Management Accounting Report: Finance Module, Semester 1

VerifiedAdded on 2020/11/06

|17

|3594

|41

Report

AI Summary

This report provides a comprehensive overview of management accounting, exploring its role in organizational decision-making and strategic planning. It delves into the core concepts of management accounting systems, explaining essential requirements and different reporting methods. The report examines the key differences between management and financial accounting, highlighting areas of overlap. Furthermore, it applies various management accounting techniques, including cost analysis, marginal costing, and absorption costing, to prepare income statements. The report also covers break-even analysis and net profit calculations, emphasizing their significance in financial planning. Through practical examples and case studies, the report illustrates the application of these techniques in real-world scenarios, offering valuable insights for students and professionals seeking to enhance their understanding of management accounting principles and practices.

Manag

ement

Accou

nting

ement

Accou

nting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Introduction......................................................................................................................................1

LO1-Demonstrate an understanding of management accounting systems......................................1

P1 Explain management accounting and give the essential requirements of different types of

management accounting systems.................................................................................................1

Question 1- Management Accounting and The role of Management Accounting in an

Organization............................................................................................................................1

Question 2- The scope of the role of management accounting and the part it plays within

each function of the business...................................................................................................2

Question 3- Key differences between management accountant and financial accountant and

areas where two disciplines may overlap................................................................................5

P2 Explain different methods used for management accounting reporting.................................7

Question 4- Different types of cost report in Management Accounting Reports....................7

LO2 Apply a range of management accounting techniques............................................................8

P3 Calculate costs using appropriate techniques of cost analysis to prepare an income

statement using marginal and absorption costing........................................................................8

Question 5- Income statement using Marginal costing and Absorption Costing....................8

Question 6- Break Even Analysis and its importance...........................................................11

Question 7- Net Profit Calculation and Its importance.........................................................13

Conclusion.....................................................................................................................................14

References......................................................................................................................................15

Introduction......................................................................................................................................1

LO1-Demonstrate an understanding of management accounting systems......................................1

P1 Explain management accounting and give the essential requirements of different types of

management accounting systems.................................................................................................1

Question 1- Management Accounting and The role of Management Accounting in an

Organization............................................................................................................................1

Question 2- The scope of the role of management accounting and the part it plays within

each function of the business...................................................................................................2

Question 3- Key differences between management accountant and financial accountant and

areas where two disciplines may overlap................................................................................5

P2 Explain different methods used for management accounting reporting.................................7

Question 4- Different types of cost report in Management Accounting Reports....................7

LO2 Apply a range of management accounting techniques............................................................8

P3 Calculate costs using appropriate techniques of cost analysis to prepare an income

statement using marginal and absorption costing........................................................................8

Question 5- Income statement using Marginal costing and Absorption Costing....................8

Question 6- Break Even Analysis and its importance...........................................................11

Question 7- Net Profit Calculation and Its importance.........................................................13

Conclusion.....................................................................................................................................14

References......................................................................................................................................15

Introduction

Management Accounting is nothing but a means of achieving organizational goals by making

sustainable decision with the help of relevant information. Management accounting helps

managers to take correct decision in their daily activities as well as helps them to develop

strategic planning and operational planning for their business by analyzing various types of

financial data, reports etc. prepared by the financial managers. In this report the scope and

application of management accounting in business functions have been discussed with some

practical examples that will add value in our learning regarding management accounting and its

process.

LO1-Demonstrate an understanding of management

accounting systems

P1 Explain management accounting and give the essential requirements of

different types of management accounting systems

Question 1- Management Accounting and The role of Management

Accounting in an Organization

Management Accounting: Management accounting is also called managerial accounting which

is the process of identifying, measuring, analyzing, interpreting, and communicating information

to managers for the pursuit of an organization's goals (Horngren, C. 2016). Basically the

process helps managers to make day-to-day and short-term decisions by preparing management

reports and accounts that provide accurate and timely financial and statistical information. These

reports show the amount of available cash, amount of orders in hand, sales revenue generated,

outstanding debts, state of accounts payable and accounts receivable, raw material and inventory

etc.

1 | P a g e

Management Accounting is nothing but a means of achieving organizational goals by making

sustainable decision with the help of relevant information. Management accounting helps

managers to take correct decision in their daily activities as well as helps them to develop

strategic planning and operational planning for their business by analyzing various types of

financial data, reports etc. prepared by the financial managers. In this report the scope and

application of management accounting in business functions have been discussed with some

practical examples that will add value in our learning regarding management accounting and its

process.

