ACC3101 Accounting Info Systems: Xero Software and MSC Controls

VerifiedAdded on 2023/06/03

|13

|2610

|190

Project

AI Summary

This project solution provides a comprehensive review of Xero accounting software, including its key features, advantages, and disadvantages, illustrated with screenshots. It also evaluates the change controls at Mining Support Services (MSC), identifying weaknesses in their backup and Disaster Recovery Planning (DRP) procedures. Recommendations for improved data security, backup strategies, and change management processes are provided, emphasizing the importance of written change requests, regular data backups, and secure data center locations. The analysis covers aspects like GST reconciliation, financial reporting, and the need for robust internal controls to protect critical data, offering valuable insights for accounting information systems and risk management.

Accounting

Information System

Assignment

Information System

Assignment

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

By student name

Professor

University

Date: 25 April 2018.

Page 1 of 13

By student name

Professor

University

Date: 25 April 2018.

Page 1 of 13

2

Contents

Background and Abstract............................................................................................................................2

Question 1...................................................................................................................................................3

Overview of Xero Software......................................................................................................................3

Key Features with screenshots................................................................................................................3

Advantages and Disadvantages...............................................................................................................8

Question 2...................................................................................................................................................9

Evaluation of change controls at MSC...................................................................................................10

References.................................................................................................................................................12

Page 2 of 13

Contents

Background and Abstract............................................................................................................................2

Question 1...................................................................................................................................................3

Overview of Xero Software......................................................................................................................3

Key Features with screenshots................................................................................................................3

Advantages and Disadvantages...............................................................................................................8

Question 2...................................................................................................................................................9

Evaluation of change controls at MSC...................................................................................................10

References.................................................................................................................................................12

Page 2 of 13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

Background and Abstract

A report has been prepared on the xero software and a brief overview of the same has been

given. The advantages and disadvantages of using the same as an accounting software has been

using the screenshots and how the same is being used in the given business scenario. The second

case study is on Mining Support Services (MSC), which is one of the specialist in software

designing for the mining industry. Since it has many critical data, back up and software so the

requisite internal control processes has been discussed. Along with the same, the disaster

recovery planning (DRP) procedure of the company has been discussed along and

recommendations have been given for what are the changes in control that are required.

Question 1

Overview of Xero Software

Xero is one of the widely used web based accounting software in the industry for accounting and

financial report preparation and book keeping purposes. All the given transactions of the

business for the given period can be recorded in the software and various reports can be

generated through it for the decision-making by the users of financial statements (Belton, 2017).

It was established in 2006 and is generally being used by small businesses. It helps in connecting

with the partners and give the financial overview and visibility of the given business in a

consolidated manner. Even the people with no accounting knowledge find it easy to operate the

software as it converts some of the most complex and standardised transactions into the easiest

transactions and in a user-friendly manner. More than 475000 businesses are using it as of now

(Boccia & Leonardi, 2016).

Page 3 of 13

Background and Abstract

A report has been prepared on the xero software and a brief overview of the same has been

given. The advantages and disadvantages of using the same as an accounting software has been

using the screenshots and how the same is being used in the given business scenario. The second

case study is on Mining Support Services (MSC), which is one of the specialist in software

designing for the mining industry. Since it has many critical data, back up and software so the

requisite internal control processes has been discussed. Along with the same, the disaster

recovery planning (DRP) procedure of the company has been discussed along and

recommendations have been given for what are the changes in control that are required.

Question 1

Overview of Xero Software

Xero is one of the widely used web based accounting software in the industry for accounting and

financial report preparation and book keeping purposes. All the given transactions of the

business for the given period can be recorded in the software and various reports can be

generated through it for the decision-making by the users of financial statements (Belton, 2017).

It was established in 2006 and is generally being used by small businesses. It helps in connecting

with the partners and give the financial overview and visibility of the given business in a

consolidated manner. Even the people with no accounting knowledge find it easy to operate the

software as it converts some of the most complex and standardised transactions into the easiest

transactions and in a user-friendly manner. More than 475000 businesses are using it as of now

(Boccia & Leonardi, 2016).

