FNSACC601 & FNSACC603: Administering Tax for Legal Entities Task

VerifiedAdded on 2023/03/30

|34

|6555

|61

Homework Assignment

AI Summary

This assignment solution for FNSACC601 and FNSACC603, part of the Diploma of Accounting, focuses on taxation for legal entities, plans, and obligations. It includes multiple activities based on "Advanced Income Tax Law" and covers topics such as calculating tax for prescribed persons, inter vivos trusts, allocation of partnership net income, and reconciliation of taxable income. The assignment requires students to determine excepted and eligible assessable income, calculate net tax payable, identify beneficiaries' entitlements in trusts, and reconcile accounting profit with taxable income, demonstrating competency in preparing and administering tax documentation and implementing tax plans.

FNS50215 Diploma of Accounting

Module 4.2 Assignment

Instructions:

This assignment contains multiple Assessment Activities

Please complete the Declaration of Authenticity at the bottom of this page

Save this assignment (e.g. on your desktop)

To complete the assignment, read the instructions for each question carefully.

You may be required to refer to your learning materials or other sources to complete

this assessment.

You are required to type all your responses in the spaces provided

Once you have completed all parts of the assignment and saved it, login to the

Monarch Institute LMS to submit your assignment for grading

To submit your assignment click on the file ”Submit Diploma of Accounting Module 4.2

Assignment” in the Module 4.2 section of your course and upload your assignment file.

Please be sure to click “Continue” after clicking “submit”. This ensures your assessor receives

notification of your submission – very important!

Declaration of Understanding and Authenticity *

I have read and understood the assessment instructions provided to me in the Learning Management System.

I certify that the attached material is my original work. No other person’s work has been used without due

acknowledgement. I understand that the work submitted may be reproduced and/or communicated for the purpose

of detecting plagiarism.

Student Name*: Date:

* I understand that by typing my name or inserting a digital signature into this box that I agree and am bound by the

above student declaration.

Diploma of Accounting - Module 4.2 Assignment (2017, 14Ed) 1704 Page 1 of 34

Module 4.2 Assignment

Instructions:

This assignment contains multiple Assessment Activities

Please complete the Declaration of Authenticity at the bottom of this page

Save this assignment (e.g. on your desktop)

To complete the assignment, read the instructions for each question carefully.

You may be required to refer to your learning materials or other sources to complete

this assessment.

You are required to type all your responses in the spaces provided

Once you have completed all parts of the assignment and saved it, login to the

Monarch Institute LMS to submit your assignment for grading

To submit your assignment click on the file ”Submit Diploma of Accounting Module 4.2

Assignment” in the Module 4.2 section of your course and upload your assignment file.

Please be sure to click “Continue” after clicking “submit”. This ensures your assessor receives

notification of your submission – very important!

Declaration of Understanding and Authenticity *

I have read and understood the assessment instructions provided to me in the Learning Management System.

I certify that the attached material is my original work. No other person’s work has been used without due

acknowledgement. I understand that the work submitted may be reproduced and/or communicated for the purpose

of detecting plagiarism.

Student Name*: Date:

* I understand that by typing my name or inserting a digital signature into this box that I agree and am bound by the

above student declaration.

Diploma of Accounting - Module 4.2 Assignment (2017, 14Ed) 1704 Page 1 of 34

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Units Covered: FNSACC601 & FNSACC603

Important assessment information

Aims of this assessment

This assessment focuses on taxation for legal entities, plans and obligations.

Marking and feedback

This assignment contains multiple Assessment Activities each containing specific instructions.

You are required to attempt all questions.

This particular assessment forms part of your overall assessment for the following unit(s) of

competency:

FNSACC601 Prepare and administer tax documentation for legal entities

FNSACC603 Implement tax plans and evaluate tax obligations

Grading for this assessment will be deemed “competent” or “not-yet-competent” in line with

specified educational standards under the Australian Qualifications Framework.

What does “competent” mean?

These answers contain relevant and accurate information in response to the question/s with

limited serious errors in fact or application. If incorrect information is contained in an answer, it

must be fundamentally outweighed by the accurate information provided. This will be assessed

against a marking guide provided to assessors for their determination.

What does “not-yet-competent” mean?

This occurs when an assessment does not meet the marking guide standards provided to

assessors. These answers either do not address the question specifically, or are wrong from a

legislative perspective, or are incorrectly applied. Answers that omit to provide a response to any

significant issue (where multiple issues must be addressed in a question) may also be deemed

not-yet-competent. Answers that have faulty reasoning, a poor standard of expression or include

plagiarism may also be deemed not-yet-competent. Please note, additional information regarding

Monarch’s plagiarism policy is contained in the Student Information Guide which can be found

here: http://www.monarch.edu.au/student-info/

Diploma of Accounting - Module 4.2 Assignment (2017, 14Ed) 1704 Page 2 of 34

Important assessment information

Aims of this assessment

This assessment focuses on taxation for legal entities, plans and obligations.

Marking and feedback

This assignment contains multiple Assessment Activities each containing specific instructions.

You are required to attempt all questions.

This particular assessment forms part of your overall assessment for the following unit(s) of

competency:

FNSACC601 Prepare and administer tax documentation for legal entities

FNSACC603 Implement tax plans and evaluate tax obligations

Grading for this assessment will be deemed “competent” or “not-yet-competent” in line with

specified educational standards under the Australian Qualifications Framework.

What does “competent” mean?

These answers contain relevant and accurate information in response to the question/s with

limited serious errors in fact or application. If incorrect information is contained in an answer, it

must be fundamentally outweighed by the accurate information provided. This will be assessed

against a marking guide provided to assessors for their determination.

What does “not-yet-competent” mean?

This occurs when an assessment does not meet the marking guide standards provided to

assessors. These answers either do not address the question specifically, or are wrong from a

legislative perspective, or are incorrectly applied. Answers that omit to provide a response to any

significant issue (where multiple issues must be addressed in a question) may also be deemed

not-yet-competent. Answers that have faulty reasoning, a poor standard of expression or include

plagiarism may also be deemed not-yet-competent. Please note, additional information regarding

Monarch’s plagiarism policy is contained in the Student Information Guide which can be found

here: http://www.monarch.edu.au/student-info/

Diploma of Accounting - Module 4.2 Assignment (2017, 14Ed) 1704 Page 2 of 34

Units Covered: FNSACC601 & FNSACC603

What happens if you are deemed not-yet-competent?

In the event you do not achieve competency by your assessor on this assessment, you will be

given one more opportunity to re-submit the assessment after consultation with your Trainer/

Assessor. You will know your assessment is deemed ‘not-yet-competent’ if your grade book in the

Monarch LMS says “NYC” after you have received an email from your assessor advising your

assessment has been graded.

Important: It is your responsibility to ensure your assessment resubmission addresses all areas

deemed unsatisfactory by your assessor. Please note, if you are still unsuccessful in meeting

competency after resubmitting your assessment, you will be required to repeat those units.

In the event that you have concerns about the assessment decision then you can refer to our

Complaints & Appeals process also contained within the Student Information Guide.

Expectations from your assessor when answering different types of assessment questions:

Knowledge based questions:

A knowledge based question requires you to clearly identify and cover the key subject matter

areas raised in the question in full as part of the response.

Performance based questions:

A performance based question requires you to clearly demonstrate your ability to complete

certain tasks, that is, to perform these tasks.

Good luck

Finally, good luck with your learning and assessments and remember your trainers are here to

assist you

Diploma of Accounting - Module 4.2 Assignment (2017, 14Ed) 1704 Page 3 of 34

What happens if you are deemed not-yet-competent?

