Management Accounting Report: Techniques and Analysis for Sollatek

VerifiedAdded on 2021/01/01

|16

|5034

|167

Report

AI Summary

This report provides a detailed analysis of management accounting principles and practices, focusing on the case study of Sollatek (UK), a small-scale software systems company. The report covers essential aspects of management accounting, including the explanation of management accounting and its essential report requirements, various methods used in management accounting reports, and the benefits and applications of management accounting systems. It explores different costing methods, such as marginal and absorption costing, and demonstrates the estimation of cost and net income through profit and loss statements. Furthermore, the report delves into the merits and demerits of planning tools used under budgetary control, providing an analysis and evaluation of these tools. The report also compares how organizations adapt management accounting systems to address financial problems. The content includes financial reports, cash flow reports, sales reports, performance reports, and inventory management reports. The report also analyses cost accounting, inventory management, and price optimizing systems. Overall, the report offers a comprehensive understanding of how management accounting systems can be utilized to make effective business decisions.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1: Explain management accounting and essential requirements of management accounting

reports..........................................................................................................................................1

P2: Methods used in management accounting reports................................................................3

M1: Benefits and applications for management accounting systems.........................................4

D1: Critical analysis about the accounting report system...........................................................5

TASK 2............................................................................................................................................5

P3: Estimation of cost and net income by preparing profit and loss statement with the use

marginal and absorption costing.................................................................................................5

M2: Various kinds of management accounting techniques........................................................8

D2: Interpreting the data.............................................................................................................8

TASK 3............................................................................................................................................9

P4: Merits and Demerits of various planning tools used under budgetary control.....................9

M3: Analysis of using planning tools.......................................................................................10

D3: Evaluation of planning tools..............................................................................................11

TASK 4..........................................................................................................................................11

P5 Comparison on how organisations are adapting management accounting systems............11

M4: Analysis of financial problems..........................................................................................12

CONCLUSION ...........................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1: Explain management accounting and essential requirements of management accounting

reports..........................................................................................................................................1

P2: Methods used in management accounting reports................................................................3

M1: Benefits and applications for management accounting systems.........................................4

D1: Critical analysis about the accounting report system...........................................................5

TASK 2............................................................................................................................................5

P3: Estimation of cost and net income by preparing profit and loss statement with the use

marginal and absorption costing.................................................................................................5

M2: Various kinds of management accounting techniques........................................................8

D2: Interpreting the data.............................................................................................................8

TASK 3............................................................................................................................................9

P4: Merits and Demerits of various planning tools used under budgetary control.....................9

M3: Analysis of using planning tools.......................................................................................10

D3: Evaluation of planning tools..............................................................................................11

TASK 4..........................................................................................................................................11

P5 Comparison on how organisations are adapting management accounting systems............11

M4: Analysis of financial problems..........................................................................................12

CONCLUSION ...........................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION

Accounting process relates to recording, classifying, collecting, summarising and

interpreting information related financial transactions of business. accounting process is

broadly classified in two broad categories that is financial accounting and managerial

accounting. Financial accounting process is related with preparation of financial statements of a

company such as statement of profit and loss , balance sheet and cash flow statement. Whereas

management accounting is accounting which is related with process of preparing managerial

reports by utilising financial statements of company by taking into consideration future

economic and non economic activities of market. These managerial reports are then used by

internal management of company so that they can formulate policies for company according to

trends of market and setting of organisational goals( Abdel-Kader, 2011). below project is

prepared on “Sollatek (UK)” which is a small scale industry dealing in Software systems. This

project report discusses about systems of management accounting and how to develop a

understanding of them. Application of certain techniques of management accounting. utilisation

of planning tools that are used by managers in management accounting. Comparison of ways in

which companies can utilise management accounting reports for responding to financial issues

faced by companies.

TASK 1

P1: Explain management accounting and essential requirements of management accounting

reports

Management accounting is process of accounting which relates to preparation of

managerial accounting reports which is prepared by accountants of company so that internal

management of company can make utilisation of them for purpose of formulation of policies

and setting of objectives of company according to trends that are applicable in market.

management accounting reports are prepared with use of financial statements of company such

as statement of profit and loss, balance sheet and cash flow statement. These reports also takes

into consideration future economic and non economic trends of market that will be applicable in

economy in future. managerial accounting can also be called as cost accounting which enables

managers of company in decision making process that create value of organisation with a

1

Accounting process relates to recording, classifying, collecting, summarising and

interpreting information related financial transactions of business. accounting process is

broadly classified in two broad categories that is financial accounting and managerial

accounting. Financial accounting process is related with preparation of financial statements of a

company such as statement of profit and loss , balance sheet and cash flow statement. Whereas

management accounting is accounting which is related with process of preparing managerial

reports by utilising financial statements of company by taking into consideration future

economic and non economic activities of market. These managerial reports are then used by

internal management of company so that they can formulate policies for company according to

trends of market and setting of organisational goals( Abdel-Kader, 2011). below project is

prepared on “Sollatek (UK)” which is a small scale industry dealing in Software systems. This

project report discusses about systems of management accounting and how to develop a

understanding of them. Application of certain techniques of management accounting. utilisation

of planning tools that are used by managers in management accounting. Comparison of ways in

which companies can utilise management accounting reports for responding to financial issues

faced by companies.

TASK 1

P1: Explain management accounting and essential requirements of management accounting

reports

Management accounting is process of accounting which relates to preparation of

managerial accounting reports which is prepared by accountants of company so that internal

management of company can make utilisation of them for purpose of formulation of policies

and setting of objectives of company according to trends that are applicable in market.

management accounting reports are prepared with use of financial statements of company such

as statement of profit and loss, balance sheet and cash flow statement. These reports also takes

into consideration future economic and non economic trends of market that will be applicable in

economy in future. managerial accounting can also be called as cost accounting which enables

managers of company in decision making process that create value of organisation with a

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

effective use of organisation, efficient actions and managing people of company. information

of management accounting is:

Intended and designed so that it can be used by internal management of company,

instead of being used by shareholders , investors and creditors of company.

Related with forward looking instead of historical.

