Detailed Management Accounting Report: Systems, Costing, Budgeting

VerifiedAdded on 2021/02/19

|21

|6035

|116

Report

AI Summary

This report delves into the principles and practices of management accounting, examining its role in internal decision-making within an organization. It differentiates between management and financial accounting, highlighting the significance of management accounting systems in cost control, performance evaluation, and risk mitigation. The report explores various management accounting systems, including cost accounting, inventory management, job costing, and price optimization, detailing their functionalities and benefits. It then discusses different types of management accounting reports, such as cost accounting reports, budget reports, performance reports, and accounts receivable reports, emphasizing their importance in providing insights for strategic decision-making. Furthermore, the report explains marginal costing and absorption costing techniques, using them to prepare an income statement. Finally, it addresses the advantages and disadvantages of planning tools used in budgetary control and discusses the application of management accounting in resolving financial problems within a business organization.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Content

INTRODUCTION...........................................................................................................................1

ACTIVITY 1....................................................................................................................................1

1 Management Accounting & its requirements..........................................................................1

2 Different types of Management Accounting Reporting...........................................................3

3. Calculation of Cost through different Cost Accounting Techniques......................................5

Annex A......................................................................................................................................6

Annex B......................................................................................................................................6

ACTIVITY 2....................................................................................................................................8

4. Advantage & Disadvantages of planning tools used in Budgetary Control............................8

5. Adaption of Management Accounting System for resolving financial problems.................10

Annex C....................................................................................................................................14

REFERENCES..............................................................................................................................16

INTRODUCTION...........................................................................................................................1

ACTIVITY 1....................................................................................................................................1

1 Management Accounting & its requirements..........................................................................1

2 Different types of Management Accounting Reporting...........................................................3

3. Calculation of Cost through different Cost Accounting Techniques......................................5

Annex A......................................................................................................................................6

Annex B......................................................................................................................................6

ACTIVITY 2....................................................................................................................................8

4. Advantage & Disadvantages of planning tools used in Budgetary Control............................8

5. Adaption of Management Accounting System for resolving financial problems.................10

Annex C....................................................................................................................................14

REFERENCES..............................................................................................................................16

INTRODUCTION

Management Accounting is a method of accounting used by internal managers of

business organisation. Managers of company make various decisions related to cost minimisation

and preparation of future financial plan in accordance with organisations objectives. Different

reports are prepared by managers with the help of management accounting such as Costing

Report and Budgeting Report which in turn helps managers in decision making & formulating

strategies.

This report explain Management Accounting. Further, the below report elaborate various

types of systems used by managers in management accounting. Furthermore, importance of

management accounting systems are discussed in this report. Moreover, this report include

different types of report prepared by managers with the help of management accounting. Further,

this report prepare Income Statement with the help of different management accounting

techniques such as Marginal & Absorption Costing. Furthermore, the below stated report

includes advantages & disadvantages of planning tools used in Budgetary Control. At last, this

report explains application of management accounting in a business organisation with the

purpose of resolving financial problems.

ACTIVITY 1

1 Management Accounting & its requirements

Management Accounting

Financial Accounting & Management Accounting are two accounting methods. Financial

Accounting is used for disclosing financial information of a company to its external users

whereas Management Accounting essential for internal managers of a business firm.

Management Accounting helps managers in managing companies production process by

reducing cost. Further, This cost is also known as Cost Accounting as with this accounting

technique internal managers of company monitors and control cost incurred during

manufacturing process which in turn benefits business organisations in achieving high

profitability and Customer Base(Hague, 2018).

Further, with the help of this accounting method managers of company are able to

compare estimated cost of production with the actual cost and if there is any difference in both

actual & estimated cost than managers make further plans to eliminate unnecessary cost.

1

Management Accounting is a method of accounting used by internal managers of

business organisation. Managers of company make various decisions related to cost minimisation

and preparation of future financial plan in accordance with organisations objectives. Different

reports are prepared by managers with the help of management accounting such as Costing

Report and Budgeting Report which in turn helps managers in decision making & formulating

strategies.

This report explain Management Accounting. Further, the below report elaborate various

types of systems used by managers in management accounting. Furthermore, importance of

management accounting systems are discussed in this report. Moreover, this report include

different types of report prepared by managers with the help of management accounting. Further,

this report prepare Income Statement with the help of different management accounting

techniques such as Marginal & Absorption Costing. Furthermore, the below stated report

includes advantages & disadvantages of planning tools used in Budgetary Control. At last, this

report explains application of management accounting in a business organisation with the

purpose of resolving financial problems.

ACTIVITY 1

1 Management Accounting & its requirements

Management Accounting

Financial Accounting & Management Accounting are two accounting methods. Financial

Accounting is used for disclosing financial information of a company to its external users

whereas Management Accounting essential for internal managers of a business firm.

Management Accounting helps managers in managing companies production process by

reducing cost. Further, This cost is also known as Cost Accounting as with this accounting

technique internal managers of company monitors and control cost incurred during

manufacturing process which in turn benefits business organisations in achieving high

profitability and Customer Base(Hague, 2018).

Further, with the help of this accounting method managers of company are able to

compare estimated cost of production with the actual cost and if there is any difference in both

actual & estimated cost than managers make further plans to eliminate unnecessary cost.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Management Accounting Systems

Management Accounting systems are important for managers as with this systems

managers are able evaluated and difference between actual & estimated performance. Managers

of a company are also able to minimise risk associate in production & other business activities

which in turn enhances profitability of company. Thus, this system is having a significant

importance for managers and a business organisation. Different Types of Management

Accounting Systems are discussed below-

Cost Accounting System- This is the most required management accounting system as

with this managers of a company develop a structure through which they can analyse or make an

estimation of cost incurred during manufacturing process. After determining cost with the help of

this system managers are able to decide profit margin. Thus, this system is also important in

analysing profitability of a firm. Further, with this management accounting system managers can

determine value of inventory available for manufacturing process this benefits them in managing

& maintaining cost(Kaplan and Atkinson, 2015).

