ACCT20074 Contemporary Accounting Theory: Framework & Reporting

VerifiedAdded on 2023/03/31

|14

|3538

|172

Report

AI Summary

This report provides an analysis of contemporary accounting theory, evaluating the conceptual framework and sustainability reporting. It uses data from a South African company and Australian companies, including an integrated report table for one Australian company. The report examines the historical development of the conceptual framework in the USA, UK, Australia, and globally under IASB, discussing concerns about its application in Australia and its benefits and limitations. It also compares GRI and IIRC reporting guidelines, assesses the strengths and limitations of conventional accounting, and explores the applicability of theories to explain sustainability and integrated reports. The analysis includes a comparison of Australian and South African companies' reporting practices.

Running Head: ACCOUNTING THEORY 1

Accounting Theory

Student’s Name

Institutional Affiliation

Accounting Theory

Student’s Name

Institutional Affiliation

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING THEORY 2

Accounting Theory

Executive Summary

This report provides an assays of different parts in the contemporary accounting theory, it

evaluates conceptual framework and sustainability. It uses data from the South Africa Company

and other companies that are located in Australia. Also, it provides a table integrated report of

one of the companies in Australia. Therefore, the purpose of the report is to analyze in details the

conceptual framework and the sustainability that occurs in the accounting field.

Introduction

Accounting theory is a set of framework assumptions and methodologies that are used in

the development, study, and application of the financial reporting principles. It more so involves

the review of practices, the historical foundation of accounting and the way these methods are

changing over time (Accounting Standards Board, 1999). Therefore, there is a need to study

what needs to be changed or added to the framework that governs and regulate the financial

reporting and financial information so as to be at par with the contemporary accounting theory.

Hence the following assessment is research and report of several aspects of the business

external report practices. It has the two parts which are part A and B. the first part talks about the

conceptual framework. The framework encourage the evaluation and development of existing

and new standards. Therefore, the paper is going to analyze the historical development of the

conceptual framework in various countries. Moreover, it’s going to discuss the professor's

concern about the application of the conceptual framework in Australia under IASB. Also, the

benefit and the limitation that entails the framework in academic fields. Finally, it will analyze

the application of this conceptual framework in several companies in Australia.

Accounting Theory

Executive Summary

This report provides an assays of different parts in the contemporary accounting theory, it

evaluates conceptual framework and sustainability. It uses data from the South Africa Company

and other companies that are located in Australia. Also, it provides a table integrated report of

one of the companies in Australia. Therefore, the purpose of the report is to analyze in details the

conceptual framework and the sustainability that occurs in the accounting field.

Introduction

Accounting theory is a set of framework assumptions and methodologies that are used in

the development, study, and application of the financial reporting principles. It more so involves

the review of practices, the historical foundation of accounting and the way these methods are

changing over time (Accounting Standards Board, 1999). Therefore, there is a need to study

what needs to be changed or added to the framework that governs and regulate the financial

reporting and financial information so as to be at par with the contemporary accounting theory.

Hence the following assessment is research and report of several aspects of the business

external report practices. It has the two parts which are part A and B. the first part talks about the

conceptual framework. The framework encourage the evaluation and development of existing

and new standards. Therefore, the paper is going to analyze the historical development of the

conceptual framework in various countries. Moreover, it’s going to discuss the professor's

concern about the application of the conceptual framework in Australia under IASB. Also, the

benefit and the limitation that entails the framework in academic fields. Finally, it will analyze

the application of this conceptual framework in several companies in Australia.

ACCOUNTING THEORY 3

The part B of the paper is going to evaluate integrated or sustainability reporting. The

research paper is going to analyze the Comparison of Reporting Guidelines GRI and IIRC. Also,

the strengths and limitations of conventional accounting. Moreover, it will discuss the

Applicability of the theories to explain the contents of sustainability as well as integrated reports.

Prepare an index table of various components of an integrated report. More so, develop a

comparison of the Australian company’s reporting practices with the index and the integrated

reporting practices in the selected South African company.

Part A

a) History and development of the conceptual framework.

Conceptual framework is regarded to as system of objectives which leads to the

generation of consistent accounting set standards. Since its inception in 1989, the conceptual

framework has largely remained unchanged. More so, this was the time that the financial stamen

preparation and the presentation were accepted by the International Accounting Standard

Committee board. Globally the conceptual framework has undergone through various stages, in

July 1989, it was the time which the framework was published. IASB further adopted the

conceptual framework and in 2010, IASB passed the conceptual framework for financial

Reporting. Also, in March 2018, was the time where the framework was published.

The institutional effort for the USA to start and develop the Business Corporation

framework which can be traced from in 1940 by work of Littleton and Paton monograph. It was

later followed studies done by Sprouse and Moonitz in attempt to develop accounting literature

which was laid out by Patron William. Australian accounting research foundation (AARF) and

the Australian Accounting Standard Board (AASB) developed the conceptual framework for

Australia over the period of 1985-1995. The main objective of the conceptual framework was to

The part B of the paper is going to evaluate integrated or sustainability reporting. The

research paper is going to analyze the Comparison of Reporting Guidelines GRI and IIRC. Also,

the strengths and limitations of conventional accounting. Moreover, it will discuss the

Applicability of the theories to explain the contents of sustainability as well as integrated reports.