In the event you do not achieve competency by your assessor on this assessment, you will be

given one more opportunity to re-submit the assessment after consultation with your Trainer/

Assessor. You will know your assessment is deemed ‘not-yet-competent’ if your grade book in the

Monarch LMS says “NYC” after you have received an email from your assessor advising your

assessment has been graded.

Important: It is your responsibility to ensure your assessment resubmission addresses all areas

deemed unsatisfactory by your assessor. Please note, if you are still unsuccessful in meeting

competency after resubmitting your assessment, you will be required to repeat those units.

In the event that you have concerns about the assessment decision then you can refer to our

Complaints & Appeals process also contained within the Student Information Guide.

Expectations from your assessor when answering different types of assessment questions:

Knowledge based questions:

A knowledge based question requires you to clearly identify and cover the key subject matter

areas raised in the question in full as part of the response.

Performance based questions:

A performance based question requires you to clearly demonstrate your ability to complete

certain tasks, that is, to perform these tasks.

Good luck

Finally, good luck with your learning and assessments and remember your trainers are here to

assist you

Diploma of Accounting - Module 4.2 Assignment (2017, 14Ed) 1704 Page 3 of 34

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Units Covered: FNSACC601 & FNSACC603

Assessment Activities

Short Answer and Worked Answer Questions

FNSACC601 Prepare and administer tax documentation for legal entities

FNSACC603 Implement tax plans and evaluate tax obligations

The following questions are based on the material in the textbook “Advanced Income Tax Law” by Peter Baker,

Geoff Cliff & Sonia Deaner, 14th Edition (January 2017)

Activity instructions to candidates

This is an open book assessment activity.

You may use a financial calculator or computer application to help calculate values

You are required to read this assessment and answer all questions that follow.

Please type your answers in the spaces provided.

Please ensure you have read “Important assessment information” at the front of this assessment

Estimated time for completion of this assessment activity: approximately 3 hours

Diploma of Accounting - Module 4.2 Assignment (2017, 14Ed) 1704 Page 4 of 34

Assessment Activities

Short Answer and Worked Answer Questions

FNSACC601 Prepare and administer tax documentation for legal entities

FNSACC603 Implement tax plans and evaluate tax obligations

The following questions are based on the material in the textbook “Advanced Income Tax Law” by Peter Baker,

Geoff Cliff & Sonia Deaner, 14th Edition (January 2017)

Activity instructions to candidates

This is an open book assessment activity.

You may use a financial calculator or computer application to help calculate values

You are required to read this assessment and answer all questions that follow.

Please type your answers in the spaces provided.

Please ensure you have read “Important assessment information” at the front of this assessment

Estimated time for completion of this assessment activity: approximately 3 hours

Diploma of Accounting - Module 4.2 Assignment (2017, 14Ed) 1704 Page 4 of 34

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Units Covered: FNSACC601 & FNSACC603

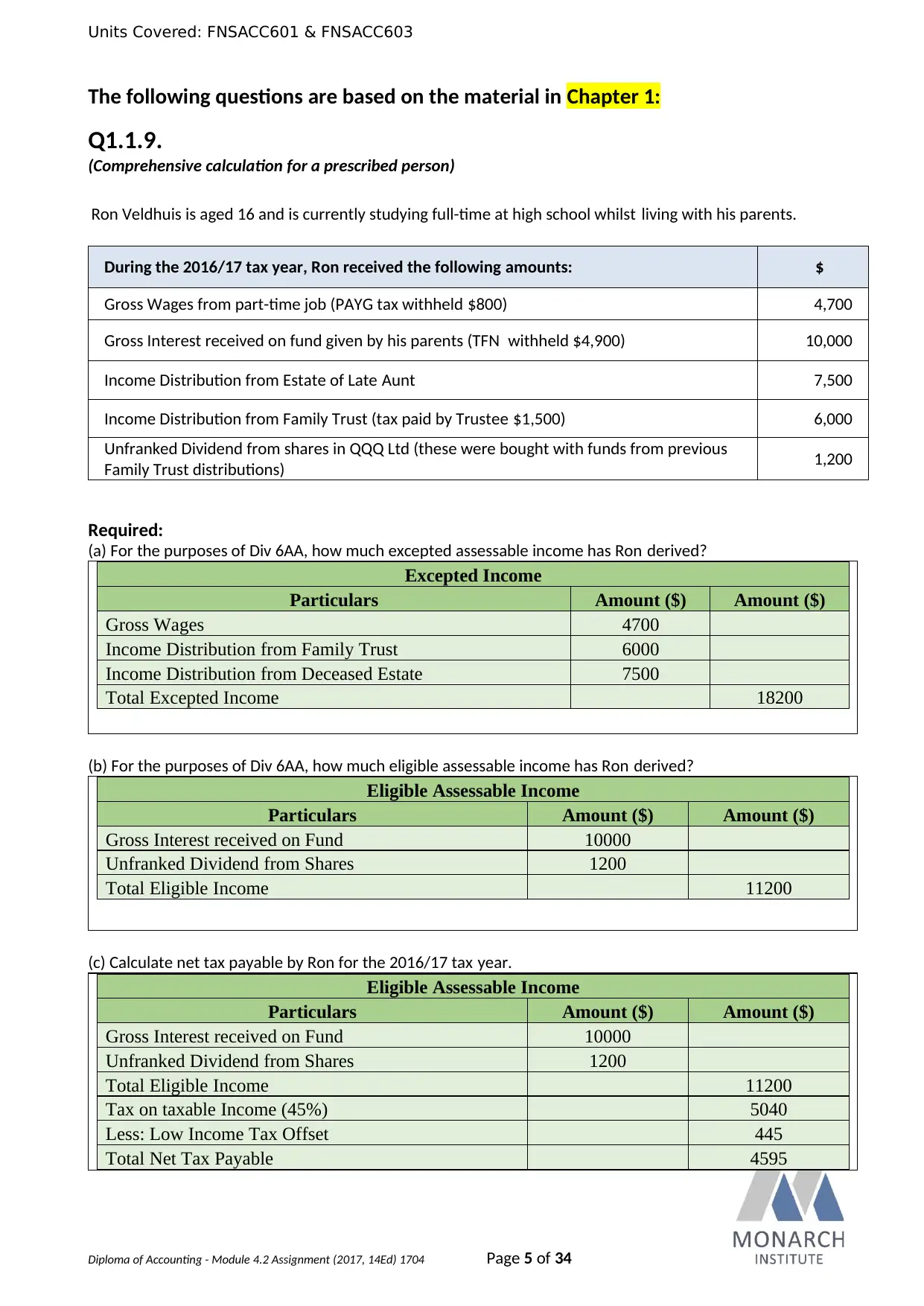

The following questions are based on the material in Chapter 1:

Q1.1.9.

(Comprehensive calculation for a prescribed person)

Ron Veldhuis is aged 16 and is currently studying full-time at high school whilst living with his parents.

During the 2016/17 tax year, Ron received the following amounts: $

Gross Wages from part-time job (PAYG tax withheld $800) 4,700

Gross Interest received on fund given by his parents (TFN withheld $4,900) 10,000

Income Distribution from Estate of Late Aunt 7,500

Income Distribution from Family Trust (tax paid by Trustee $1,500) 6,000

Unfranked Dividend from shares in QQQ Ltd (these were bought with funds from previous

Family Trust distributions) 1,200

Required:

(a) For the purposes of Div 6AA, how much excepted assessable income has Ron derived?

Excepted Income

Particulars Amount ($) Amount ($)

Gross Wages 4700

Income Distribution from Family Trust 6000

Income Distribution from Deceased Estate 7500

Total Excepted Income 18200

(b) For the purposes of Div 6AA, how much eligible assessable income has Ron derived?

