Management Accounting Report for Capital Joinery: Analysis and Systems

VerifiedAdded on 2022/12/27

|23

|5285

|66

Report

AI Summary

This report provides a comprehensive overview of management accounting, beginning with its definition, relevance, and underlying principles. It then delves into the application of management accounting systems, including cost accounting, price optimization, job order, and inventory management. The report explores various types of management accounting reports, such as inventory management, performance, and product/service profitability reports, highlighting their benefits and integration within an organization. Furthermore, it examines cost techniques, including marginal and absorption costing, and their impact on decision-making. The report also covers budgetary control, different types of budgets, and planning tools used for budgetary control. It discusses financial problem-solving and the application of management accounting tools to address financial challenges, including the use of benchmarking and key performance indicators. The analysis is exemplified by using a case study of Capital Joinery.

Managing Accounts

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

EXECUTIVE SUMMMARY

Management accounting is a process of collecting, analysing, organizing and representing

information in such a way which useful in take decision and operate business in effective way.

This report is prepared to define how managerial system, techniques tools of planning use to

measure performance and help in decision making process . It is also recognize how various

technique of management accounting useful in solving financial problem.

Management accounting is a process of collecting, analysing, organizing and representing

information in such a way which useful in take decision and operate business in effective way.

This report is prepared to define how managerial system, techniques tools of planning use to

measure performance and help in decision making process . It is also recognize how various

technique of management accounting useful in solving financial problem.

Table of Contents

INTRODUCTION...........................................................................................................................1

SECTION 1......................................................................................................................................1

PART A...........................................................................................................................................1

Meaning of management accounting. .........................................................................................1

Relevance of management accounting. ......................................................................................1

Principle of management accounting. .........................................................................................2

Benefits of managing accounting approach in business. ............................................................2

PART B............................................................................................................................................3

Meaning of management accounting system. .............................................................................3

Types of system of management accounting. .............................................................................3

Meaning of management accounting reports...............................................................................4

Explanation of various types of reports of management accounting. .........................................4

Benefits of management accounting system................................................................................4

Integration of system of management accounting & its reports..................................................5

PART C...........................................................................................................................................5

Meaning of cost. ..........................................................................................................................5

Explanation of types of cost techniques. .....................................................................................6

Meaning of marginal costing and formulation of its statement. .................................................6

Meaning of absorption costing & formulation of its statement. ................................................7

PART D...........................................................................................................................................8

Impact of techniques of management accounting........................................................................8

SECTION 2......................................................................................................................................9

PART A...........................................................................................................................................9

Meaning of budget.......................................................................................................................9

Types of budget............................................................................................................................9

Planning tools use for the purpose of budgetary control...........................................................10

PART B..........................................................................................................................................12

Explanation regarding financial problem and how organization deal with theses problems.. 12

PART C..........................................................................................................................................12

INTRODUCTION...........................................................................................................................1

SECTION 1......................................................................................................................................1

PART A...........................................................................................................................................1

Meaning of management accounting. .........................................................................................1

Relevance of management accounting. ......................................................................................1

Principle of management accounting. .........................................................................................2

Benefits of managing accounting approach in business. ............................................................2

PART B............................................................................................................................................3

Meaning of management accounting system. .............................................................................3

Types of system of management accounting. .............................................................................3

Meaning of management accounting reports...............................................................................4

Explanation of various types of reports of management accounting. .........................................4

Benefits of management accounting system................................................................................4

Integration of system of management accounting & its reports..................................................5

PART C...........................................................................................................................................5

Meaning of cost. ..........................................................................................................................5

Explanation of types of cost techniques. .....................................................................................6

Meaning of marginal costing and formulation of its statement. .................................................6

Meaning of absorption costing & formulation of its statement. ................................................7

PART D...........................................................................................................................................8

Impact of techniques of management accounting........................................................................8

SECTION 2......................................................................................................................................9

PART A...........................................................................................................................................9

Meaning of budget.......................................................................................................................9

Types of budget............................................................................................................................9

Planning tools use for the purpose of budgetary control...........................................................10

PART B..........................................................................................................................................12

Explanation regarding financial problem and how organization deal with theses problems.. 12

PART C..........................................................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Application of tools of planning to control financial problem..................................................12

Use of tools of management accounting to respond financial problem.....................................12

CONCLUSION..............................................................................................................................14

REFERENCES................................................................................................................................1

APPENDIX......................................................................................................................................3

Use of tools of management accounting to respond financial problem.....................................12

CONCLUSION..............................................................................................................................14

REFERENCES................................................................................................................................1

APPENDIX......................................................................................................................................3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION

Management accounting is define as branch of accounting which applicable in every

business organization. This approach is developed for effectively use profession knowledge in

decision making process. This report is formulated to define relevance of managing accounting.