LO1-Demonstrate an understanding of management

accounting systems

P1 Explain management accounting and give the essential requirements of

different types of management accounting systems

Question 1- Management Accounting and The role of Management

Accounting in an Organization

Management Accounting: Management accounting is also called managerial accounting which

is the process of identifying, measuring, analyzing, interpreting, and communicating information

to managers for the pursuit of an organization's goals (Horngren, C. 2016). Basically the

process helps managers to make day-to-day and short-term decisions by preparing management

reports and accounts that provide accurate and timely financial and statistical information. These

reports show the amount of available cash, amount of orders in hand, sales revenue generated,

outstanding debts, state of accounts payable and accounts receivable, raw material and inventory

etc.

1 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The role of Management Accounting in an Organization:

Management accounting helps those persons in an organization who are liable for any

type of financial decisions by providing necessary information required for any type of

decision making. It basically serves the internal users of the organization.

Management accounting helps to predict the future by providing answers of various

questions like should the invest in the market or should the company diversify their

investments by analyzing the financial reports.

Management accounting also helps an organization by predicting the cash flows and the

impact of the cash flows in the organizational activities. As this process involves budgets

and trend charts which help managers to analyze from where the revenues will come

from and will the company is going to have more or less revenue in the future.

This process helps to analyze the variance between the expectation and the reality in

terms of costs, revenues, inventory management etc.

It also helps in making the decision of whether the company should buy materials from

other company or make it. As the cost functions and resource allocation is related to the

management accounting system, an insight of the analyzing of these elements will help in

making the decision also.

Question 2- The scope of the role of management accounting and the

part it plays within each function of the business

The main objective of management accounting is to provide necessary information to the

managers of any firm for planning and controlling. The scope of management accounting is very

wide and it covers almost all of the sides of any business’ operations.

i. Financial Accounting: Financial accounting refers to analyse financial data and

preparing financial statements of an organisation. It contains a lot of data that is used by

the management team for any kind of decision making. Without a proper financial

accounting system in an organization management accounting can’t be fully effective

because management accounting contains only some tools and techniques but it analyses

2 | P a g e

Management accounting helps those persons in an organization who are liable for any

type of financial decisions by providing necessary information required for any type of

decision making. It basically serves the internal users of the organization.

Management accounting helps to predict the future by providing answers of various

questions like should the invest in the market or should the company diversify their

investments by analyzing the financial reports.

Management accounting also helps an organization by predicting the cash flows and the

impact of the cash flows in the organizational activities. As this process involves budgets

and trend charts which help managers to analyze from where the revenues will come

from and will the company is going to have more or less revenue in the future.

This process helps to analyze the variance between the expectation and the reality in

terms of costs, revenues, inventory management etc.

It also helps in making the decision of whether the company should buy materials from

other company or make it. As the cost functions and resource allocation is related to the

management accounting system, an insight of the analyzing of these elements will help in

making the decision also.

Question 2- The scope of the role of management accounting and the

part it plays within each function of the business

The main objective of management accounting is to provide necessary information to the

managers of any firm for planning and controlling. The scope of management accounting is very

wide and it covers almost all of the sides of any business’ operations.

i. Financial Accounting: Financial accounting refers to analyse financial data and

preparing financial statements of an organisation. It contains a lot of data that is used by

the management team for any kind of decision making. Without a proper financial

accounting system in an organization management accounting can’t be fully effective

because management accounting contains only some tools and techniques but it analyses

2 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

and interprets the data obtained from financial accounting system. So an effective

financial accounting system is very much needed for an effective management

accounting.

ii. Cost Accounting: Cost accounting is the backbone of management accounting. It

provides tools like budgetary control, standard costing, inventory control, marginal

costing, and differential costing etc. All of these tools are very important for determining

the cost of providing services or manufacturing any product. These help in an efficient

planning, decision making and controlling of a management team.

iii. Budgeting & Forecasting: The budgetary control and forecasting tools are used in the

management accounting system also. The budgetary control system explains the budget

prepared for the operational activities, measures the actual performance and find the

variance between these two for taking proper corrective action that is required.

iv. Cost Control Procedures: inventory control, cost control, time control, budgetary

control, standard costing etc. are discussed here. An analyze of these tools provide an

insight to the decision makers for making or providing any products or service efficiently.

