Accounting Theory and Current Issues Tutorial Question Assignment

VerifiedAdded on 2023/01/11

|11

|1935

|20

Homework Assignment

AI Summary

This assignment provides a comprehensive analysis of accounting theory and current issues, addressing key topics through tutorial questions. It begins by examining relevance and faithful representation in financial reporting, providing examples where information is relevant but not faithfully represented, not relevant but faithfully represented, and relevant and faithfully represented. The assignment then delves into the social contract and its relationship with legitimacy, exploring how companies use disclosure policies. Further, the assignment covers depreciation calculations, goodwill impairment entries, and lease accounting, including implicit interest rate calculations and journal entries for both the lessee and lessor. The document includes worked examples and journal entries for each concept, providing a thorough understanding of the topics covered.

Accounting Theory & Current Issues Tutorial Question Assignment

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION.......................................................................................................................................3

MAIN BODY..............................................................................................................................................3

Week 1....................................................................................................................................................3

Week 2....................................................................................................................................................4

Week 3....................................................................................................................................................5

Week 4....................................................................................................................................................6

Week 5....................................................................................................................................................7

CONCLUSION.........................................................................................................................................10

REFERENCES..........................................................................................................................................11

INTRODUCTION.......................................................................................................................................3

MAIN BODY..............................................................................................................................................3

Week 1....................................................................................................................................................3

Week 2....................................................................................................................................................4

Week 3....................................................................................................................................................5

Week 4....................................................................................................................................................6

Week 5....................................................................................................................................................7

CONCLUSION.........................................................................................................................................10

REFERENCES..........................................................................................................................................11

INTRODUCTION

An accounting philosophy is a term used to analyze financial statements through

inference, methodologies and structure as well as how the concepts of financial management are

implemented in the accounting industry (Hoque, 2018). In principle, theory of accounting serves

as a basis for comprehending financial statements and how firms can stream their income reports

with effective methods. The project report is based on various tasks that cover detailed

information about different aspects. In the first part of report information about different

examples is given in which information is relevant but not faithfully presented. While second

part of report, includes information about social contract and ways in which organization use

disclosure policy to maintain legitimacy. As well as third part of report covers information

regards to journal entries of depreciation. In the further part of report, journal entries have been

done about goodwill and in the end part of report information about interest rate implicit and

journal entries is done.

MAIN BODY

Week 1

Relevance is the key attribute of financial reporting that allows the details to be important for

decision-making (Adhikari and Gårseth-Nesbakk, 2016). Faithful portraying a corporation with a

real and equal view without any secret motive is financial reporting.

(a) Provide one example where information is relevant but not faithfully represented.

Example- Surplus stock in a trading plan where the cost value is of $10000. But it is shown

as $15000.

Explanation- In this scenario, the recording of the inventory is important in essence, but

displaying that at the time is not the real inventory expense.

(b) Provide one example where information is not relevant but is faithfully represented.

Example- the Company’s method of depreciation is vital to the organization, as it can

lead to cost and tax change.

An accounting philosophy is a term used to analyze financial statements through

inference, methodologies and structure as well as how the concepts of financial management are

implemented in the accounting industry (Hoque, 2018). In principle, theory of accounting serves

as a basis for comprehending financial statements and how firms can stream their income reports

with effective methods. The project report is based on various tasks that cover detailed

information about different aspects. In the first part of report information about different

examples is given in which information is relevant but not faithfully presented. While second

part of report, includes information about social contract and ways in which organization use

disclosure policy to maintain legitimacy. As well as third part of report covers information

regards to journal entries of depreciation. In the further part of report, journal entries have been

done about goodwill and in the end part of report information about interest rate implicit and

journal entries is done.

MAIN BODY

Week 1

Relevance is the key attribute of financial reporting that allows the details to be important for

decision-making (Adhikari and Gårseth-Nesbakk, 2016). Faithful portraying a corporation with a

real and equal view without any secret motive is financial reporting.

(a) Provide one example where information is relevant but not faithfully represented.

Example- Surplus stock in a trading plan where the cost value is of $10000. But it is shown

as $15000.

Explanation- In this scenario, the recording of the inventory is important in essence, but

displaying that at the time is not the real inventory expense.

(b) Provide one example where information is not relevant but is faithfully represented.

Example- the Company’s method of depreciation is vital to the organization, as it can

lead to cost and tax change.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Explanation- However that may contribute to a lack of faithful interpretation of the facts,

without discussing the system for depreciation and the explanations for the use of one

process over the other.

(c) Provide one example where information is relevant and faithfully represented.

Example- In the case when lower part of debt that is long term debt is presented as

current liability of $25.

Explanation- Herein, value of $25 needs to be considered as long term debt but it is

presented in the form of current liability. Thus, this can be stated that information is

relevant to business and aspect because debt is considered as short term debt. But it is

presented in wrong manner. So this is that example where information is relevant and

faithfully represented.

