Comprehensive Review: Accounting Theory and Current Issues

VerifiedAdded on 2023/06/05

|14

|2843

|473

Essay

AI Summary

This essay provides a comprehensive overview of accounting theory and current issues, focusing on management accounting and structured literature reviews (SLR). It analyzes two journals to identify relevant theories and prevalent issues in accounting practices, particularly within Australian and German contexts. The study examines the research-practice gap in management accounting, highlighting differences and similarities between Australia and Germany, and explores the role of SLR in enhancing financial accountability and resolving conflicts within organizations. The essay also discusses the implications of various factors, such as academic research, diffusion barriers, and the effectiveness of accounting management, on organizational performance. It concludes that financial theories and practices, including SLR and accounting management, are crucial for addressing accountability issues in Australian firms.

Running head: ACCOUNTING THEORY AND CURRENT ISSUES

Accounting Theory and Current Issues

Student Number

Page 1

Accounting Theory and Current Issues

Student Number

Page 1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING THEORY AND CURRENT ISSUES

Table of Contents

Introduction...............................................................................................................................3

Reasons for Journal selection....................................................................................................3

Research Questions of Selected Journal....................................................................................5

Major Implications within the Research Findings......................................................................5

Conclusion................................................................................................................................12

References................................................................................................................................13

Page 2

Table of Contents

Introduction...............................................................................................................................3

Reasons for Journal selection....................................................................................................3

Research Questions of Selected Journal....................................................................................5

Major Implications within the Research Findings......................................................................5

Conclusion................................................................................................................................12

References................................................................................................................................13

Page 2

ACCOUNTING THEORY AND CURRENT ISSUES

Introduction

This study intends to reflect a brief discussion regarding the theory of accounting and the

current issues that are prevalent in accounting. In this context, accounting is a process of

measure, wherein the higher authorities of an organization focus on determining the

organizational profit, loss, expenditure, income, liabilities, asset, debtors, and creditors

among others. Thus, based on this process of measuring, an organization focuses on the

development of its performance within its market (Tsamenyi, Cullen, & Gonzalez, 2006). On

the other hand, certain issues also initiate regarding this process of measuring. Hence, two

journals have been selected for the study. This includes “Same play, different actors?

Comparing the research-practice gap in management accounting in Australia and Germany”

and “On the shoulders of giants: undertaking a structured literature review in accounting”.

By analyzing these journals, potential theory related to the accounting and current issues

have been recognized.

Reasons for Journal selection

In order to conduct this study, both journals have been selected based on the accounting

along with its issues. The case first journal “Same Play, Different Actors? Comparing the

Research-Practice Gap in Management Accounting in Australia and Germany” focuses on

management accounting. This type of accounting is considered to be one of the major

operational activities within an organization. This is due to the fact that without proper

management of accounting, an organization is not able to measure its adequate profit or

loss within the market (Wiesel, Modell, & Moll, 2011). At the same time, management of

accounting helps an organization to avoid major accounting issues, which are conducted by

the organizational individuals. Hence, it can be considered as a first reason behind the

Page 3

Introduction

This study intends to reflect a brief discussion regarding the theory of accounting and the

current issues that are prevalent in accounting. In this context, accounting is a process of

measure, wherein the higher authorities of an organization focus on determining the

organizational profit, loss, expenditure, income, liabilities, asset, debtors, and creditors

among others. Thus, based on this process of measuring, an organization focuses on the

development of its performance within its market (Tsamenyi, Cullen, & Gonzalez, 2006). On

the other hand, certain issues also initiate regarding this process of measuring. Hence, two

journals have been selected for the study. This includes “Same play, different actors?

Comparing the research-practice gap in management accounting in Australia and Germany”

and “On the shoulders of giants: undertaking a structured literature review in accounting”.

By analyzing these journals, potential theory related to the accounting and current issues

have been recognized.

Reasons for Journal selection

In order to conduct this study, both journals have been selected based on the accounting

along with its issues. The case first journal “Same Play, Different Actors? Comparing the

Research-Practice Gap in Management Accounting in Australia and Germany” focuses on

management accounting. This type of accounting is considered to be one of the major

operational activities within an organization. This is due to the fact that without proper

management of accounting, an organization is not able to measure its adequate profit or

loss within the market (Wiesel, Modell, & Moll, 2011). At the same time, management of

accounting helps an organization to avoid major accounting issues, which are conducted by

the organizational individuals. Hence, it can be considered as a first reason behind the

Page 3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ACCOUNTING THEORY AND CURRENT ISSUES

selecting afore-mentioned journal. This particular journal majorly focuses on management

accounting and its implications within an organization in order to mitigate issues related to

the accounting (Broadbent & Guthrie, 2008).

In case of the second journal, “On the Shoulders of Giants: Undertaking a Structured

Literature Review in Accounting” has been selected to identify an adequate theoretical

review of the accounting as well as its issues. Theory of accounting plays a major role within

an organization, as it provides an appropriate path of accountability. In addition, the entire

accounting system of an organization is based on the day to day transactions. Hence, the

theory of accounting helps the financial experts for segmenting information relating to

organizational transactions in a decent manner. By implementing and following the theory

of accounting an organization can help in mitigating any difficulties within the operating

market. Thus, due to owing to this reason, the aforementioned journal has been selected to

develop this study. Appropriate or structured literature research can assist in maintaining

internal activities of the organizations in Australia (Brüggen, Vergauwen, & Dao, 2009).

Overall, accounting management along with structured research of accounting can aid an

organization to achieve market goals. Apart from this, both journals have reflected different

outcomes of accounting. At the same time, the journal also focuses on the management of

accounting along with the accounting literature. Simultaneously, major factors regarding

accounting along with its practice such as auditing, financial diffusion, the traditional

accounting system, and its implications have been possible for identifying these journals.

