Accounting Theory and Contemporary Issues: BHP Billiton GPFR Analysis

VerifiedAdded on 2023/06/13

|24

|4158

|158

Report

AI Summary

This report evaluates BHP Billiton's disclosures and financial performance, finding the company uses straight-line and units-of-production depreciation methods. Financial analysis reveals a failure to maintain a competitive edge over Rio Tinto due to increased operating expenses and high leverage. The company adheres to ASX corporate governance principles and uses the historical cost approach for tangible assets. The report also discusses the introduction of new AASB standards, ethical obligations, and the relationship between AASB and the conceptual framework. It identifies instances where BHP Billiton may have breached deontological ethics and virtue ethics, while also highlighting its adherence to utilitarianism. The report concludes with an assessment of BHP Billiton's global reports and measurement approaches.

Running head: ACCOUNTING THEORY AND CONTEMPORARY ISSUES

Accounting Theory and Contemporary Issues

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Accounting Theory and Contemporary Issues

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ACCOUNTING THEORY AND CONTEMPORARY ISSUES

Executive Summary:

The current report intends to evaluate the disclosures and financial performance of

BHP Billiton in accordance with the prevailing laws and principles in Australia. It has been

found out that the organisation uses straight-line method and units-of-production method for

depreciating its fixed tangible assets. The financial analysis carried out states that BHP

Billiton has failed to maintain competitive edge over Rio Tinto due to increased operating

expenses and high leverage. It has followed all the corporate governance principles

mentioned in ASX by reviewing its own standards and efforts are made continuously to

improve them further. Finally, it could be assessed that the organisation uses historical cost

approach for recognising its tangible assets such as property, plant and equipment.

Executive Summary:

The current report intends to evaluate the disclosures and financial performance of

BHP Billiton in accordance with the prevailing laws and principles in Australia. It has been

found out that the organisation uses straight-line method and units-of-production method for

depreciating its fixed tangible assets. The financial analysis carried out states that BHP

Billiton has failed to maintain competitive edge over Rio Tinto due to increased operating

expenses and high leverage. It has followed all the corporate governance principles

mentioned in ASX by reviewing its own standards and efforts are made continuously to

improve them further. Finally, it could be assessed that the organisation uses historical cost

approach for recognising its tangible assets such as property, plant and equipment.

2ACCOUNTING THEORY AND CONTEMPORARY ISSUES

Table of Contents

Introduction:...............................................................................................................................4

1. Methods employed by BHP Billiton in the construction of general purpose financial

reporting (GPFR):......................................................................................................................4

1.1 Method of depreciation used and useful life:...................................................................4

1.2 Amount of accounts receivable:.......................................................................................5

1.3 Provision for bad debts:...................................................................................................5

1.4 Contingent liability:.........................................................................................................6

1.6 Lease liability:..................................................................................................................7

1.7 Three non-financial areas included with the GPFR:........................................................8

2. Process for introduction of new AASB standard:................................................................10

2.1 Relationship between AASB and conceptual framework:.............................................11

2.2 Key points in relation to the new lease standard:...........................................................11

2.3 Lease of BHP Billiton and approach taken to record leases:.........................................12

3. Ethical obligations of BHP Billiton:....................................................................................13

3.1 Application of ethical theories:..........................................................................................13

3.2 Addressing conflict between profit and ethics:..............................................................14

4. Financial analysis of BHP Billiton and its competitor, Rio Tinto:......................................14

5. BHP Billiton’s global reports for the consolidated group:...................................................18

5.1 Key points in relation to accounting measurement:.......................................................18

5.2 Current system of accounting including historical cost and other accounting models:. 18

Table of Contents

Introduction:...............................................................................................................................4

1. Methods employed by BHP Billiton in the construction of general purpose financial

reporting (GPFR):......................................................................................................................4

1.1 Method of depreciation used and useful life:...................................................................4

1.2 Amount of accounts receivable:.......................................................................................5

1.3 Provision for bad debts:...................................................................................................5

1.4 Contingent liability:.........................................................................................................6

1.6 Lease liability:..................................................................................................................7

1.7 Three non-financial areas included with the GPFR:........................................................8

2. Process for introduction of new AASB standard:................................................................10

2.1 Relationship between AASB and conceptual framework:.............................................11

2.2 Key points in relation to the new lease standard:...........................................................11

2.3 Lease of BHP Billiton and approach taken to record leases:.........................................12

3. Ethical obligations of BHP Billiton:....................................................................................13

3.1 Application of ethical theories:..........................................................................................13

3.2 Addressing conflict between profit and ethics:..............................................................14

4. Financial analysis of BHP Billiton and its competitor, Rio Tinto:......................................14

5. BHP Billiton’s global reports for the consolidated group:...................................................18

5.1 Key points in relation to accounting measurement:.......................................................18

5.2 Current system of accounting including historical cost and other accounting models:. 18

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ACCOUNTING THEORY AND CONTEMPORARY ISSUES

5.3 Approach taken towards measurement on the part of BHP Billiton:.............................18

Conclusion:..............................................................................................................................19

References:...............................................................................................................................21

