ACC307 Accounting Theory Assignment: Fair Value and Mixed Attributes

VerifiedAdded on 2022/08/26

|16

|4046

|10

Report

AI Summary

This report addresses key concepts in accounting theory, including the differences between principle-based and rules-based accounting standards (IFRS vs. GAAP), their respective advantages and disadvantages, and a comparative analysis. The report then delves into the fair value measurement model, as defined by IFRS 13, and its application, advantages, and disadvantages. It examines relevant standards such as FASB 159 and IAS 39. Furthermore, the report analyzes the mixed-attribute financial reporting model, discussing its use, the perspectives of banking federations and the CFA Institute, and arguments for and against its implementation. The report concludes with a discussion of how these models impact financial reporting and the valuation of assets and liabilities, providing a comprehensive overview of these critical accounting topics.

Running Head: ACCOUNTING

ACCOUNTING

Name of the Student

Name of the University

Author Note

ACCOUNTING

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

ACCOUNTING

Table of Contents

Theoretical Question..................................................................................................................2

Case Study..................................................................................................................................5

Fair value measurement model..............................................................................................5

Mixed-attribute financial reporting Model.............................................................................8

References................................................................................................................................12

ACCOUNTING

Table of Contents

Theoretical Question..................................................................................................................2

Case Study..................................................................................................................................5

Fair value measurement model..............................................................................................5

Mixed-attribute financial reporting Model.............................................................................8

References................................................................................................................................12

2

ACCOUNTING

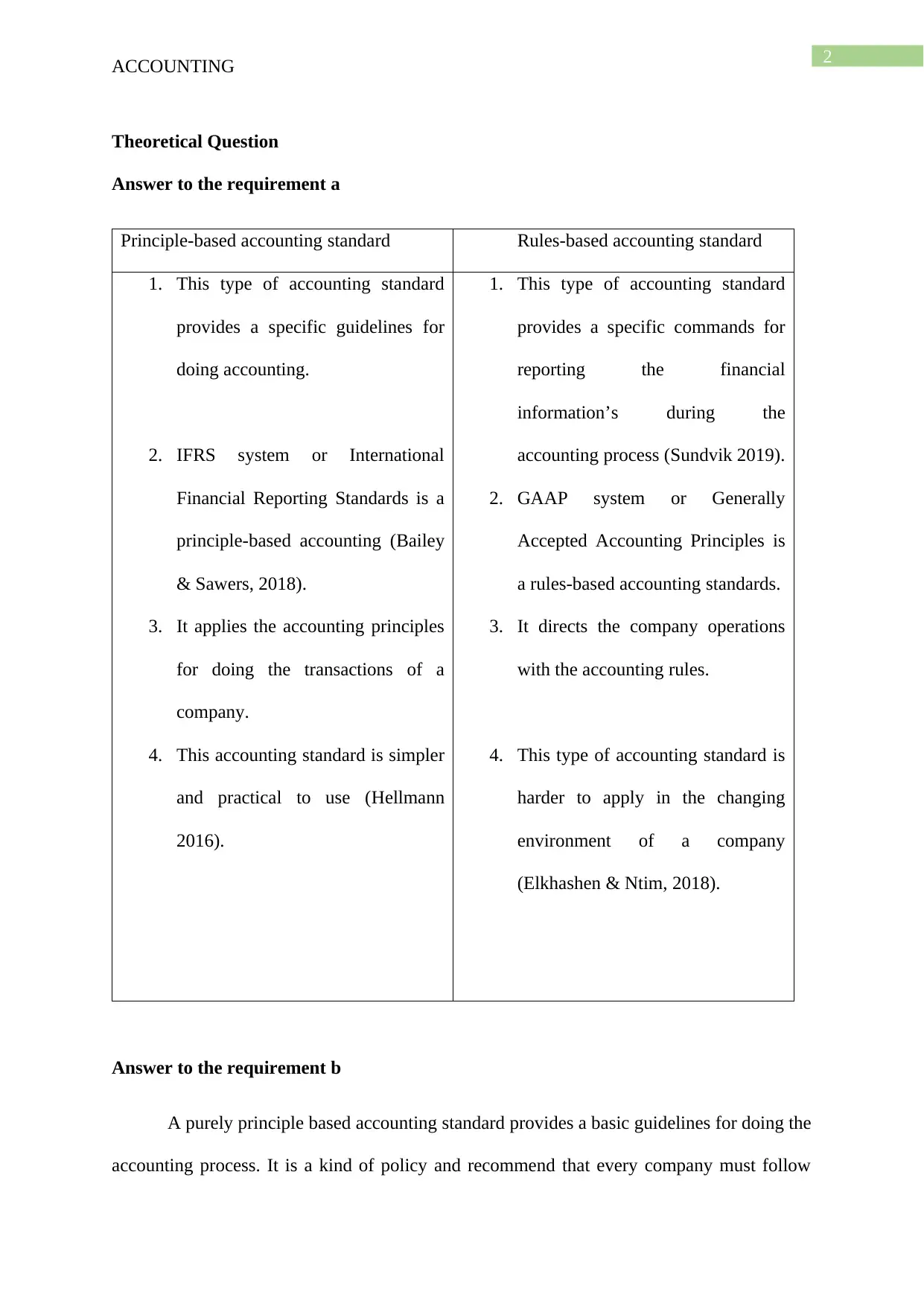

Theoretical Question

Answer to the requirement a

Principle-based accounting standard Rules-based accounting standard

1. This type of accounting standard

provides a specific guidelines for

doing accounting.