Week 2

(a) What is social contract and how it relates with legitimacy?

The legitimacy of companies relates to tacit and clear society's perceptions as to

how corporations will behave to guarantee their continued existence. The theory of social

contract is that all businesses are subject to an unwritten arrangement with the entire

country, whereby the corporation may do business, if its activities support society

(Merkl-Davies and Brennan, 2017). In other words, a social contract is a two-party shared

arrangement. Social contracts embody corporate expectations, particularly from a social

point of view. The corporate social contract theory claims that both firms are expected to

enhance the position of shareholders. To accomplish so, corporations must maintain an

eye on the needs of workers without violating the law in a specific community. For

business, social contract ideas are drawn from conventional contract structures.

without discussing the system for depreciation and the explanations for the use of one

process over the other.

(c) Provide one example where information is relevant and faithfully represented.

Example- In the case when lower part of debt that is long term debt is presented as

current liability of $25.

Explanation- Herein, value of $25 needs to be considered as long term debt but it is

presented in the form of current liability. Thus, this can be stated that information is

relevant to business and aspect because debt is considered as short term debt. But it is

presented in wrong manner. So this is that example where information is relevant and

faithfully represented.

Week 2

(a) What is social contract and how it relates with legitimacy?

The legitimacy of companies relates to tacit and clear society's perceptions as to

how corporations will behave to guarantee their continued existence. The theory of social

contract is that all businesses are subject to an unwritten arrangement with the entire

country, whereby the corporation may do business, if its activities support society

(Merkl-Davies and Brennan, 2017). In other words, a social contract is a two-party shared

arrangement. Social contracts embody corporate expectations, particularly from a social

point of view. The corporate social contract theory claims that both firms are expected to

enhance the position of shareholders. To accomplish so, corporations must maintain an

eye on the needs of workers without violating the law in a specific community. For

business, social contract ideas are drawn from conventional contract structures.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The theory of legitimacy seeks to explain the actions of the company in its social

responsibility policies. The central principle of the philosophy of legitimacy is to

conform to the social contract of an organization that requires its goals to be

acknowledged.

There is a relation between social contract and legitimacy. This is so because by help of

legitimacy, there will be scope that social contract will be fulfilled. Due to legitimacy, it

becomes easier for both parties to fulfill their own responsibilities. In the absence of link

between these two aspects, this may be difficult for companies to consider their liabilities

towards different parties.

(b) Ways in which companies use corporate disclosure policy.

Corporate disclosure may be described as "conveying corporate results and

governance to third party owners" through entities inside public institutions to citizens

beyond the key objective of corporate disclosure (Walker, 2016). The income and living

of data on the Company's Web site alone is not necessary. Non-public knowledge deemed

content. Both personal knowledge reports must be treated. Pursuant to this Policy until

the website launch. The corporate disclosure policy can be used by organizations in such

ways that are as follows:

The CEO or Chief Financial Officer may appoint from time to time. Other

directors, officers, employees, contractors or others to speak on behalf of the

Commission. Business as backups or to address particular questions. Speakers are

limited to provision of information from freely accessible knowledge

automatically transmitted or as the Chief Executive Officer or the Chief Financial

Officer is not specifically allowed.

As well as corporate disclosure policy may be used by companies for providing

information about their key aims and objectives.

responsibility policies. The central principle of the philosophy of legitimacy is to

conform to the social contract of an organization that requires its goals to be

acknowledged.

There is a relation between social contract and legitimacy. This is so because by help of

legitimacy, there will be scope that social contract will be fulfilled. Due to legitimacy, it

becomes easier for both parties to fulfill their own responsibilities. In the absence of link

between these two aspects, this may be difficult for companies to consider their liabilities

towards different parties.

(b) Ways in which companies use corporate disclosure policy.

Corporate disclosure may be described as "conveying corporate results and

governance to third party owners" through entities inside public institutions to citizens

beyond the key objective of corporate disclosure (Walker, 2016). The income and living

of data on the Company's Web site alone is not necessary. Non-public knowledge deemed

content. Both personal knowledge reports must be treated. Pursuant to this Policy until

the website launch. The corporate disclosure policy can be used by organizations in such

ways that are as follows:

The CEO or Chief Financial Officer may appoint from time to time. Other

directors, officers, employees, contractors or others to speak on behalf of the

Commission. Business as backups or to address particular questions. Speakers are

limited to provision of information from freely accessible knowledge

automatically transmitted or as the Chief Executive Officer or the Chief Financial

Officer is not specifically allowed.

As well as corporate disclosure policy may be used by companies for providing

information about their key aims and objectives.