5.3 Approach taken towards measurement on the part of BHP Billiton:.............................18

Conclusion:..............................................................................................................................19

References:...............................................................................................................................21

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ACCOUNTING THEORY AND CONTEMPORARY ISSUES

Introduction:

Different methods are used by the organisations these days in construction of GPFR,

in which many companies attempt to maintain the conceptual framework of ethical

obligations. The objective of the report is to analyse the general purpose financial reports of

the selected company BHP Billiton. Moreover, the paper will also focus on analysing

whether the selected company has failed to comply with the ethical obligations. BHP Billiton

is positioned as global resources company that has an asset group operating in all over

Australia that operates within several commodities such as iron ore, metallurgical coal,

titanium and copper. The competitor of the company Rio Tinto has been selected in

evaluating and comparing the financial performance of these companies.

1. Methods employed by BHP Billiton in the construction of general purpose financial

reporting (GPFR):

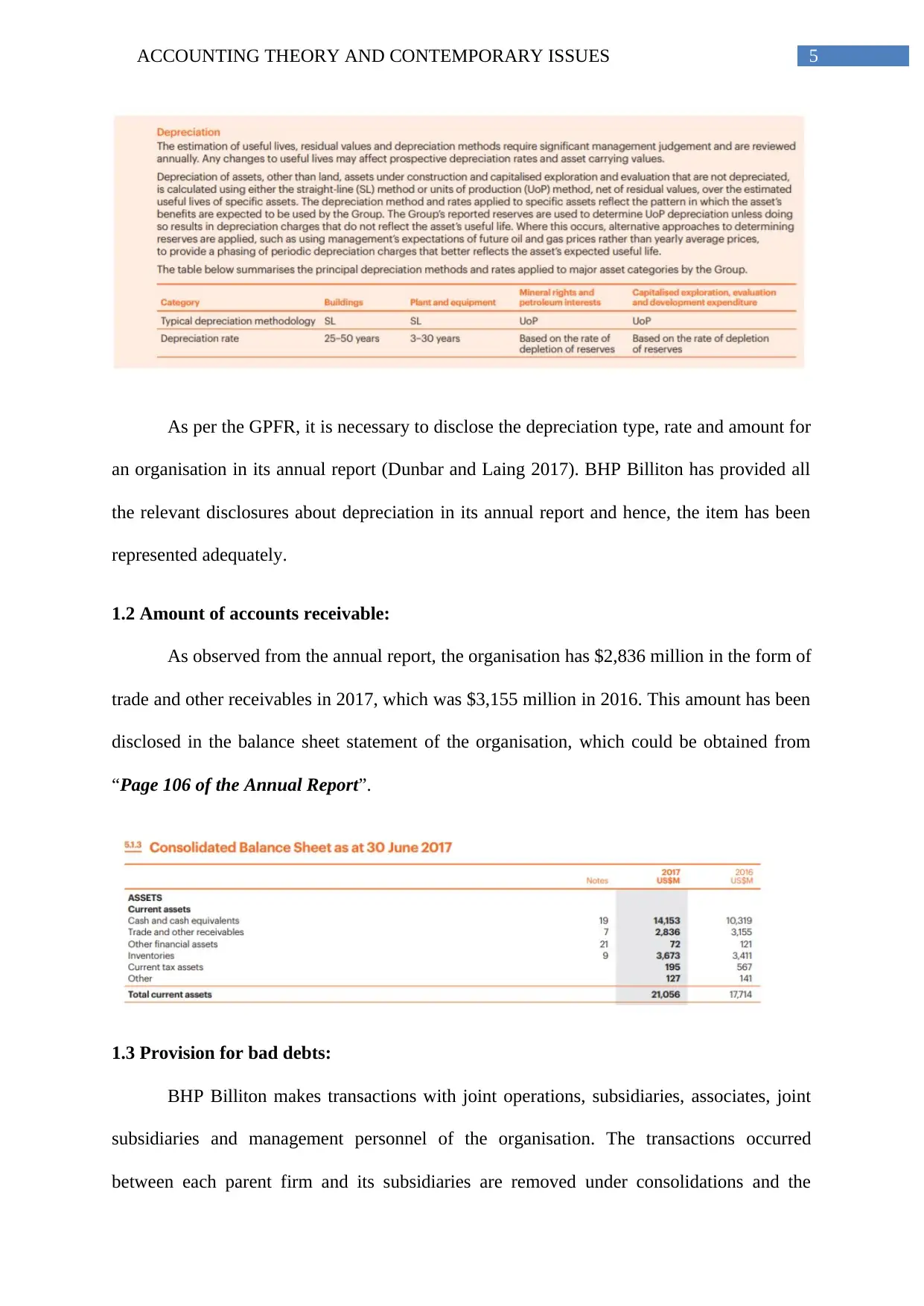

1.1 Method of depreciation used and useful life:

It could be observed from the annual report of 2017 that BHP Billiton uses straight-

line method as well as units of production method for depreciating its various classes of

assets. There are four types of assets that are depreciated in BHP Billiton and they include

buildings, plant and equipment, mineral rights and petroleum interests along with capitalised

exploration, evaluation and development expenditure. It has disclosed its useful lives of the

assets and the depreciation methods applied for such assets in “Page 178 of the Annual

Report”.