So this is an important part of the management accounting system.

v. Statistical Methods: In order to make the financial information more comprehensive and

impressive various statistical tools like graph, charts, diagrams and index numbers etc.

are used. Tools like regression analysis, time series, sampling techniques etc. are highly

useful in the decision making process of any organization.

vi. Management Reporting: Keeping top level managers well informed about the condition

of business operations is an important responsibility of the management accounting. In

order to make the best use of firm’s resources clearly informative and timely reports are

very important. The management accountant send interim reports may be monthly,

quarterly, half yearly that contains profits or order in hand etc. which provide a constant

review of the firm’s current situation.

vii. Taxation: As per the laws it includes the income tax calculation, filing returns etc. for

calculating this taxes financial information is required which is an essential part of the

management accounting system.

viii. Interpreting Data: The interpretation of data to management is very sensitive for any

company. The management accountant performs the task of interpreting all the financial

3 | P a g e

financial accounting system is very much needed for an effective management

accounting.

ii. Cost Accounting: Cost accounting is the backbone of management accounting. It

provides tools like budgetary control, standard costing, inventory control, marginal

costing, and differential costing etc. All of these tools are very important for determining

the cost of providing services or manufacturing any product. These help in an efficient

planning, decision making and controlling of a management team.

iii. Budgeting & Forecasting: The budgetary control and forecasting tools are used in the

management accounting system also. The budgetary control system explains the budget

prepared for the operational activities, measures the actual performance and find the

variance between these two for taking proper corrective action that is required.

iv. Cost Control Procedures: inventory control, cost control, time control, budgetary

control, standard costing etc. are discussed here. An analyze of these tools provide an

insight to the decision makers for making or providing any products or service efficiently.

So this is an important part of the management accounting system.

v. Statistical Methods: In order to make the financial information more comprehensive and

impressive various statistical tools like graph, charts, diagrams and index numbers etc.

are used. Tools like regression analysis, time series, sampling techniques etc. are highly

useful in the decision making process of any organization.

vi. Management Reporting: Keeping top level managers well informed about the condition

of business operations is an important responsibility of the management accounting. In

order to make the best use of firm’s resources clearly informative and timely reports are

very important. The management accountant send interim reports may be monthly,

quarterly, half yearly that contains profits or order in hand etc. which provide a constant

review of the firm’s current situation.

vii. Taxation: As per the laws it includes the income tax calculation, filing returns etc. for

calculating this taxes financial information is required which is an essential part of the

management accounting system.

viii. Interpreting Data: The interpretation of data to management is very sensitive for any

company. The management accountant performs the task of interpreting all the financial

3 | P a g e

data in a easily understandable language. He interprets data, compares the financial

reports with the financial reports of previous times or with the reports of similar types of

other companies. Wrong interpretation can mislead the managers in taking decision. So

this plays a vital role in the business operations.

ix. Internal Auditing: In order to have an effective internal auditing by the business itself it

requires financial reports and other relevant information. Under the management

accounting system all the relevant data are maintained and recorded properly to have the

full benefit of an internal auditing procedure.

It should be noted that the management accounting is a mean through which an organization can

achieve its goals. The objective of management accounting is to help organization to achieve

strategic objectives. It also helps managers to have competitive advantages in achieving the

organizational goals by maintaining strategic resources like time, quality and cost. Through the

collection and dissemination of information and collaborating with the information gathered

from management accounting an effective planning, organizing, controlling can be done. This

mix or

Figure 1: The strategic elements

combination helps the company to fulfill the expectation of all its stakeholders and can achieve

the organizational goal. (Hirsch, Nitzl, and Schauß 2015). In the functions of business

management accounting plays an important role also. An effective management accounting

makes the way very smooth for any company to achieve their organizational goal properly.

4 | P a g e

Cost Time

Quality

reports with the financial reports of previous times or with the reports of similar types of

other companies. Wrong interpretation can mislead the managers in taking decision. So

this plays a vital role in the business operations.

ix. Internal Auditing: In order to have an effective internal auditing by the business itself it

requires financial reports and other relevant information. Under the management

accounting system all the relevant data are maintained and recorded properly to have the

full benefit of an internal auditing procedure.

It should be noted that the management accounting is a mean through which an organization can

achieve its goals. The objective of management accounting is to help organization to achieve

strategic objectives. It also helps managers to have competitive advantages in achieving the

organizational goals by maintaining strategic resources like time, quality and cost. Through the

collection and dissemination of information and collaborating with the information gathered

from management accounting an effective planning, organizing, controlling can be done. This

mix or

Figure 1: The strategic elements

combination helps the company to fulfill the expectation of all its stakeholders and can achieve

the organizational goal. (Hirsch, Nitzl, and Schauß 2015). In the functions of business

management accounting plays an important role also. An effective management accounting

makes the way very smooth for any company to achieve their organizational goal properly.

4 | P a g e

Cost Time

Quality

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Planning: Budgeting is one of the major task for any manager because with the help of

this budgeting a manager can formalize and express a business plan. Whenever this

planning gets done it works as a standard for comparing actual work in the future. As a

result, manager can use this as predetermined criteria in the controlling process.

