Conceptual Framework in Accounting: RIO TINTO and Glen Core Analysis

VerifiedAdded on 2023/03/23

|23

|5814

|70

Report

AI Summary

This report critically examines the application of the Conceptual Framework (CF) in financial reporting, focusing on two companies: RIO TINTO (Australian) and Glen Core PLC (South African). Section A reviews the history and development of the CF, addresses concerns from the Australian accounting profession and academics, and explains how RIO TINTO applies the CF in its financial statements, including recognition principles, measurement bases, and qualitative characteristics of information. Section B compares sustainability reporting guidelines with the International Integrated Reporting Framework, evaluates the strengths and limitations of conventional accounting based on the CF, discusses the applicability of theories to explain sustainability and integrated reports, and presents an index of integrated report components, assessing Glen Core PLC's disclosures against these criteria. The report concludes with a comparison of RIO TINTO's reporting practices with the index and Glen Core PLC's integrated reporting practices.

Running head: CONTEMPORARY ACCOUNTING THEORY

Contemporary Accounting Theory (Part A and B)

Student’s Name

Institution Affiliation

Date

1

Contemporary Accounting Theory (Part A and B)

Student’s Name

Institution Affiliation

Date

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CONTEMPORARY ACCOUNTING THEORY

1. Executive Summary

The main rationale behind the creation of the Conceptual Framework in the

accounting sector is the aim to identify fundamental concerns; which are relevant when

evaluating financial statements. As such, the framework enables the firm’s managers to

evaluate their financial health hence assuring the company’s profitability. In that regard, this

paper will critically consider applying the framework on an Australian company: RIO

TINTO, which further explains, in section A, how the selected company applies this

framework when selecting financial statements, key concerns and events. In section B, a

comparison of the sustainability reporting and the international integration reporting

framework will be evaluated. Moreover, this segment includes an evaluation of the strengths

and limitations of financial statements considering the conceptual framework. To critically

evaluate the rationale intended by the section B, a South African Country named Glen Core

PLC will be used, based on a provided index of components available in an integrated report.

2

1. Executive Summary

The main rationale behind the creation of the Conceptual Framework in the

accounting sector is the aim to identify fundamental concerns; which are relevant when

evaluating financial statements. As such, the framework enables the firm’s managers to

evaluate their financial health hence assuring the company’s profitability. In that regard, this

paper will critically consider applying the framework on an Australian company: RIO

TINTO, which further explains, in section A, how the selected company applies this

framework when selecting financial statements, key concerns and events. In section B, a

comparison of the sustainability reporting and the international integration reporting

framework will be evaluated. Moreover, this segment includes an evaluation of the strengths

and limitations of financial statements considering the conceptual framework. To critically

evaluate the rationale intended by the section B, a South African Country named Glen Core

PLC will be used, based on a provided index of components available in an integrated report.

2

CONTEMPORARY ACCOUNTING THEORY

Table of Contents

1. Executive Summary.......................................................................................................................2

2. Introduction...................................................................................................................................4

3. Part A.............................................................................................................................................4

a) Review of the history and development of the Conceptual Framework for Financial Reporting

4

b) Explanation of Australian accounting profession’s concerns regarding Conceptual Framework

5

c) Discussion of academic’s concerns about the quality (potential benefits and limitations) of

the Conceptual Framework...............................................................................................................6

d) Explanation of how the conceptual framework has been applied by the selected Australian

Company...........................................................................................................................................7

i. How many statements/reports have been prepared as per the Conceptual Framework and

what are their major components...................................................................................................7

ii. Which recognition principles and measurement bases have been applied for revenue, assets

and liabilities.................................................................................................................................9

iii. What qualitative characteristics of information exhibit in company’s various financial

reports?........................................................................................................................................10

4. Part B...........................................................................................................................................11

a) Comparison of Sustainability Reporting Guidelines and International Integrated Reporting

Framework......................................................................................................................................11

b) Rigour (strength & limitations) of the conventional accounting, based upon the Conceptual

