of reports for the company. These reports provide

information regarding cost of product, performance of an employee and budget stated for the

production. The managers of Ovation system require Accounting management reports because

this provides them information’s about various kinds of financial activities (Melnyk and et.al.,

2014). Such reports can be concluded from various departments of an organization. This is

helpful in decision making of the management. Different reports provides comprehensive view

about the management of financial status in business. Following such reports are described

below:

Cost report: This report gives a view about the total cost incurred of a product. This includes

cost of raw material, labour expanses and extra costs in manufacturing the product. Cost report

gives an extracted orientation of all this information in respect with a manufacturing of

commodity. This report is used to ascertain the actual cost of the commodity. This report tells

about the overhead expanses of a product.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Performance report: This report gives an overview about the performance of the company as a

whole. This report also provides the presentation of various departments in organization. It is

facilitates managers in decision making for growth and development of firm. Performance

reports are generally used to estimate the capabilities of the business in and its employees. It is

important for Ovation system in order to improve performance of business and making correct

decision for the successful growth of company.

Budget report: Budget managerial accounting reports are created according to previous data of

business. This is basically an estimated approx. figure which is generated to get an idea about all

the expanses and earnings of business. This report is generated to give an overview about

budgets of company and this budget can be further used for development of the business. Larger

budget of Ovation system can also guide managers to offer incentive plans to their employees. It

possesses a good quality of preparing plans of business activity to achieve common objective.

C. Benefits of types of inventory management and job costing system

Inventory management: These records help to keep information aboutsale and production of

the product. This is very important information which helps in smooth flow of production and

sale of the product. Stock is considered as one of the important assets of company and needs to

be well maintained. So inventory management provides managers with an appropriate

knowledge about managing stock of business. This is helpful in balancing the supply and

demand of product. It is also provides streamlined operations in business. Inventory or stock

management is also involved in adjusting time efficiency in product manufacturing. It reduces

the burden of liabilities in an organization.

Job costing system: This accounting managerial activity helps in providing data about cost of

the product incurred in manufacturing of product. This system is helpful in providing accurate

cost or figures of production. In many SMEs like Ovation system this factor is considered as

source of revenue generation or loses incurred in business (Otley, 2015). This system is helpful

in predicting cost of commodity and labour included in manufacturing of a specific product. It

provides managers with summarised information of direct expenses and cost of labour and

material included to get correct visual idea of company's profits. It determines the profitability of

firm. It controls the comprehensive costing structure of goods and services. It provides the

estimated calculations about profits earned in individual jobs. These operations are carried

against the specific demands of customers.

3

whole. This report also provides the presentation of various departments in organization. It is

facilitates managers in decision making for growth and development of firm. Performance

reports are generally used to estimate the capabilities of the business in and its employees. It is

important for Ovation system in order to improve performance of business and making correct

decision for the successful growth of company.

Budget report: Budget managerial accounting reports are created according to previous data of

business. This is basically an estimated approx. figure which is generated to get an idea about all

the expanses and earnings of business. This report is generated to give an overview about

budgets of company and this budget can be further used for development of the business. Larger

budget of Ovation system can also guide managers to offer incentive plans to their employees. It

possesses a good quality of preparing plans of business activity to achieve common objective.

C. Benefits of types of inventory management and job costing system

Inventory management: These records help to keep information aboutsale and production of

the product. This is very important information which helps in smooth flow of production and

sale of the product. Stock is considered as one of the important assets of company and needs to

be well maintained. So inventory management provides managers with an appropriate

knowledge about managing stock of business. This is helpful in balancing the supply and

demand of product. It is also provides streamlined operations in business. Inventory or stock

management is also involved in adjusting time efficiency in product manufacturing. It reduces

the burden of liabilities in an organization.

Job costing system: This accounting managerial activity helps in providing data about cost of

the product incurred in manufacturing of product. This system is helpful in providing accurate

cost or figures of production. In many SMEs like Ovation system this factor is considered as

source of revenue generation or loses incurred in business (Otley, 2015). This system is helpful

in predicting cost of commodity and labour included in manufacturing of a specific product. It

provides managers with summarised information of direct expenses and cost of labour and

material included to get correct visual idea of company's profits. It determines the profitability of

firm. It controls the comprehensive costing structure of goods and services. It provides the

estimated calculations about profits earned in individual jobs. These operations are carried

against the specific demands of customers.