For this purpose Capital Joinery has been taken. In this report requirement of management

accounting, its principle use of system as well as how cost calculate to determine profit. It is also

measure tools of planning for budgetary control and use of benchmarking, key performance

indicator to overcome financial problem.

SECTION 1

PART A

Meaning of management accounting.

Management accounting: This term define as accounts which formulate for enhance

managerial efficiency of organization by providing accurate and relevant business data. In other

words it is concerned with provide professional knowledge in such a way which beneficial for

management of organization to formulate policies, strategies and take decision to run data to day

business operations (Bloom, Sadun and Van Reenen, 2016).

Relevance of management accounting.

Management accounting approach is useful for run business in systematic way,

management department of Capital Joinery apply this approach for following reasons:

Formulation of plan: With the use of various tools and technique of management

accounting, manager formulate their future business plan on the basis of analysis and observing

the future market conditions.

Useful in take decision: By recognize and calculate cost of each department manager

able to find out which project is much more beneficial for their organization, on the basis of that

they take decision regarding selection of projects or business alternatives.

Measure performance: Management accounting is essential as with the use of tools of

this approach, manager of can evaluate their organizations' financial performance for given time

period which beneficial for identify the position of entity in market.

Management accounting is define as branch of accounting which applicable in every

business organization. This approach is developed for effectively use profession knowledge in

decision making process. This report is formulated to define relevance of managing accounting.

For this purpose Capital Joinery has been taken. In this report requirement of management

accounting, its principle use of system as well as how cost calculate to determine profit. It is also

measure tools of planning for budgetary control and use of benchmarking, key performance

indicator to overcome financial problem.

SECTION 1

PART A

Meaning of management accounting.

Management accounting: This term define as accounts which formulate for enhance

managerial efficiency of organization by providing accurate and relevant business data. In other

words it is concerned with provide professional knowledge in such a way which beneficial for

management of organization to formulate policies, strategies and take decision to run data to day

business operations (Bloom, Sadun and Van Reenen, 2016).

Relevance of management accounting.

Management accounting approach is useful for run business in systematic way,

management department of Capital Joinery apply this approach for following reasons:

Formulation of plan: With the use of various tools and technique of management

accounting, manager formulate their future business plan on the basis of analysis and observing

the future market conditions.

Useful in take decision: By recognize and calculate cost of each department manager

able to find out which project is much more beneficial for their organization, on the basis of that

they take decision regarding selection of projects or business alternatives.

Measure performance: Management accounting is essential as with the use of tools of

this approach, manager of can evaluate their organizations' financial performance for given time

period which beneficial for identify the position of entity in market.

Principle of management accounting.

While applying approach of management accounting following are some principle which every

organization need to follow, these are define below:

Relevance: It is essential that every information which collect by accountant is relevant

and reliable. As on the basis of data collect from using different managing accounting tools

manager take decision on the basis of observing these data.

Value analysis: Management accounting principle based on the connect that each and

every detail and calculation useful in analysis value of organization (Botzem and Dobusch,

2017).

Communication: This is consider as most important principle of managerial accounting. This

principle states that every information and decision must be communicate in such as way which

help in decision making process. It is easily understand by each department. As well as

information provides by managing reports must be understood by internal & external

stakeholder. Thus manager of Capital Joinery need to formulate reports in such a way which is

easily communicate to every department of organization.

Product & strategies: This principle is useful apply for practical life, t is based on the

assumption is that, product and strategies holds be made in such a way which beneficial to

satisfy customer demand.

Benefits of managing accounting approach in business.

Following are the benefits of applying this approach:

Provides reliability: By using management accounting approach it provide base to

formulate financial statement which showcase relevant and reliable information regarding

financial performance of Capital Joinery.

Raise profitability: On the basis of using techniques of cost calculation manager

recognize which activity or item is the reason of arising of high cost, on the basis of tat manager

formulate polices to cut cost of operating operation which useful in raise profits. By using

effective pricing strategy also beneficial for Capital Joinery to increase their rate of generate

revenue (Bourmistrov and Kaarbøe, 2017).

Better services to customer: On the basis of analysis market condition they analysis

demand of customer and formulate their product design in such a way which helpful in satisfy

their customers.