Framework for contents of sustainability as well as integrated reports..........................................12

c) Applicability (usefulness of limitations) of the theories to explain contents of sustainability as

well as integrated reports................................................................................................................14

d) Preparation of an index (a table or checklist) of various components (criteria) of an integrated

report, and discussion of whether and how the selected South African Company has disclosed

information against each of those components (criteria)...............................................................15

e) Comparison of Australian company’s reporting practices with the index and the integrated

reporting practices in the selected South African Company............................................................17

5. Conclusion...................................................................................................................................19

References...........................................................................................................................................20

Appendix.............................................................................................................................................23

List of Abbreviations........................................................................................................................23

3

Table of Contents

1. Executive Summary.......................................................................................................................2

2. Introduction...................................................................................................................................4

3. Part A.............................................................................................................................................4

a) Review of the history and development of the Conceptual Framework for Financial Reporting

4

b) Explanation of Australian accounting profession’s concerns regarding Conceptual Framework

5

c) Discussion of academic’s concerns about the quality (potential benefits and limitations) of

the Conceptual Framework...............................................................................................................6

d) Explanation of how the conceptual framework has been applied by the selected Australian

Company...........................................................................................................................................7

i. How many statements/reports have been prepared as per the Conceptual Framework and

what are their major components...................................................................................................7

ii. Which recognition principles and measurement bases have been applied for revenue, assets

and liabilities.................................................................................................................................9

iii. What qualitative characteristics of information exhibit in company’s various financial

reports?........................................................................................................................................10

4. Part B...........................................................................................................................................11

a) Comparison of Sustainability Reporting Guidelines and International Integrated Reporting

Framework......................................................................................................................................11

b) Rigour (strength & limitations) of the conventional accounting, based upon the Conceptual

Framework for contents of sustainability as well as integrated reports..........................................12

c) Applicability (usefulness of limitations) of the theories to explain contents of sustainability as

well as integrated reports................................................................................................................14

d) Preparation of an index (a table or checklist) of various components (criteria) of an integrated

report, and discussion of whether and how the selected South African Company has disclosed

information against each of those components (criteria)...............................................................15

e) Comparison of Australian company’s reporting practices with the index and the integrated

reporting practices in the selected South African Company............................................................17

5. Conclusion...................................................................................................................................19

References...........................................................................................................................................20

Appendix.............................................................................................................................................23

List of Abbreviations........................................................................................................................23

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CONTEMPORARY ACCOUNTING THEORY

2. Introduction

The Conceptual Framework (CF) is essential for the formulation of standardized

financial protocols that enable auditors and accountants to determine and monitor the

company’s financial statements, which is significant for evaluating the company’s

profitability. Thus, the financial statements are applicable by company’s users and the

relevant key stakeholders to fundamentally create the conceptual framework, which aid in the

purposes of evaluating the company’s finances. This paper considers approaching the thesis

on CF application on two companies: RIO TINTO and the Glen Core PLC. The International

Accounting Standards Board (IASB) plays a significant mandate in the formation of

standardize and revised financial guidelines that also play a crucial obligation to help analysts

to managing and solving financial issues. In that case, the framework enables managers to

make the necessary decisions, which are in compliance with specific protocols.

3. Part A

a) Review of the history and development of the Conceptual Framework for

Financial Reporting

According to literature review concerning the history and development of the

Conceptual Framework for financial reporting, in reference to IASB denote that there is a

standardized purpose, which contribute to the introduction of the CF for financial reporting

by businesses in United Kingdom (UK), United States (US), Australia, among other nations.

According to Ehoff (2010), the CF was formulated by the AASB dated from 1985 to 1995.

The accounting concepts considering the financial statement had been delivered before 2002,

the moment when FRC decide to implement the International Accounting Standard in

Australia (Ehoff, 2010). The accounting statements included c1, 2, 3 and 4 Romolini, Fissi &

Gori, 2017). Following the joint project in 2004, the accounting bodies agreed to include

respective key components and concerns as an interlinked project to formulate a single

4

2. Introduction

The Conceptual Framework (CF) is essential for the formulation of standardized

financial protocols that enable auditors and accountants to determine and monitor the

company’s financial statements, which is significant for evaluating the company’s

profitability. Thus, the financial statements are applicable by company’s users and the

relevant key stakeholders to fundamentally create the conceptual framework, which aid in the

purposes of evaluating the company’s finances. This paper considers approaching the thesis

on CF application on two companies: RIO TINTO and the Glen Core PLC. The International

Accounting Standards Board (IASB) plays a significant mandate in the formation of

standardize and revised financial guidelines that also play a crucial obligation to help analysts

to managing and solving financial issues. In that case, the framework enables managers to

make the necessary decisions, which are in compliance with specific protocols.