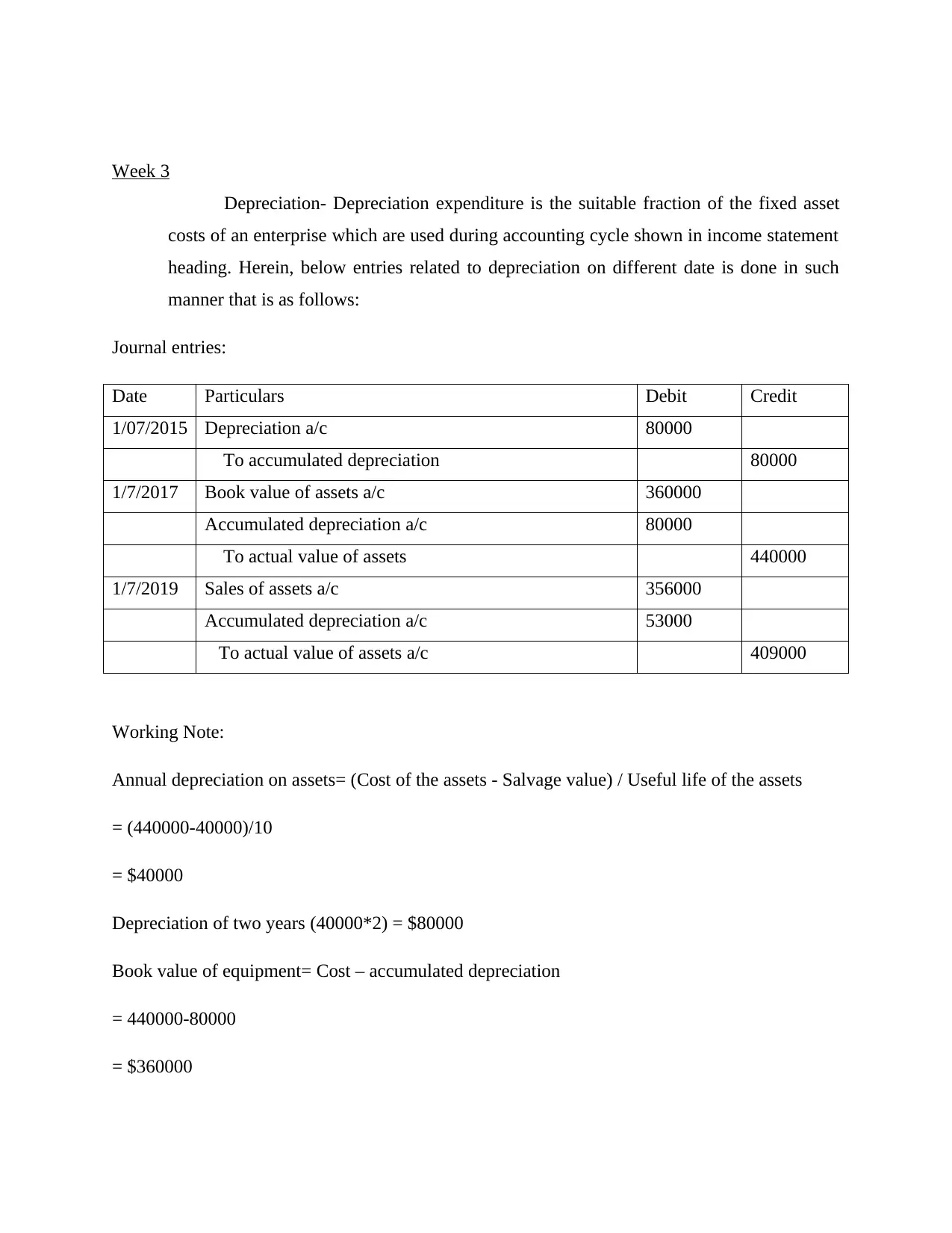

Week 3

Depreciation- Depreciation expenditure is the suitable fraction of the fixed asset

costs of an enterprise which are used during accounting cycle shown in income statement

heading. Herein, below entries related to depreciation on different date is done in such

manner that is as follows:

Journal entries:

Date Particulars Debit Credit

1/07/2015 Depreciation a/c 80000

To accumulated depreciation 80000

1/7/2017 Book value of assets a/c 360000

Accumulated depreciation a/c 80000

To actual value of assets 440000

1/7/2019 Sales of assets a/c 356000

Accumulated depreciation a/c 53000

To actual value of assets a/c 409000

Working Note:

Annual depreciation on assets= (Cost of the assets - Salvage value) / Useful life of the assets

= (440000-40000)/10

= $40000

Depreciation of two years (40000*2) = $80000

Book value of equipment= Cost – accumulated depreciation

= 440000-80000

= $360000

Depreciation- Depreciation expenditure is the suitable fraction of the fixed asset

costs of an enterprise which are used during accounting cycle shown in income statement

heading. Herein, below entries related to depreciation on different date is done in such

manner that is as follows:

Journal entries:

Date Particulars Debit Credit

1/07/2015 Depreciation a/c 80000

To accumulated depreciation 80000

1/7/2017 Book value of assets a/c 360000

Accumulated depreciation a/c 80000

To actual value of assets 440000

1/7/2019 Sales of assets a/c 356000

Accumulated depreciation a/c 53000

To actual value of assets a/c 409000

Working Note:

Annual depreciation on assets= (Cost of the assets - Salvage value) / Useful life of the assets

= (440000-40000)/10

= $40000

Depreciation of two years (40000*2) = $80000

Book value of equipment= Cost – accumulated depreciation

= 440000-80000

= $360000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

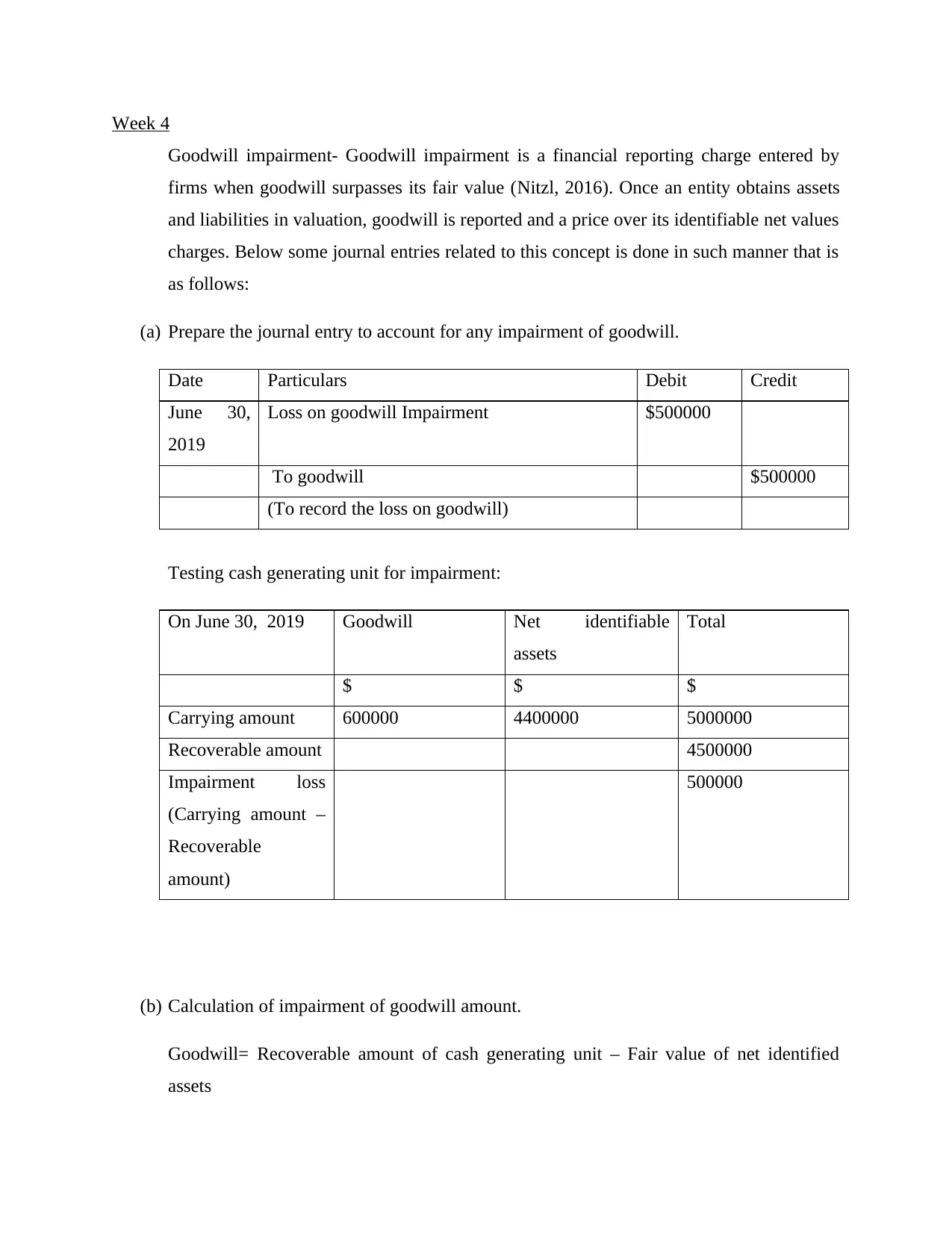

Week 4

Goodwill impairment- Goodwill impairment is a financial reporting charge entered by

firms when goodwill surpasses its fair value (Nitzl, 2016). Once an entity obtains assets

and liabilities in valuation, goodwill is reported and a price over its identifiable net values

charges. Below some journal entries related to this concept is done in such manner that is

as follows:

(a) Prepare the journal entry to account for any impairment of goodwill.

