Accounting Theory: Stakeholder Impact on Financial Reports (HI6025)

VerifiedAdded on 2023/06/03

|11

|2167

|145

Report

AI Summary

This report examines the significance of accounting theories and their relevance to companies, particularly in the context of financial reporting. It compares and interprets two journal articles, revealing the implications of these theories on external stakeholders. The analysis covers the role of accounting theory in developing accounting principles and the measurements of accounting conservatism in research-intensive industries. Key findings highlight the importance of clear accounting theories for accountants in Australian companies, the role of accounting regulators in developing valid accounting principles, and how stakeholders can better understand organizations' financial reports. The report concludes by emphasizing the crucial role of accounting theory in generating financial reports and its impact on external stakeholders.

Accounting Theory and Current Issues

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Executive Summary

This report reflects the importance of accounting theories, how they are relevant to the

companies and what are their importance in financial reports. Two journal articles were chosen

to compare and interpret the above facts. It can be derived from the findings of the two articles

that these theories have different kinds of implications on external stake holders, these findings

have been discussed in details in this report. Thus, from the above findings of the article

significance and relevance of accounting theory can be learnt.

2

This report reflects the importance of accounting theories, how they are relevant to the

companies and what are their importance in financial reports. Two journal articles were chosen

to compare and interpret the above facts. It can be derived from the findings of the two articles

that these theories have different kinds of implications on external stake holders, these findings

have been discussed in details in this report. Thus, from the above findings of the article

significance and relevance of accounting theory can be learnt.

2

Table of Contents

Introduction......................................................................................................................................4

a. An explanation of the reasons (at least 3) why our group has selected these two research

articles relating to our topic.............................................................................................................5

b. An explanation of the purpose of the two studies and what research question(s) they set out to

explore about the topic.....................................................................................................................6

c. A discussion about the similarities and differences in the findings of the two studies...............7

d. For each of the two studies, provide two (2) major implications of their research findings that

will be useful to inform each of the three external reporting stakeholders below...........................8

i) Accountants in Australian companies......................................................................................8

ii) Accounting regulators.............................................................................................................8

iii) Stakeholders...........................................................................................................................9

Conclusion.....................................................................................................................................10

References......................................................................................................................................11

3

Introduction......................................................................................................................................4

a. An explanation of the reasons (at least 3) why our group has selected these two research

articles relating to our topic.............................................................................................................5

b. An explanation of the purpose of the two studies and what research question(s) they set out to

explore about the topic.....................................................................................................................6

c. A discussion about the similarities and differences in the findings of the two studies...............7

d. For each of the two studies, provide two (2) major implications of their research findings that

will be useful to inform each of the three external reporting stakeholders below...........................8

i) Accountants in Australian companies......................................................................................8

ii) Accounting regulators.............................................................................................................8

iii) Stakeholders...........................................................................................................................9

Conclusion.....................................................................................................................................10

References......................................................................................................................................11

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Introduction

Accounting is the most crucial part for any business. However, when it comes to accounts of an

organization, one need to have good knowledge about the various theories related to accounting

(Wang, 2015). The theory of accounting can be defined as a set of framework, methodologies or

an assumption used for the application and study of the principles in financial reporting work.

Information about the economic affairs of an organization about their finances is provided in the

report that will be helpful in decision making for the interested parties. This shows the

importance of accounting theory in the preparation of financial reports for a company. Two very

diverse journals have been used to conduct this study and prepare this report. An evaluation of

the questions raised by the journals and its purpose is given in the report. Three specific research

findings from this article have been taken in consideration, and a detail analysis is been done on

the implications of these outcomes, these three stakeholders reporting externally are –Australian

companies accountants, shareholders and accounting regulators.

4

Accounting is the most crucial part for any business. However, when it comes to accounts of an

organization, one need to have good knowledge about the various theories related to accounting

(Wang, 2015). The theory of accounting can be defined as a set of framework, methodologies or

an assumption used for the application and study of the principles in financial reporting work.

Information about the economic affairs of an organization about their finances is provided in the

report that will be helpful in decision making for the interested parties. This shows the

importance of accounting theory in the preparation of financial reports for a company. Two very

diverse journals have been used to conduct this study and prepare this report. An evaluation of

the questions raised by the journals and its purpose is given in the report. Three specific research

findings from this article have been taken in consideration, and a detail analysis is been done on

the implications of these outcomes, these three stakeholders reporting externally are –Australian

companies accountants, shareholders and accounting regulators.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

a. An explanation of the reasons (at least 3) why our group has selected these two research

articles relating to our topic

Accounting theory is considered to be of great importance (Gaffikin & Aitken, 2014). This

report has been prepared based on the two journal articles selected, these articles are “The role of

accounting theory in the development of accounting principles” by D Coetsee (2010) and the

second one is “Measurements of Accounting Conservatism in Research Intensive Industries from

Different Financial Reporting Settings”, by Philip Rickard (2016). The theory of accounting can

be justified by these two articles selected. The selection of these two journal article was based on

various factors.

