Accounting Theory and Contemporary Issues: AASB Report Analysis 2017

VerifiedAdded on 2020/03/02

|16

|3383

|36

Report

AI Summary

This report provides an executive summary and detailed analysis of the Australian Accounting Standards Board (AASB), focusing on its role in framing and implementing accounting standards for both public and private organizations. The report delves into the AASB's functions, powers, and the process of standard setting, including the consideration of stakeholder input and the adoption of IFRS. Part A reviews the literature on AASB's standard-setting process, including the identification of technical issues, project proposals, consultation with stakeholders, and the issuance of pronouncements. Part B focuses on ED116, examining its implications for the recognition of property, plant, and equipment, the adoption of fair value, and the impact on both profit and non-profit organizations. The report highlights the benefits of fair value analysis, the changes proposed, and the overall impact on transparency and financial reporting. It also discusses how the AASB considers the needs of domestic companies and aligns its standards with international financial reporting standards, including the specifics for AASB 136.

Accounting theory

and contemporary

issues

and contemporary

issues

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

By student name

Professor

Date: 24 August, 2017.

1 | P a g e

By student name

Professor

Date: 24 August, 2017.

1 | P a g e

2

Executive summary

The Australian Accounting Standard Board is an Australian agency that has the major

responsibility of framing of the accounting standards. These standards are applicable in the

preparation and presentation of the financial statements of the public and private organisations

to the best of their ability. It has a set of functions and powers that are well defined by the

government. In this report we will confer upon its right of making changes to the already

exsisting standards, issuing new standards, the basis of framing standards and what effect does

it have on other entities. We will also present a brief report on the new ED116, and its overall

effect on the various entities.

2 | P a g e

Executive summary

The Australian Accounting Standard Board is an Australian agency that has the major

responsibility of framing of the accounting standards. These standards are applicable in the

preparation and presentation of the financial statements of the public and private organisations

to the best of their ability. It has a set of functions and powers that are well defined by the

government. In this report we will confer upon its right of making changes to the already

exsisting standards, issuing new standards, the basis of framing standards and what effect does

it have on other entities. We will also present a brief report on the new ED116, and its overall

effect on the various entities.

2 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

Contents

Introduction……………………………………………………………………………………………………....4

Part A ......................…………………….......................................................................... 5

Part B......................…………………….......................................................................... 9

Conclusions and recommendations........................................................................13

References.............................................................................................................. 14

3 | P a g e

Contents

Introduction……………………………………………………………………………………………………....4

Part A ......................…………………….......................................................................... 5

Part B......................…………………….......................................................................... 9

Conclusions and recommendations........................................................................13

References.............................................................................................................. 14

3 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

Introduction

An accounting standard is a basis of accounting that applies to various transactions and

events of accounting. All the organisations are expected to prepare their financial statements

on the basis of these standards. If there is any change in the methods, then proper disclosure

must be given by the company. The framing body that frames these standards has to apply a lot

of rational thinking before framing them. The standards must be easy to understand, price and

clear. It is important that the members of the board of AASB, that is part of the framing comity,

takes into consideration all the people who depend on these standards and policies to show the

true state of business affairs. While in the process of formulation of the accounting standards

the Australian stakeholder can also suggest the board regarding some technical issue that they

face and the board can comment on the same. After the issue is identified, a project proposal

will be designed which will cover all the important points relating to the project. The overall

benefits, the total cost consideration and what affect it will have on the organisations. (Abbott

& Kantor, 2017).

4 | P a g e

Introduction

An accounting standard is a basis of accounting that applies to various transactions and

events of accounting. All the organisations are expected to prepare their financial statements

on the basis of these standards. If there is any change in the methods, then proper disclosure

must be given by the company. The framing body that frames these standards has to apply a lot

of rational thinking before framing them. The standards must be easy to understand, price and

clear. It is important that the members of the board of AASB, that is part of the framing comity,

takes into consideration all the people who depend on these standards and policies to show the

true state of business affairs. While in the process of formulation of the accounting standards

the Australian stakeholder can also suggest the board regarding some technical issue that they

face and the board can comment on the same. After the issue is identified, a project proposal

will be designed which will cover all the important points relating to the project. The overall

benefits, the total cost consideration and what affect it will have on the organisations. (Abbott

& Kantor, 2017).