2. IFRS system or International

Financial Reporting Standards is a

principle-based accounting (Bailey

& Sawers, 2018).

3. It applies the accounting principles

for doing the transactions of a

company.

4. This accounting standard is simpler

and practical to use (Hellmann

2016).

1. This type of accounting standard

provides a specific commands for

reporting the financial

information’s during the

accounting process (Sundvik 2019).

2. GAAP system or Generally

Accepted Accounting Principles is

a rules-based accounting standards.

3. It directs the company operations

with the accounting rules.

4. This type of accounting standard is

harder to apply in the changing

environment of a company

(Elkhashen & Ntim, 2018).

Answer to the requirement b

A purely principle based accounting standard provides a basic guidelines for doing the

accounting process. It is a kind of policy and recommend that every company must follow

ACCOUNTING

Theoretical Question

Answer to the requirement a

Principle-based accounting standard Rules-based accounting standard

1. This type of accounting standard

provides a specific guidelines for

doing accounting.

2. IFRS system or International

Financial Reporting Standards is a

principle-based accounting (Bailey

& Sawers, 2018).

3. It applies the accounting principles

for doing the transactions of a

company.

4. This accounting standard is simpler

and practical to use (Hellmann

2016).

1. This type of accounting standard

provides a specific commands for

reporting the financial

information’s during the

accounting process (Sundvik 2019).

2. GAAP system or Generally

Accepted Accounting Principles is

a rules-based accounting standards.

3. It directs the company operations

with the accounting rules.

4. This type of accounting standard is

harder to apply in the changing

environment of a company

(Elkhashen & Ntim, 2018).

Answer to the requirement b

A purely principle based accounting standard provides a basic guidelines for doing the

accounting process. It is a kind of policy and recommend that every company must follow

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

ACCOUNTING

these principles. Since, IFRS is a principle based accounting system. But still it is not used by

all the countries. A nearby of 120 countries uses this accounting standard across the world.

Hence, IFRS is not purely a principle based accounting standard. GAAP or generally

Accepted Accounting Principles is a rule-based accounting standard (Penno, 2019). A pure

rule based accounting system is defined as, the company following this type of accounting

system must follow the rules and regulations and should not be deviated from the rules.

GAAP is not a pure rule based accounting system. It is also considered as principles based

because it includes basic guidelines for the accountants. These guidelines include regularity,

prudence, continuity, sincerity and good faith. If the accountant’s does not follow these rules,

then they will not pay any penalties. Therefore, it is not a pure-rule based accounting systems.

In pure-rules based accounting system the commands are needed to be followed, and

accountants will have to pay for the penalties for not following the rules. The accounting

standard forces the bookkeepers to follow the rules during reporting the financial

information. Therefore, it can be seen that, any single set of accounting standards is not

purely a principles-based or rules-based accounting standard.

Answer to requirement c

Advantages

Principles-based accounting Rules based accounting standard

1. It is very broad and practical to use.

2. This is more flexible with respect to rapid

changes in the business environment.

1. It can increase the accuracy of

the requirements.

2. It reduces the chances of

earnings management by

making a strict judgements in

the accounting.

ACCOUNTING

these principles. Since, IFRS is a principle based accounting system. But still it is not used by

all the countries. A nearby of 120 countries uses this accounting standard across the world.

Hence, IFRS is not purely a principle based accounting standard. GAAP or generally

Accepted Accounting Principles is a rule-based accounting standard (Penno, 2019). A pure

rule based accounting system is defined as, the company following this type of accounting

system must follow the rules and regulations and should not be deviated from the rules.

GAAP is not a pure rule based accounting system. It is also considered as principles based

because it includes basic guidelines for the accountants. These guidelines include regularity,

prudence, continuity, sincerity and good faith. If the accountant’s does not follow these rules,

then they will not pay any penalties. Therefore, it is not a pure-rule based accounting systems.

In pure-rules based accounting system the commands are needed to be followed, and

accountants will have to pay for the penalties for not following the rules. The accounting

standard forces the bookkeepers to follow the rules during reporting the financial

information. Therefore, it can be seen that, any single set of accounting standards is not

purely a principles-based or rules-based accounting standard.

Answer to requirement c

Advantages

Principles-based accounting Rules based accounting standard

1. It is very broad and practical to use.

2. This is more flexible with respect to rapid

changes in the business environment.

1. It can increase the accuracy of

the requirements.