Prepare an index table of various components of an integrated report. More so, develop a

comparison of the Australian company’s reporting practices with the index and the integrated

reporting practices in the selected South African company.

Part A

a) History and development of the conceptual framework.

Conceptual framework is regarded to as system of objectives which leads to the

generation of consistent accounting set standards. Since its inception in 1989, the conceptual

framework has largely remained unchanged. More so, this was the time that the financial stamen

preparation and the presentation were accepted by the International Accounting Standard

Committee board. Globally the conceptual framework has undergone through various stages, in

July 1989, it was the time which the framework was published. IASB further adopted the

conceptual framework and in 2010, IASB passed the conceptual framework for financial

Reporting. Also, in March 2018, was the time where the framework was published.

The institutional effort for the USA to start and develop the Business Corporation

framework which can be traced from in 1940 by work of Littleton and Paton monograph. It was

later followed studies done by Sprouse and Moonitz in attempt to develop accounting literature

which was laid out by Patron William. Australian accounting research foundation (AARF) and

the Australian Accounting Standard Board (AASB) developed the conceptual framework for

Australia over the period of 1985-1995. The main objective of the conceptual framework was to

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ACCOUNTING THEORY 4

provide a set related concept that defines the subject, nature, purpose and broad base of

understanding financial reporting and give a unique rendition on the thinking that governs the set

standards. IASB adopt the framework in 2001, the framework describes the basic concept of how

financial statement can be prepared. Therefore the adoption of IASB standard in Australia

reviewed the conceptual framework to ensure that the framework fulfills its function when

AASB gives out standards that are based on IFRS (Mosso, 1998). Moreover, they check whether

the framework has been changed to meet the changed circumstances in the Australian setting.

The conceptual framework in the United Kingdom over a few years has been based on the rules-

based, as opposed to the principle-based system as set by the ASB standard. However as time

goes by the nation has been adopting the principle base standard which is been used by another

country such as Canada, USA, and Australia. In 1999, the country formed its own conceptual

framework base on the stated principle that was issued by the Accounting standard board (ASB)

(Solomon, et al., 2000). The move was very essential due to the increase due to the increasing

international needs for accounting and more so the influence that the nation received in term of

globalization from countries such as the USA.

b) Australian professors concern about the application of the conceptual framework

In 2010, as part of the joint mission with FASB, IASB gave out two chapters of the

revised conceptual framework that they would like to amend in the standards that were already

set. The chapter deal with the general objective of the purpose of the financial reporting and the

useful information and the quantitative characteristics that the report must include. However, in

2012, IASB decided to restart the work of the conceptual framework so that they can reconsider

making changes in these chapters (Financial Accounting Standards Board, 2004). The decision

aroused concerns in the accounting profession and more IASB considers and proposes new rules

provide a set related concept that defines the subject, nature, purpose and broad base of

understanding financial reporting and give a unique rendition on the thinking that governs the set

standards. IASB adopt the framework in 2001, the framework describes the basic concept of how

financial statement can be prepared. Therefore the adoption of IASB standard in Australia

reviewed the conceptual framework to ensure that the framework fulfills its function when

AASB gives out standards that are based on IFRS (Mosso, 1998). Moreover, they check whether

the framework has been changed to meet the changed circumstances in the Australian setting.

The conceptual framework in the United Kingdom over a few years has been based on the rules-

based, as opposed to the principle-based system as set by the ASB standard. However as time

goes by the nation has been adopting the principle base standard which is been used by another

country such as Canada, USA, and Australia. In 1999, the country formed its own conceptual

framework base on the stated principle that was issued by the Accounting standard board (ASB)

(Solomon, et al., 2000). The move was very essential due to the increase due to the increasing

international needs for accounting and more so the influence that the nation received in term of

globalization from countries such as the USA.

b) Australian professors concern about the application of the conceptual framework

In 2010, as part of the joint mission with FASB, IASB gave out two chapters of the

revised conceptual framework that they would like to amend in the standards that were already

set. The chapter deal with the general objective of the purpose of the financial reporting and the

useful information and the quantitative characteristics that the report must include. However, in

2012, IASB decided to restart the work of the conceptual framework so that they can reconsider

making changes in these chapters (Financial Accounting Standards Board, 2004). The decision

aroused concerns in the accounting profession and more IASB considers and proposes new rules

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING THEORY 5

of the application which includes; to provide more prominence in the discussion about the

objective of the financial reports so that it may include or provide important information that can

assess the organization management stewardship when it comes to the company resources.

Moreover, to reintroduce a unique reference on the notion of prudence and state importance of

prudence in achieving neutrality. Also, define explicitly that a faithful representation represents

the economic scenario substance in lieu of rather legal form.