Introduction:

Different methods are used by the organisations these days in construction of GPFR,

in which many companies attempt to maintain the conceptual framework of ethical

obligations. The objective of the report is to analyse the general purpose financial reports of

the selected company BHP Billiton. Moreover, the paper will also focus on analysing

whether the selected company has failed to comply with the ethical obligations. BHP Billiton

is positioned as global resources company that has an asset group operating in all over

Australia that operates within several commodities such as iron ore, metallurgical coal,

titanium and copper. The competitor of the company Rio Tinto has been selected in

evaluating and comparing the financial performance of these companies.

1. Methods employed by BHP Billiton in the construction of general purpose financial

reporting (GPFR):

1.1 Method of depreciation used and useful life:

It could be observed from the annual report of 2017 that BHP Billiton uses straight-

line method as well as units of production method for depreciating its various classes of

assets. There are four types of assets that are depreciated in BHP Billiton and they include

buildings, plant and equipment, mineral rights and petroleum interests along with capitalised

exploration, evaluation and development expenditure. It has disclosed its useful lives of the

assets and the depreciation methods applied for such assets in “Page 178 of the Annual

Report”.

5ACCOUNTING THEORY AND CONTEMPORARY ISSUES

As per the GPFR, it is necessary to disclose the depreciation type, rate and amount for

an organisation in its annual report (Dunbar and Laing 2017). BHP Billiton has provided all

the relevant disclosures about depreciation in its annual report and hence, the item has been

represented adequately.

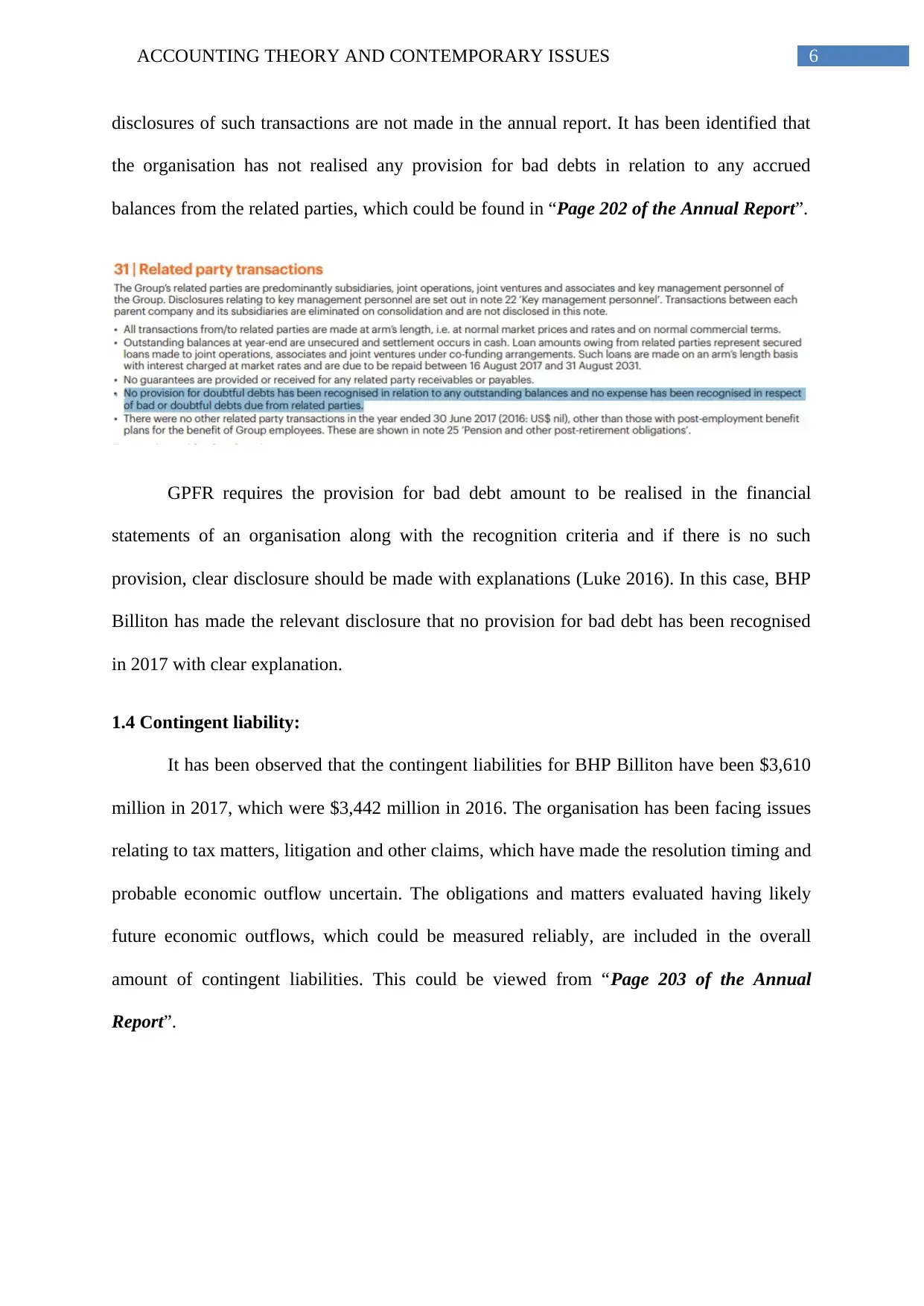

1.2 Amount of accounts receivable:

As observed from the annual report, the organisation has $2,836 million in the form of

trade and other receivables in 2017, which was $3,155 million in 2016. This amount has been

disclosed in the balance sheet statement of the organisation, which could be obtained from