4 | P a g e

5

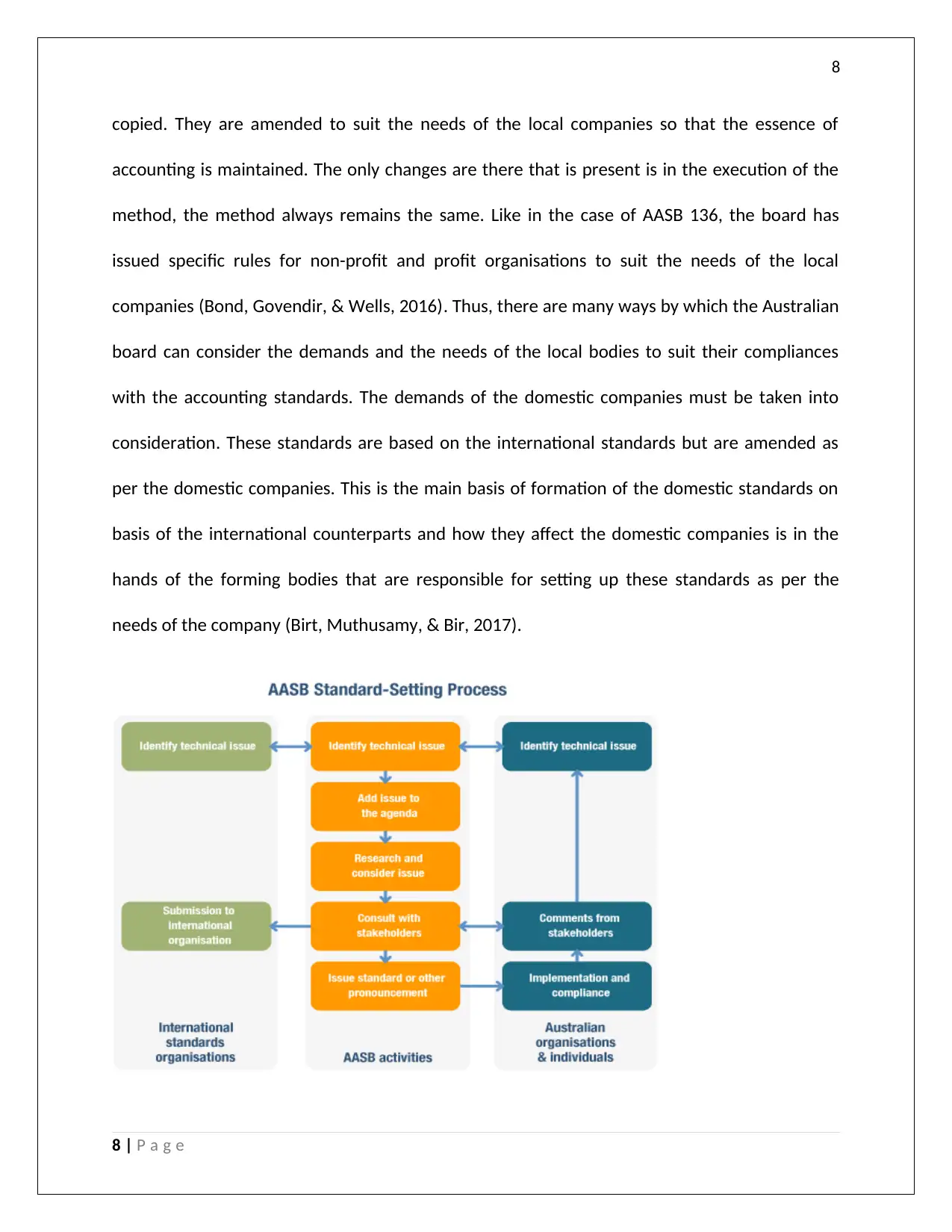

Part A literature review

One of the most important functions of the AASB is the preparation and presentation of

the accounting standards. This standard setting process is a technical process and a lot has to

be considered before the formation of particular standard.