However, the raised concern on this issue by the proffers still believe that IASB has not

yet covered all the purpose of the changes fully. They raised issues that since 2010, the

conceptual framework has no to identify reliability as a quantitative characteristic of useful

information. More so, their main concern seemed to be that of the measurement of uncertainty

that makes financial reporting and information to be less useful (International Accounting

Standards Board. 2004). Therefore, in response to this IASB proposed to clarify the

measurement of uncertainty and make it be one of the major factors in determining the relevance

of financial information and reporting. Additionally, the board retained the description of the

reliability in the existing conceptual framework as it contains quantitative characteristics of

faithful representation.

c) Benefit and limitation of the conceptual framework

Some of the academic concern about the benefit of the conceptual framework in the

financial report includes; development of the concept in an orderly manner that makes financial

reporting and accounting to be more consistent, logical and overall enhances communication in

it. Furthermore, developing of standards that are backed with the conceptual framework is more

economical and easier since it is based on the basic principles that are already discussed and put

in place hence the students are able to understand it easily. Additionally, the conceptual

of the application which includes; to provide more prominence in the discussion about the

objective of the financial reports so that it may include or provide important information that can

assess the organization management stewardship when it comes to the company resources.

Moreover, to reintroduce a unique reference on the notion of prudence and state importance of

prudence in achieving neutrality. Also, define explicitly that a faithful representation represents

the economic scenario substance in lieu of rather legal form.

However, the raised concern on this issue by the proffers still believe that IASB has not

yet covered all the purpose of the changes fully. They raised issues that since 2010, the

conceptual framework has no to identify reliability as a quantitative characteristic of useful

information. More so, their main concern seemed to be that of the measurement of uncertainty

that makes financial reporting and information to be less useful (International Accounting

Standards Board. 2004). Therefore, in response to this IASB proposed to clarify the

measurement of uncertainty and make it be one of the major factors in determining the relevance

of financial information and reporting. Additionally, the board retained the description of the

reliability in the existing conceptual framework as it contains quantitative characteristics of

faithful representation.

c) Benefit and limitation of the conceptual framework

Some of the academic concern about the benefit of the conceptual framework in the

financial report includes; development of the concept in an orderly manner that makes financial

reporting and accounting to be more consistent, logical and overall enhances communication in

it. Furthermore, developing of standards that are backed with the conceptual framework is more

economical and easier since it is based on the basic principles that are already discussed and put

in place hence the students are able to understand it easily. Additionally, the conceptual

ACCOUNTING THEORY 6

framework contributes to an increase in public confidence and credibility this is because of the

uniformity in the procedure and practices in all company that it is employed.

However, the framework consists of a number of limitation. One, it is too general in

nature also, the principle that encompasses it release majorly in a lot of assumption which is very

complicated for academic personnel to understand. Therefore, provides little help when it comes

to its application. Moreover, the framework tends to focus on the usefulness of the financial

information that is on it and it can never be used to assess factors such as the management

stewardship. More so, the user’s requirement such as shareholders and the investors are very

diverse, and for a student, it is very difficult to use the framework because of its inadequate in

the information provided and over generalization.

d) Application of conceptual framework in a selected Australian company.

The annual financial report of Suncorp Company was used in the report so as to discuss

how the conceptual framework is applied. It is a company that provides financial services and

solution, more so, they help the customer to make good choices so that they can enhance their

financial well-being. The company was listed in the Australian security exchange market as it

brings together a strong portfolio of banking and insurance and wealth solution from across all

the brands such as AAMI, Apia, Shannon, Suncorp as well as product from another partner.

Hence the director report and the financial statement of 2017-18 of Suncorp Company was used

in the report.

They were four statements or report that was prepared by the company. They include;

statement of financial position, statement of change in equity, cash flow statement and

comprehensive income. The report was prepared as per the conceptual framework. It is because

the financial statement helps in increasing the user confidence and understanding and make it

framework contributes to an increase in public confidence and credibility this is because of the

uniformity in the procedure and practices in all company that it is employed.

However, the framework consists of a number of limitation. One, it is too general in

nature also, the principle that encompasses it release majorly in a lot of assumption which is very

complicated for academic personnel to understand. Therefore, provides little help when it comes

to its application. Moreover, the framework tends to focus on the usefulness of the financial

information that is on it and it can never be used to assess factors such as the management

stewardship. More so, the user’s requirement such as shareholders and the investors are very

diverse, and for a student, it is very difficult to use the framework because of its inadequate in

the information provided and over generalization.

d) Application of conceptual framework in a selected Australian company.

The annual financial report of Suncorp Company was used in the report so as to discuss

how the conceptual framework is applied. It is a company that provides financial services and

solution, more so, they help the customer to make good choices so that they can enhance their

financial well-being. The company was listed in the Australian security exchange market as it

brings together a strong portfolio of banking and insurance and wealth solution from across all

the brands such as AAMI, Apia, Shannon, Suncorp as well as product from another partner.

Hence the director report and the financial statement of 2017-18 of Suncorp Company was used

in the report.