Therefore, this afore-mentioned reason can be considered as the third reason behind the

selection of these journals for this study (Isik, Dogru & Turk, 2018).

Page 4

selecting afore-mentioned journal. This particular journal majorly focuses on management

accounting and its implications within an organization in order to mitigate issues related to

the accounting (Broadbent & Guthrie, 2008).

In case of the second journal, “On the Shoulders of Giants: Undertaking a Structured

Literature Review in Accounting” has been selected to identify an adequate theoretical

review of the accounting as well as its issues. Theory of accounting plays a major role within

an organization, as it provides an appropriate path of accountability. In addition, the entire

accounting system of an organization is based on the day to day transactions. Hence, the

theory of accounting helps the financial experts for segmenting information relating to

organizational transactions in a decent manner. By implementing and following the theory

of accounting an organization can help in mitigating any difficulties within the operating

market. Thus, due to owing to this reason, the aforementioned journal has been selected to

develop this study. Appropriate or structured literature research can assist in maintaining

internal activities of the organizations in Australia (Brüggen, Vergauwen, & Dao, 2009).

Overall, accounting management along with structured research of accounting can aid an

organization to achieve market goals. Apart from this, both journals have reflected different

outcomes of accounting. At the same time, the journal also focuses on the management of

accounting along with the accounting literature. Simultaneously, major factors regarding

accounting along with its practice such as auditing, financial diffusion, the traditional

accounting system, and its implications have been possible for identifying these journals.

Therefore, this afore-mentioned reason can be considered as the third reason behind the

selection of these journals for this study (Isik, Dogru & Turk, 2018).

Page 4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING THEORY AND CURRENT ISSUES

Research Questions of Selected Journal

In the case of the first journal, the researcher has implied quantitative research approach.

Research has been focusing on the diffusion of innovation. Hence, a survey has been

conducted among 33 respondents, wherein certain questionnaires have been asked relating

to the Australian and German accounting standards along with bodies. This article thus

focuses on the management of accounting, which has been implemented by the Australian

and German accounting bodies, which is also the main research question of the study. Based

on this research, survey questions have been segmented into four parts, which includes

accounting literature, the translation stage, the dissemination stage, and areas of inquiry.

The final section of the questionnaire has been used for a personal interview (Migacz, Zou &

Petrick, 2018).

In case of the second journal, the authors Maurizio Massaro, John Dumay, and James

Guthrie have considered both qualitative as well as a quantitative research method.

Through this research, they have identified the structured literature review in accounting or

SLR. The key question focuses on the ways through which accounting literatures have been

helping organizations to develop accountability. In order to conduct the research, the

authors are analyzing various peer-reviewed journals along with books. At the same time,

the logic behind the SLR using within an organization also has been developed through the

research.

Page 5

Research Questions of Selected Journal

In the case of the first journal, the researcher has implied quantitative research approach.

Research has been focusing on the diffusion of innovation. Hence, a survey has been

conducted among 33 respondents, wherein certain questionnaires have been asked relating

to the Australian and German accounting standards along with bodies. This article thus

focuses on the management of accounting, which has been implemented by the Australian

and German accounting bodies, which is also the main research question of the study. Based

on this research, survey questions have been segmented into four parts, which includes

accounting literature, the translation stage, the dissemination stage, and areas of inquiry.

The final section of the questionnaire has been used for a personal interview (Migacz, Zou &

Petrick, 2018).

In case of the second journal, the authors Maurizio Massaro, John Dumay, and James

Guthrie have considered both qualitative as well as a quantitative research method.

Through this research, they have identified the structured literature review in accounting or

SLR. The key question focuses on the ways through which accounting literatures have been

helping organizations to develop accountability. In order to conduct the research, the

authors are analyzing various peer-reviewed journals along with books. At the same time,

the logic behind the SLR using within an organization also has been developed through the

research.