“Page 106 of the Annual Report”.

1.3 Provision for bad debts:

BHP Billiton makes transactions with joint operations, subsidiaries, associates, joint

subsidiaries and management personnel of the organisation. The transactions occurred

between each parent firm and its subsidiaries are removed under consolidations and the

As per the GPFR, it is necessary to disclose the depreciation type, rate and amount for

an organisation in its annual report (Dunbar and Laing 2017). BHP Billiton has provided all

the relevant disclosures about depreciation in its annual report and hence, the item has been

represented adequately.

1.2 Amount of accounts receivable:

As observed from the annual report, the organisation has $2,836 million in the form of

trade and other receivables in 2017, which was $3,155 million in 2016. This amount has been

disclosed in the balance sheet statement of the organisation, which could be obtained from

“Page 106 of the Annual Report”.

1.3 Provision for bad debts:

BHP Billiton makes transactions with joint operations, subsidiaries, associates, joint

subsidiaries and management personnel of the organisation. The transactions occurred

between each parent firm and its subsidiaries are removed under consolidations and the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ACCOUNTING THEORY AND CONTEMPORARY ISSUES

disclosures of such transactions are not made in the annual report. It has been identified that

the organisation has not realised any provision for bad debts in relation to any accrued

balances from the related parties, which could be found in “Page 202 of the Annual Report”.

GPFR requires the provision for bad debt amount to be realised in the financial

statements of an organisation along with the recognition criteria and if there is no such

provision, clear disclosure should be made with explanations (Luke 2016). In this case, BHP

Billiton has made the relevant disclosure that no provision for bad debt has been recognised

in 2017 with clear explanation.