2

While applying approach of management accounting following are some principle which every

organization need to follow, these are define below:

Relevance: It is essential that every information which collect by accountant is relevant

and reliable. As on the basis of data collect from using different managing accounting tools

manager take decision on the basis of observing these data.

Value analysis: Management accounting principle based on the connect that each and

every detail and calculation useful in analysis value of organization (Botzem and Dobusch,

2017).

Communication: This is consider as most important principle of managerial accounting. This

principle states that every information and decision must be communicate in such as way which

help in decision making process. It is easily understand by each department. As well as

information provides by managing reports must be understood by internal & external

stakeholder. Thus manager of Capital Joinery need to formulate reports in such a way which is

easily communicate to every department of organization.

Product & strategies: This principle is useful apply for practical life, t is based on the

assumption is that, product and strategies holds be made in such a way which beneficial to

satisfy customer demand.

Benefits of managing accounting approach in business.

Following are the benefits of applying this approach:

Provides reliability: By using management accounting approach it provide base to

formulate financial statement which showcase relevant and reliable information regarding

financial performance of Capital Joinery.

Raise profitability: On the basis of using techniques of cost calculation manager

recognize which activity or item is the reason of arising of high cost, on the basis of tat manager

formulate polices to cut cost of operating operation which useful in raise profits. By using

effective pricing strategy also beneficial for Capital Joinery to increase their rate of generate

revenue (Bourmistrov and Kaarbøe, 2017).

Better services to customer: On the basis of analysis market condition they analysis

demand of customer and formulate their product design in such a way which helpful in satisfy

their customers.

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Useful to spread business share: On the basis of using effective pricing strategies they

increase their profitability rate and improve quality of product which beneficial in build strong

goodwill which is helpful in spread market share of Capital Joinery.

PART B

Meaning of management accounting system.

Management accounting system: These are consider as system which manager use for

implement strategies and management accounting approach in order to successfully manage

organization (E]Guindy and Basuony, 2018).

Types of system of management accounting.

Following are the system which management department of Capital Joinery implement within

their organization:

Cost accounting system: This system is implement for calculate cost of each business

activity. Manager of Following are the system which management department of Capital Joinery

implement within their organization: use different technique which includes, marginal,

absorption and standard costing to evaluate cost of each business activity which useful in find

out activities which incurred high cash outflow and measure rate of profit (Bakhodirovna, 2019).

Price optimization system:This system help in provide various approach to apply

pricing strategies, manager of Following are the system which management department of

Capital Joinery implement within their organization have option to choose, price penetration,

price skimming, discounting and premium strategy, with the implementation of correct pricing

strategy , they can satisfy their customers able to generate profit (Hörisch, Schaltegger and

Freeman, 2020).

Job order system: Manager implement this system for find out cost required to complete

requirement of order of each job. On the basis of that manager can evaluate time require for

completion of demand of customer and revenue generate from completion of each order of

customer. Theses type of system useful for organization which work on the basis of demand of

different customer (El Guindy, and Basuony, 2018).

Inventory management system: This system is implemented within the organization for

evaluate cost of managing stock as well as time required to conversion of raw materials into

finished goods selling inventory to their final customer. Stock is consider as essential element of

3

increase their profitability rate and improve quality of product which beneficial in build strong

goodwill which is helpful in spread market share of Capital Joinery.

PART B

Meaning of management accounting system.

Management accounting system: These are consider as system which manager use for

implement strategies and management accounting approach in order to successfully manage

organization (E]Guindy and Basuony, 2018).

Types of system of management accounting.

Following are the system which management department of Capital Joinery implement within

their organization:

Cost accounting system: This system is implement for calculate cost of each business

activity. Manager of Following are the system which management department of Capital Joinery

implement within their organization: use different technique which includes, marginal,

absorption and standard costing to evaluate cost of each business activity which useful in find

out activities which incurred high cash outflow and measure rate of profit (Bakhodirovna, 2019).

Price optimization system:This system help in provide various approach to apply

pricing strategies, manager of Following are the system which management department of

Capital Joinery implement within their organization have option to choose, price penetration,

price skimming, discounting and premium strategy, with the implementation of correct pricing

strategy , they can satisfy their customers able to generate profit (Hörisch, Schaltegger and

Freeman, 2020).

Job order system: Manager implement this system for find out cost required to complete

requirement of order of each job. On the basis of that manager can evaluate time require for

completion of demand of customer and revenue generate from completion of each order of

customer. Theses type of system useful for organization which work on the basis of demand of

different customer (El Guindy, and Basuony, 2018).