Page 3 of 13

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

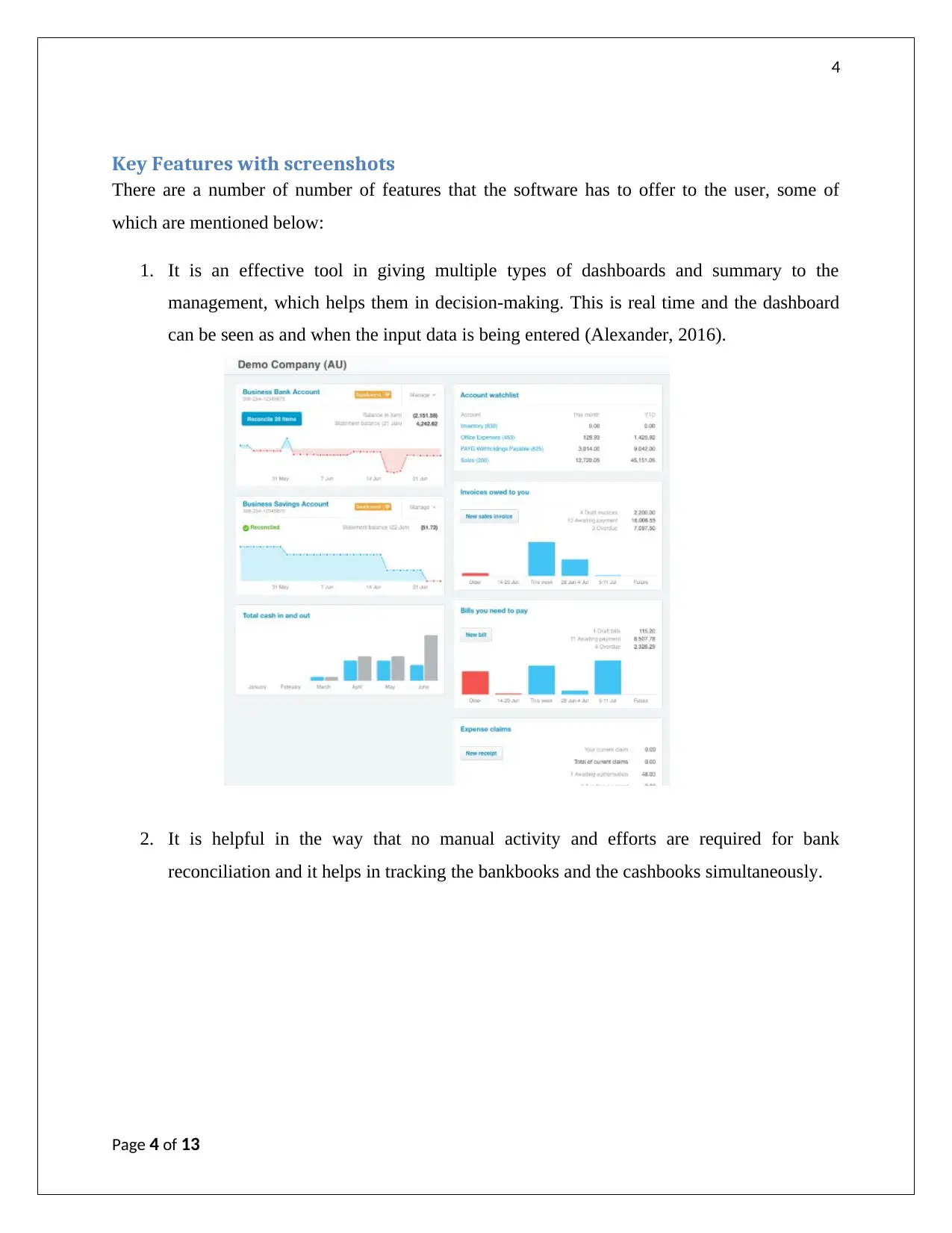

Key Features with screenshots

There are a number of number of features that the software has to offer to the user, some of

which are mentioned below:

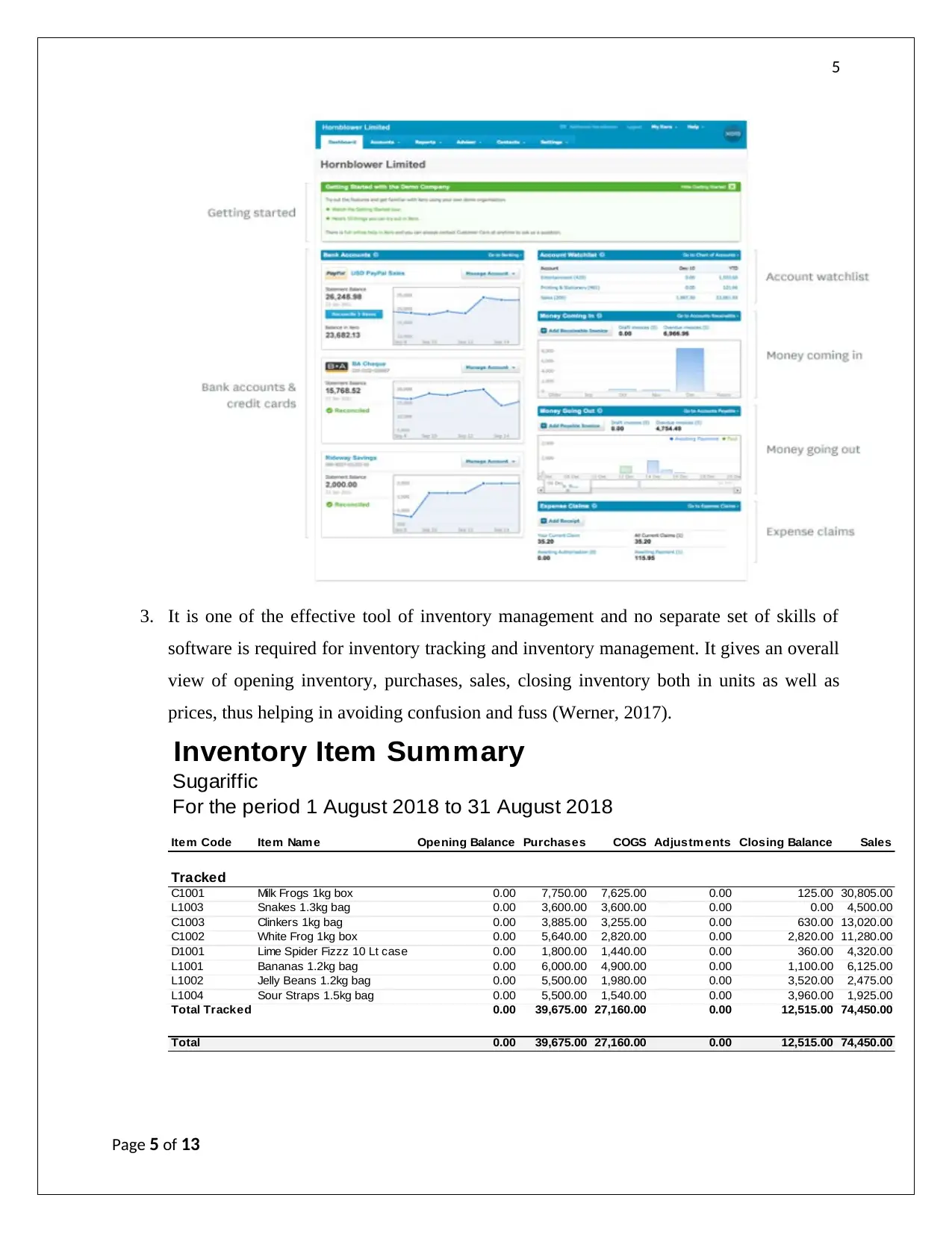

1. It is an effective tool in giving multiple types of dashboards and summary to the

management, which helps them in decision-making. This is real time and the dashboard

can be seen as and when the input data is being entered (Alexander, 2016).

2. It is helpful in the way that no manual activity and efforts are required for bank

reconciliation and it helps in tracking the bankbooks and the cashbooks simultaneously.

Page 4 of 13

Key Features with screenshots

There are a number of number of features that the software has to offer to the user, some of

which are mentioned below:

1. It is an effective tool in giving multiple types of dashboards and summary to the

management, which helps them in decision-making. This is real time and the dashboard

can be seen as and when the input data is being entered (Alexander, 2016).

2. It is helpful in the way that no manual activity and efforts are required for bank

reconciliation and it helps in tracking the bankbooks and the cashbooks simultaneously.

Page 4 of 13

5

3. It is one of the effective tool of inventory management and no separate set of skills of

software is required for inventory tracking and inventory management. It gives an overall

view of opening inventory, purchases, sales, closing inventory both in units as well as

prices, thus helping in avoiding confusion and fuss (Werner, 2017).

Item Code Item Name Opening Balance Purchases COGS Adjustm ents Closing Balance Sales

C1001 Milk Frogs 1kg box 0.00 7,750.00 7,625.00 0.00 125.00 30,805.00

L1003 Snakes 1.3kg bag 0.00 3,600.00 3,600.00 0.00 0.00 4,500.00

C1003 Clinkers 1kg bag 0.00 3,885.00 3,255.00 0.00 630.00 13,020.00

C1002 White Frog 1kg box 0.00 5,640.00 2,820.00 0.00 2,820.00 11,280.00

D1001 Lime Spider Fizzz 10 Lt case 0.00 1,800.00 1,440.00 0.00 360.00 4,320.00

L1001 Bananas 1.2kg bag 0.00 6,000.00 4,900.00 0.00 1,100.00 6,125.00

L1002 Jelly Beans 1.2kg bag 0.00 5,500.00 1,980.00 0.00 3,520.00 2,475.00

L1004 Sour Straps 1.5kg bag 0.00 5,500.00 1,540.00 0.00 3,960.00 1,925.00

Total Tracked 0.00 39,675.00 27,160.00 0.00 12,515.00 74,450.00

Total 0.00 39,675.00 27,160.00 0.00 12,515.00 74,450.00

Inventory Item Summary

For the period 1 August 2018 to 31 August 2018

Tracked

Sugariffic

Page 5 of 13

3. It is one of the effective tool of inventory management and no separate set of skills of

software is required for inventory tracking and inventory management. It gives an overall

view of opening inventory, purchases, sales, closing inventory both in units as well as

prices, thus helping in avoiding confusion and fuss (Werner, 2017).

