Management Accounting: Report and Analysis for Tech UK Ltd

VerifiedAdded on 2020/06/05

|16

|4917

|298

Report

AI Summary

This report provides a comprehensive overview of management accounting practices, focusing on Tech UK Ltd. It explores the meaning and needs of management accounting, emphasizing its role in financial transaction management and profitability enhancement. The report details various reporting methods, including inventory, performance, and job costing reports, and highlights the importance of collected financial information. It examines different costing methods like cost accounting, inventory management, and job costing systems, illustrating how these techniques calculate net profit. Furthermore, the report discusses the merits and demerits of different budgeting types and analyzes the use of planning tools. The application of the balance scorecard method for evaluating financial issues is also addressed, concluding with an evaluation of overall financial issues and providing insights into effective financial management strategies for organizations.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Table of Contents.............................................................................................................................2

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1: Meaning of management accounting and their needs......................................................1

P2: Various types of reporting methods.................................................................................4

(b): Importance of collected information..............................................................................5

M1: Benefits of using management accounting system.........................................................5

D1: Critical evaluation of accounting reporting method........................................................5

TASK 2............................................................................................................................................6

P3: Various types of costing method used to calculate total net profit..................................6

M2: Various types of accounting techniques.........................................................................9

D2: Analysis of data collected or reconciliation....................................................................9

TASK 3............................................................................................................................................9

P4: Merits and demerits of various types of budget...............................................................9

M3: Analysis of different planning tools..............................................................................11

D3: Critical evaluation of financial issues............................................................................11

TASK 4..........................................................................................................................................12

P5: Balance scorecard method..............................................................................................12

M4: Evaluating financial issues............................................................................................13

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

Table of Contents.............................................................................................................................2

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1: Meaning of management accounting and their needs......................................................1

P2: Various types of reporting methods.................................................................................4

(b): Importance of collected information..............................................................................5

M1: Benefits of using management accounting system.........................................................5

D1: Critical evaluation of accounting reporting method........................................................5

TASK 2............................................................................................................................................6

P3: Various types of costing method used to calculate total net profit..................................6

M2: Various types of accounting techniques.........................................................................9

D2: Analysis of data collected or reconciliation....................................................................9

TASK 3............................................................................................................................................9

P4: Merits and demerits of various types of budget...............................................................9

M3: Analysis of different planning tools..............................................................................11

D3: Critical evaluation of financial issues............................................................................11

TASK 4..........................................................................................................................................12

P5: Balance scorecard method..............................................................................................12

M4: Evaluating financial issues............................................................................................13

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION

Management accounting is an essential aspect for an organisation. By the help of this

company would able to manage and control their financial transaction in more effective manner.

The main aims of Tech UK are to attain maximum gain through using resources in more proper

ways. This project report is providing crucial information about various accounting and reporting

systems those are used for the purpose of recording transactions into their respective set format.

Moreover, it will be discussing various costing methods that are used for calculating net profit

for the company. With the use of merits and demerits of various budgets managers of Tech UK

would be able to control their costs and future expenses. Apart for this, all those financial issues

those are present in an organisation can be analyse by accountant and resolve them by using

balance scorecard method in an effective manner (Amoako, 2013).

TASK 1

P1: Meaning of management accounting and their needs

In every business enterprises, management tried to manage their day to day financial

transactions through using appropriate accounting system. These are helpful for an organisation

to increase the profitability for an organisation. The primary motive of every business is to make

use of vital accounting systems that are always assists Tech UK Ltd to regulate their operations

in more effective manner (Klemstine and Maher, 2014). Management accounting is a systematic

recording of all financial transactions that are incurred in an organisation during a specific period

of time. by the help of a well organise accounting systems which is the only key to perform their

operations at internal level. It is necessary to make evaluation of data through using appropriate

tools and accounting standards. It will assist them to increase overall aims and objectives at the

same point of time. The manager’s main aims are to enhance profitability as well as efficiency

by proper allocation of organisation resources. It has been analyse that financial accounting and

management accounting are having certain kind of similarities. Those are being discussed

underneath:

Management accounting Financial accounting

According to this accounting system which is

aid the internal and external department of

Tech UK to provide all necessary information

While in case of this, all the policies and rules

that are being made by organisation are used

for the purpose of preparing specific financial

1

Management accounting is an essential aspect for an organisation. By the help of this

company would able to manage and control their financial transaction in more effective manner.

The main aims of Tech UK are to attain maximum gain through using resources in more proper

ways. This project report is providing crucial information about various accounting and reporting

systems those are used for the purpose of recording transactions into their respective set format.

Moreover, it will be discussing various costing methods that are used for calculating net profit

for the company. With the use of merits and demerits of various budgets managers of Tech UK

would be able to control their costs and future expenses. Apart for this, all those financial issues

those are present in an organisation can be analyse by accountant and resolve them by using

balance scorecard method in an effective manner (Amoako, 2013).