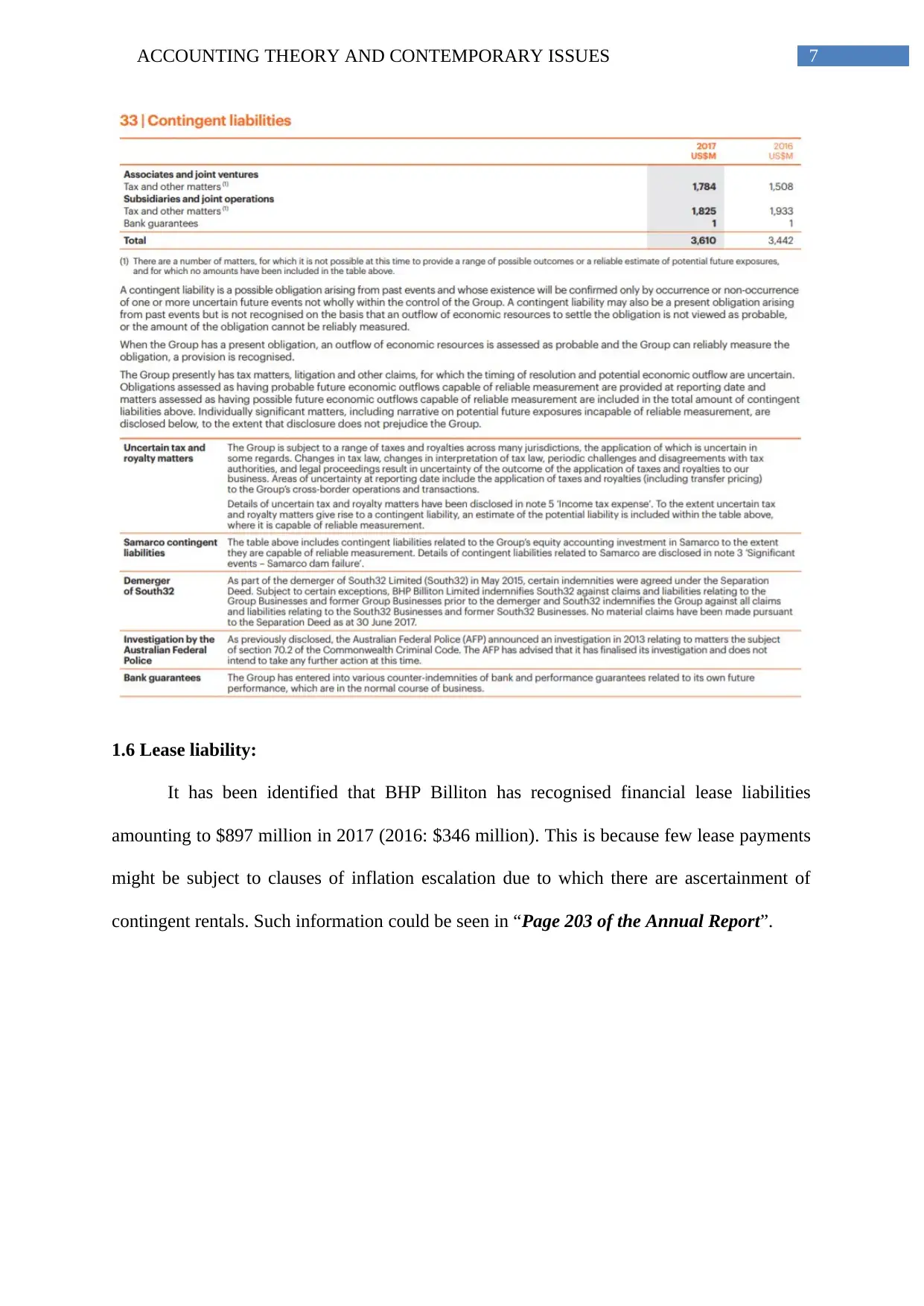

1.4 Contingent liability:

It has been observed that the contingent liabilities for BHP Billiton have been $3,610

million in 2017, which were $3,442 million in 2016. The organisation has been facing issues

relating to tax matters, litigation and other claims, which have made the resolution timing and

probable economic outflow uncertain. The obligations and matters evaluated having likely

future economic outflows, which could be measured reliably, are included in the overall

amount of contingent liabilities. This could be viewed from “Page 203 of the Annual

Report”.

disclosures of such transactions are not made in the annual report. It has been identified that

the organisation has not realised any provision for bad debts in relation to any accrued

balances from the related parties, which could be found in “Page 202 of the Annual Report”.

GPFR requires the provision for bad debt amount to be realised in the financial

statements of an organisation along with the recognition criteria and if there is no such

provision, clear disclosure should be made with explanations (Luke 2016). In this case, BHP

Billiton has made the relevant disclosure that no provision for bad debt has been recognised

in 2017 with clear explanation.

1.4 Contingent liability:

It has been observed that the contingent liabilities for BHP Billiton have been $3,610

million in 2017, which were $3,442 million in 2016. The organisation has been facing issues

relating to tax matters, litigation and other claims, which have made the resolution timing and

probable economic outflow uncertain. The obligations and matters evaluated having likely

future economic outflows, which could be measured reliably, are included in the overall

amount of contingent liabilities. This could be viewed from “Page 203 of the Annual

Report”.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ACCOUNTING THEORY AND CONTEMPORARY ISSUES