Important factors for selection of the article “The role of accounting theory in the development

of accounting principles” is:

This article focus on the developments made in accounting theory based on normative

and descriptive approach.

This article will help to develop more knowledge on the role of accounting theories and

its importance in accounting principles development to prepare financial reports.

It also give emphasis on the determination of role played by the decision making theory

in accounting to create accounting principles.

In addition, the three important points for the selection of article “Measurements of Accounting

Conservatism in Research Intensive Industries from Different Financial Reporting Settings” is:

This particular journal helped in the understanding and preparation of assessments those

are to be conducted to assess the research-intensive type of industry for accounting

conservatism.

This journal helped to give a basic idea of accounting conservatism, which is considered

to be very important theory of accounting.

This journal also give an idea that with respect to research-intensive industries, financial

reporting is considered less conservative, and this idea have arrived because of the

differences in the approach of Local GAAP’s (Generally Accepted Accounting

Principles) and IFRS (International Financial Reporting Standards).

5

articles relating to our topic

Accounting theory is considered to be of great importance (Gaffikin & Aitken, 2014). This

report has been prepared based on the two journal articles selected, these articles are “The role of

accounting theory in the development of accounting principles” by D Coetsee (2010) and the

second one is “Measurements of Accounting Conservatism in Research Intensive Industries from

Different Financial Reporting Settings”, by Philip Rickard (2016). The theory of accounting can

be justified by these two articles selected. The selection of these two journal article was based on

various factors.

Important factors for selection of the article “The role of accounting theory in the development

of accounting principles” is:

This article focus on the developments made in accounting theory based on normative

and descriptive approach.

This article will help to develop more knowledge on the role of accounting theories and

its importance in accounting principles development to prepare financial reports.

It also give emphasis on the determination of role played by the decision making theory

in accounting to create accounting principles.

In addition, the three important points for the selection of article “Measurements of Accounting

Conservatism in Research Intensive Industries from Different Financial Reporting Settings” is:

This particular journal helped in the understanding and preparation of assessments those

are to be conducted to assess the research-intensive type of industry for accounting

conservatism.

This journal helped to give a basic idea of accounting conservatism, which is considered

to be very important theory of accounting.

This journal also give an idea that with respect to research-intensive industries, financial

reporting is considered less conservative, and this idea have arrived because of the

differences in the approach of Local GAAP’s (Generally Accepted Accounting

Principles) and IFRS (International Financial Reporting Standards).

5

b. An explanation of the purpose of the two studies and what research question(s) they set

out to explore about the topic

The purpose for considering the two studies has been stated in this report. The objective of the

journal “The role of accounting theory in the development of accounting principles” has been

given below:

To find out important developments that has directed an impact on the recent status of

accounting theory.

To find out the developments responsible for a positive theory in accounting.

Determining the second outcome of accounting theory that is decision usefulness.

Determining the development and nature of accounting theory.

To determine various other developments taking part in imperative and critical research

account research.

The research questions that can be deduced from the journal article for future research in the

field are stated below:

How the development taken from the articles does helps in the development of the

principles of accounting in accordance with the research medium or in the research gap

and accounts practices that continues to widen?

Other than the accounting research, what other factors are present, which contributes to

the existence and development of strong principles for accounting that creates an impact

on financial reports?

On the other side, the article written by Philip Rickard is taken into consideration for the

following reason:

To determine the idea behind conservative context about the intensive-research industry

have which has arrived because of the differences in the approach of Local GAAP’s

(Generally Accepted Accounting Principles) and IFRS (International Financial

Reporting Standards).

To provide a comparative and quantitative design of research which will feature the

conservatism means of accounting by using financial measurement as a medium, which

will follow a professional structure.

6

out to explore about the topic

The purpose for considering the two studies has been stated in this report. The objective of the

journal “The role of accounting theory in the development of accounting principles” has been

given below:

To find out important developments that has directed an impact on the recent status of

accounting theory.

To find out the developments responsible for a positive theory in accounting.

Determining the second outcome of accounting theory that is decision usefulness.

Determining the development and nature of accounting theory.

To determine various other developments taking part in imperative and critical research

account research.