Management accounting helps in making this business plan for any business. In the

following figure we can see an example of production budget which is related with other

costs. This can be done through the management accounting process. Management finds

that they should plan about the sales, production, capital expenditure etc. in this manner

they need to put Strategic planning and operational planning.

Control: Controlling means the process of finding deviation between actual performance

and predetermined criteria. There are many accounting techniques that helps management

with controlling information such as standard cost, responsibility accounting, budgeting

etc. with the help of this types of techniques management can take necessary steps if

required in the controlling process.

Deciding: Financial reports, cost accounting, inventory accounting, cost control

procedure etc helps to develop an insight in order to making any kind of decisions. The

analysis of these reports helps manager to decide where they should invest, how much

they should invest, should they buy or make the product or services etc. Management

Accounting in this way helps the business function to work smoothly. (Lal and

Srivastava 2013).

Question 3- Key differences between management accountant and

financial accountant and areas where two disciplines may overlap

Points of

Difference

Management Accountant Financial Accountant

Definition A person who provides financial data and

advice to a company for use in the

organization and development of its

A person who draws up the profit and

loss account, balance sheet and cash

flow, statement for the company as a

5 | P a g e

this budgeting a manager can formalize and express a business plan. Whenever this

planning gets done it works as a standard for comparing actual work in the future. As a

result, manager can use this as predetermined criteria in the controlling process.

Management accounting helps in making this business plan for any business. In the

following figure we can see an example of production budget which is related with other

costs. This can be done through the management accounting process. Management finds

that they should plan about the sales, production, capital expenditure etc. in this manner

they need to put Strategic planning and operational planning.

Control: Controlling means the process of finding deviation between actual performance

and predetermined criteria. There are many accounting techniques that helps management

with controlling information such as standard cost, responsibility accounting, budgeting

etc. with the help of this types of techniques management can take necessary steps if

required in the controlling process.

Deciding: Financial reports, cost accounting, inventory accounting, cost control

procedure etc helps to develop an insight in order to making any kind of decisions. The

analysis of these reports helps manager to decide where they should invest, how much

they should invest, should they buy or make the product or services etc. Management

Accounting in this way helps the business function to work smoothly. (Lal and

Srivastava 2013).

Question 3- Key differences between management accountant and

financial accountant and areas where two disciplines may overlap

Points of

Difference

Management Accountant Financial Accountant

Definition A person who provides financial data and

advice to a company for use in the

organization and development of its

A person who draws up the profit and

loss account, balance sheet and cash

flow, statement for the company as a

5 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

business. whole.

Role They help in making managerial

decisions

Like planning, organizing, controlling,

deciding by providing sufficient

information.

They Support in financial decision-

making by collecting, analysing,

investigating, and reporting financial

data.

Scope Scope is very wide and vast. Scope is pervasive .

Dependence Management accountant is dependent on

financial accountant in order to make

correct decision.

Financial Accountant is not dependent

on management accountant for

performing his activity.

Serving Parties Mainly serves the internal users. Serves both the internal and external

users.

Type of

measurement

Deals with both qualitative and

Quantitative data.

Deals with only Quantitative data.

Decision

Making

Historical data and predictive data help

management Accountant to take decision.

Only historical data helps financial

Accountant to take decision

Verification and

Rules

They don’t follow any specific rules and

their work is not verifiable immediately.

They follow the rules of GAAP or

IFRS and their work is verifiable.

We can see there is lots of difference between the two principles of management accounting and

financial accounting but in terms of cost accounting this two overlap. Cost accounting create an

overlap between financial accounting and managerial accounting by providing cost based

information and some quantitative information to managers for making their decision and for the

financial managers it provides product costing information for financial statements.

6 | P a g e

Role They help in making managerial

decisions

Like planning, organizing, controlling,

deciding by providing sufficient

information.

They Support in financial decision-

making by collecting, analysing,

investigating, and reporting financial

data.

Scope Scope is very wide and vast. Scope is pervasive .

Dependence Management accountant is dependent on

financial accountant in order to make

correct decision.

Financial Accountant is not dependent

on management accountant for

performing his activity.

Serving Parties Mainly serves the internal users. Serves both the internal and external

users.

Type of

measurement

Deals with both qualitative and

Quantitative data.

Deals with only Quantitative data.

Decision

Making

Historical data and predictive data help

management Accountant to take decision.

Only historical data helps financial

Accountant to take decision

Verification and

Rules

They don’t follow any specific rules and

their work is not verifiable immediately.

They follow the rules of GAAP or

IFRS and their work is verifiable.

We can see there is lots of difference between the two principles of management accounting and

financial accounting but in terms of cost accounting this two overlap. Cost accounting create an

overlap between financial accounting and managerial accounting by providing cost based

information and some quantitative information to managers for making their decision and for the

financial managers it provides product costing information for financial statements.