This system is also advantageous in determining different types of cost & products of

manufacturing such as Direct Cost and Standard Cost. Direct Cost includes Cost of Direct Raw

Material, Direct Overhead and Labour used in production process whereas, Standard cost is

estimated cost required to manufacture a product. Further, this system is also essential for

identifying profitability of different products offered by a business organisation and with that

managers can make decisions related to elimination of a product which is giving loss. This

further helps company in increasing its profits, performance, customer and market share.

Inventory Management System- Inventory is a most essential element without which a

company is note able to start its production process thus, it is necessary for a business

organisation to check availability of stock and determine value of its available stock. This can be

done by managers with the help of Inventory Management System as this system track inventory

level, sales orders and helps in developing different types bills related to material and other

production elements. Thus, this system is beneficial in managing inventory in a manner which

minimises cost.

Further, Managers are able to make decision related to selection of an inventory valuation

methods such as LIFO & FIFO. This cost evaluate cost included in each method and provides an

2

Management Accounting systems are important for managers as with this systems

managers are able evaluated and difference between actual & estimated performance. Managers

of a company are also able to minimise risk associate in production & other business activities

which in turn enhances profitability of company. Thus, this system is having a significant

importance for managers and a business organisation. Different Types of Management

Accounting Systems are discussed below-

Cost Accounting System- This is the most required management accounting system as

with this managers of a company develop a structure through which they can analyse or make an

estimation of cost incurred during manufacturing process. After determining cost with the help of

this system managers are able to decide profit margin. Thus, this system is also important in

analysing profitability of a firm. Further, with this management accounting system managers can

determine value of inventory available for manufacturing process this benefits them in managing

& maintaining cost(Kaplan and Atkinson, 2015).

This system is also advantageous in determining different types of cost & products of

manufacturing such as Direct Cost and Standard Cost. Direct Cost includes Cost of Direct Raw

Material, Direct Overhead and Labour used in production process whereas, Standard cost is

estimated cost required to manufacture a product. Further, this system is also essential for

identifying profitability of different products offered by a business organisation and with that

managers can make decisions related to elimination of a product which is giving loss. This

further helps company in increasing its profits, performance, customer and market share.

Inventory Management System- Inventory is a most essential element without which a

company is note able to start its production process thus, it is necessary for a business

organisation to check availability of stock and determine value of its available stock. This can be

done by managers with the help of Inventory Management System as this system track inventory

level, sales orders and helps in developing different types bills related to material and other

production elements. Thus, this system is beneficial in managing inventory in a manner which

minimises cost.

Further, Managers are able to make decision related to selection of an inventory valuation

methods such as LIFO & FIFO. This cost evaluate cost included in each method and provides an

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

appropriate method to company. This system is an essential requirement of management

accounting as it provides detailed information related to Reorder Point, Lead Demand, Order

Quantity, Stock Cover and Accuracy. This in turn benefits business in optimising cost & level f

inventory. Inventory Management System is applicable in all types of organisations such as

Manufacturing Firm, Retail Companies and other industries(Labro, 2019).

Job Costing System- A Costing System which helps managers in determining cost

involved in a particular job performed by a company is known as Job Costing. This system is

important as with this production managers of a business organisation can assess cost of each job

and make decisions of investment in a job which is more profitable. This system is implemented

in organisations which are introducing more than one product line and job. Further, it is also

beneficial for business ventures which are engaging in a manufacturing activity of unique

products. Event Management Companies and Interior designers most commonly use this system

as they their products & services differs with time.

This system is an essential requirement for companies which are paying high cost in

manufacturing of their products & services(Maas, Schaltegger and Crutzen, 2016).

Price Optimising System- Benefit of this management accounting system is it helps

managers in optimising prices of products & services offered by company according to the

demand & preference of customer which in turn benefits business firms in maximisation of its

customer base. This system enable managers in analysing response of customers at different

price and on that basis managers set a price which is accepted by most of the customers.

This system is applicable on organisations which are distributing their products &

services in more than one market. As individuals of different geographical area are having

different income level and different purchasing power. Further, managers determine price of

products after considering profit margin which in turn increases revenue of business(Advantages

of Benchmarking. 2016).

2 Different types of Management Accounting Reporting

Management Accounting Reports

Management Accounting Reports are prepared by managers which gives detailed

information related to cost, inventory and other elements used in process of product

development. This reports are disclosed to internal managers of company so that they can make

3

accounting as it provides detailed information related to Reorder Point, Lead Demand, Order

Quantity, Stock Cover and Accuracy. This in turn benefits business in optimising cost & level f

inventory. Inventory Management System is applicable in all types of organisations such as

Manufacturing Firm, Retail Companies and other industries(Labro, 2019).

Job Costing System- A Costing System which helps managers in determining cost

involved in a particular job performed by a company is known as Job Costing. This system is

important as with this production managers of a business organisation can assess cost of each job

and make decisions of investment in a job which is more profitable. This system is implemented

in organisations which are introducing more than one product line and job. Further, it is also

beneficial for business ventures which are engaging in a manufacturing activity of unique

products. Event Management Companies and Interior designers most commonly use this system

as they their products & services differs with time.

This system is an essential requirement for companies which are paying high cost in

manufacturing of their products & services(Maas, Schaltegger and Crutzen, 2016).

Price Optimising System- Benefit of this management accounting system is it helps

managers in optimising prices of products & services offered by company according to the

demand & preference of customer which in turn benefits business firms in maximisation of its

customer base. This system enable managers in analysing response of customers at different

price and on that basis managers set a price which is accepted by most of the customers.

This system is applicable on organisations which are distributing their products &

services in more than one market. As individuals of different geographical area are having

different income level and different purchasing power. Further, managers determine price of

products after considering profit margin which in turn increases revenue of business(Advantages

of Benchmarking. 2016).