The process starts with identification of technical issue that may be there in the

accounting process. The International Accounting Standards Board (IASB) or the IFRS

Interpretations Committee (IFRIC) identifies it. Since January 1, 2005, the Australian

government has adopted IFRS, therefore all the issues that were part of the IASB or the IFRIC

committee were also a part of the AASB. The International Public Sector Accounting Standards

Board (IPSASB) also identified the issues. The main work of the AASB is to monitor the work of

the (IPSASB), and take its decision based on the same. It undertakes works on particular topics

and then comment on the same (Chariri, 2017). The Australian stakeholder can also suggest

the board regarding some technical issue that they face and the board can comment on the

same. After the issue is identified, a project proposal will be designed which will cover all the

important points relating to the project. The overall benefits, the total cost consideration and

what affect it will have on the organisations. After considering all the factors, it will be decided

whether to carry forward the project. If the project is considered it will be added to the agenda,

once the agenda is considered the AASB will look into the specific details of the matter based

on the reports submitted by the members of the board. Relevant materials may be taken from

the other standard setting board like the IASB, the IPSASB and the New Zealand Accounting

Standards Board, or from other organisations. After the research is completed, proper

5 | P a g e

Part A literature review

One of the most important functions of the AASB is the preparation and presentation of

the accounting standards. This standard setting process is a technical process and a lot has to

be considered before the formation of particular standard.

The process starts with identification of technical issue that may be there in the

accounting process. The International Accounting Standards Board (IASB) or the IFRS

Interpretations Committee (IFRIC) identifies it. Since January 1, 2005, the Australian

government has adopted IFRS, therefore all the issues that were part of the IASB or the IFRIC

committee were also a part of the AASB. The International Public Sector Accounting Standards

Board (IPSASB) also identified the issues. The main work of the AASB is to monitor the work of

the (IPSASB), and take its decision based on the same. It undertakes works on particular topics

and then comment on the same (Chariri, 2017). The Australian stakeholder can also suggest

the board regarding some technical issue that they face and the board can comment on the

same. After the issue is identified, a project proposal will be designed which will cover all the

important points relating to the project. The overall benefits, the total cost consideration and

what affect it will have on the organisations. After considering all the factors, it will be decided

whether to carry forward the project. If the project is considered it will be added to the agenda,

once the agenda is considered the AASB will look into the specific details of the matter based

on the reports submitted by the members of the board. Relevant materials may be taken from

the other standard setting board like the IASB, the IPSASB and the New Zealand Accounting

Standards Board, or from other organisations. After the research is completed, proper

5 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

consultation is taken from the stakeholders. All the necessary public documents related to the

project like the exposure draft that is a draft on the proposed standard, invitation to comment,

draft interpretations and discussion papers are made available to the public and the

stakeholders to give their comment on the same.

The AASB may choose to issue international document in Australia in line with the

standards that they are considering for framework. The other ways to getting proper opinion

for the proposed standards is by Roundtable discussions, Project Advisory Panels,

Interpretation Advisory Panels etc (Abbott & Kantor, 2017).

After considering all the opinions, the board may decide to issue the pronouncement

either in the form of document, or an announcement. When it comes to standards for the

profitable organisations, they must be in line with the international standards that are issued by

the international bodies like the IFRS. It is to make sure that the standards that are issued by

the AASB must be in line with the IFRS. In case of AASB, it follows a neutrality policy, where

transaction whether it belong to a public company or private company, it must follow the same

basis of accounting. It does not matter whether it is a profit oriented industry or a non-profit

industry. After the formation of the draft, it is submitted to the international organisations after

taking into considerations all the inputs and feedbacks that it received from various sources.

After finalisation, the board looks after the proper implementation of the proposed standards

and makes sure that all the companies on which it is applicable follows the same to the best of

their ability, with proper disclosure (Guragai, Hunt, Neri, & Taylor, 2017). While making changes

to the existing standards, the board considers any kind of technical issues that the companies

6 | P a g e

consultation is taken from the stakeholders. All the necessary public documents related to the

project like the exposure draft that is a draft on the proposed standard, invitation to comment,

draft interpretations and discussion papers are made available to the public and the

stakeholders to give their comment on the same.

The AASB may choose to issue international document in Australia in line with the

standards that they are considering for framework. The other ways to getting proper opinion

for the proposed standards is by Roundtable discussions, Project Advisory Panels,

Interpretation Advisory Panels etc (Abbott & Kantor, 2017).