Item Code Item Name Opening Balance Purchases COGS Adjustm ents Closing Balance Sales

C1001 Milk Frogs 1kg box 0.00 7,750.00 7,625.00 0.00 125.00 30,805.00

L1003 Snakes 1.3kg bag 0.00 3,600.00 3,600.00 0.00 0.00 4,500.00

C1003 Clinkers 1kg bag 0.00 3,885.00 3,255.00 0.00 630.00 13,020.00

C1002 White Frog 1kg box 0.00 5,640.00 2,820.00 0.00 2,820.00 11,280.00

D1001 Lime Spider Fizzz 10 Lt case 0.00 1,800.00 1,440.00 0.00 360.00 4,320.00

L1001 Bananas 1.2kg bag 0.00 6,000.00 4,900.00 0.00 1,100.00 6,125.00

L1002 Jelly Beans 1.2kg bag 0.00 5,500.00 1,980.00 0.00 3,520.00 2,475.00

L1004 Sour Straps 1.5kg bag 0.00 5,500.00 1,540.00 0.00 3,960.00 1,925.00

Total Tracked 0.00 39,675.00 27,160.00 0.00 12,515.00 74,450.00

Total 0.00 39,675.00 27,160.00 0.00 12,515.00 74,450.00

Inventory Item Summary

For the period 1 August 2018 to 31 August 2018

Tracked

Sugariffic

Page 5 of 13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

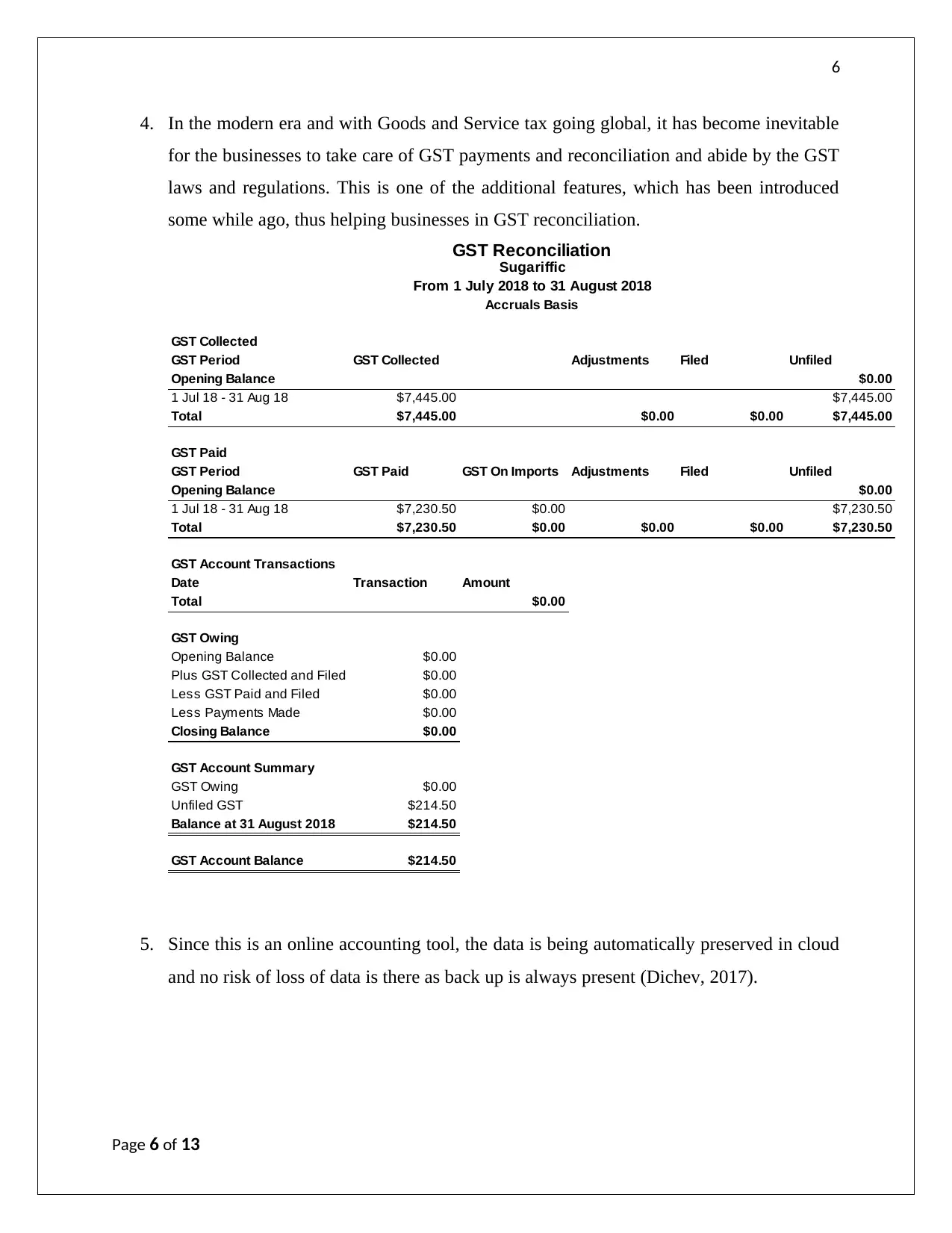

4. In the modern era and with Goods and Service tax going global, it has become inevitable

for the businesses to take care of GST payments and reconciliation and abide by the GST

laws and regulations. This is one of the additional features, which has been introduced

some while ago, thus helping businesses in GST reconciliation.

GST Collected

GST Period GST Collected Adjustments Filed Unfiled

Opening Balance $0.00

1 Jul 18 - 31 Aug 18 $7,445.00 $7,445.00

Total $7,445.00 $0.00 $0.00 $7,445.00

GST Paid

GST Period GST Paid GST On Imports Adjustments Filed Unfiled

Opening Balance $0.00

1 Jul 18 - 31 Aug 18 $7,230.50 $0.00 $7,230.50

Total $7,230.50 $0.00 $0.00 $0.00 $7,230.50

GST Account Transactions

Date Transaction Amount

Total $0.00

GST Owing

Opening Balance $0.00

Plus GST Collected and Filed $0.00

Less GST Paid and Filed $0.00

Less Payments Made $0.00

Closing Balance $0.00

GST Account Summary

GST Owing $0.00

Unfiled GST $214.50

Balance at 31 August 2018 $214.50

GST Account Balance $214.50

GST Reconciliation

Sugariffic

From 1 July 2018 to 31 August 2018

Accruals Basis

5. Since this is an online accounting tool, the data is being automatically preserved in cloud

and no risk of loss of data is there as back up is always present (Dichev, 2017).

Page 6 of 13

4. In the modern era and with Goods and Service tax going global, it has become inevitable