2 Different types of Management Accounting Reporting

Management Accounting Reports

Management Accounting Reports are prepared by managers which gives detailed

information related to cost, inventory and other elements used in process of product

development. This reports are disclosed to internal managers of company so that they can make

3

decisions & develop strategies related investment, expansion, Increment in employees salary,

Introduction & minimisation of product line and elimination of cost. This reports are prepared

according to the business requirements. IT can be prepared monthly, Quarterly and

Annually(McVay, Kennedy and Fullerton, 2016).

Further, no specific format is used by companies for preparing management accounting

reports. Various types of management accounting reports are explained below-

Cost Managerial Accounting Reports- This report provide information related to cost of

each element used in manufacturing process like Raw Material, Labour and overheads. Further,

this report show amount of selling & manufacturing cost so that managers can identify amount of

profit generated by each unit. This reports are useful for managers as with this they can analyse

expenses done by company and it also provide information related to use of organisational

resources which in turn helps organisations in effective utilisation of their resources. Manager

also makes decisions related to waste management and determining hourly cost of labours on the

basis of this report(Medudula, Sagar and Gandhi, 2016).

Cost Accounting Reports are beneficial for companies a with this managers are able to

estimate future profits & expenses and which further plays a significant role in achieving

business objectives with formulating strategy of minimising cost.

Budget Reports- Budget Report shows future financial plan of a company according to

its future objectives which in turn benefits managers in evaluating performance of a business

firm. Budget is prepared by managers on the basis of historical data and this reports includes

information related to expenses, revenue, income & cost. This report is essential as whole

business operations of a company is decided on the basis of future budget.

Further, this report is an essential requirement for managers as managers decide amount

of incentives for employees and negotiate with suppliers of raw materials on the basis of this

report. A company can also achieve future goals & objectives if it operates its business in

accordance with Budget Reports.

Performance Report- Performance Report gives details of overall business activities

performed by an organisation so that managers of company can review performance of company

and its employees. Further, managers develop plans & policies if performance of company is not

4

Introduction & minimisation of product line and elimination of cost. This reports are prepared

according to the business requirements. IT can be prepared monthly, Quarterly and

Annually(McVay, Kennedy and Fullerton, 2016).

Further, no specific format is used by companies for preparing management accounting

reports. Various types of management accounting reports are explained below-

Cost Managerial Accounting Reports- This report provide information related to cost of

each element used in manufacturing process like Raw Material, Labour and overheads. Further,

this report show amount of selling & manufacturing cost so that managers can identify amount of

profit generated by each unit. This reports are useful for managers as with this they can analyse

expenses done by company and it also provide information related to use of organisational

resources which in turn helps organisations in effective utilisation of their resources. Manager

also makes decisions related to waste management and determining hourly cost of labours on the

basis of this report(Medudula, Sagar and Gandhi, 2016).

Cost Accounting Reports are beneficial for companies a with this managers are able to

estimate future profits & expenses and which further plays a significant role in achieving

business objectives with formulating strategy of minimising cost.

Budget Reports- Budget Report shows future financial plan of a company according to

its future objectives which in turn benefits managers in evaluating performance of a business

firm. Budget is prepared by managers on the basis of historical data and this reports includes

information related to expenses, revenue, income & cost. This report is essential as whole

business operations of a company is decided on the basis of future budget.

Further, this report is an essential requirement for managers as managers decide amount

of incentives for employees and negotiate with suppliers of raw materials on the basis of this

report. A company can also achieve future goals & objectives if it operates its business in

accordance with Budget Reports.

Performance Report- Performance Report gives details of overall business activities

performed by an organisation so that managers of company can review performance of company

and its employees. Further, managers develop plans & policies if performance of company is not

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

favourable according to this report and managers also conduct training & development

programmes for improving employees skills(Modugno and Di Carlo, 2019).

Different Department operated in an organisation also prepare their own performance

report so that managers which in turn helps in improving efficiency & effectiveness of operations

of each department. Managers also develop strategic objectives after reviewing performance

report of business firm.

Account Receivable Reports- If a company is selling its products & services on credit

than there is a requirement of Account Receivable Aging Report. With this report managers are

able to determine amount of bad debts and according to that they formulate their credit policy.

Further, managers can determine liquidity of company with the help of this report.

This report is essential as it gives information related to cash inflows and with this

managers are able to recover due amount from trade debtors.

Integration of Management Accounting Systems & Reports in Organisation Processes

Management Accounting Reports & Systems are inter related with each other. Because,

all the information included in managing accounting reports are abstract through systems of

management accounting. Further, both are an integrated part of organisation process as managers

make future decisions in accordance with results provided by management accounting reports.

Management Accounting System manage inventory level, determine cost of each job and

enhances profits of firm all this activities are part of business an organisation. Thus, management

accounting systems are integrated with operations of companies. Similarly, future estimation of

cost & revenue and analysis of performance is a part of business process as with that only a

company can make improvement in its operational process(Ndemewah, Menges and Hiebl,

2019).

Inventory is something without which a manufacturing process is impossible thus,

Inventory management System is useful and an integrated part of organisations process.

Management of Cost leads to profit maximisation and it is essential for a business. Formulation

of Credit Collection Policy manages cash inflow and cash is necessary for running a business

thus, Account Receivable Reports are also merged in business process.

5

programmes for improving employees skills(Modugno and Di Carlo, 2019).

Different Department operated in an organisation also prepare their own performance

report so that managers which in turn helps in improving efficiency & effectiveness of operations

of each department. Managers also develop strategic objectives after reviewing performance

report of business firm.

Account Receivable Reports- If a company is selling its products & services on credit

than there is a requirement of Account Receivable Aging Report. With this report managers are

able to determine amount of bad debts and according to that they formulate their credit policy.

Further, managers can determine liquidity of company with the help of this report.