2. It reduces the chances of

earnings management by

making a strict judgements in

the accounting.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

ACCOUNTING

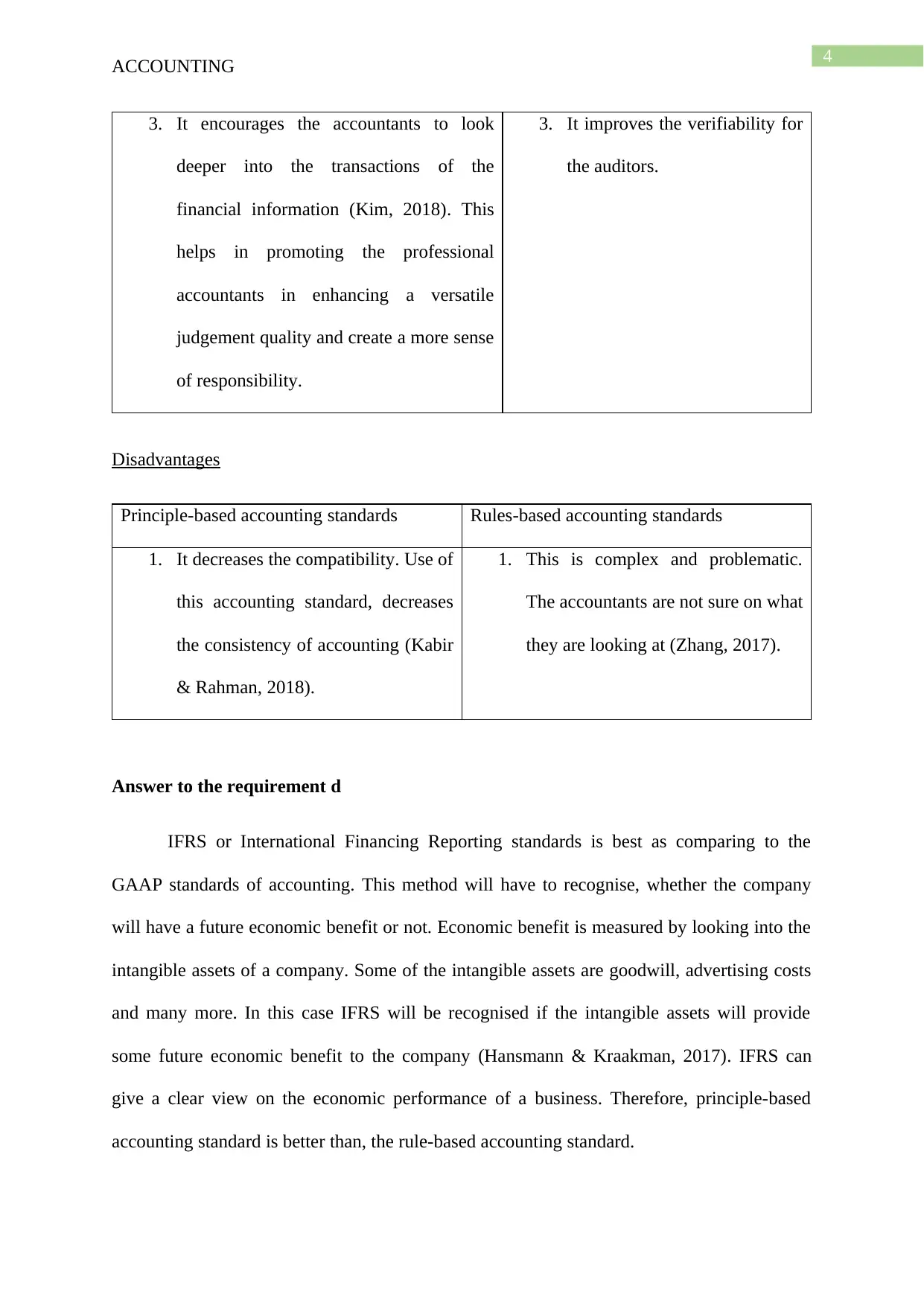

3. It encourages the accountants to look

deeper into the transactions of the

financial information (Kim, 2018). This

helps in promoting the professional

accountants in enhancing a versatile

judgement quality and create a more sense

of responsibility.

3. It improves the verifiability for

the auditors.

Disadvantages

Principle-based accounting standards Rules-based accounting standards

1. It decreases the compatibility. Use of

this accounting standard, decreases

the consistency of accounting (Kabir

& Rahman, 2018).

1. This is complex and problematic.

The accountants are not sure on what

they are looking at (Zhang, 2017).

Answer to the requirement d

IFRS or International Financing Reporting standards is best as comparing to the

GAAP standards of accounting. This method will have to recognise, whether the company

will have a future economic benefit or not. Economic benefit is measured by looking into the

intangible assets of a company. Some of the intangible assets are goodwill, advertising costs

and many more. In this case IFRS will be recognised if the intangible assets will provide

some future economic benefit to the company (Hansmann & Kraakman, 2017). IFRS can

give a clear view on the economic performance of a business. Therefore, principle-based

accounting standard is better than, the rule-based accounting standard.