Eligible Assessable Income

Particulars Amount ($) Amount ($)

Gross Interest received on Fund 10000

Unfranked Dividend from Shares 1200

Total Eligible Income 11200

(c) Calculate net tax payable by Ron for the 2016/17 tax year.

Eligible Assessable Income

Particulars Amount ($) Amount ($)

Gross Interest received on Fund 10000

Unfranked Dividend from Shares 1200

Total Eligible Income 11200

Tax on taxable Income (45%) 5040

Less: Low Income Tax Offset 445

Total Net Tax Payable 4595

Diploma of Accounting - Module 4.2 Assignment (2017, 14Ed) 1704 Page 5 of 34

The following questions are based on the material in Chapter 1:

Q1.1.9.

(Comprehensive calculation for a prescribed person)

Ron Veldhuis is aged 16 and is currently studying full-time at high school whilst living with his parents.

During the 2016/17 tax year, Ron received the following amounts: $

Gross Wages from part-time job (PAYG tax withheld $800) 4,700

Gross Interest received on fund given by his parents (TFN withheld $4,900) 10,000

Income Distribution from Estate of Late Aunt 7,500

Income Distribution from Family Trust (tax paid by Trustee $1,500) 6,000

Unfranked Dividend from shares in QQQ Ltd (these were bought with funds from previous

Family Trust distributions) 1,200

Required:

(a) For the purposes of Div 6AA, how much excepted assessable income has Ron derived?

Excepted Income

Particulars Amount ($) Amount ($)

Gross Wages 4700

Income Distribution from Family Trust 6000

Income Distribution from Deceased Estate 7500

Total Excepted Income 18200

(b) For the purposes of Div 6AA, how much eligible assessable income has Ron derived?

Eligible Assessable Income

Particulars Amount ($) Amount ($)

Gross Interest received on Fund 10000

Unfranked Dividend from Shares 1200

Total Eligible Income 11200

(c) Calculate net tax payable by Ron for the 2016/17 tax year.

Eligible Assessable Income

Particulars Amount ($) Amount ($)

Gross Interest received on Fund 10000

Unfranked Dividend from Shares 1200

Total Eligible Income 11200

Tax on taxable Income (45%) 5040

Less: Low Income Tax Offset 445

Total Net Tax Payable 4595

Diploma of Accounting - Module 4.2 Assignment (2017, 14Ed) 1704 Page 5 of 34

Units Covered: FNSACC601 & FNSACC603

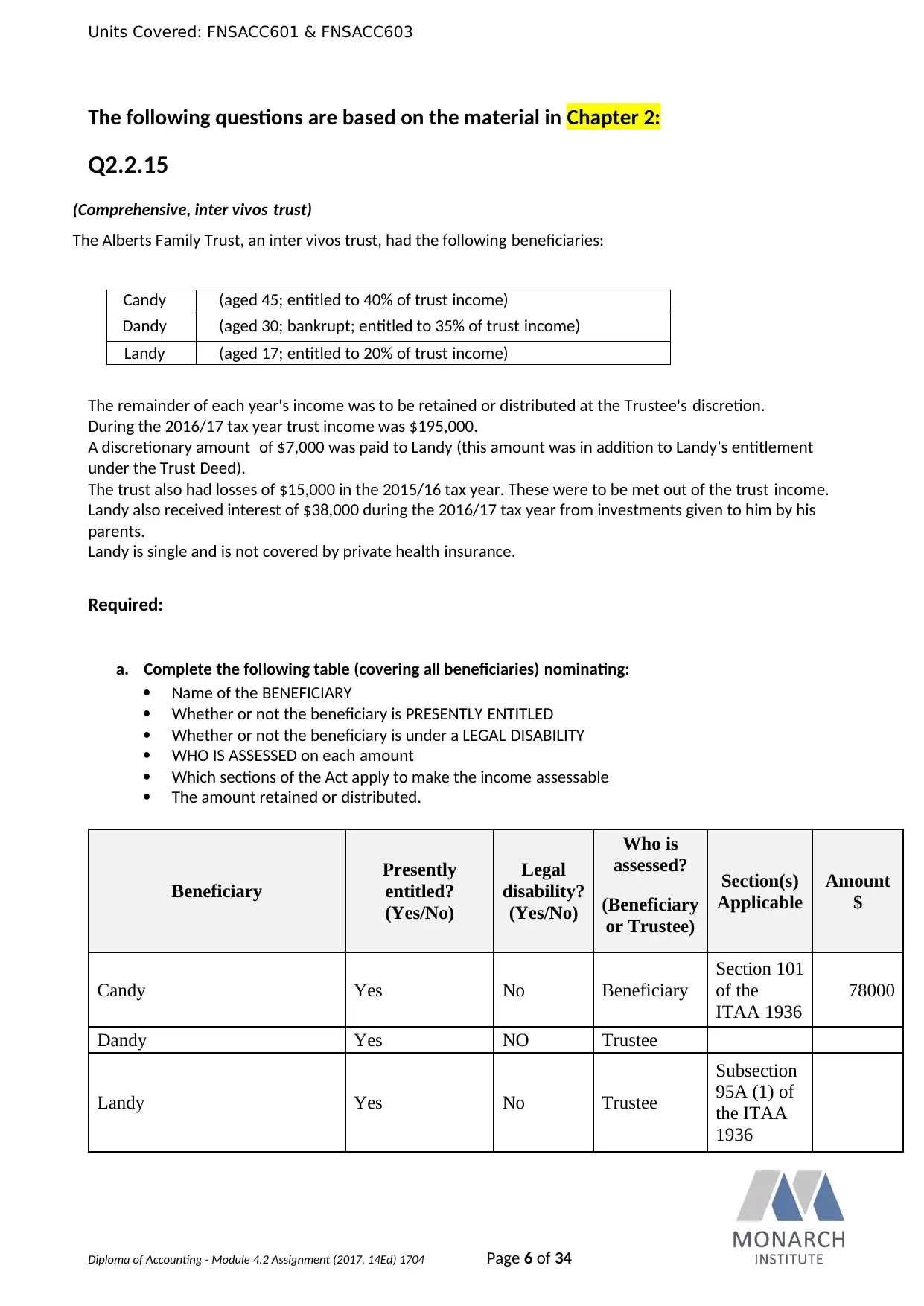

The following questions are based on the material in Chapter 2:

Q2.2.15

(Comprehensive, inter vivos trust)

The Alberts Family Trust, an inter vivos trust, had the following beneficiaries:

Candy (aged 45; entitled to 40% of trust income)

Dandy (aged 30; bankrupt; entitled to 35% of trust income)

Landy (aged 17; entitled to 20% of trust income)

The remainder of each year's income was to be retained or distributed at the Trustee's discretion.

During the 2016/17 tax year trust income was $195,000.

A discretionary amount of $7,000 was paid to Landy (this amount was in addition to Landy’s entitlement

under the Trust Deed).

The trust also had losses of $15,000 in the 2015/16 tax year. These were to be met out of the trust income.

Landy also received interest of $38,000 during the 2016/17 tax year from investments given to him by his

parents.

Landy is single and is not covered by private health insurance.

Required:

a. Complete the following table (covering all beneficiaries) nominating:

Name of the BENEFICIARY

Whether or not the beneficiary is PRESENTLY ENTITLED

Whether or not the beneficiary is under a LEGAL DISABILITY

WHO IS ASSESSED on each amount

Which sections of the Act apply to make the income assessable

The amount retained or distributed.

Beneficiary

Presently

entitled?

(Yes/No)

Legal

disability?