Inventory management system: This system is implemented within the organization for

evaluate cost of managing stock as well as time required to conversion of raw materials into

finished goods selling inventory to their final customer. Stock is consider as essential element of

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

business organization, thus manager of Capital Joinery by using ABC analysis, VED and LIFO,

FIFO method of accounting able to manage and control their level of inventory (Hörisch,

Schaltegger, and Freeman, 2020).

Meaning of management accounting reports.

Management accounting reports: Theses are documents which are used for the purpose of

collection of data wand represent them in such a way which beneficial for decision making

process (Hyndman and Liguori, 2016).

Explanation of various types of reports of management accounting.

There are different types of managerial accounting reports which are formulated by

manager of Capital Joinery, these are define below:

Inventory management report: This report is formulated on the basis of collection of

data of from technique and tools use in system of inventory management. This report define all

the essential information regarding time require for management of stock and delivering it to

customers and cost require storing of inventory, maximum, minimum and normal level of stock

require for specific period of time. These information are given in inventory management report,

on the basis of that manager take decision for managing inventory.

Performance report: This report is formulate for define summery of each report, it

includes the performance of each department, time require for manufacturing of product ,,

delivering of service, rate of employee turnover, their performance, on the basis of that manager

of Capital Joinery formulate polices and give rewards to employee by evaluate their

performance.

Product / Service profitability report: This is consider as one of the most relevant

report of management accounting. Product report is formulate to measure the rate of profitability

and income generate by running business operations (Jack, Florez-Lopez and Ramon-Jeronimo,

2018).

On the basis of data summarised in this report manager of Capital Joinery find out which

product or service provides them more benefit as compare to others.

Benefits of management accounting system.

System Benefits

Job costing This system is implemented for recognise cost

4

FIFO method of accounting able to manage and control their level of inventory (Hörisch,

Schaltegger, and Freeman, 2020).

Meaning of management accounting reports.

Management accounting reports: Theses are documents which are used for the purpose of

collection of data wand represent them in such a way which beneficial for decision making

process (Hyndman and Liguori, 2016).

Explanation of various types of reports of management accounting.

There are different types of managerial accounting reports which are formulated by

manager of Capital Joinery, these are define below:

Inventory management report: This report is formulated on the basis of collection of

data of from technique and tools use in system of inventory management. This report define all

the essential information regarding time require for management of stock and delivering it to

customers and cost require storing of inventory, maximum, minimum and normal level of stock

require for specific period of time. These information are given in inventory management report,

on the basis of that manager take decision for managing inventory.

Performance report: This report is formulate for define summery of each report, it

includes the performance of each department, time require for manufacturing of product ,,

delivering of service, rate of employee turnover, their performance, on the basis of that manager

of Capital Joinery formulate polices and give rewards to employee by evaluate their

performance.

Product / Service profitability report: This is consider as one of the most relevant

report of management accounting. Product report is formulate to measure the rate of profitability

and income generate by running business operations (Jack, Florez-Lopez and Ramon-Jeronimo,

2018).

On the basis of data summarised in this report manager of Capital Joinery find out which

product or service provides them more benefit as compare to others.

Benefits of management accounting system.

System Benefits

Job costing This system is implemented for recognise cost

4

required for completion of each job. Job

costing system help in evaluate time require for

completion of demand on the basis of that

manager formulate policies regarding each job.

Costing system Manager of Capital Joinery implement this

system for evaluate cost of each business

operation, on the basis of formulation of cost

statement manager recognize which alternative

is benefit for the purpose of minimize cost and

generate high profit (Kruis, Speklé and

Widener, 2016).

Price optimization On the basis of using this system manager

select pricing strategy which help in generate

profits. By applying price skimming strategy

manager of Capital Joinery able to generate

profit and attain competitive business

advantage.

Inventory management system This system is apply for controlling cost

require to manage and store of inventory. On

the basis of tools use by this system

Integration of system of management accounting & its reports.

Manager of Capital Joinery use various concept of management accounting they apply

system of cost, inventory and job order system on the basis of that they collect essential

information which beneficial to proved base for formulation of accounting report. Thus

integration of systems in reports require to play essential role while applying this approach.

5

costing system help in evaluate time require for

completion of demand on the basis of that

manager formulate policies regarding each job.