Various kinds of management accounting systems and their need in companies:

system of management accounting provides a structure to companies for assisting

managers in accurate preparation of reports so that effective decisions can be

formulated(Callahan, Stetz, and Brooks, 2011).

1. Product costing: This costing system of management accounting assist internal

management in identification of costs that is incurred in producing products, such that

managers of company like Sollatek can make an analysis of expenses related to

manufacturing overheads and allocate them in an efficient manner. product costing

system is very suitable for small scale companies whose operation activities are

simplified in nature and they are able to allocate expenditures of company and

determine profitability. This system of management accounting also allows managers in

identification of break even point for company.

2. Cost accounting system: This system of management accounting is done by managers

for estimating overall cost that are related to manufacturing process of Sollatek

company. This is beneficial for companies as it assists managers in making estimation

regarding future costs that may be incurred in production process and thereby also

estimates profitability of company. Cost accounting system also assists management in

estimating individual cost related to various heads such as Direct labour costs, Direct

material cost, cost of inventory etc. This system does not provide as-surety about

accurate costs but budgeted cost helps in allocating cost to different overheads.

3. Job costing: In this costing process internal management of company makes an estimate

about costs that are related to production of specific product or cost involved in specific

job function. companies like sollatek which is indulge in production of unique products

are benefited from this costing process.

4. Inventory management system: According to this system of management accounting ,

it assists mangers of company in managing and controlling inventory levels of

2

of management accounting is:

Intended and designed so that it can be used by internal management of company,

instead of being used by shareholders , investors and creditors of company.

Related with forward looking instead of historical.

Various kinds of management accounting systems and their need in companies:

system of management accounting provides a structure to companies for assisting

managers in accurate preparation of reports so that effective decisions can be

formulated(Callahan, Stetz, and Brooks, 2011).

1. Product costing: This costing system of management accounting assist internal

management in identification of costs that is incurred in producing products, such that

managers of company like Sollatek can make an analysis of expenses related to

manufacturing overheads and allocate them in an efficient manner. product costing

system is very suitable for small scale companies whose operation activities are

simplified in nature and they are able to allocate expenditures of company and

determine profitability. This system of management accounting also allows managers in

identification of break even point for company.

2. Cost accounting system: This system of management accounting is done by managers

for estimating overall cost that are related to manufacturing process of Sollatek

company. This is beneficial for companies as it assists managers in making estimation

regarding future costs that may be incurred in production process and thereby also

estimates profitability of company. Cost accounting system also assists management in

estimating individual cost related to various heads such as Direct labour costs, Direct

material cost, cost of inventory etc. This system does not provide as-surety about

accurate costs but budgeted cost helps in allocating cost to different overheads.

3. Job costing: In this costing process internal management of company makes an estimate

about costs that are related to production of specific product or cost involved in specific

job function. companies like sollatek which is indulge in production of unique products

are benefited from this costing process.

4. Inventory management system: According to this system of management accounting ,

it assists mangers of company in managing and controlling inventory levels of

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

company so that operation of company does not get hindered because of lack of raw

material, this system also focuses on optimum satisfaction of demand of customers.

This system of inventory management is effective for companies like Sollatek who have

to keep an optimum stock of raw material for efficient supply to manufacturing

department as and when they require and supplying it efficiently to wholesalers so that

their product is distributed in market according to demands. companies adopt various

inventory management systems such as LIFO, FIFO etc. for optimum management of

inventory which are discussed below:

LIFO: This system of inventory management implies Last in first Out. According to

which those goods are utilised firstly by companies which came last in stock and and good

which came later are used afterwards, same is applicable at time of sales. In which COGS

represents goods which came later and earlier came goods go to ending inventory(Christ, 2014).

FIFO: This system of inventory management means First in first out and according to

this system COGS represents goods which came in earlier and Ending inventory represents

goods which came in later.

P2: Methods used in management accounting reports

reports of management accounting are documents which are used by internal

management and these reports provides true and fair view of organisation and its functioning.

preparation of these reports are very necessary as they provide managers with relevant

informations. reports such as cash flow reports assist managers in knowing about liquidity

position of company , budget reports are prepared to provide managers with overview about

future operations of company and many more. These all reports are used by Sollatek limited as

they are discussed in brief as below:

Financial reports: These reports assists managers in knowing financial position of

company. These reports allows managers to have a accurate knowledge regarding

financial health of company so that they can formulate policies and objectives for

company accordingly. Sollatek limited prepares financial report by including statement

of profit and loss which tells about revenues and expenditures of firm and includes

balance sheet to keep a know about assets and liabilities of company.

Cash Flow report: cash flow report is formulated to keep a knowledge and record

about cash position of company. These reports keep a track record about total cash

3

material, this system also focuses on optimum satisfaction of demand of customers.

This system of inventory management is effective for companies like Sollatek who have

to keep an optimum stock of raw material for efficient supply to manufacturing

department as and when they require and supplying it efficiently to wholesalers so that

their product is distributed in market according to demands. companies adopt various

inventory management systems such as LIFO, FIFO etc. for optimum management of

inventory which are discussed below:

LIFO: This system of inventory management implies Last in first Out. According to

which those goods are utilised firstly by companies which came last in stock and and good

which came later are used afterwards, same is applicable at time of sales. In which COGS

represents goods which came later and earlier came goods go to ending inventory(Christ, 2014).

FIFO: This system of inventory management means First in first out and according to

this system COGS represents goods which came in earlier and Ending inventory represents

goods which came in later.

P2: Methods used in management accounting reports

reports of management accounting are documents which are used by internal

management and these reports provides true and fair view of organisation and its functioning.

preparation of these reports are very necessary as they provide managers with relevant

informations. reports such as cash flow reports assist managers in knowing about liquidity

position of company , budget reports are prepared to provide managers with overview about

future operations of company and many more. These all reports are used by Sollatek limited as

they are discussed in brief as below:

Financial reports: These reports assists managers in knowing financial position of

company. These reports allows managers to have a accurate knowledge regarding

financial health of company so that they can formulate policies and objectives for

company accordingly. Sollatek limited prepares financial report by including statement

of profit and loss which tells about revenues and expenditures of firm and includes

balance sheet to keep a know about assets and liabilities of company.