6 | P a g e

P2 Explain different methods used for management accounting reporting

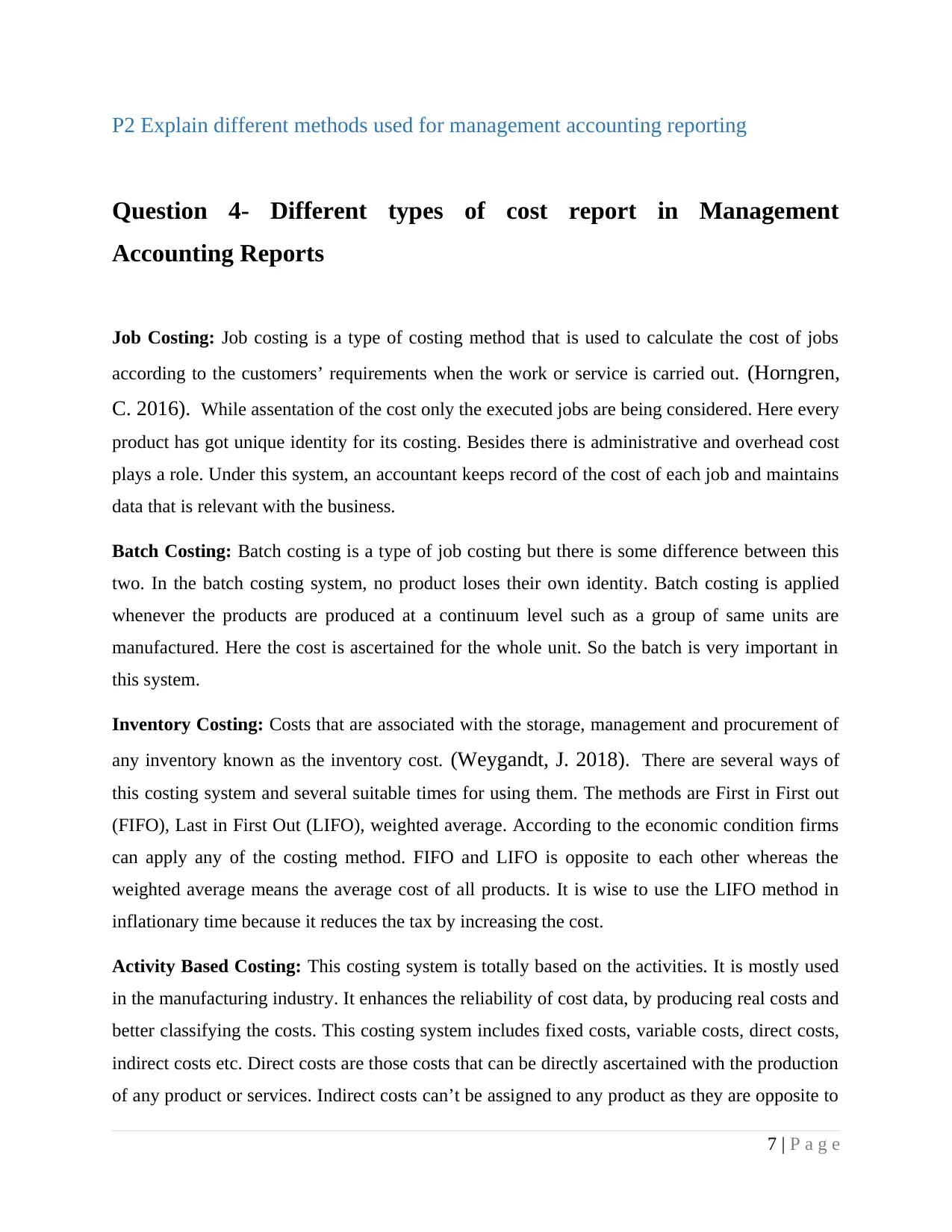

Question 4- Different types of cost report in Management

Accounting Reports

Job Costing: Job costing is a type of costing method that is used to calculate the cost of jobs

according to the customers’ requirements when the work or service is carried out. (Horngren,

C. 2016). While assentation of the cost only the executed jobs are being considered. Here every

product has got unique identity for its costing. Besides there is administrative and overhead cost

plays a role. Under this system, an accountant keeps record of the cost of each job and maintains

data that is relevant with the business.

Batch Costing: Batch costing is a type of job costing but there is some difference between this

two. In the batch costing system, no product loses their own identity. Batch costing is applied

whenever the products are produced at a continuum level such as a group of same units are

manufactured. Here the cost is ascertained for the whole unit. So the batch is very important in

this system.