Costing system Manager of Capital Joinery implement this

system for evaluate cost of each business

operation, on the basis of formulation of cost

statement manager recognize which alternative

is benefit for the purpose of minimize cost and

generate high profit (Kruis, Speklé and

Widener, 2016).

Price optimization On the basis of using this system manager

select pricing strategy which help in generate

profits. By applying price skimming strategy

manager of Capital Joinery able to generate

profit and attain competitive business

advantage.

Inventory management system This system is apply for controlling cost

require to manage and store of inventory. On

the basis of tools use by this system

Integration of system of management accounting & its reports.

Manager of Capital Joinery use various concept of management accounting they apply

system of cost, inventory and job order system on the basis of that they collect essential

information which beneficial to proved base for formulation of accounting report. Thus

integration of systems in reports require to play essential role while applying this approach.

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

PART C

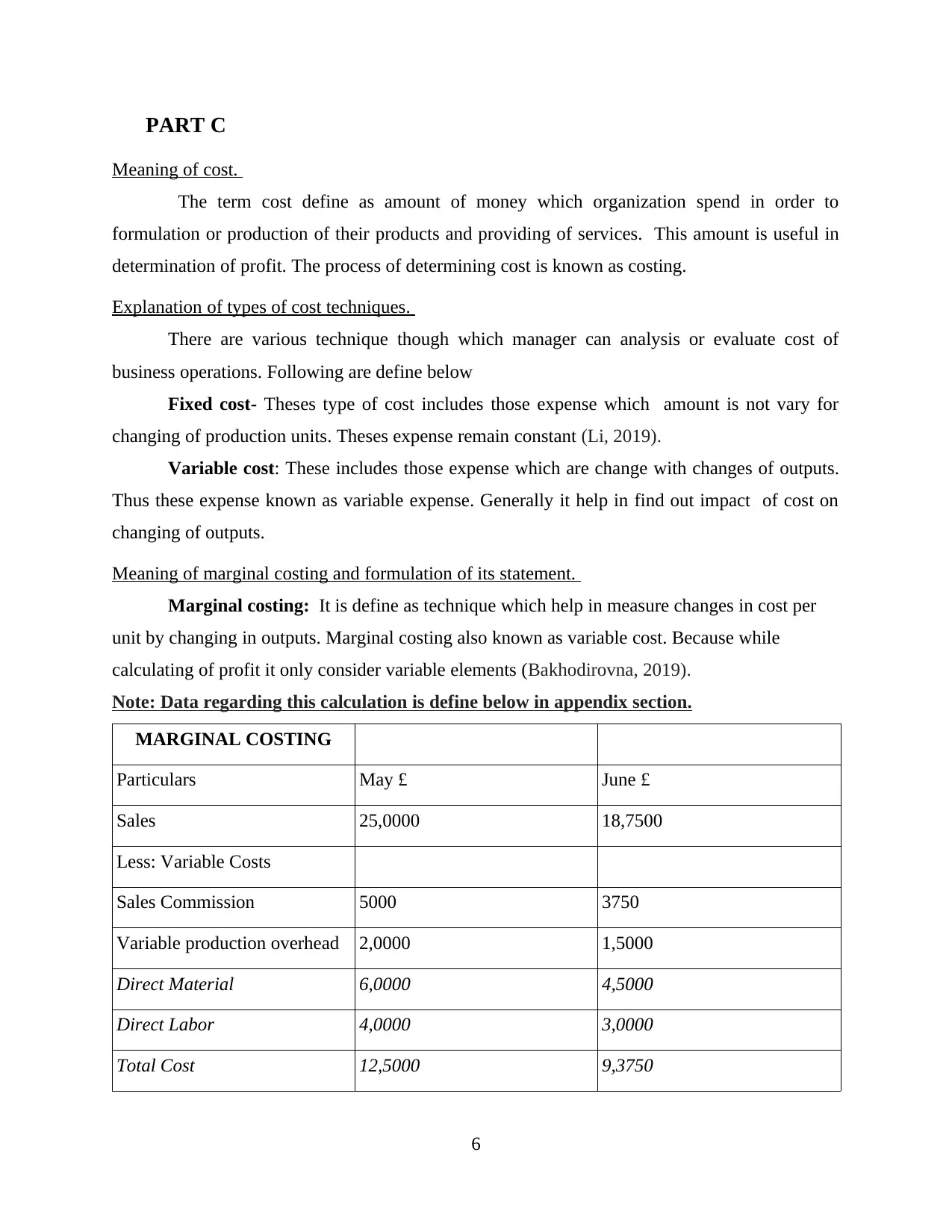

Meaning of cost.