Cash Flow report: cash flow report is formulated to keep a knowledge and record

about cash position of company. These reports keep a track record about total cash

3

inflows and outflows of firm. cash flows about various activities such as operating,

investing and financing activities of firm are taken into consideration.

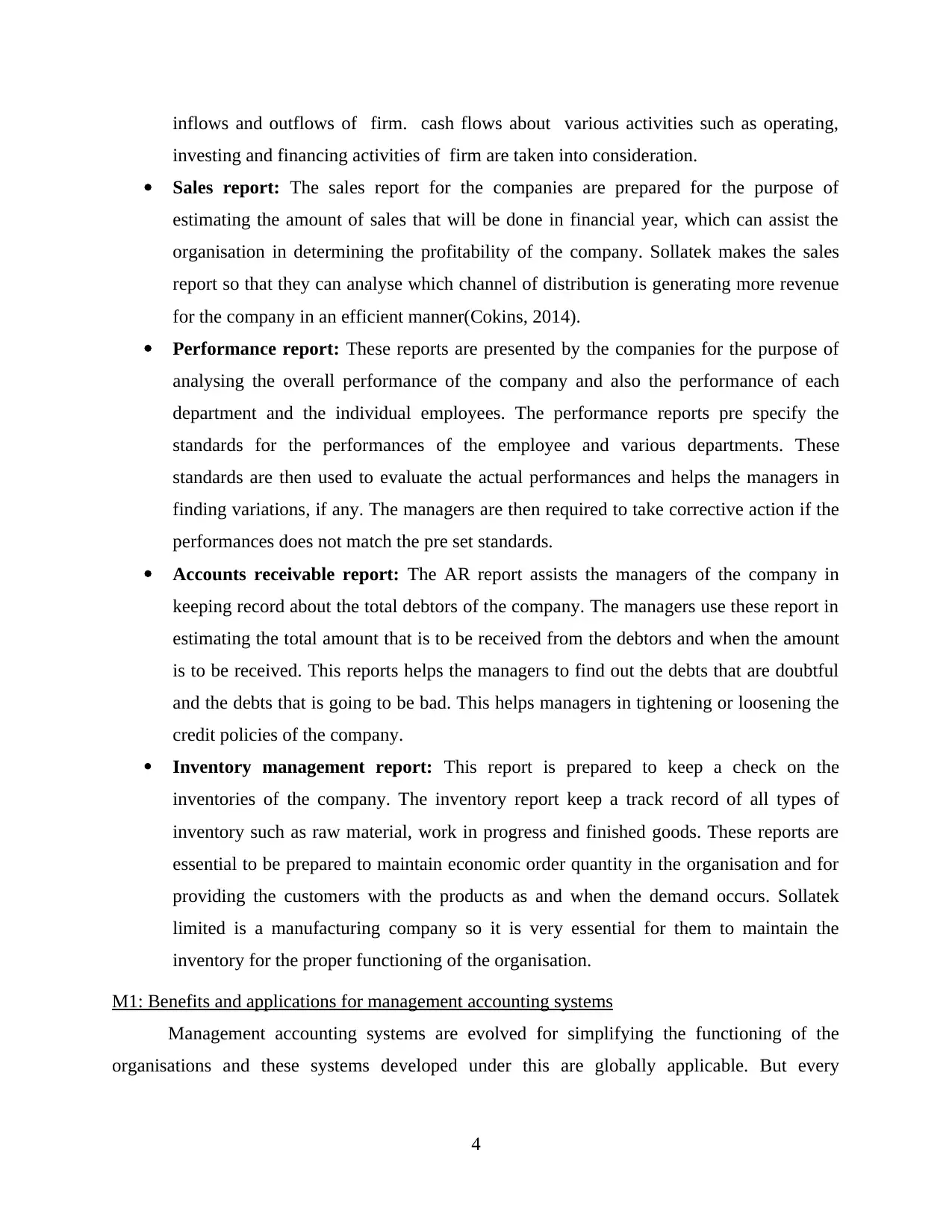

Sales report: The sales report for the companies are prepared for the purpose of

estimating the amount of sales that will be done in financial year, which can assist the

organisation in determining the profitability of the company. Sollatek makes the sales

report so that they can analyse which channel of distribution is generating more revenue

for the company in an efficient manner(Cokins, 2014).

Performance report: These reports are presented by the companies for the purpose of

analysing the overall performance of the company and also the performance of each

department and the individual employees. The performance reports pre specify the

standards for the performances of the employee and various departments. These

standards are then used to evaluate the actual performances and helps the managers in

finding variations, if any. The managers are then required to take corrective action if the

performances does not match the pre set standards.

Accounts receivable report: The AR report assists the managers of the company in

keeping record about the total debtors of the company. The managers use these report in

estimating the total amount that is to be received from the debtors and when the amount

is to be received. This reports helps the managers to find out the debts that are doubtful

and the debts that is going to be bad. This helps managers in tightening or loosening the

credit policies of the company.

Inventory management report: This report is prepared to keep a check on the

inventories of the company. The inventory report keep a track record of all types of

inventory such as raw material, work in progress and finished goods. These reports are

essential to be prepared to maintain economic order quantity in the organisation and for

providing the customers with the products as and when the demand occurs. Sollatek

limited is a manufacturing company so it is very essential for them to maintain the

inventory for the proper functioning of the organisation.

M1: Benefits and applications for management accounting systems

Management accounting systems are evolved for simplifying the functioning of the

organisations and these systems developed under this are globally applicable. But every

4

investing and financing activities of firm are taken into consideration.

Sales report: The sales report for the companies are prepared for the purpose of

estimating the amount of sales that will be done in financial year, which can assist the

organisation in determining the profitability of the company. Sollatek makes the sales

report so that they can analyse which channel of distribution is generating more revenue

for the company in an efficient manner(Cokins, 2014).