The research questions that can be deduced from the journal article for future research in the

field are stated below:

How the development taken from the articles does helps in the development of the

principles of accounting in accordance with the research medium or in the research gap

and accounts practices that continues to widen?

Other than the accounting research, what other factors are present, which contributes to

the existence and development of strong principles for accounting that creates an impact

on financial reports?

On the other side, the article written by Philip Rickard is taken into consideration for the

following reason:

To determine the idea behind conservative context about the intensive-research industry

have which has arrived because of the differences in the approach of Local GAAP’s

(Generally Accepted Accounting Principles) and IFRS (International Financial

Reporting Standards).

To provide a comparative and quantitative design of research which will feature the

conservatism means of accounting by using financial measurement as a medium, which

will follow a professional structure.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

To guide the creditors, auditors, investors, corporate managers and regulators those come

under conservatism accounting. The understanding and preparation of assessments those

are to be conducted to assess the research-intensive type of industry for accounting

conservatism for financial reports.

The research questions that can be deduced from the journal article for future research in the

field are stated below:

Excluding the research-intensive industries, how can the financial reports produced can

be less conservative?

How will the creditors, auditors, investors, corporate managers and regulators will be

affected by conservatism in accounting?

c. A discussion about the similarities and differences in the findings of the two studies

On studying and analyzing both the journals in this report, it can be seen that both the articles

written by Philip Rickard and D Coetsee, have certain similarities and some dissimilarities or

clash in opinions. Below are given the similarities between the two articles:

These two journals are based on same topic that is accounting theory. Both the articles

shows how relevant is accounting theory, and they have also stated the various

developments done in these theories.

These two journal articles are written keeping in mind the influence and effect of

accounting theory on financial reports of an organization. Moreover, they have also

reported how these accounting tools can be used to develop and prepare financial reports

for any kind of industries.

Following table shows the differences between the outcomes and findings of the two journals

selected for this report.

Journal written by D Coetsee Journal written by Philip Rickard

7

under conservatism accounting. The understanding and preparation of assessments those

are to be conducted to assess the research-intensive type of industry for accounting

conservatism for financial reports.

The research questions that can be deduced from the journal article for future research in the

field are stated below:

Excluding the research-intensive industries, how can the financial reports produced can

be less conservative?

How will the creditors, auditors, investors, corporate managers and regulators will be

affected by conservatism in accounting?

c. A discussion about the similarities and differences in the findings of the two studies

On studying and analyzing both the journals in this report, it can be seen that both the articles

written by Philip Rickard and D Coetsee, have certain similarities and some dissimilarities or

clash in opinions. Below are given the similarities between the two articles:

These two journals are based on same topic that is accounting theory. Both the articles

shows how relevant is accounting theory, and they have also stated the various

developments done in these theories.

These two journal articles are written keeping in mind the influence and effect of

accounting theory on financial reports of an organization. Moreover, they have also

reported how these accounting tools can be used to develop and prepare financial reports

for any kind of industries.

Following table shows the differences between the outcomes and findings of the two journals

selected for this report.