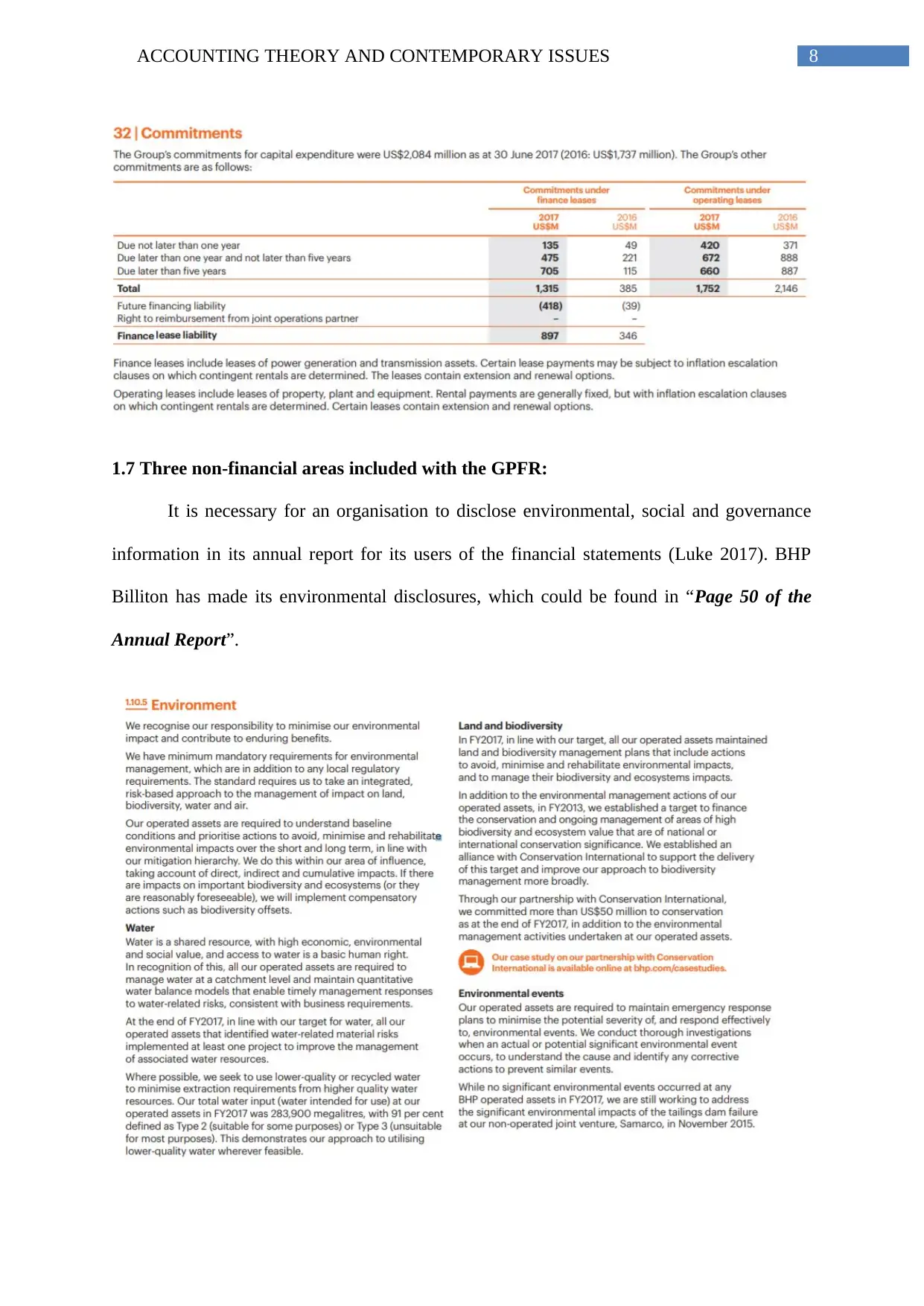

1.6 Lease liability:

It has been identified that BHP Billiton has recognised financial lease liabilities

amounting to $897 million in 2017 (2016: $346 million). This is because few lease payments

might be subject to clauses of inflation escalation due to which there are ascertainment of

contingent rentals. Such information could be seen in “Page 203 of the Annual Report”.

1.6 Lease liability:

It has been identified that BHP Billiton has recognised financial lease liabilities

amounting to $897 million in 2017 (2016: $346 million). This is because few lease payments

might be subject to clauses of inflation escalation due to which there are ascertainment of

contingent rentals. Such information could be seen in “Page 203 of the Annual Report”.

8ACCOUNTING THEORY AND CONTEMPORARY ISSUES

1.7 Three non-financial areas included with the GPFR:

It is necessary for an organisation to disclose environmental, social and governance

information in its annual report for its users of the financial statements (Luke 2017). BHP

Billiton has made its environmental disclosures, which could be found in “Page 50 of the

Annual Report”.

1.7 Three non-financial areas included with the GPFR:

It is necessary for an organisation to disclose environmental, social and governance

information in its annual report for its users of the financial statements (Luke 2017). BHP

Billiton has made its environmental disclosures, which could be found in “Page 50 of the

Annual Report”.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ACCOUNTING THEORY AND CONTEMPORARY ISSUES