Performance report: These reports are presented by the companies for the purpose of

analysing the overall performance of the company and also the performance of each

department and the individual employees. The performance reports pre specify the

standards for the performances of the employee and various departments. These

standards are then used to evaluate the actual performances and helps the managers in

finding variations, if any. The managers are then required to take corrective action if the

performances does not match the pre set standards.

Accounts receivable report: The AR report assists the managers of the company in

keeping record about the total debtors of the company. The managers use these report in

estimating the total amount that is to be received from the debtors and when the amount

is to be received. This reports helps the managers to find out the debts that are doubtful

and the debts that is going to be bad. This helps managers in tightening or loosening the

credit policies of the company.

Inventory management report: This report is prepared to keep a check on the

inventories of the company. The inventory report keep a track record of all types of

inventory such as raw material, work in progress and finished goods. These reports are

essential to be prepared to maintain economic order quantity in the organisation and for

providing the customers with the products as and when the demand occurs. Sollatek

limited is a manufacturing company so it is very essential for them to maintain the

inventory for the proper functioning of the organisation.

M1: Benefits and applications for management accounting systems

Management accounting systems are evolved for simplifying the functioning of the

organisations and these systems developed under this are globally applicable. But every

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

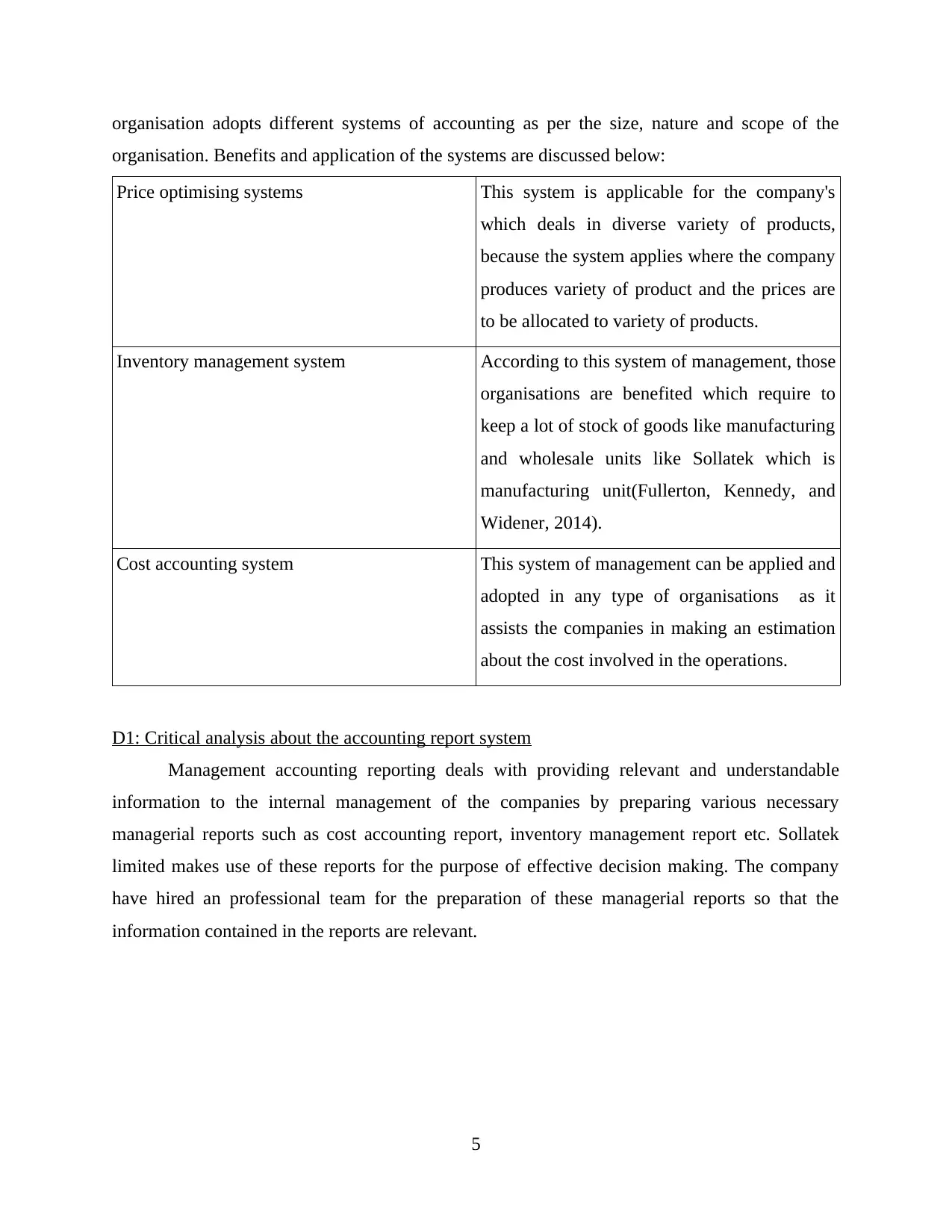

organisation adopts different systems of accounting as per the size, nature and scope of the

organisation. Benefits and application of the systems are discussed below:

Price optimising systems This system is applicable for the company's

which deals in diverse variety of products,

because the system applies where the company

produces variety of product and the prices are

to be allocated to variety of products.

Inventory management system According to this system of management, those

organisations are benefited which require to

keep a lot of stock of goods like manufacturing

and wholesale units like Sollatek which is

manufacturing unit(Fullerton, Kennedy, and

Widener, 2014).

Cost accounting system This system of management can be applied and

adopted in any type of organisations as it

assists the companies in making an estimation

about the cost involved in the operations.

D1: Critical analysis about the accounting report system

Management accounting reporting deals with providing relevant and understandable

information to the internal management of the companies by preparing various necessary

managerial reports such as cost accounting report, inventory management report etc. Sollatek

limited makes use of these reports for the purpose of effective decision making. The company

have hired an professional team for the preparation of these managerial reports so that the

information contained in the reports are relevant.

5

organisation. Benefits and application of the systems are discussed below:

Price optimising systems This system is applicable for the company's

which deals in diverse variety of products,

because the system applies where the company

produces variety of product and the prices are

to be allocated to variety of products.