ACCOUNTING

3. It encourages the accountants to look

deeper into the transactions of the

financial information (Kim, 2018). This

helps in promoting the professional

accountants in enhancing a versatile

judgement quality and create a more sense

of responsibility.

3. It improves the verifiability for

the auditors.

Disadvantages

Principle-based accounting standards Rules-based accounting standards

1. It decreases the compatibility. Use of

this accounting standard, decreases

the consistency of accounting (Kabir

& Rahman, 2018).

1. This is complex and problematic.

The accountants are not sure on what

they are looking at (Zhang, 2017).

Answer to the requirement d

IFRS or International Financing Reporting standards is best as comparing to the

GAAP standards of accounting. This method will have to recognise, whether the company

will have a future economic benefit or not. Economic benefit is measured by looking into the

intangible assets of a company. Some of the intangible assets are goodwill, advertising costs

and many more. In this case IFRS will be recognised if the intangible assets will provide

some future economic benefit to the company (Hansmann & Kraakman, 2017). IFRS can

give a clear view on the economic performance of a business. Therefore, principle-based

accounting standard is better than, the rule-based accounting standard.

5

ACCOUNTING

Case Study

In this article, the International banking federation have supported the mixed attribute

measurement model, but the CFA Institute in the opposite side, have gone against to this

model.

Fair value measurement model

IFRS 13, Fair value Measured was issued in the year 2011. In this model, all guidance

related to IAS and IFRS that is superseded. The main goal of IFRS 13 is to define the fair

value, to set out all the frameworks needed for measuring the fair value, and to disclosure the

afir value measured. It tells how to set a assets fair value, instead of when to set the fair value

(Barker & Schulte, 2017).

According to the international accounting standard setters proposed by the United

States, fair value measurement is suitable for those fiscal instruments that are involved in

trading purpose. Fair value of an asset is the selling price of the asset, agreed at the time of

contract. The fair value is a market basis measurement, not an entity based. Fair value

represents the real worth of various assets and the liabilities. A company must consider the

following things for determining the fair value.

Determine the particular asset or liability for which the fair value is to be calculated.

Only non-financial assets can be used.

Principal market is more advantage market for an asset and liability. It has greater

volumes of asset and liability. The most advantage market is that performs maximum sell and

minimum the amount of sell.

A fair value measurements model provides some guidance to the existing standards

of accounting (Zamora-Ramirez & Morales, 2018). The various standard related to fair value

measurement model are:

ACCOUNTING

Case Study

In this article, the International banking federation have supported the mixed attribute

measurement model, but the CFA Institute in the opposite side, have gone against to this

model.

Fair value measurement model

IFRS 13, Fair value Measured was issued in the year 2011. In this model, all guidance

related to IAS and IFRS that is superseded. The main goal of IFRS 13 is to define the fair

value, to set out all the frameworks needed for measuring the fair value, and to disclosure the

afir value measured. It tells how to set a assets fair value, instead of when to set the fair value

(Barker & Schulte, 2017).

According to the international accounting standard setters proposed by the United

States, fair value measurement is suitable for those fiscal instruments that are involved in

trading purpose. Fair value of an asset is the selling price of the asset, agreed at the time of

contract. The fair value is a market basis measurement, not an entity based. Fair value

represents the real worth of various assets and the liabilities. A company must consider the

following things for determining the fair value.

Determine the particular asset or liability for which the fair value is to be calculated.

Only non-financial assets can be used.

Principal market is more advantage market for an asset and liability. It has greater

volumes of asset and liability. The most advantage market is that performs maximum sell and

minimum the amount of sell.

A fair value measurements model provides some guidance to the existing standards

of accounting (Zamora-Ramirez & Morales, 2018). The various standard related to fair value

measurement model are:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

ACCOUNTING

Financial accounting standard board of FASB 159, helps to measure the fair value of

any instrument at its fair value. The main goal of this accounting standards is, to

reduce the earnings management without applying any hedging accounting practices.

FASB 159 can be applied in all type of entities both the profit and non-profit

organisations.

International Accounting Standards Board of IAS 39 is subjected to that accounting

policy, which helps to recognise and measure the financial assets, liabilities and other

financial contracts whether to purchase or sell the financial items. The principles will

help to recognise the financial instruments. According to this accounting standard, a

financial instrument will be recognised when the entity will become a party to the

contract with the financial instrument (Gebhardt, 2016). The contract is termed to be

expired, when the entity removes its liability from the balance sheet, when it transfers

the assets and the ownerships. In this accounting standard, the financial asset is

measured at its fair value. Some of the assets is also measured at its fair value.

According to FAS 17 of the financial accounting standard, the assets and liability of a

company should be measured at its fair value. This is the original price that is

received when the asset is sold during the transfer of liability. FAS 17 have classified

the assets and liabilities into three categories:

(a) The securities that are traded and quoted on daily basis.