They were four statements or report that was prepared by the company. They include;

statement of financial position, statement of change in equity, cash flow statement and

comprehensive income. The report was prepared as per the conceptual framework. It is because

the financial statement helps in increasing the user confidence and understanding and make it

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ACCOUNTING THEORY 7

easier for the organization to be compared to another organization (FASB, 1980). The major

components that entail the financial reports of the company are that it provides the objective of

the financial reports of the organization, second, it has the qualitative characteristic of the

accounting information useful information. Third, the report has the element of financial

statement, recognition, and derecognition, measurement, presentation, and disclosure. Also, the

concepts of capital and capital maintenance.

The revenue recognition principle demands that an organization should record or realize

revenue at the moment it is earned. In other words, the business should not wait until all the

revenue has accumulated so that it can be recorded, therefore, the concept forms a key basis of

accruals in accounting. Their three principles of recognition. However, in the report, Suncorp

limited company has prepared consolidated financial statements using historical cost. Therefore

the company has used the revenue recognition principle that demands that revenue to be

recognized when cash has been actually received (In Bebbington, In Unerman, & In O'Dwyer,

2014). Moreover, the company has used asset recognition criteria where assets are being

included in the balance sheet and the expenditure are recognized as expense being the default

presumption. The liability of the company is recognized in the financial statement because they

have met the criteria of being a present obligation of the business that aroused from the past

event.

Qualitative characteristic of the financial reporting must contain the information that it is

very useful to the users, especially when it comes to the case of decision making. Therefore,

Suncorp limited company financial report has relevant financial information because it can

enable the organization management to make judgment, estimate, and assumption so that they

can come out with valid decision especially when it comes to recognition of revenue, asset, and

easier for the organization to be compared to another organization (FASB, 1980). The major

components that entail the financial reports of the company are that it provides the objective of

the financial reports of the organization, second, it has the qualitative characteristic of the

accounting information useful information. Third, the report has the element of financial

statement, recognition, and derecognition, measurement, presentation, and disclosure. Also, the

concepts of capital and capital maintenance.

The revenue recognition principle demands that an organization should record or realize

revenue at the moment it is earned. In other words, the business should not wait until all the

revenue has accumulated so that it can be recorded, therefore, the concept forms a key basis of

accruals in accounting. Their three principles of recognition. However, in the report, Suncorp

limited company has prepared consolidated financial statements using historical cost. Therefore

the company has used the revenue recognition principle that demands that revenue to be

recognized when cash has been actually received (In Bebbington, In Unerman, & In O'Dwyer,

2014). Moreover, the company has used asset recognition criteria where assets are being

included in the balance sheet and the expenditure are recognized as expense being the default

presumption. The liability of the company is recognized in the financial statement because they

have met the criteria of being a present obligation of the business that aroused from the past

event.

Qualitative characteristic of the financial reporting must contain the information that it is

very useful to the users, especially when it comes to the case of decision making. Therefore,

Suncorp limited company financial report has relevant financial information because it can

enable the organization management to make judgment, estimate, and assumption so that they

can come out with valid decision especially when it comes to recognition of revenue, asset, and

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING THEORY 8

liability (Miller, et al. 1998). Also, the company has a faithful representing this is because in its

financial reports they have use represents the economic phenomena both in numbers and in

words. More so, the company has sought to maximize the characteristic of neutrality,

completeness, and freedom of error by using faithful presentation. The financial report of

Suncor Company is represented in 2017 and in 2018, thus they enhance qualitative characteristic

by providing a means of comparability, timeliness, understandability, and verifiability of the

usefulness of the accounting information.

Part B

Sustainability

A) Comparison of Reporting Guidelines and the International Integrated Reporting

Framework

Global Reporting Initiative is an independent body whose objective is to develop and

disseminate report guidelines that are globally accepted to help businesses and organization to

report environmental, economic and social dimension of their services, product, and activities.

While, international integrated reporting council main objection is to create a globally accepted

framework, which will ease the process that results in communication by a business entity about

the value creation over time (Potter, 2005). Therefore the aim of IIRC is to bring together factor

represented from investment accounting, regulator, securities and academic standard sector in the

civil society. In 2010 there was the inception of GRI to IIRC, therefore, GRI has immensely

continued to participate to IIRC management bodies and also collaborate in the events where

IIRC advocated for a multi-stakeholder method of reporting financial information and material

sustainability (Roubini, Wachtel, & National Bureau of Economic Research, 1998). They share a

goal, which is to change the corporate reporting alignment, reporting framework and standards

liability (Miller, et al. 1998). Also, the company has a faithful representing this is because in its

financial reports they have use represents the economic phenomena both in numbers and in

words. More so, the company has sought to maximize the characteristic of neutrality,

completeness, and freedom of error by using faithful presentation. The financial report of

Suncor Company is represented in 2017 and in 2018, thus they enhance qualitative characteristic

by providing a means of comparability, timeliness, understandability, and verifiability of the

usefulness of the accounting information.