Page 5

ACCOUNTING THEORY AND CURRENT ISSUES

Major Implications within the Research Findings

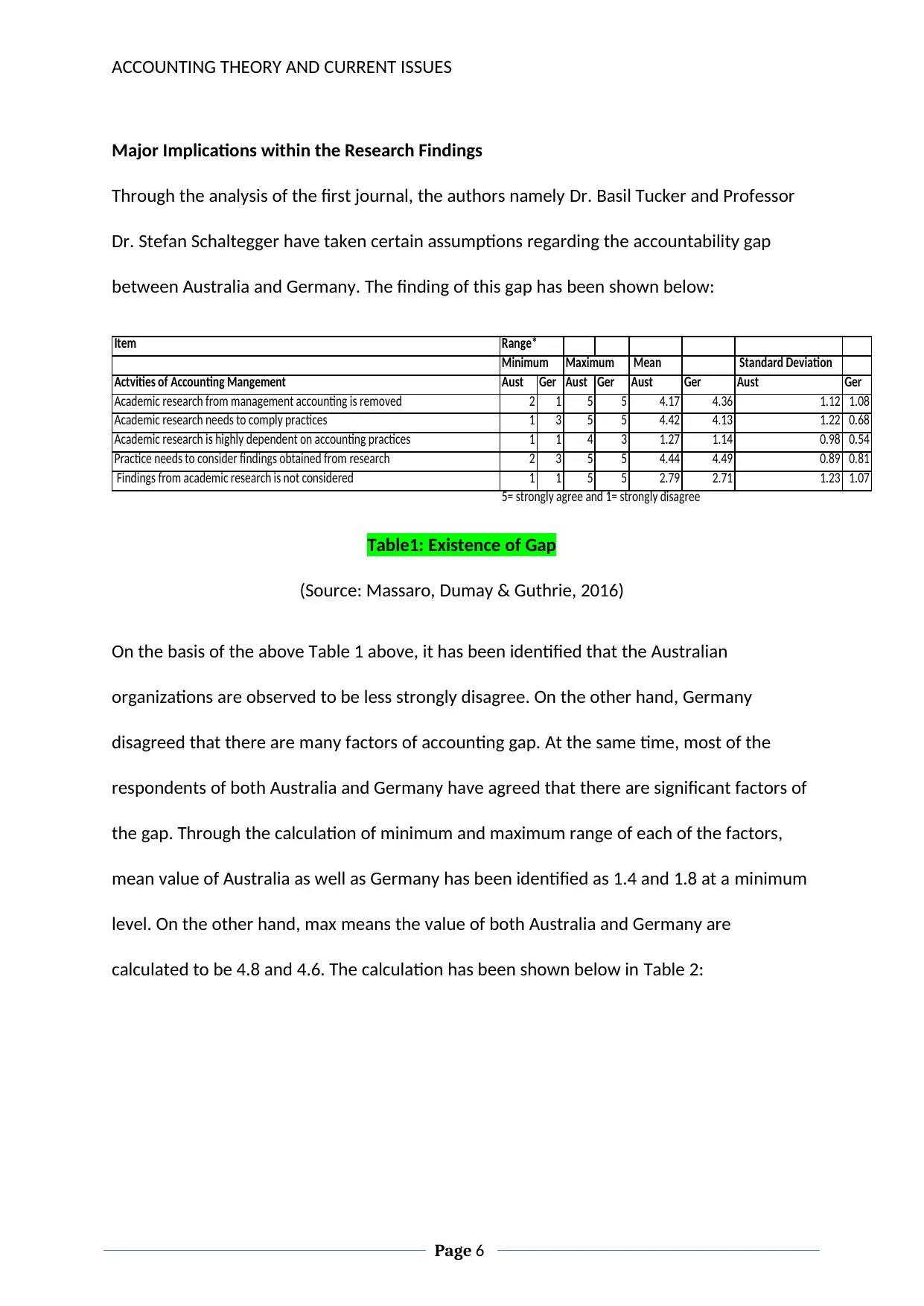

Through the analysis of the first journal, the authors namely Dr. Basil Tucker and Professor

Dr. Stefan Schaltegger have taken certain assumptions regarding the accountability gap

between Australia and Germany. The finding of this gap has been shown below:

Item Range*

Minimum Maximum Mean Standard Deviation

Actvities of Accounting Mangement Aust Ger Aust Ger Aust Ger Aust Ger

Academic research from management accounting is removed 2 1 5 5 4.17 4.36 1.12 1.08

Academic research needs to comply practices 1 3 5 5 4.42 4.13 1.22 0.68

Academic research is highly dependent on accounting practices 1 1 4 3 1.27 1.14 0.98 0.54

Practice needs to consider findings obtained from research 2 3 5 5 4.44 4.49 0.89 0.81

Findings from academic research is not considered 1 1 5 5 2.79 2.71 1.23 1.07

5= strongly agree and 1= strongly disagree

Table1: Existence of Gap

(Source: Massaro, Dumay & Guthrie, 2016)

On the basis of the above Table 1 above, it has been identified that the Australian

organizations are observed to be less strongly disagree. On the other hand, Germany

disagreed that there are many factors of accounting gap. At the same time, most of the

respondents of both Australia and Germany have agreed that there are significant factors of

the gap. Through the calculation of minimum and maximum range of each of the factors,

mean value of Australia as well as Germany has been identified as 1.4 and 1.8 at a minimum

level. On the other hand, max means the value of both Australia and Germany are

calculated to be 4.8 and 4.6. The calculation has been shown below in Table 2:

Page 6

Major Implications within the Research Findings

Through the analysis of the first journal, the authors namely Dr. Basil Tucker and Professor

Dr. Stefan Schaltegger have taken certain assumptions regarding the accountability gap

between Australia and Germany. The finding of this gap has been shown below:

Item Range*

Minimum Maximum Mean Standard Deviation

Actvities of Accounting Mangement Aust Ger Aust Ger Aust Ger Aust Ger

Academic research from management accounting is removed 2 1 5 5 4.17 4.36 1.12 1.08

Academic research needs to comply practices 1 3 5 5 4.42 4.13 1.22 0.68

Academic research is highly dependent on accounting practices 1 1 4 3 1.27 1.14 0.98 0.54

Practice needs to consider findings obtained from research 2 3 5 5 4.44 4.49 0.89 0.81

Findings from academic research is not considered 1 1 5 5 2.79 2.71 1.23 1.07

5= strongly agree and 1= strongly disagree

Table1: Existence of Gap

(Source: Massaro, Dumay & Guthrie, 2016)

On the basis of the above Table 1 above, it has been identified that the Australian

organizations are observed to be less strongly disagree. On the other hand, Germany

disagreed that there are many factors of accounting gap. At the same time, most of the

respondents of both Australia and Germany have agreed that there are significant factors of

the gap. Through the calculation of minimum and maximum range of each of the factors,

mean value of Australia as well as Germany has been identified as 1.4 and 1.8 at a minimum

level. On the other hand, max means the value of both Australia and Germany are

calculated to be 4.8 and 4.6. The calculation has been shown below in Table 2:

Page 6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ACCOUNTING THEORY AND CURRENT ISSUES