Journal written by D Coetsee Journal written by Philip Rickard

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

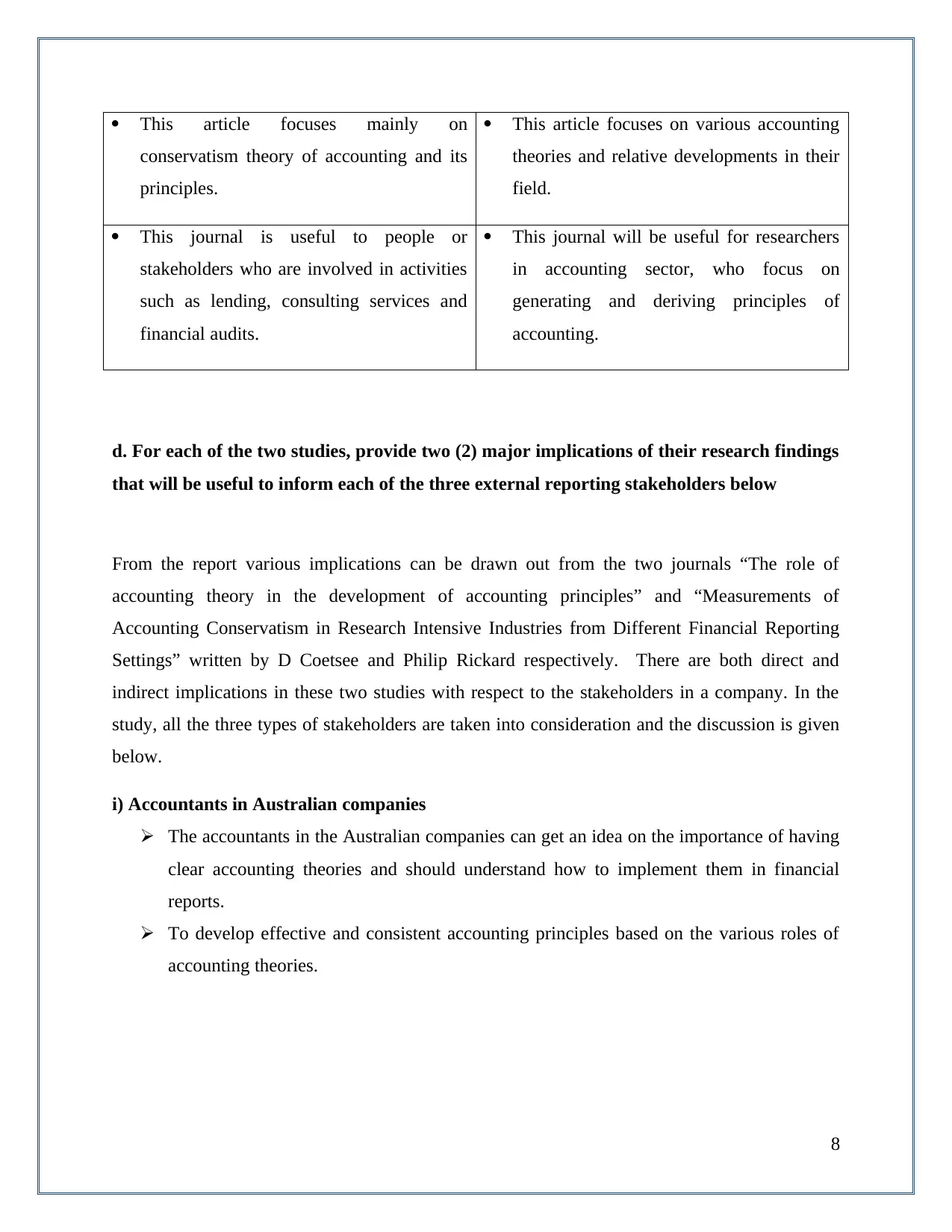

This article focuses mainly on

conservatism theory of accounting and its

principles.

This article focuses on various accounting

theories and relative developments in their

field.

This journal is useful to people or

stakeholders who are involved in activities

such as lending, consulting services and

financial audits.

This journal will be useful for researchers

in accounting sector, who focus on

generating and deriving principles of

accounting.

d. For each of the two studies, provide two (2) major implications of their research findings

that will be useful to inform each of the three external reporting stakeholders below

From the report various implications can be drawn out from the two journals “The role of

accounting theory in the development of accounting principles” and “Measurements of

Accounting Conservatism in Research Intensive Industries from Different Financial Reporting

Settings” written by D Coetsee and Philip Rickard respectively. There are both direct and

indirect implications in these two studies with respect to the stakeholders in a company. In the

study, all the three types of stakeholders are taken into consideration and the discussion is given

below.

i) Accountants in Australian companies

The accountants in the Australian companies can get an idea on the importance of having

clear accounting theories and should understand how to implement them in financial

reports.

To develop effective and consistent accounting principles based on the various roles of

accounting theories.

8

conservatism theory of accounting and its

principles.

This article focuses on various accounting

theories and relative developments in their

field.

This journal is useful to people or

stakeholders who are involved in activities

such as lending, consulting services and

financial audits.

This journal will be useful for researchers

in accounting sector, who focus on

generating and deriving principles of

accounting.

d. For each of the two studies, provide two (2) major implications of their research findings

that will be useful to inform each of the three external reporting stakeholders below

From the report various implications can be drawn out from the two journals “The role of

accounting theory in the development of accounting principles” and “Measurements of

Accounting Conservatism in Research Intensive Industries from Different Financial Reporting

Settings” written by D Coetsee and Philip Rickard respectively. There are both direct and

indirect implications in these two studies with respect to the stakeholders in a company. In the

study, all the three types of stakeholders are taken into consideration and the discussion is given

below.

i) Accountants in Australian companies

The accountants in the Australian companies can get an idea on the importance of having

clear accounting theories and should understand how to implement them in financial

reports.

To develop effective and consistent accounting principles based on the various roles of

accounting theories.