(Yes/No)

Who is

assessed? Section(s)

Applicable

Amount

$(Beneficiary

or Trustee)

Candy Yes No Beneficiary

Section 101

of the

ITAA 1936

78000

Dandy Yes NO Trustee

Landy Yes No Trustee

Subsection

95A (1) of

the ITAA

1936

Diploma of Accounting - Module 4.2 Assignment (2017, 14Ed) 1704 Page 6 of 34

The following questions are based on the material in Chapter 2:

Q2.2.15

(Comprehensive, inter vivos trust)

The Alberts Family Trust, an inter vivos trust, had the following beneficiaries:

Candy (aged 45; entitled to 40% of trust income)

Dandy (aged 30; bankrupt; entitled to 35% of trust income)

Landy (aged 17; entitled to 20% of trust income)

The remainder of each year's income was to be retained or distributed at the Trustee's discretion.

During the 2016/17 tax year trust income was $195,000.

A discretionary amount of $7,000 was paid to Landy (this amount was in addition to Landy’s entitlement

under the Trust Deed).

The trust also had losses of $15,000 in the 2015/16 tax year. These were to be met out of the trust income.

Landy also received interest of $38,000 during the 2016/17 tax year from investments given to him by his

parents.

Landy is single and is not covered by private health insurance.

Required:

a. Complete the following table (covering all beneficiaries) nominating:

Name of the BENEFICIARY

Whether or not the beneficiary is PRESENTLY ENTITLED

Whether or not the beneficiary is under a LEGAL DISABILITY

WHO IS ASSESSED on each amount

Which sections of the Act apply to make the income assessable

The amount retained or distributed.

Beneficiary

Presently

entitled?

(Yes/No)

Legal

disability?

(Yes/No)

Who is

assessed? Section(s)

Applicable

Amount

$(Beneficiary

or Trustee)

Candy Yes No Beneficiary

Section 101

of the

ITAA 1936

78000

Dandy Yes NO Trustee

Landy Yes No Trustee

Subsection

95A (1) of

the ITAA

1936

Diploma of Accounting - Module 4.2 Assignment (2017, 14Ed) 1704 Page 6 of 34

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Units Covered: FNSACC601 & FNSACC603

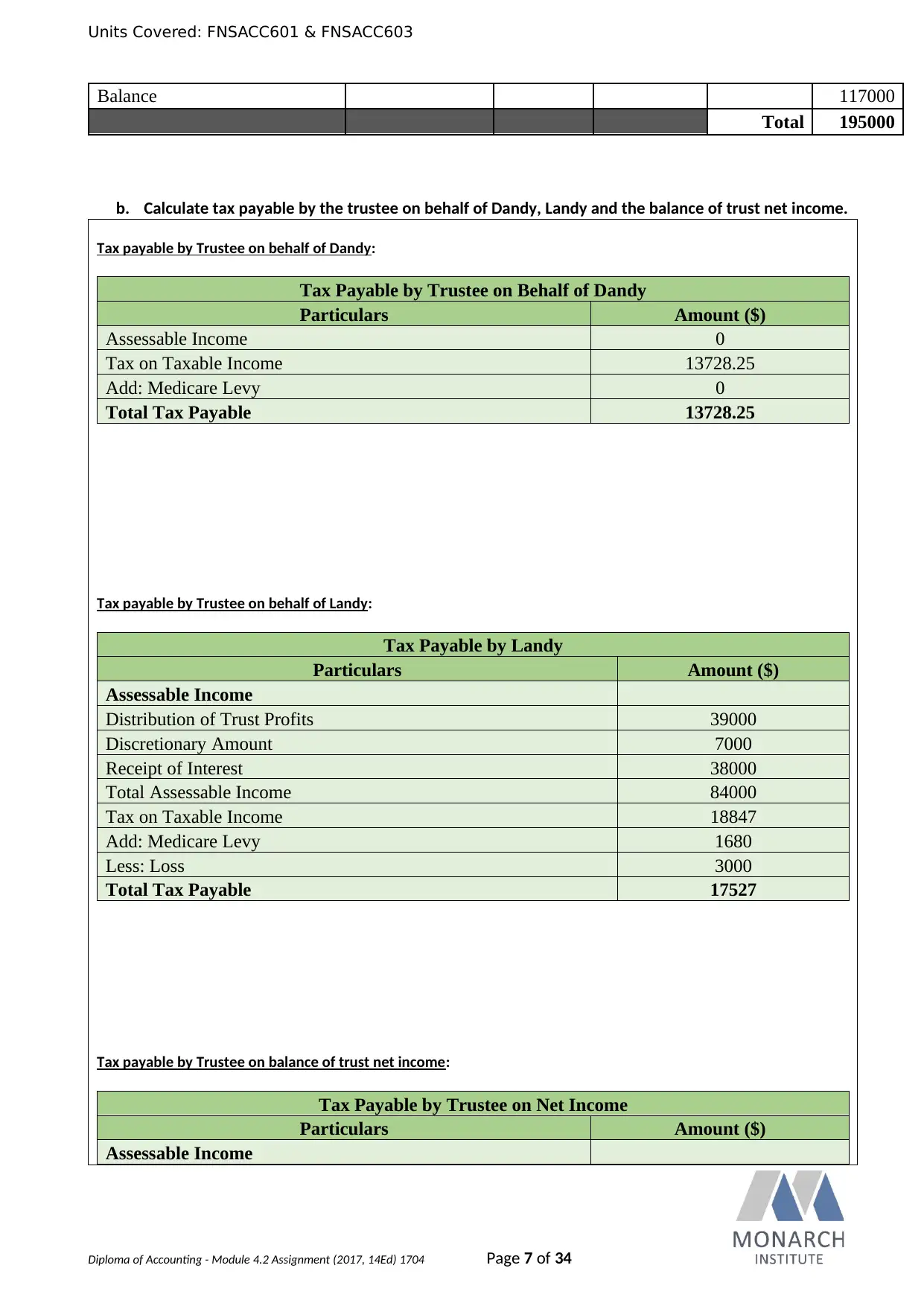

Balance 117000

Total 195000

b. Calculate tax payable by the trustee on behalf of Dandy, Landy and the balance of trust net income.

Tax payable by Trustee on behalf of Dandy:

Tax Payable by Trustee on Behalf of Dandy

Particulars Amount ($)

Assessable Income 0

Tax on Taxable Income 13728.25

Add: Medicare Levy 0

Total Tax Payable 13728.25

Tax payable by Trustee on behalf of Landy:

Tax Payable by Landy

Particulars Amount ($)

Assessable Income

Distribution of Trust Profits 39000

Discretionary Amount 7000

Receipt of Interest 38000

Total Assessable Income 84000

Tax on Taxable Income 18847

Add: Medicare Levy 1680

Less: Loss 3000

Total Tax Payable 17527

Tax payable by Trustee on balance of trust net income:

Tax Payable by Trustee on Net Income

Particulars Amount ($)

Assessable Income

Diploma of Accounting - Module 4.2 Assignment (2017, 14Ed) 1704 Page 7 of 34

Balance 117000

Total 195000

b. Calculate tax payable by the trustee on behalf of Dandy, Landy and the balance of trust net income.

Tax payable by Trustee on behalf of Dandy:

Tax Payable by Trustee on Behalf of Dandy

Particulars Amount ($)

Assessable Income 0

Tax on Taxable Income 13728.25

Add: Medicare Levy 0

Total Tax Payable 13728.25

Tax payable by Trustee on behalf of Landy:

Tax Payable by Landy

Particulars Amount ($)

Assessable Income

Distribution of Trust Profits 39000

Discretionary Amount 7000

Receipt of Interest 38000

Total Assessable Income 84000

Tax on Taxable Income 18847

Add: Medicare Levy 1680

Less: Loss 3000

Total Tax Payable 17527

Tax payable by Trustee on balance of trust net income:

Tax Payable by Trustee on Net Income

Particulars Amount ($)

Assessable Income

Diploma of Accounting - Module 4.2 Assignment (2017, 14Ed) 1704 Page 7 of 34

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Units Covered: FNSACC601 & FNSACC603

Balance Amount 117000

Tax on Taxable Income 30922

Add: Medicare Levy 2340

Total Tax Payable 33262

c. Calculate tax payable by Landy (only).