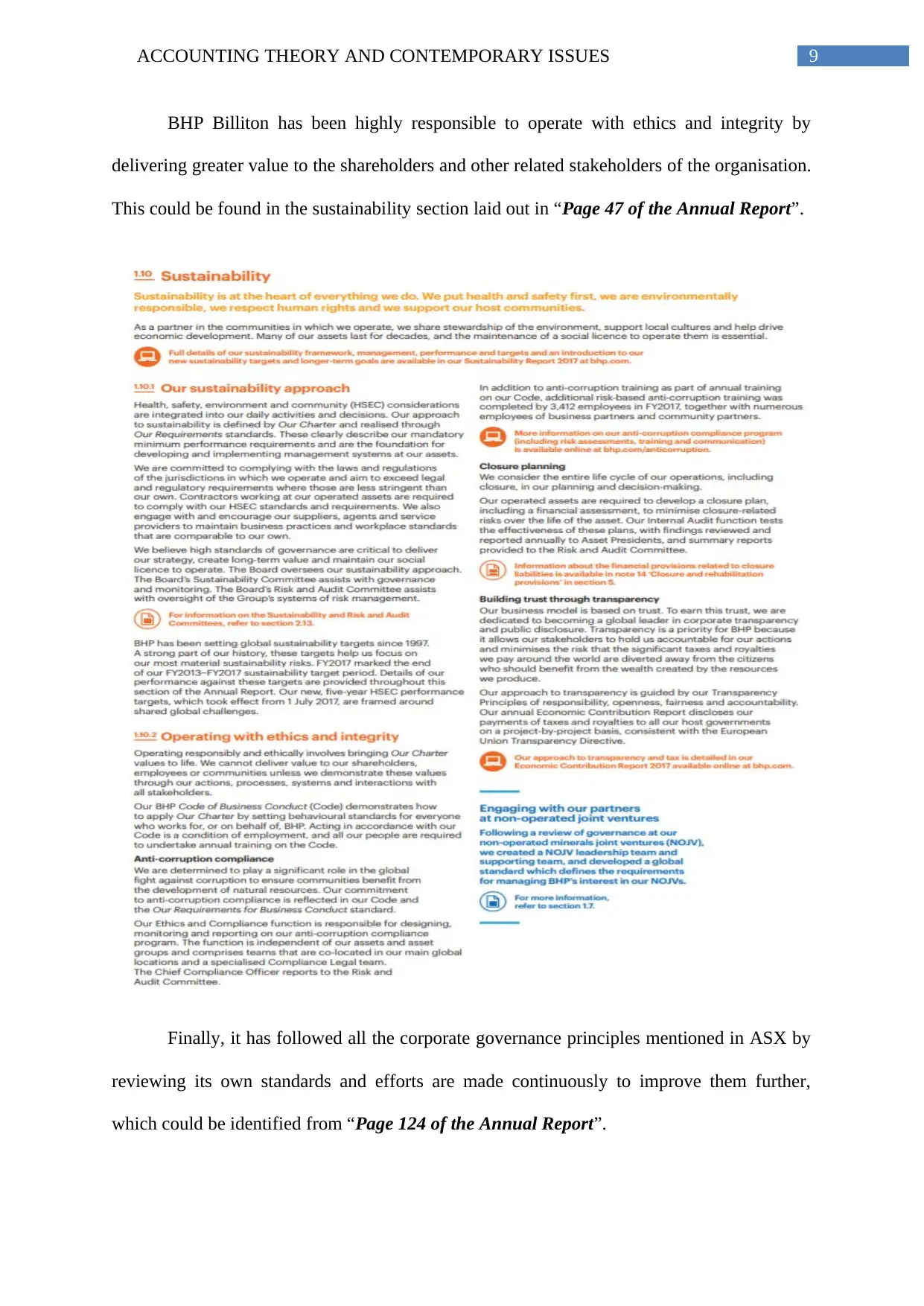

BHP Billiton has been highly responsible to operate with ethics and integrity by

delivering greater value to the shareholders and other related stakeholders of the organisation.

This could be found in the sustainability section laid out in “Page 47 of the Annual Report”.

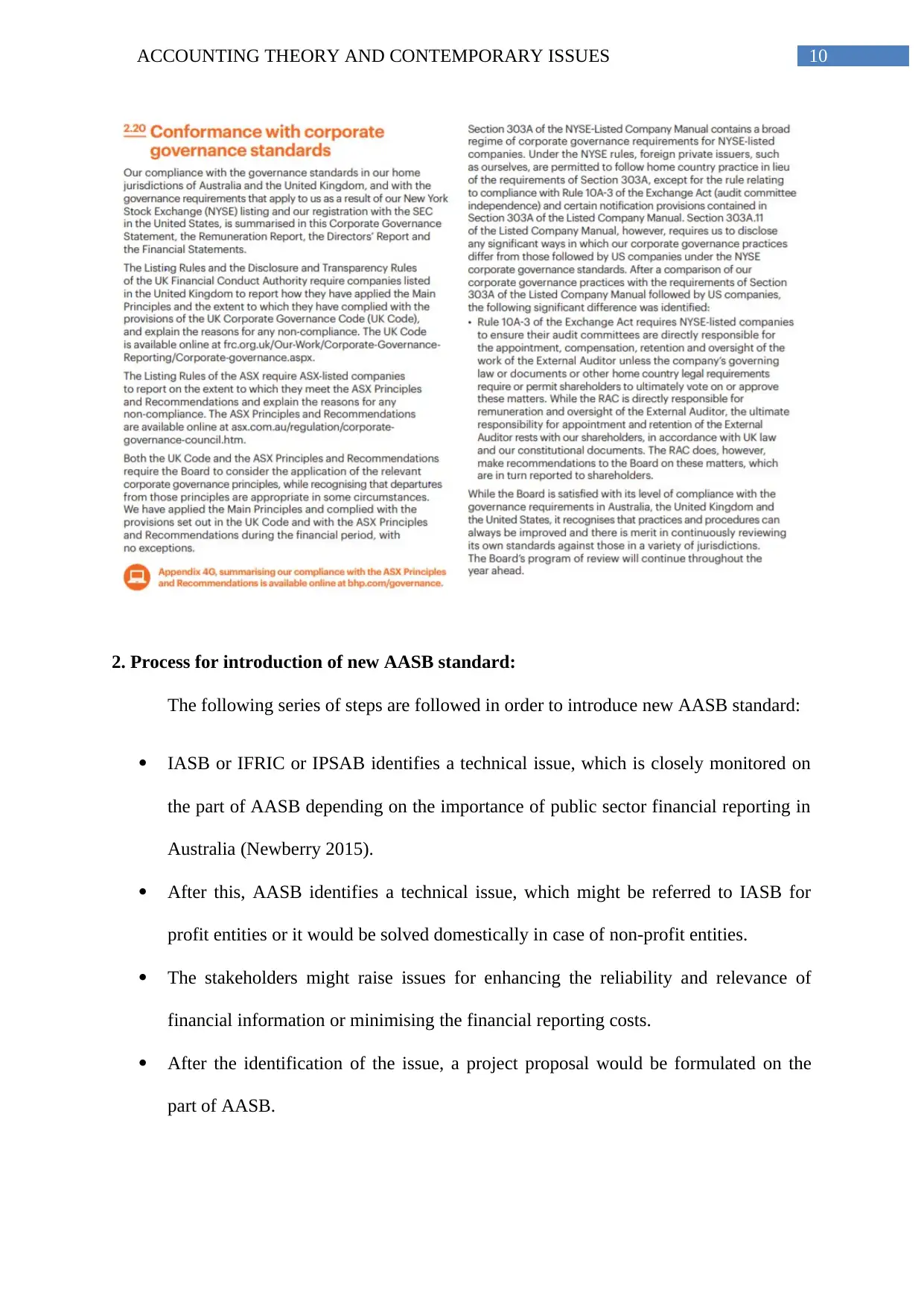

Finally, it has followed all the corporate governance principles mentioned in ASX by