for the businesses to take care of GST payments and reconciliation and abide by the GST

laws and regulations. This is one of the additional features, which has been introduced

some while ago, thus helping businesses in GST reconciliation.

GST Collected

GST Period GST Collected Adjustments Filed Unfiled

Opening Balance $0.00

1 Jul 18 - 31 Aug 18 $7,445.00 $7,445.00

Total $7,445.00 $0.00 $0.00 $7,445.00

GST Paid

GST Period GST Paid GST On Imports Adjustments Filed Unfiled

Opening Balance $0.00

1 Jul 18 - 31 Aug 18 $7,230.50 $0.00 $7,230.50

Total $7,230.50 $0.00 $0.00 $0.00 $7,230.50

GST Account Transactions

Date Transaction Amount

Total $0.00

GST Owing

Opening Balance $0.00

Plus GST Collected and Filed $0.00

Less GST Paid and Filed $0.00

Less Payments Made $0.00

Closing Balance $0.00

GST Account Summary

GST Owing $0.00

Unfiled GST $214.50

Balance at 31 August 2018 $214.50

GST Account Balance $214.50

GST Reconciliation

Sugariffic

From 1 July 2018 to 31 August 2018

Accruals Basis

5. Since this is an online accounting tool, the data is being automatically preserved in cloud

and no risk of loss of data is there as back up is always present (Dichev, 2017).

Page 6 of 13

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

6. One of the most important and critical features of the software is financial reporting. It

helps in preparing all the financial closing books of accounts like the profit and loss

account, the balance sheet, the statement of changes in equity etc.

Account Aug 2018

Sales – Chocolates 55,105.00

Sales – Drinks 4,320.00

Sales – Lollies 15,025.00

Total Trading Income 74,450.00

Cost of Sales – Chocolates 13,700.00

Cost of Sales – Drinks 1,440.00

Cost of Sales – Lollies 12,020.00

Total Cost of Sales 27,160.00

Gross Profit 47,290.00

Advertising 4,180.00

Printing & Stationery 480.00

Rent 2,200.00

Wages and Salaries 4,400.00

Total Operating Expenses 11,260.00

Net Profit 36,030.00

Profit and Loss

Operating Expenses

Cost of Sales

For the month ended 31 August 2018

Sugariffic

Trading Income

Page 7 of 13

6. One of the most important and critical features of the software is financial reporting. It

helps in preparing all the financial closing books of accounts like the profit and loss

account, the balance sheet, the statement of changes in equity etc.