TASK 1

P1: Meaning of management accounting and their needs

In every business enterprises, management tried to manage their day to day financial

transactions through using appropriate accounting system. These are helpful for an organisation

to increase the profitability for an organisation. The primary motive of every business is to make

use of vital accounting systems that are always assists Tech UK Ltd to regulate their operations

in more effective manner (Klemstine and Maher, 2014). Management accounting is a systematic

recording of all financial transactions that are incurred in an organisation during a specific period

of time. by the help of a well organise accounting systems which is the only key to perform their

operations at internal level. It is necessary to make evaluation of data through using appropriate

tools and accounting standards. It will assist them to increase overall aims and objectives at the

same point of time. The manager’s main aims are to enhance profitability as well as efficiency

by proper allocation of organisation resources. It has been analyse that financial accounting and

management accounting are having certain kind of similarities. Those are being discussed

underneath:

Management accounting Financial accounting

According to this accounting system which is

aid the internal and external department of

Tech UK to provide all necessary information

While in case of this, all the policies and rules

that are being made by organisation are used

for the purpose of preparing specific financial

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

to accountant so that overall aims and

objectives can be attain in reliable manner.

statements during the time.

All the data which is being provided by

owners are always assists them to future

planning and growth for the company.

The main objectives of using this accounting

are to provide essential information about

financial position of Tech UK to their

investors.

Every data and information are taken into

account those are related with financial as

well as non-financial at similar stage.

Only financial data is taken into consideration

to make accurate report for the company.

This accounting only provides practical

overview and information about the company

so that future decision making can be done.

Only theoretical aspects are analyse through

using reliable accounting rule and regulation

for the company.

Some examples are: Cash flow management,

sales tactics or budgeting are taken into

account.

Examples are: Balances sheet, profit and loss

statements and cash flow statements.

It often consists of companies total available

cash and recent sales earning and many more.

Physical money and account receivable

earned but not yet collected.

Various types of accounting system:

Cost accounting system: According to this accounting method which assists managers

to control and operate their internal operations in effective manner. All the costs that are used for

the production of product and services are taken into account at the same point of time. There are

certain types of costing which are needed to be taken into consideration such as:

Normal costing: It is said to be an appropriate costing methods which a company normal

incurred at the time of production of products with the same resources.

Actual costing: It is known as those costs that are actually incurred while production of

one unit by Tech UK Ltd in their daily course of business.

Standard costing: As per this costing this charged as per the set standard by the owner

of the company. This seems to be used for the purpose of making comparison of actual

results to that with actual one.

2

objectives can be attain in reliable manner.

statements during the time.

All the data which is being provided by

owners are always assists them to future

planning and growth for the company.

The main objectives of using this accounting

are to provide essential information about

financial position of Tech UK to their

investors.

Every data and information are taken into

account those are related with financial as

well as non-financial at similar stage.

Only financial data is taken into consideration

to make accurate report for the company.

This accounting only provides practical

overview and information about the company

so that future decision making can be done.

Only theoretical aspects are analyse through

using reliable accounting rule and regulation

for the company.

Some examples are: Cash flow management,

sales tactics or budgeting are taken into

account.

Examples are: Balances sheet, profit and loss

statements and cash flow statements.

It often consists of companies total available

cash and recent sales earning and many more.

Physical money and account receivable

earned but not yet collected.

Various types of accounting system:

Cost accounting system: According to this accounting method which assists managers

to control and operate their internal operations in effective manner. All the costs that are used for

the production of product and services are taken into account at the same point of time. There are

certain types of costing which are needed to be taken into consideration such as:

Normal costing: It is said to be an appropriate costing methods which a company normal

incurred at the time of production of products with the same resources.

Actual costing: It is known as those costs that are actually incurred while production of

one unit by Tech UK Ltd in their daily course of business.

Standard costing: As per this costing this charged as per the set standard by the owner

of the company. This seems to be used for the purpose of making comparison of actual

results to that with actual one.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Examples of cost accounting systems is, it is the costing that is more appropriate for a

specific activities of an organisation, a niche furniture producers or formulation of high cost of

air surveillances system. Some other are auto mechanic repair shop rebuilding of any machine.

Inventory management system: According to this accounting system that play an essential role

in analysing total position of inventory which is been kept by Tech UK in an accounting period

of time. This seems to be more reliable only to make comparison or tracking of stocks that are

being provided by suppliers for the process of production. There are certain types of inventory

systems such as:

LIFO: It said to be cost flow assumption which can be helpful for the company in respect

to analyse total moving of costs of products from stock to the cost of product sold. It

means that last inventory which is kept by the company will be discharged first.

FIFO: As per this method of stock valuation which is associated with cost flow basis that

initial costs are firstly recorded and realise during the period of time.

AVCO: It is known as effective method of inventory control which is being used to taken

into account the total cost of products still present for sales and divided through total sum

of products at the initial stage (Lim, 2011).

Examples are periodic inventory entries such as purchase transactions and sales is

recording using a cost of sales account.

Job costing system: It is known as one of the appropriate costing system which is being assign

during the production cost to a single products or job of products. Basically, the job cost is used

at the time when produce products are sufficiently different from one another. There are various

types of costing systems such as:

Contract costing: This is that kind of cost which is used to track overall production level

of a product produce by Tech UK. It is mostly associated with Construction Company.

Batch costing: It a kind of specific order costing which is similar to job costing system.

Every batch of products is being provided a specific number which is more identical and

different from one other (Van der Stede, 2015).