3

D. Integrated features of management accounting system and management accounting reports in

organization

The role of management accounting in an organization is to support decision-making and

management helps in controlling financial and non-financial activities of business. As this is

helpful in estimating economic status of firm so it effects company's strategies and decision

making policy. This process of estimating the situation of business is identified by preparing

multiple reports of an organization. These accounting reports provides short summary of

information about management and operational activities performed in the entity. So basically

accounting management is a system that has capabilities to manage various activities of different

departments and accounting reports and shows the actual status of business. This way

management accounting plays an important role in the organization. Managers of Ovation

system plan, control and evaluate processing of strategies according to these management

activities and reports of the firm. Cost accounting tracks information related to cost of product

while inventory management estimate demand and supply of a particular product. Management

of these separate activities as a whole is referred as management accounting (Quinn and et.al.,

2018). This can be concluded that process of management accounting is the technique of creating

and using the cost quality and time based information to take effective decisions within the

organization. Overall, controller of an Ovation system contributes in planning decision making

and evaluating the performance of business.

TASK 2

A1. Absorption and marginal costing methods

Absorption costing is a system in which valuing of inventory is done. Expenses related to

manufacturing of specific products are absorbed, that include fixed and variable costs. Overhead

expenses, which are indirect, are considered as inventory's price. This provides an accurate view

of the amount spent on production of inventory and is a method of variable costing (Senftlechner

and Hiebl, 2015). Its results are accurate when it comes to end year inventory. It is also known as

full costing. Elements of absorption costing include:

Direct material

Direct labour

Fixed manufacturing overhead.

4

organization

The role of management accounting in an organization is to support decision-making and

management helps in controlling financial and non-financial activities of business. As this is

helpful in estimating economic status of firm so it effects company's strategies and decision

making policy. This process of estimating the situation of business is identified by preparing

multiple reports of an organization. These accounting reports provides short summary of

information about management and operational activities performed in the entity. So basically

accounting management is a system that has capabilities to manage various activities of different

departments and accounting reports and shows the actual status of business. This way

management accounting plays an important role in the organization. Managers of Ovation

system plan, control and evaluate processing of strategies according to these management

activities and reports of the firm. Cost accounting tracks information related to cost of product

while inventory management estimate demand and supply of a particular product. Management

of these separate activities as a whole is referred as management accounting (Quinn and et.al.,

2018). This can be concluded that process of management accounting is the technique of creating

and using the cost quality and time based information to take effective decisions within the

organization. Overall, controller of an Ovation system contributes in planning decision making

and evaluating the performance of business.

TASK 2

A1. Absorption and marginal costing methods

Absorption costing is a system in which valuing of inventory is done. Expenses related to

manufacturing of specific products are absorbed, that include fixed and variable costs. Overhead

expenses, which are indirect, are considered as inventory's price. This provides an accurate view

of the amount spent on production of inventory and is a method of variable costing (Senftlechner

and Hiebl, 2015). Its results are accurate when it comes to end year inventory. It is also known as

full costing. Elements of absorption costing include:

Direct material

Direct labour

Fixed manufacturing overhead.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Variable manufacturing overhead

The costs which are considered under this method consists of:

Variable selling and administrative

Fixed administrative and selling

Illustration 1: Costs Overview

(Source: Absorption Costing, 2018)

§

Marginal costing is a method in which all variable expenses are included in costs unit and

fixed cost is written off in full as it is not favourable of specific contributions of that period

(Kokubu and Kitada, 2015). It is related to marginal cost and its impact on changes of profits

regarding volume or outcome that creates variation in fixed and variable expenses.