Account Aug 2018

Sales – Chocolates 55,105.00

Sales – Drinks 4,320.00

Sales – Lollies 15,025.00

Total Trading Income 74,450.00

Cost of Sales – Chocolates 13,700.00

Cost of Sales – Drinks 1,440.00

Cost of Sales – Lollies 12,020.00

Total Cost of Sales 27,160.00

Gross Profit 47,290.00

Advertising 4,180.00

Printing & Stationery 480.00

Rent 2,200.00

Wages and Salaries 4,400.00

Total Operating Expenses 11,260.00

Net Profit 36,030.00

Profit and Loss

Operating Expenses

Cost of Sales

For the month ended 31 August 2018

Sugariffic

Trading Income

Page 7 of 13

8

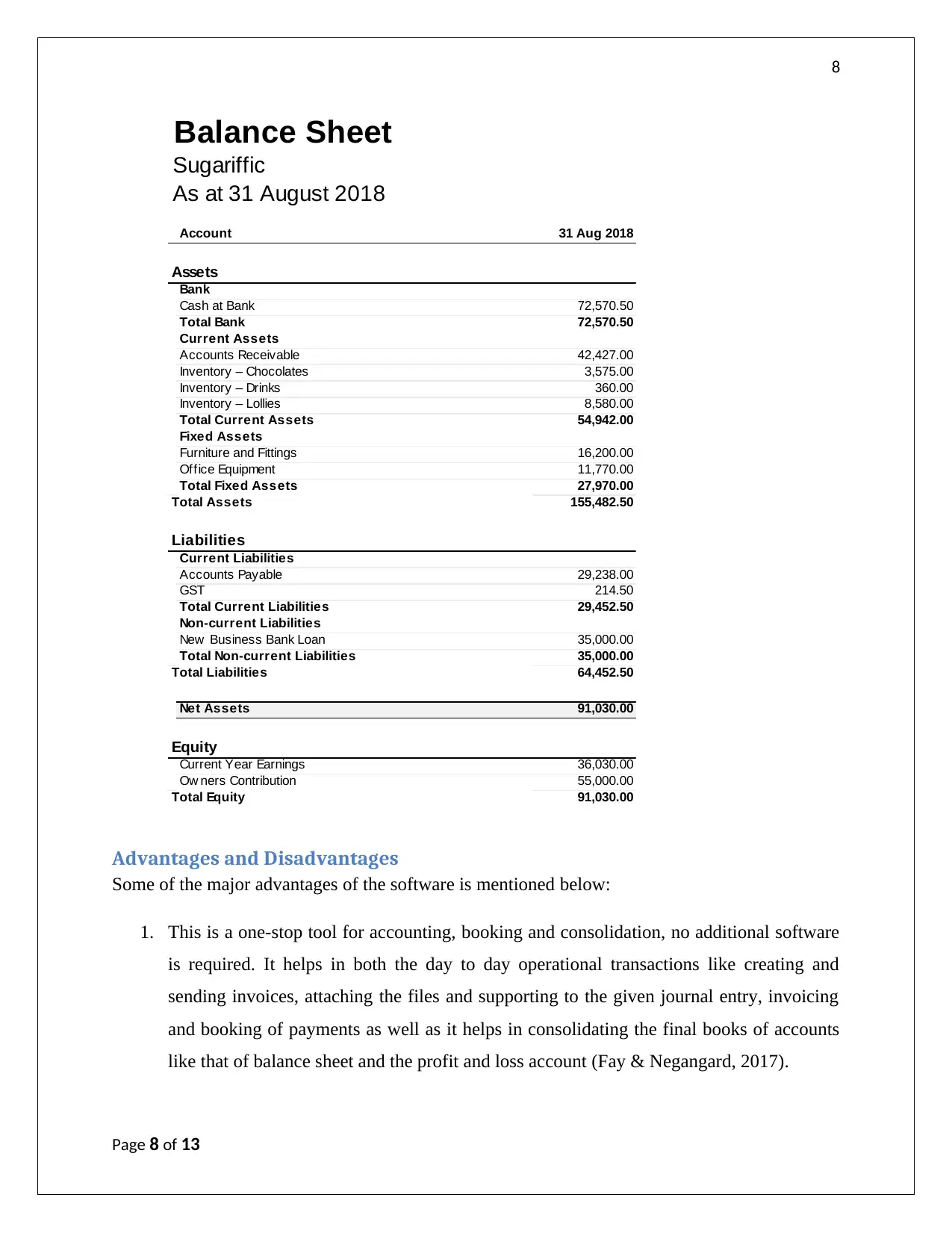

Account 31 Aug 2018

Cash at Bank 72,570.50

Total Bank 72,570.50

Accounts Receivable 42,427.00

Inventory – Chocolates 3,575.00

Inventory – Drinks 360.00

Inventory – Lollies 8,580.00

Total Current Assets 54,942.00

Furniture and Fittings 16,200.00

Office Equipment 11,770.00

Total Fixed Assets 27,970.00

Total Assets 155,482.50

Accounts Payable 29,238.00

GST 214.50

Total Current Liabilities 29,452.50

New Business Bank Loan 35,000.00

Total Non-current Liabilities 35,000.00

Total Liabilities 64,452.50

Net Assets 91,030.00

Current Year Earnings 36,030.00

Ow ners Contribution 55,000.00

Total Equity 91,030.00

Equity

Bank

Balance Sheet

As at 31 August 2018

Current Assets

Fixed Assets

Current Liabilities

Non-current Liabilities

Sugariffic

Liabilities

Assets

Advantages and Disadvantages

Some of the major advantages of the software is mentioned below:

1. This is a one-stop tool for accounting, booking and consolidation, no additional software

is required. It helps in both the day to day operational transactions like creating and

sending invoices, attaching the files and supporting to the given journal entry, invoicing

and booking of payments as well as it helps in consolidating the final books of accounts

like that of balance sheet and the profit and loss account (Fay & Negangard, 2017).

Page 8 of 13

Account 31 Aug 2018

Cash at Bank 72,570.50

Total Bank 72,570.50

Accounts Receivable 42,427.00

Inventory – Chocolates 3,575.00

Inventory – Drinks 360.00

Inventory – Lollies 8,580.00

Total Current Assets 54,942.00

Furniture and Fittings 16,200.00

Office Equipment 11,770.00

Total Fixed Assets 27,970.00

Total Assets 155,482.50

Accounts Payable 29,238.00

GST 214.50

Total Current Liabilities 29,452.50

New Business Bank Loan 35,000.00

Total Non-current Liabilities 35,000.00

Total Liabilities 64,452.50

Net Assets 91,030.00

Current Year Earnings 36,030.00

Ow ners Contribution 55,000.00

Total Equity 91,030.00

Equity

Bank

Balance Sheet

As at 31 August 2018

Current Assets

Fixed Assets

Current Liabilities

Non-current Liabilities

Sugariffic

Liabilities

Assets

Advantages and Disadvantages

Some of the major advantages of the software is mentioned below:

1. This is a one-stop tool for accounting, booking and consolidation, no additional software

is required. It helps in both the day to day operational transactions like creating and