Inventory management system According to this system of management, those

organisations are benefited which require to

keep a lot of stock of goods like manufacturing

and wholesale units like Sollatek which is

manufacturing unit(Fullerton, Kennedy, and

Widener, 2014).

Cost accounting system This system of management can be applied and

adopted in any type of organisations as it

assists the companies in making an estimation

about the cost involved in the operations.

D1: Critical analysis about the accounting report system

Management accounting reporting deals with providing relevant and understandable

information to the internal management of the companies by preparing various necessary

managerial reports such as cost accounting report, inventory management report etc. Sollatek

limited makes use of these reports for the purpose of effective decision making. The company

have hired an professional team for the preparation of these managerial reports so that the

information contained in the reports are relevant.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TASK 2

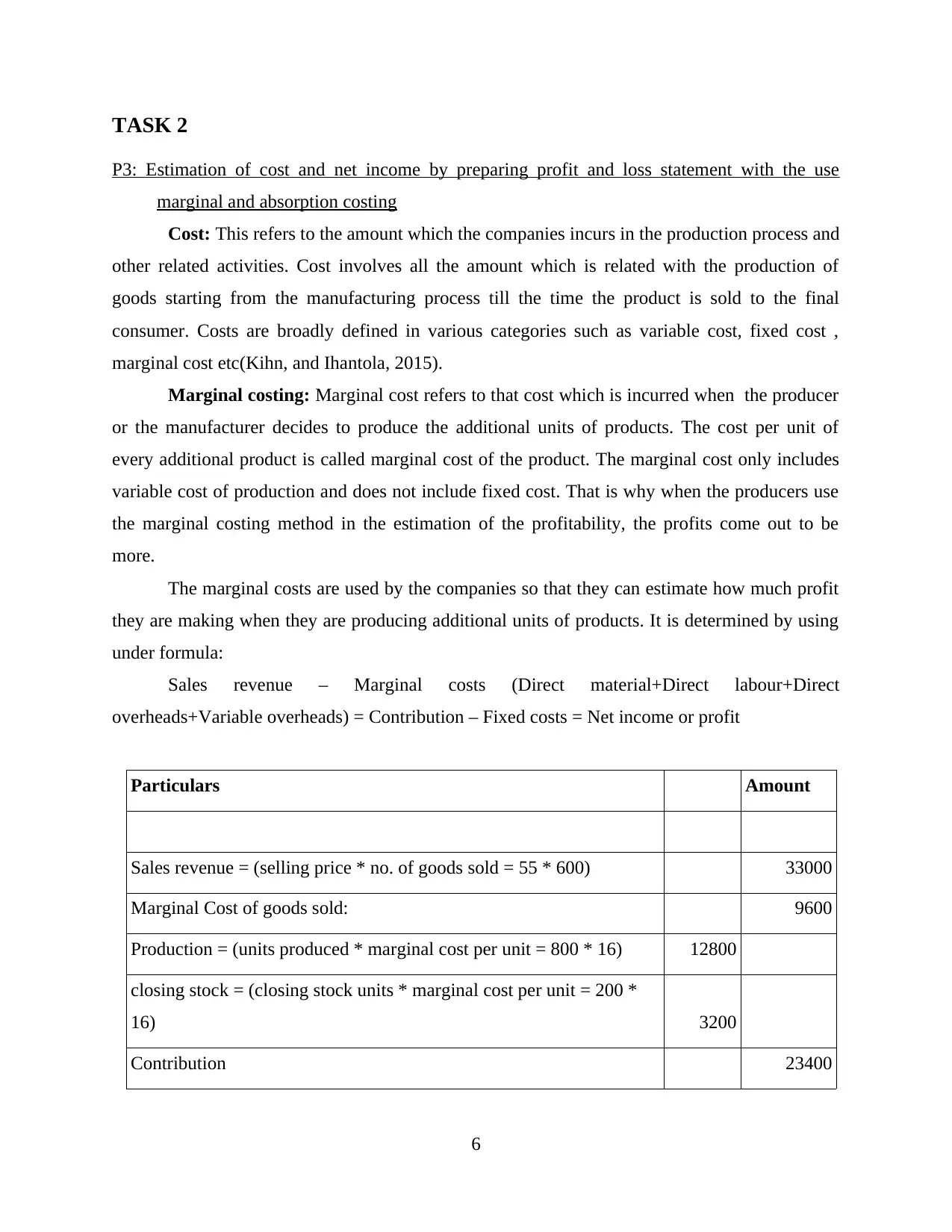

P3: Estimation of cost and net income by preparing profit and loss statement with the use

marginal and absorption costing

Cost: This refers to the amount which the companies incurs in the production process and

other related activities. Cost involves all the amount which is related with the production of

goods starting from the manufacturing process till the time the product is sold to the final

consumer. Costs are broadly defined in various categories such as variable cost, fixed cost ,

marginal cost etc(Kihn, and Ihantola, 2015).

Marginal costing: Marginal cost refers to that cost which is incurred when the producer

or the manufacturer decides to produce the additional units of products. The cost per unit of

every additional product is called marginal cost of the product. The marginal cost only includes

variable cost of production and does not include fixed cost. That is why when the producers use

the marginal costing method in the estimation of the profitability, the profits come out to be

more.

The marginal costs are used by the companies so that they can estimate how much profit

they are making when they are producing additional units of products. It is determined by using

under formula:

Sales revenue – Marginal costs (Direct material+Direct labour+Direct

overheads+Variable overheads) = Contribution – Fixed costs = Net income or profit

Particulars Amount

Sales revenue = (selling price * no. of goods sold = 55 * 600) 33000

Marginal Cost of goods sold: 9600

Production = (units produced * marginal cost per unit = 800 * 16) 12800

closing stock = (closing stock units * marginal cost per unit = 200 *

16) 3200

Contribution 23400

6

P3: Estimation of cost and net income by preparing profit and loss statement with the use

marginal and absorption costing

Cost: This refers to the amount which the companies incurs in the production process and

other related activities. Cost involves all the amount which is related with the production of

goods starting from the manufacturing process till the time the product is sold to the final

consumer. Costs are broadly defined in various categories such as variable cost, fixed cost ,

marginal cost etc(Kihn, and Ihantola, 2015).