This report is essential as it gives information related to cash inflows and with this

managers are able to recover due amount from trade debtors.

Integration of Management Accounting Systems & Reports in Organisation Processes

Management Accounting Reports & Systems are inter related with each other. Because,

all the information included in managing accounting reports are abstract through systems of

management accounting. Further, both are an integrated part of organisation process as managers

make future decisions in accordance with results provided by management accounting reports.

Management Accounting System manage inventory level, determine cost of each job and

enhances profits of firm all this activities are part of business an organisation. Thus, management

accounting systems are integrated with operations of companies. Similarly, future estimation of

cost & revenue and analysis of performance is a part of business process as with that only a

company can make improvement in its operational process(Ndemewah, Menges and Hiebl,

2019).

Inventory is something without which a manufacturing process is impossible thus,

Inventory management System is useful and an integrated part of organisations process.

Management of Cost leads to profit maximisation and it is essential for a business. Formulation

of Credit Collection Policy manages cash inflow and cash is necessary for running a business

thus, Account Receivable Reports are also merged in business process.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

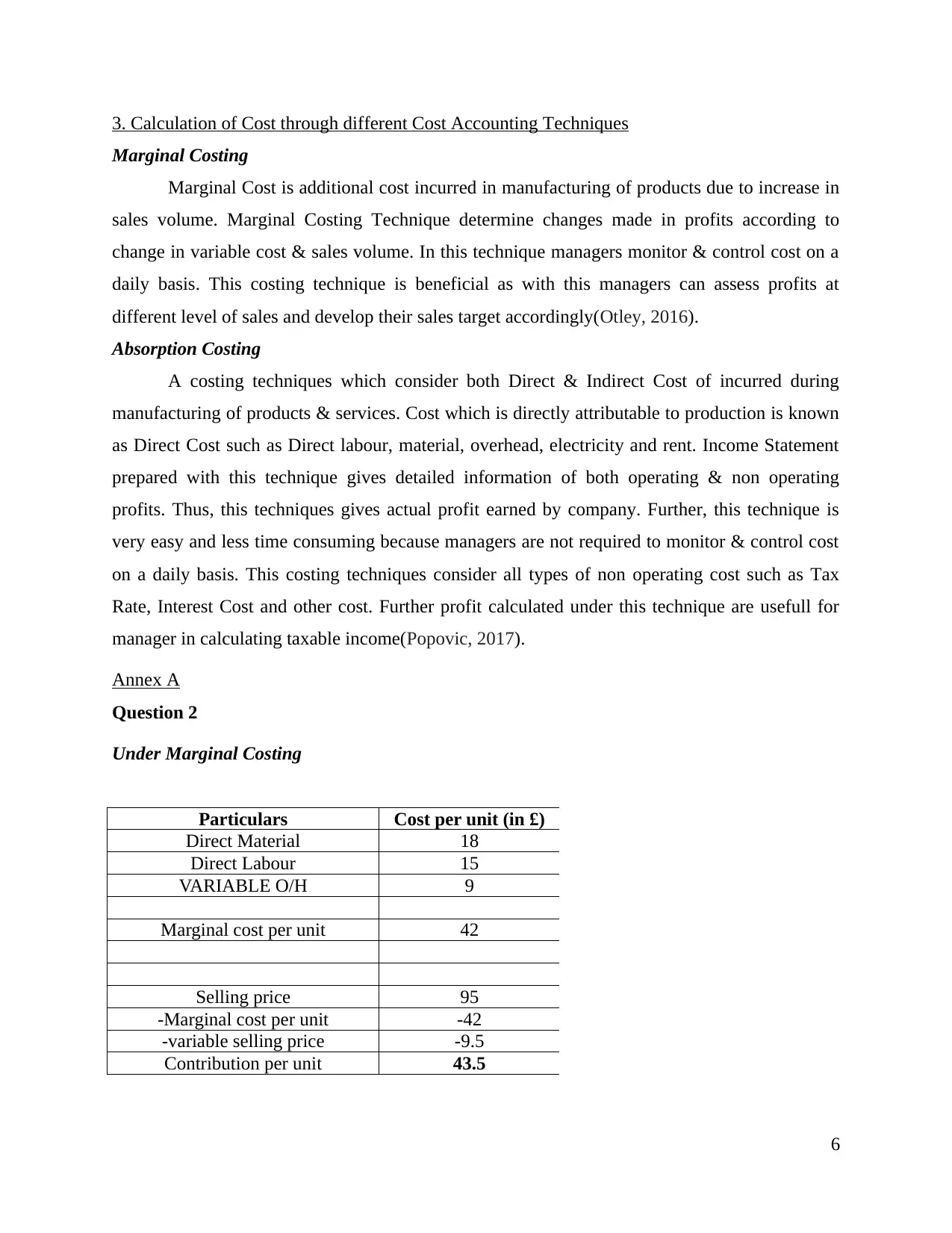

3. Calculation of Cost through different Cost Accounting Techniques

Marginal Costing

Marginal Cost is additional cost incurred in manufacturing of products due to increase in

sales volume. Marginal Costing Technique determine changes made in profits according to

change in variable cost & sales volume. In this technique managers monitor & control cost on a

daily basis. This costing technique is beneficial as with this managers can assess profits at

different level of sales and develop their sales target accordingly(Otley, 2016).

Absorption Costing

A costing techniques which consider both Direct & Indirect Cost of incurred during

manufacturing of products & services. Cost which is directly attributable to production is known

as Direct Cost such as Direct labour, material, overhead, electricity and rent. Income Statement

prepared with this technique gives detailed information of both operating & non operating

profits. Thus, this techniques gives actual profit earned by company. Further, this technique is

very easy and less time consuming because managers are not required to monitor & control cost

on a daily basis. This costing techniques consider all types of non operating cost such as Tax

Rate, Interest Cost and other cost. Further profit calculated under this technique are usefull for

manager in calculating taxable income(Popovic, 2017).