sending invoices, attaching the files and supporting to the given journal entry, invoicing

and booking of payments as well as it helps in consolidating the final books of accounts

like that of balance sheet and the profit and loss account (Fay & Negangard, 2017).

Page 8 of 13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

2. It is relatively cheap than other such software is available in the market and is used

extensively by the small businesses. It is apt and appropriate for their use, as they cannot

afford high priced software’s like those of SAP and ERP for accounting.

3. It has a painless set up and set up costs and efforts is next to zero unlike the case of SAP

where the chart of accounts are to be prepared and a lot of effort and time is required.

Furthermore, it has an editing feature, which makes it even faster, and accurate in case an

incorrect transaction has been posted and it needs to be corrected (Farmer, 2018).

Some of the major disadvantages of the accounting tool are as follows:

1. However, it is easy to use and apply but it is not suitable for large business houses

considering the complexity of transactions there.

2. Since this is a much-consolidated tool occupying less space, navigating between the tabs

and different windows is difficult in case the correction is required in the books of

accounts (Jefferson, 2017).

3. The customization of the vendor and the customer report is restricted as a result of which

the businesses only need to use the reports which is only inbuilt and since there is an

option of exporting all the reports to excel the chances of manipulation increases.

Question 2

In the given case, the scenario for Mining Support Services (MCS), a mining industry software

specialist has been given as to how they keep up with their back up and the DRP plan and what

can be changes in the control.

Weaknesses in MCS’s backup and DRP procedures

Some of the major weaknesses in the MSC’s backup and DRP procedures are mentioned below:

1. The company’s data centre is installed in the basement of the building, that increase the

risk of losing all the IT data, and the backup of the companies in case there is a flooding

or any other natural calamity, the ground floor, and the basement are the main areas,

which face many consequences of natural calamities. This poses a risk on both the data

Page 9 of 13

2. It is relatively cheap than other such software is available in the market and is used

extensively by the small businesses. It is apt and appropriate for their use, as they cannot

afford high priced software’s like those of SAP and ERP for accounting.

3. It has a painless set up and set up costs and efforts is next to zero unlike the case of SAP

where the chart of accounts are to be prepared and a lot of effort and time is required.

Furthermore, it has an editing feature, which makes it even faster, and accurate in case an

incorrect transaction has been posted and it needs to be corrected (Farmer, 2018).