(b) The financial instruments that have some observable prices but are not quoted on

daily basis.

(c) The instruments that donot have any observable prices and are calculated based on

certain assumptions.

IFRS 13 of fair value measurement states that a business entity uses various

assumptions for executing the fair value. One of the assumption is that, the market

ACCOUNTING

Financial accounting standard board of FASB 159, helps to measure the fair value of

any instrument at its fair value. The main goal of this accounting standards is, to

reduce the earnings management without applying any hedging accounting practices.

FASB 159 can be applied in all type of entities both the profit and non-profit

organisations.

International Accounting Standards Board of IAS 39 is subjected to that accounting

policy, which helps to recognise and measure the financial assets, liabilities and other

financial contracts whether to purchase or sell the financial items. The principles will

help to recognise the financial instruments. According to this accounting standard, a

financial instrument will be recognised when the entity will become a party to the

contract with the financial instrument (Gebhardt, 2016). The contract is termed to be

expired, when the entity removes its liability from the balance sheet, when it transfers

the assets and the ownerships. In this accounting standard, the financial asset is

measured at its fair value. Some of the assets is also measured at its fair value.

According to FAS 17 of the financial accounting standard, the assets and liability of a

company should be measured at its fair value. This is the original price that is

received when the asset is sold during the transfer of liability. FAS 17 have classified

the assets and liabilities into three categories:

(a) The securities that are traded and quoted on daily basis.

(b) The financial instruments that have some observable prices but are not quoted on

daily basis.

(c) The instruments that donot have any observable prices and are calculated based on

certain assumptions.

IFRS 13 of fair value measurement states that a business entity uses various

assumptions for executing the fair value. One of the assumption is that, the market

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

ACCOUNTING

participants must use their best monetary interest in executing the fair value of assets or

liability. The price of assets must be on the basis of orderly transactions (Sundgren, Maki &

Somoza-Lopez, 018). This type of transactions happens when there is adequate market

exposure & traded frequently in the market and the participants are not forced to do the

transactions. Orderly transactions are done, if there is highest and best use of market

transactions. The transactions must be legally permitted and financial feasible in the market.

The Principle state by IFRS 13, for applying the fair value of liabilities and own

equity instruments are:

The entity must assume the transfer as the non-settlement of the liability or the equity

instrument. This means that, the buyer of the liabilities will still have to fulfil the

obligations and the liabilities continue after the transfer. The quoted price of the asset

is used to measure the fair value of the asset (Martín, Felipe & Garcia Osma, 2018). If

there is no quoted price, then the valuation techniques like present value of costs is

used to find the exact fair value of the assets or liabilities.

The fair value of liability should reflect the risk of non-performance. It includes the

own credit risk of the business entity. No adjustment is included. The fair value of the

liability is paid on demand.

The fair value of an assets can be measured on entity based, if an entity holds the

commercial assets and liabilities with an offsetting positions. If a business entity holds the

assets and liabilities in the same foreign currencies, then the foreign exchange gain from

assets can be offset with the foreign exchange gain of liabilities or vice-versa. In such fair

value of the assets or liabilities depend on, the price to sell it on net long position or the price

to transfer the liabilities at the net short position. For this kind of fair value transactions, the

company must have a risk management strategy. So, basically, the fair value of the asset is

ACCOUNTING

participants must use their best monetary interest in executing the fair value of assets or

liability. The price of assets must be on the basis of orderly transactions (Sundgren, Maki &

Somoza-Lopez, 018). This type of transactions happens when there is adequate market

exposure & traded frequently in the market and the participants are not forced to do the

transactions. Orderly transactions are done, if there is highest and best use of market

transactions. The transactions must be legally permitted and financial feasible in the market.

The Principle state by IFRS 13, for applying the fair value of liabilities and own

equity instruments are:

The entity must assume the transfer as the non-settlement of the liability or the equity

instrument. This means that, the buyer of the liabilities will still have to fulfil the

obligations and the liabilities continue after the transfer. The quoted price of the asset

is used to measure the fair value of the asset (Martín, Felipe & Garcia Osma, 2018). If

there is no quoted price, then the valuation techniques like present value of costs is

used to find the exact fair value of the assets or liabilities.

The fair value of liability should reflect the risk of non-performance. It includes the

own credit risk of the business entity. No adjustment is included. The fair value of the

liability is paid on demand.

The fair value of an assets can be measured on entity based, if an entity holds the

commercial assets and liabilities with an offsetting positions. If a business entity holds the

assets and liabilities in the same foreign currencies, then the foreign exchange gain from

assets can be offset with the foreign exchange gain of liabilities or vice-versa. In such fair

value of the assets or liabilities depend on, the price to sell it on net long position or the price

to transfer the liabilities at the net short position. For this kind of fair value transactions, the

company must have a risk management strategy. So, basically, the fair value of the asset is

8

ACCOUNTING

the selling price of the asset during the transactions (Raji, Kazem & Mohammed, 2019). It is

also considered as the exit price of the asset during the market transactions. Therefore, an

entity must use appropriate valuation techniques for measuring the fair value of an assets.