3. Part A

a) Review of the history and development of the Conceptual Framework for

Financial Reporting

According to literature review concerning the history and development of the

Conceptual Framework for financial reporting, in reference to IASB denote that there is a

standardized purpose, which contribute to the introduction of the CF for financial reporting

by businesses in United Kingdom (UK), United States (US), Australia, among other nations.

According to Ehoff (2010), the CF was formulated by the AASB dated from 1985 to 1995.

The accounting concepts considering the financial statement had been delivered before 2002,

the moment when FRC decide to implement the International Accounting Standard in

Australia (Ehoff, 2010). The accounting statements included c1, 2, 3 and 4 Romolini, Fissi &

Gori, 2017). Following the joint project in 2004, the accounting bodies agreed to include

respective key components and concerns as an interlinked project to formulate a single

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CONTEMPORARY ACCOUNTING THEORY

Conceptual Framework. This initiative as governed and established based on the original

IASB conceptual framework (Timbate & Park, 2018). All the two boards utilized the

developed framework as a foundation of their accounting standards for financial reporting.

b) Explanation of Australian accounting profession’s concerns regarding

Conceptual Framework

The introduction and implementation of the conceptual framework for financial reporting has

presented some concerns denoted by the Australian profession (Aasb.gov.au, 2019). These

profession’s concerns include:

Unpredictability concerning the standardized value measurement introduced on

assets, liabilities and revenue. This is a major concern presented by the accounting

profession in Australia concerning the conceptual framework. Moreover, the

emphasis on valuation of intangible company’s assets has also been reconsidered as a

concern by the relevant stakeholders when it comes to fair value determination

(Aasb.gov.au, 2019).

The negative implications relating to the introduction of the IASB conceptual

framework for financial reporting is another concern expressed by the Australian

accounting profession. This concern relates to the measuring and recognition of assets

and liabilities of businesses. Indeed, this is a significant concern to consider because

businesses are subjected to negative economic effects due to rapidly transforming

measurement and recognition criteria of assets, liabilities and revenue (Graymore,

2014)

The introduction and implementation of the conceptual framework for financial

reporting affect non-profit businesses in Australia, which presents another concern for

the Accounting profession. It is significant to note that the conceptual framework of

the IASB was introduced and implemented for profit organization; however, there is a

5

Conceptual Framework. This initiative as governed and established based on the original

IASB conceptual framework (Timbate & Park, 2018). All the two boards utilized the

developed framework as a foundation of their accounting standards for financial reporting.

b) Explanation of Australian accounting profession’s concerns regarding

Conceptual Framework

The introduction and implementation of the conceptual framework for financial reporting has

presented some concerns denoted by the Australian profession (Aasb.gov.au, 2019). These

profession’s concerns include:

Unpredictability concerning the standardized value measurement introduced on

assets, liabilities and revenue. This is a major concern presented by the accounting

profession in Australia concerning the conceptual framework. Moreover, the

emphasis on valuation of intangible company’s assets has also been reconsidered as a

concern by the relevant stakeholders when it comes to fair value determination

(Aasb.gov.au, 2019).

The negative implications relating to the introduction of the IASB conceptual

framework for financial reporting is another concern expressed by the Australian

accounting profession. This concern relates to the measuring and recognition of assets

and liabilities of businesses. Indeed, this is a significant concern to consider because

businesses are subjected to negative economic effects due to rapidly transforming

measurement and recognition criteria of assets, liabilities and revenue (Graymore,

2014)

The introduction and implementation of the conceptual framework for financial

reporting affect non-profit businesses in Australia, which presents another concern for

the Accounting profession. It is significant to note that the conceptual framework of

the IASB was introduced and implemented for profit organization; however, there is a

5

CONTEMPORARY ACCOUNTING THEORY

legal necessity to separate the financial guidelines for various companies in Australia

(Timbate & Park, 2018).

c) Discussion of academic’s concerns about the quality (potential benefits and

limitations) of the Conceptual Framework

The CF has potential benefits and limitations to consider as an academic concern.