Annex A

Question 2

Under Marginal Costing

Particulars Cost per unit (in £)

Direct Material 18

Direct Labour 15

VARIABLE O/H 9

Marginal cost per unit 42

Selling price 95

-Marginal cost per unit -42

-variable selling price -9.5

Contribution per unit 43.5

6

Marginal Costing

Marginal Cost is additional cost incurred in manufacturing of products due to increase in

sales volume. Marginal Costing Technique determine changes made in profits according to

change in variable cost & sales volume. In this technique managers monitor & control cost on a

daily basis. This costing technique is beneficial as with this managers can assess profits at

different level of sales and develop their sales target accordingly(Otley, 2016).

Absorption Costing

A costing techniques which consider both Direct & Indirect Cost of incurred during

manufacturing of products & services. Cost which is directly attributable to production is known

as Direct Cost such as Direct labour, material, overhead, electricity and rent. Income Statement

prepared with this technique gives detailed information of both operating & non operating

profits. Thus, this techniques gives actual profit earned by company. Further, this technique is

very easy and less time consuming because managers are not required to monitor & control cost

on a daily basis. This costing techniques consider all types of non operating cost such as Tax

Rate, Interest Cost and other cost. Further profit calculated under this technique are usefull for

manager in calculating taxable income(Popovic, 2017).

Annex A

Question 2

Under Marginal Costing

Particulars Cost per unit (in £)

Direct Material 18

Direct Labour 15

VARIABLE O/H 9

Marginal cost per unit 42

Selling price 95

-Marginal cost per unit -42

-variable selling price -9.5

Contribution per unit 43.5

6

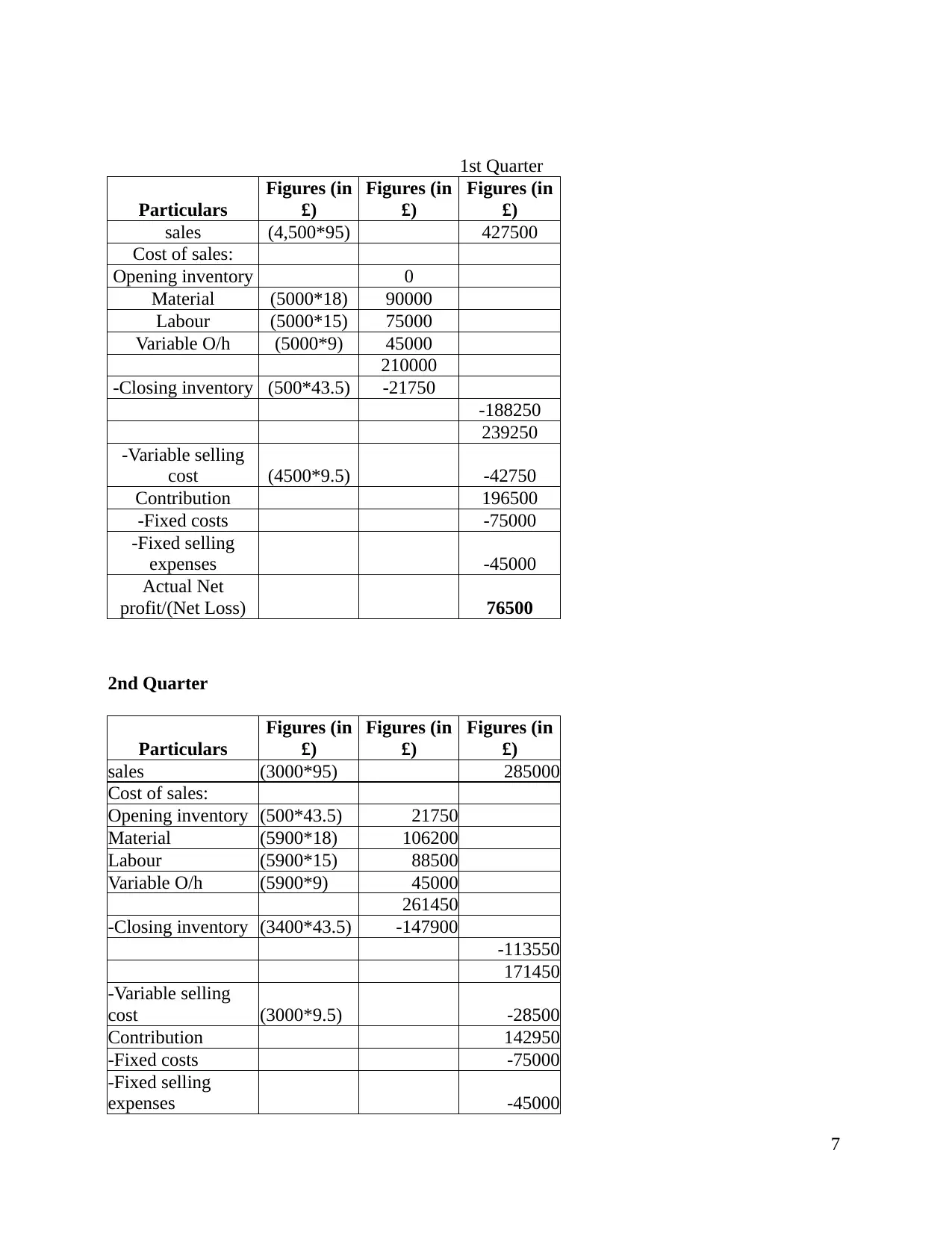

1st Quarter

Particulars

Figures (in

£)

Figures (in

£)

Figures (in

£)

sales (4,500*95) 427500

Cost of sales:

Opening inventory 0

Material (5000*18) 90000

Labour (5000*15) 75000

Variable O/h (5000*9) 45000

210000

-Closing inventory (500*43.5) -21750

-188250

239250

-Variable selling

cost (4500*9.5) -42750

Contribution 196500

-Fixed costs -75000

-Fixed selling

expenses -45000

Actual Net

profit/(Net Loss) 76500

2nd Quarter

Particulars

Figures (in

£)