This can be done on the basis of market approach method, cost approaches including the

depreciation and the income approach.

Advantage- The fair value measurement model, it provides an accurate estimation of

the assets and liability. The value of this assets determine the market price.

Disadvantage- The value of the assets is done on the basis of estimated fair market

prices. There can be a change in the assets and the liabilities.

But, according to the bankers, the fair value measurements is not essential for the non-

financial assets like land, vehicles, equipments and buildings.

Mixed-attribute financial reporting Model

According to the bankers, this model will be best suitable for doing a strict valuation

of the financial instruments. This model uses both the fair value and the historical cost. The

bankers have given an example of loan to understand this concept (Roychowdhury, Shroff &

Verdi, 2019). The lender provides a loan to receive interest from the borrower. In such cases,

the expected cash flows from the loan is already known during the contract. The assets and

liabilities are recorded as the amortised cost. If the fair value measurement model is

considered, then the expected cash flows from the loan amount cannot be easily predicted.

In this type of measurement basis, the valuation of assets and liabilities is done under

both the International Financial Reporting Standard and Generally Accepted Accounting

Principles. According to International Banking Federation, this model is best for the true

value representation of the entity (Kusnadi et al., 2016). This model will simplify the

complexity in valuation of the assets and liabilities of the real life companies. The main

ACCOUNTING

the selling price of the asset during the transactions (Raji, Kazem & Mohammed, 2019). It is

also considered as the exit price of the asset during the market transactions. Therefore, an

entity must use appropriate valuation techniques for measuring the fair value of an assets.

This can be done on the basis of market approach method, cost approaches including the

depreciation and the income approach.

Advantage- The fair value measurement model, it provides an accurate estimation of

the assets and liability. The value of this assets determine the market price.

Disadvantage- The value of the assets is done on the basis of estimated fair market

prices. There can be a change in the assets and the liabilities.

But, according to the bankers, the fair value measurements is not essential for the non-

financial assets like land, vehicles, equipments and buildings.

Mixed-attribute financial reporting Model

According to the bankers, this model will be best suitable for doing a strict valuation

of the financial instruments. This model uses both the fair value and the historical cost. The

bankers have given an example of loan to understand this concept (Roychowdhury, Shroff &

Verdi, 2019). The lender provides a loan to receive interest from the borrower. In such cases,

the expected cash flows from the loan is already known during the contract. The assets and

liabilities are recorded as the amortised cost. If the fair value measurement model is

considered, then the expected cash flows from the loan amount cannot be easily predicted.

In this type of measurement basis, the valuation of assets and liabilities is done under

both the International Financial Reporting Standard and Generally Accepted Accounting

Principles. According to International Banking Federation, this model is best for the true

value representation of the entity (Kusnadi et al., 2016). This model will simplify the

complexity in valuation of the assets and liabilities of the real life companies. The main

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

ACCOUNTING

objective of this model is to analyse the impact of transactions on the company’s financial

statements. This model is used to signify the reliable information of a financial statements.

Some of the information includes, assessments of risks. Timing, the expected future cash

flows.

But, according to the chairman of FASB, Robert Herz, the permanently impaired

assets should be written. The loans are always held at maturity and all the information’s

related to loans are collected during the contract (Zamora-Ramirez, & Morales-Diaz, 2018).

Many other Chief Financial Accountants have argued this model as they have created burden

to the investors (Acharya & Ryan, 2016). In this case, the investors will have to rework on

their historical cost calculations. These calculations depends on the quality of the financial

exposure by the company.

But, mixed attribute financing model helps to simplify the complexity of valuation of

an assets. In this case, the valuation of assets & liabilities is done on the basis of historical

data and current information (Call et al., 2017). This model helps the users and the

accountants, to better translate the financial information into their expected future cash flows

in the future. Acquisition cost is used for executing the historical value for the assets.

Acquisition cost is the amount that is initially paid for purchasing the assets (Davern et al.,

2018). This model uses both the GAAP and IFRS accounting standards.

GAAP- According to this accounting standard, the income tax expense of the

company, indicates the income taxes that is generated from the income of the

continuing operations. Under GAAP accounting standard, historical cost principles

for the asset valuation of a company’s balance sheet is done. Under this standard, the

value of an asset is on the basis of the capital that have been spent to buy the asset.

The past financial transactions of the financial asset is used to understand the asset’s

ACCOUNTING

objective of this model is to analyse the impact of transactions on the company’s financial

statements. This model is used to signify the reliable information of a financial statements.

Some of the information includes, assessments of risks. Timing, the expected future cash

flows.

But, according to the chairman of FASB, Robert Herz, the permanently impaired

assets should be written. The loans are always held at maturity and all the information’s

related to loans are collected during the contract (Zamora-Ramirez, & Morales-Diaz, 2018).

