Management Accounting Report: Systems, Costing, and Financial Analysis

VerifiedAdded on 2020/07/23

|17

|5260

|37

Report

AI Summary

This report delves into the realm of management accounting, exploring its vital role in organizational decision-making, particularly for a grocery business, Unicorn, operating in Manchester, England. It commences with an introduction to management accounting and its importance in recording and analyzing financial data for both short-term and long-term strategic decisions. The report then examines various management accounting systems, including inventory management, cost accounting, job costing, and price optimization, highlighting their advantages and disadvantages. Following this, the report explores different management accounting reporting methods, such as performance reports, inventory control reports, budget reporting, job cost reporting, and variable analysis reporting. The report then compares marginal and absorption costing methods, detailing their differences in cost recognition and impact on profitability. Finally, the report examines the merits and demerits of planning tools used in budgetary control and discusses the adoption of management accounting systems in addressing financial problems, concluding with a summary of the key findings and recommendations.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1 ..........................................................................................................................................1

P1 Different kind of management accounting systems...............................................................1

P2 Methods for management accounting reporting ...................................................................3

TASK2.............................................................................................................................................5

P3 Comparison between marginal and absorption costing.........................................................5

TASK3.............................................................................................................................................9

P4 Merit and demerit of different kind of planning tools which are used in budgetary control. 9

P5 Adoption of management accounting systems for responding financial problems ............11

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

.......................................................................................................................................................15

INTRODUCTION...........................................................................................................................1

TASK 1 ..........................................................................................................................................1

P1 Different kind of management accounting systems...............................................................1

P2 Methods for management accounting reporting ...................................................................3

TASK2.............................................................................................................................................5

P3 Comparison between marginal and absorption costing.........................................................5

TASK3.............................................................................................................................................9

P4 Merit and demerit of different kind of planning tools which are used in budgetary control. 9

P5 Adoption of management accounting systems for responding financial problems ............11

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

.......................................................................................................................................................15

INTRODUCTION

A process where different financial data is recorded and analysed in termed as

management accounting. It is very popular is modern era because it assist in making short as

well as long term decisions which can help an organisation in achieving their mission and vision.

It support all the department of an enterprise by giving them appropriate advice so they can find

their flaws and deliver better results. Unicorn is a company which is operating in grocery

industry. They sell organisation food and other eatables in Manchester, England. This file will

discuss about various kind of systems of management accounting. Different method of reporting

will also become part of this report (Ward, 2012). Planning tools, their merits and demerits,

which are used in budgetary tool will get cover under this assignment. Comparison of adaption

of management accounting in order to face financial problems will be included in this project.

TASK 1

P1 Different kind of management accounting systems

The main reason for adopting an accounting technique in an organisation is to record

various types of data so managers can use them in upcoming time for planning their future

activities. With time the some major improvements happened in this filed and companies

introduced management accounting in their enterprise because it assist them in reduction cost of

their business operations and support them in finding the areas which can help them in earning

more profits. This system play significant role in making long term decision which has either

direct or indirect connection with organisation's vision. Normally people think that it is only

related to finance division but this perception is wrong because this technique assist in other

activities like monitoring risk, formation of business strategies etc. Management accounting is

important for other departments like human resource, IT and production. It is involved in day to

day operation of a company and analyse current trends as well as cash-flow (Parker, 2012).

An enterprise has option to adopt any kind of accounting system, it depends on their need

and way of doing business. Management accounting also has many advantages and

disadvantages. It can help a small firm in locating the areas where they can reduce their cost,

they have limited finds so it is very important for them to management their money properly and

invest them in right direction. This will also stop them from moving in wrong direction which is

a common mistake done by small and new businesses. This system can also provide them

1

A process where different financial data is recorded and analysed in termed as

management accounting. It is very popular is modern era because it assist in making short as

well as long term decisions which can help an organisation in achieving their mission and vision.

It support all the department of an enterprise by giving them appropriate advice so they can find

their flaws and deliver better results. Unicorn is a company which is operating in grocery

industry. They sell organisation food and other eatables in Manchester, England. This file will

discuss about various kind of systems of management accounting. Different method of reporting

will also become part of this report (Ward, 2012). Planning tools, their merits and demerits,

which are used in budgetary tool will get cover under this assignment. Comparison of adaption

of management accounting in order to face financial problems will be included in this project.

TASK 1

P1 Different kind of management accounting systems

The main reason for adopting an accounting technique in an organisation is to record

various types of data so managers can use them in upcoming time for planning their future

activities. With time the some major improvements happened in this filed and companies

introduced management accounting in their enterprise because it assist them in reduction cost of

their business operations and support them in finding the areas which can help them in earning

more profits. This system play significant role in making long term decision which has either

direct or indirect connection with organisation's vision. Normally people think that it is only

related to finance division but this perception is wrong because this technique assist in other

activities like monitoring risk, formation of business strategies etc. Management accounting is

important for other departments like human resource, IT and production. It is involved in day to

day operation of a company and analyse current trends as well as cash-flow (Parker, 2012).

