Accounting Systems and Processes: Finance Homework Solution

VerifiedAdded on 2020/04/01

|25

|1311

|33

Homework Assignment

AI Summary

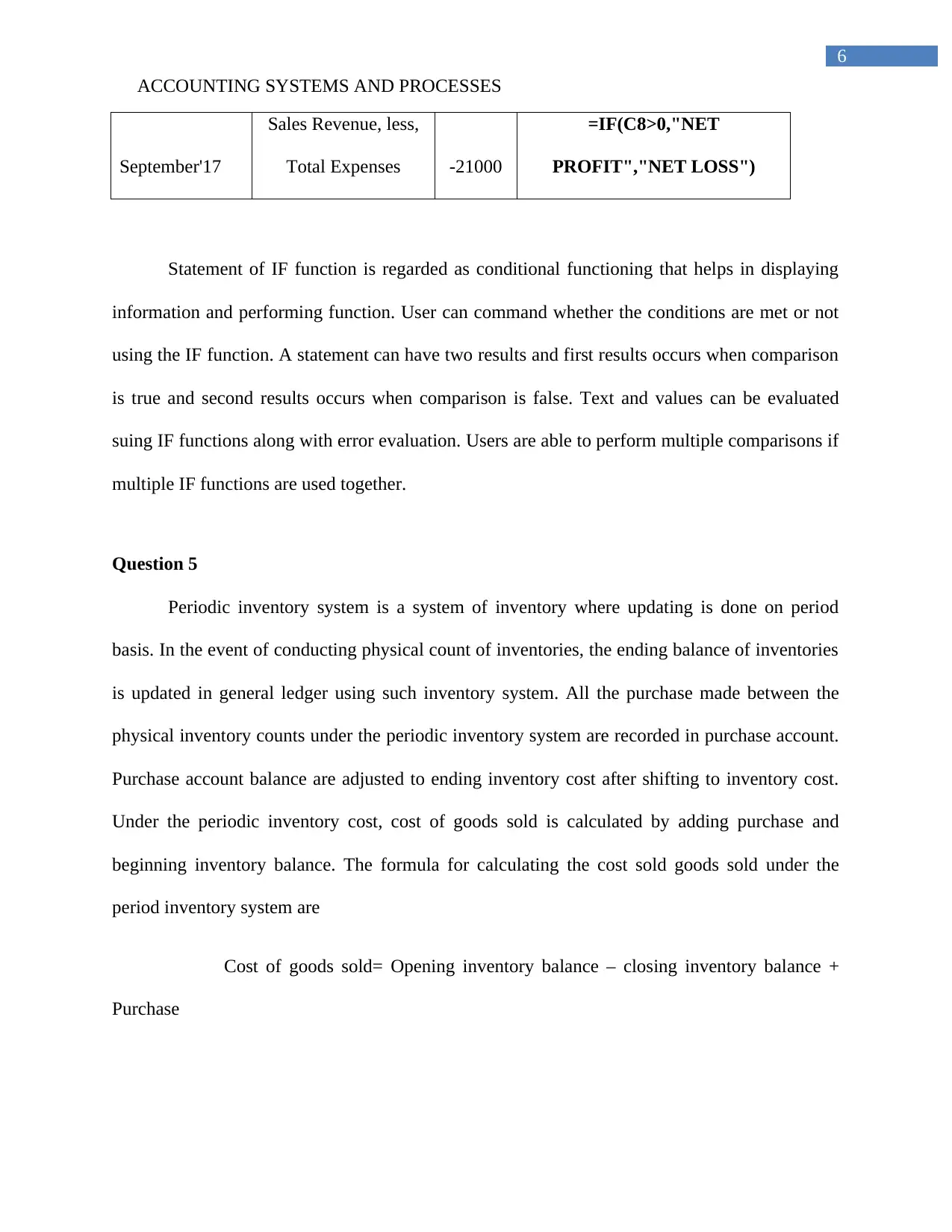

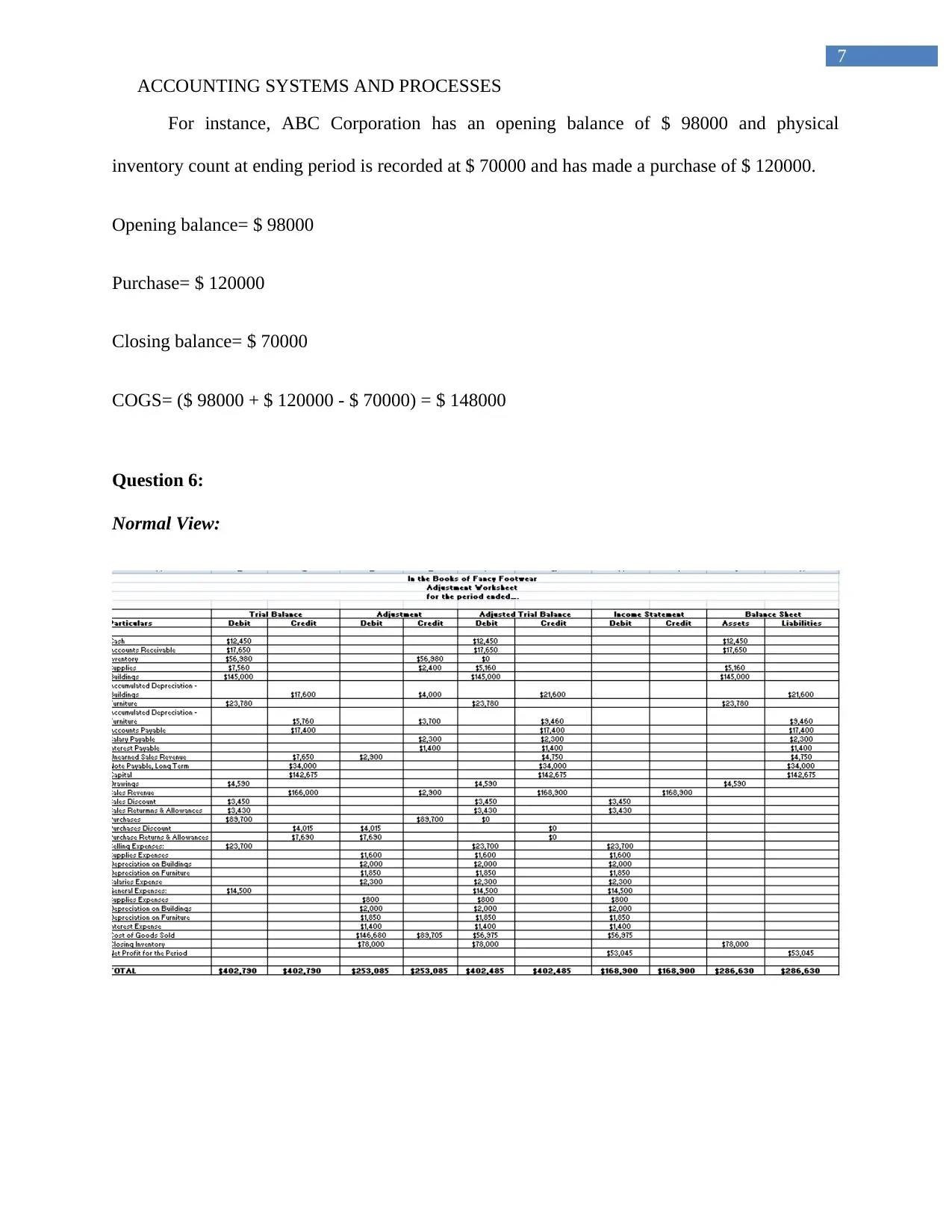