Many other Chief Financial Accountants have argued this model as they have created burden

to the investors (Acharya & Ryan, 2016). In this case, the investors will have to rework on

their historical cost calculations. These calculations depends on the quality of the financial

exposure by the company.

But, mixed attribute financing model helps to simplify the complexity of valuation of

an assets. In this case, the valuation of assets & liabilities is done on the basis of historical

data and current information (Call et al., 2017). This model helps the users and the

accountants, to better translate the financial information into their expected future cash flows

in the future. Acquisition cost is used for executing the historical value for the assets.

Acquisition cost is the amount that is initially paid for purchasing the assets (Davern et al.,

2018). This model uses both the GAAP and IFRS accounting standards.

GAAP- According to this accounting standard, the income tax expense of the

company, indicates the income taxes that is generated from the income of the

continuing operations. Under GAAP accounting standard, historical cost principles

for the asset valuation of a company’s balance sheet is done. Under this standard, the

value of an asset is on the basis of the capital that have been spent to buy the asset.

The past financial transactions of the financial asset is used to understand the asset’s

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

ACCOUNTING

fair value. It is a very conservative method, which is considered as reliable and easy

for the measurement. But, the main disadvantage of this type of value measurement is

that, the historical cost value may be irrelevant at certain circumstances.

IFRS- According to this accounting standard, the exceptional items should be

separately disclosed in their financial statement. This standard is followed by all the

companies across the globe. IFRS stands are known as International Financial

Reporting Standard (IFRS). The objective is to make the company’s financial

information’s, and other accounts easy understandable in all the companies present

internationally. These standards are followed by the companies doing business

internationally.

In this model, most of the financial elements are recorded at their cash flow value, on

the basis of date of their transactions. Hence, this is an historical cost of that financial

elements.