An enterprise has option to adopt any kind of accounting system, it depends on their need

and way of doing business. Management accounting also has many advantages and

disadvantages. It can help a small firm in locating the areas where they can reduce their cost,

they have limited finds so it is very important for them to management their money properly and

invest them in right direction. This will also stop them from moving in wrong direction which is

a common mistake done by small and new businesses. This system can also provide them

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

significant assistance in managing their cash-flow appropriately so they by predict their future

expense and income. If they will has a clear picture of these two important elements of business

than they can do optimum utilisation of their available resources. This will help them in

triggering the useless expenditure which can be invested in other areas (Renz, 2016). One of the

major disadvantage of this management accounting technique is that its installation is bit costly

so it can not be adopted by every organisation. Necessary requirement of various kind of

management accounting method is as follows:

Inventory management system – This process focuses on quality and quantity of stock.

It is involved with planning of various arrangements which are essential for timely deliver of

goods. Inventory is managed in a way that the cost of keeping the stock goes down and problems

relating to under or over stocking minimises. It can be done by using a software, but small

organisations like Unicorn groceries can also adopt manual method because they do not need

expensive soft-wares as their area of operation is very limited.

Cost accounting system – This process concentrate on minimising the cost of business

so company can increase their profit in long run. Profitability analysis is its essential part where

manager compare the expenditure they will do on an activity and the return it will deliver in a set

period of time (Fullerton, Kennedy and Widener, 2014). Valuation of inventory and controlling

of cost are other areas where this system focuses.

Job costing technique – It is generally used when an organisation produces different

products so they try to determine their cost either on the individual basis or by allocating cost to

a batch. For example a small firm like Unicorn can adopt this in their company because it will

help them in bifurcation the cost of various organic item which they are selling in their outlets. If

they were selling similar or only one commodity than they could prefer process costing but they

produce variety of products.

Price optimisation – In this system an organisation try to find an appropriate price which

customers are ready to pay and company is happy to sell goods on that value. This can be done

by analysing market and expenditure incurred in production. If they charge more money for a

product than its demand will go down, if they sell it at less price than the revenue which they

could earn will decrease. This system help in determining a price of a commodity which is

favourable for both sides. An enterprise can make quality goods but if they do not adopt correct

method of pricing than they can face severe losses. It can become main reason for failure of an

2

expense and income. If they will has a clear picture of these two important elements of business

than they can do optimum utilisation of their available resources. This will help them in

triggering the useless expenditure which can be invested in other areas (Renz, 2016). One of the

major disadvantage of this management accounting technique is that its installation is bit costly

so it can not be adopted by every organisation. Necessary requirement of various kind of

management accounting method is as follows:

Inventory management system – This process focuses on quality and quantity of stock.

It is involved with planning of various arrangements which are essential for timely deliver of

goods. Inventory is managed in a way that the cost of keeping the stock goes down and problems

relating to under or over stocking minimises. It can be done by using a software, but small

organisations like Unicorn groceries can also adopt manual method because they do not need

expensive soft-wares as their area of operation is very limited.

Cost accounting system – This process concentrate on minimising the cost of business

so company can increase their profit in long run. Profitability analysis is its essential part where

manager compare the expenditure they will do on an activity and the return it will deliver in a set

period of time (Fullerton, Kennedy and Widener, 2014). Valuation of inventory and controlling

of cost are other areas where this system focuses.

Job costing technique – It is generally used when an organisation produces different

products so they try to determine their cost either on the individual basis or by allocating cost to

a batch. For example a small firm like Unicorn can adopt this in their company because it will

help them in bifurcation the cost of various organic item which they are selling in their outlets. If

they were selling similar or only one commodity than they could prefer process costing but they

produce variety of products.

Price optimisation – In this system an organisation try to find an appropriate price which

customers are ready to pay and company is happy to sell goods on that value. This can be done

by analysing market and expenditure incurred in production. If they charge more money for a

product than its demand will go down, if they sell it at less price than the revenue which they

could earn will decrease. This system help in determining a price of a commodity which is

favourable for both sides. An enterprise can make quality goods but if they do not adopt correct

method of pricing than they can face severe losses. It can become main reason for failure of an

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

item (Christ and Burritt, 2013). Response of customers is recorded under this system by using

different channels.

P2 Methods for management accounting reporting

An organisation can use various kind of management accounting reports which can help

them in collecting data that can be used in upcoming time. Below are some methods which are

used in reporting:

Performance report – Employees are considered as one of the most importance resource

that is present in a company. In this methods their performance is measured in regular interval of

time so their shortcoming can be identified and removed in order to improve their efficiency in

upcoming time. An annual report relating to performance can help in determining the success or

failure of a project. It can be done by comparing allotted budget and actual expenditure or

income. If cited organisation check various performance on continuous basis than they can solve

various issues at the point of its generation which can help them in concentrating on their long as

well as short term objectives.

Inventory control report – Inventory is a significant part of a business, this report record

all the activities relating to this activity like deliver of goods, storage, etc. It provide information

about under-stocking which can make a huge impact on supply chain (Lambert and Sponem,

2012). Troubles relating to overstocking are also become part of this report because, indirectly, it

3

different channels.