Date Particulars Debit Credit

June 30,

2019

Loss on goodwill Impairment $500000

To goodwill $500000

(To record the loss on goodwill)

Testing cash generating unit for impairment:

On June 30, 2019 Goodwill Net identifiable

assets

Total

$ $ $

Carrying amount 600000 4400000 5000000

Recoverable amount 4500000

Impairment loss

(Carrying amount –

Recoverable

amount)

500000

(b) Calculation of impairment of goodwill amount.

Goodwill= Recoverable amount of cash generating unit – Fair value of net identified

assets

Goodwill impairment- Goodwill impairment is a financial reporting charge entered by

firms when goodwill surpasses its fair value (Nitzl, 2016). Once an entity obtains assets

and liabilities in valuation, goodwill is reported and a price over its identifiable net values

charges. Below some journal entries related to this concept is done in such manner that is

as follows:

(a) Prepare the journal entry to account for any impairment of goodwill.

Date Particulars Debit Credit

June 30,

2019

Loss on goodwill Impairment $500000

To goodwill $500000

(To record the loss on goodwill)

Testing cash generating unit for impairment:

On June 30, 2019 Goodwill Net identifiable

assets

Total

$ $ $

Carrying amount 600000 4400000 5000000

Recoverable amount 4500000

Impairment loss

(Carrying amount –

Recoverable

amount)

500000

(b) Calculation of impairment of goodwill amount.

Goodwill= Recoverable amount of cash generating unit – Fair value of net identified

assets

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

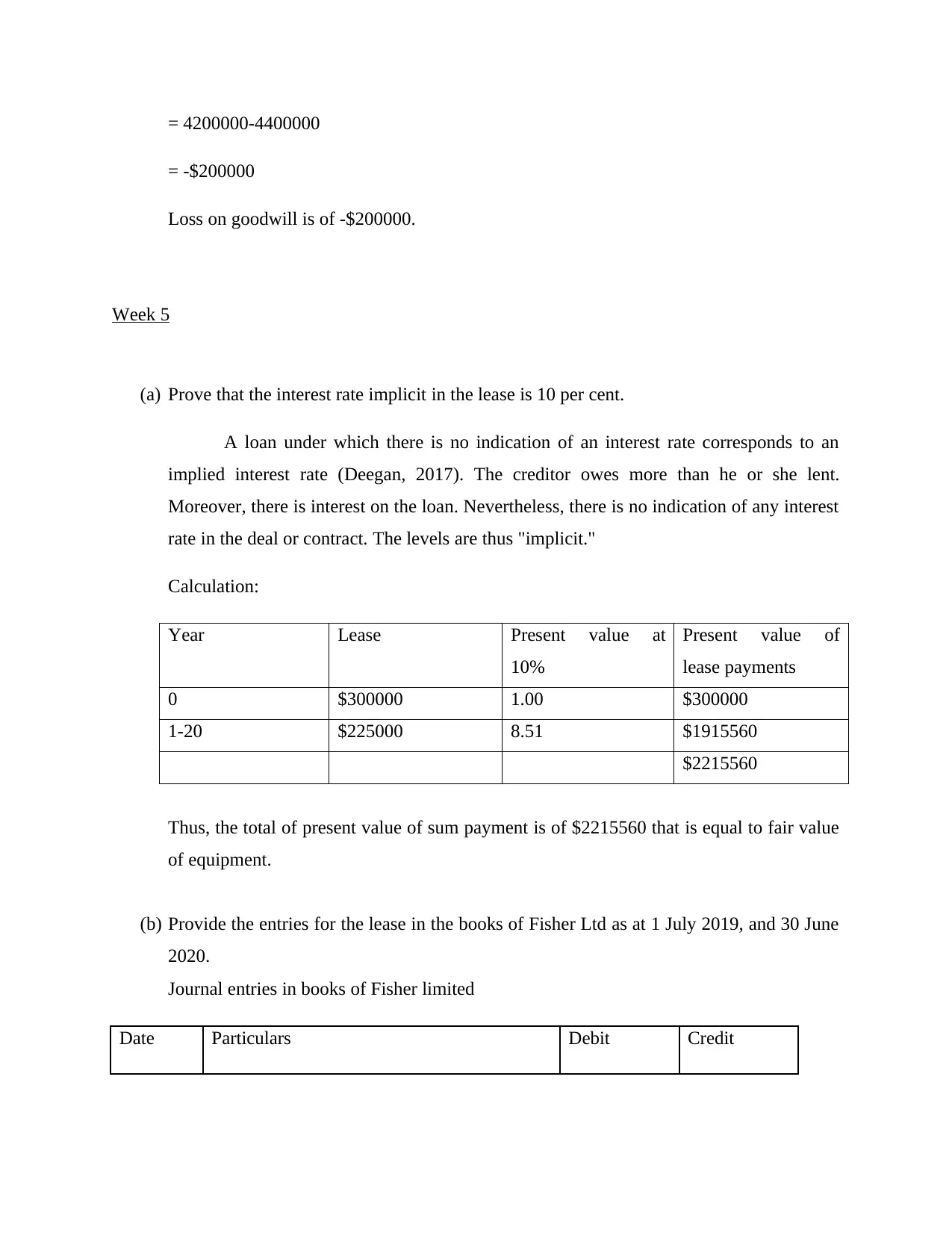

= 4200000-4400000

= -$200000

Loss on goodwill is of -$200000.