Part B

Sustainability

A) Comparison of Reporting Guidelines and the International Integrated Reporting

Framework

Global Reporting Initiative is an independent body whose objective is to develop and

disseminate report guidelines that are globally accepted to help businesses and organization to

report environmental, economic and social dimension of their services, product, and activities.

While, international integrated reporting council main objection is to create a globally accepted

framework, which will ease the process that results in communication by a business entity about

the value creation over time (Potter, 2005). Therefore the aim of IIRC is to bring together factor

represented from investment accounting, regulator, securities and academic standard sector in the

civil society. In 2010 there was the inception of GRI to IIRC, therefore, GRI has immensely

continued to participate to IIRC management bodies and also collaborate in the events where

IIRC advocated for a multi-stakeholder method of reporting financial information and material

sustainability (Roubini, Wachtel, & National Bureau of Economic Research, 1998). They share a

goal, which is to change the corporate reporting alignment, reporting framework and standards

ACCOUNTING THEORY 9

so that they can develop consistency in the application on the way which financial report is done

in the organization. Thus both organization is committed to identifying ways in corporate

reporting can be strengthened. More so, they provide guidelines that pro-actively communicate

the nature of the market, role, and alignment of each other framework, guidelines, and standards

so they can help in providing a better understanding of the corporate environment. Therefore

through working together, they can come up with ways that they can voice to guide the

organization on relevant information.

B) Rigour (strengths & limitations) of the conventional accounting

Conventional accounting minimizes the degree to which an individual may be influenced

by personal judgment. As it is based on the actual transaction, it provides information that is less

disputable as compared to another accounting system.

Data from this approach are free from bias and can be verified independently. Therefore, it is

easy to invest in public and other external entities. The financial statement can be verified easily

with the presence of a document or other supportive documents. Since it can be proved, account

expertise prefers the traditional method to other systems. Besides, the system can be accepted

by legal institutional as a way of defining legal capital, dividend declaration, and capital.

Furthermore, conventional accounting is supported basing on its legal acceptability in areas such

as declaration of dividend and taxation.

Weakness

The weakness of conventional accounting includes the unrealistic value of fixed assets.

Therefore, in time of inflation, the conventional system is based on historical cost data and does

not reflect the true and fair value of the business. Normally, a fixed asset is calculated using

historical cost but not the current value

so that they can develop consistency in the application on the way which financial report is done

in the organization. Thus both organization is committed to identifying ways in corporate

reporting can be strengthened. More so, they provide guidelines that pro-actively communicate

the nature of the market, role, and alignment of each other framework, guidelines, and standards

so they can help in providing a better understanding of the corporate environment. Therefore

through working together, they can come up with ways that they can voice to guide the

organization on relevant information.

B) Rigour (strengths & limitations) of the conventional accounting

Conventional accounting minimizes the degree to which an individual may be influenced

by personal judgment. As it is based on the actual transaction, it provides information that is less

disputable as compared to another accounting system.

Data from this approach are free from bias and can be verified independently. Therefore, it is

easy to invest in public and other external entities. The financial statement can be verified easily

with the presence of a document or other supportive documents. Since it can be proved, account

expertise prefers the traditional method to other systems. Besides, the system can be accepted

by legal institutional as a way of defining legal capital, dividend declaration, and capital.

Furthermore, conventional accounting is supported basing on its legal acceptability in areas such

as declaration of dividend and taxation.

Weakness

The weakness of conventional accounting includes the unrealistic value of fixed assets.

Therefore, in time of inflation, the conventional system is based on historical cost data and does

not reflect the true and fair value of the business. Normally, a fixed asset is calculated using