After considering all the opinions, the board may decide to issue the pronouncement

either in the form of document, or an announcement. When it comes to standards for the

profitable organisations, they must be in line with the international standards that are issued by

the international bodies like the IFRS. It is to make sure that the standards that are issued by

the AASB must be in line with the IFRS. In case of AASB, it follows a neutrality policy, where

transaction whether it belong to a public company or private company, it must follow the same

basis of accounting. It does not matter whether it is a profit oriented industry or a non-profit

industry. After the formation of the draft, it is submitted to the international organisations after

taking into considerations all the inputs and feedbacks that it received from various sources.

After finalisation, the board looks after the proper implementation of the proposed standards

and makes sure that all the companies on which it is applicable follows the same to the best of

their ability, with proper disclosure (Guragai, Hunt, Neri, & Taylor, 2017). While making changes

to the existing standards, the board considers any kind of technical issues that the companies

6 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

or the stakeholders are facing. After doing proper research into the matter and taking

knowledge about the same in conformity with the other international standards, the board will

follow the e same method of preparation and presentation of the draft, and then implement

the same and monitor the results. This is the standards procedure for formation of the

standards and for making any changes to the exsisting standards. The main point is that all the

standards that the AASB develops are in line with the international standards that are framed

by the international organisations. All the changes that the board proposes in the relevant

standards are given out in the media news with all the necessary details. Details about the

same can be ascertained on the official site of the company (Drew & Grant, 2017).

While developing these standards it is important that the board must consider the local

domestic issues that the companies in Australia faces because of any technical issues. It is

important that the same must be considered while formation of the standards. The boards ask

for feedbacks from various stakeholders and corporate on the proposed draft that is related to

any standard in various ways. It releases exposure draft on which the public can give their

feedback; it also arranges panel discussions, in house discussions, to get the opinion of the

people who might be affected by the decision of the standard (Maynard, 2017). After taking all

the feedback that is necessary the board incorporates the same, that is feel is relevant in the

proposes draft and then finalises the same. The companies have the option to make proposals

to the board in cases where they might find any technical issues and ask the board to provide a

solution on the same. While formation of the standard the board considers all these

recommendations that are given by the companies in its board report. The domestic body

prepares the standard that is in line the international financial reporting standards but are not

7 | P a g e

or the stakeholders are facing. After doing proper research into the matter and taking

knowledge about the same in conformity with the other international standards, the board will

follow the e same method of preparation and presentation of the draft, and then implement

the same and monitor the results. This is the standards procedure for formation of the

standards and for making any changes to the exsisting standards. The main point is that all the

standards that the AASB develops are in line with the international standards that are framed

by the international organisations. All the changes that the board proposes in the relevant

standards are given out in the media news with all the necessary details. Details about the

same can be ascertained on the official site of the company (Drew & Grant, 2017).

While developing these standards it is important that the board must consider the local

domestic issues that the companies in Australia faces because of any technical issues. It is

important that the same must be considered while formation of the standards. The boards ask

for feedbacks from various stakeholders and corporate on the proposed draft that is related to

any standard in various ways. It releases exposure draft on which the public can give their

feedback; it also arranges panel discussions, in house discussions, to get the opinion of the

people who might be affected by the decision of the standard (Maynard, 2017). After taking all

the feedback that is necessary the board incorporates the same, that is feel is relevant in the

proposes draft and then finalises the same. The companies have the option to make proposals

to the board in cases where they might find any technical issues and ask the board to provide a

solution on the same. While formation of the standard the board considers all these

recommendations that are given by the companies in its board report. The domestic body

prepares the standard that is in line the international financial reporting standards but are not

7 | P a g e

8

copied. They are amended to suit the needs of the local companies so that the essence of

accounting is maintained. The only changes are there that is present is in the execution of the

method, the method always remains the same. Like in the case of AASB 136, the board has

issued specific rules for non-profit and profit organisations to suit the needs of the local

companies (Bond, Govendir, & Wells, 2016). Thus, there are many ways by which the Australian

board can consider the demands and the needs of the local bodies to suit their compliances

with the accounting standards. The demands of the domestic companies must be taken into

consideration. These standards are based on the international standards but are amended as

per the domestic companies. This is the main basis of formation of the domestic standards on

basis of the international counterparts and how they affect the domestic companies is in the

hands of the forming bodies that are responsible for setting up these standards as per the

needs of the company (Birt, Muthusamy, & Bir, 2017).