Week 5

(a) Prove that the interest rate implicit in the lease is 10 per cent.

A loan under which there is no indication of an interest rate corresponds to an

implied interest rate (Deegan, 2017). The creditor owes more than he or she lent.

Moreover, there is interest on the loan. Nevertheless, there is no indication of any interest

rate in the deal or contract. The levels are thus "implicit."

Calculation:

Year Lease Present value at

10%

Present value of

lease payments

0 $300000 1.00 $300000

1-20 $225000 8.51 $1915560

$2215560

Thus, the total of present value of sum payment is of $2215560 that is equal to fair value

of equipment.

(b) Provide the entries for the lease in the books of Fisher Ltd as at 1 July 2019, and 30 June

2020.

Journal entries in books of Fisher limited

Date Particulars Debit Credit

= -$200000

Loss on goodwill is of -$200000.

Week 5

(a) Prove that the interest rate implicit in the lease is 10 per cent.

A loan under which there is no indication of an interest rate corresponds to an

implied interest rate (Deegan, 2017). The creditor owes more than he or she lent.

Moreover, there is interest on the loan. Nevertheless, there is no indication of any interest

rate in the deal or contract. The levels are thus "implicit."

Calculation:

Year Lease Present value at

10%

Present value of

lease payments

0 $300000 1.00 $300000

1-20 $225000 8.51 $1915560

$2215560

Thus, the total of present value of sum payment is of $2215560 that is equal to fair value

of equipment.

(b) Provide the entries for the lease in the books of Fisher Ltd as at 1 July 2019, and 30 June

2020.