historical cost but not the current value

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ACCOUNTING THEORY 10

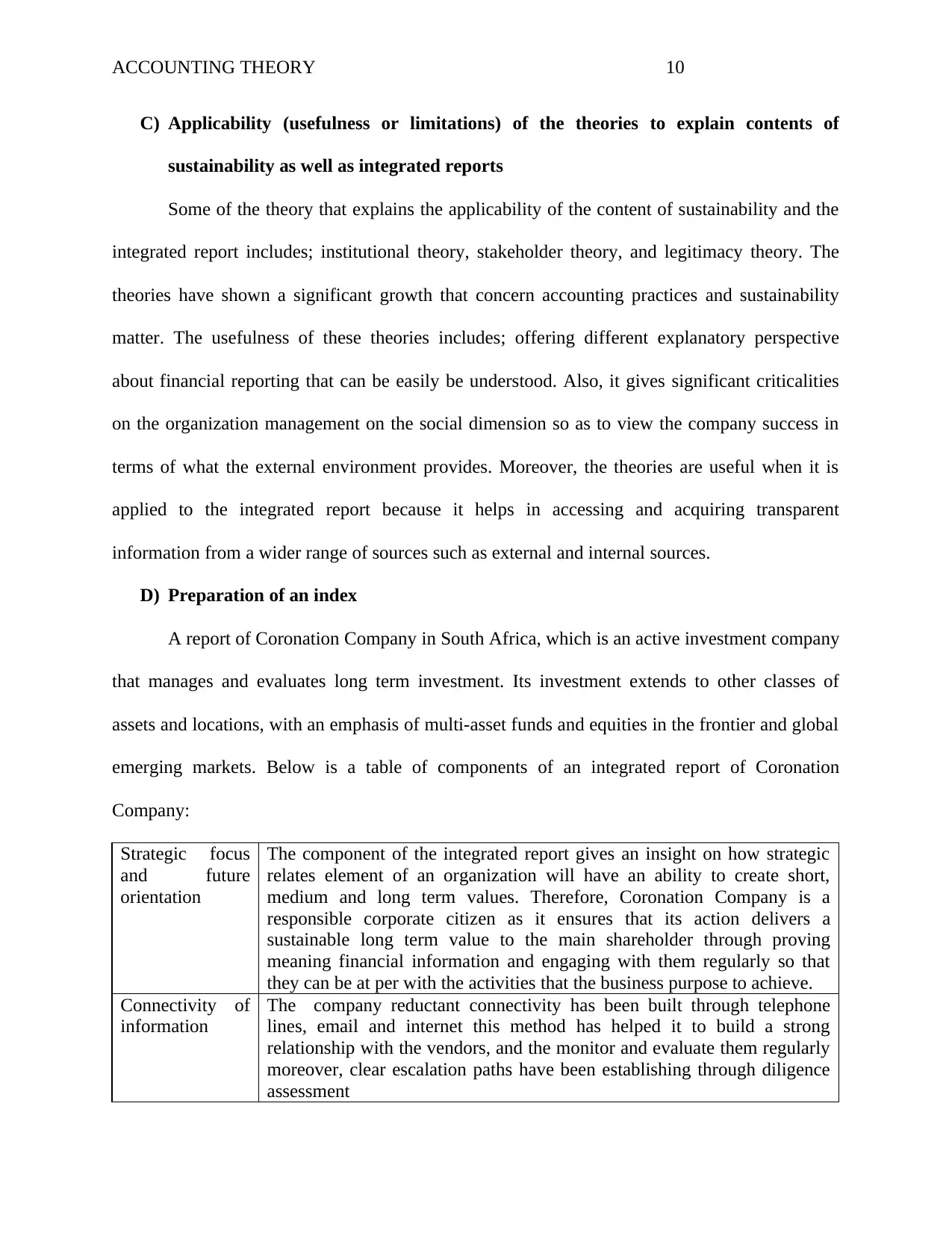

C) Applicability (usefulness or limitations) of the theories to explain contents of

sustainability as well as integrated reports

Some of the theory that explains the applicability of the content of sustainability and the

integrated report includes; institutional theory, stakeholder theory, and legitimacy theory. The

theories have shown a significant growth that concern accounting practices and sustainability

matter. The usefulness of these theories includes; offering different explanatory perspective

about financial reporting that can be easily be understood. Also, it gives significant criticalities

on the organization management on the social dimension so as to view the company success in

terms of what the external environment provides. Moreover, the theories are useful when it is

applied to the integrated report because it helps in accessing and acquiring transparent

information from a wider range of sources such as external and internal sources.

D) Preparation of an index

A report of Coronation Company in South Africa, which is an active investment company

that manages and evaluates long term investment. Its investment extends to other classes of

assets and locations, with an emphasis of multi-asset funds and equities in the frontier and global

emerging markets. Below is a table of components of an integrated report of Coronation

Company:

Strategic focus

and future

orientation

The component of the integrated report gives an insight on how strategic

relates element of an organization will have an ability to create short,

medium and long term values. Therefore, Coronation Company is a

responsible corporate citizen as it ensures that its action delivers a

sustainable long term value to the main shareholder through proving

meaning financial information and engaging with them regularly so that

they can be at per with the activities that the business purpose to achieve.

Connectivity of

information

The company reductant connectivity has been built through telephone

lines, email and internet this method has helped it to build a strong

relationship with the vendors, and the monitor and evaluate them regularly

moreover, clear escalation paths have been establishing through diligence

assessment

C) Applicability (usefulness or limitations) of the theories to explain contents of

sustainability as well as integrated reports

Some of the theory that explains the applicability of the content of sustainability and the

integrated report includes; institutional theory, stakeholder theory, and legitimacy theory. The

theories have shown a significant growth that concern accounting practices and sustainability

matter. The usefulness of these theories includes; offering different explanatory perspective

about financial reporting that can be easily be understood. Also, it gives significant criticalities

on the organization management on the social dimension so as to view the company success in

terms of what the external environment provides. Moreover, the theories are useful when it is

applied to the integrated report because it helps in accessing and acquiring transparent

information from a wider range of sources such as external and internal sources.