Inventory Costing: Costs that are associated with the storage, management and procurement of

any inventory known as the inventory cost. (Weygandt, J. 2018). There are several ways of

this costing system and several suitable times for using them. The methods are First in First out

(FIFO), Last in First Out (LIFO), weighted average. According to the economic condition firms

can apply any of the costing method. FIFO and LIFO is opposite to each other whereas the

weighted average means the average cost of all products. It is wise to use the LIFO method in

inflationary time because it reduces the tax by increasing the cost.

Activity Based Costing: This costing system is totally based on the activities. It is mostly used

in the manufacturing industry. It enhances the reliability of cost data, by producing real costs and

better classifying the costs. This costing system includes fixed costs, variable costs, direct costs,

indirect costs etc. Direct costs are those costs that can be directly ascertained with the production

of any product or services. Indirect costs can’t be assigned to any product as they are opposite to

7 | P a g e

Question 4- Different types of cost report in Management

Accounting Reports

Job Costing: Job costing is a type of costing method that is used to calculate the cost of jobs

according to the customers’ requirements when the work or service is carried out. (Horngren,

C. 2016). While assentation of the cost only the executed jobs are being considered. Here every

product has got unique identity for its costing. Besides there is administrative and overhead cost

plays a role. Under this system, an accountant keeps record of the cost of each job and maintains

data that is relevant with the business.

Batch Costing: Batch costing is a type of job costing but there is some difference between this

two. In the batch costing system, no product loses their own identity. Batch costing is applied

whenever the products are produced at a continuum level such as a group of same units are

manufactured. Here the cost is ascertained for the whole unit. So the batch is very important in

this system.

Inventory Costing: Costs that are associated with the storage, management and procurement of

any inventory known as the inventory cost. (Weygandt, J. 2018). There are several ways of

this costing system and several suitable times for using them. The methods are First in First out

(FIFO), Last in First Out (LIFO), weighted average. According to the economic condition firms

can apply any of the costing method. FIFO and LIFO is opposite to each other whereas the

weighted average means the average cost of all products. It is wise to use the LIFO method in

inflationary time because it reduces the tax by increasing the cost.

Activity Based Costing: This costing system is totally based on the activities. It is mostly used

in the manufacturing industry. It enhances the reliability of cost data, by producing real costs and

better classifying the costs. This costing system includes fixed costs, variable costs, direct costs,

indirect costs etc. Direct costs are those costs that can be directly ascertained with the production

of any product or services. Indirect costs can’t be assigned to any product as they are opposite to

7 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

direct costs. Fixed costs are the cost that doesn’t vary whether the production is going on or not.

Semi variable cost is a combination of both the fixed costs and variable costs also known as the

semi fixed cost.

LO2 Apply a range of management accounting techniques

P3 Calculate costs using appropriate techniques of cost analysis to prepare an

income statement using marginal and absorption costing

Question 5- Income statement using Marginal costing and

Absorption Costing

Marginal Costing

Period 1 Period 2 Period 3 Period 4 Period 5

Produced 230 270 260 240 250

Sold 200 210 260 280 300

Held in

stock at nil

End of

period

30 90 90 50 0

8 | P a g e

Selling price per unit

Variable cost per unit

Fixed costs for each period

£

20

9

500

Semi variable cost is a combination of both the fixed costs and variable costs also known as the

semi fixed cost.