Some of the major disadvantages of the accounting tool are as follows:

1. However, it is easy to use and apply but it is not suitable for large business houses

considering the complexity of transactions there.

2. Since this is a much-consolidated tool occupying less space, navigating between the tabs

and different windows is difficult in case the correction is required in the books of

accounts (Jefferson, 2017).

3. The customization of the vendor and the customer report is restricted as a result of which

the businesses only need to use the reports which is only inbuilt and since there is an

option of exporting all the reports to excel the chances of manipulation increases.

Question 2

In the given case, the scenario for Mining Support Services (MCS), a mining industry software

specialist has been given as to how they keep up with their back up and the DRP plan and what

can be changes in the control.

Weaknesses in MCS’s backup and DRP procedures

Some of the major weaknesses in the MSC’s backup and DRP procedures are mentioned below:

1. The company’s data centre is installed in the basement of the building, that increase the

risk of losing all the IT data, and the backup of the companies in case there is a flooding

or any other natural calamity, the ground floor, and the basement are the main areas,

which face many consequences of natural calamities. This poses a risk on both the data

Page 9 of 13

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

back up as well as how the data, which is lost in a calamity, can be recovered (DeZoort &

Harrison, 2016).

2. The company’s operational staff is working for 5 days a week over two shifts and all the

programming staff, which is located in the same building, has access to the data centre

and all the critical and private data. All of them are authorised to test the new programs

and make the changes to the programs when the operational staff is not around. This

poses a huge risk on the security of the data and thus it may be modified or changed and

there might be a scenario that no one comes to know of the same and thus the business

may face the consequences as a whole (Kuhn & Morris, 2016).

3. Programmers do respond to the oral requests made by the customers and make changes to

the program accordingly. This might land MCS into legal and regulatory issues in future

if the respective businesses suffers a loss due to this and they put a legal claim on MCS.

Thus, absence of written change request is a huge risk (Raiborn, et al., 2016).

4. System and programming documentation is being done only when the time is available

and thus no proper data backup is available. This is due to huge work demands and less

capacity of the company but this shows that the company has no adequate back up of the

data and there are huge chances that the data and information once lost, might not be

available or recovered in future.

Evaluation of change controls at MSC

There are a number of changes, which are warranted in the control measures. Some of them are:

1. The company should ask for change requests in the programs and software coding in

written from the clients. This will help in having the proper supporting and thus reiterate

the same to the client in case of any issues.

2. The company should be taking the data back up every day or probably twice or thrice a

week as many important and critical client data is at disposal of the company and it needs

to be properly preserved for future (Sithole, et al., 2017).

3. The company should be planning to relocate the data centre from the basement to the first

floor or second floor of the building, as it would help the cause in case of floods or in

case of other natural calamities in the future.

Page 10 of 13

back up as well as how the data, which is lost in a calamity, can be recovered (DeZoort &

Harrison, 2016).

2. The company’s operational staff is working for 5 days a week over two shifts and all the

programming staff, which is located in the same building, has access to the data centre

and all the critical and private data. All of them are authorised to test the new programs

and make the changes to the programs when the operational staff is not around. This

poses a huge risk on the security of the data and thus it may be modified or changed and

there might be a scenario that no one comes to know of the same and thus the business

may face the consequences as a whole (Kuhn & Morris, 2016).

3. Programmers do respond to the oral requests made by the customers and make changes to

the program accordingly. This might land MCS into legal and regulatory issues in future

if the respective businesses suffers a loss due to this and they put a legal claim on MCS.

Thus, absence of written change request is a huge risk (Raiborn, et al., 2016).

4. System and programming documentation is being done only when the time is available

and thus no proper data backup is available. This is due to huge work demands and less

capacity of the company but this shows that the company has no adequate back up of the

data and there are huge chances that the data and information once lost, might not be

available or recovered in future.

Evaluation of change controls at MSC

There are a number of changes, which are warranted in the control measures. Some of them are:

1. The company should ask for change requests in the programs and software coding in

written from the clients. This will help in having the proper supporting and thus reiterate

the same to the client in case of any issues.

2. The company should be taking the data back up every day or probably twice or thrice a

week as many important and critical client data is at disposal of the company and it needs

to be properly preserved for future (Sithole, et al., 2017).

3. The company should be planning to relocate the data centre from the basement to the first

floor or second floor of the building, as it would help the cause in case of floods or in

case of other natural calamities in the future.

Page 10 of 13

11

4. Lastly, the company should be making the records and maintaining the same in the

chronological manner as it would help to retrieve the information anytime in future and

should also plan of insuring the data such that the loss can be minimised (Chron, 2017).

Page 11 of 13

4. Lastly, the company should be making the records and maintaining the same in the

chronological manner as it would help to retrieve the information anytime in future and

should also plan of insuring the data such that the loss can be minimised (Chron, 2017).

Page 11 of 13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.