Academic are concerned with accounting logic and consistency, which implies that

accounting standards established following the application of CF should be logical and

consistent (Ehoff, 2010).

Potential benefits include:

Since many nations have established CF, which is similar globally (or might have

alternatively adopted the IASC frameworks), there is the need for countries to

embrace considerable global compatibility on the basic of various accounting

standards (Prosic, 2015). In that case, academic’s concern on quality features on the

standard’s comparability and consistency over the global financial reporting (whereby

professions argues that it is relevant for the evaluation of foreign investment capitals

and flows. CF provides the global fundamentals of accounting systems. In that case,

the standard-setters are expected to be accountable for all their financial decisions

(Romolini, Fissi & Gori, 2017). In case these decisions are retrieved from key

concerns evaluated in the CF, the accounting professions expect the standards to be

clear thereby necessitating more explanation prior the implementation.

The CF establishes an appropriate methodology of communicating the fundamental

concepts based on the present financial reports. Therefore, this framework provides

the best guidance for entities to reports on particular accounting standards and

evaluation any financial concern (Crombie, 2012).

6

legal necessity to separate the financial guidelines for various companies in Australia

(Timbate & Park, 2018).

c) Discussion of academic’s concerns about the quality (potential benefits and

limitations) of the Conceptual Framework

The CF has potential benefits and limitations to consider as an academic concern.

Academic are concerned with accounting logic and consistency, which implies that

accounting standards established following the application of CF should be logical and

consistent (Ehoff, 2010).

Potential benefits include:

Since many nations have established CF, which is similar globally (or might have

alternatively adopted the IASC frameworks), there is the need for countries to

embrace considerable global compatibility on the basic of various accounting

standards (Prosic, 2015). In that case, academic’s concern on quality features on the

standard’s comparability and consistency over the global financial reporting (whereby

professions argues that it is relevant for the evaluation of foreign investment capitals

and flows. CF provides the global fundamentals of accounting systems. In that case,

the standard-setters are expected to be accountable for all their financial decisions

(Romolini, Fissi & Gori, 2017). In case these decisions are retrieved from key

concerns evaluated in the CF, the accounting professions expect the standards to be

clear thereby necessitating more explanation prior the implementation.

The CF establishes an appropriate methodology of communicating the fundamental

concepts based on the present financial reports. Therefore, this framework provides

the best guidance for entities to reports on particular accounting standards and

evaluation any financial concern (Crombie, 2012).

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CONTEMPORARY ACCOUNTING THEORY

Accounting-setters will experience minimal political pressure during the formulation

of more accounting standards since the relevant concerns like the objectives of

financial reports, criterion to recognition have been considered following the

establishment of the CF.

A portion of the limitations that have been related to conceptual frameworks of bookkeeping

include:

Conceptual frameworks are outrageous to formulate.

The enhancement of the CF is affected by the governmental actions. With this, some

accountants present the concern that CFs is more inclined to political procedures.

Linked to the limitation outlined above, whenever the CF considers involving

accounting concerns, there is always an issue of financial estimation of given assets as

argued by (Molyneux & Wilson, 2017).

The CFs considers more on financial-related matters. In that case, this framework will

consider disregarding various execution segments such as ecological and social revealing

components (Timbate & Park, 2018). Moreover, through the evaluation of financial

execution, CFs critically transits the consideration of financial analysts based on corporate

execution.

d) Explanation of how the conceptual framework has been applied by the selected

Australian Company

i. How many statements/reports have been prepared as per the Conceptual Framework

and what are their major components

7

Accounting-setters will experience minimal political pressure during the formulation

of more accounting standards since the relevant concerns like the objectives of

financial reports, criterion to recognition have been considered following the

establishment of the CF.

A portion of the limitations that have been related to conceptual frameworks of bookkeeping

include:

Conceptual frameworks are outrageous to formulate.

The enhancement of the CF is affected by the governmental actions. With this, some

accountants present the concern that CFs is more inclined to political procedures.

Linked to the limitation outlined above, whenever the CF considers involving

accounting concerns, there is always an issue of financial estimation of given assets as

argued by (Molyneux & Wilson, 2017).