Marginal costing: Marginal cost refers to that cost which is incurred when the producer

or the manufacturer decides to produce the additional units of products. The cost per unit of

every additional product is called marginal cost of the product. The marginal cost only includes

variable cost of production and does not include fixed cost. That is why when the producers use

the marginal costing method in the estimation of the profitability, the profits come out to be

more.

The marginal costs are used by the companies so that they can estimate how much profit

they are making when they are producing additional units of products. It is determined by using

under formula:

Sales revenue – Marginal costs (Direct material+Direct labour+Direct

overheads+Variable overheads) = Contribution – Fixed costs = Net income or profit

Particulars Amount

Sales revenue = (selling price * no. of goods sold = 55 * 600) 33000

Marginal Cost of goods sold: 9600

Production = (units produced * marginal cost per unit = 800 * 16) 12800

closing stock = (closing stock units * marginal cost per unit = 200 *

16) 3200

Contribution 23400

6

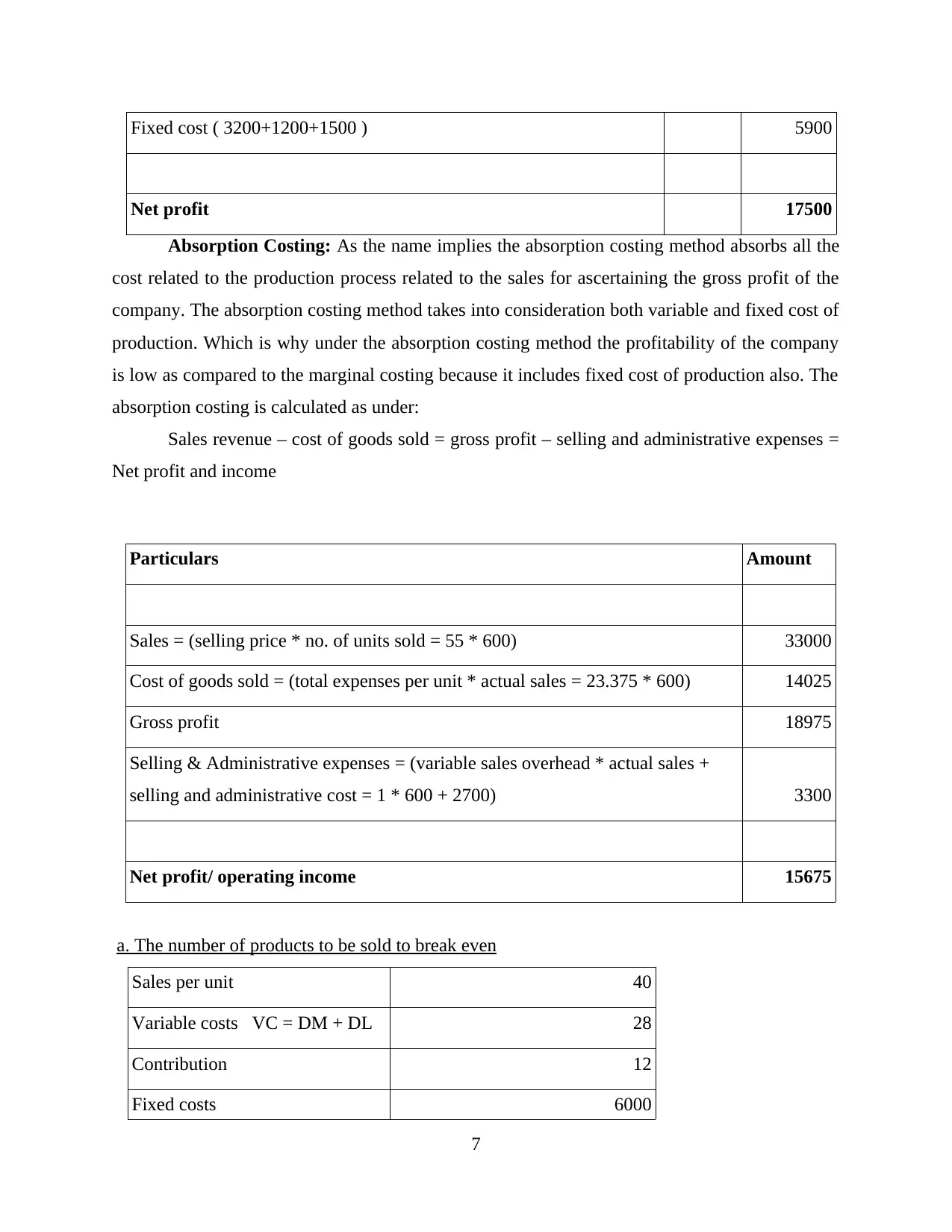

Fixed cost ( 3200+1200+1500 ) 5900

Net profit 17500

Absorption Costing: As the name implies the absorption costing method absorbs all the

cost related to the production process related to the sales for ascertaining the gross profit of the

company. The absorption costing method takes into consideration both variable and fixed cost of

production. Which is why under the absorption costing method the profitability of the company

is low as compared to the marginal costing because it includes fixed cost of production also. The

absorption costing is calculated as under:

Sales revenue – cost of goods sold = gross profit – selling and administrative expenses =

Net profit and income

Particulars Amount

Sales = (selling price * no. of units sold = 55 * 600) 33000

Cost of goods sold = (total expenses per unit * actual sales = 23.375 * 600) 14025

