Accounting Theory and Contemporary Issues Analysis Report - ACC301

VerifiedAdded on 2022/09/17

|6

|1135

|20

Report

AI Summary

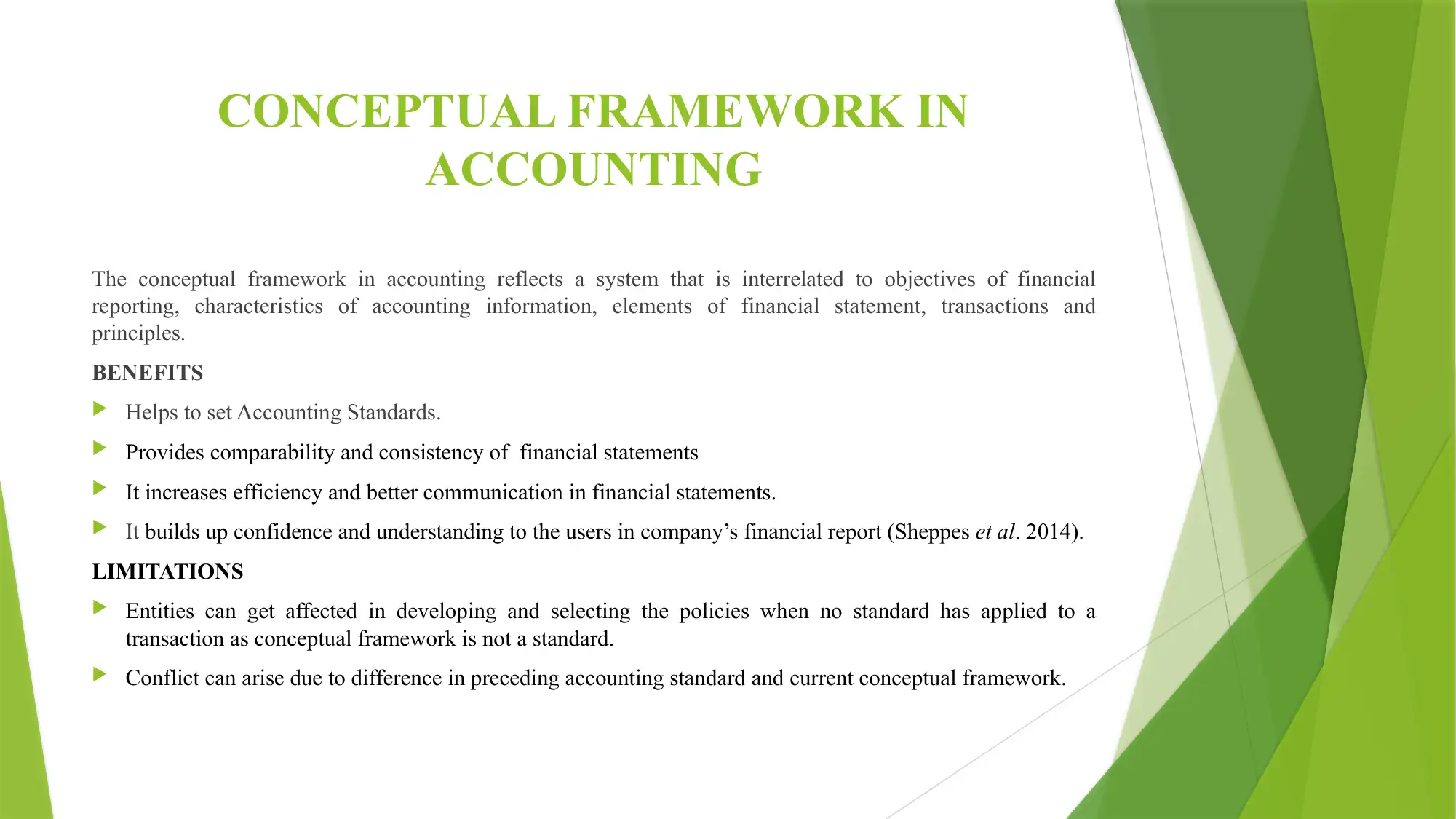

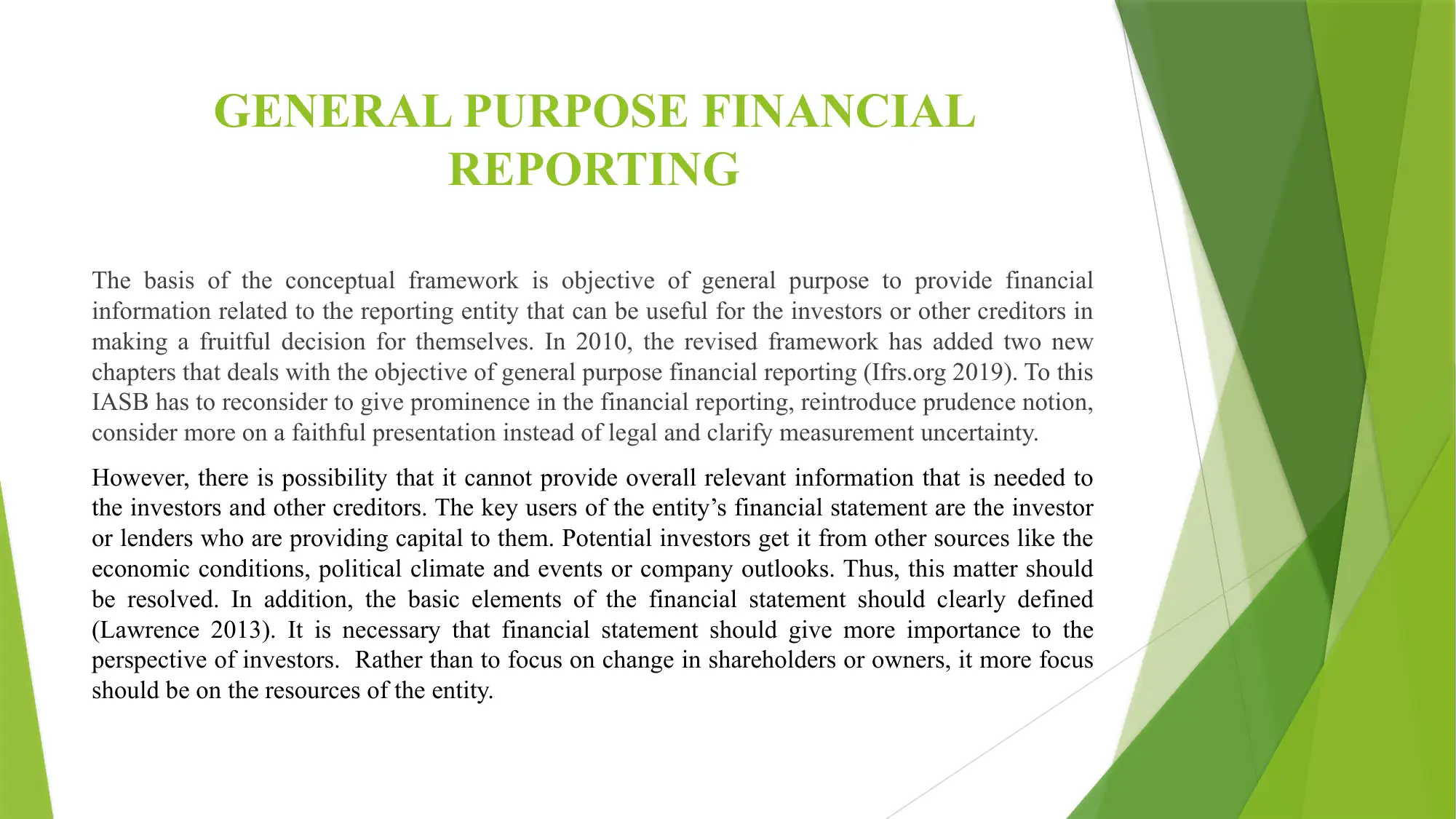

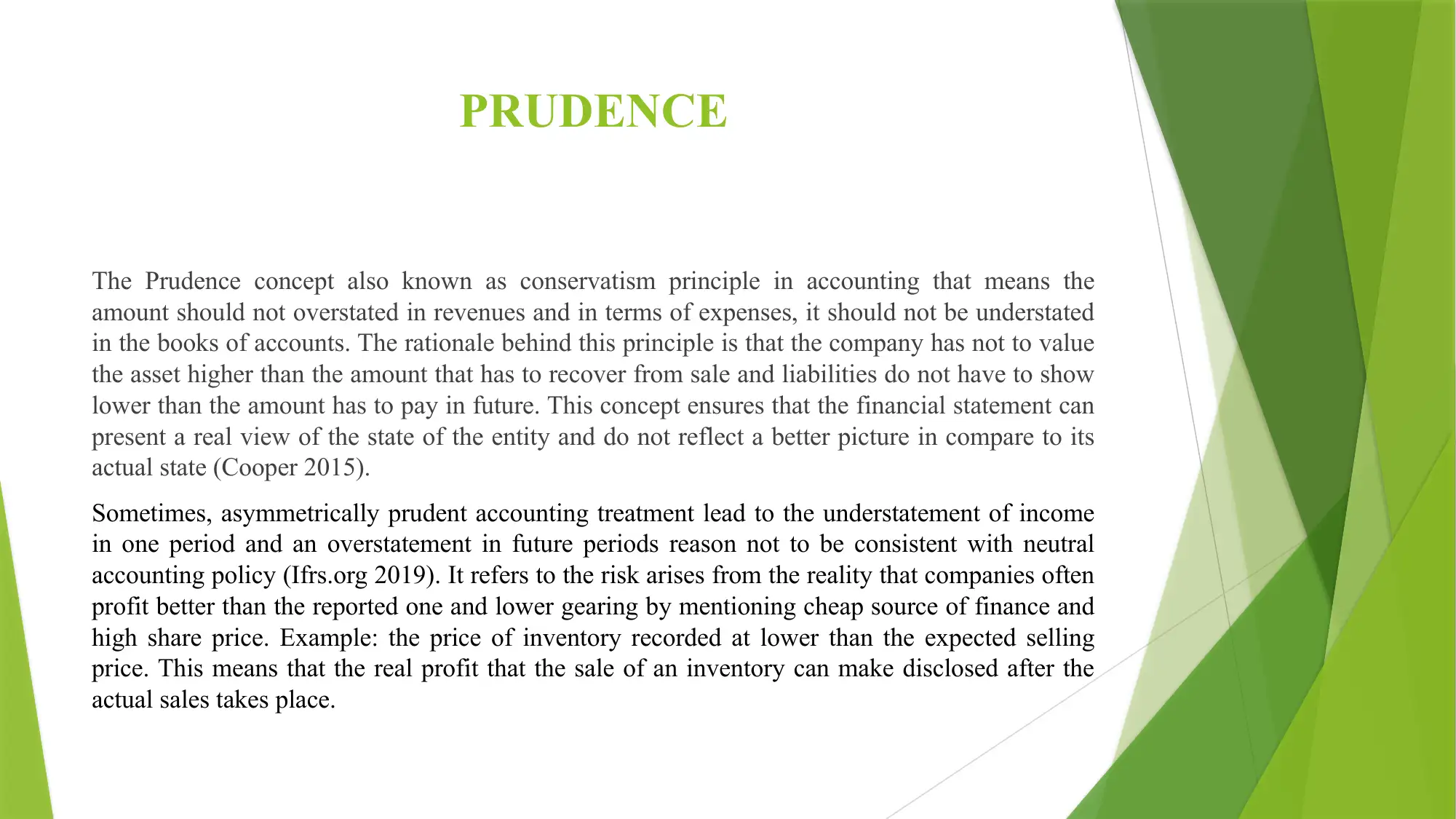

This report provides an analysis of the conceptual framework in accounting, focusing on the revised (2018) framework finalized by the IASB. The report explores the benefits and limitations of the framework, emphasizing its role in setting accounting standards and ensuring comparability. It delves into the objective of general-purpose financial reporting, highlighting its importance for investors and creditors, while also addressing potential limitations. The concept of prudence, or conservatism, is examined, including its implications for financial statement presentation. Furthermore, the report discusses the principle of substance over form, illustrating its application with examples and contrasting its implementation under GAAP and IFRS. The report leverages the provided references to support its claims and provides a comprehensive overview of the contemporary accounting issues. The report also addresses the key users of financial statements and emphasizes the importance of focusing on the resources of the entity rather than on changes in shareholders or owners. The report highlights the importance of the substance over form principle in financial reporting, which emphasizes the economic substance of transactions rather than their legal form.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.