Process costing: It is mainly a method of assigned cost to particular products units

produce during a period of time. This seems to be product costing which is being measure

the product cost.

3

specific activities of an organisation, a niche furniture producers or formulation of high cost of

air surveillances system. Some other are auto mechanic repair shop rebuilding of any machine.

Inventory management system: According to this accounting system that play an essential role

in analysing total position of inventory which is been kept by Tech UK in an accounting period

of time. This seems to be more reliable only to make comparison or tracking of stocks that are

being provided by suppliers for the process of production. There are certain types of inventory

systems such as:

LIFO: It said to be cost flow assumption which can be helpful for the company in respect

to analyse total moving of costs of products from stock to the cost of product sold. It

means that last inventory which is kept by the company will be discharged first.

FIFO: As per this method of stock valuation which is associated with cost flow basis that

initial costs are firstly recorded and realise during the period of time.

AVCO: It is known as effective method of inventory control which is being used to taken

into account the total cost of products still present for sales and divided through total sum

of products at the initial stage (Lim, 2011).

Examples are periodic inventory entries such as purchase transactions and sales is

recording using a cost of sales account.

Job costing system: It is known as one of the appropriate costing system which is being assign

during the production cost to a single products or job of products. Basically, the job cost is used

at the time when produce products are sufficiently different from one another. There are various

types of costing systems such as:

Contract costing: This is that kind of cost which is used to track overall production level

of a product produce by Tech UK. It is mostly associated with Construction Company.

Batch costing: It a kind of specific order costing which is similar to job costing system.

Every batch of products is being provided a specific number which is more identical and

different from one other (Van der Stede, 2015).

Process costing: It is mainly a method of assigned cost to particular products units

produce during a period of time. This seems to be product costing which is being measure

the product cost.

3

Examples: Direct materiel, labour and overhead are taken into consideration while making any

particular costing system. It is must be helpful to track the cost of the labour use on an individual

job.

P2: Various types of reporting methods

Management accounting is all about managing funds in appropriate manner in order to

accomplish things in effective manner as well as main objective is to control possibilities of

losses. It helps in maximizing more or more profit by planning each or every aspect of an

association. Capital is seen as lifeblood for corporate companies because it helps in managing

various business activities in more appropriate manner. Along with this it aids an enterprise

while making proper company plans with the help of useful strategies and schemes. Basically, it

is not easy to manage expenses in appropriate manner. In order to allocate sufficient amount of

funds an organization needs to design an effective report for various other departments. Their

main objective is to manage things in better way by considering necessary facts or figures.

Hence, numerous of reports which is going to be falls under finance department is described as

follows:-

Inventory report: - Stock management is very much essential for delivering products to

right time at right place in a defined time period. Along with this, it’s all about management

of goods which is produced by company, closing and opening balance for supplying it as per

consumer need or demand. Mainly, it aids in controlling the level of mistakes and errors

which might occur at the time of producing products. However, inventory report is consisting

of various necessary details about transferring of goods across the international boundaries.

Performance report: - According to this component it is essential to analyse the

performance of employees in order to make necessary changes as per need or demand of staff

members. Basically, it helps managers while conducting training programmes for employees

as well as helps during judgement process so that company can easily improve the

performance of an organization in much better way.

Account receivable report: It is known as one of the crucial aspect which is used to

determine total list of unpaid customers invoices and credit memo. It is mainly related with

that particular report which deals with recovery of amount form debtors.

Job costing report: The job cost report is the initial place for much of information which

contained in other report. This report contain list of each job those are working on and cost

4

particular costing system. It is must be helpful to track the cost of the labour use on an individual

job.

P2: Various types of reporting methods

Management accounting is all about managing funds in appropriate manner in order to

accomplish things in effective manner as well as main objective is to control possibilities of

losses. It helps in maximizing more or more profit by planning each or every aspect of an

association. Capital is seen as lifeblood for corporate companies because it helps in managing

various business activities in more appropriate manner. Along with this it aids an enterprise

while making proper company plans with the help of useful strategies and schemes. Basically, it

is not easy to manage expenses in appropriate manner. In order to allocate sufficient amount of

funds an organization needs to design an effective report for various other departments. Their

main objective is to manage things in better way by considering necessary facts or figures.

Hence, numerous of reports which is going to be falls under finance department is described as

follows:-

Inventory report: - Stock management is very much essential for delivering products to

right time at right place in a defined time period. Along with this, it’s all about management

of goods which is produced by company, closing and opening balance for supplying it as per

consumer need or demand. Mainly, it aids in controlling the level of mistakes and errors

which might occur at the time of producing products. However, inventory report is consisting

of various necessary details about transferring of goods across the international boundaries.

Performance report: - According to this component it is essential to analyse the

performance of employees in order to make necessary changes as per need or demand of staff

members. Basically, it helps managers while conducting training programmes for employees

as well as helps during judgement process so that company can easily improve the

performance of an organization in much better way.

Account receivable report: It is known as one of the crucial aspect which is used to

determine total list of unpaid customers invoices and credit memo. It is mainly related with

that particular report which deals with recovery of amount form debtors.