P2 Methods for management accounting reporting

An organisation can use various kind of management accounting reports which can help

them in collecting data that can be used in upcoming time. Below are some methods which are

used in reporting:

Performance report – Employees are considered as one of the most importance resource

that is present in a company. In this methods their performance is measured in regular interval of

time so their shortcoming can be identified and removed in order to improve their efficiency in

upcoming time. An annual report relating to performance can help in determining the success or

failure of a project. It can be done by comparing allotted budget and actual expenditure or

income. If cited organisation check various performance on continuous basis than they can solve

various issues at the point of its generation which can help them in concentrating on their long as

well as short term objectives.

Inventory control report – Inventory is a significant part of a business, this report record

all the activities relating to this activity like deliver of goods, storage, etc. It provide information

about under-stocking which can make a huge impact on supply chain (Lambert and Sponem,

2012). Troubles relating to overstocking are also become part of this report because, indirectly, it

3

enhances of cost of a product. Techniques like economic order quantity are beneficial for this

issue. Company can also think about activity based costing whose effectiveness still do not face

any big issue. Incidents like short of goods or raw material are reported in this system which can

decrease the profit of an enterprise. Cited organisation can save lot of money if they make an

effective system for controlling inventory. They can reduce their carrying and storing cost and

deliver supply their products by avoiding any kind of delaying.

Budget reporting – This report is based on the income which an organisation has earned

in their business (Taipaleenmäki and Ikäheimo, 2013). They compare their set targets with latest

figure in order to report the actual situation. Expenses that is occurred in previous year is also

become part of this method. It support in allocating the area where company can reduce their

cost and divert this money in right direction. Normally a enterprise have various departments,

their individual performance can be analysed by this method. It can help in distribution of

incentives because managers can compare set goals of a division or employee from their actual

achievement and than take decisions relating to increment. This will help Unicorn in determining

their actual position where they are standing, it will also support them in finding the areas where

they need improvement so they can stop committing same mistakes more than once and invest

their available resources in right direction.

Job cost reporting – In this report, the cost incurred on every job is reported. It contain

expenses related to labour, raw material and various overheads which has occurred on a project.

This will give crucial information relating to profitability by providing cost of every single unit

which can be compared from earn by each of them. Cited organisation an shut down the projects

which are not delivering return according to their exception or they can find the loophole in the

complete system so they can remove it can increase its efficiency in upcoming time.

Variable analysis reporting – This report is based on variable factors, they have ability to

make a significant impact on business so they are considered as the time of decision making.

Variable cost fluctuates from time time, it is important to find the reason of variation in order to

bring down the cost and reduce wastage of necessary resources. This will help an organisation in

making a proper control on the recurring expenditure which is essential for stability of the

organisation.

4

issue. Company can also think about activity based costing whose effectiveness still do not face

any big issue. Incidents like short of goods or raw material are reported in this system which can

decrease the profit of an enterprise. Cited organisation can save lot of money if they make an

effective system for controlling inventory. They can reduce their carrying and storing cost and

deliver supply their products by avoiding any kind of delaying.

Budget reporting – This report is based on the income which an organisation has earned

in their business (Taipaleenmäki and Ikäheimo, 2013). They compare their set targets with latest

figure in order to report the actual situation. Expenses that is occurred in previous year is also

become part of this method. It support in allocating the area where company can reduce their

cost and divert this money in right direction. Normally a enterprise have various departments,

their individual performance can be analysed by this method. It can help in distribution of

incentives because managers can compare set goals of a division or employee from their actual

achievement and than take decisions relating to increment. This will help Unicorn in determining

their actual position where they are standing, it will also support them in finding the areas where

they need improvement so they can stop committing same mistakes more than once and invest

their available resources in right direction.

Job cost reporting – In this report, the cost incurred on every job is reported. It contain

expenses related to labour, raw material and various overheads which has occurred on a project.

This will give crucial information relating to profitability by providing cost of every single unit

which can be compared from earn by each of them. Cited organisation an shut down the projects

which are not delivering return according to their exception or they can find the loophole in the

complete system so they can remove it can increase its efficiency in upcoming time.

Variable analysis reporting – This report is based on variable factors, they have ability to

make a significant impact on business so they are considered as the time of decision making.

Variable cost fluctuates from time time, it is important to find the reason of variation in order to

bring down the cost and reduce wastage of necessary resources. This will help an organisation in

making a proper control on the recurring expenditure which is essential for stability of the

organisation.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TASK2

P3 Comparison between marginal and absorption costing

Cost incurred on various activities should be calculated and analysed because it can help

in controlling the expenditure which is done by cited organisation. It can make a signifiant

impact on revenue of company because if their expenses will be high than their profit will go

down (Boitier and Rivière, 2013). Unicorn can consider following types of costing for optimum

utilisation of available resources:

Marginal costing – It is the cost that is incurred on manufacturing of an extra unit. Under

this costing, fixed cost is ignored and only variable cost in taken in account at the time of

decision making process. It focuses on expenditure relating to material and labour, selling

expenses are also included at the time of determination of cost. It clarify the difference between

fixed and variable cost and its main area of focus is expenditure which changes from time to

time. It has capacity to play crucial role in increasing the profitability of cited organisation before

fixed expenses can not make any short term impact on the business but variables expenses can

enhance revenue of a company because managers can find a way to minimise them in order to

earn more profit (Gaizauskas and Martinavicius, 2013). Marginal cost is important for

determining the price of a product, if variable cost is going down than cited organisation can

decrease price of their organisation goods which can increase their sale in long run. An enterprise

can tock can do valuation of their inventory by adopting this method.