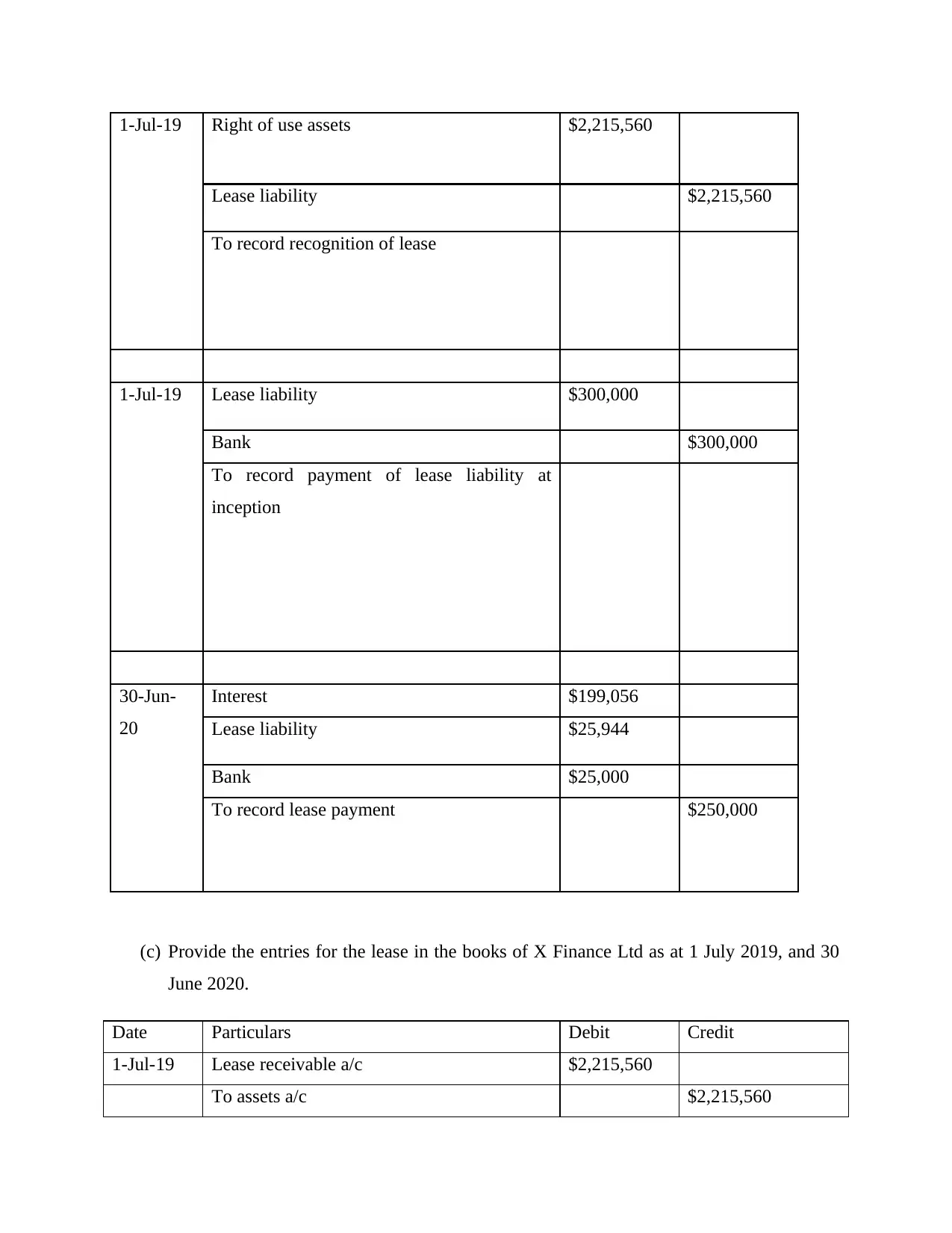

Journal entries in books of Fisher limited

Date Particulars Debit Credit

1-Jul-19 Right of use assets $2,215,560

Lease liability $2,215,560

To record recognition of lease

1-Jul-19 Lease liability $300,000

Bank $300,000

To record payment of lease liability at

inception

30-Jun-

20

Interest $199,056

Lease liability $25,944

Bank $25,000

To record lease payment $250,000

(c) Provide the entries for the lease in the books of X Finance Ltd as at 1 July 2019, and 30

June 2020.

Date Particulars Debit Credit

1-Jul-19 Lease receivable a/c $2,215,560

To assets a/c $2,215,560

Lease liability $2,215,560

To record recognition of lease

1-Jul-19 Lease liability $300,000

Bank $300,000

To record payment of lease liability at

inception

30-Jun-

20

Interest $199,056

Lease liability $25,944

Bank $25,000

To record lease payment $250,000

(c) Provide the entries for the lease in the books of X Finance Ltd as at 1 July 2019, and 30

June 2020.