The CFs considers more on financial-related matters. In that case, this framework will

consider disregarding various execution segments such as ecological and social revealing

components (Timbate & Park, 2018). Moreover, through the evaluation of financial

execution, CFs critically transits the consideration of financial analysts based on corporate

execution.

d) Explanation of how the conceptual framework has been applied by the selected

Australian Company

i. How many statements/reports have been prepared as per the Conceptual Framework

and what are their major components

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CONTEMPORARY ACCOUNTING THEORY

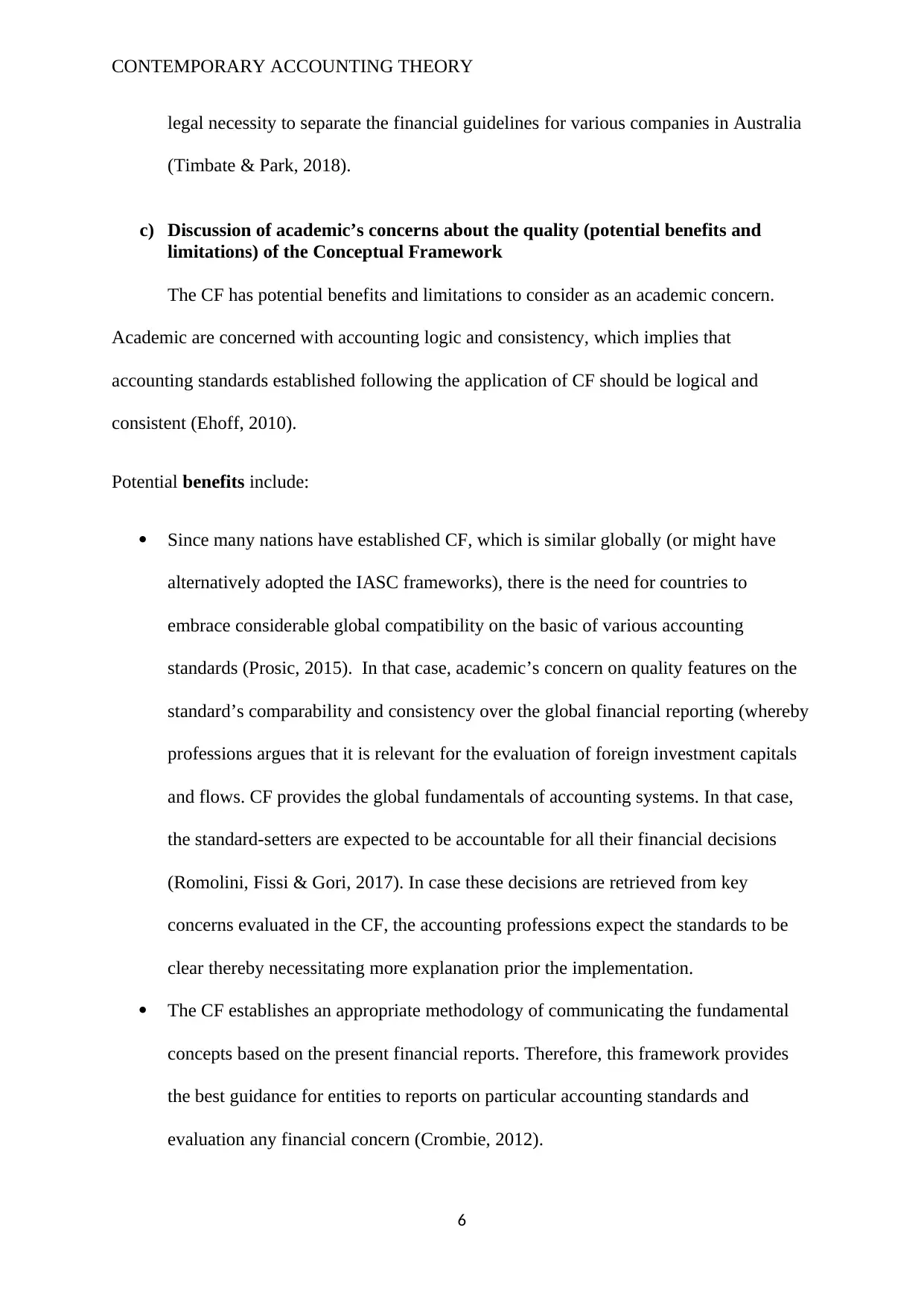

Fig. 1: Consolidate Financial Statement Position of RIO TINTO

Conferring to the Fig. 1 above, the company has prepared 11 financial reports considering

the components in financial reporting based on the CF; the components include: assets,

liabilities, and equity.