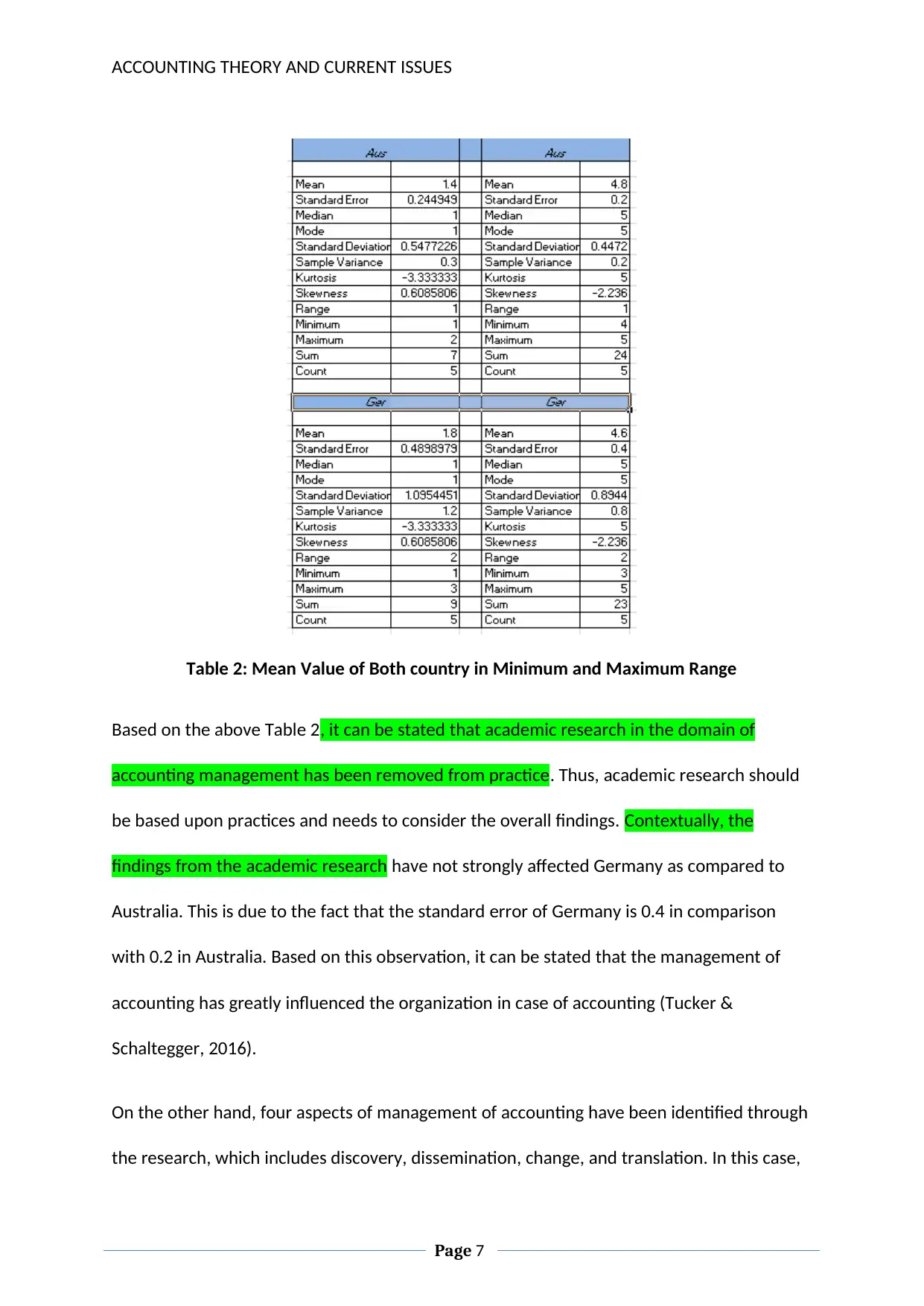

Table 2: Mean Value of Both country in Minimum and Maximum Range

Based on the above Table 2, it can be stated that academic research in the domain of

accounting management has been removed from practice. Thus, academic research should

be based upon practices and needs to consider the overall findings. Contextually, the

findings from the academic research have not strongly affected Germany as compared to

Australia. This is due to the fact that the standard error of Germany is 0.4 in comparison

with 0.2 in Australia. Based on this observation, it can be stated that the management of

accounting has greatly influenced the organization in case of accounting (Tucker &

Schaltegger, 2016).

On the other hand, four aspects of management of accounting have been identified through

the research, which includes discovery, dissemination, change, and translation. In this case,

Page 7

Table 2: Mean Value of Both country in Minimum and Maximum Range

Based on the above Table 2, it can be stated that academic research in the domain of

accounting management has been removed from practice. Thus, academic research should

be based upon practices and needs to consider the overall findings. Contextually, the

findings from the academic research have not strongly affected Germany as compared to

Australia. This is due to the fact that the standard error of Germany is 0.4 in comparison

with 0.2 in Australia. Based on this observation, it can be stated that the management of

accounting has greatly influenced the organization in case of accounting (Tucker &

Schaltegger, 2016).