Date Particulars Debit Credit

1-Jul-19 Lease receivable a/c $2,215,560

To assets a/c $2,215,560

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

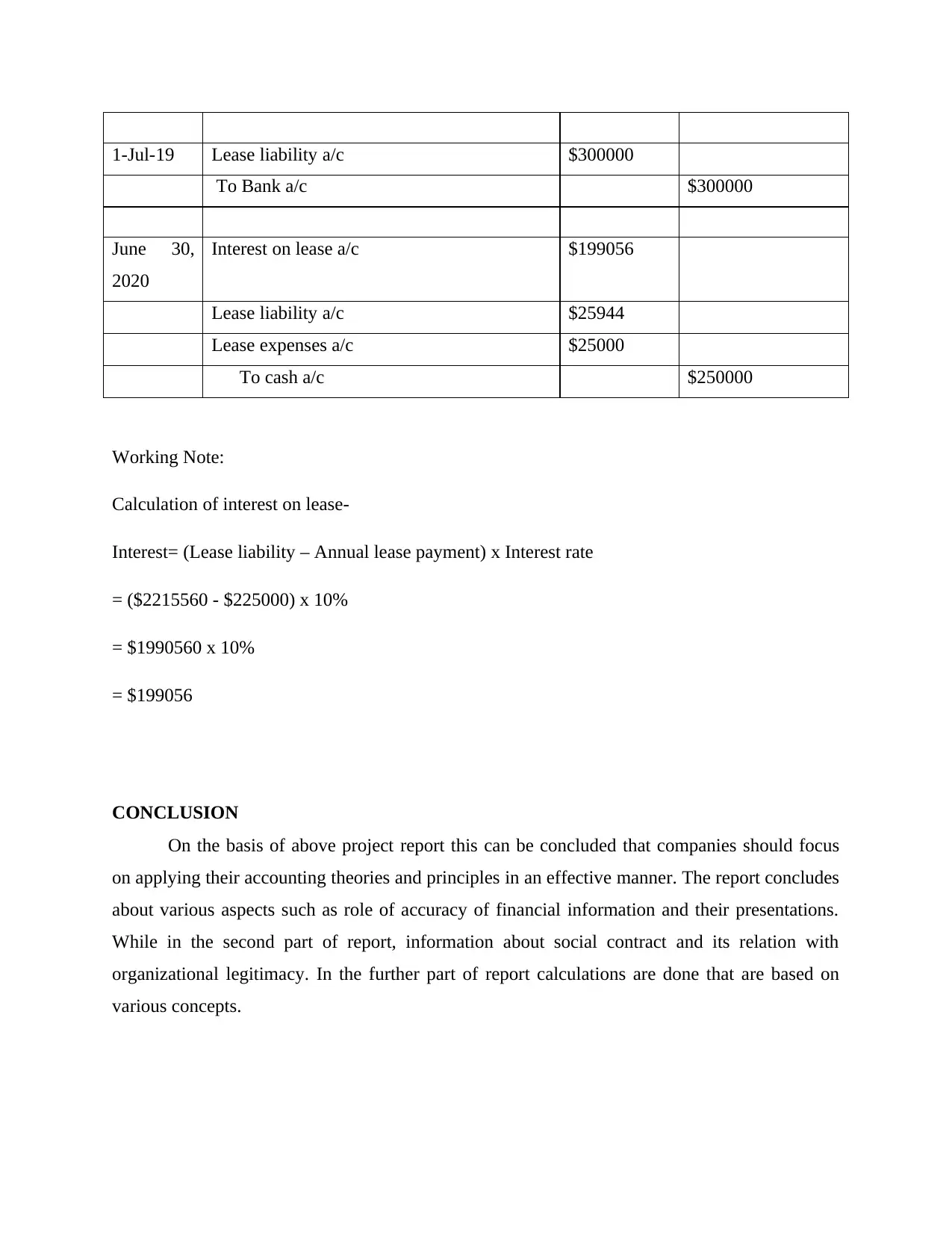

1-Jul-19 Lease liability a/c $300000

To Bank a/c $300000

June 30,

2020

Interest on lease a/c $199056

Lease liability a/c $25944

Lease expenses a/c $25000

To cash a/c $250000

Working Note:

Calculation of interest on lease-

Interest= (Lease liability – Annual lease payment) x Interest rate

= ($2215560 - $225000) x 10%

= $1990560 x 10%

= $199056

CONCLUSION

On the basis of above project report this can be concluded that companies should focus

on applying their accounting theories and principles in an effective manner. The report concludes

about various aspects such as role of accuracy of financial information and their presentations.

While in the second part of report, information about social contract and its relation with

organizational legitimacy. In the further part of report calculations are done that are based on

various concepts.

To Bank a/c $300000

June 30,

2020

Interest on lease a/c $199056

Lease liability a/c $25944

Lease expenses a/c $25000

To cash a/c $250000

Working Note:

Calculation of interest on lease-

Interest= (Lease liability – Annual lease payment) x Interest rate

= ($2215560 - $225000) x 10%

= $1990560 x 10%

= $199056

CONCLUSION

On the basis of above project report this can be concluded that companies should focus

on applying their accounting theories and principles in an effective manner. The report concludes

about various aspects such as role of accuracy of financial information and their presentations.

While in the second part of report, information about social contract and its relation with

organizational legitimacy. In the further part of report calculations are done that are based on

various concepts.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and journal:

Hoque, Z., 2018. Methodological issues in accounting research. Spiramus Press Ltd.

Adhikari, P. and Gårseth-Nesbakk, L., 2016, June. Implementing public sector accruals in OECD

member states: Major issues and challenges. In Accounting Forum (Vol. 40, No. 2, pp.

125-142). Taylor & Francis.

Merkl-Davies, D.M. and Brennan, N.M., 2017. A theoretical framework of external accounting

communication. Accounting, Auditing & Accountability Journal.

Walker, S.P., 2016. Revisiting the roles of accounting in society. Accounting, Organizations and

Society, 49, pp.41-50.

Deegan, C., 2017. Twenty five years of social and environmental accounting research within

Critical Perspectives of Accounting: Hits, misses and ways forward. Critical Perspectives

on Accounting, 43, pp.65-87.

Nitzl, C., 2016. The use of partial least squares structural equation modelling (PLS-SEM) in

management accounting research: Directions for future theory development. Journal of

Accounting Literature, 37, pp.19-35.

Books and journal:

Hoque, Z., 2018. Methodological issues in accounting research. Spiramus Press Ltd.

Adhikari, P. and Gårseth-Nesbakk, L., 2016, June. Implementing public sector accruals in OECD

member states: Major issues and challenges. In Accounting Forum (Vol. 40, No. 2, pp.

125-142). Taylor & Francis.

Merkl-Davies, D.M. and Brennan, N.M., 2017. A theoretical framework of external accounting

communication. Accounting, Auditing & Accountability Journal.

Walker, S.P., 2016. Revisiting the roles of accounting in society. Accounting, Organizations and

Society, 49, pp.41-50.

Deegan, C., 2017. Twenty five years of social and environmental accounting research within

Critical Perspectives of Accounting: Hits, misses and ways forward. Critical Perspectives

on Accounting, 43, pp.65-87.

Nitzl, C., 2016. The use of partial least squares structural equation modelling (PLS-SEM) in

management accounting research: Directions for future theory development. Journal of

Accounting Literature, 37, pp.19-35.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.