The term cost define as amount of money which organization spend in order to

formulation or production of their products and providing of services. This amount is useful in

determination of profit. The process of determining cost is known as costing.

Explanation of types of cost techniques.

There are various technique though which manager can analysis or evaluate cost of

business operations. Following are define below

Fixed cost- Theses type of cost includes those expense which amount is not vary for

changing of production units. Theses expense remain constant (Li, 2019).

Variable cost: These includes those expense which are change with changes of outputs.

Thus these expense known as variable expense. Generally it help in find out impact of cost on

changing of outputs.

Meaning of marginal costing and formulation of its statement.

Marginal costing: It is define as technique which help in measure changes in cost per

unit by changing in outputs. Marginal costing also known as variable cost. Because while

calculating of profit it only consider variable elements (Bakhodirovna, 2019).

Note: Data regarding this calculation is define below in appendix section.

MARGINAL COSTING

Particulars May £ June £

Sales 25,0000 18,7500

Less: Variable Costs

Sales Commission 5000 3750

Variable production overhead 2,0000 1,5000

Direct Material 6,0000 4,5000

Direct Labor 4,0000 3,0000

Total Cost 12,5000 9,3750

6

Meaning of cost.

The term cost define as amount of money which organization spend in order to

formulation or production of their products and providing of services. This amount is useful in

determination of profit. The process of determining cost is known as costing.

Explanation of types of cost techniques.

There are various technique though which manager can analysis or evaluate cost of

business operations. Following are define below

Fixed cost- Theses type of cost includes those expense which amount is not vary for

changing of production units. Theses expense remain constant (Li, 2019).

Variable cost: These includes those expense which are change with changes of outputs.

Thus these expense known as variable expense. Generally it help in find out impact of cost on

changing of outputs.

Meaning of marginal costing and formulation of its statement.

Marginal costing: It is define as technique which help in measure changes in cost per

unit by changing in outputs. Marginal costing also known as variable cost. Because while

calculating of profit it only consider variable elements (Bakhodirovna, 2019).

Note: Data regarding this calculation is define below in appendix section.