LO2 Apply a range of management accounting techniques

P3 Calculate costs using appropriate techniques of cost analysis to prepare an

income statement using marginal and absorption costing

Question 5- Income statement using Marginal costing and

Absorption Costing

Marginal Costing

Period 1 Period 2 Period 3 Period 4 Period 5

Produced 230 270 260 240 250

Sold 200 210 260 280 300

Held in

stock at nil

End of

period

30 90 90 50 0

8 | P a g e

Selling price per unit

Variable cost per unit

Fixed costs for each period

£

20

9

500

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Period

1

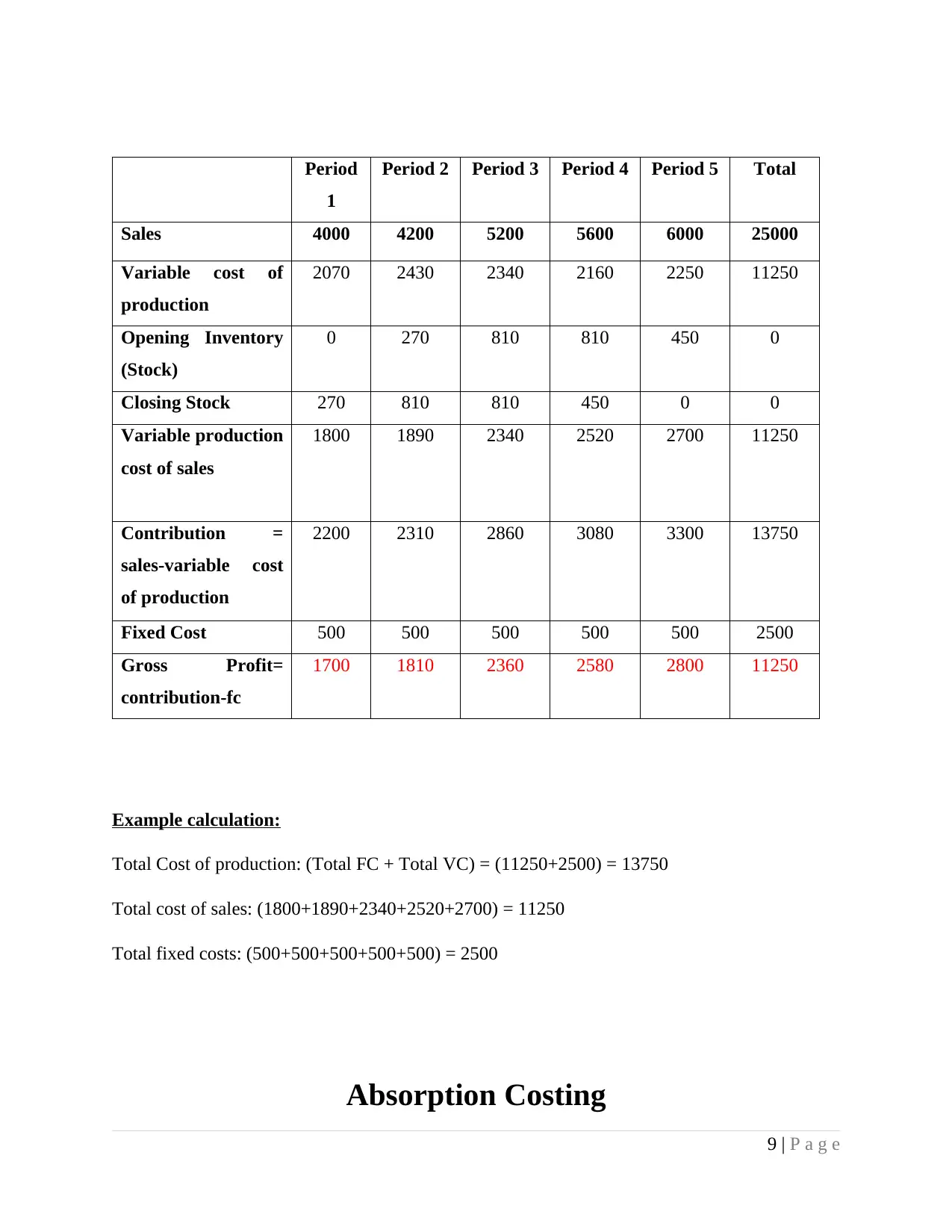

Period 2 Period 3 Period 4 Period 5 Total

Sales 4000 4200 5200 5600 6000 25000

Variable cost of

production

2070 2430 2340 2160 2250 11250

Opening Inventory

(Stock)

0 270 810 810 450 0

Closing Stock 270 810 810 450 0 0

Variable production

cost of sales

1800 1890 2340 2520 2700 11250

Contribution =

sales-variable cost

of production

2200 2310 2860 3080 3300 13750

Fixed Cost 500 500 500 500 500 2500

Gross Profit=

contribution-fc

1700 1810 2360 2580 2800 11250

Example calculation:

Total Cost of production: (Total FC + Total VC) = (11250+2500) = 13750

Total cost of sales: (1800+1890+2340+2520+2700) = 11250

Total fixed costs: (500+500+500+500+500) = 2500

Absorption Costing

9 | P a g e

1

Period 2 Period 3 Period 4 Period 5 Total

Sales 4000 4200 5200 5600 6000 25000

Variable cost of

production

2070 2430 2340 2160 2250 11250

Opening Inventory

(Stock)

0 270 810 810 450 0

Closing Stock 270 810 810 450 0 0

Variable production

cost of sales

1800 1890 2340 2520 2700 11250

Contribution =

sales-variable cost

of production

2200 2310 2860 3080 3300 13750

Fixed Cost 500 500 500 500 500 2500

Gross Profit=

contribution-fc

1700 1810 2360 2580 2800 11250

Example calculation:

Total Cost of production: (Total FC + Total VC) = (11250+2500) = 13750

Total cost of sales: (1800+1890+2340+2520+2700) = 11250

Total fixed costs: (500+500+500+500+500) = 2500

Absorption Costing

9 | P a g e

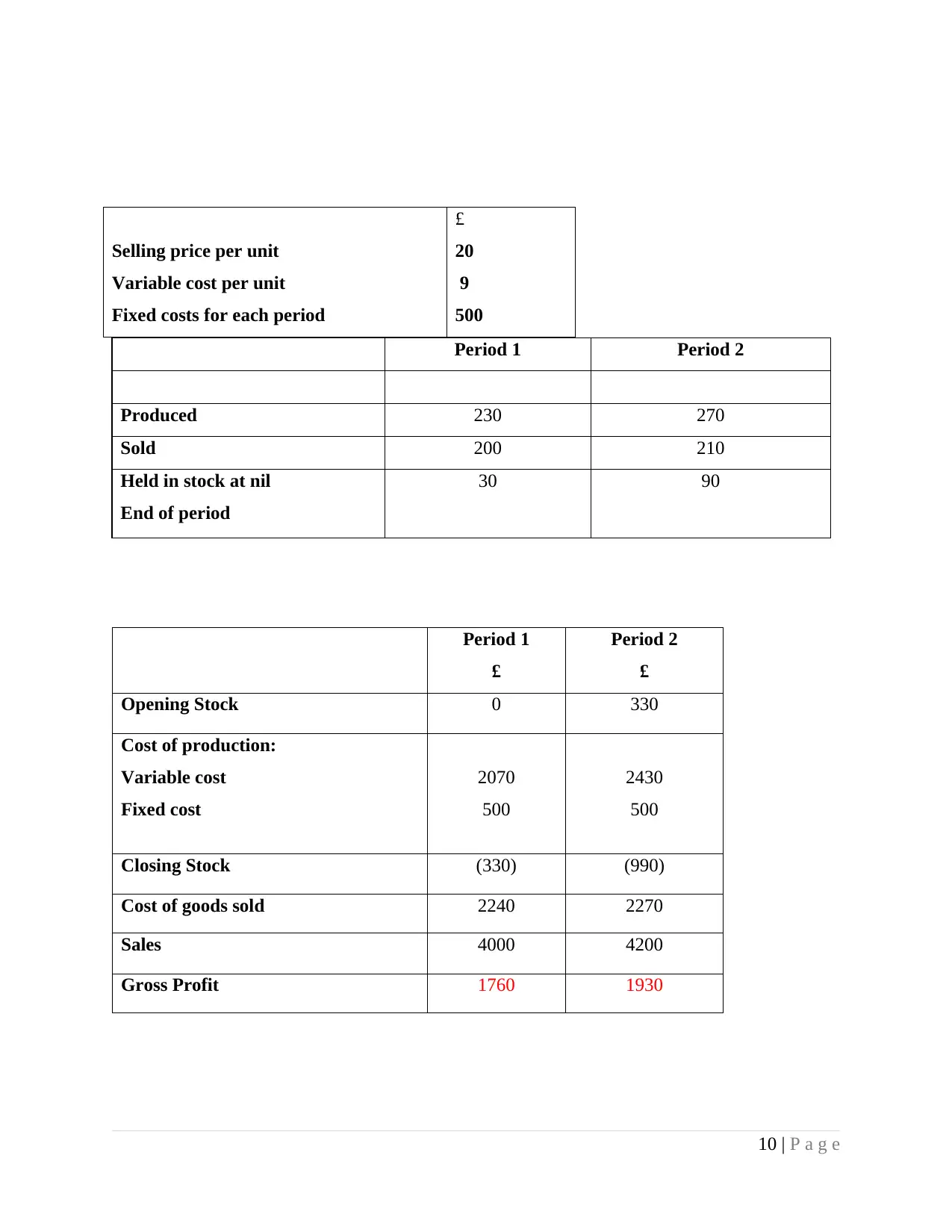

Period 1 Period 2

Produced 230 270

Sold 200 210

Held in stock at nil

End of period

30 90

Period 1

£

Period 2

£

Opening Stock 0 330

Cost of production:

Variable cost

Fixed cost

2070

500

2430

500

Closing Stock (330) (990)

Cost of goods sold 2240 2270

Sales 4000 4200

Gross Profit 1760 1930

10 | P a g e

Selling price per unit

Variable cost per unit

Fixed costs for each period

£

20

9

500

Produced 230 270

Sold 200 210

Held in stock at nil

End of period

30 90

Period 1

£

Period 2

£

Opening Stock 0 330

Cost of production:

Variable cost

Fixed cost

2070

500

2430

500

Closing Stock (330) (990)

Cost of goods sold 2240 2270

Sales 4000 4200

Gross Profit 1760 1930

10 | P a g e

Selling price per unit

Variable cost per unit

Fixed costs for each period

£

20

9

500

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.