Job costing report: The job cost report is the initial place for much of information which

contained in other report. This report contain list of each job those are working on and cost

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

incurred on a job in last period of time. It is kind of process which is assigning the cost those

are incur to a particular production of a product (Lavia López and Hiebl, 2014).

(b): Importance of collected information

In the mentioned case of Tech UK Limited, they need to make proper understanding of

all necessary information about financial position. This is major part for them to analyse every

financial report that are necessary to increase profitability and growth in near future time.

Financial reporting provides executive a clear image of the financial health of Tech Ltd. It cannot

provide every data on necessary to assist them to determine business performance at operational

level. There are certain accounting standard which are needed to be followed as per the GAAP

rules and regulations. It is the collection of similar standards which is associated with financial

transactions of an organisation. There are certain principles are needed to be followed before

preparing report. Some of them are discussed underneath:

It seems to be basic report of accounting principles and regulations.

The one of the appropriate regulations those are being issued by FASB as per the

requirement of the company.

M1: Benefits of using management accounting system

It has been seen that all those accounting methods a company is using in an organisation

are having some kind of benefits which will assist in increasing overall growth and profitability

for the company. In case Tech UK is using cost accounting system they are able to determine

specific relationship amount normal, actual and standard cost they are incurring in production of

products. While inventory management system which assist them to track current position of

inventory those are being kept by an organisation with them. Whereas job costing is use to

analyse total cost they are investing in manufacturing of a specific job cost (Bennett, Schaltegger

and Zvezdov, 2013).

D1: Critical evaluation of accounting reporting method

In accordance with generating more appropriate results for the company. Manager need to

make use of valuable reporting methods. These reports are being presenting in front of various

investors and stakeholder for the purpose of making future valuable decision regarding their

capital investment in their upcoming projects. Methods like performance report which is needed

5

are incur to a particular production of a product (Lavia López and Hiebl, 2014).

(b): Importance of collected information

In the mentioned case of Tech UK Limited, they need to make proper understanding of

all necessary information about financial position. This is major part for them to analyse every

financial report that are necessary to increase profitability and growth in near future time.

Financial reporting provides executive a clear image of the financial health of Tech Ltd. It cannot

provide every data on necessary to assist them to determine business performance at operational

level. There are certain accounting standard which are needed to be followed as per the GAAP

rules and regulations. It is the collection of similar standards which is associated with financial

transactions of an organisation. There are certain principles are needed to be followed before

preparing report. Some of them are discussed underneath:

It seems to be basic report of accounting principles and regulations.

The one of the appropriate regulations those are being issued by FASB as per the

requirement of the company.

M1: Benefits of using management accounting system

It has been seen that all those accounting methods a company is using in an organisation

are having some kind of benefits which will assist in increasing overall growth and profitability

for the company. In case Tech UK is using cost accounting system they are able to determine

specific relationship amount normal, actual and standard cost they are incurring in production of

products. While inventory management system which assist them to track current position of

inventory those are being kept by an organisation with them. Whereas job costing is use to

analyse total cost they are investing in manufacturing of a specific job cost (Bennett, Schaltegger

and Zvezdov, 2013).

D1: Critical evaluation of accounting reporting method

In accordance with generating more appropriate results for the company. Manager need to

make use of valuable reporting methods. These reports are being presenting in front of various

investors and stakeholder for the purpose of making future valuable decision regarding their

capital investment in their upcoming projects. Methods like performance report which is needed

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

to be implemented in specific manner so that actual position can be analyse. While of account

receivable report which is used to determine total time period for collecting necessary capital

from the debtors.

TASK 2

P3: Various types of costing method used to calculate total net profit

Cost is an essential aspect for every manufacturing company to analyse their total cost

needed for the production of one unit of products. The primary aims of using these costs is to

make specific analyse of total capital they are going to invest in the production or goods. Cost is

basically said to be value of amount which is being paid to get something (Abdel-Kader, 2011).

There are various types of costing methods that are used by accounting to evaluate total profit for

the company. Some of them are discussed underneath:

Absorption costing: It is known as one of the effective costing method which is used by

Tech UK at the time of manufacturing products during the time. These costs included both

variable and fixed costs because of which it is known as full costing method. It is not appropriate

for making future decision for the company.

Marginal costing: It is said to be most appropriate costing method which is helpful or

applicable for the company that is paid for additional production of units. It consists of only

variable cost and fixed costs are not taken into account for analysing net profit for the company.

This seems to be more reliable method which is being used for future decision making.