Information retrieved from the "Global home" (2019), published in 2018, signify the

obligation of RIO TINTO to prepare its consolidated accounts considering the conceptual

framework under the Australian business laws. The financial reports, especially the 2018

statements disclose the implication of adjusting the company’s consolidated revenues, assets

and liabilities as shown in page 149. The valuations, as organized under the IFRS would

8

Fig. 1: Consolidate Financial Statement Position of RIO TINTO

Conferring to the Fig. 1 above, the company has prepared 11 financial reports considering

the components in financial reporting based on the CF; the components include: assets,

liabilities, and equity.

Information retrieved from the "Global home" (2019), published in 2018, signify the

obligation of RIO TINTO to prepare its consolidated accounts considering the conceptual

framework under the Australian business laws. The financial reports, especially the 2018

statements disclose the implication of adjusting the company’s consolidated revenues, assets

and liabilities as shown in page 149. The valuations, as organized under the IFRS would

8

CONTEMPORARY ACCOUNTING THEORY

necessitate the IFRS version applied in Australia, denoted as the Australian Accounting

Standard (AAS) (Carnevale & Mazzuca, 2012).

ii. Which recognition principles and measurement bases have been applied for revenue,

assets and liabilities

The recognition principle and measurement for assets, liabilities and revenue is based on

a criterion that focusses on recognizing if the benefits of sale or sure are likely (Hodge,

Rajgopal & Shevlin, 2009).

Assets: The RIO TINTO recognizes its financial assets by evaluating them into

categories. Thus, the assets are now measured at a fair valuation through

comprehensive income Fair Value through Other Comprehensive Income (FVOCI),

including the one help at an amortised cost. The recognition principle and

measurement for this case depends on the company’s business model that signifies the

management of contractual agreements and financial assets of cash flows. The

management obligation controls the categorization of financial assets upon

recognition. As indicated in Note 30, the company clearly included the relevant

financial risk management frameworks following the recognition of the financial

statements.

Liabilities: All the RIO TINTO’s financial liabilities and borrowings, which include

the trade payables, are recognized based on the principle of fair value and overall

amount of transaction recorded. These valuations are subsequently determined at an

amortized cost. The company also participates in supply chain financial management,

which enables vendors to elect to obtain payments from banks through factoring

receivables from the company. This form of arrangement does not modify the

agreement of initial liability, which imply that financial liabilities from the supply

chain can progressively be recognized under the categorization of trade payables.

9

necessitate the IFRS version applied in Australia, denoted as the Australian Accounting

Standard (AAS) (Carnevale & Mazzuca, 2012).

ii. Which recognition principles and measurement bases have been applied for revenue,

assets and liabilities

The recognition principle and measurement for assets, liabilities and revenue is based on

a criterion that focusses on recognizing if the benefits of sale or sure are likely (Hodge,

Rajgopal & Shevlin, 2009).

Assets: The RIO TINTO recognizes its financial assets by evaluating them into

categories. Thus, the assets are now measured at a fair valuation through

comprehensive income Fair Value through Other Comprehensive Income (FVOCI),

including the one help at an amortised cost. The recognition principle and

measurement for this case depends on the company’s business model that signifies the

management of contractual agreements and financial assets of cash flows. The

management obligation controls the categorization of financial assets upon

recognition. As indicated in Note 30, the company clearly included the relevant

financial risk management frameworks following the recognition of the financial

statements.