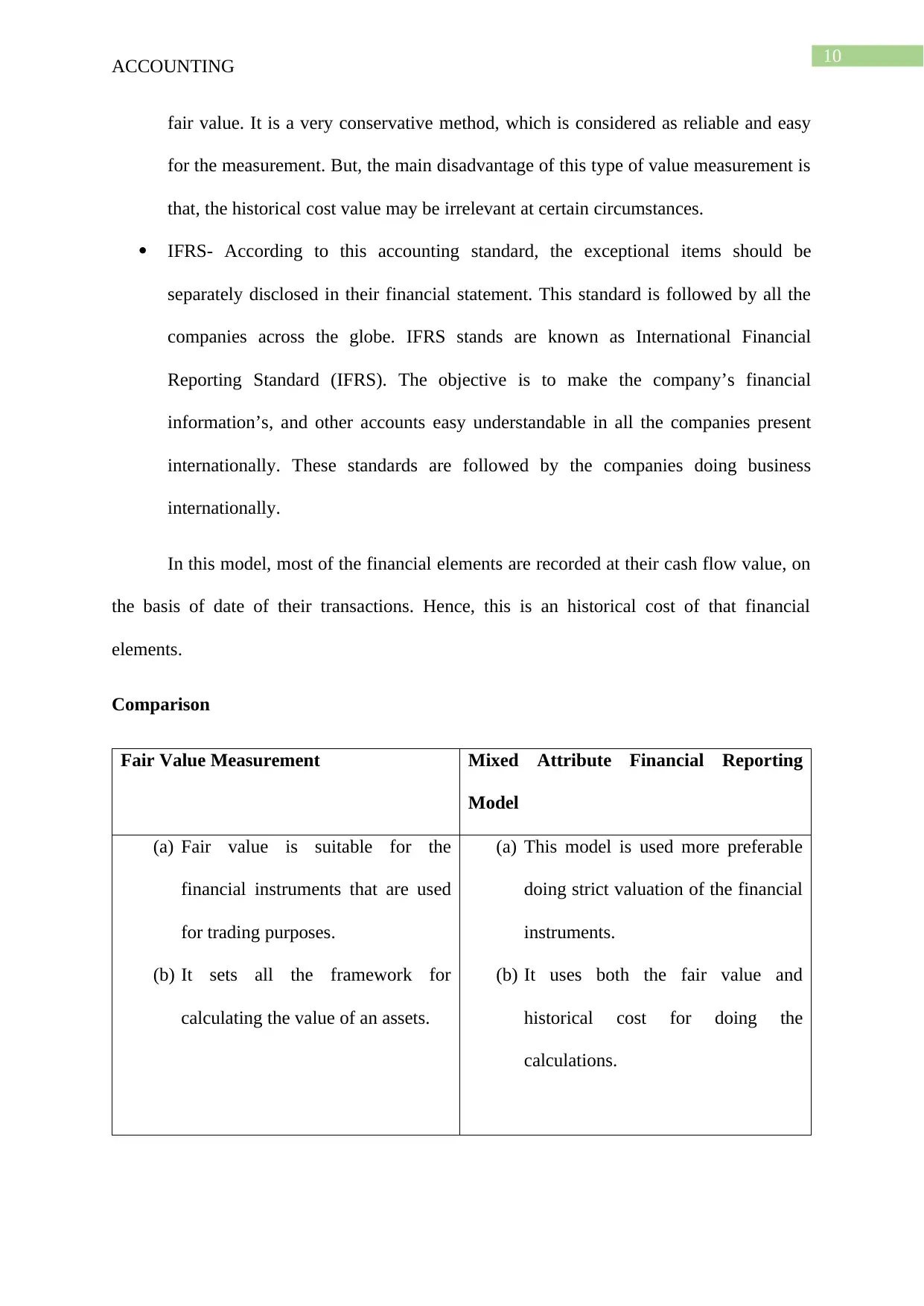

Comparison

Fair Value Measurement Mixed Attribute Financial Reporting

Model

(a) Fair value is suitable for the

financial instruments that are used

for trading purposes.

(b) It sets all the framework for

calculating the value of an assets.

(a) This model is used more preferable

doing strict valuation of the financial

instruments.

(b) It uses both the fair value and

historical cost for doing the

calculations.

ACCOUNTING

fair value. It is a very conservative method, which is considered as reliable and easy

for the measurement. But, the main disadvantage of this type of value measurement is

that, the historical cost value may be irrelevant at certain circumstances.

IFRS- According to this accounting standard, the exceptional items should be

separately disclosed in their financial statement. This standard is followed by all the

companies across the globe. IFRS stands are known as International Financial

Reporting Standard (IFRS). The objective is to make the company’s financial

information’s, and other accounts easy understandable in all the companies present

internationally. These standards are followed by the companies doing business

internationally.

In this model, most of the financial elements are recorded at their cash flow value, on

the basis of date of their transactions. Hence, this is an historical cost of that financial

elements.

Comparison

Fair Value Measurement Mixed Attribute Financial Reporting

Model

(a) Fair value is suitable for the

financial instruments that are used

for trading purposes.

(b) It sets all the framework for

calculating the value of an assets.

(a) This model is used more preferable

doing strict valuation of the financial

instruments.

(b) It uses both the fair value and

historical cost for doing the

calculations.

11

ACCOUNTING

Comparing the two model, it can be seen that, mixed attribute measurement model

helps to measure the assets, liabilities, expenses, revenues and other financial information’s

with the most relevant measurements. This model will help to measure the following

elements:

(a) Historical Cost- this is the monetary value of the assets.

(b) Fair Value

(c) Present value of the future cash flows

(d) Net realizable value

Disadvantage- When the market is unstable in case of financial crisis, the

measurements of the fair value of the assets may not be appropriate. The price may be

volatile. But, fair value measurements is the modification of mixed attribute model in IFRS

13 (Andon et al., 2018). In this case, the fair value is measured with respect to the historical

cost of the assets or liability. Therefore, historical cost accounting is used in this case. This

method can be appropriate for determining the fair value in fresh-start accounting process.

But, mixed measurement model is more flexible for valuation of the assets and the

other financial information. No active market for the assets exists in this case. This method

demoralizes the other measurement methods used by the companies. The most important

limitations in this type of measurement model is that, it represents the total financial assets as

the summation of total assets and liabilities that are measured at different bases. Therefore, it

can trump the actual value of the assets & liabilities (Mousavi et al., 2018). This model is

widely used by various companies because, a variety of measurement approaches are used in

this model, for measuring the value of the assets and liabilities. This model is a combination

of amortization cost & fair value and can be used to report the fair value of loans and deposits

depending on the nature of financial instruments (Marra, 2016). The value measured is

ACCOUNTING

Comparing the two model, it can be seen that, mixed attribute measurement model

helps to measure the assets, liabilities, expenses, revenues and other financial information’s

with the most relevant measurements. This model will help to measure the following

elements:

(a) Historical Cost- this is the monetary value of the assets.

(b) Fair Value

(c) Present value of the future cash flows

(d) Net realizable value

Disadvantage- When the market is unstable in case of financial crisis, the

measurements of the fair value of the assets may not be appropriate. The price may be

volatile. But, fair value measurements is the modification of mixed attribute model in IFRS

13 (Andon et al., 2018). In this case, the fair value is measured with respect to the historical

cost of the assets or liability. Therefore, historical cost accounting is used in this case. This

method can be appropriate for determining the fair value in fresh-start accounting process.

But, mixed measurement model is more flexible for valuation of the assets and the

other financial information. No active market for the assets exists in this case. This method

demoralizes the other measurement methods used by the companies. The most important

limitations in this type of measurement model is that, it represents the total financial assets as

the summation of total assets and liabilities that are measured at different bases. Therefore, it

can trump the actual value of the assets & liabilities (Mousavi et al., 2018). This model is

widely used by various companies because, a variety of measurement approaches are used in

this model, for measuring the value of the assets and liabilities. This model is a combination

of amortization cost & fair value and can be used to report the fair value of loans and deposits

depending on the nature of financial instruments (Marra, 2016). The value measured is

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.