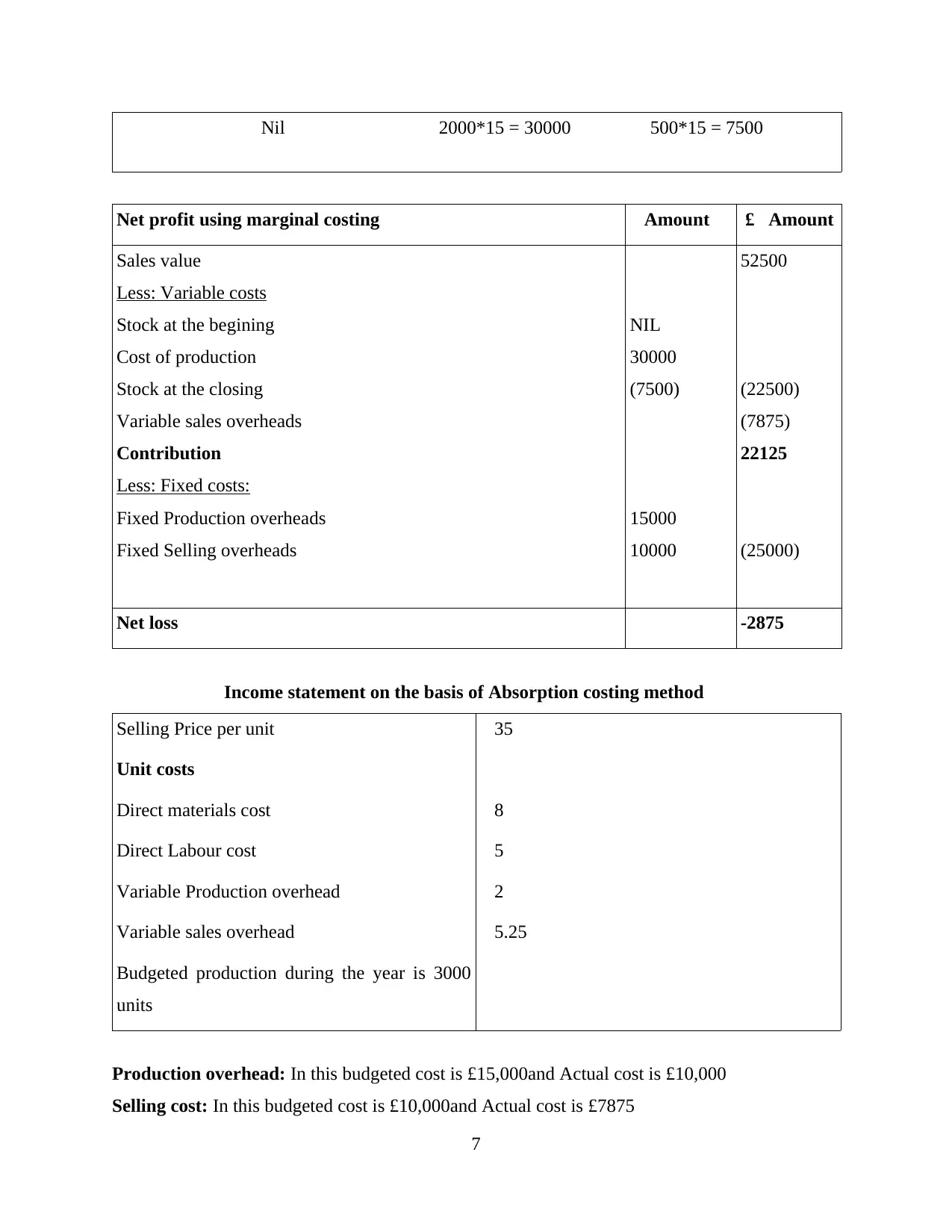

Income statement as on September by using Marginal costing method:

Working 1: Calculate variable production cost £

Direct material cost 8

Direct labour cost 5

Variable production O/h 2

Variable production cost 15

Working 2: Calculate value of inventory and production

Opening inventory Production Closing inventory

6

receivable report which is used to determine total time period for collecting necessary capital

from the debtors.

TASK 2

P3: Various types of costing method used to calculate total net profit

Cost is an essential aspect for every manufacturing company to analyse their total cost

needed for the production of one unit of products. The primary aims of using these costs is to

make specific analyse of total capital they are going to invest in the production or goods. Cost is

basically said to be value of amount which is being paid to get something (Abdel-Kader, 2011).

There are various types of costing methods that are used by accounting to evaluate total profit for

the company. Some of them are discussed underneath:

Absorption costing: It is known as one of the effective costing method which is used by

Tech UK at the time of manufacturing products during the time. These costs included both

variable and fixed costs because of which it is known as full costing method. It is not appropriate

for making future decision for the company.

Marginal costing: It is said to be most appropriate costing method which is helpful or

applicable for the company that is paid for additional production of units. It consists of only

variable cost and fixed costs are not taken into account for analysing net profit for the company.

This seems to be more reliable method which is being used for future decision making.

Income statement as on September by using Marginal costing method:

Working 1: Calculate variable production cost £

Direct material cost 8

Direct labour cost 5

Variable production O/h 2

Variable production cost 15

Working 2: Calculate value of inventory and production

Opening inventory Production Closing inventory

6

Nil 2000*15 = 30000 500*15 = 7500

Net profit using marginal costing £Amount £ Amount

Sales value

Less: Variable costs

Stock at the begining

Cost of production

Stock at the closing

Variable sales overheads

Contribution

Less: Fixed costs:

Fixed Production overheads

Fixed Selling overheads

NIL

30000

(7500)

15000

10000

52500

(22500)

(7875)

22125

(25000)

Net loss -2875

Income statement on the basis of Absorption costing method

Selling Price per unit £35

Unit costs

Direct materials cost £8

Direct Labour cost £5

Variable Production overhead £2

Variable sales overhead £5.25

Budgeted production during the year is 3000

units

Production overhead: In this budgeted cost is £15,000and Actual cost is £10,000

Selling cost: In this budgeted cost is £10,000and Actual cost is £7875

7

Net profit using marginal costing £Amount £ Amount

Sales value

Less: Variable costs

Stock at the begining

Cost of production

Stock at the closing

Variable sales overheads

Contribution

Less: Fixed costs:

Fixed Production overheads

Fixed Selling overheads

NIL

30000

(7500)

15000

10000

52500

(22500)

(7875)

22125

(25000)

Net loss -2875

Income statement on the basis of Absorption costing method

Selling Price per unit £35

Unit costs

Direct materials cost £8

Direct Labour cost £5

Variable Production overhead £2

Variable sales overhead £5.25

Budgeted production during the year is 3000

units

Production overhead: In this budgeted cost is £15,000and Actual cost is £10,000

Selling cost: In this budgeted cost is £10,000and Actual cost is £7875

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

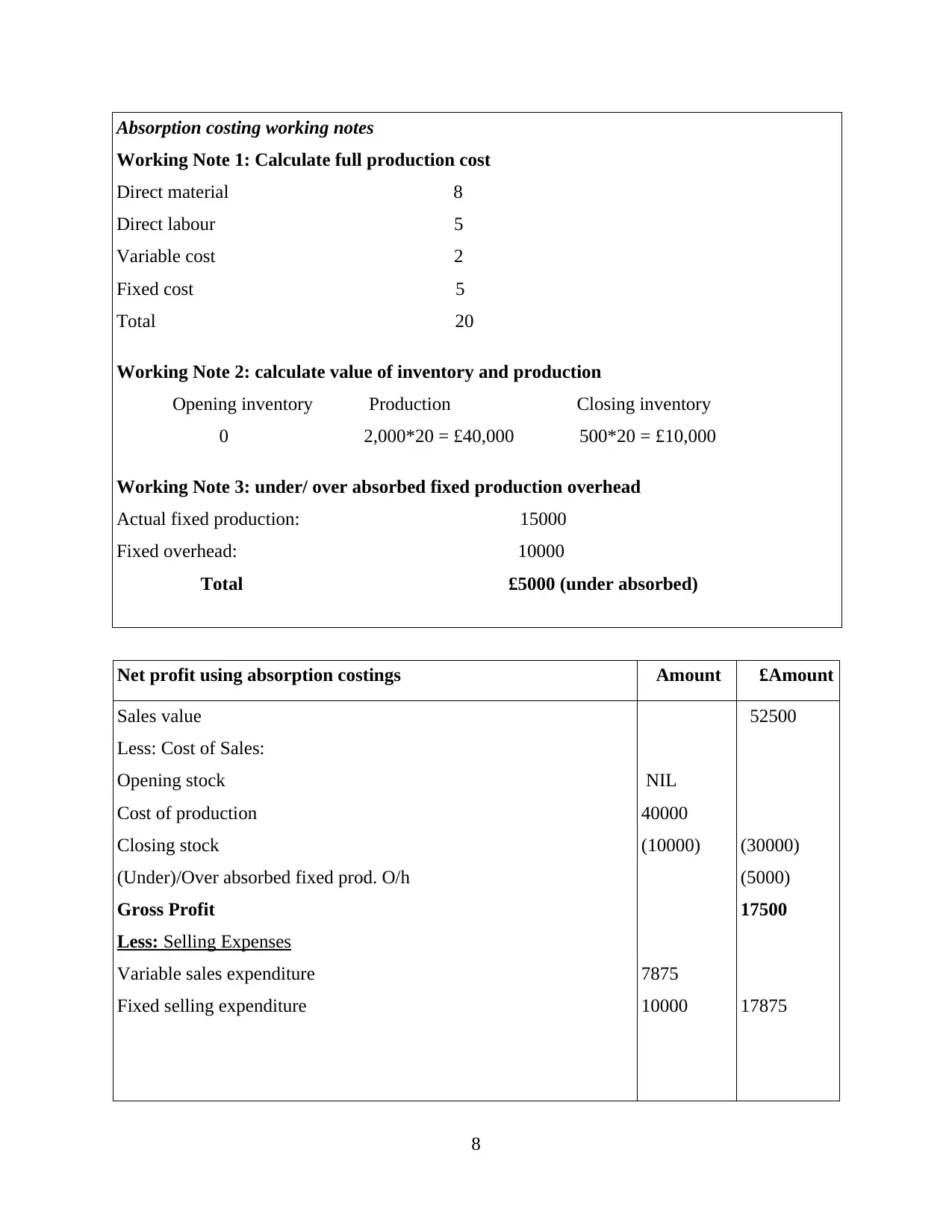

Absorption costing working notes

Working Note 1: Calculate full production cost

Direct material £8

Direct labour £5

Variable cost £2

Fixed cost £5

Total £20

Working Note 2: calculate value of inventory and production

Opening inventory Production Closing inventory

0 2,000*20 = £40,000 500*20 = £10,000

Working Note 3: under/ over absorbed fixed production overhead

Actual fixed production: £15000

Fixed overhead: £10000

Total £5000 (under absorbed)

Net profit using absorption costings £Amount £Amount

Sales value

Less: Cost of Sales:

Opening stock

Cost of production

Closing stock

(Under)/Over absorbed fixed prod. O/h

Gross Profit

Less: Selling Expenses

Variable sales expenditure

Fixed selling expenditure

NIL

40000

(10000)

7875

10000

52500

(30000)

(5000)

17500

17875

8

Working Note 1: Calculate full production cost

Direct material £8

Direct labour £5

Variable cost £2

Fixed cost £5

Total £20

Working Note 2: calculate value of inventory and production

Opening inventory Production Closing inventory

0 2,000*20 = £40,000 500*20 = £10,000

Working Note 3: under/ over absorbed fixed production overhead

Actual fixed production: £15000

Fixed overhead: £10000

Total £5000 (under absorbed)

Net profit using absorption costings £Amount £Amount

Sales value

Less: Cost of Sales:

Opening stock

Cost of production

Closing stock

(Under)/Over absorbed fixed prod. O/h

Gross Profit

Less: Selling Expenses

Variable sales expenditure

Fixed selling expenditure

NIL

40000

(10000)

7875

10000

52500

(30000)

(5000)

17500

17875

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

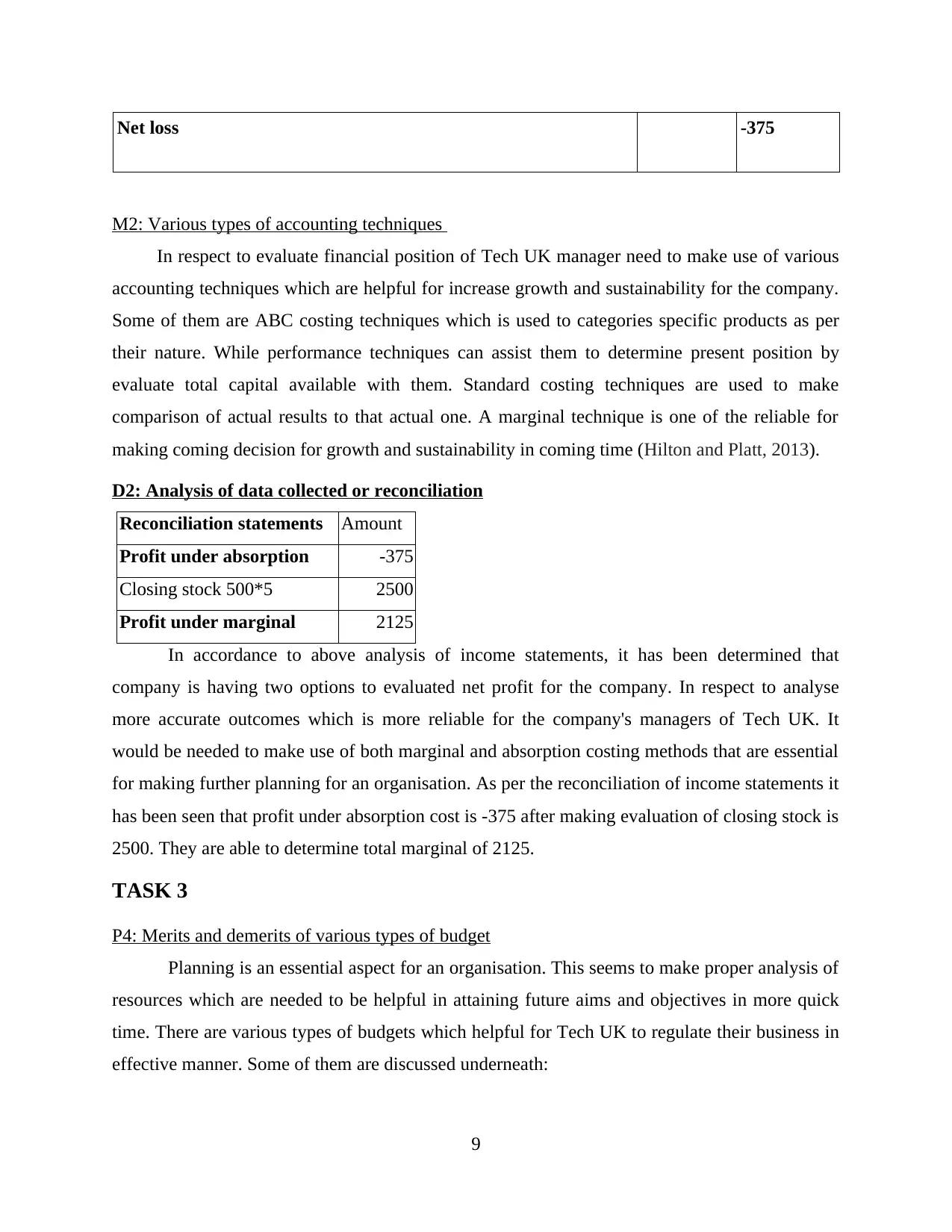

Net loss -375

M2: Various types of accounting techniques

In respect to evaluate financial position of Tech UK manager need to make use of various

accounting techniques which are helpful for increase growth and sustainability for the company.

Some of them are ABC costing techniques which is used to categories specific products as per

their nature. While performance techniques can assist them to determine present position by

evaluate total capital available with them. Standard costing techniques are used to make

comparison of actual results to that actual one. A marginal technique is one of the reliable for

making coming decision for growth and sustainability in coming time (Hilton and Platt, 2013).