Liabilities: All the RIO TINTO’s financial liabilities and borrowings, which include

the trade payables, are recognized based on the principle of fair value and overall

amount of transaction recorded. These valuations are subsequently determined at an

amortized cost. The company also participates in supply chain financial management,

which enables vendors to elect to obtain payments from banks through factoring

receivables from the company. This form of arrangement does not modify the

agreement of initial liability, which imply that financial liabilities from the supply

chain can progressively be recognized under the categorization of trade payables.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CONTEMPORARY ACCOUNTING THEORY

Revenue: The RIO TINTO recognizes its revenue connected to the transfers of good

and services whenever the products pass to the clients. The valuation of these

revenues denoted reflect the deliberation to which the company is, including its state

it desires to entitle its exchange of products. Revenues are also recognizes under

individual sales whenever control is assigned to the clients. In most cases, the sales

revenues and control passes are recognizes when the goods and services are delivered

to client’s premises.

iii. What qualitative characteristics of information exhibit in company’s various financial

reports?

The qualitative characteristics of information exhibited in company’s various financial

reports include:

Understandability: The RIO TINTO presents its financial statements, which are

readily understandable by its users. The company also ensured to clearly present its

data, including additional information supported by past financial reports and

reference documentation, which aid in clarification.

Relevance: According to Crombie (2012), financial information must be relevant to

users especially when it significantly impact the financial decision of the company’s

users. In that case, the RIO TINTO ensures to report on particular relevant financial

data, or information whose misstatement and omission might have a significant

impact on economic planning of users.

Reliability: Financial information has to be free from bias and material errors. In that

case, the company ensures that the data released is not misleading and faithfully

presented of its financial statements and transactions. The valuation of statements for

this case ensures that information consider underlying events, uncertainties and

estimates in appropriate disclosure.

10

Revenue: The RIO TINTO recognizes its revenue connected to the transfers of good

and services whenever the products pass to the clients. The valuation of these

revenues denoted reflect the deliberation to which the company is, including its state

it desires to entitle its exchange of products. Revenues are also recognizes under

individual sales whenever control is assigned to the clients. In most cases, the sales

revenues and control passes are recognizes when the goods and services are delivered

to client’s premises.

iii. What qualitative characteristics of information exhibit in company’s various financial

reports?

The qualitative characteristics of information exhibited in company’s various financial

reports include:

Understandability: The RIO TINTO presents its financial statements, which are

readily understandable by its users. The company also ensured to clearly present its

data, including additional information supported by past financial reports and

reference documentation, which aid in clarification.

Relevance: According to Crombie (2012), financial information must be relevant to

users especially when it significantly impact the financial decision of the company’s

users. In that case, the RIO TINTO ensures to report on particular relevant financial

data, or information whose misstatement and omission might have a significant

impact on economic planning of users.

Reliability: Financial information has to be free from bias and material errors. In that

case, the company ensures that the data released is not misleading and faithfully

presented of its financial statements and transactions. The valuation of statements for

this case ensures that information consider underlying events, uncertainties and

estimates in appropriate disclosure.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CONTEMPORARY ACCOUNTING THEORY

Comparability: According to Alfiero, Cane, Doronzo & Esposito (2018), an entity’s

information must be comparable to financial data retrieved from other consecutive

financial periods. The RIO TINTO’s users are able to identify the performance trends

of the company since the company considers evaluating the past financial reports

when preparing new reports.

Timeliness: Financial information must be produced within the scheduled time span

(Mostyn, 2012). RIO TINTO’s disclosures are produced in time and not delayed,

since the information is relevant for users to make the necessary decisions about

profitability or sustainability.

4. Part B

a) Comparison of Sustainability Reporting Guidelines and International Integrated

Reporting Framework

There has been a significant inception of the sustainability reporting under the Global

Reporting Initiative (GRI) and the integrated reporting framework under the International

Integrated Reporting Council (IIRC), which can be evident for the aims of corporate social

responsibility of evaluating a company’s financial performance. Nonetheless, it is vital to

note that there are particular difference between the sustainability and integrated reporting as

analysed below:

Sustainability Reporting

The Sustainability Reporting Guideline presents the relevant standards, under the GRI

applicable to the help companies to enhance competitive advantage (Ceulemans, Lozano &

Alonso-Almeida, 2015). Moreover, the component of environmental sustainability in the

guideline is critically recommended for firms to apply the world today. However, this form of

reporting concentrates more on a selected segment of the entity’s status but unable to

11

Comparability: According to Alfiero, Cane, Doronzo & Esposito (2018), an entity’s

information must be comparable to financial data retrieved from other consecutive

financial periods. The RIO TINTO’s users are able to identify the performance trends

of the company since the company considers evaluating the past financial reports

when preparing new reports.