MARGINAL COSTING

Particulars May £ June £

Sales 25,0000 18,7500

Less: Variable Costs

Sales Commission 5000 3750

Variable production overhead 2,0000 1,5000

Direct Material 6,0000 4,5000

Direct Labor 4,0000 3,0000

Total Cost 12,5000 9,3750

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

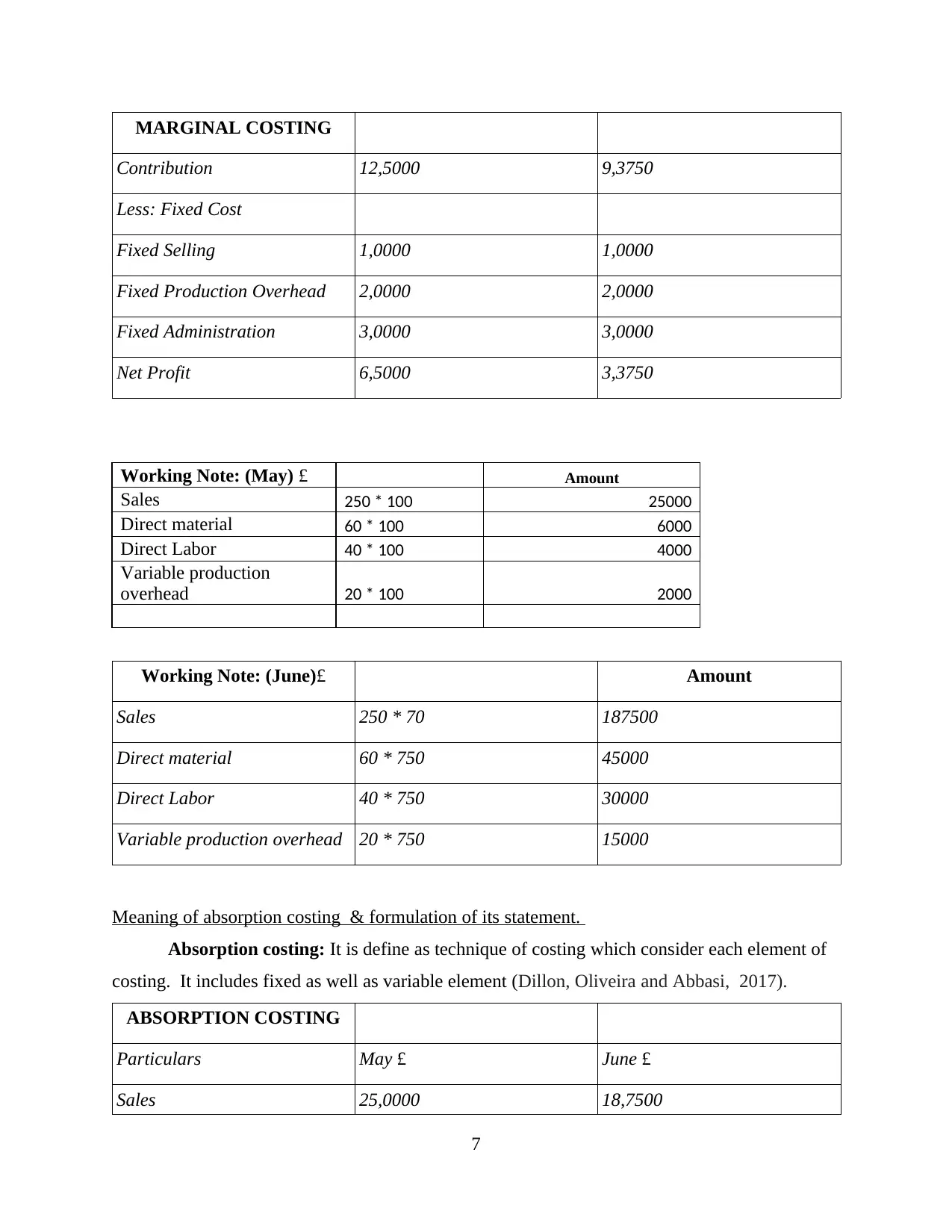

MARGINAL COSTING

Contribution 12,5000 9,3750

Less: Fixed Cost

Fixed Selling 1,0000 1,0000

Fixed Production Overhead 2,0000 2,0000

Fixed Administration 3,0000 3,0000

Net Profit 6,5000 3,3750

Working Note: (May) £ Amount

Sales 250 * 100 25000

Direct material 60 * 100 6000

Direct Labor 40 * 100 4000

Variable production

overhead 20 * 100 2000

Working Note: (June)£ Amount

Sales 250 * 70 187500

Direct material 60 * 750 45000

Direct Labor 40 * 750 30000

Variable production overhead 20 * 750 15000

Meaning of absorption costing & formulation of its statement.

Absorption costing: It is define as technique of costing which consider each element of

costing. It includes fixed as well as variable element (Dillon, Oliveira and Abbasi, 2017).

ABSORPTION COSTING

Particulars May £ June £

Sales 25,0000 18,7500

7

Contribution 12,5000 9,3750

Less: Fixed Cost

Fixed Selling 1,0000 1,0000

Fixed Production Overhead 2,0000 2,0000

Fixed Administration 3,0000 3,0000

Net Profit 6,5000 3,3750

Working Note: (May) £ Amount

Sales 250 * 100 25000

Direct material 60 * 100 6000

Direct Labor 40 * 100 4000

Variable production

overhead 20 * 100 2000

Working Note: (June)£ Amount

Sales 250 * 70 187500

Direct material 60 * 750 45000

Direct Labor 40 * 750 30000

Variable production overhead 20 * 750 15000

Meaning of absorption costing & formulation of its statement.

Absorption costing: It is define as technique of costing which consider each element of

costing. It includes fixed as well as variable element (Dillon, Oliveira and Abbasi, 2017).