8 | P a g e

copied. They are amended to suit the needs of the local companies so that the essence of

accounting is maintained. The only changes are there that is present is in the execution of the

method, the method always remains the same. Like in the case of AASB 136, the board has

issued specific rules for non-profit and profit organisations to suit the needs of the local

companies (Bond, Govendir, & Wells, 2016). Thus, there are many ways by which the Australian

board can consider the demands and the needs of the local bodies to suit their compliances

with the accounting standards. The demands of the domestic companies must be taken into

consideration. These standards are based on the international standards but are amended as

per the domestic companies. This is the main basis of formation of the domestic standards on

basis of the international counterparts and how they affect the domestic companies is in the

hands of the forming bodies that are responsible for setting up these standards as per the

needs of the company (Birt, Muthusamy, & Bir, 2017).

8 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

Part B

Introduction

The ED 116 is issued for the recognition of the property plant and equipment of the

company. It gives basis to the relevance of fir value in accounting and measurement. As per the

AASB consideration, if the companies adopt this method for valuation of their plant property

and equipment, they will have more benefits and the overall cost will reduce. After considering

all the points that the board laid down in the matter of adoption of these policies, it can be

stated that adoption of fair value analysis is better because it is more financially viable then

recognition based on historical data. The rules have been set out for the profit and the non-

profit organisation. It is said that the in case of revaluation of any class of asset, the net

revaluation shall be recognised under the heading of revaluation surplus. It has also been laid

down that if the companies are acquiring any asset at cost the company shall recognise less

than the fair value, then the extra amount as surplus. The main point to be considered is that

the company should recognise all the fixed assets at the fair value so that the accounting

transactions and records are more viable. As a critic, if a comment is to be given on the

proposed draft of the board, it can be said that the change is very effective and will help in

improving transparency in the business, if fair value approach is followed. Previously while

recognising fixed assets and calculating depreciation, historical costs were considered which

often led to under or over valuation of the assets of the company. Moreover the propend

exposure is in line with the international standards that have been framed in this regard this

lends a uniformity to the overall transaction and the business of the company much more

9 | P a g e

Part B

Introduction

The ED 116 is issued for the recognition of the property plant and equipment of the

company. It gives basis to the relevance of fir value in accounting and measurement. As per the

AASB consideration, if the companies adopt this method for valuation of their plant property

and equipment, they will have more benefits and the overall cost will reduce. After considering

all the points that the board laid down in the matter of adoption of these policies, it can be

stated that adoption of fair value analysis is better because it is more financially viable then

recognition based on historical data. The rules have been set out for the profit and the non-

profit organisation. It is said that the in case of revaluation of any class of asset, the net

revaluation shall be recognised under the heading of revaluation surplus. It has also been laid

down that if the companies are acquiring any asset at cost the company shall recognise less

than the fair value, then the extra amount as surplus. The main point to be considered is that

the company should recognise all the fixed assets at the fair value so that the accounting

transactions and records are more viable. As a critic, if a comment is to be given on the

proposed draft of the board, it can be said that the change is very effective and will help in

improving transparency in the business, if fair value approach is followed. Previously while

recognising fixed assets and calculating depreciation, historical costs were considered which

often led to under or over valuation of the assets of the company. Moreover the propend

exposure is in line with the international standards that have been framed in this regard this

lends a uniformity to the overall transaction and the business of the company much more

9 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

viable when it comes to international terms. The disclosure policies under this standard are also

very simple, with importance given to recognition of the cost-carrying model along with the fair

value recognition. However, the same does not apply to the non-profit companies. The board

can made specific changes in the proposed standard for non-profit and profit generating

organisations of the country (Minnis & Sutherland, 2017).

Analysis

If we see closely the main points that have been stated by the board for the adoption

and modification of the new standard is that previously the revenue-based models that were

used by the companies for calculation of the net depreciation is not correct. This is because

when the revenue-based model is used, the depreciation calculated does not show reduction in

the economic benefit of the asset, because many other points are also taken into consideration.

Hence, it does not provide a very clear picture. It is thus considered that fair value approach

must be followed for recognition of the assets and the calculation of depreciation. It is a very

good step that the board has proposed specific changes, that are applicable to the profit and

the non-profit generation companies, based on their functioning (Drew & Grant, 2017).