Figures (in

£)

Figures (in

£)

sales (3000*95) 285000

Cost of sales:

Opening inventory (500*43.5) 21750

Material (5900*18) 106200

Labour (5900*15) 88500

Variable O/h (5900*9) 45000

261450

-Closing inventory (3400*43.5) -147900

-113550

171450

-Variable selling

cost (3000*9.5) -28500

Contribution 142950

-Fixed costs -75000

-Fixed selling

expenses -45000

7

Particulars

Figures (in

£)

Figures (in

£)

Figures (in

£)

sales (4,500*95) 427500

Cost of sales:

Opening inventory 0

Material (5000*18) 90000

Labour (5000*15) 75000

Variable O/h (5000*9) 45000

210000

-Closing inventory (500*43.5) -21750

-188250

239250

-Variable selling

cost (4500*9.5) -42750

Contribution 196500

-Fixed costs -75000

-Fixed selling

expenses -45000

Actual Net

profit/(Net Loss) 76500

2nd Quarter

Particulars

Figures (in

£)

Figures (in

£)

Figures (in

£)

sales (3000*95) 285000

Cost of sales:

Opening inventory (500*43.5) 21750

Material (5900*18) 106200

Labour (5900*15) 88500

Variable O/h (5900*9) 45000

261450

-Closing inventory (3400*43.5) -147900

-113550

171450

-Variable selling

cost (3000*9.5) -28500

Contribution 142950

-Fixed costs -75000

-Fixed selling

expenses -45000

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

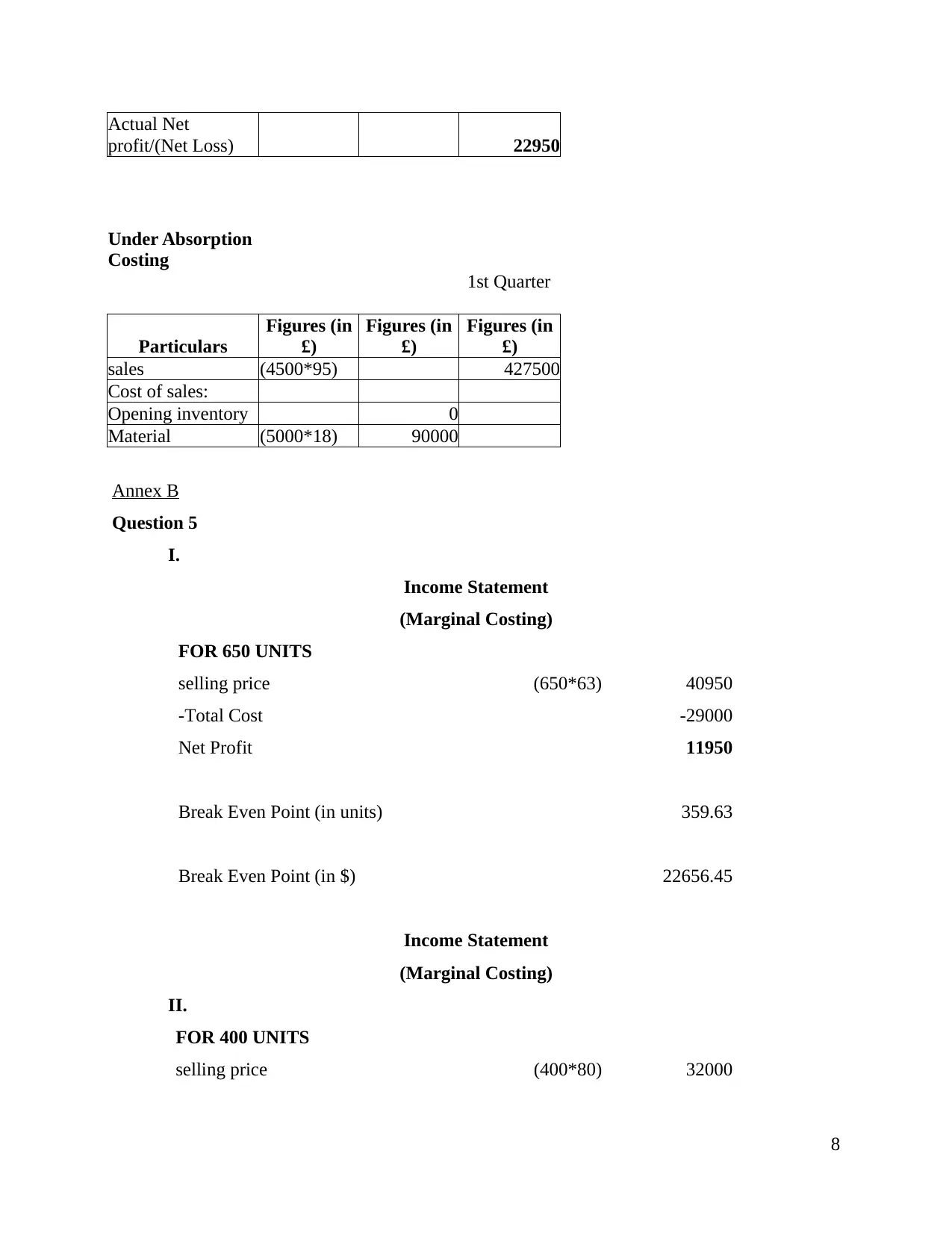

Actual Net

profit/(Net Loss) 22950

Under Absorption

Costing

1st Quarter

Particulars

Figures (in

£)

Figures (in

£)

Figures (in

£)

sales (4500*95) 427500

Cost of sales:

Opening inventory 0

Material (5000*18) 90000

Annex B

Question 5

I.