Tax Payable by Landy

Particulars Amount ($)

Assessable Income

Distribution of Trust Profits 39000

Discritionary Amount 7000

Receipt of Interest 38000

Total Assessable Income 84000

Tax on Taxable Income 18847

Add: Medicare Levy 1680

Less: Loss 3000

Total Tax Payable 17527

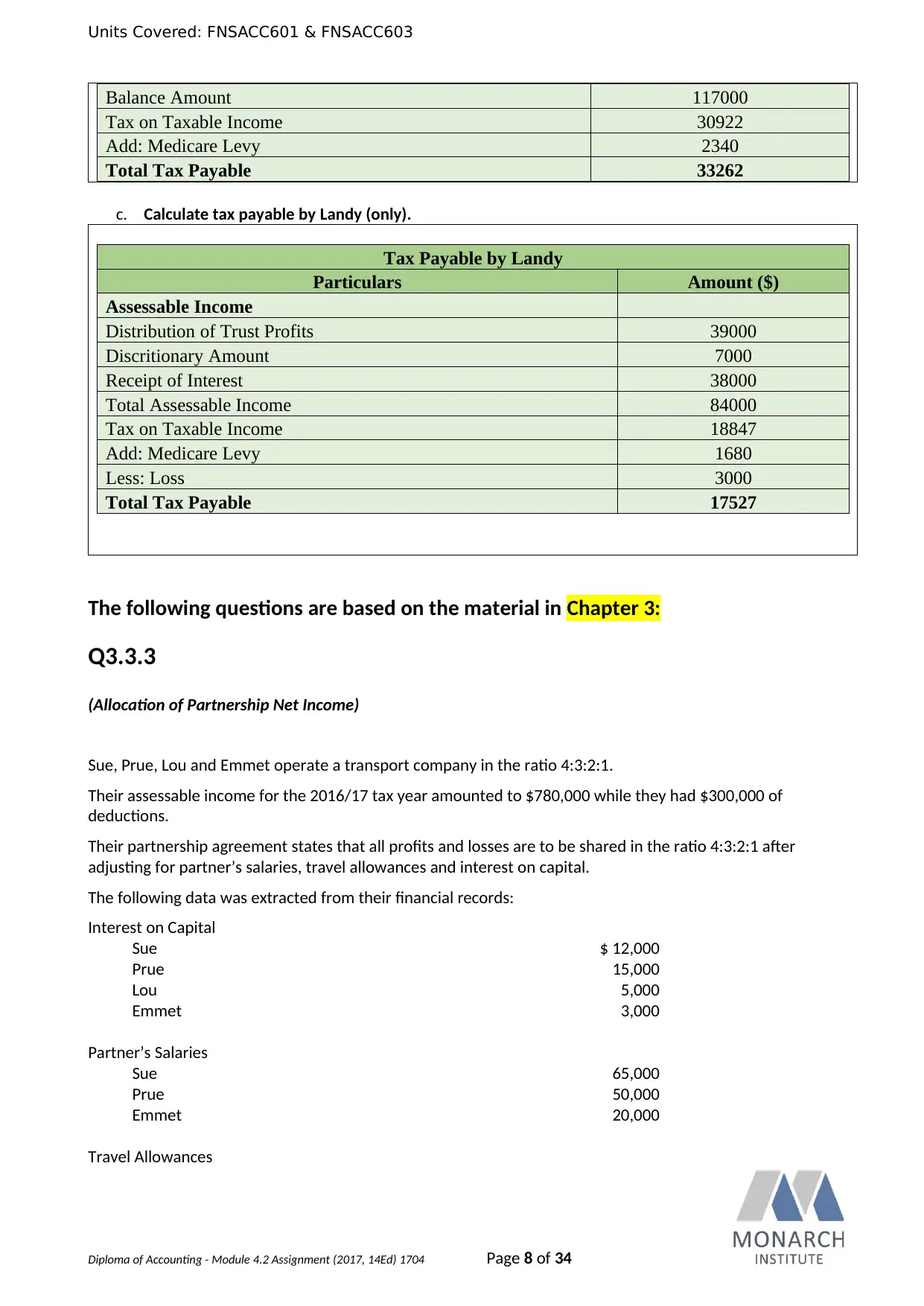

The following questions are based on the material in Chapter 3:

Q3.3.3

(Allocation of Partnership Net Income)

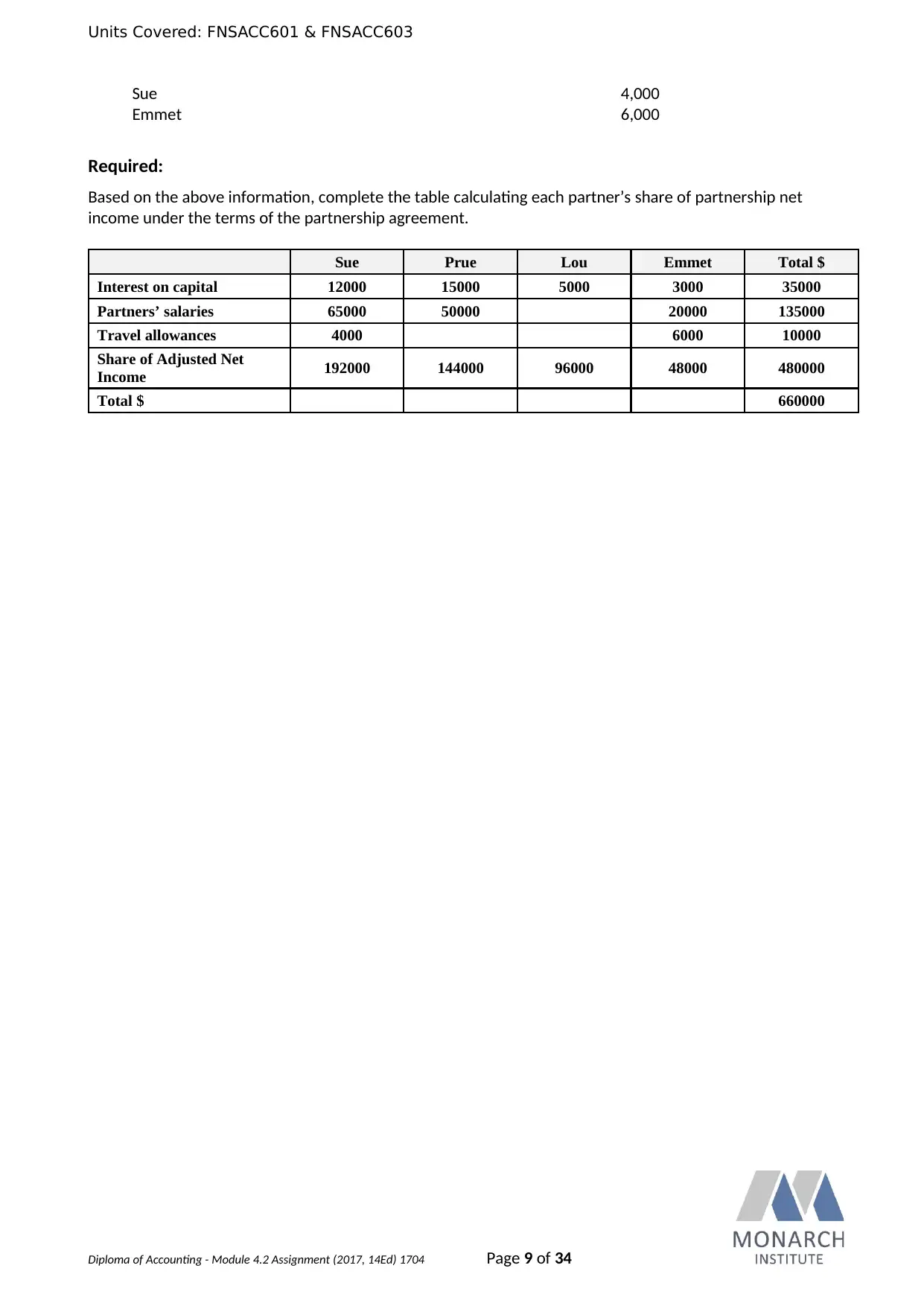

Sue, Prue, Lou and Emmet operate a transport company in the ratio 4:3:2:1.