Absorption costing – In this method, both fixed and variable cost is included as they

become part of total expenditure. Fixed cost do not fluctuates, it remains same in every situation

and it is considered as the time of distribution of expenses. It cover complete area which is the

main reason that it is also called fulling costing. Variable cost is also included in this method

which can change every years. In mainly incudes wages of employees, expenditure on raw

material and other direct expenses.

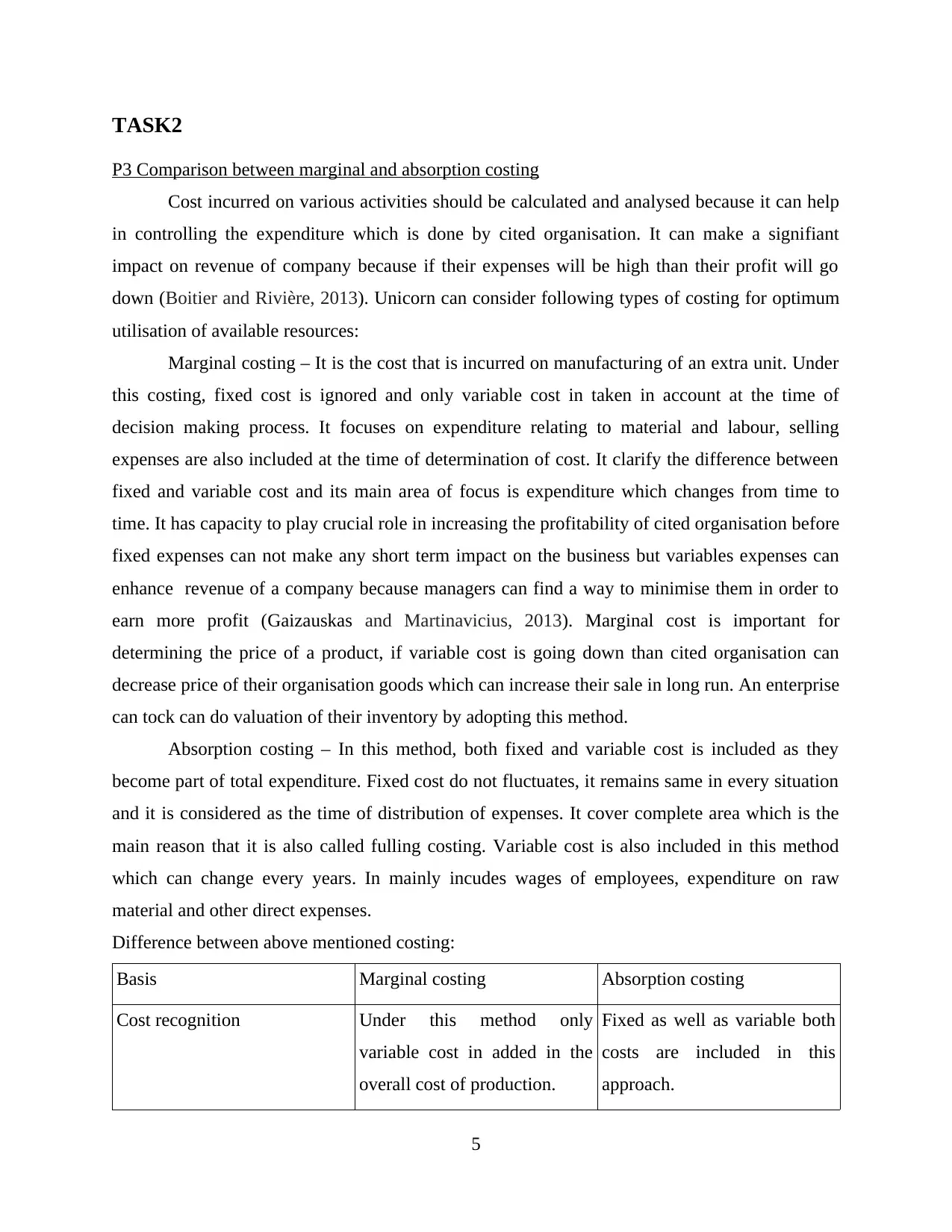

Difference between above mentioned costing:

Basis Marginal costing Absorption costing

Cost recognition Under this method only

variable cost in added in the

overall cost of production.

Fixed as well as variable both

costs are included in this

approach.