Income Statement

(Marginal Costing)

FOR 650 UNITS

selling price (650*63) 40950

-Total Cost -29000

Net Profit 11950

Break Even Point (in units) 359.63

Break Even Point (in $) 22656.45

Income Statement

(Marginal Costing)

II.

FOR 400 UNITS

selling price (400*80) 32000

8

profit/(Net Loss) 22950

Under Absorption

Costing

1st Quarter

Particulars

Figures (in

£)

Figures (in

£)

Figures (in

£)

sales (4500*95) 427500

Cost of sales:

Opening inventory 0

Material (5000*18) 90000

Annex B

Question 5

I.

Income Statement

(Marginal Costing)

FOR 650 UNITS

selling price (650*63) 40950

-Total Cost -29000

Net Profit 11950

Break Even Point (in units) 359.63

Break Even Point (in $) 22656.45

Income Statement

(Marginal Costing)

II.

FOR 400 UNITS

selling price (400*80) 32000

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

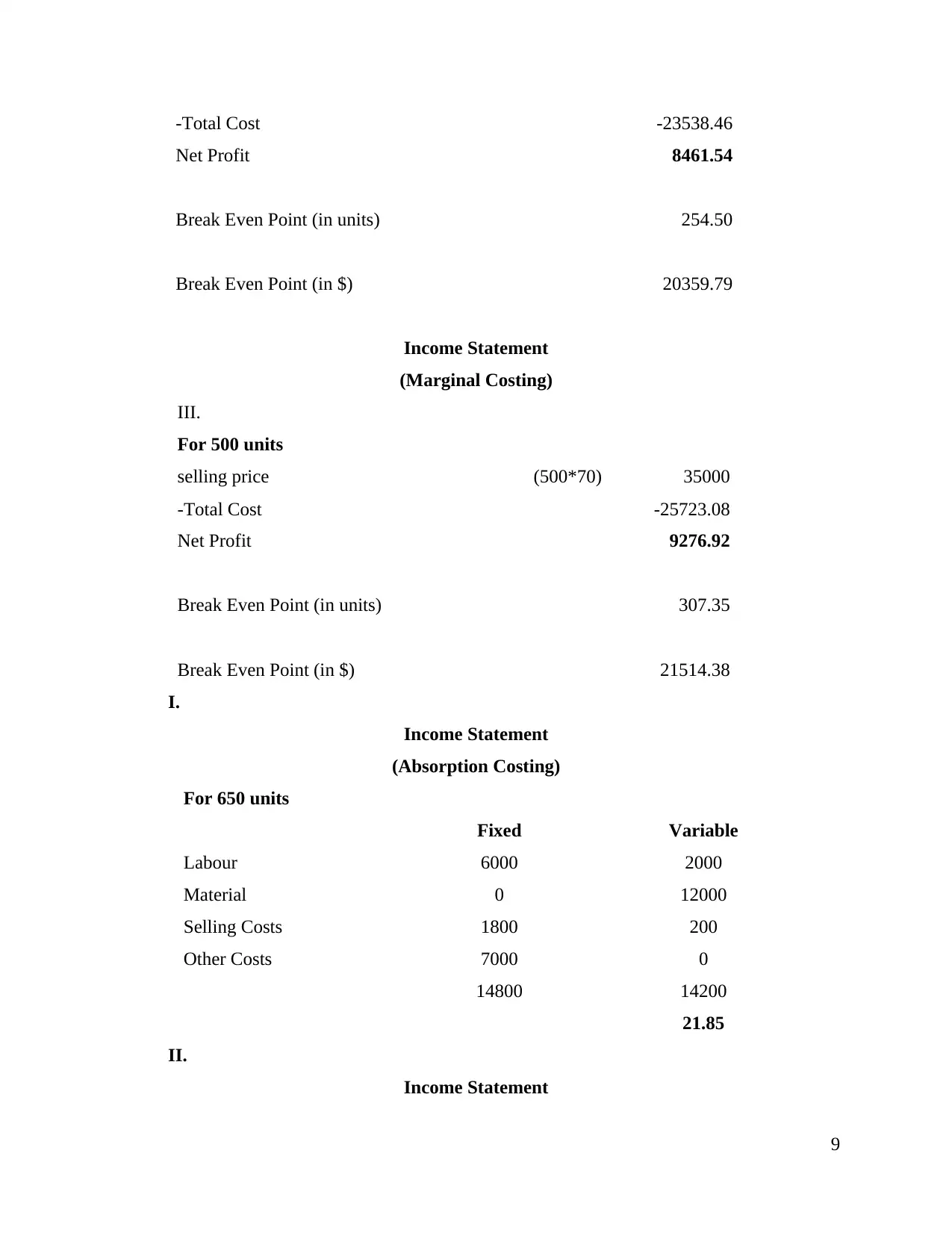

-Total Cost -23538.46

Net Profit 8461.54

Break Even Point (in units) 254.50

Break Even Point (in $) 20359.79

Income Statement

(Marginal Costing)

III.

For 500 units

selling price (500*70) 35000

-Total Cost -25723.08

Net Profit 9276.92

Break Even Point (in units) 307.35

Break Even Point (in $) 21514.38

I.

Income Statement

(Absorption Costing)

For 650 units

Fixed Variable

Labour 6000 2000

Material 0 12000

Selling Costs 1800 200

Other Costs 7000 0

14800 14200

21.85

II.

Income Statement

9

Net Profit 8461.54

Break Even Point (in units) 254.50

Break Even Point (in $) 20359.79

Income Statement

(Marginal Costing)

III.

For 500 units

selling price (500*70) 35000

-Total Cost -25723.08

Net Profit 9276.92

Break Even Point (in units) 307.35

Break Even Point (in $) 21514.38

I.

Income Statement

(Absorption Costing)

For 650 units

Fixed Variable

Labour 6000 2000

Material 0 12000

Selling Costs 1800 200

Other Costs 7000 0

14800 14200

21.85

II.