D2: Analysis of data collected or reconciliation

Reconciliation statements Amount

Profit under absorption -375

Closing stock 500*5 2500

Profit under marginal 2125

In accordance to above analysis of income statements, it has been determined that

company is having two options to evaluated net profit for the company. In respect to analyse

more accurate outcomes which is more reliable for the company's managers of Tech UK. It

would be needed to make use of both marginal and absorption costing methods that are essential

for making further planning for an organisation. As per the reconciliation of income statements it

has been seen that profit under absorption cost is -375 after making evaluation of closing stock is

2500. They are able to determine total marginal of 2125.

TASK 3

P4: Merits and demerits of various types of budget

Planning is an essential aspect for an organisation. This seems to make proper analysis of

resources which are needed to be helpful in attaining future aims and objectives in more quick

time. There are various types of budgets which helpful for Tech UK to regulate their business in

effective manner. Some of them are discussed underneath:

9

M2: Various types of accounting techniques

In respect to evaluate financial position of Tech UK manager need to make use of various

accounting techniques which are helpful for increase growth and sustainability for the company.

Some of them are ABC costing techniques which is used to categories specific products as per

their nature. While performance techniques can assist them to determine present position by

evaluate total capital available with them. Standard costing techniques are used to make

comparison of actual results to that actual one. A marginal technique is one of the reliable for

making coming decision for growth and sustainability in coming time (Hilton and Platt, 2013).

D2: Analysis of data collected or reconciliation

Reconciliation statements Amount

Profit under absorption -375

Closing stock 500*5 2500

Profit under marginal 2125

In accordance to above analysis of income statements, it has been determined that

company is having two options to evaluated net profit for the company. In respect to analyse

more accurate outcomes which is more reliable for the company's managers of Tech UK. It

would be needed to make use of both marginal and absorption costing methods that are essential

for making further planning for an organisation. As per the reconciliation of income statements it

has been seen that profit under absorption cost is -375 after making evaluation of closing stock is

2500. They are able to determine total marginal of 2125.

TASK 3

P4: Merits and demerits of various types of budget

Planning is an essential aspect for an organisation. This seems to make proper analysis of

resources which are needed to be helpful in attaining future aims and objectives in more quick

time. There are various types of budgets which helpful for Tech UK to regulate their business in

effective manner. Some of them are discussed underneath:

9

Operation budget: As it is known as one of the effective forecasting income and

expenses over the course of a specific period. There are certain factors needed to be taken into

account in this budget such as labour cost, overhead and manufacturing cost.

Advantage: It is prepared on weekly, annually and monthly basis to determine total

estimated cost and expense incur during production (Parker, 2012).

Disadvantage: Only limited information is collected with this report which is not

effective for prepared final account.

Cash flow budget: It is a projecting about total cash comes in flows out of Tech UK

within a specific period of time. It used to consider factors like accounts payable and accounts

receivables.

Advantage: It is useful in determining whether company is able to managing their cash

in effective manner (Renz and Herman, 2016).

Disadvantage: Once the recovery period is over, manager would be able to take into

account this budget.

Rolling budget: It is said to be continually updated to include a new budget time frame as

the most recent budget get completed. It consists of incremental extension of present budget

model.

Advantage: It is considering as one of the best planning and controlling that will be based

on more accurate budget.

Disadvantage: These are costlier and time consuming other than incremental budgets.

Process of budget:

Identification of budget ideas which is primary aims of managers to prepare budget for

the company.

Collecting necessary information from different department those are operating at

internal level.

Obtaining capital forecasting from various sources.

Collect budget request from upper department by taking appropriate suggestion.

Update budget model in more proper manner in the manner of master budgets for the

company.

Review of budget is a end process which is completed by taking feedbacks from various

employees and departments.

10

expenses over the course of a specific period. There are certain factors needed to be taken into

account in this budget such as labour cost, overhead and manufacturing cost.

Advantage: It is prepared on weekly, annually and monthly basis to determine total

estimated cost and expense incur during production (Parker, 2012).

Disadvantage: Only limited information is collected with this report which is not

effective for prepared final account.

Cash flow budget: It is a projecting about total cash comes in flows out of Tech UK

within a specific period of time. It used to consider factors like accounts payable and accounts

receivables.

Advantage: It is useful in determining whether company is able to managing their cash

in effective manner (Renz and Herman, 2016).

Disadvantage: Once the recovery period is over, manager would be able to take into

account this budget.

Rolling budget: It is said to be continually updated to include a new budget time frame as

the most recent budget get completed. It consists of incremental extension of present budget

model.

Advantage: It is considering as one of the best planning and controlling that will be based

on more accurate budget.

Disadvantage: These are costlier and time consuming other than incremental budgets.

Process of budget:

Identification of budget ideas which is primary aims of managers to prepare budget for

the company.

Collecting necessary information from different department those are operating at

internal level.

Obtaining capital forecasting from various sources.

Collect budget request from upper department by taking appropriate suggestion.

Update budget model in more proper manner in the manner of master budgets for the

company.

Review of budget is a end process which is completed by taking feedbacks from various

employees and departments.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.