D) Preparation of an index

A report of Coronation Company in South Africa, which is an active investment company

that manages and evaluates long term investment. Its investment extends to other classes of

assets and locations, with an emphasis of multi-asset funds and equities in the frontier and global

emerging markets. Below is a table of components of an integrated report of Coronation

Company:

Strategic focus

and future

orientation

The component of the integrated report gives an insight on how strategic

relates element of an organization will have an ability to create short,

medium and long term values. Therefore, Coronation Company is a

responsible corporate citizen as it ensures that its action delivers a

sustainable long term value to the main shareholder through proving

meaning financial information and engaging with them regularly so that

they can be at per with the activities that the business purpose to achieve.

Connectivity of

information

The company reductant connectivity has been built through telephone

lines, email and internet this method has helped it to build a strong

relationship with the vendors, and the monitor and evaluate them regularly

moreover, clear escalation paths have been establishing through diligence

assessment

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING THEORY 11

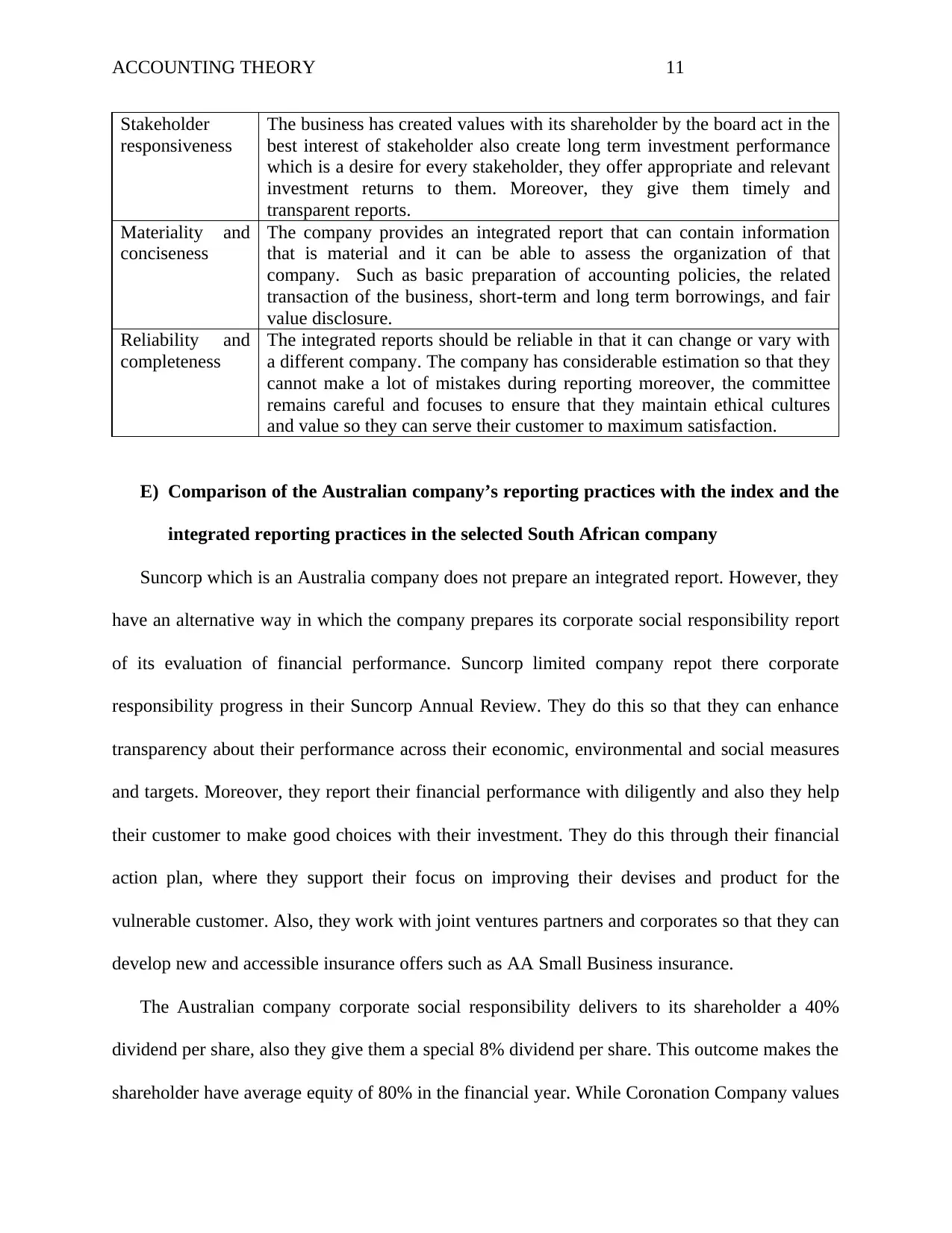

Stakeholder

responsiveness

The business has created values with its shareholder by the board act in the

best interest of stakeholder also create long term investment performance

which is a desire for every stakeholder, they offer appropriate and relevant

investment returns to them. Moreover, they give them timely and

transparent reports.

Materiality and

conciseness

The company provides an integrated report that can contain information

that is material and it can be able to assess the organization of that

company. Such as basic preparation of accounting policies, the related

transaction of the business, short-term and long term borrowings, and fair

value disclosure.