5

The costs which are considered under this method consists of:

Variable selling and administrative

Fixed administrative and selling

Illustration 1: Costs Overview

(Source: Absorption Costing, 2018)

§

Marginal costing is a method in which all variable expenses are included in costs unit and

fixed cost is written off in full as it is not favourable of specific contributions of that period

(Kokubu and Kitada, 2015). It is related to marginal cost and its impact on changes of profits

regarding volume or outcome that creates variation in fixed and variable expenses.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Illustration 2: Marginal costing approaches

(Source: Marginal costing, 2018)

Marginal and direct costing are specified as interchangeable terms. Their key difference is

that expenses which are determined as variable in nature and is covered in marginal expense,

while costs that are fixed in nature come under objective of cost. This is a different technique,

used by managers that have to make decisions and provides them a base for understanding

profitability of various products. Cost behaviour varies across different levels of volumes and

their results.

A2. Preparation of income statements

Using Absorption costing method:

Income Statement of Ovation systems

6

(Source: Marginal costing, 2018)

Marginal and direct costing are specified as interchangeable terms. Their key difference is

that expenses which are determined as variable in nature and is covered in marginal expense,

while costs that are fixed in nature come under objective of cost. This is a different technique,

used by managers that have to make decisions and provides them a base for understanding

profitability of various products. Cost behaviour varies across different levels of volumes and

their results.

A2. Preparation of income statements

Using Absorption costing method:

Income Statement of Ovation systems

6

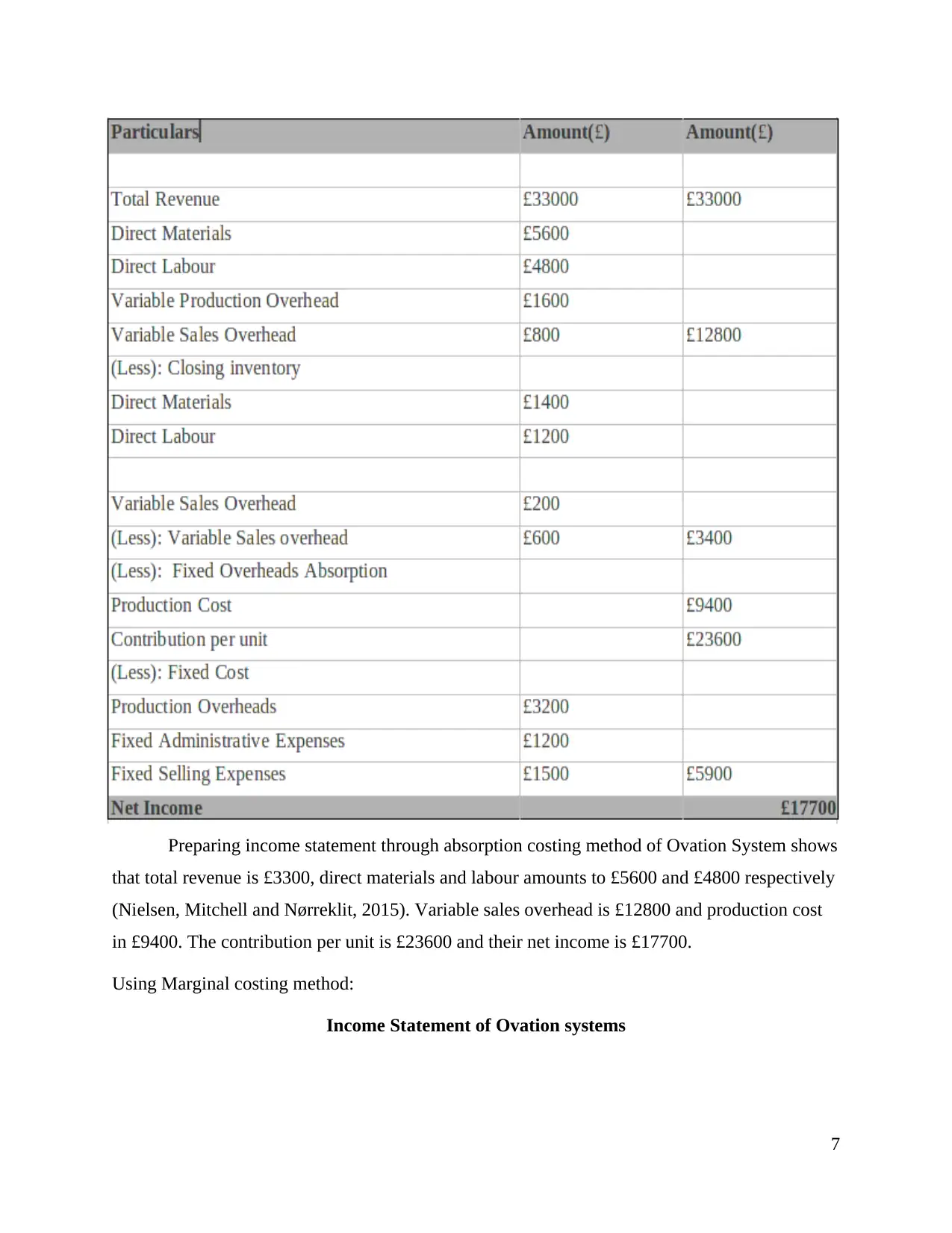

Preparing income statement through absorption costing method of Ovation System shows

that total revenue is £3300, direct materials and labour amounts to £5600 and £4800 respectively

(Nielsen, Mitchell and Nørreklit, 2015). Variable sales overhead is £12800 and production cost

in £9400. The contribution per unit is £23600 and their net income is £17700.

Using Marginal costing method:

Income Statement of Ovation systems

7

that total revenue is £3300, direct materials and labour amounts to £5600 and £4800 respectively

(Nielsen, Mitchell and Nørreklit, 2015). Variable sales overhead is £12800 and production cost

in £9400. The contribution per unit is £23600 and their net income is £17700.

Using Marginal costing method:

Income Statement of Ovation systems

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

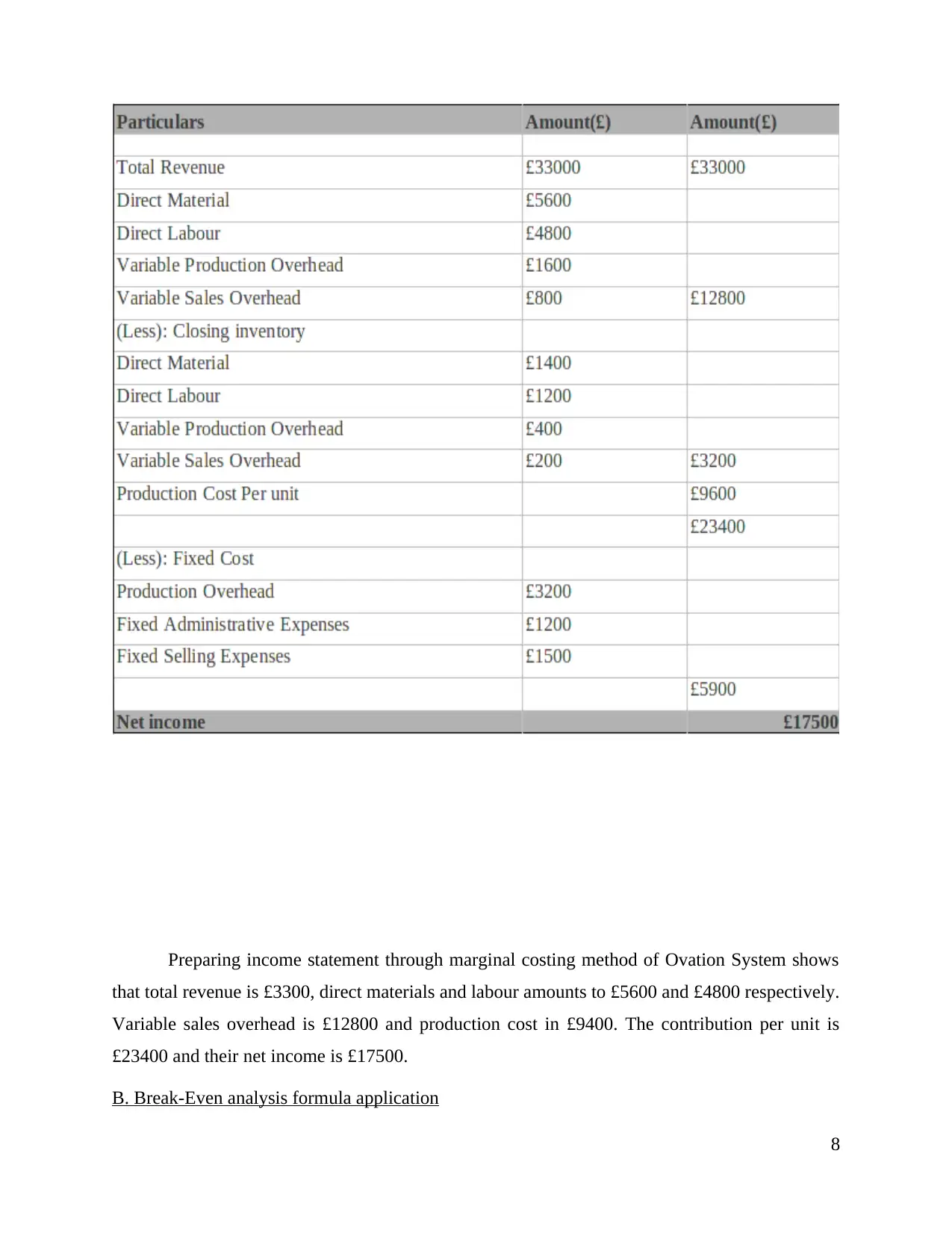

Preparing income statement through marginal costing method of Ovation System shows

that total revenue is £3300, direct materials and labour amounts to £5600 and £4800 respectively.

Variable sales overhead is £12800 and production cost in £9400. The contribution per unit is

£23400 and their net income is £17500.

B. Break-Even analysis formula application

8

that total revenue is £3300, direct materials and labour amounts to £5600 and £4800 respectively.

Variable sales overhead is £12800 and production cost in £9400. The contribution per unit is

£23400 and their net income is £17500.