reviewing its own standards and efforts are made continuously to improve them further,

which could be identified from “Page 124 of the Annual Report”.

BHP Billiton has been highly responsible to operate with ethics and integrity by

delivering greater value to the shareholders and other related stakeholders of the organisation.

This could be found in the sustainability section laid out in “Page 47 of the Annual Report”.

Finally, it has followed all the corporate governance principles mentioned in ASX by

reviewing its own standards and efforts are made continuously to improve them further,

which could be identified from “Page 124 of the Annual Report”.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ACCOUNTING THEORY AND CONTEMPORARY ISSUES

2. Process for introduction of new AASB standard:

The following series of steps are followed in order to introduce new AASB standard:

IASB or IFRIC or IPSAB identifies a technical issue, which is closely monitored on

the part of AASB depending on the importance of public sector financial reporting in

Australia (Newberry 2015).

After this, AASB identifies a technical issue, which might be referred to IASB for

profit entities or it would be solved domestically in case of non-profit entities.

The stakeholders might raise issues for enhancing the reliability and relevance of

financial information or minimising the financial reporting costs.

After the identification of the issue, a project proposal would be formulated on the

part of AASB.

2. Process for introduction of new AASB standard:

The following series of steps are followed in order to introduce new AASB standard:

IASB or IFRIC or IPSAB identifies a technical issue, which is closely monitored on

the part of AASB depending on the importance of public sector financial reporting in

Australia (Newberry 2015).

After this, AASB identifies a technical issue, which might be referred to IASB for

profit entities or it would be solved domestically in case of non-profit entities.

The stakeholders might raise issues for enhancing the reliability and relevance of

financial information or minimising the financial reporting costs.

After the identification of the issue, a project proposal would be formulated on the

part of AASB.

11ACCOUNTING THEORY AND CONTEMPORARY ISSUES

The proposal developed through agenda papers would address the issue scopes,

alternate options and output timings (Ryan et al. 2014).

After the completion of the research, associated documents would be published for

public comments and discussions with the shareholders.

AASB issues the proposed standard by considering the needs based on the nature of

the entities regardless of their operating sectors.

The inputs received from the stakeholders are submitted to the international

regulations.

Comments are received from the Australian stakeholders further for different

consultative documents.

Finally, the standard would be implemented backed by constant follow-up to ensure

compliance with the introduced standard (Sharma 2016).

2.1 Relationship between AASB and conceptual framework:

AASB is an Australian government agency and it receives considerable funds from

the Australian territories and states. On the other hand, the IASB has developed the

conceptual framework, which is a private sector organisation working independently in

London, UK (Watts and Zuo 2016). The AASB provides considerable monetary contribution

yearly to the IASB contributions.

2.2 Key points in relation to the new lease standard:

The new lease standard, AASB (IFRS) 16, would make the companies to disclose

operating leases on their balance sheet statements. The equipment and property leases not

realised previously on balance sheet would be recorded as right-of-use asset and lease

liability. This would help in ensuring transparency regarding the lease commitments of an

organisation and as a result, certain financial indicators like asset turnover, gearing ratios and

The proposal developed through agenda papers would address the issue scopes,

alternate options and output timings (Ryan et al. 2014).

After the completion of the research, associated documents would be published for

public comments and discussions with the shareholders.

AASB issues the proposed standard by considering the needs based on the nature of

the entities regardless of their operating sectors.

The inputs received from the stakeholders are submitted to the international

regulations.

Comments are received from the Australian stakeholders further for different

consultative documents.

Finally, the standard would be implemented backed by constant follow-up to ensure

compliance with the introduced standard (Sharma 2016).

2.1 Relationship between AASB and conceptual framework:

AASB is an Australian government agency and it receives considerable funds from

the Australian territories and states. On the other hand, the IASB has developed the

conceptual framework, which is a private sector organisation working independently in

London, UK (Watts and Zuo 2016). The AASB provides considerable monetary contribution

yearly to the IASB contributions.

2.2 Key points in relation to the new lease standard:

The new lease standard, AASB (IFRS) 16, would make the companies to disclose

operating leases on their balance sheet statements. The equipment and property leases not

realised previously on balance sheet would be recorded as right-of-use asset and lease

liability. This would help in ensuring transparency regarding the lease commitments of an

organisation and as a result, certain financial indicators like asset turnover, gearing ratios and

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 24

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.