Gross profit 18975

Selling & Administrative expenses = (variable sales overhead * actual sales +

selling and administrative cost = 1 * 600 + 2700) 3300

Net profit/ operating income 15675

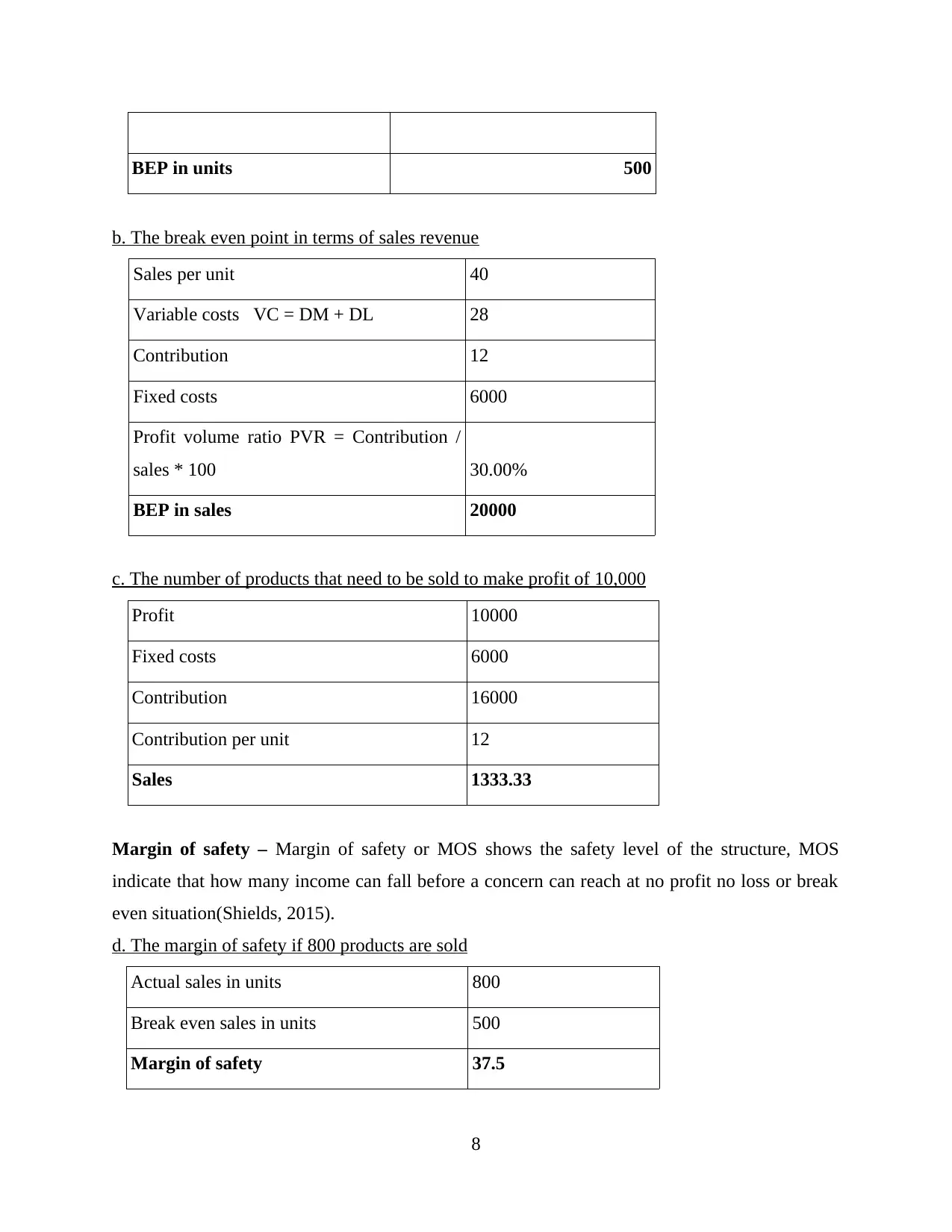

a. The number of products to be sold to break even

Sales per unit 40

Variable costs VC = DM + DL 28

Contribution 12

Fixed costs 6000

7

Net profit 17500

Absorption Costing: As the name implies the absorption costing method absorbs all the

cost related to the production process related to the sales for ascertaining the gross profit of the

company. The absorption costing method takes into consideration both variable and fixed cost of

production. Which is why under the absorption costing method the profitability of the company

is low as compared to the marginal costing because it includes fixed cost of production also. The

absorption costing is calculated as under:

Sales revenue – cost of goods sold = gross profit – selling and administrative expenses =

Net profit and income

Particulars Amount

Sales = (selling price * no. of units sold = 55 * 600) 33000

Cost of goods sold = (total expenses per unit * actual sales = 23.375 * 600) 14025

Gross profit 18975

Selling & Administrative expenses = (variable sales overhead * actual sales +

selling and administrative cost = 1 * 600 + 2700) 3300

Net profit/ operating income 15675

a. The number of products to be sold to break even

Sales per unit 40

Variable costs VC = DM + DL 28

Contribution 12

Fixed costs 6000

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

BEP in units 500

b. The break even point in terms of sales revenue

Sales per unit 40

Variable costs VC = DM + DL 28

Contribution 12

Fixed costs 6000

Profit volume ratio PVR = Contribution /

sales * 100 30.00%

BEP in sales 20000

c. The number of products that need to be sold to make profit of 10,000

Profit 10000

Fixed costs 6000

Contribution 16000

Contribution per unit 12

Sales 1333.33

Margin of safety – Margin of safety or MOS shows the safety level of the structure, MOS

indicate that how many income can fall before a concern can reach at no profit no loss or break

even situation(Shields, 2015).

d. The margin of safety if 800 products are sold

Actual sales in units 800

Break even sales in units 500

Margin of safety 37.5

8

b. The break even point in terms of sales revenue

Sales per unit 40

Variable costs VC = DM + DL 28

Contribution 12

Fixed costs 6000

Profit volume ratio PVR = Contribution /

sales * 100 30.00%

BEP in sales 20000

c. The number of products that need to be sold to make profit of 10,000

Profit 10000

Fixed costs 6000

Contribution 16000

Contribution per unit 12

Sales 1333.33

Margin of safety – Margin of safety or MOS shows the safety level of the structure, MOS

indicate that how many income can fall before a concern can reach at no profit no loss or break

even situation(Shields, 2015).

d. The margin of safety if 800 products are sold

Actual sales in units 800

Break even sales in units 500

Margin of safety 37.5

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

M2: Various kinds of management accounting techniques

The techniques of management accounting consists the tools which are used for the

determination of profitability of the company by charging various cost such as fixed cost,

variable cost, manufacturing and selling etc. Various types of the management accounting tools

are discussed as under:

Standard costing: The standard costing process is the procedure for the estimation of

future profitability of the company, by the pre determination of the costs related to the

production process. The standards costs are set by the managers for comparing it with the actual

cost that is incurred during the process of production.

