Taxation Report: University Taxation and Financial Reporting Analysis

VerifiedAdded on 2020/04/15

|14

|2639

|35

Report

AI Summary

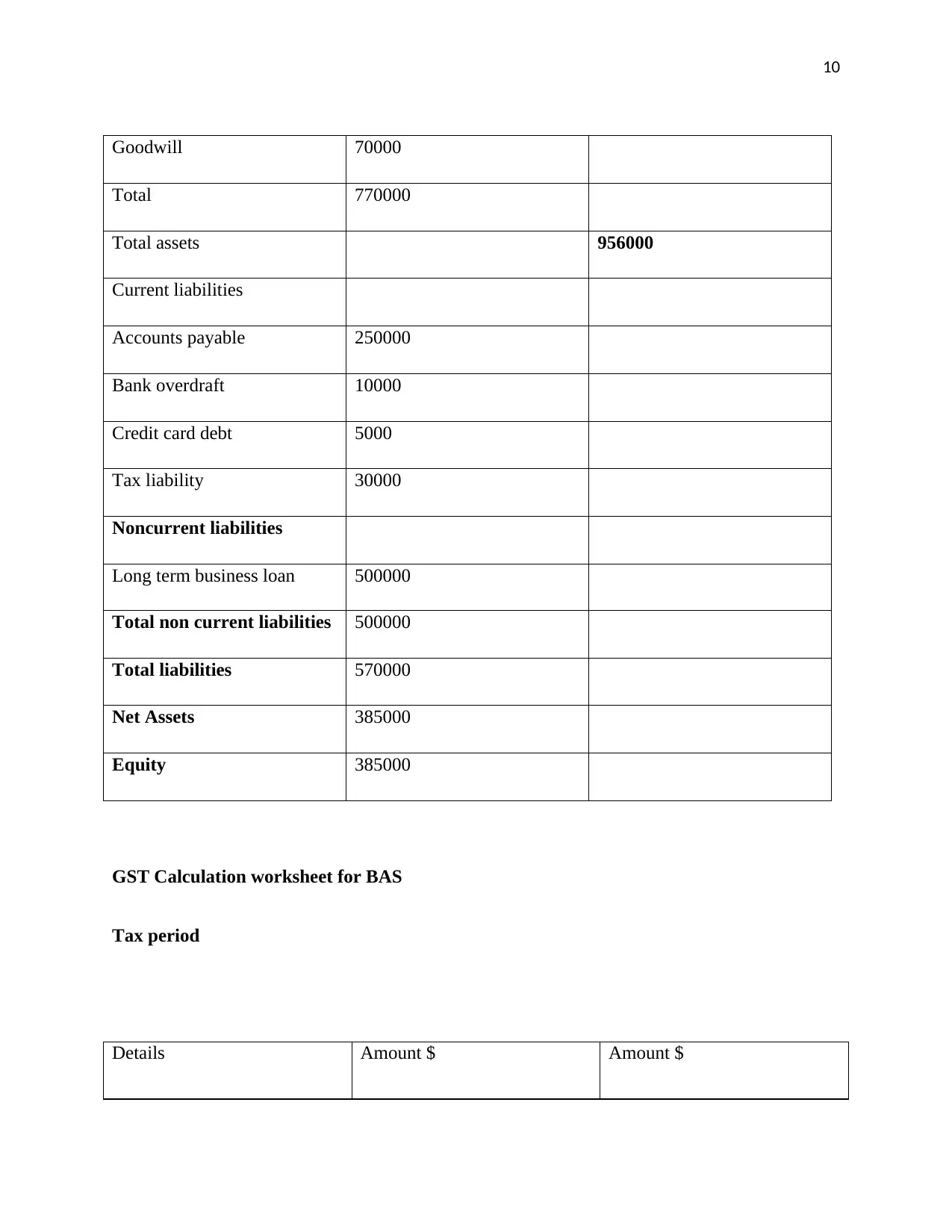

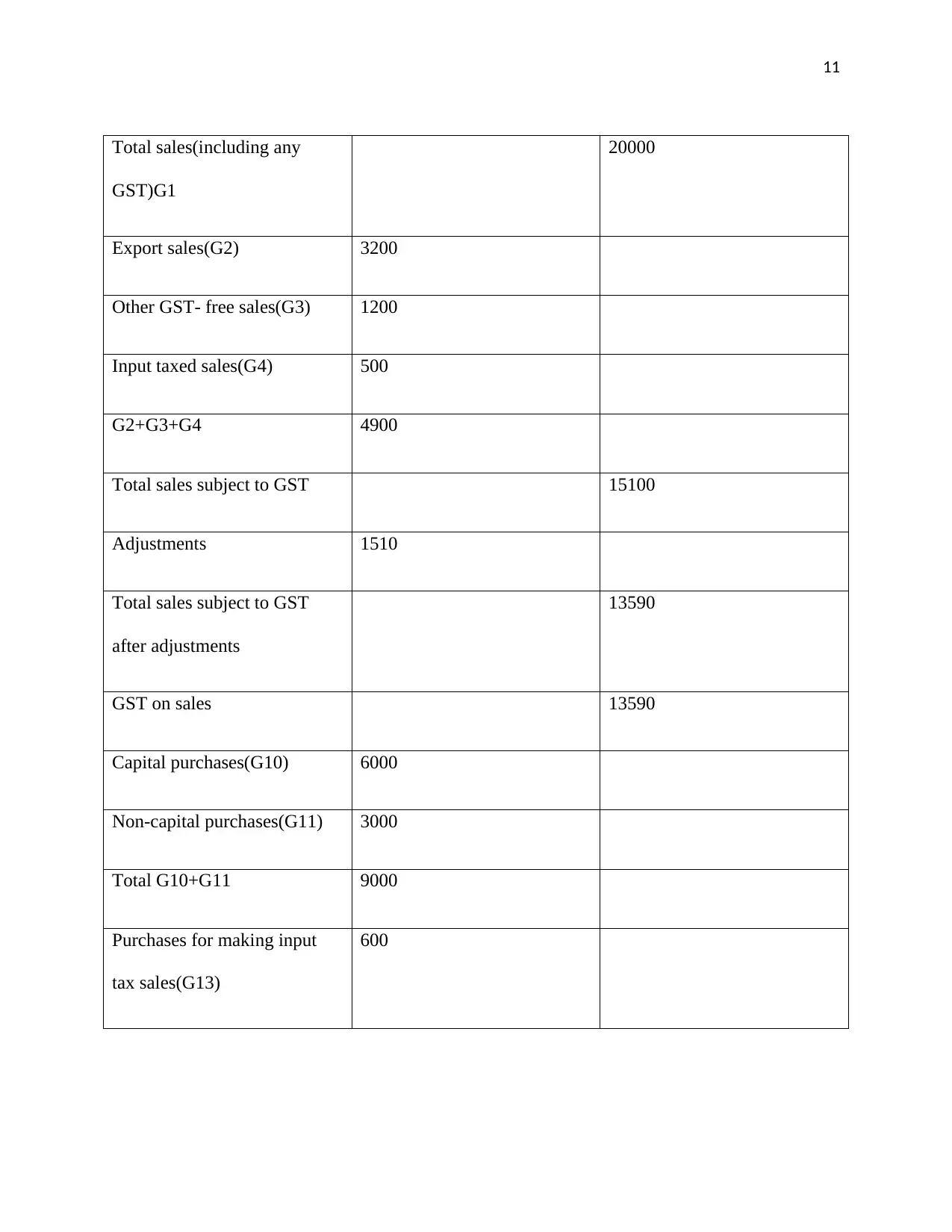

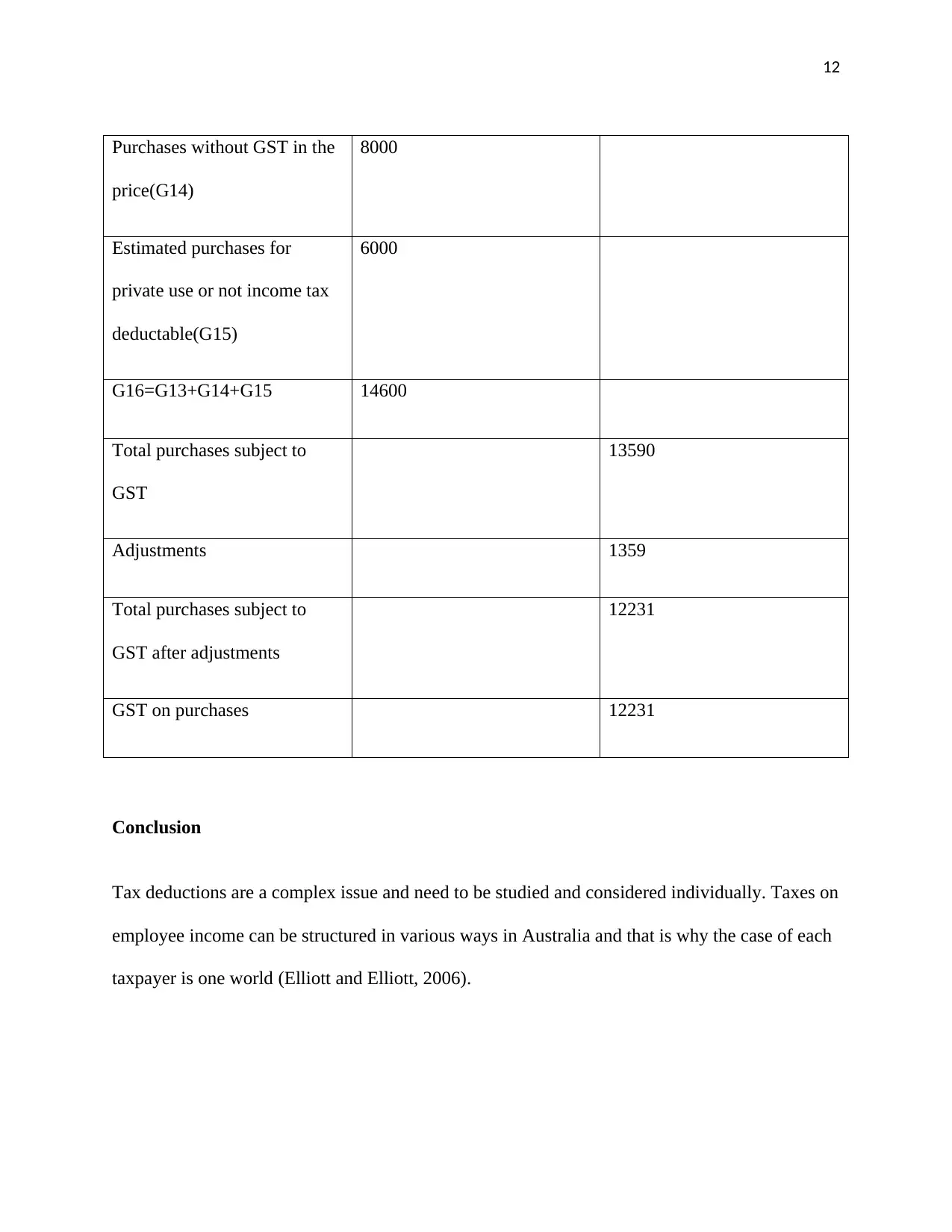

This report provides a comprehensive analysis of taxation and its relationship with accounting and financial performance. It begins by differentiating between accounting and taxation, emphasizing their interconnectedness, especially through corporate tax and income tax. The report covers asset and liability valuation methods, the significance of accounting in controlling fiscal aspects like VAT and tax deductions, and the integration of accounting and taxation in business software. It also discusses the challenges of aligning accounting and tax results, including permanent and temporary differences, and the importance of various tax receipts. Furthermore, the report addresses the taxation of income tax, highlighting issues related to tax base calculation, and explores significant issues in financial performance, such as differential rates and tax discounts. The report includes recommendations for tax financial reports, emphasizing transparency and fairness, and suggests modernizing tax language. It also delves into goodwill accounting, analyzing its recognition, measurement, and reporting. The report concludes with a discussion of financial business recommendations, focusing on the impact of taxes on cash flow and the importance of Goods and Services Tax (GST). It also covers the structure and formats of reports, including the roles of management, external auditors, and the Audit Committee, along with a sample balance sheet and GST calculation worksheet.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.