With changes in the method of calculation and recognition of the asset, the large

number of companies over the world will also be affected. The industries like minning and

petroleum and mostly that are based on manufacturing, will be affected. As previously there

were many different methods to calculate the total csost of manufacture and record the same,

so companies who were not in this field found it difficult to analyse.These standards are

proposed keeping in view establishing uniformity between the various accounting policies and

10 | P a g e

viable when it comes to international terms. The disclosure policies under this standard are also

very simple, with importance given to recognition of the cost-carrying model along with the fair

value recognition. However, the same does not apply to the non-profit companies. The board

can made specific changes in the proposed standard for non-profit and profit generating

organisations of the country (Minnis & Sutherland, 2017).

Analysis

If we see closely the main points that have been stated by the board for the adoption

and modification of the new standard is that previously the revenue-based models that were

used by the companies for calculation of the net depreciation is not correct. This is because

when the revenue-based model is used, the depreciation calculated does not show reduction in

the economic benefit of the asset, because many other points are also taken into consideration.

Hence, it does not provide a very clear picture. It is thus considered that fair value approach

must be followed for recognition of the assets and the calculation of depreciation. It is a very

good step that the board has proposed specific changes, that are applicable to the profit and

the non-profit generation companies, based on their functioning (Drew & Grant, 2017).

With changes in the method of calculation and recognition of the asset, the large

number of companies over the world will also be affected. The industries like minning and

petroleum and mostly that are based on manufacturing, will be affected. As previously there

were many different methods to calculate the total csost of manufacture and record the same,

so companies who were not in this field found it difficult to analyse.These standards are

proposed keeping in view establishing uniformity between the various accounting policies and

10 | P a g e

11

assumptions of the countries around the world. The manufacturing sector is the biggest sector

that uses these plants and equipments for manufacture of products. Changes in the method of

depreciation and to recognise them at their fair value will affect the overall financials of the

company. Now since recognition will be at fair value, it will help in improving the overall

profitability of the company, as it will help in improving the overall transparency. Correct value

of depreciation without considering the various other factors just on the basis of the economic

value of the asset, will help in improving the overall profitability of the company, as les

depreciation will mean more profit but the companies will have to pay more taxes, this is a

drawback for the company. However, for the government it will be beneficial to adopt such

methods.

Conclusion and Recommendations

The need of a "one size fits all" approach in relation to the various other international

standards framing body is more or less important and in the long run much more viable. If the

independent board forms their won standard that is different from the international bodies, it

will not lead to uniformity between the accounting standards within different countries. If the

basis is the same, with some modification as per the requirements, it will help in inter firm and

intra firm comparison between the countries and help the companies to judge the effectiveness

and their standing in the international world. In case the need arises that, the domestic

companies are facing many issues because of the international standards or the technicalities

are too much, then the domestic board can make changes but that should be in line with the

international standards. There are many advantages of uniformity, as it will help in maintaining

11 | P a g e

assumptions of the countries around the world. The manufacturing sector is the biggest sector

that uses these plants and equipments for manufacture of products. Changes in the method of

depreciation and to recognise them at their fair value will affect the overall financials of the

company. Now since recognition will be at fair value, it will help in improving the overall

profitability of the company, as it will help in improving the overall transparency. Correct value

of depreciation without considering the various other factors just on the basis of the economic

value of the asset, will help in improving the overall profitability of the company, as les

depreciation will mean more profit but the companies will have to pay more taxes, this is a

drawback for the company. However, for the government it will be beneficial to adopt such

methods.

Conclusion and Recommendations

The need of a "one size fits all" approach in relation to the various other international

standards framing body is more or less important and in the long run much more viable. If the

independent board forms their won standard that is different from the international bodies, it

will not lead to uniformity between the accounting standards within different countries. If the

basis is the same, with some modification as per the requirements, it will help in inter firm and

intra firm comparison between the countries and help the companies to judge the effectiveness

and their standing in the international world. In case the need arises that, the domestic

companies are facing many issues because of the international standards or the technicalities

are too much, then the domestic board can make changes but that should be in line with the

international standards. There are many advantages of uniformity, as it will help in maintaining

11 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.