On the other hand, four aspects of management of accounting have been identified through

the research, which includes discovery, dissemination, change, and translation. In this case,

Page 7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING THEORY AND CURRENT ISSUES

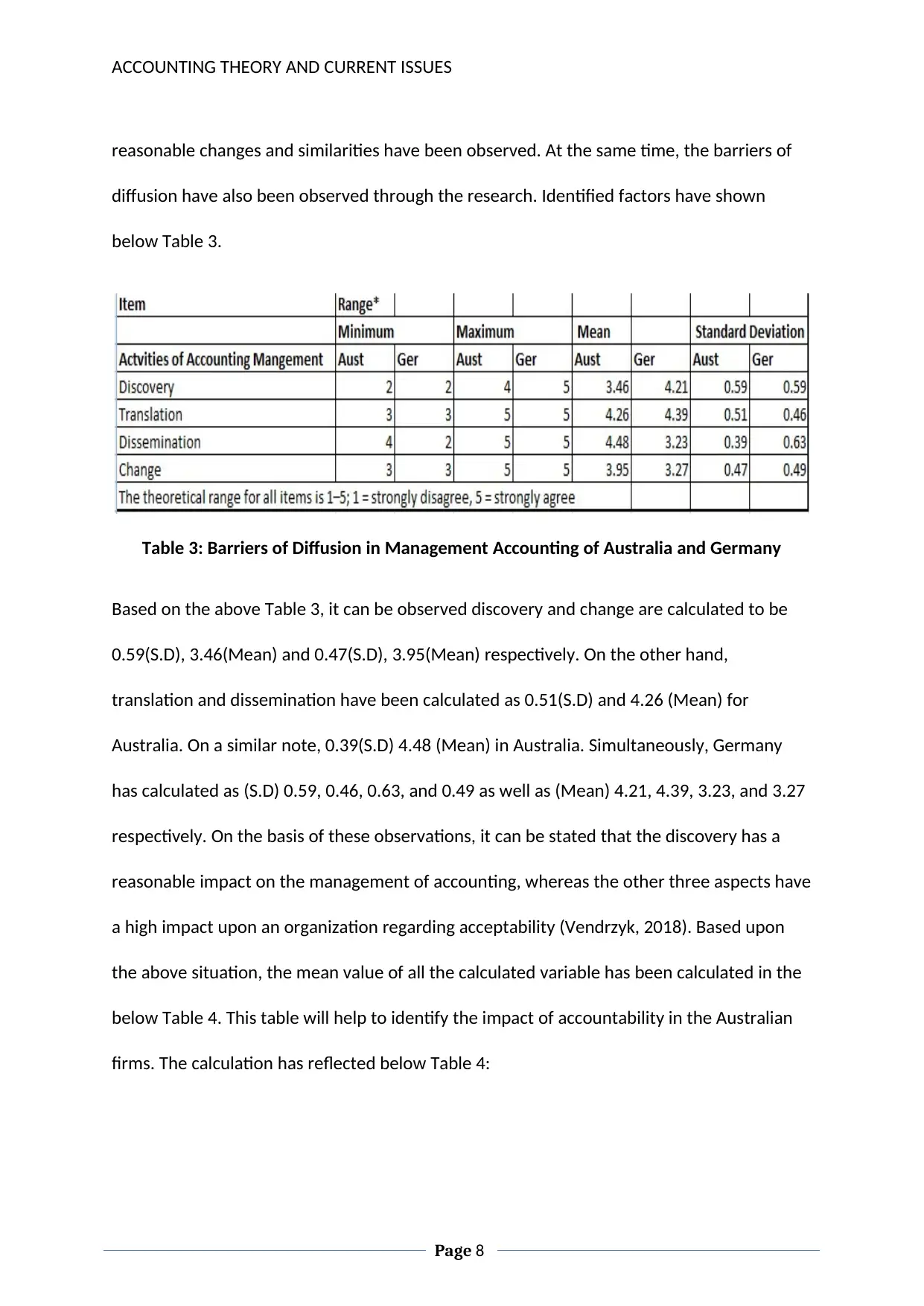

reasonable changes and similarities have been observed. At the same time, the barriers of

diffusion have also been observed through the research. Identified factors have shown

below Table 3.

Table 3: Barriers of Diffusion in Management Accounting of Australia and Germany

Based on the above Table 3, it can be observed discovery and change are calculated to be

0.59(S.D), 3.46(Mean) and 0.47(S.D), 3.95(Mean) respectively. On the other hand,

translation and dissemination have been calculated as 0.51(S.D) and 4.26 (Mean) for

Australia. On a similar note, 0.39(S.D) 4.48 (Mean) in Australia. Simultaneously, Germany

has calculated as (S.D) 0.59, 0.46, 0.63, and 0.49 as well as (Mean) 4.21, 4.39, 3.23, and 3.27

respectively. On the basis of these observations, it can be stated that the discovery has a

reasonable impact on the management of accounting, whereas the other three aspects have

a high impact upon an organization regarding acceptability (Vendrzyk, 2018). Based upon

the above situation, the mean value of all the calculated variable has been calculated in the

below Table 4. This table will help to identify the impact of accountability in the Australian

firms. The calculation has reflected below Table 4:

Page 8

reasonable changes and similarities have been observed. At the same time, the barriers of

diffusion have also been observed through the research. Identified factors have shown

below Table 3.

Table 3: Barriers of Diffusion in Management Accounting of Australia and Germany

Based on the above Table 3, it can be observed discovery and change are calculated to be

0.59(S.D), 3.46(Mean) and 0.47(S.D), 3.95(Mean) respectively. On the other hand,

translation and dissemination have been calculated as 0.51(S.D) and 4.26 (Mean) for

Australia. On a similar note, 0.39(S.D) 4.48 (Mean) in Australia. Simultaneously, Germany

has calculated as (S.D) 0.59, 0.46, 0.63, and 0.49 as well as (Mean) 4.21, 4.39, 3.23, and 3.27

respectively. On the basis of these observations, it can be stated that the discovery has a

reasonable impact on the management of accounting, whereas the other three aspects have

a high impact upon an organization regarding acceptability (Vendrzyk, 2018). Based upon

the above situation, the mean value of all the calculated variable has been calculated in the

below Table 4. This table will help to identify the impact of accountability in the Australian

firms. The calculation has reflected below Table 4:

Page 8

ACCOUNTING THEORY AND CURRENT ISSUES

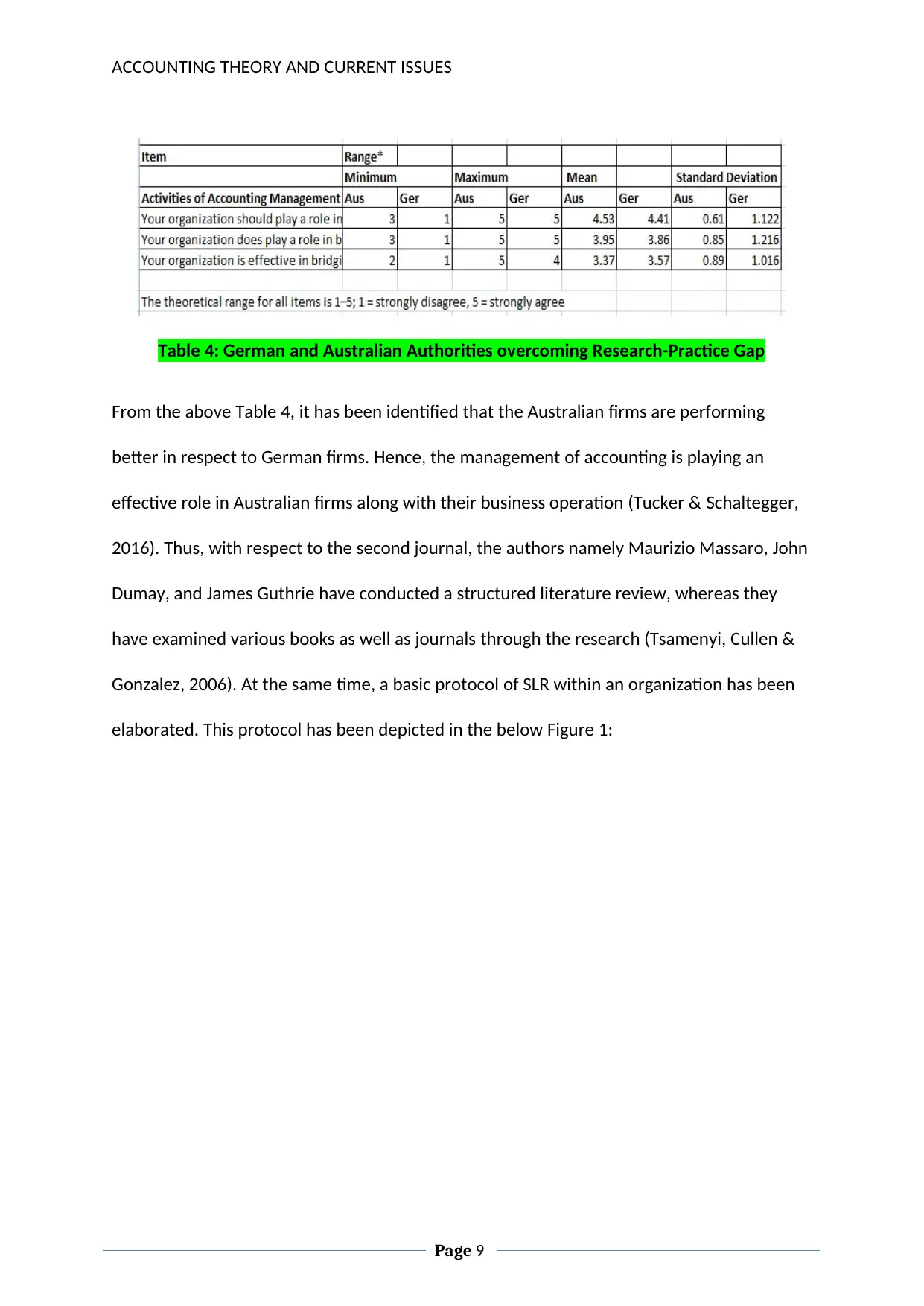

Table 4: German and Australian Authorities overcoming Research-Practice Gap

From the above Table 4, it has been identified that the Australian firms are performing

better in respect to German firms. Hence, the management of accounting is playing an

effective role in Australian firms along with their business operation (Tucker & Schaltegger,

2016). Thus, with respect to the second journal, the authors namely Maurizio Massaro, John

Dumay, and James Guthrie have conducted a structured literature review, whereas they

have examined various books as well as journals through the research (Tsamenyi, Cullen &

Gonzalez, 2006). At the same time, a basic protocol of SLR within an organization has been

elaborated. This protocol has been depicted in the below Figure 1:

Page 9

Table 4: German and Australian Authorities overcoming Research-Practice Gap

From the above Table 4, it has been identified that the Australian firms are performing

better in respect to German firms. Hence, the management of accounting is playing an

effective role in Australian firms along with their business operation (Tucker & Schaltegger,

2016). Thus, with respect to the second journal, the authors namely Maurizio Massaro, John

Dumay, and James Guthrie have conducted a structured literature review, whereas they

have examined various books as well as journals through the research (Tsamenyi, Cullen &

Gonzalez, 2006). At the same time, a basic protocol of SLR within an organization has been

elaborated. This protocol has been depicted in the below Figure 1:

Page 9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ACCOUNTING THEORY AND CURRENT ISSUES