Marginal costing: The marginal cost is that cost which is incurred when the companies

produce additional units of products. The cost that is involved in the marginal costing is variable

cost, marginal cost does not include fixed cost of production which increases the profitability of

the company(Smith, 2017).

D2: Interpreting the data

According to the above data it has been seen that profit that was calculated under

marginal costing has come out to be 17500 which is way higher then the profit which is

determined under absorption costing that is 15675. This difference has been seen because the

marginal costing only includes variable cost and the absorption cost includes both variable as

well as fixed cost of production.

From the data it can be seen that interpreted that this organisation produces at least

produces 500 units for incurring an situation of no profit and no loss. Margin of safety has been

calculated by the company for 37.5

TASK 3

P4: Merits and Demerits of various planning tools used under budgetary control

Budgetary Control is a tool of management control which relates to the preparation of

budgets and comparing budgeted estimates with the actual outcomes, the budgetary control

process relates with the preparation of various budgets like cash budget, fixed budget, flexible

budget etc. which helps an company for generating profits.

9

The techniques of management accounting consists the tools which are used for the

determination of profitability of the company by charging various cost such as fixed cost,

variable cost, manufacturing and selling etc. Various types of the management accounting tools

are discussed as under:

Standard costing: The standard costing process is the procedure for the estimation of

future profitability of the company, by the pre determination of the costs related to the

production process. The standards costs are set by the managers for comparing it with the actual

cost that is incurred during the process of production.

Marginal costing: The marginal cost is that cost which is incurred when the companies

produce additional units of products. The cost that is involved in the marginal costing is variable

cost, marginal cost does not include fixed cost of production which increases the profitability of

the company(Smith, 2017).

D2: Interpreting the data

According to the above data it has been seen that profit that was calculated under

marginal costing has come out to be 17500 which is way higher then the profit which is

determined under absorption costing that is 15675. This difference has been seen because the

marginal costing only includes variable cost and the absorption cost includes both variable as

well as fixed cost of production.

From the data it can be seen that interpreted that this organisation produces at least

produces 500 units for incurring an situation of no profit and no loss. Margin of safety has been

calculated by the company for 37.5

TASK 3

P4: Merits and Demerits of various planning tools used under budgetary control

Budgetary Control is a tool of management control which relates to the preparation of

budgets and comparing budgeted estimates with the actual outcomes, the budgetary control

process relates with the preparation of various budgets like cash budget, fixed budget, flexible

budget etc. which helps an company for generating profits.

9

Cash budget: Cash budget is prepared to estimate the the cash holding position of the

company. The cash budgets also keep a track record of all the cash inflows and outflows of the

company from the different activities such as operating, investing and financing.

Advantages: This budget assists in the indication of the actual cash [position of the

company and also helps the organisation in making an reliable forecast about the future

cash position of the company(Stergiou, Ashraf, and Uddin, 2013).

Disadvantages: This budget only includes the cash transaction and does not provide any

information regarding the Non monetary transactions which makes unfeasible for the

company to find the actual profitability or loss of the company.

Operational budget: The operational budgets are prepared by the companies for the purpose of

financial planning of the regular operations of the companies such that the company does not

face any financial issues or monetary problems in the future in operations of business.

Operational budgets are formulated by the companies on monthly, semi annually or quarterly

basis. The management uses these budgets for the to compare the performances related to the

operations of the company.

Advantages: this budgets makes as estimation about the company ability to meet its daily

obligations with the operational revenues of the company and to evaluate where the

finance of the company should be spend in order to earn maximum return.

Disadvantage: The preparation of these budgets requires intensive research and analysis,

which leads to consummation of time and it is also an expensive approach.

Sales budget: Sales budget are prepared to fore cast the sales related to the future period it can

be annual, semi annual etc. when the company prepares the sales budget it means that the

employees have a target to achieve the sales target as shown in the sales budget. This budget is

used by the companies in measuring the actual sales with the budgeted sales and finding

variations if any and taking actions if the criteria is not met.

Advantages : Sales budget enables the managers in planning a sales target and planning

accordingly to achieve them which motivates the employees to work towards the set

target.

Disadvantage: Preparation of sales budget is done on the basis of the analysis of trends

and assumptions which makes it less accurate and reliable.

10

company. The cash budgets also keep a track record of all the cash inflows and outflows of the

company from the different activities such as operating, investing and financing.

Advantages: This budget assists in the indication of the actual cash [position of the

company and also helps the organisation in making an reliable forecast about the future

cash position of the company(Stergiou, Ashraf, and Uddin, 2013).

Disadvantages: This budget only includes the cash transaction and does not provide any

information regarding the Non monetary transactions which makes unfeasible for the

company to find the actual profitability or loss of the company.

Operational budget: The operational budgets are prepared by the companies for the purpose of

financial planning of the regular operations of the companies such that the company does not

face any financial issues or monetary problems in the future in operations of business.

Operational budgets are formulated by the companies on monthly, semi annually or quarterly

basis. The management uses these budgets for the to compare the performances related to the

operations of the company.

Advantages: this budgets makes as estimation about the company ability to meet its daily

obligations with the operational revenues of the company and to evaluate where the

finance of the company should be spend in order to earn maximum return.

Disadvantage: The preparation of these budgets requires intensive research and analysis,

which leads to consummation of time and it is also an expensive approach.

Sales budget: Sales budget are prepared to fore cast the sales related to the future period it can

be annual, semi annual etc. when the company prepares the sales budget it means that the

employees have a target to achieve the sales target as shown in the sales budget. This budget is

used by the companies in measuring the actual sales with the budgeted sales and finding

variations if any and taking actions if the criteria is not met.

Advantages : Sales budget enables the managers in planning a sales target and planning

accordingly to achieve them which motivates the employees to work towards the set

target.

Disadvantage: Preparation of sales budget is done on the basis of the analysis of trends

and assumptions which makes it less accurate and reliable.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.