Timeliness: Financial information must be produced within the scheduled time span

(Mostyn, 2012). RIO TINTO’s disclosures are produced in time and not delayed,

since the information is relevant for users to make the necessary decisions about

profitability or sustainability.

4. Part B

a) Comparison of Sustainability Reporting Guidelines and International Integrated

Reporting Framework

There has been a significant inception of the sustainability reporting under the Global

Reporting Initiative (GRI) and the integrated reporting framework under the International

Integrated Reporting Council (IIRC), which can be evident for the aims of corporate social

responsibility of evaluating a company’s financial performance. Nonetheless, it is vital to

note that there are particular difference between the sustainability and integrated reporting as

analysed below:

Sustainability Reporting

The Sustainability Reporting Guideline presents the relevant standards, under the GRI

applicable to the help companies to enhance competitive advantage (Ceulemans, Lozano &

Alonso-Almeida, 2015). Moreover, the component of environmental sustainability in the

guideline is critically recommended for firms to apply the world today. However, this form of

reporting concentrates more on a selected segment of the entity’s status but unable to

11

CONTEMPORARY ACCOUNTING THEORY

indicated the specific and relevant climatic transitions and environmental factors (Crombie,

2012). Apart from that sustainability reports do not effectively indicated financial information

relevant for evaluating the opportunities and risks of an entity.

International Integrated Reporting

On the other hand, International Integrated Reporting Framework, under the IIRC,

improves the corporation’s reputation; thus, the profitability of the firm can be evaluated

based on global norms and laws (Messner, 2010). The reporting necessitates investors to

build the relationship with both the accounting and non-accounting data analysts to be able to

effectively evaluate potential risks. Numerous organizations have energetically begun to get

readily integrated reports in different configurations and each report has been shaped as per

the requirements of business properties. Moreover, integrated announcing standards and rules

have been distributed by the Worldwide Integrated Detailing Board, so as to give direction to

report evaluators (Soyka, 2013). With the expanding significance and spread of integrated

detailing, banters about the advantages and issues experienced in the readiness expanded. In

this investigation, the followings are clarified: the terms of monetary announcing,

sustainability analysis, and accounting detailing; the development of these terms; advantages

of integrated revealing and issues that might be experienced while readiness; and the

connection between budgetary announcing and integrated detailing.

b) Rigour (strength & limitations) of the conventional accounting, based upon the

Conceptual Framework for contents of sustainability as well as integrated

reports

Strengths

The Convectional Accounting is a significant tool that is applicable in the management of

businesses today (Graymore, 2014). The conventional accounting, centred on the CF provides

12

indicated the specific and relevant climatic transitions and environmental factors (Crombie,

2012). Apart from that sustainability reports do not effectively indicated financial information

relevant for evaluating the opportunities and risks of an entity.

International Integrated Reporting

On the other hand, International Integrated Reporting Framework, under the IIRC,

improves the corporation’s reputation; thus, the profitability of the firm can be evaluated

based on global norms and laws (Messner, 2010). The reporting necessitates investors to

build the relationship with both the accounting and non-accounting data analysts to be able to

effectively evaluate potential risks. Numerous organizations have energetically begun to get

readily integrated reports in different configurations and each report has been shaped as per

the requirements of business properties. Moreover, integrated announcing standards and rules

have been distributed by the Worldwide Integrated Detailing Board, so as to give direction to

report evaluators (Soyka, 2013). With the expanding significance and spread of integrated

detailing, banters about the advantages and issues experienced in the readiness expanded. In

this investigation, the followings are clarified: the terms of monetary announcing,

sustainability analysis, and accounting detailing; the development of these terms; advantages

of integrated revealing and issues that might be experienced while readiness; and the

connection between budgetary announcing and integrated detailing.

b) Rigour (strength & limitations) of the conventional accounting, based upon the

Conceptual Framework for contents of sustainability as well as integrated

reports

Strengths

The Convectional Accounting is a significant tool that is applicable in the management of

businesses today (Graymore, 2014). The conventional accounting, centred on the CF provides

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 23

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.