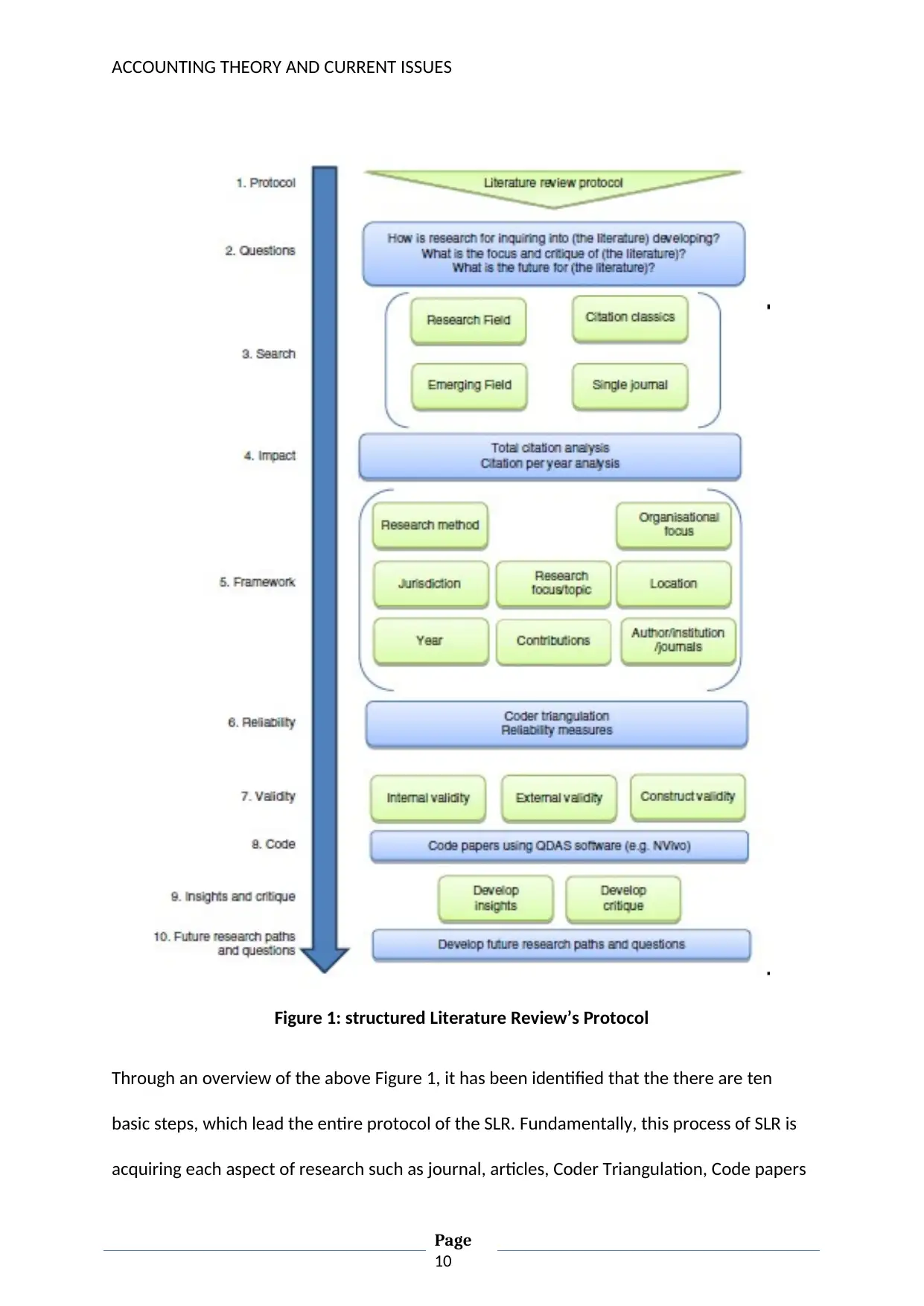

Figure 1: structured Literature Review’s Protocol

Through an overview of the above Figure 1, it has been identified that the there are ten

basic steps, which lead the entire protocol of the SLR. Fundamentally, this process of SLR is

acquiring each aspect of research such as journal, articles, Coder Triangulation, Code papers

Page

10

Figure 1: structured Literature Review’s Protocol

Through an overview of the above Figure 1, it has been identified that the there are ten

basic steps, which lead the entire protocol of the SLR. Fundamentally, this process of SLR is

acquiring each aspect of research such as journal, articles, Coder Triangulation, Code papers

Page

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING THEORY AND CURRENT ISSUES

(QDAS and NVivo), and scope. Hence, through the process of SLR, an organization can be

made aware regarding the potential issues relating to accounting (De Villiers & Dumay,

2013). Based on the entire research, certain issues of accounting include improper

budgeting, lack of auditing, unskilled financial employees, and whistleblowing before the

time among others. These can affect the operations of the organization reasonably. Thus,

due to these reasons, SLR is helping to overcome the issues in a decent manner. By

implementing appropriate SLR technique, an organization can easily develop its financial

efficiency and effectiveness. Apart from this, the research also reflects different scenario

relating to accountability changes through SLR (Flower, 2015).