5

P3 Comparison between marginal and absorption costing

Cost incurred on various activities should be calculated and analysed because it can help

in controlling the expenditure which is done by cited organisation. It can make a signifiant

impact on revenue of company because if their expenses will be high than their profit will go

down (Boitier and Rivière, 2013). Unicorn can consider following types of costing for optimum

utilisation of available resources:

Marginal costing – It is the cost that is incurred on manufacturing of an extra unit. Under

this costing, fixed cost is ignored and only variable cost in taken in account at the time of

decision making process. It focuses on expenditure relating to material and labour, selling

expenses are also included at the time of determination of cost. It clarify the difference between

fixed and variable cost and its main area of focus is expenditure which changes from time to

time. It has capacity to play crucial role in increasing the profitability of cited organisation before

fixed expenses can not make any short term impact on the business but variables expenses can

enhance revenue of a company because managers can find a way to minimise them in order to

earn more profit (Gaizauskas and Martinavicius, 2013). Marginal cost is important for

determining the price of a product, if variable cost is going down than cited organisation can

decrease price of their organisation goods which can increase their sale in long run. An enterprise

can tock can do valuation of their inventory by adopting this method.

Absorption costing – In this method, both fixed and variable cost is included as they

become part of total expenditure. Fixed cost do not fluctuates, it remains same in every situation

and it is considered as the time of distribution of expenses. It cover complete area which is the

main reason that it is also called fulling costing. Variable cost is also included in this method

which can change every years. In mainly incudes wages of employees, expenditure on raw

material and other direct expenses.

Difference between above mentioned costing:

Basis Marginal costing Absorption costing

Cost recognition Under this method only

variable cost in added in the

overall cost of production.

Fixed as well as variable both

costs are included in this

approach.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

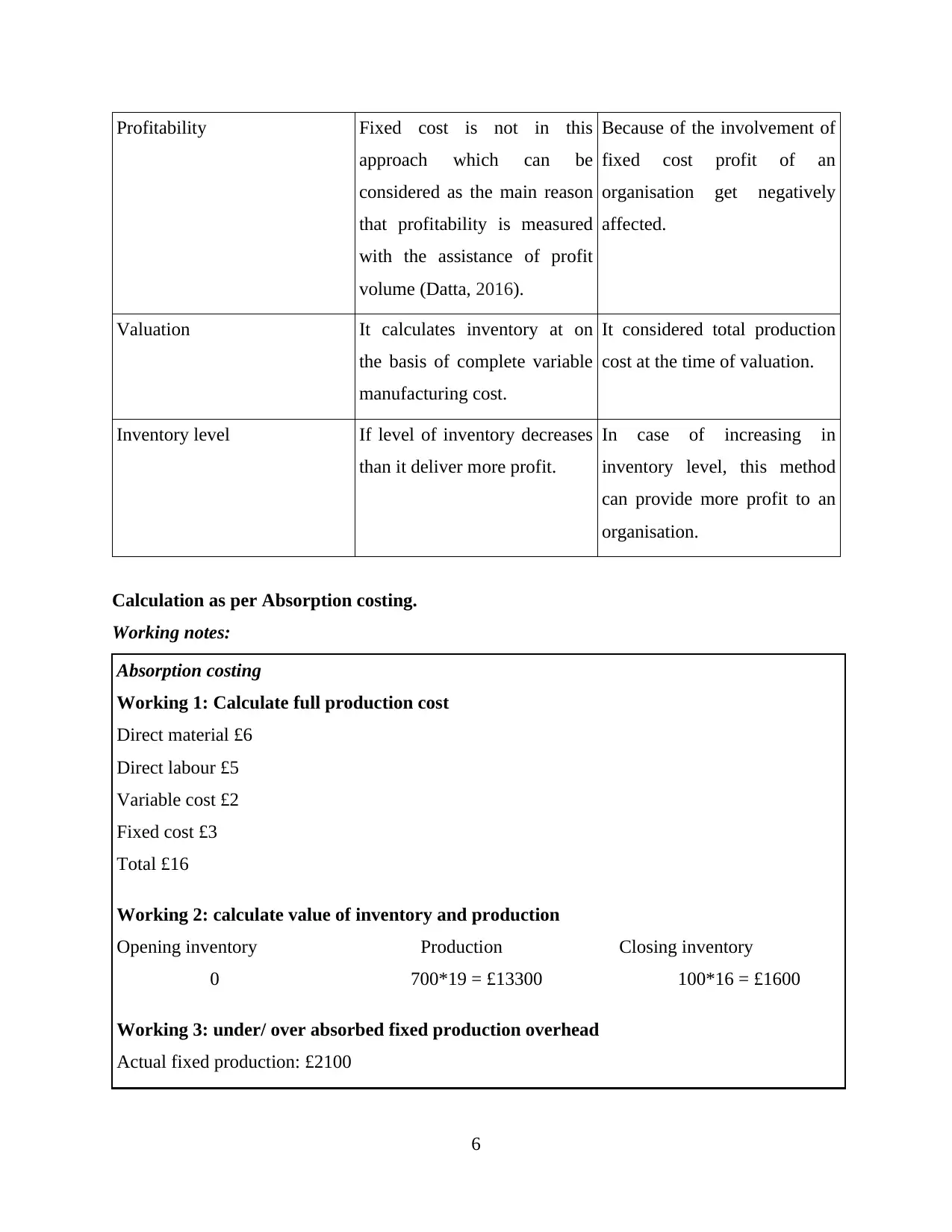

Profitability Fixed cost is not in this

approach which can be

considered as the main reason

that profitability is measured

with the assistance of profit

volume (Datta, 2016).