8

ii) Accounting regulators

Accounting regulators can determine how to conduct research depending on accounting

theories so that they can be able to develop valid accounting principles. These principles

can be used to further develop financial reports for the organization.

This study also takes in account the various levels of conservatism existing in terms of

preparing financial reports following accounting theories in different industries like the

intensive-research based industries.

iii) Stakeholders

From the given journals, stakeholders can get an understanding of the organizations

financial reports were they have invested. It also takes in account how accounting

theories affect their role in an organization.

They can analyse the financial reports of the company they have invested taking in view

the various accounting laws.

9

Accounting regulators can determine how to conduct research depending on accounting

theories so that they can be able to develop valid accounting principles. These principles

can be used to further develop financial reports for the organization.

This study also takes in account the various levels of conservatism existing in terms of

preparing financial reports following accounting theories in different industries like the

intensive-research based industries.

iii) Stakeholders

From the given journals, stakeholders can get an understanding of the organizations

financial reports were they have invested. It also takes in account how accounting

theories affect their role in an organization.

They can analyse the financial reports of the company they have invested taking in view

the various accounting laws.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Conclusion

On studying and analyzing both the journal articles in this report, a very useful data was

obtained. It gave an insight into the various types of accounting theory from various prospective.

It also gives the significance of the theory. From the comparison of the two journals one can

understand and conclude the functions of accounting theory and understand the important role it

plays in the generation of financial reports for any organization. The end part of the study

revolves around the concept of clients and stakeholders involved, and how accounting theories

affect their role in an organization. They get an idea as to how these accounting theories can be

implemented to prepare financial reports for their organization. The article also reflects on the

impact it produce on the external stakeholders.

10

On studying and analyzing both the journal articles in this report, a very useful data was

obtained. It gave an insight into the various types of accounting theory from various prospective.

It also gives the significance of the theory. From the comparison of the two journals one can

understand and conclude the functions of accounting theory and understand the important role it

plays in the generation of financial reports for any organization. The end part of the study

revolves around the concept of clients and stakeholders involved, and how accounting theories

affect their role in an organization. They get an idea as to how these accounting theories can be

implemented to prepare financial reports for their organization. The article also reflects on the

impact it produce on the external stakeholders.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

References

Rickard, P. K. (2016). Measurements of accounting conservatism in research intensive industries

from different financial reporting settings (Order No. 10118783). Available from Business

Premium Collection. (1805060679). Retrieved from

https://search.proquest.com/docview/1805060679?accountid=30552

Coetsee, D. (2010). The role of accounting theory in the development of accounting

principles. Meditari Accountancy Research, 18(1), 1-16.

doi:http://dx.doi.org/10.1108/10222529201000001

Vollmer, H. (2018). Accounting for tacit coordination: The passing of accounts and the broader

case for accounting theory. Accounting, Organizations and Society.

Downey, D. H., & Bedard, J. C. (2018). Coordination and communication challenges in global

group audits. Auditing: A Journal of Practice and Theory.

Leong, R. (2015). Structuring an undergraduate accounting theory course to enhance the learning

experience of Australian students: Preliminary findings.

Gaffikin, M., & Aitken, M. (Eds.). (2014). The Development of Accounting Theory (RLE

Accounting): Significant Contributors to Accounting Thought in the 20th Century. Routledge.

Glöckner, A. (2016). New development: The protective role of conservatism in public sector

accounting. Public Money & Management, 36(7), 527-530.

11

Rickard, P. K. (2016). Measurements of accounting conservatism in research intensive industries

from different financial reporting settings (Order No. 10118783). Available from Business

Premium Collection. (1805060679). Retrieved from

https://search.proquest.com/docview/1805060679?accountid=30552

Coetsee, D. (2010). The role of accounting theory in the development of accounting

principles. Meditari Accountancy Research, 18(1), 1-16.

doi:http://dx.doi.org/10.1108/10222529201000001

Vollmer, H. (2018). Accounting for tacit coordination: The passing of accounts and the broader

case for accounting theory. Accounting, Organizations and Society.

Downey, D. H., & Bedard, J. C. (2018). Coordination and communication challenges in global

group audits. Auditing: A Journal of Practice and Theory.

Leong, R. (2015). Structuring an undergraduate accounting theory course to enhance the learning

experience of Australian students: Preliminary findings.

Gaffikin, M., & Aitken, M. (Eds.). (2014). The Development of Accounting Theory (RLE

Accounting): Significant Contributors to Accounting Thought in the 20th Century. Routledge.

Glöckner, A. (2016). New development: The protective role of conservatism in public sector

accounting. Public Money & Management, 36(7), 527-530.

11

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.