Income Statement

9

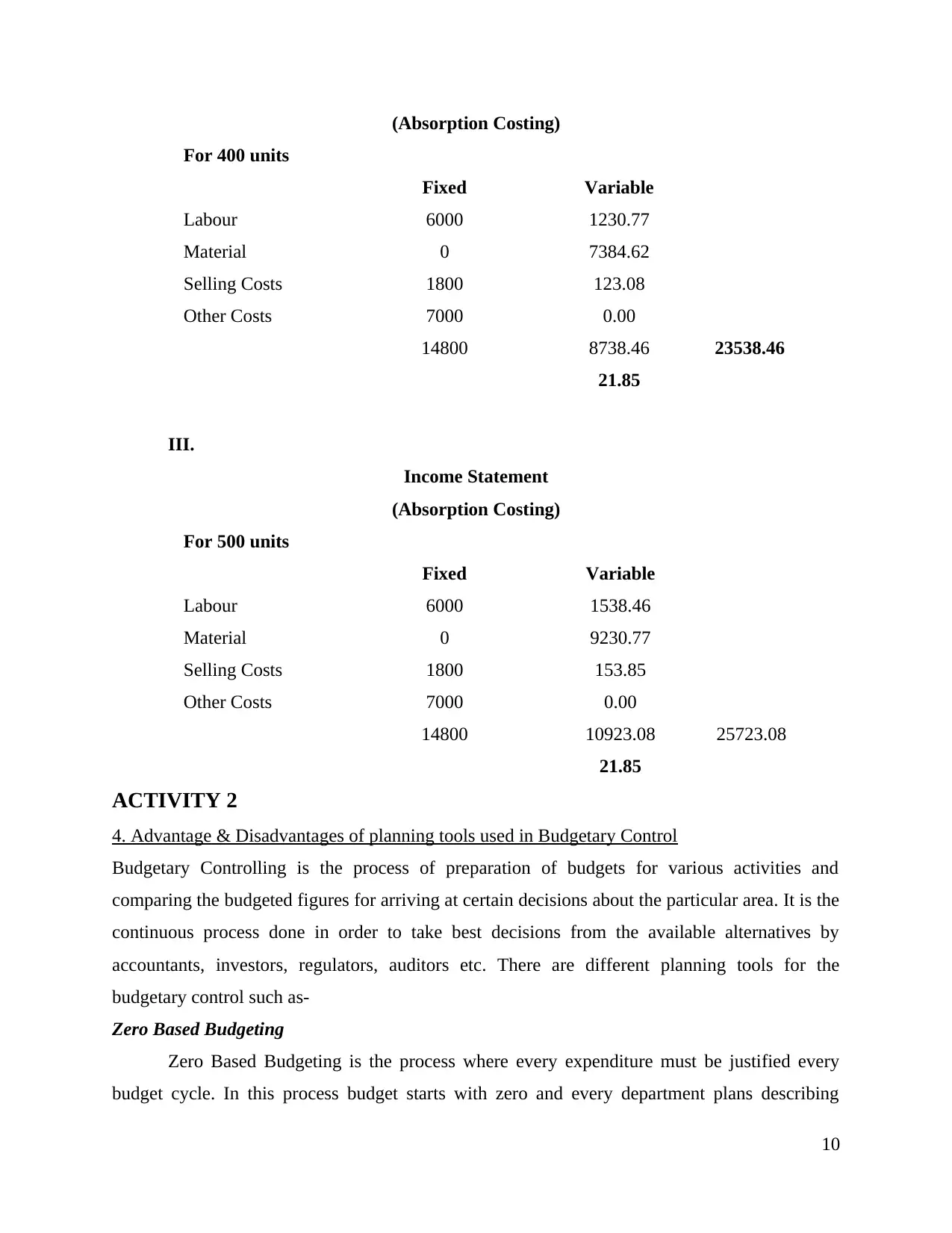

(Absorption Costing)

For 400 units

Fixed Variable

Labour 6000 1230.77

Material 0 7384.62

Selling Costs 1800 123.08

Other Costs 7000 0.00

14800 8738.46 23538.46

21.85

III.

Income Statement

(Absorption Costing)

For 500 units

Fixed Variable

Labour 6000 1538.46

Material 0 9230.77

Selling Costs 1800 153.85

Other Costs 7000 0.00

14800 10923.08 25723.08

21.85

ACTIVITY 2

4. Advantage & Disadvantages of planning tools used in Budgetary Control

Budgetary Controlling is the process of preparation of budgets for various activities and

comparing the budgeted figures for arriving at certain decisions about the particular area. It is the

continuous process done in order to take best decisions from the available alternatives by

accountants, investors, regulators, auditors etc. There are different planning tools for the

budgetary control such as-

Zero Based Budgeting

Zero Based Budgeting is the process where every expenditure must be justified every

budget cycle. In this process budget starts with zero and every department plans describing

10

For 400 units

Fixed Variable

Labour 6000 1230.77

Material 0 7384.62

Selling Costs 1800 123.08

Other Costs 7000 0.00

14800 8738.46 23538.46

21.85

III.

Income Statement

(Absorption Costing)

For 500 units

Fixed Variable

Labour 6000 1538.46

Material 0 9230.77

Selling Costs 1800 153.85

Other Costs 7000 0.00

14800 10923.08 25723.08

21.85

ACTIVITY 2

4. Advantage & Disadvantages of planning tools used in Budgetary Control

Budgetary Controlling is the process of preparation of budgets for various activities and

comparing the budgeted figures for arriving at certain decisions about the particular area. It is the

continuous process done in order to take best decisions from the available alternatives by

accountants, investors, regulators, auditors etc. There are different planning tools for the

budgetary control such as-

Zero Based Budgeting

Zero Based Budgeting is the process where every expenditure must be justified every

budget cycle. In this process budget starts with zero and every department plans describing

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.