Because of the involvement of

fixed cost profit of an

organisation get negatively

affected.

Valuation It calculates inventory at on

the basis of complete variable

manufacturing cost.

It considered total production

cost at the time of valuation.

Inventory level If level of inventory decreases

than it deliver more profit.

In case of increasing in

inventory level, this method

can provide more profit to an

organisation.

Calculation as per Absorption costing.

Working notes:

Absorption costing

Working 1: Calculate full production cost

Direct material £6

Direct labour £5

Variable cost £2

Fixed cost £3

Total £16

Working 2: calculate value of inventory and production

Opening inventory Production Closing inventory

0 700*19 = £13300 100*16 = £1600

Working 3: under/ over absorbed fixed production overhead

Actual fixed production: £2100

6

approach which can be

considered as the main reason

that profitability is measured

with the assistance of profit

volume (Datta, 2016).

Because of the involvement of

fixed cost profit of an

organisation get negatively

affected.

Valuation It calculates inventory at on

the basis of complete variable

manufacturing cost.

It considered total production

cost at the time of valuation.

Inventory level If level of inventory decreases

than it deliver more profit.

In case of increasing in

inventory level, this method

can provide more profit to an

organisation.

Calculation as per Absorption costing.

Working notes:

Absorption costing

Working 1: Calculate full production cost

Direct material £6

Direct labour £5

Variable cost £2

Fixed cost £3

Total £16

Working 2: calculate value of inventory and production

Opening inventory Production Closing inventory

0 700*19 = £13300 100*16 = £1600

Working 3: under/ over absorbed fixed production overhead

Actual fixed production: £2100

6

Fixed overhead: £2000

Total £100(over absorbed)

Administration Cost: In this budgeted cost is £800 and Actual cost is £700

Selling cost: In this budgeted cost is £400 and Actual cost is £600

Net profit using absorption costing £ £

Sales

(-) Cost of Sales:

Opening stock

Manufacturing

Closing stock

(Under)/ Over absorbed fixed prod.

O/h

Gross Profit

Less Expenses

Variable sales expenditure

Fixed administration expenses

Fixed selling expenditure

Over absorption

Net Profit

0

11200

(1600)

600

700

600

(100)

21000

(9600)

11400

(1800)

9600

Working 1: Calculate variable production cost £

Direct material 6

Direct labour 5

Variable production O/h 3

Variable production cost 14

Working 2: Calculate value of inventory and production

Opening inventory Production Closing inventory

7

Total £100(over absorbed)

Administration Cost: In this budgeted cost is £800 and Actual cost is £700

Selling cost: In this budgeted cost is £400 and Actual cost is £600

Net profit using absorption costing £ £

Sales

(-) Cost of Sales:

Opening stock

Manufacturing

Closing stock

(Under)/ Over absorbed fixed prod.

O/h

Gross Profit

Less Expenses

Variable sales expenditure

Fixed administration expenses

Fixed selling expenditure

Over absorption

Net Profit

0

11200

(1600)

600

700

600

(100)

21000

(9600)

11400

(1800)