Their assessable income for the 2016/17 tax year amounted to $780,000 while they had $300,000 of

deductions.

Their partnership agreement states that all profits and losses are to be shared in the ratio 4:3:2:1 after

adjusting for partner’s salaries, travel allowances and interest on capital.

The following data was extracted from their financial records:

Interest on Capital

Sue $ 12,000

Prue 15,000

Lou 5,000

Emmet 3,000

Partner’s Salaries

Sue 65,000

Prue 50,000

Emmet 20,000

Travel Allowances

Diploma of Accounting - Module 4.2 Assignment (2017, 14Ed) 1704 Page 8 of 34

Balance Amount 117000

Tax on Taxable Income 30922

Add: Medicare Levy 2340

Total Tax Payable 33262

c. Calculate tax payable by Landy (only).

Tax Payable by Landy

Particulars Amount ($)

Assessable Income

Distribution of Trust Profits 39000

Discritionary Amount 7000

Receipt of Interest 38000

Total Assessable Income 84000

Tax on Taxable Income 18847

Add: Medicare Levy 1680

Less: Loss 3000

Total Tax Payable 17527

The following questions are based on the material in Chapter 3:

Q3.3.3

(Allocation of Partnership Net Income)

Sue, Prue, Lou and Emmet operate a transport company in the ratio 4:3:2:1.

Their assessable income for the 2016/17 tax year amounted to $780,000 while they had $300,000 of

deductions.

Their partnership agreement states that all profits and losses are to be shared in the ratio 4:3:2:1 after

adjusting for partner’s salaries, travel allowances and interest on capital.

The following data was extracted from their financial records:

Interest on Capital

Sue $ 12,000

Prue 15,000

Lou 5,000

Emmet 3,000

Partner’s Salaries

Sue 65,000

Prue 50,000

Emmet 20,000

Travel Allowances

Diploma of Accounting - Module 4.2 Assignment (2017, 14Ed) 1704 Page 8 of 34

Units Covered: FNSACC601 & FNSACC603

Sue 4,000

Emmet 6,000

Required:

Based on the above information, complete the table calculating each partner’s share of partnership net

income under the terms of the partnership agreement.

Sue Prue Lou Emmet Total $

Interest on capital 12000 15000 5000 3000 35000

Partners’ salaries 65000 50000 20000 135000

Travel allowances 4000 6000 10000

Share of Adjusted Net

Income 192000 144000 96000 48000 480000

Total $ 660000

Diploma of Accounting - Module 4.2 Assignment (2017, 14Ed) 1704 Page 9 of 34

Sue 4,000

Emmet 6,000

Required:

Based on the above information, complete the table calculating each partner’s share of partnership net

income under the terms of the partnership agreement.

Sue Prue Lou Emmet Total $

Interest on capital 12000 15000 5000 3000 35000

Partners’ salaries 65000 50000 20000 135000

Travel allowances 4000 6000 10000

Share of Adjusted Net

Income 192000 144000 96000 48000 480000

Total $ 660000

Diploma of Accounting - Module 4.2 Assignment (2017, 14Ed) 1704 Page 9 of 34

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Units Covered: FNSACC601 & FNSACC603

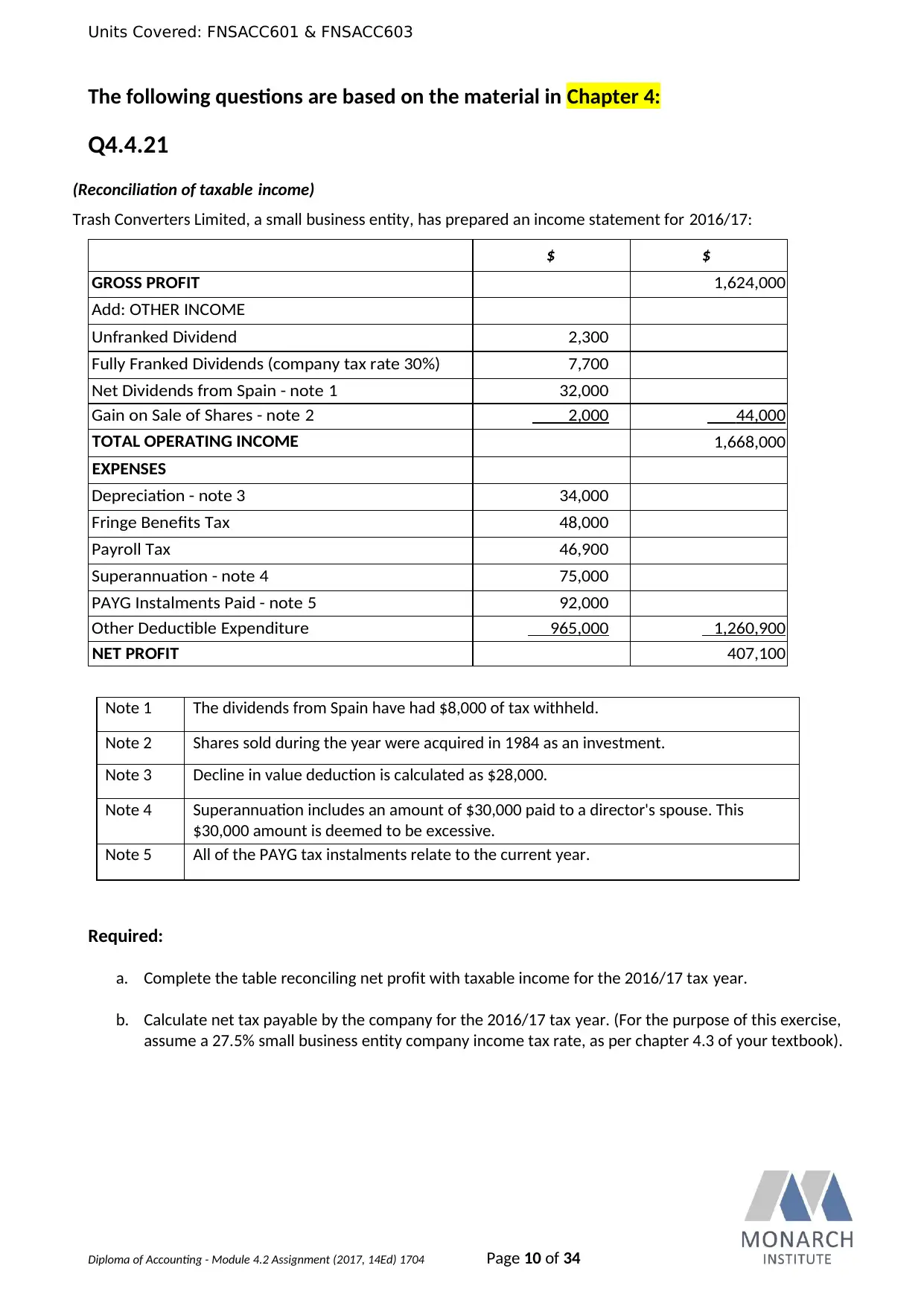

The following questions are based on the material in Chapter 4:

Q4.4.21

(Reconciliation of taxable income)

Trash Converters Limited, a small business entity, has prepared an income statement for 2016/17:

$ $

GROSS PROFIT 1,624,000

Add: OTHER INCOME

Unfranked Dividend 2,300

Fully Franked Dividends (company tax rate 30%) 7,700

Net Dividends from Spain - note 1 32,000

Gain on Sale of Shares - note 2 2,000 44,000

TOTAL OPERATING INCOME 1,668,000

EXPENSES

Depreciation - note 3 34,000

Fringe Benefits Tax 48,000

Payroll Tax 46,900

Superannuation - note 4 75,000

PAYG Instalments Paid - note 5 92,000

Other Deductible Expenditure 965,000 1,260,900

NET PROFIT 407,100

Note 1 The dividends from Spain have had $8,000 of tax withheld.

Note 2 Shares sold during the year were acquired in 1984 as an investment.

Note 3 Decline in value deduction is calculated as $28,000.

Note 4 Superannuation includes an amount of $30,000 paid to a director's spouse. This

$30,000 amount is deemed to be excessive.

Note 5 All of the PAYG tax instalments relate to the current year.

Required:

a. Complete the table reconciling net profit with taxable income for the 2016/17 tax year.

b. Calculate net tax payable by the company for the 2016/17 tax year. (For the purpose of this exercise,

assume a 27.5% small business entity company income tax rate, as per chapter 4.3 of your textbook).

Diploma of Accounting - Module 4.2 Assignment (2017, 14Ed) 1704 Page 10 of 34

The following questions are based on the material in Chapter 4:

Q4.4.21

(Reconciliation of taxable income)

Trash Converters Limited, a small business entity, has prepared an income statement for 2016/17:

$ $

GROSS PROFIT 1,624,000

Add: OTHER INCOME

Unfranked Dividend 2,300

Fully Franked Dividends (company tax rate 30%) 7,700

Net Dividends from Spain - note 1 32,000

Gain on Sale of Shares - note 2 2,000 44,000

TOTAL OPERATING INCOME 1,668,000

EXPENSES

Depreciation - note 3 34,000

Fringe Benefits Tax 48,000

Payroll Tax 46,900

Superannuation - note 4 75,000

PAYG Instalments Paid - note 5 92,000

Other Deductible Expenditure 965,000 1,260,900

NET PROFIT 407,100

Note 1 The dividends from Spain have had $8,000 of tax withheld.

Note 2 Shares sold during the year were acquired in 1984 as an investment.

Note 3 Decline in value deduction is calculated as $28,000.

Note 4 Superannuation includes an amount of $30,000 paid to a director's spouse. This

$30,000 amount is deemed to be excessive.

Note 5 All of the PAYG tax instalments relate to the current year.

Required:

a. Complete the table reconciling net profit with taxable income for the 2016/17 tax year.

b. Calculate net tax payable by the company for the 2016/17 tax year. (For the purpose of this exercise,

assume a 27.5% small business entity company income tax rate, as per chapter 4.3 of your textbook).

Diploma of Accounting - Module 4.2 Assignment (2017, 14Ed) 1704 Page 10 of 34

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Units Covered: FNSACC601 & FNSACC603

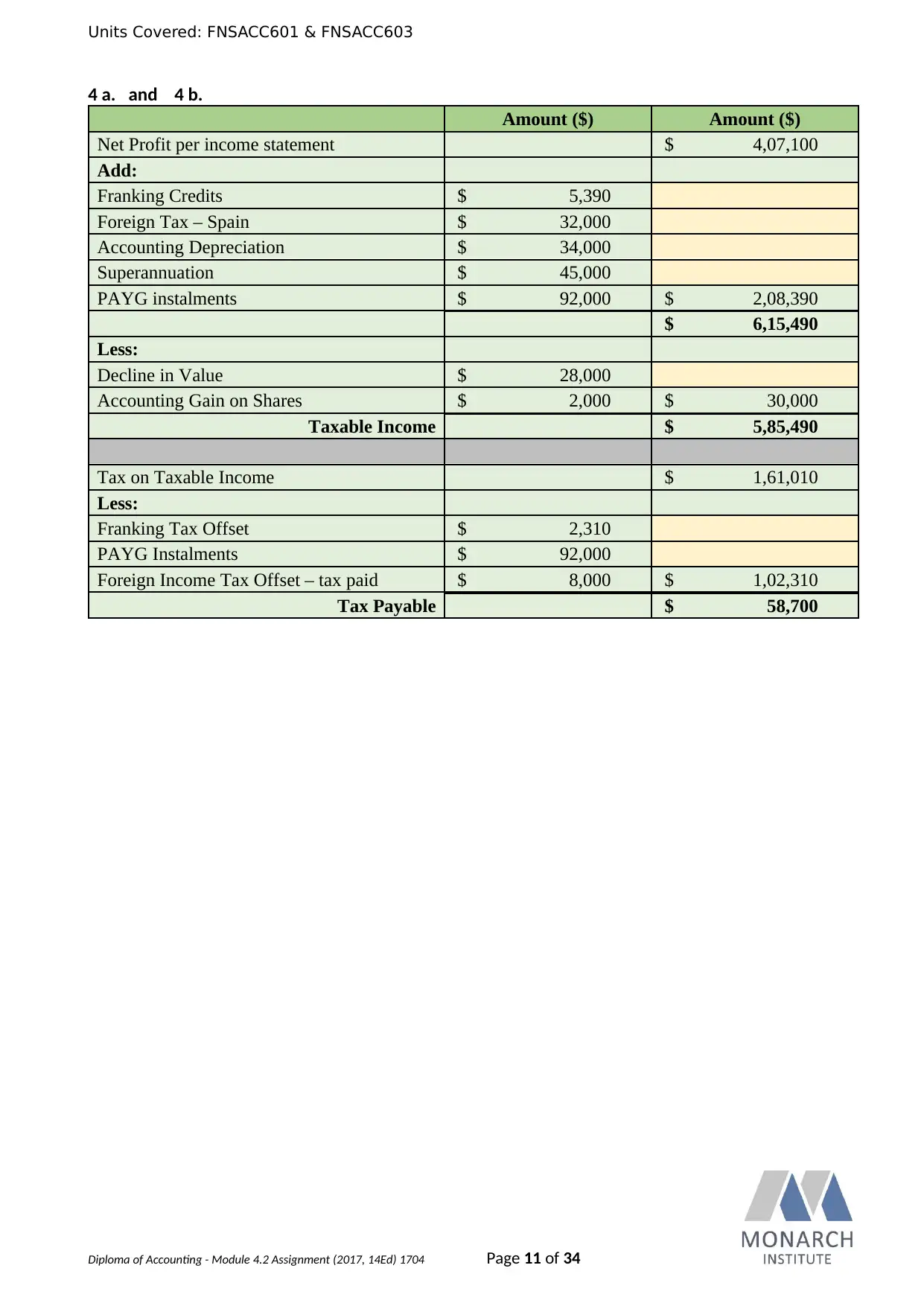

4 a. and 4 b.