Reliability and

completeness

The integrated reports should be reliable in that it can change or vary with

a different company. The company has considerable estimation so that they

cannot make a lot of mistakes during reporting moreover, the committee

remains careful and focuses to ensure that they maintain ethical cultures

and value so they can serve their customer to maximum satisfaction.

E) Comparison of the Australian company’s reporting practices with the index and the

integrated reporting practices in the selected South African company

Suncorp which is an Australia company does not prepare an integrated report. However, they

have an alternative way in which the company prepares its corporate social responsibility report

of its evaluation of financial performance. Suncorp limited company repot there corporate

responsibility progress in their Suncorp Annual Review. They do this so that they can enhance

transparency about their performance across their economic, environmental and social measures

and targets. Moreover, they report their financial performance with diligently and also they help

their customer to make good choices with their investment. They do this through their financial

action plan, where they support their focus on improving their devises and product for the

vulnerable customer. Also, they work with joint ventures partners and corporates so that they can

develop new and accessible insurance offers such as AA Small Business insurance.

The Australian company corporate social responsibility delivers to its shareholder a 40%

dividend per share, also they give them a special 8% dividend per share. This outcome makes the

shareholder have average equity of 80% in the financial year. While Coronation Company values

Stakeholder

responsiveness

The business has created values with its shareholder by the board act in the

best interest of stakeholder also create long term investment performance

which is a desire for every stakeholder, they offer appropriate and relevant

investment returns to them. Moreover, they give them timely and

transparent reports.

Materiality and

conciseness

The company provides an integrated report that can contain information

that is material and it can be able to assess the organization of that

company. Such as basic preparation of accounting policies, the related

transaction of the business, short-term and long term borrowings, and fair

value disclosure.

Reliability and

completeness

The integrated reports should be reliable in that it can change or vary with

a different company. The company has considerable estimation so that they

cannot make a lot of mistakes during reporting moreover, the committee

remains careful and focuses to ensure that they maintain ethical cultures

and value so they can serve their customer to maximum satisfaction.

E) Comparison of the Australian company’s reporting practices with the index and the

integrated reporting practices in the selected South African company

Suncorp which is an Australia company does not prepare an integrated report. However, they

have an alternative way in which the company prepares its corporate social responsibility report

of its evaluation of financial performance. Suncorp limited company repot there corporate

responsibility progress in their Suncorp Annual Review. They do this so that they can enhance

transparency about their performance across their economic, environmental and social measures

and targets. Moreover, they report their financial performance with diligently and also they help

their customer to make good choices with their investment. They do this through their financial

action plan, where they support their focus on improving their devises and product for the

vulnerable customer. Also, they work with joint ventures partners and corporates so that they can

develop new and accessible insurance offers such as AA Small Business insurance.

The Australian company corporate social responsibility delivers to its shareholder a 40%

dividend per share, also they give them a special 8% dividend per share. This outcome makes the

shareholder have average equity of 80% in the financial year. While Coronation Company values

ACCOUNTING THEORY 12

its company shareholder by delivering consistent financial performance report, continuously

engaging them in their activities and maintain significant distribution to cash flow. Also, when it

comes to reliability and completeness, Suncorp has provided and gave out some estimation to

contingent assets and liabilities. While Coronation Company has also provided the same

estimation in their contingent liabilities such as the South Africa Revenue Service group.

Conclusion

In summary, the report provides a need of why it is important to study needs to be changed or

added to the framework that governs and regulate the financial reporting and financial

information so as to be at par with the contemporary accounting theory. Therefore, the knowing

the history of the conceptual framework history, its limitation and strength is important for its

application in practical terms. Furthermore, sustainability deals with the non-financial

information of the organization performance also it deals with activities impact on economic

performance, environment, and society in general. Hence the report has summaries some of the

difference in guidelines that some of the accounting bodies have implemented. Also, its strength

and limitation have been highlighted in different accounting convection. Finally, the report has

provided a framework of the integrated report in South Africa Coronation Company and has

compared it with an Australian company which uses a different corporate responsibility report.

References

its company shareholder by delivering consistent financial performance report, continuously

engaging them in their activities and maintain significant distribution to cash flow. Also, when it

comes to reliability and completeness, Suncorp has provided and gave out some estimation to

contingent assets and liabilities. While Coronation Company has also provided the same

estimation in their contingent liabilities such as the South Africa Revenue Service group.

Conclusion

In summary, the report provides a need of why it is important to study needs to be changed or

added to the framework that governs and regulate the financial reporting and financial

information so as to be at par with the contemporary accounting theory. Therefore, the knowing

the history of the conceptual framework history, its limitation and strength is important for its

application in practical terms. Furthermore, sustainability deals with the non-financial

information of the organization performance also it deals with activities impact on economic

performance, environment, and society in general. Hence the report has summaries some of the

difference in guidelines that some of the accounting bodies have implemented. Also, its strength

and limitation have been highlighted in different accounting convection. Finally, the report has

provided a framework of the integrated report in South Africa Coronation Company and has

compared it with an Australian company which uses a different corporate responsibility report.

References

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.