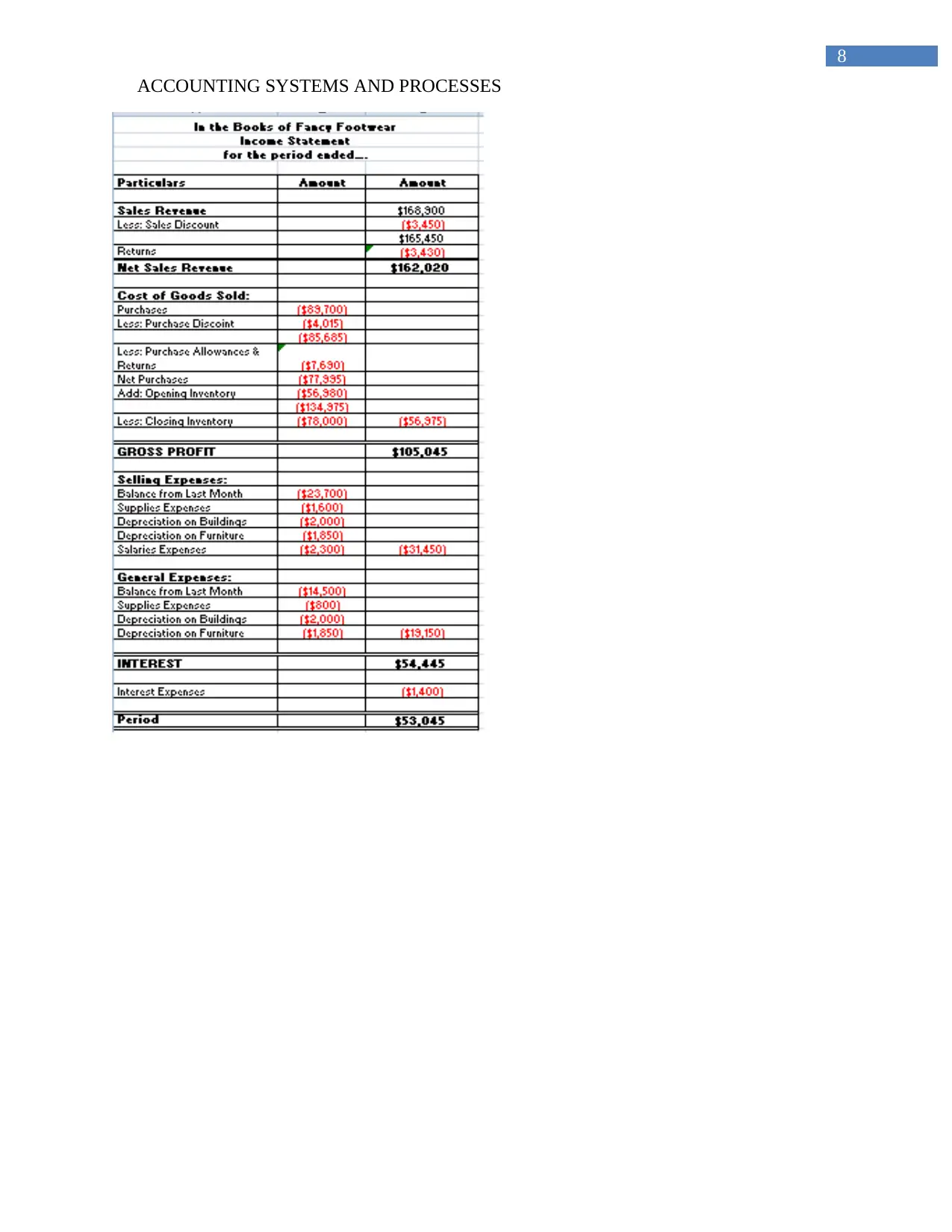

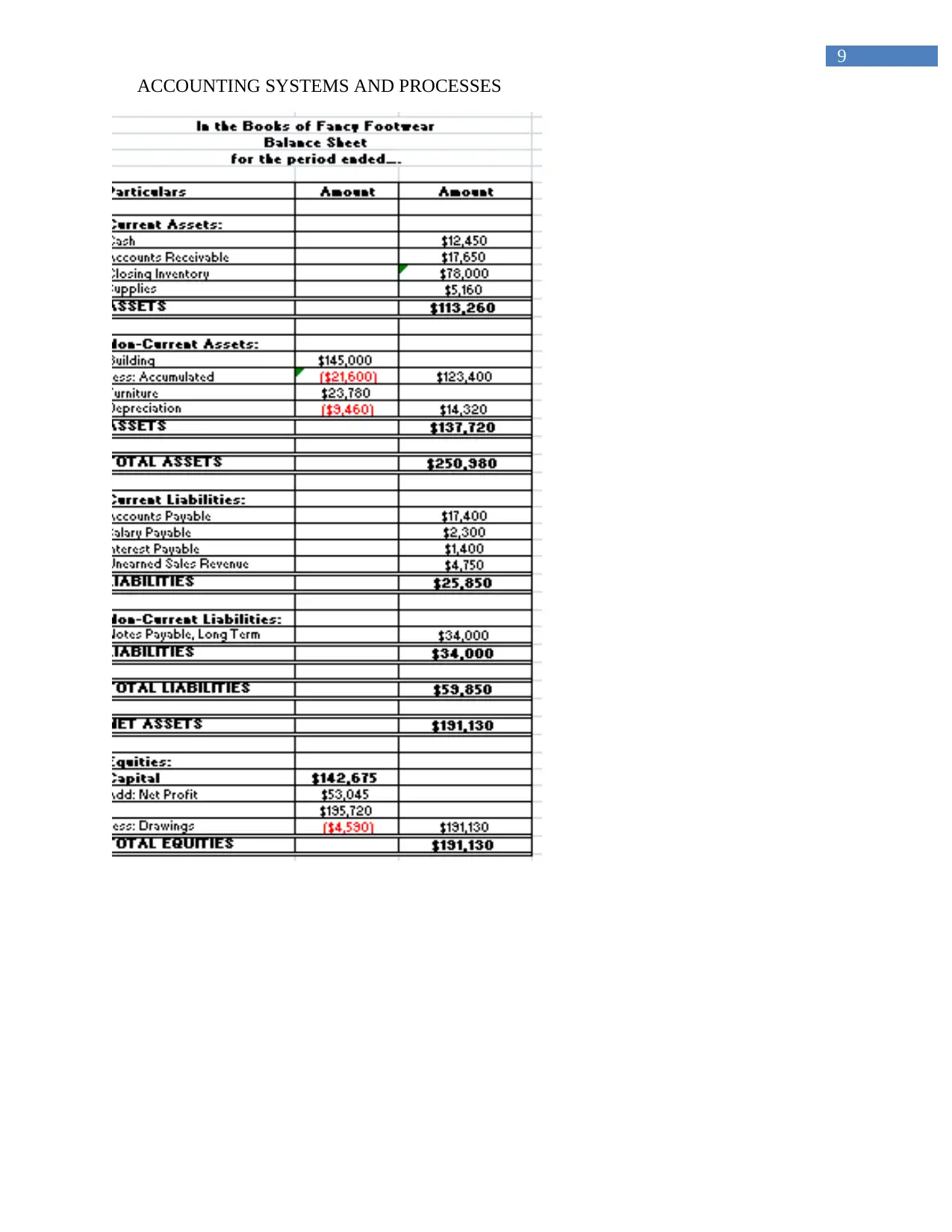

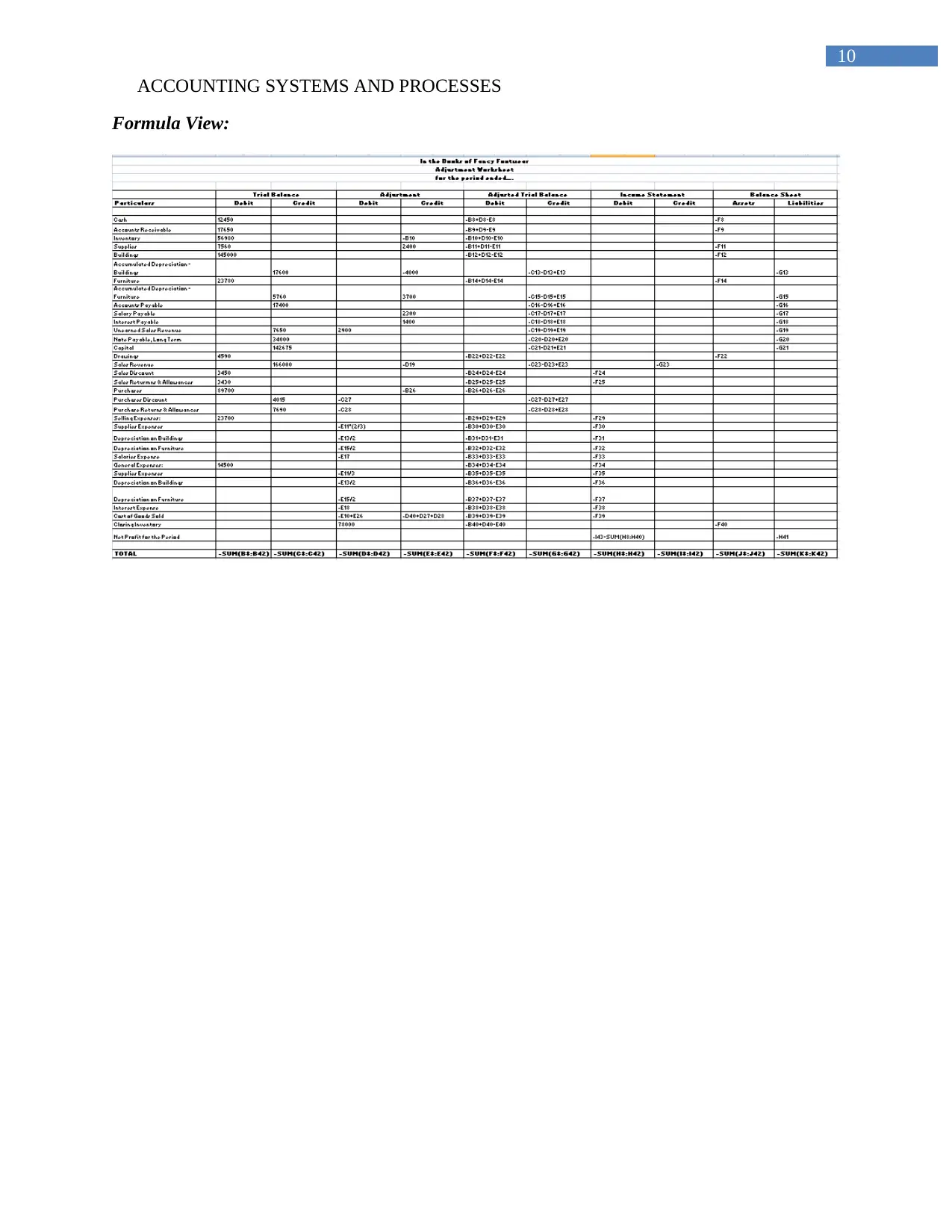

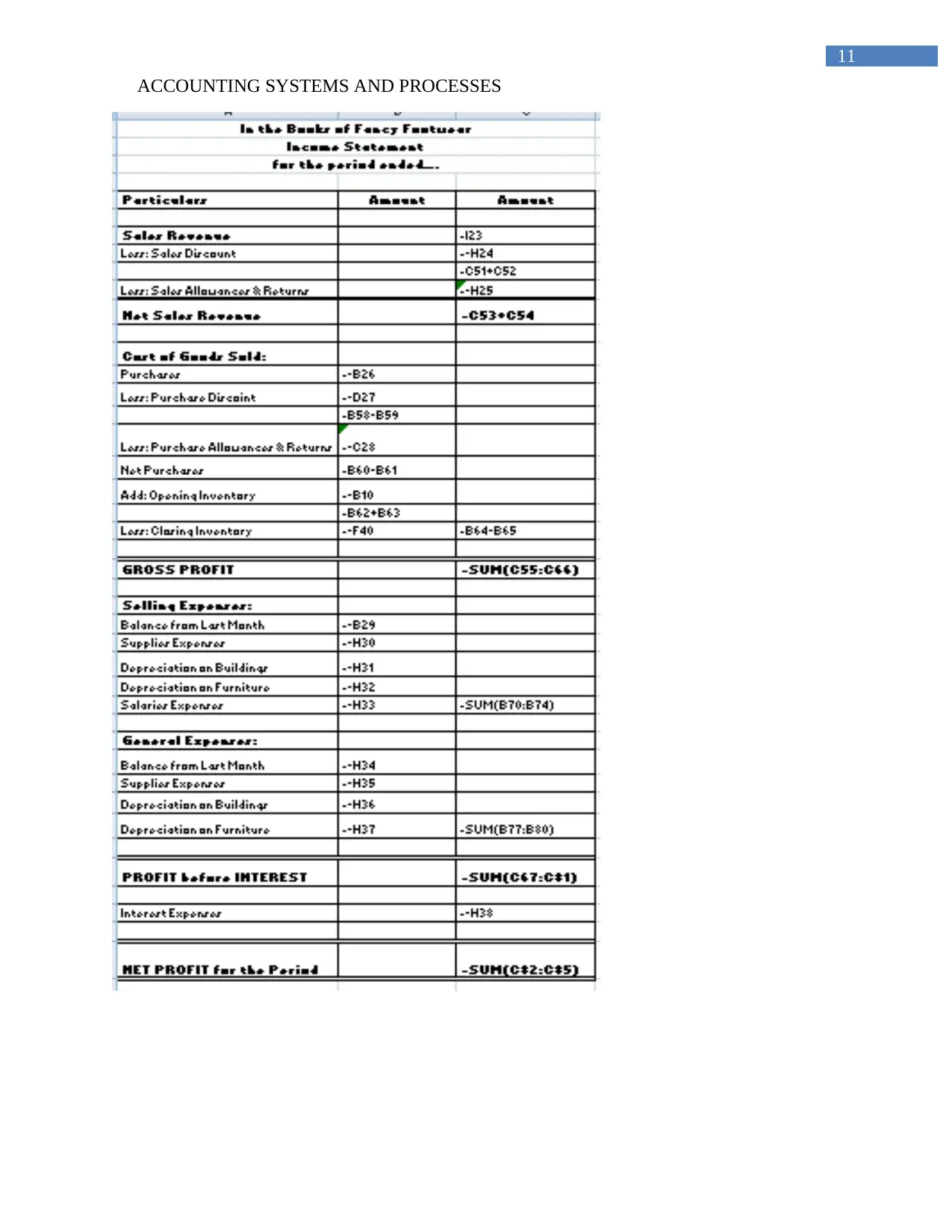

This document presents a comprehensive solution to an accounting systems and processes assignment. It addresses various aspects of accounting, starting with naming cells in spreadsheets and their benefits for formula maintenance. The solution explores displaying negative numbers, designing spreadsheets for error minimization, and using the IF function for conditional statements. It also covers the periodic inventory system, including calculations for cost of goods sold. The assignment further delves into financial statement analysis, including direct write-off and allowance methods for bad debts, and evaluating an organization's financial position using receivables. The final section provides an analysis of Wesfarmers' financial performance, discussing dividends, return on equity, earnings per share, working capital ratio, and net profit tax, culminating in an investment recommendation for an individual. The document includes formula views, normal views, and workings for clarity.

1 out of 25

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.