Amount ($) Amount ($)

Net Profit per income statement $ 4,07,100

Add:

Franking Credits $ 5,390

Foreign Tax – Spain $ 32,000

Accounting Depreciation $ 34,000

Superannuation $ 45,000

PAYG instalments $ 92,000 $ 2,08,390

$ 6,15,490

Less:

Decline in Value $ 28,000

Accounting Gain on Shares $ 2,000 $ 30,000

Taxable Income $ 5,85,490

Tax on Taxable Income $ 1,61,010

Less:

Franking Tax Offset $ 2,310

PAYG Instalments $ 92,000

Foreign Income Tax Offset – tax paid $ 8,000 $ 1,02,310

Tax Payable $ 58,700

Diploma of Accounting - Module 4.2 Assignment (2017, 14Ed) 1704 Page 11 of 34

4 a. and 4 b.

Amount ($) Amount ($)

Net Profit per income statement $ 4,07,100

Add:

Franking Credits $ 5,390

Foreign Tax – Spain $ 32,000

Accounting Depreciation $ 34,000

Superannuation $ 45,000

PAYG instalments $ 92,000 $ 2,08,390

$ 6,15,490

Less:

Decline in Value $ 28,000

Accounting Gain on Shares $ 2,000 $ 30,000

Taxable Income $ 5,85,490

Tax on Taxable Income $ 1,61,010

Less:

Franking Tax Offset $ 2,310

PAYG Instalments $ 92,000

Foreign Income Tax Offset – tax paid $ 8,000 $ 1,02,310

Tax Payable $ 58,700

Diploma of Accounting - Module 4.2 Assignment (2017, 14Ed) 1704 Page 11 of 34

Units Covered: FNSACC601 & FNSACC603

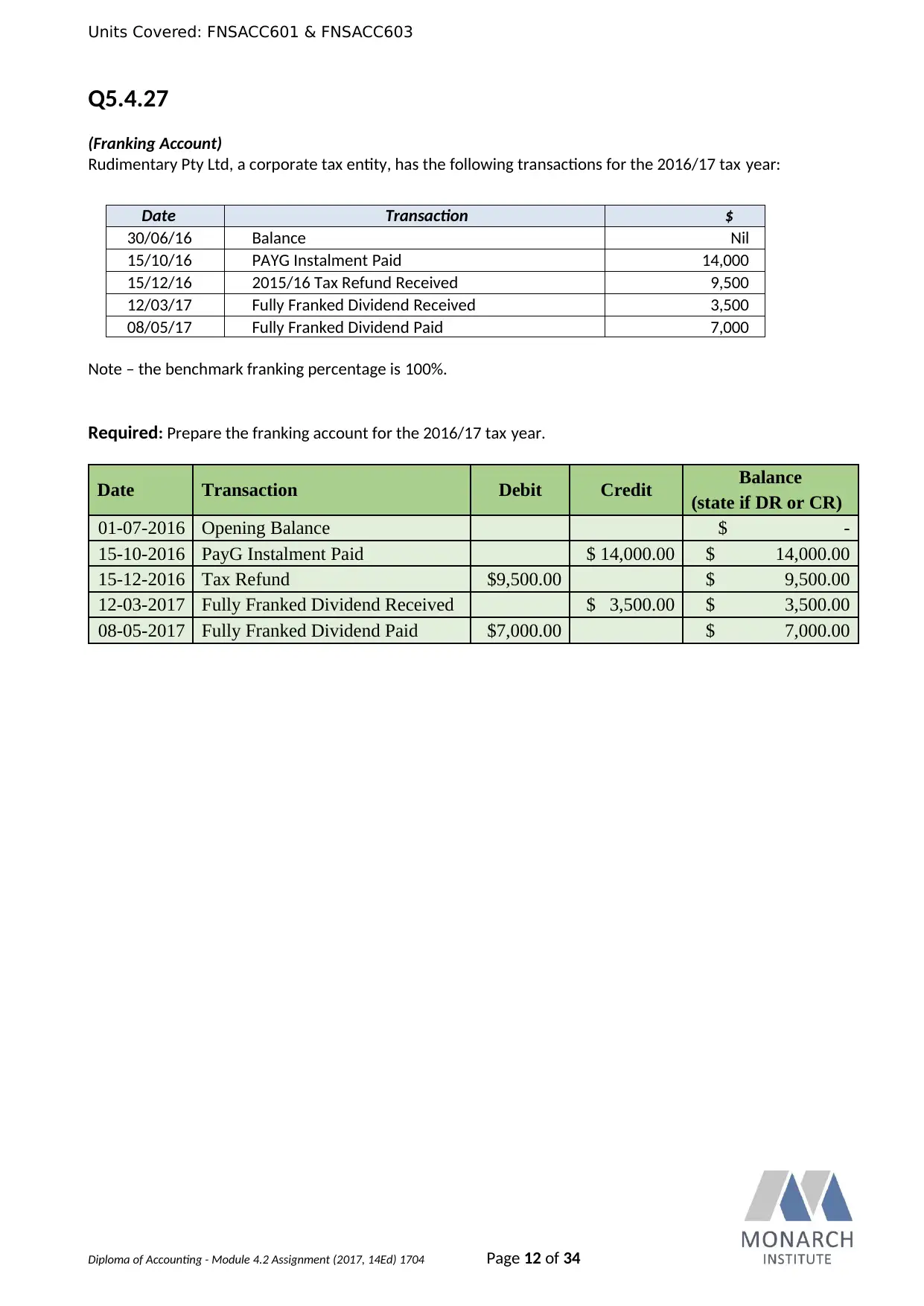

Q5.4.27

(Franking Account)

Rudimentary Pty Ltd, a corporate tax entity, has the following transactions for the 2016/17 tax year:

Date Transaction $

30/06/16 Balance Nil

15/10/16 PAYG Instalment Paid 14,000

15/12/16 2015/16 Tax Refund Received 9,500

12/03/17 Fully Franked Dividend Received 3,500

08/05/17 Fully Franked Dividend Paid 7,000

Note – the benchmark franking percentage is 100%.

Required: Prepare the franking account for the 2016/17 tax year.

Date Transaction Debit Credit Balance

(state if DR or CR)

01-07-2016 Opening Balance $ -

15-10-2016 PayG Instalment Paid $ 14,000.00 $ 14,000.00

15-12-2016 Tax Refund $9,500.00 $ 9,500.00

12-03-2017 Fully Franked Dividend Received $ 3,500.00 $ 3,500.00

08-05-2017 Fully Franked Dividend Paid $7,000.00 $ 7,000.00

Diploma of Accounting - Module 4.2 Assignment (2017, 14Ed) 1704 Page 12 of 34

Q5.4.27

(Franking Account)

Rudimentary Pty Ltd, a corporate tax entity, has the following transactions for the 2016/17 tax year:

Date Transaction $

30/06/16 Balance Nil

15/10/16 PAYG Instalment Paid 14,000

15/12/16 2015/16 Tax Refund Received 9,500

12/03/17 Fully Franked Dividend Received 3,500

08/05/17 Fully Franked Dividend Paid 7,000

Note – the benchmark franking percentage is 100%.

Required: Prepare the franking account for the 2016/17 tax year.

Date Transaction Debit Credit Balance

(state if DR or CR)

01-07-2016 Opening Balance $ -

15-10-2016 PayG Instalment Paid $ 14,000.00 $ 14,000.00

15-12-2016 Tax Refund $9,500.00 $ 9,500.00

12-03-2017 Fully Franked Dividend Received $ 3,500.00 $ 3,500.00

08-05-2017 Fully Franked Dividend Paid $7,000.00 $ 7,000.00

Diploma of Accounting - Module 4.2 Assignment (2017, 14Ed) 1704 Page 12 of 34

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 34

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.