B. Break-Even analysis formula application

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

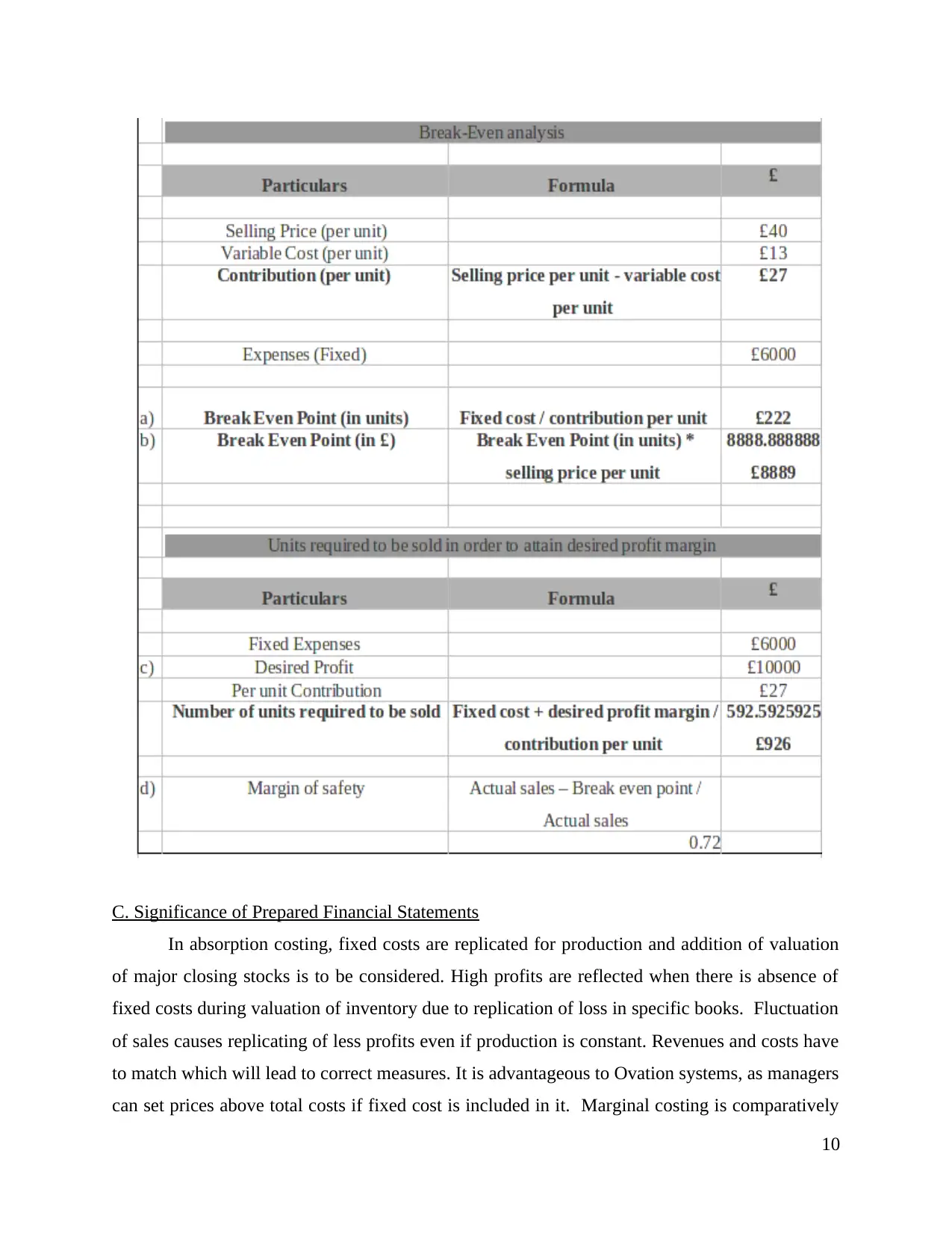

Break even analysis helps in determining what is needed to be sold and how costs are to

be covered while running business operations (Van der Stede, 2015). Its formula calculates total

number of units that have to be sold so that company can generate enough revenues to cover all

expenses.

Break Even Point in units = Fixed Costs/ Sales Price per Unit – Variable Cost per Unit.

Or Break-Even Point in £ = Sales Price per Unit x Break Even point in units

The average per unit sales price, cost and monthly fixed costs are analysed. Ovation

Systems has a selling price of £40 per unit and variable cost of £13 which leads to a contribution

of £27 each. Their fixed expense amounts to £6000. Breakeven point is £8889 with £222 per unit

contribution. If they want to aim at achieving a desired profit of £10000, they have to contribute

£926 per unit.

9

be covered while running business operations (Van der Stede, 2015). Its formula calculates total

number of units that have to be sold so that company can generate enough revenues to cover all

expenses.

Break Even Point in units = Fixed Costs/ Sales Price per Unit – Variable Cost per Unit.

Or Break-Even Point in £ = Sales Price per Unit x Break Even point in units

The average per unit sales price, cost and monthly fixed costs are analysed. Ovation

Systems has a selling price of £40 per unit and variable cost of £13 which leads to a contribution

of £27 each. Their fixed expense amounts to £6000. Breakeven point is £8889 with £222 per unit

contribution. If they want to aim at achieving a desired profit of £10000, they have to contribute

£926 per unit.

9

C. Significance of Prepared Financial Statements

In absorption costing, fixed costs are replicated for production and addition of valuation

of major closing stocks is to be considered. High profits are reflected when there is absence of

fixed costs during valuation of inventory due to replication of loss in specific books. Fluctuation

of sales causes replicating of less profits even if production is constant. Revenues and costs have

to match which will lead to correct measures. It is advantageous to Ovation systems, as managers

can set prices above total costs if fixed cost is included in it. Marginal costing is comparatively

10

In absorption costing, fixed costs are replicated for production and addition of valuation

of major closing stocks is to be considered. High profits are reflected when there is absence of

fixed costs during valuation of inventory due to replication of loss in specific books. Fluctuation

of sales causes replicating of less profits even if production is constant. Revenues and costs have

to match which will lead to correct measures. It is advantageous to Ovation systems, as managers

can set prices above total costs if fixed cost is included in it. Marginal costing is comparatively

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.