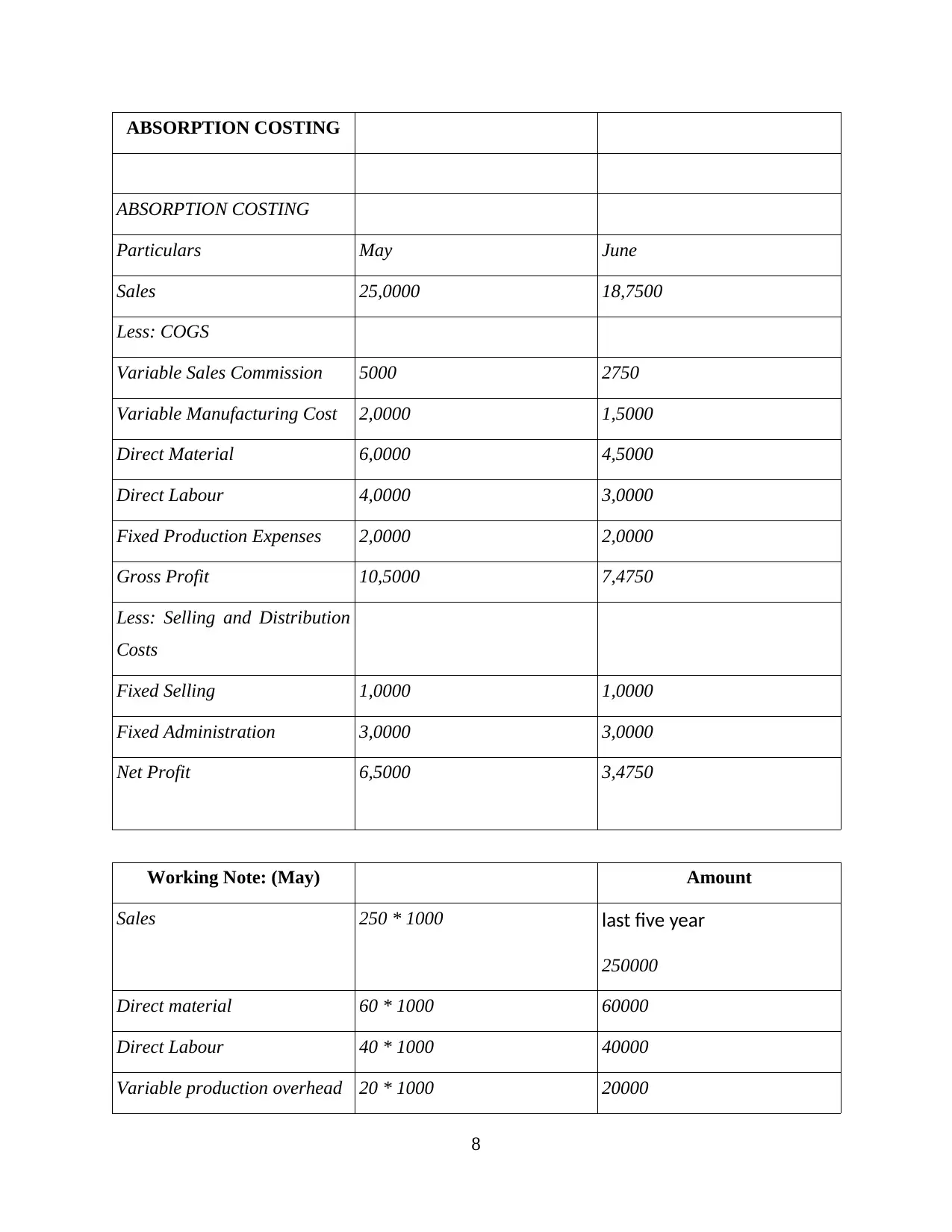

ABSORPTION COSTING

Particulars May £ June £

Sales 25,0000 18,7500

7

ABSORPTION COSTING

ABSORPTION COSTING

Particulars May June

Sales 25,0000 18,7500

Less: COGS

Variable Sales Commission 5000 2750

Variable Manufacturing Cost 2,0000 1,5000

Direct Material 6,0000 4,5000

Direct Labour 4,0000 3,0000

Fixed Production Expenses 2,0000 2,0000

Gross Profit 10,5000 7,4750

Less: Selling and Distribution

Costs

Fixed Selling 1,0000 1,0000

Fixed Administration 3,0000 3,0000

Net Profit 6,5000 3,4750

Working Note: (May) Amount

Sales 250 * 1000 last five year

250000

Direct material 60 * 1000 60000

Direct Labour 40 * 1000 40000

Variable production overhead 20 * 1000 20000

8

ABSORPTION COSTING

Particulars May June

Sales 25,0000 18,7500

Less: COGS

Variable Sales Commission 5000 2750

Variable Manufacturing Cost 2,0000 1,5000

Direct Material 6,0000 4,5000

Direct Labour 4,0000 3,0000

Fixed Production Expenses 2,0000 2,0000

Gross Profit 10,5000 7,4750

Less: Selling and Distribution

Costs

Fixed Selling 1,0000 1,0000

Fixed Administration 3,0000 3,0000

Net Profit 6,5000 3,4750

Working Note: (May) Amount

Sales 250 * 1000 last five year

250000

Direct material 60 * 1000 60000

Direct Labour 40 * 1000 40000

Variable production overhead 20 * 1000 20000

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 23

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.