9600

Working 1: Calculate variable production cost £

Direct material 6

Direct labour 5

Variable production O/h 3

Variable production cost 14

Working 2: Calculate value of inventory and production

Opening inventory Production Closing inventory

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

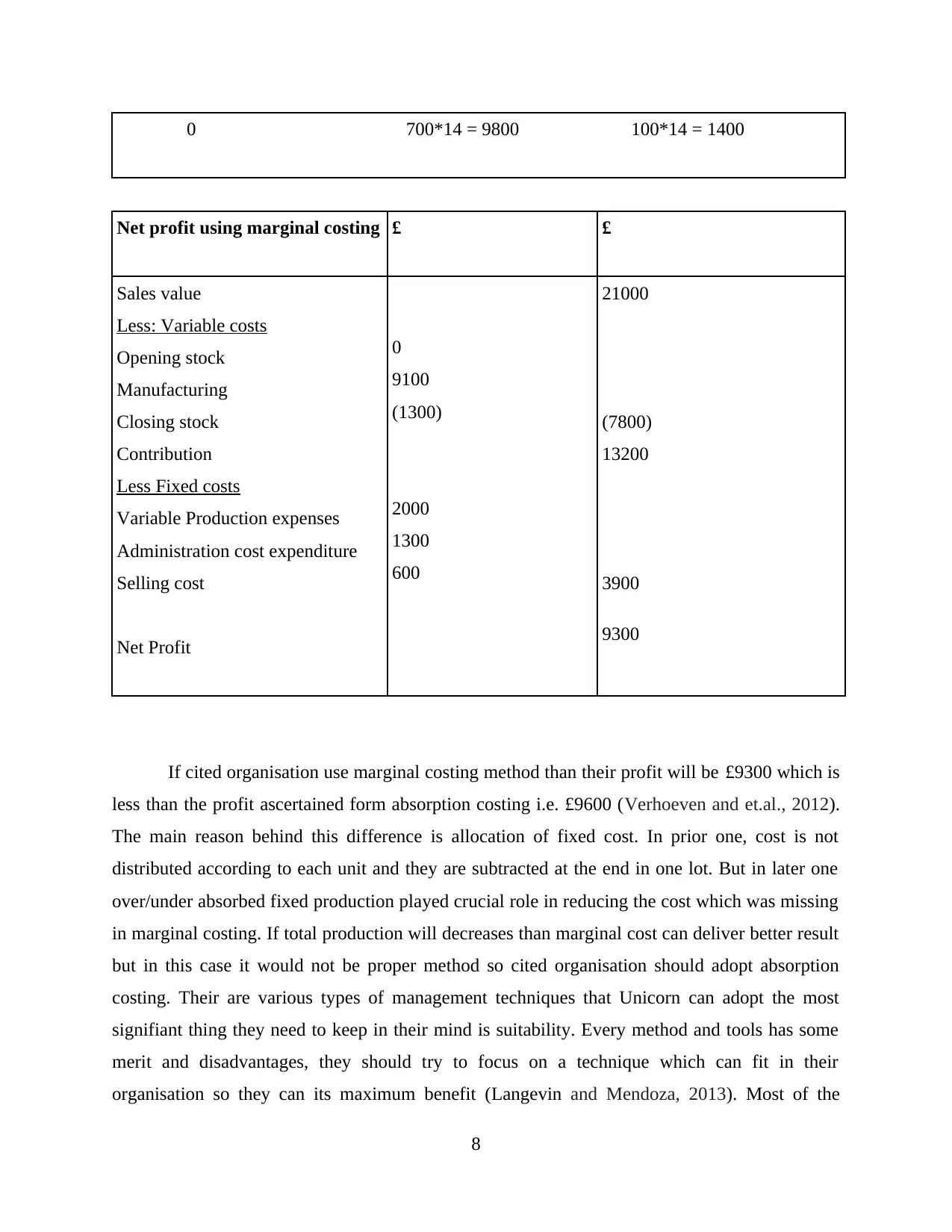

0 700*14 = 9800 100*14 = 1400

Net profit using marginal costing £ £

Sales value

Less: Variable costs

Opening stock

Manufacturing

Closing stock

Contribution

Less Fixed costs

Variable Production expenses

Administration cost expenditure

Selling cost

Net Profit

0

9100

(1300)

2000

1300

600

21000

(7800)

13200

3900

9300

If cited organisation use marginal costing method than their profit will be £9300 which is

less than the profit ascertained form absorption costing i.e. £9600 (Verhoeven and et.al., 2012).

The main reason behind this difference is allocation of fixed cost. In prior one, cost is not

distributed according to each unit and they are subtracted at the end in one lot. But in later one

over/under absorbed fixed production played crucial role in reducing the cost which was missing

in marginal costing. If total production will decreases than marginal cost can deliver better result

but in this case it would not be proper method so cited organisation should adopt absorption

costing. Their are various types of management techniques that Unicorn can adopt the most

signifiant thing they need to keep in their mind is suitability. Every method and tools has some

merit and disadvantages, they should try to focus on a technique which can fit in their

organisation so they can its maximum benefit (Langevin and Mendoza, 2013). Most of the

8

Net profit using marginal costing £ £

Sales value

Less: Variable costs

Opening stock

Manufacturing

Closing stock

Contribution

Less Fixed costs

Variable Production expenses

Administration cost expenditure

Selling cost

Net Profit

0

9100

(1300)

2000

1300

600

21000

(7800)

13200

3900

9300

If cited organisation use marginal costing method than their profit will be £9300 which is

less than the profit ascertained form absorption costing i.e. £9600 (Verhoeven and et.al., 2012).

The main reason behind this difference is allocation of fixed cost. In prior one, cost is not

distributed according to each unit and they are subtracted at the end in one lot. But in later one

over/under absorbed fixed production played crucial role in reducing the cost which was missing

in marginal costing. If total production will decreases than marginal cost can deliver better result

but in this case it would not be proper method so cited organisation should adopt absorption

costing. Their are various types of management techniques that Unicorn can adopt the most

signifiant thing they need to keep in their mind is suitability. Every method and tools has some

merit and disadvantages, they should try to focus on a technique which can fit in their

organisation so they can its maximum benefit (Langevin and Mendoza, 2013). Most of the

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

elements under both costing approach are same but the main difference occur because of fixed

cost which is allocated in under absorption costing but it is ignore in marginal.

TASK3

P4 Merit and demerit of different kind of planning tools which are used in budgetary control

Budget control relates to monitoring various operations which are present in a business, it

also deals with controlling of cost for a particular accounting period. Managers of cited

organisation can compare their actual performance and records with set financial and other goals

so they can determine the variance and make necessary changes in upcoming time. This will

assist them in optimum utilisation of the resources which are present in company so they can

minimise the waste and invest saved money in appropriate direction. One of the main advantage

of budgetary control is that it can support cited firm in evaluating the performance of their

employees which are their significant resource (Ueckerdt and et.al., 2013). They can find the

their mistakes and work on them in upcoming time, it will also help company in determining the

right amount of incentives because if a worker achieved his/her target than he/she should get

more incentives compare to other who missed his/her goals.