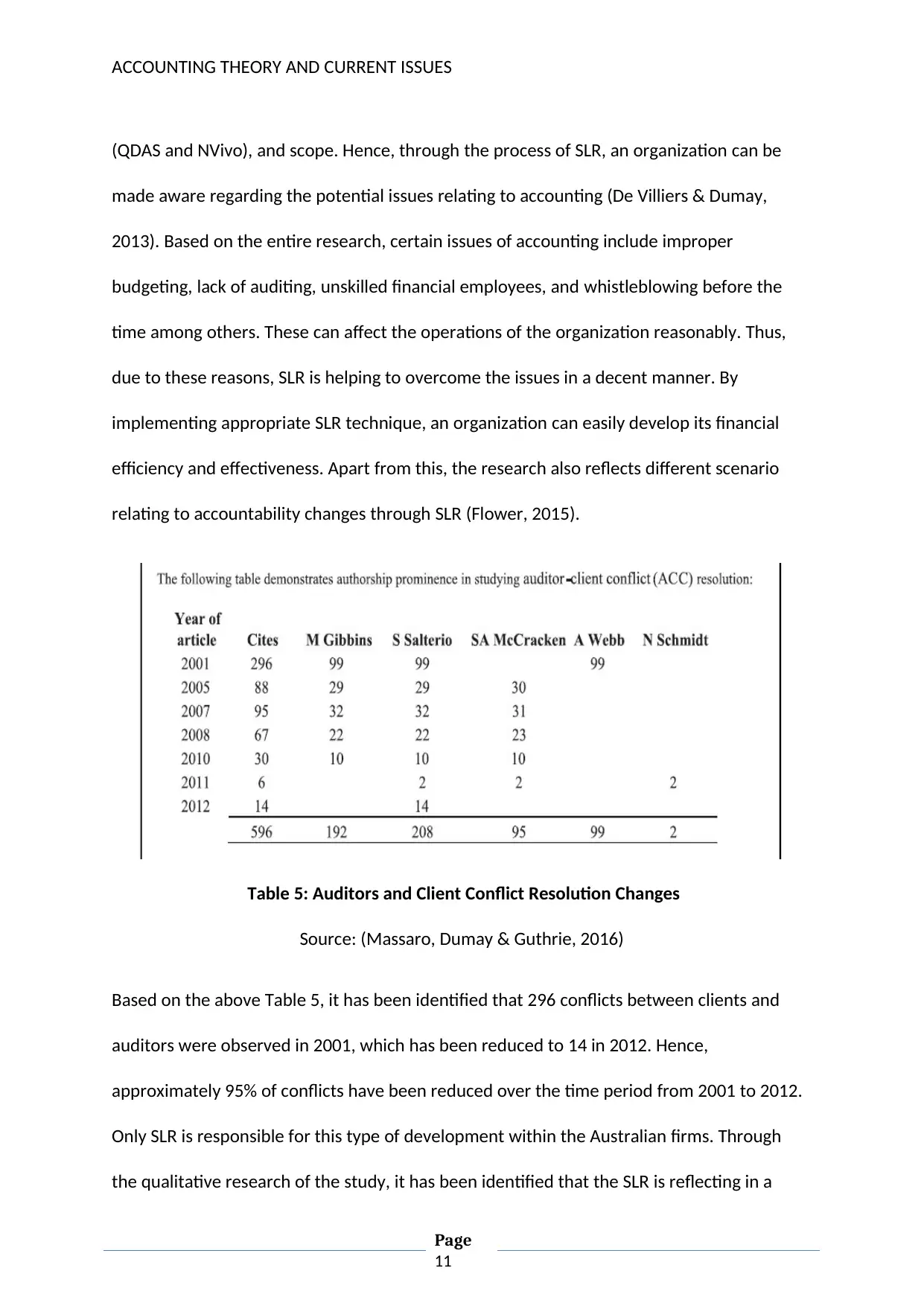

Table 5: Auditors and Client Conflict Resolution Changes

Source: (Massaro, Dumay & Guthrie, 2016)

Based on the above Table 5, it has been identified that 296 conflicts between clients and

auditors were observed in 2001, which has been reduced to 14 in 2012. Hence,

approximately 95% of conflicts have been reduced over the time period from 2001 to 2012.

Only SLR is responsible for this type of development within the Australian firms. Through

the qualitative research of the study, it has been identified that the SLR is reflecting in a

Page

11

(QDAS and NVivo), and scope. Hence, through the process of SLR, an organization can be

made aware regarding the potential issues relating to accounting (De Villiers & Dumay,

2013). Based on the entire research, certain issues of accounting include improper

budgeting, lack of auditing, unskilled financial employees, and whistleblowing before the

time among others. These can affect the operations of the organization reasonably. Thus,

due to these reasons, SLR is helping to overcome the issues in a decent manner. By

implementing appropriate SLR technique, an organization can easily develop its financial

efficiency and effectiveness. Apart from this, the research also reflects different scenario

relating to accountability changes through SLR (Flower, 2015).

Table 5: Auditors and Client Conflict Resolution Changes

Source: (Massaro, Dumay & Guthrie, 2016)

Based on the above Table 5, it has been identified that 296 conflicts between clients and

auditors were observed in 2001, which has been reduced to 14 in 2012. Hence,

approximately 95% of conflicts have been reduced over the time period from 2001 to 2012.

Only SLR is responsible for this type of development within the Australian firms. Through

the qualitative research of the study, it has been identified that the SLR is reflecting in a

Page

11

ACCOUNTING THEORY AND CURRENT ISSUES

different way. In addition, SLR is developing and creating knowledge ground, whereas the

organization is developing its financial implications. At the same time, researchers have

stated that SLR has been establishing a new journey for an organization. Through this, an

organization is resolving internal issues related to the accountability (Chenhall & Smith,

2011).

Conclusion

From the study, it has been identified that the financial theories and its implication plays a

major role within the Australian organizations. Thus, it can further be inferred that the

process SLR and accounting management along with organization are facing issues and

internal problems regarding the accountability and its implications within the Australian

firms.

Page

12

different way. In addition, SLR is developing and creating knowledge ground, whereas the

organization is developing its financial implications. At the same time, researchers have

stated that SLR has been establishing a new journey for an organization. Through this, an

organization is resolving internal issues related to the accountability (Chenhall & Smith,

2011).

Conclusion

From the study, it has been identified that the financial theories and its implication plays a

major role within the Australian organizations. Thus, it can further be inferred that the

process SLR and accounting management along with organization are facing issues and

internal problems regarding the accountability and its implications within the Australian

firms.

Page

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.