It can also support in making strong coordination between various levels and departments

so an organisation can work with their full efficiency and reach their objectives in short period of

9

cost which is allocated in under absorption costing but it is ignore in marginal.

TASK3

P4 Merit and demerit of different kind of planning tools which are used in budgetary control

Budget control relates to monitoring various operations which are present in a business, it

also deals with controlling of cost for a particular accounting period. Managers of cited

organisation can compare their actual performance and records with set financial and other goals

so they can determine the variance and make necessary changes in upcoming time. This will

assist them in optimum utilisation of the resources which are present in company so they can

minimise the waste and invest saved money in appropriate direction. One of the main advantage

of budgetary control is that it can support cited firm in evaluating the performance of their

employees which are their significant resource (Ueckerdt and et.al., 2013). They can find the

their mistakes and work on them in upcoming time, it will also help company in determining the

right amount of incentives because if a worker achieved his/her target than he/she should get

more incentives compare to other who missed his/her goals.

It can also support in making strong coordination between various levels and departments

so an organisation can work with their full efficiency and reach their objectives in short period of

9

time. Budgetary control also has some disadvantages, it is a lengthy process and most of the

organisations do not have much time to waste of planning because they give more importance to

execution. It also involve huge cost which small and medium enterprises can not afford because

they do not have deep pockets so they have to invest their money in right areas (Rumble, 2012).

Budget is prepared on the basis of estimation, its accuracy has a big question mark which is the

main reason that managers do not like high dependence on budget. Unicorn can consider

following planning tools for budgetary control:

Master budget – It covers all the part of an organisation which is the main reason that it

is known as master budget. It is made for long term but this does not mean that it ignore day to

day operation because they are signifiant for achieving bigger objectives. Normally a planning

tool assist one or two department but this budget help all the division of an enterprise by showing

them right track which they have to following in current scenario and in upcoming time. It has

direct relation with strategic planning which includes capital investment, sales, expenses, etc.

One of the prime merit of this budget is that it depicts big picture which is necessary for

achieving mission of an organisation (Schaber, Steinke and Hamacher, 2012). It covers all

department so it can support in proper synchronisation of all division which can give surprising

results in forthcoming time. It also has many disadvantages, formation of master budget is very

time consuming process which can takes years. If a company is operating in more than one

country and they are present in various industry than this planning tools will not be effective. It is

very costly so small, micro and medium enterprises can not afford it.

Cash flow budgeting – All the transaction that has direct or indirect relation with cash

are recorded under cash-flow statement. It assist in optimum utilisation of cash which is

available n the organisation so company can pay their suppliers in right time and reduce the

wastages of liquid assets. Some manager do not support this planning tools because they do not

think that it can tell the exact amount which they will be needing in a particular time as situation

of market changes in very short period of time.

Variable analysis budget – This planning tool focuses on variable factors which are

necessary which play signifiant role in increasing profit of an organisation (Hirth, 2013.). These

factors changes from time to time so elements like raw material cost also get altered. It do not

involves fixed expenditure and investment which can be considered as its main disadvantage.

10

organisations do not have much time to waste of planning because they give more importance to

execution. It also involve huge cost which small and medium enterprises can not afford because

they do not have deep pockets so they have to invest their money in right areas (Rumble, 2012).

Budget is prepared on the basis of estimation, its accuracy has a big question mark which is the

main reason that managers do not like high dependence on budget. Unicorn can consider

following planning tools for budgetary control:

Master budget – It covers all the part of an organisation which is the main reason that it

is known as master budget. It is made for long term but this does not mean that it ignore day to

day operation because they are signifiant for achieving bigger objectives. Normally a planning

tool assist one or two department but this budget help all the division of an enterprise by showing

them right track which they have to following in current scenario and in upcoming time. It has

direct relation with strategic planning which includes capital investment, sales, expenses, etc.

One of the prime merit of this budget is that it depicts big picture which is necessary for

achieving mission of an organisation (Schaber, Steinke and Hamacher, 2012). It covers all

department so it can support in proper synchronisation of all division which can give surprising

results in forthcoming time. It also has many disadvantages, formation of master budget is very

time consuming process which can takes years. If a company is operating in more than one

country and they are present in various industry than this planning tools will not be effective. It is

very costly so small, micro and medium enterprises can not afford it.

Cash flow budgeting – All the transaction that has direct or indirect relation with cash

are recorded under cash-flow statement. It assist in optimum utilisation of cash which is

available n the organisation so company can pay their suppliers in right time and reduce the

wastages of liquid assets. Some manager do not support this planning tools because they do not

think that it can tell the exact amount which they will be needing in a particular time as situation

of market changes in very short period of time.

Variable analysis budget – This planning tool focuses on variable factors which are

necessary which play signifiant role in increasing profit of an organisation (Hirth, 2013.). These

factors changes from time to time so elements like raw material cost also get altered. It do not

involves fixed expenditure and investment which can be considered as its main disadvantage.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.